Management Accounting Report: XLG Company's Financial Analysis

VerifiedAdded on 2023/01/07

|15

|3285

|47

Report

AI Summary

This report provides a detailed analysis of XLG, an eastern British cleaning product service, focusing on management accounting principles. It examines sales price variance, sales volume contribution variance, material price planning and operational variances, and the merits and demerits of using variance analysis to assess manager performance. The report includes calculations and interpretations of variances for chemical products X and Y, highlighting their impact on XLG's financial position. Furthermore, it addresses the competitive advantage of FamaQ and the impact of increased demand on the company. The report also explores the benefits and drawbacks of variance analysis, emphasizing its role in cost control, performance evaluation, and budgetary adjustments. The analysis considers the implications of operational changes and the challenges of behavioral issues in performance management.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................................3

PART A.........................................................................................................................................................3

1. Sales price variance and sales volume contribution variance...............................................................3

2. The material price planning variance and material price operational variance....................................5

3. Change in operation and critical analysis of merits and demerits of using variance in assessing the

performance of managers........................................................................................................................7

PART B.......................................................................................................................................................10

1. FamaQ gives XLG competitive advantage........................................................................................10

2. Demand for chemical X and Y has increased by 45% which is likely to continue according to market

research.................................................................................................................................................10

3. The cost of making a unit of Fama Q in the UK is £3 with delivery times reducing by 15 working

days.......................................................................................................................................................11

CONCLUSION.............................................................................................................................................12

REFERENCES..............................................................................................................................................13

INTRODUCTION...........................................................................................................................................3

PART A.........................................................................................................................................................3

1. Sales price variance and sales volume contribution variance...............................................................3

2. The material price planning variance and material price operational variance....................................5

3. Change in operation and critical analysis of merits and demerits of using variance in assessing the

performance of managers........................................................................................................................7

PART B.......................................................................................................................................................10

1. FamaQ gives XLG competitive advantage........................................................................................10

2. Demand for chemical X and Y has increased by 45% which is likely to continue according to market

research.................................................................................................................................................10

3. The cost of making a unit of Fama Q in the UK is £3 with delivery times reducing by 15 working

days.......................................................................................................................................................11

CONCLUSION.............................................................................................................................................12

REFERENCES..............................................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Accounting is the method of tracking, categorizing, analyzing, reviewing and evaluating the

company's overall financial activities for the advantage of administration and other parties

involved such as stakeholders, investors, banks, customers, workers and administration.

Therefore, it is associated only with facets of financial statements and corporate decision taking.

Accounts administration is not a common accounting framework (Al-Mawali and et.al, 2018).

This could be any method of accounting that would allow a company to be operated more

efficiently and economically. It is mainly concerned with supplying managers with knowledge of

economics to achieve the organizational goals. The present study was depending on XLG, an

eastern British cleaning product service. This produces two different kinds of cleaning agents

that are chemical X and Y. Present assignment include variety of topics including such sale

price, volume allocation variance, material price preparation and operational variance and

benefits and drawbacks and use all differences to evaluate efficiency. Aside from all this, this

study also addresses the issues that may occur whenever the chemical famaQ is manufactured

and the direction the threat could be addressed.

PART A

1. Sales price variance and sales volume contribution variance

There are mentioned all the required information which is required for the calculation of

Sales price variance and sales volume contribution variance:

Given Information:

Total units sold: 1600

Material price variance: £ 27000 Favorable

Sales and Contribution:

Chemical X Chemical Y

Budgeted total sales 595 units 595 units

Actual Sales Volume 850 units 750 units

Accounting is the method of tracking, categorizing, analyzing, reviewing and evaluating the

company's overall financial activities for the advantage of administration and other parties

involved such as stakeholders, investors, banks, customers, workers and administration.

Therefore, it is associated only with facets of financial statements and corporate decision taking.

Accounts administration is not a common accounting framework (Al-Mawali and et.al, 2018).

This could be any method of accounting that would allow a company to be operated more

efficiently and economically. It is mainly concerned with supplying managers with knowledge of

economics to achieve the organizational goals. The present study was depending on XLG, an

eastern British cleaning product service. This produces two different kinds of cleaning agents

that are chemical X and Y. Present assignment include variety of topics including such sale

price, volume allocation variance, material price preparation and operational variance and

benefits and drawbacks and use all differences to evaluate efficiency. Aside from all this, this

study also addresses the issues that may occur whenever the chemical famaQ is manufactured

and the direction the threat could be addressed.

