Management Accounting Report: Systems, Budgets, and Analysis

VerifiedAdded on 2020/12/10

|14

|4093

|310

Report

AI Summary

This report provides an overview of management accounting and its application within an organization, focusing on the Wentworth Company Ltd. It differentiates between management and financial accounting, detailing various management accounting systems such as cost accounting and inventory management, and their benefits. The report includes calculations for break-even analysis under different sales scenarios for ALL-ACE, demonstrating the impact of price changes on profitability. Furthermore, it explores different types of budgets, outlining their advantages and disadvantages to aid managers in financial planning. The report concludes by assessing the role of management accounting systems in addressing financial challenges, offering a comprehensive analysis of financial management techniques and their practical implications.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Content

INTRODUCTION...........................................................................................................................1

Q1. a) Explaining management accounting and role of management accounting in Wentworth

Company Ltd..........................................................................................................................1

b). Difference between financial and management accounting..............................................1

c). Different type of management accounting systems and their benefits..............................2

SECTION 1......................................................................................................................................3

Q. 2)........................................................................................................................................3

a. Computation of sales required for the two proposals in relation to getting projected profits

................................................................................................................................................4

(b) Break Even Sales if-:........................................................................................................5

Q3. a).Explaining different type of budgets with their advantage and disadvantages...........6

SECTION 2......................................................................................................................................8

Question 4 Assessing the benefits and drawbacks of inventory management systems.........8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

1

INTRODUCTION...........................................................................................................................1

Q1. a) Explaining management accounting and role of management accounting in Wentworth

Company Ltd..........................................................................................................................1

b). Difference between financial and management accounting..............................................1

c). Different type of management accounting systems and their benefits..............................2

SECTION 1......................................................................................................................................3

Q. 2)........................................................................................................................................3

a. Computation of sales required for the two proposals in relation to getting projected profits

................................................................................................................................................4

(b) Break Even Sales if-:........................................................................................................5

Q3. a).Explaining different type of budgets with their advantage and disadvantages...........6

SECTION 2......................................................................................................................................8

Question 4 Assessing the benefits and drawbacks of inventory management systems.........8

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

1

INTRODUCTION

Management accounting is an integral part of any business firm. It is the process of

preparing management reports and accounts which helps in providing accurate and timely

financial and statistical information to make short-term and long-term decisions of

organisation. Present report will give an overview on management accounting system and its

application in an organisation. Present study will address the role of management accounting

in Wentworth Company Ltd., with differentiating management accounting from financial

accounting. Further, different management accounting system is discussed with their

benefits. The report will also include the calculation on break even analysis on the different

sales prospects of ALL-ACE. Further, the report will address different budgets with their

advantage and disadvantage that will help managers in understanding the needs for

preparing budgets. Later, the report will include the role of management accounting system

in responding to the financial problems in organisation.

Q1. a) Explaining management accounting and role of management accounting in Wentworth

Company Ltd.

Management accounting is the presentation of accounting information in order to formulate

the policies to be adopted by the management and assist its day to day activities. It is a

process of transferring financial information in reports so that the management of company

can use it to make day to day decisions regarding company’s growth and performance

(DRURY, 2013). Unlike financial accounting, management accounting is used by higher

authority or management of different departments of organisation. It helps management in

making day to day decisions, budgets which helps company in achieving its pre-determined

goals.

