Management Accounting Report: XLG Case Study, Variance and Risk

VerifiedAdded on 2023/01/09

|14

|3459

|34

Report

AI Summary

This report delves into the core aspects of management accounting, focusing on variance analysis and risk assessment using the XLG case study. Part A presents practical calculations for sales price variance, sales volume contribution variance, material price planning variance, and material price operational variance. It also includes a critical analysis of the merits and demerits of using variances to evaluate managerial performance. Part B explores the risks associated with importing Farma Q, particularly patent infringement, and the impact of the COVID-19 lockdown on XLG's operations, including increased selling prices due to higher import costs. The report provides a comprehensive overview of financial reporting and decision-making in a dynamic market environment.

Management

Accounting - Report

Accounting - Report

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

PART B...........................................................................................................................................9

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION...........................................................................................................................3

PART A...........................................................................................................................................3

PART B...........................................................................................................................................9

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................14

INTRODUCTION

Companies are facing issues related to taking choices and conducting business in an efficient

manner in rapidly evolving market environment. Management Accounting is the first option for

handling workers to tackle these problems because there is a broader dimension that provides

several strategies and resources that reinforce the process for strategic decision taking (Lederer,

Umlauft and Hirche, 2019). The project report deals with the main facets of managerial

accounting required to determine the sustained performance of the company. The entire analysis

is composed of two sections: A and B. First section contains practical sums relating to numerous

variance calculations that are based on XLG case study. This also includes detailed assessment

of the benefits and disadvantages in introducing variances in the measurement of the results of

handling employees. Whereas the other section covers risk, importation of Farma Q and how this

may affect XLG during lock-down related to the study given in the brief.