PART A

1. Sales price variance and sales volume contribution variance

There are mentioned all the required information which is required for the calculation of

Sales price variance and sales volume contribution variance:

Given Information:

Total units sold: 1600

Material price variance: £ 27000 Favorable

Sales and Contribution:

Chemical X Chemical Y

Budgeted total sales 595 units 595 units

Actual Sales Volume 850 units 750 units

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

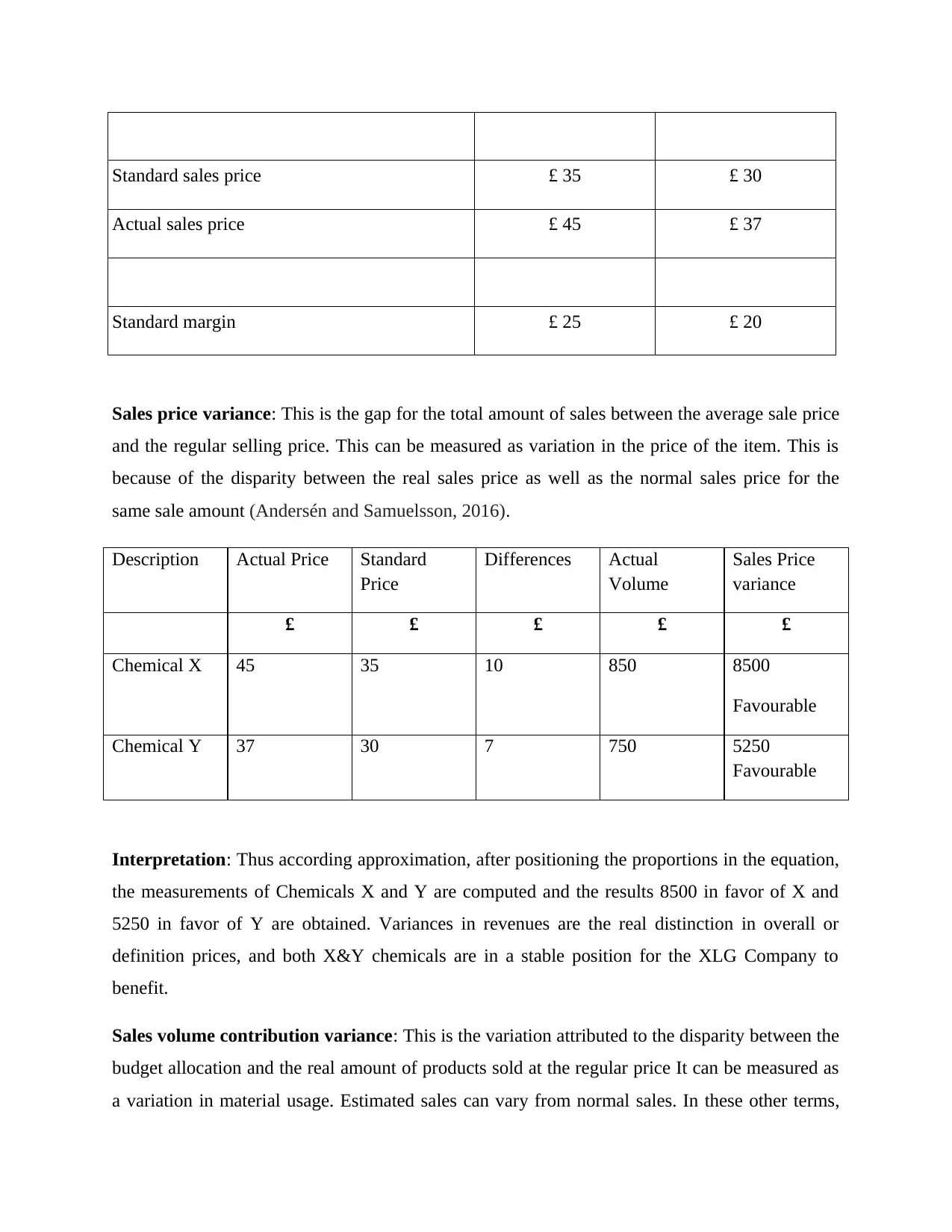

Standard sales price £ 35 £ 30

Actual sales price £ 45 £ 37

Standard margin £ 25 £ 20

Sales price variance: This is the gap for the total amount of sales between the average sale price

and the regular selling price. This can be measured as variation in the price of the item. This is

because of the disparity between the real sales price as well as the normal sales price for the

same sale amount (Andersén and Samuelsson, 2016).

Description Actual Price Standard

Price

Differences Actual

Volume

Sales Price

variance

£ £ £ £ £

Chemical X 45 35 10 850 8500

Favourable

Chemical Y 37 30 7 750 5250

Favourable

Interpretation: Thus according approximation, after positioning the proportions in the equation,

the measurements of Chemicals X and Y are computed and the results 8500 in favor of X and

5250 in favor of Y are obtained. Variances in revenues are the real distinction in overall or

definition prices, and both X&Y chemicals are in a stable position for the XLG Company to

benefit.