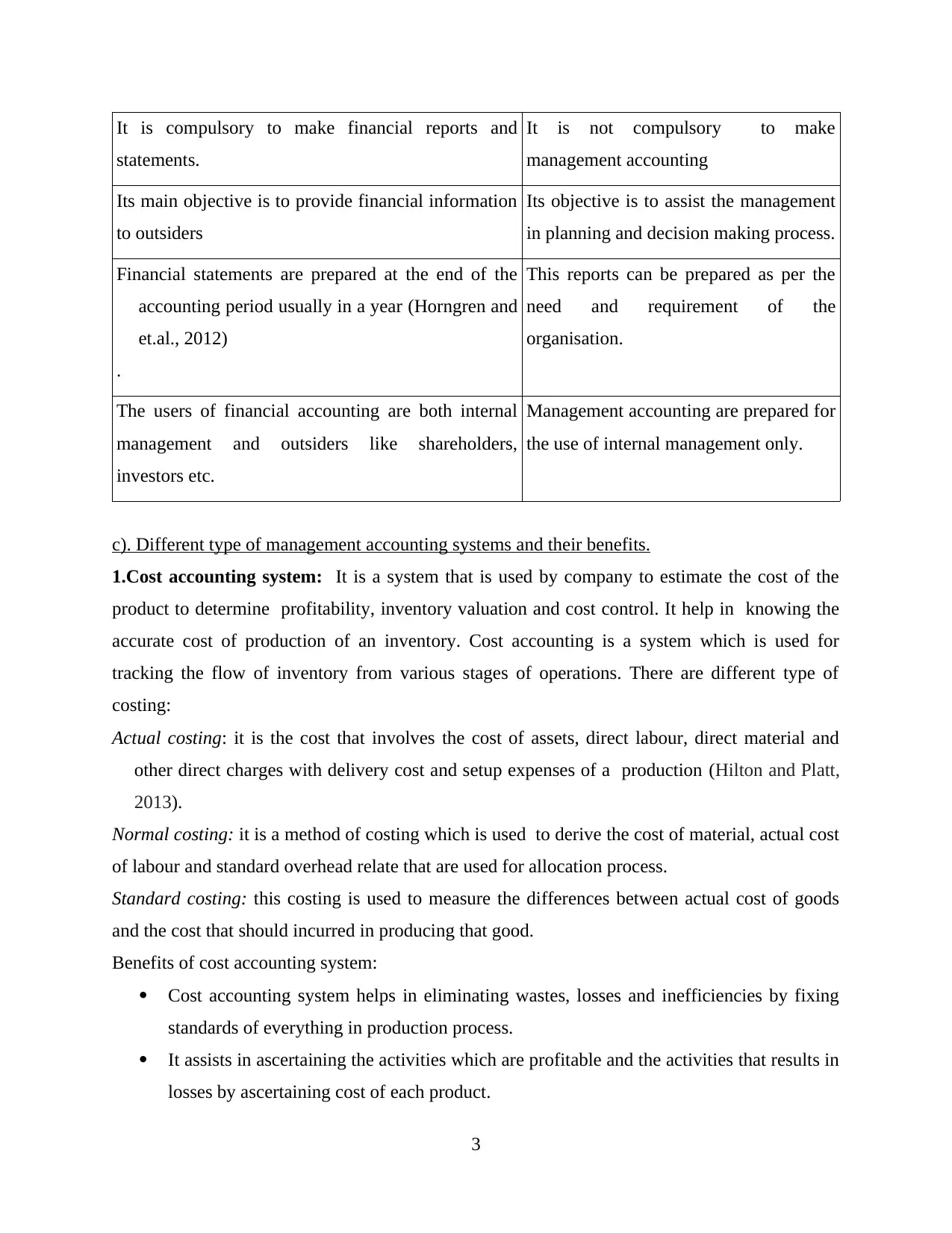

b). Difference between financial and management accounting.

Financial accounting Management accounting

Financial accounting is a system that focuses on the

preparation of financial statement to provide the

financial information

The accounting system which provides

relevant information to the managers to

make policies, plan and strategies.

2

Management accounting is an integral part of any business firm. It is the process of

preparing management reports and accounts which helps in providing accurate and timely

financial and statistical information to make short-term and long-term decisions of

organisation. Present report will give an overview on management accounting system and its

application in an organisation. Present study will address the role of management accounting

in Wentworth Company Ltd., with differentiating management accounting from financial

accounting. Further, different management accounting system is discussed with their

benefits. The report will also include the calculation on break even analysis on the different

sales prospects of ALL-ACE. Further, the report will address different budgets with their

advantage and disadvantage that will help managers in understanding the needs for

preparing budgets. Later, the report will include the role of management accounting system

in responding to the financial problems in organisation.

Q1. a) Explaining management accounting and role of management accounting in Wentworth

Company Ltd.

Management accounting is the presentation of accounting information in order to formulate

the policies to be adopted by the management and assist its day to day activities. It is a

process of transferring financial information in reports so that the management of company

can use it to make day to day decisions regarding company’s growth and performance

(DRURY, 2013). Unlike financial accounting, management accounting is used by higher

authority or management of different departments of organisation. It helps management in

making day to day decisions, budgets which helps company in achieving its pre-determined

goals.

b). Difference between financial and management accounting.

Financial accounting Management accounting

Financial accounting is a system that focuses on the

preparation of financial statement to provide the

financial information

The accounting system which provides

relevant information to the managers to

make policies, plan and strategies.

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It is compulsory to make financial reports and

statements.

It is not compulsory to make

management accounting

Its main objective is to provide financial information

to outsiders

Its objective is to assist the management

in planning and decision making process.

Financial statements are prepared at the end of the

accounting period usually in a year (Horngren and

et.al., 2012)

.

This reports can be prepared as per the

need and requirement of the

organisation.

The users of financial accounting are both internal

management and outsiders like shareholders,

investors etc.

Management accounting are prepared for

the use of internal management only.

c). Different type of management accounting systems and their benefits.

1.Cost accounting system: It is a system that is used by company to estimate the cost of the

product to determine profitability, inventory valuation and cost control. It help in knowing the

accurate cost of production of an inventory. Cost accounting is a system which is used for

tracking the flow of inventory from various stages of operations. There are different type of

costing:

Actual costing: it is the cost that involves the cost of assets, direct labour, direct material and

other direct charges with delivery cost and setup expenses of a production (Hilton and Platt,

2013).

Normal costing: it is a method of costing which is used to derive the cost of material, actual cost

of labour and standard overhead relate that are used for allocation process.

Standard costing: this costing is used to measure the differences between actual cost of goods

and the cost that should incurred in producing that good.

Benefits of cost accounting system:

Cost accounting system helps in eliminating wastes, losses and inefficiencies by fixing

standards of everything in production process.

It assists in ascertaining the activities which are profitable and the activities that results in

losses by ascertaining cost of each product.

3

statements.

It is not compulsory to make

management accounting

Its main objective is to provide financial information

to outsiders

Its objective is to assist the management

in planning and decision making process.

Financial statements are prepared at the end of the

accounting period usually in a year (Horngren and

et.al., 2012)

.

This reports can be prepared as per the

need and requirement of the

organisation.

The users of financial accounting are both internal

management and outsiders like shareholders,

investors etc.