PART A

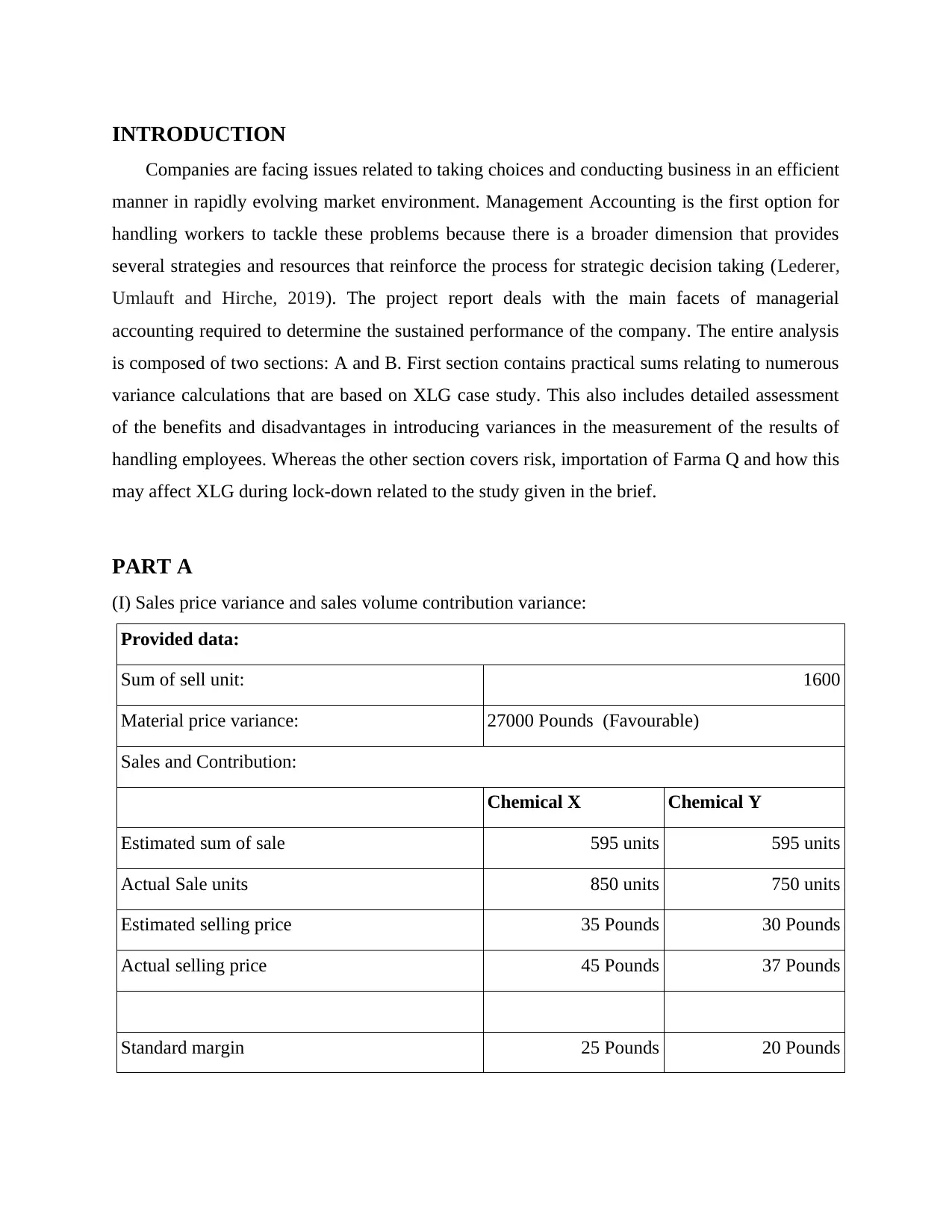

(I) Sales price variance and sales volume contribution variance:

Provided data:

Sum of sell unit: 1600

Material price variance: 27000 Pounds (Favourable)

Sales and Contribution:

Chemical X Chemical Y

Estimated sum of sale 595 units 595 units

Actual Sale units 850 units 750 units

Estimated selling price 35 Pounds 30 Pounds

Actual selling price 45 Pounds 37 Pounds

Standard margin 25 Pounds 20 Pounds

Companies are facing issues related to taking choices and conducting business in an efficient

manner in rapidly evolving market environment. Management Accounting is the first option for

handling workers to tackle these problems because there is a broader dimension that provides

several strategies and resources that reinforce the process for strategic decision taking (Lederer,

Umlauft and Hirche, 2019). The project report deals with the main facets of managerial

accounting required to determine the sustained performance of the company. The entire analysis

is composed of two sections: A and B. First section contains practical sums relating to numerous

variance calculations that are based on XLG case study. This also includes detailed assessment

of the benefits and disadvantages in introducing variances in the measurement of the results of

handling employees. Whereas the other section covers risk, importation of Farma Q and how this

may affect XLG during lock-down related to the study given in the brief.

PART A

(I) Sales price variance and sales volume contribution variance:

Provided data:

Sum of sell unit: 1600

Material price variance: 27000 Pounds (Favourable)

Sales and Contribution:

Chemical X Chemical Y

Estimated sum of sale 595 units 595 units

Actual Sale units 850 units 750 units

Estimated selling price 35 Pounds 30 Pounds

Actual selling price 45 Pounds 37 Pounds

Standard margin 25 Pounds 20 Pounds

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

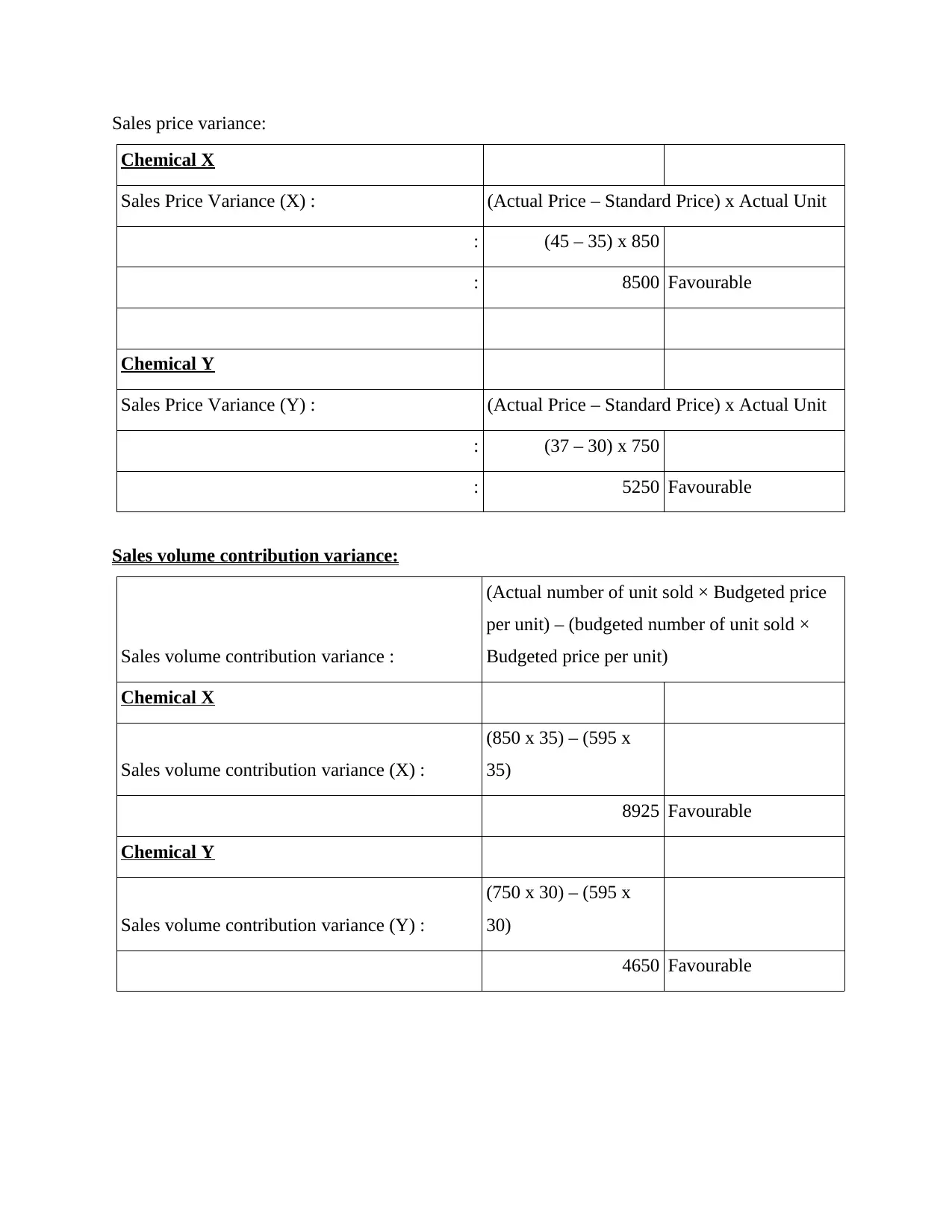

Sales price variance:

Chemical X

Sales Price Variance (X) : (Actual Price – Standard Price) x Actual Unit

: (45 – 35) x 850

: 8500 Favourable

Chemical Y

Sales Price Variance (Y) : (Actual Price – Standard Price) x Actual Unit

: (37 – 30) x 750

: 5250 Favourable

Sales volume contribution variance:

Sales volume contribution variance :

(Actual number of unit sold × Budgeted price

per unit) – (budgeted number of unit sold ×

Budgeted price per unit)

Chemical X

Sales volume contribution variance (X) :

(850 x 35) – (595 x

35)

8925 Favourable

Chemical Y

Sales volume contribution variance (Y) :

(750 x 30) – (595 x

30)

4650 Favourable

Chemical X

Sales Price Variance (X) : (Actual Price – Standard Price) x Actual Unit

: (45 – 35) x 850

: 8500 Favourable

Chemical Y

Sales Price Variance (Y) : (Actual Price – Standard Price) x Actual Unit

: (37 – 30) x 750

: 5250 Favourable

Sales volume contribution variance:

Sales volume contribution variance :

(Actual number of unit sold × Budgeted price

per unit) – (budgeted number of unit sold ×

Budgeted price per unit)