Sales volume contribution variance: This is the variation attributed to the disparity between the

budget allocation and the real amount of products sold at the regular price It can be measured as

a variation in material usage. Estimated sales can vary from normal sales. In these other terms,

Actual sales price £ 45 £ 37

Standard margin £ 25 £ 20

Sales price variance: This is the gap for the total amount of sales between the average sale price

and the regular selling price. This can be measured as variation in the price of the item. This is

because of the disparity between the real sales price as well as the normal sales price for the

same sale amount (Andersén and Samuelsson, 2016).

Description Actual Price Standard

Price

Differences Actual

Volume

Sales Price

variance

£ £ £ £ £

Chemical X 45 35 10 850 8500

Favourable

Chemical Y 37 30 7 750 5250

Favourable

Interpretation: Thus according approximation, after positioning the proportions in the equation,

the measurements of Chemicals X and Y are computed and the results 8500 in favor of X and

5250 in favor of Y are obtained. Variances in revenues are the real distinction in overall or

definition prices, and both X&Y chemicals are in a stable position for the XLG Company to

benefit.

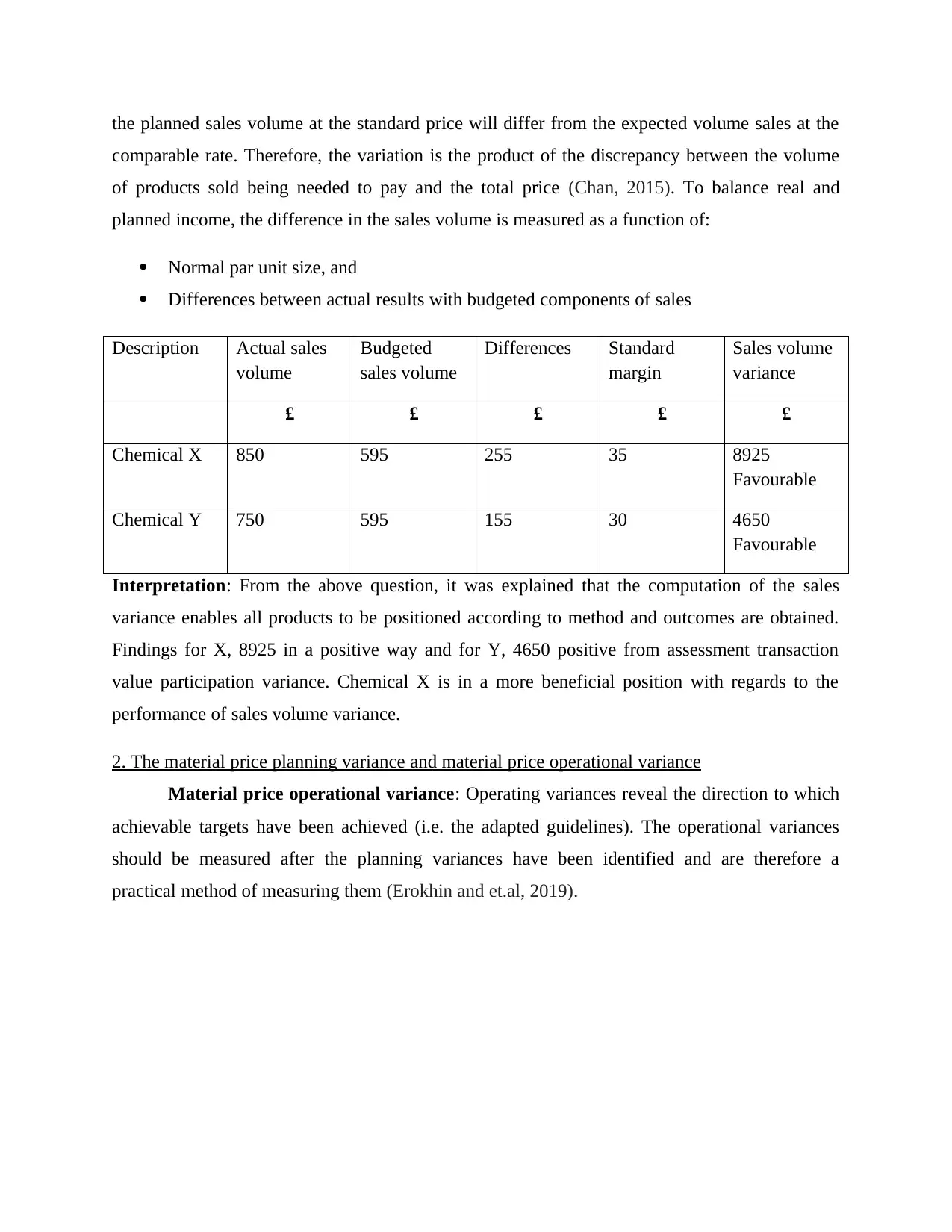

Sales volume contribution variance: This is the variation attributed to the disparity between the

budget allocation and the real amount of products sold at the regular price It can be measured as

a variation in material usage. Estimated sales can vary from normal sales. In these other terms,

the planned sales volume at the standard price will differ from the expected volume sales at the

comparable rate. Therefore, the variation is the product of the discrepancy between the volume

of products sold being needed to pay and the total price (Chan, 2015). To balance real and

planned income, the difference in the sales volume is measured as a function of:

Normal par unit size, and

Differences between actual results with budgeted components of sales

Description Actual sales

volume

Budgeted

sales volume

Differences Standard

margin

Sales volume

variance

£ £ £ £ £

Chemical X 850 595 255 35 8925

Favourable

Chemical Y 750 595 155 30 4650

Favourable

Interpretation: From the above question, it was explained that the computation of the sales

variance enables all products to be positioned according to method and outcomes are obtained.