Management accounting are prepared for

the use of internal management only.

c). Different type of management accounting systems and their benefits.

1.Cost accounting system: It is a system that is used by company to estimate the cost of the

product to determine profitability, inventory valuation and cost control. It help in knowing the

accurate cost of production of an inventory. Cost accounting is a system which is used for

tracking the flow of inventory from various stages of operations. There are different type of

costing:

Actual costing: it is the cost that involves the cost of assets, direct labour, direct material and

other direct charges with delivery cost and setup expenses of a production (Hilton and Platt,

2013).

Normal costing: it is a method of costing which is used to derive the cost of material, actual cost

of labour and standard overhead relate that are used for allocation process.

Standard costing: this costing is used to measure the differences between actual cost of goods

and the cost that should incurred in producing that good.

Benefits of cost accounting system:

Cost accounting system helps in eliminating wastes, losses and inefficiencies by fixing

standards of everything in production process.

It assists in ascertaining the activities which are profitable and the activities that results in

losses by ascertaining cost of each product.

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost accounting will help in price fixation of a product by providing actual cost of

production.

Inventory management system: This system help sin tracking goods through checking entire

supply chain process in an organisation. This system helps in analysing inventory from its

production to retail, warehousing to shipping and delivery to the final customer. The

inventory management system helps the production department in estimating thee

requirement of raw material, or the retail store to maintaining the stock(Carvalho, Gomes and

José Fernandes, 2012)

2. . There are various techniques of inventory management , like:

Just in time: it is common method of increasing efficiency and reducing waste by receiving

goods only when they are needed in production process.

Periodic inventory: in this techniques inventory are maintain or updated on a periodic basis. It

uses regular and random checking of inventory for tracking information.

FIFO: it refers to first in first out method of managing inventory, according to this system the

oldest cost of item in inventory will be removed first to sold.

Benefit of inventory management system:

It helps in increasing the sale of company.

Inventory management helps in increasing transparency as all information of inventory

are known from its production to shipping and delivery.

Job costing system: it helps in determine manufacturing costs by assigning manufacturing cost

to an individual product or stock of products. This method is mostly used when the product,

manufactured are different from each other (DeBusk, B. C. and et.al.,2018). It is used to

control the use of raw materials, labour hours and equipment by assigning different cost of

different customer separately.