Chemical X

Sales volume contribution variance (X) :

(850 x 35) – (595 x

35)

8925 Favourable

Chemical Y

Sales volume contribution variance (Y) :

(750 x 30) – (595 x

30)

4650 Favourable

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

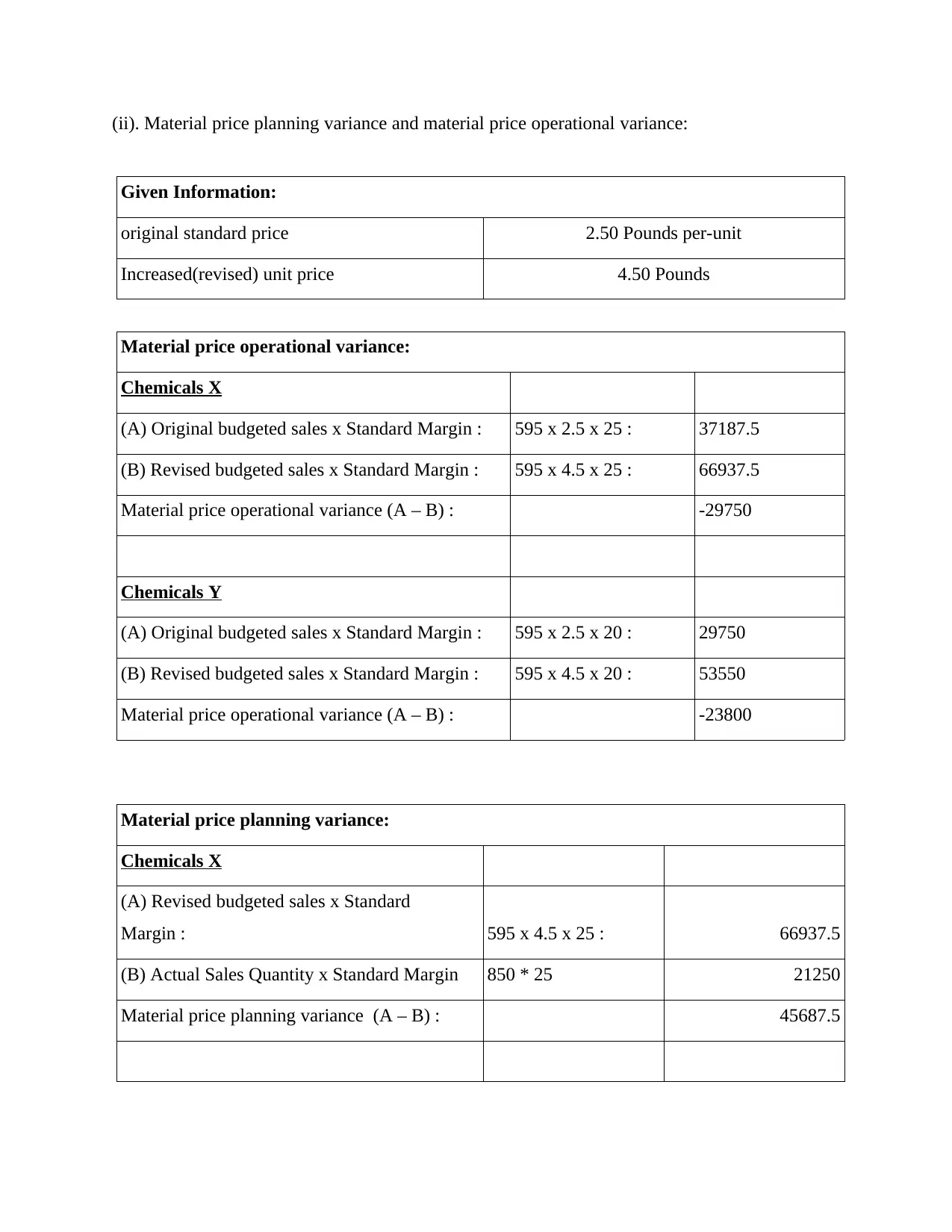

(ii). Material price planning variance and material price operational variance:

Given Information:

original standard price 2.50 Pounds per-unit

Increased(revised) unit price 4.50 Pounds

Material price operational variance:

Chemicals X

(A) Original budgeted sales x Standard Margin : 595 x 2.5 x 25 : 37187.5

(B) Revised budgeted sales x Standard Margin : 595 x 4.5 x 25 : 66937.5

Material price operational variance (A – B) : -29750

Chemicals Y

(A) Original budgeted sales x Standard Margin : 595 x 2.5 x 20 : 29750

(B) Revised budgeted sales x Standard Margin : 595 x 4.5 x 20 : 53550

Material price operational variance (A – B) : -23800

Material price planning variance:

Chemicals X

(A) Revised budgeted sales x Standard

Margin : 595 x 4.5 x 25 : 66937.5

(B) Actual Sales Quantity x Standard Margin 850 * 25 21250

Material price planning variance (A – B) : 45687.5

Given Information:

original standard price 2.50 Pounds per-unit

Increased(revised) unit price 4.50 Pounds

Material price operational variance:

Chemicals X

(A) Original budgeted sales x Standard Margin : 595 x 2.5 x 25 : 37187.5

(B) Revised budgeted sales x Standard Margin : 595 x 4.5 x 25 : 66937.5

Material price operational variance (A – B) : -29750

Chemicals Y

(A) Original budgeted sales x Standard Margin : 595 x 2.5 x 20 : 29750

(B) Revised budgeted sales x Standard Margin : 595 x 4.5 x 20 : 53550

Material price operational variance (A – B) : -23800

Material price planning variance:

Chemicals X

(A) Revised budgeted sales x Standard

Margin : 595 x 4.5 x 25 : 66937.5

(B) Actual Sales Quantity x Standard Margin 850 * 25 21250

Material price planning variance (A – B) : 45687.5

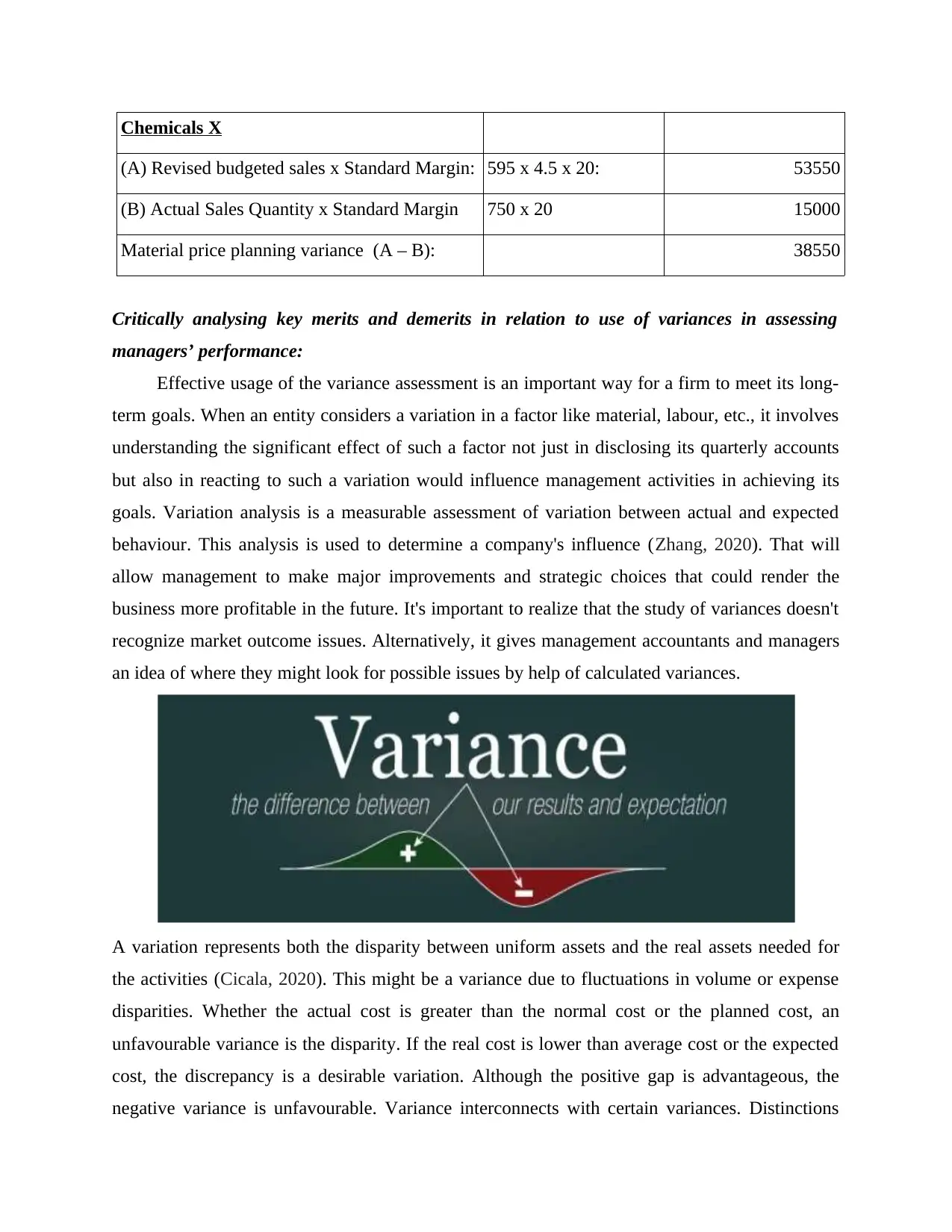

Chemicals X

(A) Revised budgeted sales x Standard Margin: 595 x 4.5 x 20: 53550

(B) Actual Sales Quantity x Standard Margin 750 x 20 15000

Material price planning variance (A – B): 38550

Critically analysing key merits and demerits in relation to use of variances in assessing

managers’ performance:

Effective usage of the variance assessment is an important way for a firm to meet its long-

term goals. When an entity considers a variation in a factor like material, labour, etc., it involves

understanding the significant effect of such a factor not just in disclosing its quarterly accounts

but also in reacting to such a variation would influence management activities in achieving its

goals. Variation analysis is a measurable assessment of variation between actual and expected

behaviour. This analysis is used to determine a company's influence (Zhang, 2020). That will

allow management to make major improvements and strategic choices that could render the

business more profitable in the future. It's important to realize that the study of variances doesn't

recognize market outcome issues. Alternatively, it gives management accountants and managers

an idea of where they might look for possible issues by help of calculated variances.

A variation represents both the disparity between uniform assets and the real assets needed for

the activities (Cicala, 2020). This might be a variance due to fluctuations in volume or expense

disparities. Whether the actual cost is greater than the normal cost or the planned cost, an

unfavourable variance is the disparity. If the real cost is lower than average cost or the expected

cost, the discrepancy is a desirable variation. Although the positive gap is advantageous, the

negative variance is unfavourable. Variance interconnects with certain variances. Distinctions

(A) Revised budgeted sales x Standard Margin: 595 x 4.5 x 20: 53550

(B) Actual Sales Quantity x Standard Margin 750 x 20 15000

Material price planning variance (A – B): 38550

Critically analysing key merits and demerits in relation to use of variances in assessing

managers’ performance:

Effective usage of the variance assessment is an important way for a firm to meet its long-

term goals. When an entity considers a variation in a factor like material, labour, etc., it involves

understanding the significant effect of such a factor not just in disclosing its quarterly accounts

but also in reacting to such a variation would influence management activities in achieving its

goals. Variation analysis is a measurable assessment of variation between actual and expected

behaviour. This analysis is used to determine a company's influence (Zhang, 2020). That will

allow management to make major improvements and strategic choices that could render the

business more profitable in the future. It's important to realize that the study of variances doesn't

recognize market outcome issues. Alternatively, it gives management accountants and managers

an idea of where they might look for possible issues by help of calculated variances.