Findings for X, 8925 in a positive way and for Y, 4650 positive from assessment transaction

value participation variance. Chemical X is in a more beneficial position with regards to the

performance of sales volume variance.

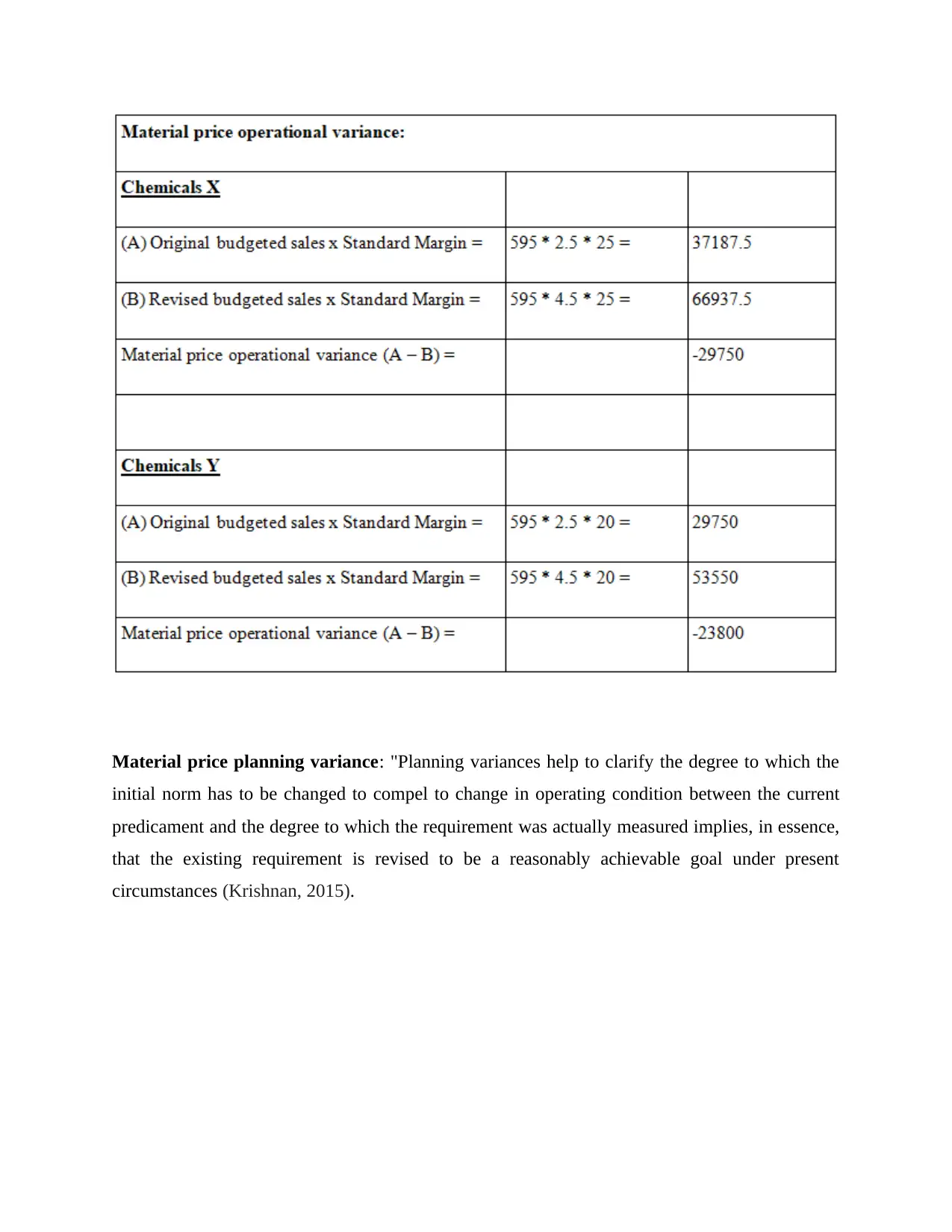

2. The material price planning variance and material price operational variance

Material price operational variance: Operating variances reveal the direction to which

achievable targets have been achieved (i.e. the adapted guidelines). The operational variances

should be measured after the planning variances have been identified and are therefore a

practical method of measuring them (Erokhin and et.al, 2019).

comparable rate. Therefore, the variation is the product of the discrepancy between the volume

of products sold being needed to pay and the total price (Chan, 2015). To balance real and

planned income, the difference in the sales volume is measured as a function of:

Normal par unit size, and

Differences between actual results with budgeted components of sales

Description Actual sales

volume

Budgeted

sales volume

Differences Standard

margin

Sales volume

variance

£ £ £ £ £

Chemical X 850 595 255 35 8925

Favourable

Chemical Y 750 595 155 30 4650

Favourable

Interpretation: From the above question, it was explained that the computation of the sales

variance enables all products to be positioned according to method and outcomes are obtained.