SECTION 1

Q. 2).

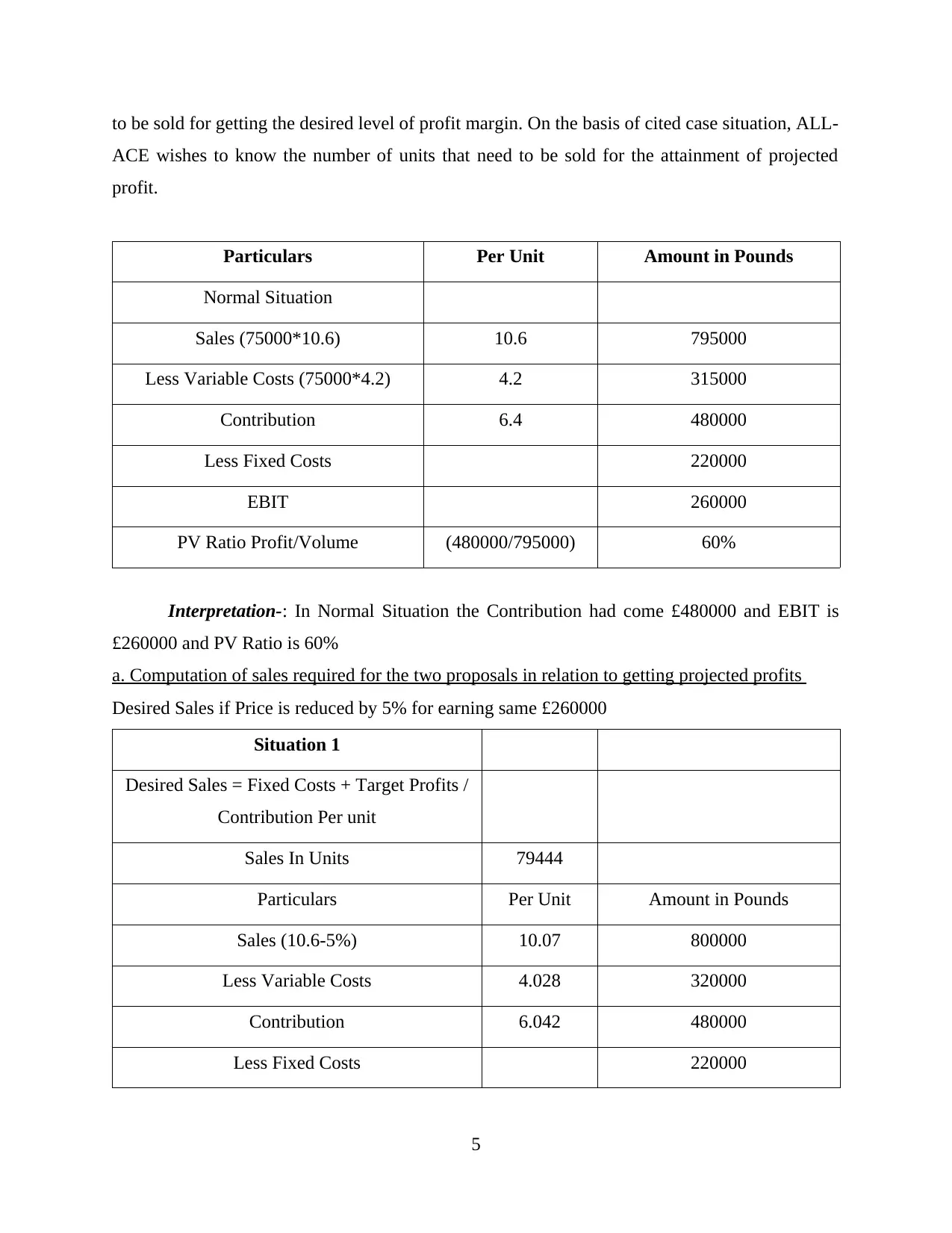

BEP is one of the most effectual techniques of management accounting which in turn

provides high level of assistance in assessing the point where business entity will attain the

position of no profit no loss. It clearly represents the level after which business unit would

become able to generate profit margin (Kaplan and Atkinson, 2015). Such technique is highly

prominent which in turn offers opportunity in relation to assessing the number of units that need

4

production.

Inventory management system: This system help sin tracking goods through checking entire

supply chain process in an organisation. This system helps in analysing inventory from its

production to retail, warehousing to shipping and delivery to the final customer. The

inventory management system helps the production department in estimating thee

requirement of raw material, or the retail store to maintaining the stock(Carvalho, Gomes and

José Fernandes, 2012)

2. . There are various techniques of inventory management , like:

Just in time: it is common method of increasing efficiency and reducing waste by receiving

goods only when they are needed in production process.

Periodic inventory: in this techniques inventory are maintain or updated on a periodic basis. It

uses regular and random checking of inventory for tracking information.

FIFO: it refers to first in first out method of managing inventory, according to this system the

oldest cost of item in inventory will be removed first to sold.

Benefit of inventory management system:

It helps in increasing the sale of company.

Inventory management helps in increasing transparency as all information of inventory

are known from its production to shipping and delivery.

Job costing system: it helps in determine manufacturing costs by assigning manufacturing cost

to an individual product or stock of products. This method is mostly used when the product,

manufactured are different from each other (DeBusk, B. C. and et.al.,2018). It is used to

control the use of raw materials, labour hours and equipment by assigning different cost of

different customer separately.

SECTION 1

Q. 2).

BEP is one of the most effectual techniques of management accounting which in turn

provides high level of assistance in assessing the point where business entity will attain the

position of no profit no loss. It clearly represents the level after which business unit would

become able to generate profit margin (Kaplan and Atkinson, 2015). Such technique is highly

prominent which in turn offers opportunity in relation to assessing the number of units that need

4

to be sold for getting the desired level of profit margin. On the basis of cited case situation, ALL-

ACE wishes to know the number of units that need to be sold for the attainment of projected

profit.

Particulars Per Unit Amount in Pounds

Normal Situation

Sales (75000*10.6) 10.6 795000

Less Variable Costs (75000*4.2) 4.2 315000

Contribution 6.4 480000

Less Fixed Costs 220000

EBIT 260000

PV Ratio Profit/Volume (480000/795000) 60%

Interpretation-: In Normal Situation the Contribution had come £480000 and EBIT is

£260000 and PV Ratio is 60%

a. Computation of sales required for the two proposals in relation to getting projected profits

Desired Sales if Price is reduced by 5% for earning same £260000

Situation 1

Desired Sales = Fixed Costs + Target Profits /

Contribution Per unit

Sales In Units 79444

Particulars Per Unit Amount in Pounds

Sales (10.6-5%) 10.07 800000

Less Variable Costs 4.028 320000

Contribution 6.042 480000

Less Fixed Costs 220000

5

ACE wishes to know the number of units that need to be sold for the attainment of projected

profit.

Particulars Per Unit Amount in Pounds

Normal Situation

Sales (75000*10.6) 10.6 795000

Less Variable Costs (75000*4.2) 4.2 315000

Contribution 6.4 480000

Less Fixed Costs 220000

EBIT 260000

PV Ratio Profit/Volume (480000/795000) 60%

Interpretation-: In Normal Situation the Contribution had come £480000 and EBIT is

£260000 and PV Ratio is 60%

a. Computation of sales required for the two proposals in relation to getting projected profits

Desired Sales if Price is reduced by 5% for earning same £260000

Situation 1

Desired Sales = Fixed Costs + Target Profits /

Contribution Per unit

Sales In Units 79444

Particulars Per Unit Amount in Pounds

Sales (10.6-5%) 10.07 800000

Less Variable Costs 4.028 320000

Contribution 6.042 480000

Less Fixed Costs 220000

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Situation 1

EBIT 260000

Interpretation-: If Prices are reduced by 5% and desired profit is £260000 then the sales

will be 79444 units.

Desired Sales if Price is increased by 10% for earning same £260000

Desired Sales =Fixed Costs + Target

Profits/Contribution Per unit

Situation 2

Sales In Units 72727

Particulars Per Unit Amount in Pounds

Sales (10.6+10%) 11 800000

Less Variable Costs 4.4 320000

Contribution 6.6 480000

Less Fixed Costs 220000

EBIT 260000

Interpretation-: In Prices are increased by 10% and for achieving EBIT of £260000 the

company is need to sales 72727 units.