Findings for X, 8925 in a positive way and for Y, 4650 positive from assessment transaction

value participation variance. Chemical X is in a more beneficial position with regards to the

performance of sales volume variance.

2. The material price planning variance and material price operational variance

Material price operational variance: Operating variances reveal the direction to which

achievable targets have been achieved (i.e. the adapted guidelines). The operational variances

should be measured after the planning variances have been identified and are therefore a

practical method of measuring them (Erokhin and et.al, 2019).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

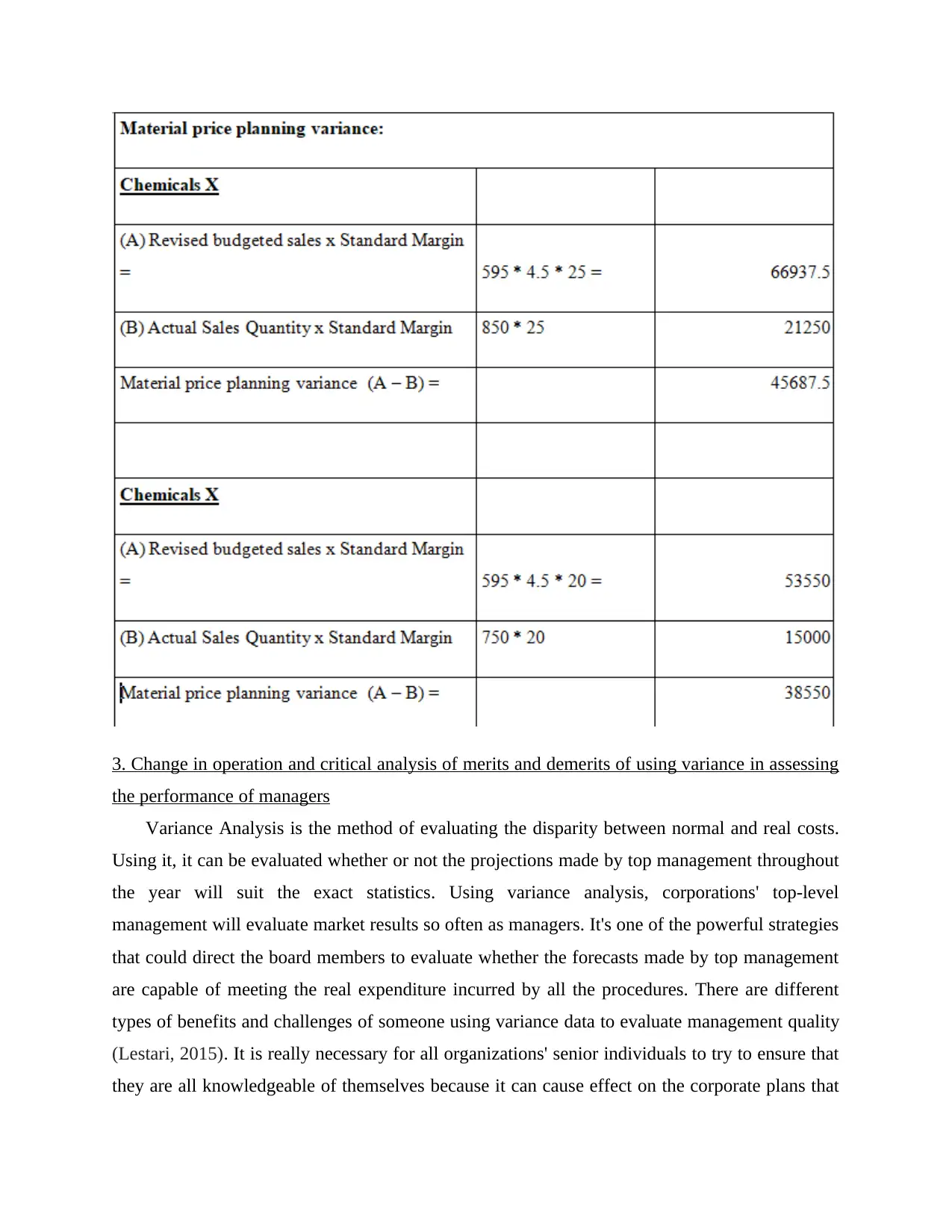

Material price planning variance: "Planning variances help to clarify the degree to which the

initial norm has to be changed to compel to change in operating condition between the current

predicament and the degree to which the requirement was actually measured implies, in essence,

that the existing requirement is revised to be a reasonably achievable goal under present

circumstances (Krishnan, 2015).

initial norm has to be changed to compel to change in operating condition between the current

predicament and the degree to which the requirement was actually measured implies, in essence,

that the existing requirement is revised to be a reasonably achievable goal under present

circumstances (Krishnan, 2015).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3. Change in operation and critical analysis of merits and demerits of using variance in assessing

the performance of managers

Variance Analysis is the method of evaluating the disparity between normal and real costs.

Using it, it can be evaluated whether or not the projections made by top management throughout

the year will suit the exact statistics. Using variance analysis, corporations' top-level

management will evaluate market results so often as managers. It's one of the powerful strategies

that could direct the board members to evaluate whether the forecasts made by top management

are capable of meeting the real expenditure incurred by all the procedures. There are different

types of benefits and challenges of someone using variance data to evaluate management quality

(Lestari, 2015). It is really necessary for all organizations' senior individuals to try to ensure that

they are all knowledgeable of themselves because it can cause effect on the corporate plans that

the performance of managers

Variance Analysis is the method of evaluating the disparity between normal and real costs.

Using it, it can be evaluated whether or not the projections made by top management throughout

the year will suit the exact statistics. Using variance analysis, corporations' top-level

management will evaluate market results so often as managers. It's one of the powerful strategies

that could direct the board members to evaluate whether the forecasts made by top management

are capable of meeting the real expenditure incurred by all the procedures. There are different

types of benefits and challenges of someone using variance data to evaluate management quality

(Lestari, 2015). It is really necessary for all organizations' senior individuals to try to ensure that

they are all knowledgeable of themselves because it can cause effect on the corporate plans that

will be developed for the successful implementation of future projects. Some of the major

advantages of enterprise variance analysis are that it will promote the study of the current market

situation. In addition, it may also allow great executives to monitor the quality of all employees

employed inside the company as a greater discrepancy between the real and standard cost will

supply all necessary data of lesser estimation skills. This will show management inadequate

results. Moreover, the administrators will better conduct all their tasks whenever the discrepancy

is small between planned and real expenditures. There are mentioning the advantage and

disadvantage of variance analysis for performance management such as:

Advantage: As differences are used by organizations to assess the output of managers and other

reasons then they that result in different merits. These are all as wants to follow:

Analysis of accountability: A framework of transparency within the corporation may be

developed with the aid of variance analysis or simulations. Whenever a owner takes steps for the

potential, the primary responsibilities would be to be responsive for these in order to assess their

results. If the findings are detrimental it will be very necessary for them to assume

accountability. If the degree of transparency in XLG is poor then the bad performance of the

management will be demonstrated (Mitter and Hiebl, 2017).

Setting system for roles and responsibilities in context of an organisation: Variance analysis

is being used to set up a framework for proper assigning of all role and obligations to the former

employees. The top management will, with the aid of it, assess the skill of all the management

and instead create the structure that will help achieve the long-term goals and priorities.

Regulations and productivity inside the company could be strengthened and strengthened with

the aid of it.

Controlling expenses: Analysis of variance plays a crucial role in monitoring trends so when the

outcomes of differences are adversely affected then the supervisors can take the appropriate

judgments to regulate the problematic thinking. Seek to find the reason for the negative impacts

to better function the management so they take care of relevant behavior so that they can boost

the efficiency of the company. The real selling is very important in the case of XLG Company

due to the increased demand resulting in the unfavorable variance. The administrators should

advantages of enterprise variance analysis are that it will promote the study of the current market

situation. In addition, it may also allow great executives to monitor the quality of all employees

employed inside the company as a greater discrepancy between the real and standard cost will

supply all necessary data of lesser estimation skills. This will show management inadequate

results. Moreover, the administrators will better conduct all their tasks whenever the discrepancy

is small between planned and real expenditures. There are mentioning the advantage and

disadvantage of variance analysis for performance management such as:

Advantage: As differences are used by organizations to assess the output of managers and other

reasons then they that result in different merits. These are all as wants to follow:

Analysis of accountability: A framework of transparency within the corporation may be

developed with the aid of variance analysis or simulations. Whenever a owner takes steps for the

potential, the primary responsibilities would be to be responsive for these in order to assess their

results. If the findings are detrimental it will be very necessary for them to assume

accountability. If the degree of transparency in XLG is poor then the bad performance of the

management will be demonstrated (Mitter and Hiebl, 2017).

Setting system for roles and responsibilities in context of an organisation: Variance analysis

is being used to set up a framework for proper assigning of all role and obligations to the former

employees. The top management will, with the aid of it, assess the skill of all the management

and instead create the structure that will help achieve the long-term goals and priorities.