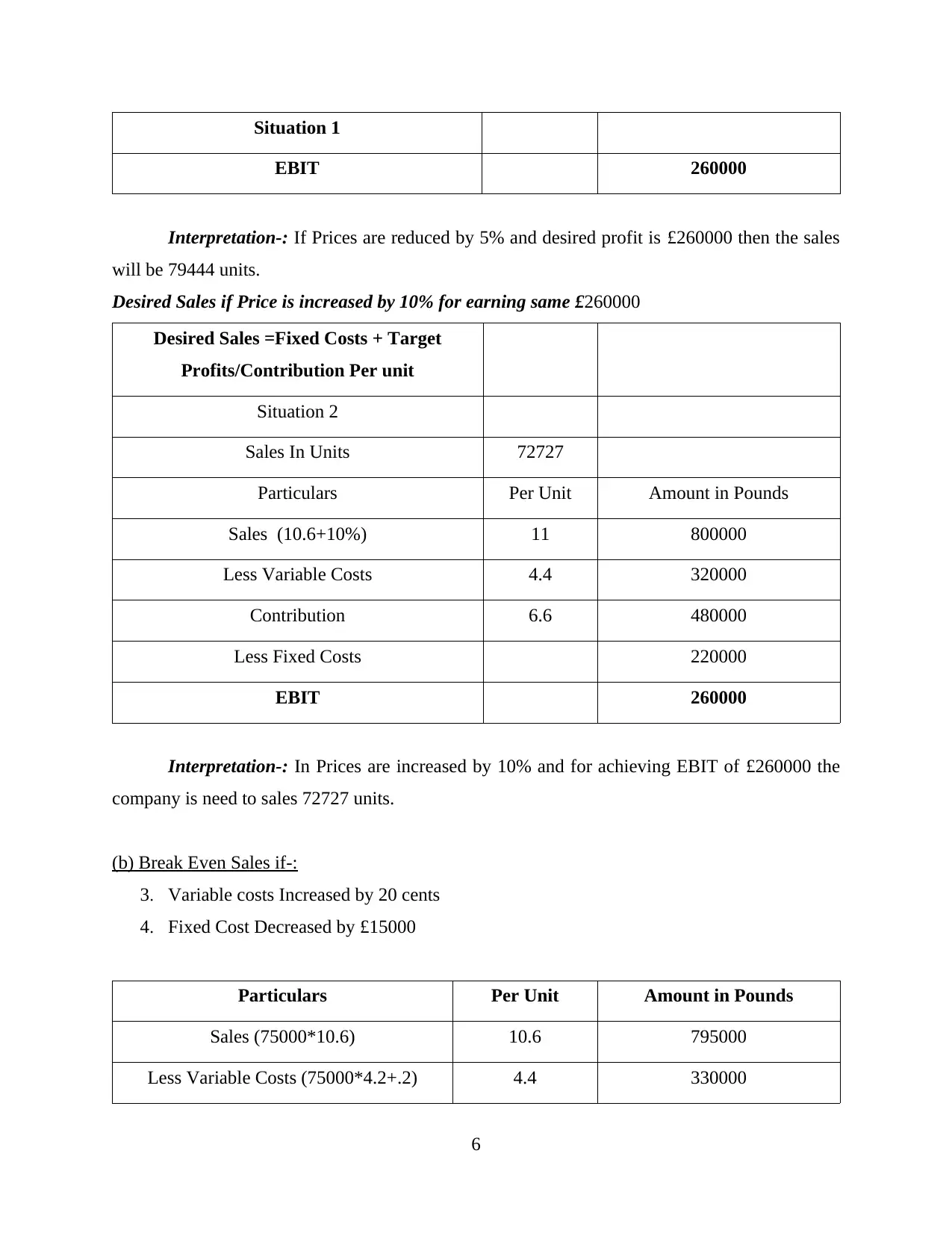

(b) Break Even Sales if-:

3. Variable costs Increased by 20 cents

4. Fixed Cost Decreased by £15000

Particulars Per Unit Amount in Pounds

Sales (75000*10.6) 10.6 795000

Less Variable Costs (75000*4.2+.2) 4.4 330000

6

EBIT 260000

Interpretation-: If Prices are reduced by 5% and desired profit is £260000 then the sales

will be 79444 units.

Desired Sales if Price is increased by 10% for earning same £260000

Desired Sales =Fixed Costs + Target

Profits/Contribution Per unit

Situation 2

Sales In Units 72727

Particulars Per Unit Amount in Pounds

Sales (10.6+10%) 11 800000

Less Variable Costs 4.4 320000

Contribution 6.6 480000

Less Fixed Costs 220000

EBIT 260000

Interpretation-: In Prices are increased by 10% and for achieving EBIT of £260000 the

company is need to sales 72727 units.

(b) Break Even Sales if-:

3. Variable costs Increased by 20 cents

4. Fixed Cost Decreased by £15000

Particulars Per Unit Amount in Pounds

Sales (75000*10.6) 10.6 795000

Less Variable Costs (75000*4.2+.2) 4.4 330000

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Particulars Per Unit Amount in Pounds

Contribution 6.2 465000

Less Fixed Costs (220000-15000) 205000

EBIT 260000

Break even Sales Total Fixed Costs/Contribution Per Unit

205000 / 6.2

Break even Sales in Units 33065

Interpretation-: If Variable costs are increased by 20 cents and fixed costs decreased by

£15000 the break even sales that sales manager had to achieve is 33065 Units respectively. Thus,

selling 33065 units business entity would become able to recover its expenditure. At this level,

business organization will not get any margin.

Q3. a).Explaining different type of budgets with their advantage and disadvantages.

Budget is the estimating the revenue and expenses over a specified future plans and

objectives of . Budget plans future savings and spending as well as outlining projected income

and expenses. Different type of budgets are as follows:

Static Budgets: A budget that remains constant even when other factors in company like sales,

expenses or revenue changes. Static budget is based on company's expected level of output and

revenue at starting of accounting period. It is prepared before the budget period began.

Advantage of static budgets:

It is very easy to implement static budget and they don't need to be updated continuously

throughout the accounting period.

It gives a strong insight of company's cost and profit when the difference between actual

and budgeted amount will analysed.

Static budgets help a company to control their costs and make smart decisions.

Disadvantage of static budgets:

The biggest disadvantage of static budget is lack of flexibility.

Changes are not possible if management have to allocate additional cost to any activity.

7

Contribution 6.2 465000

Less Fixed Costs (220000-15000) 205000

EBIT 260000

Break even Sales Total Fixed Costs/Contribution Per Unit

205000 / 6.2

Break even Sales in Units 33065

Interpretation-: If Variable costs are increased by 20 cents and fixed costs decreased by

£15000 the break even sales that sales manager had to achieve is 33065 Units respectively. Thus,

selling 33065 units business entity would become able to recover its expenditure. At this level,

business organization will not get any margin.

Q3. a).Explaining different type of budgets with their advantage and disadvantages.

Budget is the estimating the revenue and expenses over a specified future plans and

objectives of . Budget plans future savings and spending as well as outlining projected income

and expenses. Different type of budgets are as follows:

Static Budgets: A budget that remains constant even when other factors in company like sales,

expenses or revenue changes. Static budget is based on company's expected level of output and

revenue at starting of accounting period. It is prepared before the budget period began.

Advantage of static budgets:

It is very easy to implement static budget and they don't need to be updated continuously

throughout the accounting period.

It gives a strong insight of company's cost and profit when the difference between actual

and budgeted amount will analysed.

Static budgets help a company to control their costs and make smart decisions.

Disadvantage of static budgets:

The biggest disadvantage of static budget is lack of flexibility.

Changes are not possible if management have to allocate additional cost to any activity.

7

As it is based on previous data, new business may face difficulty in establishing and

implementing static budgets.

Zero based budget: Zero based budgeting is the process of creating budgets from zero base,

that in this budget previous year budgets or revenue and expenses are not taken into

consideration. In this budget management looks at every activity is evaluated before making

budgets and allocating resources to them.

Advantages of zero based budgeting:

ZBB helps manager to find cost effective ways to improve activities.

It helps in increasing staff motivation as it gives them more initiative and responsibility in

the decision making process.

It helps in increasing the coordination and communication within the organisation.

It helps in eliminating the waste activities from the business operations.

Disadvantages of Zero based budgeting:

It is very time consuming process.

ZBB requires high efforts from all the employees as analysing all the activities requires

involvement of all the employees.

Zero based budgeting can be done by effective employees, proper training have to

provide to implement the ZBB in organisation.

Rolling budget: this budget is the extension of the existing budget model. It is a continuous

budget which is the updated one that takes place of the old version when it expires. Most

companies prepare budgets on a monthly, quarterly or annual basis. This type of planning

eliminates the need to follow traditional approach as company is always has a current budgets at

its disposal.

Advantage of rolling budgets:

Rolling budgets is more responsive to unexpected changes in company’s overall

planning. It does not consider the change taking place during a forecast period.

Rolling budgets helps to be more responsive to unexpected changes in circumstances and

to make adjustments for those changes in coming period.

Disadvantages of rolling budgets:

It is similar to preparing a new budget again and again.

It requires to regularly gathering the facts from the previous period budgets.

Rolling budgets requires time and efforts from employees.

8

implementing static budgets.

Zero based budget: Zero based budgeting is the process of creating budgets from zero base,

that in this budget previous year budgets or revenue and expenses are not taken into

consideration. In this budget management looks at every activity is evaluated before making

budgets and allocating resources to them.

Advantages of zero based budgeting:

ZBB helps manager to find cost effective ways to improve activities.

It helps in increasing staff motivation as it gives them more initiative and responsibility in

the decision making process.

It helps in increasing the coordination and communication within the organisation.

It helps in eliminating the waste activities from the business operations.

Disadvantages of Zero based budgeting:

It is very time consuming process.

ZBB requires high efforts from all the employees as analysing all the activities requires

involvement of all the employees.

Zero based budgeting can be done by effective employees, proper training have to

provide to implement the ZBB in organisation.

Rolling budget: this budget is the extension of the existing budget model. It is a continuous

budget which is the updated one that takes place of the old version when it expires. Most

companies prepare budgets on a monthly, quarterly or annual basis. This type of planning

eliminates the need to follow traditional approach as company is always has a current budgets at

its disposal.

Advantage of rolling budgets:

Rolling budgets is more responsive to unexpected changes in company’s overall

planning. It does not consider the change taking place during a forecast period.