Regulations and productivity inside the company could be strengthened and strengthened with

the aid of it.

Controlling expenses: Analysis of variance plays a crucial role in monitoring trends so when the

outcomes of differences are adversely affected then the supervisors can take the appropriate

judgments to regulate the problematic thinking. Seek to find the reason for the negative impacts

to better function the management so they take care of relevant behavior so that they can boost

the efficiency of the company. The real selling is very important in the case of XLG Company

due to the increased demand resulting in the unfavorable variance. The administrators should

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

have bought more inventory than the regular one to comply with this case, because it would have

contributed in important determinants.

Evaluation performance: Examination of variances is used to assess company performance by

comparing whether or not the desired effects are consistent with the estimates money earmarked.

This also serves to evaluate the success of managing supervisors as it will show good results

whenever the differences result favorably. If the outcomes are detrimental then it will reinforce

that perhaps the supervisors have created no attempts to ensure right choices or estimates (Ojua,

2016).

Adjusting budgeted estimation: Analysis of variances promotes the modifications of actual

expenditure. If such justification for the undesirable variance in standardized measures is

incorrect calculation then the results should be changed and modified. When the leaders are

intensely aware of the things then this will help to easily assess their efficiency and increases

employee productivity. It is one of the major advantages of someone using variations to test

executives' output in XLG Company.

1. It enables for controlling costs and measurement of projects by contrasting exact numbers with

those project budget. Management accounting aims at manufacturing an item as per established

performance standards at the least total price.

2. Pinpoint unnecessary management liability so that appropriate steps can be taken.

3. It encourages workers to meet set goals.

4. It promotes contact inside an organisation , for example among top managers or supervisors,

while enabling workers to work optimally

5. It guarantees the company is in good condition

6. This means that administrators and subordinates are centered, and hence facilitates the

alignment of performance.

Disadvantage:

contributed in important determinants.

Evaluation performance: Examination of variances is used to assess company performance by

comparing whether or not the desired effects are consistent with the estimates money earmarked.

This also serves to evaluate the success of managing supervisors as it will show good results

whenever the differences result favorably. If the outcomes are detrimental then it will reinforce

that perhaps the supervisors have created no attempts to ensure right choices or estimates (Ojua,

2016).

Adjusting budgeted estimation: Analysis of variances promotes the modifications of actual

expenditure. If such justification for the undesirable variance in standardized measures is

incorrect calculation then the results should be changed and modified. When the leaders are

intensely aware of the things then this will help to easily assess their efficiency and increases

employee productivity. It is one of the major advantages of someone using variations to test

executives' output in XLG Company.

1. It enables for controlling costs and measurement of projects by contrasting exact numbers with

those project budget. Management accounting aims at manufacturing an item as per established

performance standards at the least total price.

2. Pinpoint unnecessary management liability so that appropriate steps can be taken.

3. It encourages workers to meet set goals.

4. It promotes contact inside an organisation , for example among top managers or supervisors,

while enabling workers to work optimally

5. It guarantees the company is in good condition

6. This means that administrators and subordinates are centered, and hence facilitates the

alignment of performance.

Disadvantage:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1. This enables organizations to be arrogant as they continue to ignore certain critical resources

which can benefit the companies (Oyewo, 2017).

2. Subordinates can be forced to cover up unsafe conditions or to take measures which are not in

the best interests of the organization to ensure that the differences are advantageous.

3. There may be a propensity to prioritize compliance with requirements to neglect other critical

goals including such performance maintenance and enhancement, on-time logistics and customer

service.

4. It prohibits innovation because employees would not want to implement innovations,

particularly if such technologies may lead to negative initial variances.

5. This may lead to misleading judgments that may outcome in the decline of the institution, as

the information used in the calculation of the differences may be incorrect

Behavioral issue: Analysis of variance can contribute to brief-terms due to its inherent

propensity towards validated and short-term goals, as well as performance. Besides this, whether

there is bad impression about it so the non - optimal behavior among the workforce is

encouraged. One instance of this is trying to integrate slacks in the spending plan. This is one of

the key demerit points of using variance analysis to determine whether or not the participants

performed effectively (Tan, 2016).

PART B

1. FamaQ gives XLG competitive advantage

XLG is a pharmaceutical corporation that works in the United Kingdom and a few other

European places. The marketplace in which it conducts transactions is very challenging and one

of the key chemicals that give it competitive edge is the imports famaQ from Brazil. The

nationwide lockdown ended up taking part in the second qtr of March of 2020, and it was

imposed by UK relevant authorities. Because of this, the individual's disease outbreak opted to

expand its online deals so it could handle all of the lockdown difficulties that are occurring.

which can benefit the companies (Oyewo, 2017).