Rolling budgets helps to be more responsive to unexpected changes in circumstances and

to make adjustments for those changes in coming period.

Disadvantages of rolling budgets:

It is similar to preparing a new budget again and again.

It requires to regularly gathering the facts from the previous period budgets.

Rolling budgets requires time and efforts from employees.

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Incremental budgets: These budgets prepared using a previous period’s budget or actual

performance as a basis with incremental amounts added for the new budget period.

b). The importance of preparing budgets.

In any business organization of any size, preparing budgets is like making a road map to

the destination of success. Budgets help the management in making short-term and long term

goals and control the expenses and revenue of business organization. Following are the

importance of preparing a budget in an organization:

Budgeting forces the management to study about the problems relating to the timely

implementation.

It helps the management to make planning and making policies related to the budgeting

for future references.

One of the most important is controlling income and expenditure which is been planned

by Budgeting. It provides a path to it.

It provides numerical terms for a defined period which are used to gain objectives.

It involves the management of all departments in an organisation to make strategy and

goals for the organisation for the whole.

It helps in providing responsibility to each manager in an organisation.

Budgets help in directing the capital and revenue resources in a profitable way.

SECTION 2

Question 4 Assessing the benefits and drawbacks of inventory management systems

On the basis of cited case situation, All-Ace Ltd lays emphasis on using perpetual inventory

management system for the purpose of better maintenance. Earlier, company was valuing its

stock on the basis of FIFO method. However, now for the purpose of better management,

company is employing LIFO method to evaluate its inventory. With the motive to respond

monetary problems in an effectual way company focuses on undertaking alternative ways which

makes contribution in the achievement of organizational goals and objectives. However, at the

time of method selection manager of All-Ace should keep in mind advantages and disadvantages

of methods undertaken. Moreover, by evaluating pros and cons firm can easily decide which

option is better over others. Hence, advantages and drawbacks of main inventory valuation

methods are enumerated below:

FIFO (first in first out) method: Under such method, goods which are purchased first sold

on prior basis. Such method of stock valuation is considered as appropriate theoretically because

9

performance as a basis with incremental amounts added for the new budget period.

b). The importance of preparing budgets.

In any business organization of any size, preparing budgets is like making a road map to

the destination of success. Budgets help the management in making short-term and long term

goals and control the expenses and revenue of business organization. Following are the

importance of preparing a budget in an organization:

Budgeting forces the management to study about the problems relating to the timely

implementation.

It helps the management to make planning and making policies related to the budgeting

for future references.

One of the most important is controlling income and expenditure which is been planned

by Budgeting. It provides a path to it.

It provides numerical terms for a defined period which are used to gain objectives.

It involves the management of all departments in an organisation to make strategy and

goals for the organisation for the whole.

It helps in providing responsibility to each manager in an organisation.

Budgets help in directing the capital and revenue resources in a profitable way.

SECTION 2

Question 4 Assessing the benefits and drawbacks of inventory management systems

On the basis of cited case situation, All-Ace Ltd lays emphasis on using perpetual inventory

management system for the purpose of better maintenance. Earlier, company was valuing its

stock on the basis of FIFO method. However, now for the purpose of better management,

company is employing LIFO method to evaluate its inventory. With the motive to respond

monetary problems in an effectual way company focuses on undertaking alternative ways which

makes contribution in the achievement of organizational goals and objectives. However, at the

time of method selection manager of All-Ace should keep in mind advantages and disadvantages

of methods undertaken. Moreover, by evaluating pros and cons firm can easily decide which

option is better over others. Hence, advantages and drawbacks of main inventory valuation

methods are enumerated below:

FIFO (first in first out) method: Under such method, goods which are purchased first sold

on prior basis. Such method of stock valuation is considered as appropriate theoretically because

9

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

its assumptions are in line with the actual flow of goods. FIFO concept is recognized as more

logical because it reduces the risk of obsolescence.

Advantages

Easy to understand: FIFO method provides high level of assistance in recording

inventory in a prominent way. Moreover, in this inventories are recorded on the basis of

units bought or produced.

Facilitates better valuation as per accounting principles: Such method highly suits to

the business unit which has high turnover (First in First Out (FIFO) Advantages and

Disadvantages, 2018). In other words, FIFO method is beneficial for the companies

which have ability to convert its stock into sales quickly. Further, matching principle of

accounting also supports FIFO method.

Better reflection of market prices: As per this, inventories are valued on the basis of

recent purchase so it provides business unit with appropriate reflection regarding price.

Highly relevant: In this, closing stock’s value is pivotal pertaining to total current assets

and related ratios which in turn leads reliable analysis.

Assists in increasing gross profit and covering inflated operating expenses. Moreover,

inflationary tendencies may result into rise in both operating expenses and value of

stock.

Drawbacks: Along with the benefits such method has some drawbacks such as:

In the context of companies where manufacturing is done in batches recognized as

complex and difficult to manage.

FIFO does not provide suitable inputs for costing decisions where inflationary economies

exist due to unreliable value in relation to the cost of sales (The Pros & Cons of LIFO &

FIFO, 2018).

LIFO (Last in first out) method: This tool of management accounting is used for placing

accounting value on inventory. It is based on the assumption that lastly purchased item need to

be sold firstly. In other words, as per this company sells that items on prior basis which are

purchased in last.

Advantages

Helps in matching cost and revenue to a great extent. Moreover, as per LIFO both sales

revenue as well as cost is recognized a per recent currency value.

10

logical because it reduces the risk of obsolescence.

Advantages

Easy to understand: FIFO method provides high level of assistance in recording

inventory in a prominent way. Moreover, in this inventories are recorded on the basis of

units bought or produced.

Facilitates better valuation as per accounting principles: Such method highly suits to

the business unit which has high turnover (First in First Out (FIFO) Advantages and

Disadvantages, 2018). In other words, FIFO method is beneficial for the companies

which have ability to convert its stock into sales quickly. Further, matching principle of

accounting also supports FIFO method.

Better reflection of market prices: As per this, inventories are valued on the basis of

recent purchase so it provides business unit with appropriate reflection regarding price.

Highly relevant: In this, closing stock’s value is pivotal pertaining to total current assets

and related ratios which in turn leads reliable analysis.

Assists in increasing gross profit and covering inflated operating expenses. Moreover,

inflationary tendencies may result into rise in both operating expenses and value of

stock.

Drawbacks: Along with the benefits such method has some drawbacks such as:

In the context of companies where manufacturing is done in batches recognized as

complex and difficult to manage.

FIFO does not provide suitable inputs for costing decisions where inflationary economies

exist due to unreliable value in relation to the cost of sales (The Pros & Cons of LIFO &

FIFO, 2018).

LIFO (Last in first out) method: This tool of management accounting is used for placing

accounting value on inventory. It is based on the assumption that lastly purchased item need to

be sold firstly. In other words, as per this company sells that items on prior basis which are

purchased in last.

Advantages

Helps in matching cost and revenue to a great extent. Moreover, as per LIFO both sales

revenue as well as cost is recognized a per recent currency value.

10

Easy to understand and simple to calculate

Provides assistance in recovering the material cost incurred by an organization.

Offers benefits in the context of stock valuation when prices are rising due to inflation

Facilitates better handling when net realizable value is declining.

LIFO complies with the actual physical flow of stock effectually.

Drawbacks

Sometimes, LIFO does not highlight current prices in the context of current condition

recognized as ineffectual (Last in First out (LIFO) Method, Its Advantages and

Disadvantages, 2018).

It does not help in doing comparison of similar kind of jobs due to price variation

In the case of fluctuating receipts rates such method is considered as ineffective due to

the inclusion of more complications

Some managers consider LIFO as ineffective as it requires more clerical work

On the basis of above evaluation it is suggested to All-Ace Ltd that focus needs to be placed

on the adoption of FIFO method for valuing inventory. Moreover, as per accounting standards

such method is recognized as highly effective as compared to other alternatives available

(Accounting Standards Valuation of Inventories, 2018). Moreover, it facilitates reliable valuation

of stock and helps in finding as well as presenting the suitable value of the same in final

accounts.

CONCLUSION

By summing up the above report it can be concluded that management accounting is highly

significant in the context of Wentworth. As it provides assistance to the business units in making

effectual short-term internal business decisions. Besides this, it can be inferred from the

evaluation that aspects of management and financial accounting differs on the basis of time,

motives etc. Along with this, it has been articulated that management accounting systems will

assist Wentworth in making prominent strategies and thereby makes contribution in the

profitability aspects. It can be depicted from the evaluation that BEP tool helps in company in

sales as well as profit planning to a great extent. It can be summarized from the report that

business organization should focus on the adoption of modern budgeting technique such as zero

base which in turn facilitates optimum allocation of financial resources. Business entity of

11

Provides assistance in recovering the material cost incurred by an organization.

Offers benefits in the context of stock valuation when prices are rising due to inflation

Facilitates better handling when net realizable value is declining.

LIFO complies with the actual physical flow of stock effectually.

Drawbacks

Sometimes, LIFO does not highlight current prices in the context of current condition

recognized as ineffectual (Last in First out (LIFO) Method, Its Advantages and

Disadvantages, 2018).

It does not help in doing comparison of similar kind of jobs due to price variation

In the case of fluctuating receipts rates such method is considered as ineffective due to

the inclusion of more complications

Some managers consider LIFO as ineffective as it requires more clerical work

On the basis of above evaluation it is suggested to All-Ace Ltd that focus needs to be placed

on the adoption of FIFO method for valuing inventory. Moreover, as per accounting standards

such method is recognized as highly effective as compared to other alternatives available

(Accounting Standards Valuation of Inventories, 2018). Moreover, it facilitates reliable valuation

of stock and helps in finding as well as presenting the suitable value of the same in final

accounts.

CONCLUSION

By summing up the above report it can be concluded that management accounting is highly

significant in the context of Wentworth. As it provides assistance to the business units in making

effectual short-term internal business decisions. Besides this, it can be inferred from the

evaluation that aspects of management and financial accounting differs on the basis of time,

motives etc. Along with this, it has been articulated that management accounting systems will

assist Wentworth in making prominent strategies and thereby makes contribution in the

profitability aspects. It can be depicted from the evaluation that BEP tool helps in company in

sales as well as profit planning to a great extent. It can be summarized from the report that

business organization should focus on the adoption of modern budgeting technique such as zero

base which in turn facilitates optimum allocation of financial resources. Business entity of

11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.