2. Subordinates can be forced to cover up unsafe conditions or to take measures which are not in

the best interests of the organization to ensure that the differences are advantageous.

3. There may be a propensity to prioritize compliance with requirements to neglect other critical

goals including such performance maintenance and enhancement, on-time logistics and customer

service.

4. It prohibits innovation because employees would not want to implement innovations,

particularly if such technologies may lead to negative initial variances.

5. This may lead to misleading judgments that may outcome in the decline of the institution, as

the information used in the calculation of the differences may be incorrect

Behavioral issue: Analysis of variance can contribute to brief-terms due to its inherent

propensity towards validated and short-term goals, as well as performance. Besides this, whether

there is bad impression about it so the non - optimal behavior among the workforce is

encouraged. One instance of this is trying to integrate slacks in the spending plan. This is one of

the key demerit points of using variance analysis to determine whether or not the participants

performed effectively (Tan, 2016).

PART B

1. FamaQ gives XLG competitive advantage

XLG is a pharmaceutical corporation that works in the United Kingdom and a few other

European places. The marketplace in which it conducts transactions is very challenging and one

of the key chemicals that give it competitive edge is the imports famaQ from Brazil. The

nationwide lockdown ended up taking part in the second qtr of March of 2020, and it was

imposed by UK relevant authorities. Because of this, the individual's disease outbreak opted to

expand its online deals so it could handle all of the lockdown difficulties that are occurring.

2. Demand for chemical X and Y has increased by 45% which is likely to continue according to

market research

It would be very necessary for the organization to ensure it tackles all of the negative

consequences that could arise from this. Despite of Lockdown it would be unlikely for XLG to

import famaQ from Brazil. Besides that, which ought to be transported, it can lead to multiple

dangers. There are greater chances of transmitting the corona virus, extended time delivery,

additional cost etc. After that, if it is not to be manufactured it may well lead to a decrease in

competitive edge since the key chemical that aim to ensure that is famaQ. In additament, the

requirement for chemicals X and Y has been forecast to reach by 45 percent and is sure to persist

as per the market research. Another of the key options that the company should concentrate on is

producing the famaQ in the UK so it can satisfy the needs of its consumers (Van der Stede,

2016).

3. The cost of making a unit of Fama Q in the UK is £3 with delivery times reducing by 15

working days

When it is made in the UK, the delivery of the goods can be shortened by fifteen days,

which ensures that the company will begin production earlier. With the exception of this, the

production cost per unit of famaQ in the UK would be 3 pounds which again is small in

comparison to the manufactured cost of 3.7 pounds a product. This indicates that the company,

instead of just sourcing it from Brazil, will make famaQ in the UK, because it would benefit in

different business advantages. Some of its major advantages include:

• If famaQ is manufactured it would promote the company as the production costs are very low

relative to the manufactured costs (Velasquez, Suomala and Järvenpää, 2015).

• The delivery date will be shortened by 15 days, so that development will start sooner and

satisfy economic growth.

• The risk of corona disease spreading would be zero if the famaQ chemicals are generated

instead of imported from Brazil.

• It will be very challenging to buy things at Lockdown so producing famaQ in the United

Kingdom is the best option for all activities to be carried out regularly in the potential.

market research

It would be very necessary for the organization to ensure it tackles all of the negative

consequences that could arise from this. Despite of Lockdown it would be unlikely for XLG to

import famaQ from Brazil. Besides that, which ought to be transported, it can lead to multiple

dangers. There are greater chances of transmitting the corona virus, extended time delivery,

additional cost etc. After that, if it is not to be manufactured it may well lead to a decrease in

competitive edge since the key chemical that aim to ensure that is famaQ. In additament, the

requirement for chemicals X and Y has been forecast to reach by 45 percent and is sure to persist

as per the market research. Another of the key options that the company should concentrate on is

producing the famaQ in the UK so it can satisfy the needs of its consumers (Van der Stede,

2016).

3. The cost of making a unit of Fama Q in the UK is £3 with delivery times reducing by 15

working days

When it is made in the UK, the delivery of the goods can be shortened by fifteen days,

which ensures that the company will begin production earlier. With the exception of this, the

production cost per unit of famaQ in the UK would be 3 pounds which again is small in

comparison to the manufactured cost of 3.7 pounds a product. This indicates that the company,

instead of just sourcing it from Brazil, will make famaQ in the UK, because it would benefit in

different business advantages. Some of its major advantages include:

• If famaQ is manufactured it would promote the company as the production costs are very low

relative to the manufactured costs (Velasquez, Suomala and Järvenpää, 2015).

• The delivery date will be shortened by 15 days, so that development will start sooner and

satisfy economic growth.

• The risk of corona disease spreading would be zero if the famaQ chemicals are generated

instead of imported from Brazil.

• It will be very challenging to buy things at Lockdown so producing famaQ in the United

Kingdom is the best option for all activities to be carried out regularly in the potential.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.