A variation represents both the disparity between uniform assets and the real assets needed for

the activities (Cicala, 2020). This might be a variance due to fluctuations in volume or expense

disparities. Whether the actual cost is greater than the normal cost or the planned cost, an

unfavourable variance is the disparity. If the real cost is lower than average cost or the expected

cost, the discrepancy is a desirable variation. Although the positive gap is advantageous, the

negative variance is unfavourable. Variance interconnects with certain variances. Distinctions

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

between variances, whether beneficial or detrimental, are important in strategy formulation. A

detailed evaluation on the main benefits and demerits of the usage of variances in the

measurement of managerial performance follows in this regard:

Merits:

• Assurance of deviation from norm or expected is the very first importance of the study of the

variances. These separations should focus the analysis on the management. The necessary

information for such a deviation shall be given to the management, in particular for unfavourable

variance (cost is beyond expected).

• The second benefit of the variation would be its value in budget limits. In case of adverse

variance administrators take fair monitoring steps (Choi, Sun and Chung, 2019). Where

sufficient reasons are not given and reasonable control steps are taken, evidence of an adverse

variation is assessed in first place.

• Potential change of expenditure projections is the third value of uncertainty or deviation

studies. If, in addition to an incorrect expenditure estimate, there is no rational justification for

uncertainty, the outlook for opportunity should be updated or revised.

• The fourth value of this variation is to assess the productivity of the supervisors and the

management controller. Good variance indicates great manger efficiency, whereas negative

variance suggests poor results.

• The fifth benefit of variation analysis is to create a system of roles and obligations within the

organization. Defining roles and obligations strengthens structures of efficiency and regulation

within the organization.

• The calculation of variances or the analysis of variances provides a reporting mechanism inside

the organization. The consequences of adverse variances (material or labour costs are above

predicted) are accountable to all.

• In certain cases, budget vs. real variances may indicate that the company's product line or

intended customer market needs to be reassessed (Lei, Liu and Zhang, 2019). There's a lot of

guesswork in planning an estimate. If such assumptions contribute to expenditure blow-up, this

could be because the fundamental projections for a variety of reasons are entirely inaccurate.

That can be as simple as an economic transition or as complicated as challenges as it comes to

getting products out to customers. The needed changes could be shown inside the organization at

the end of each day.

detailed evaluation on the main benefits and demerits of the usage of variances in the

measurement of managerial performance follows in this regard:

Merits:

• Assurance of deviation from norm or expected is the very first importance of the study of the

variances. These separations should focus the analysis on the management. The necessary

information for such a deviation shall be given to the management, in particular for unfavourable

variance (cost is beyond expected).

• The second benefit of the variation would be its value in budget limits. In case of adverse

variance administrators take fair monitoring steps (Choi, Sun and Chung, 2019). Where

sufficient reasons are not given and reasonable control steps are taken, evidence of an adverse

variation is assessed in first place.

• Potential change of expenditure projections is the third value of uncertainty or deviation

studies. If, in addition to an incorrect expenditure estimate, there is no rational justification for

uncertainty, the outlook for opportunity should be updated or revised.

• The fourth value of this variation is to assess the productivity of the supervisors and the

management controller. Good variance indicates great manger efficiency, whereas negative

variance suggests poor results.

• The fifth benefit of variation analysis is to create a system of roles and obligations within the

organization. Defining roles and obligations strengthens structures of efficiency and regulation

within the organization.

• The calculation of variances or the analysis of variances provides a reporting mechanism inside

the organization. The consequences of adverse variances (material or labour costs are above

predicted) are accountable to all.

• In certain cases, budget vs. real variances may indicate that the company's product line or

intended customer market needs to be reassessed (Lei, Liu and Zhang, 2019). There's a lot of

guesswork in planning an estimate. If such assumptions contribute to expenditure blow-up, this

could be because the fundamental projections for a variety of reasons are entirely inaccurate.

That can be as simple as an economic transition or as complicated as challenges as it comes to

getting products out to customers. The needed changes could be shown inside the organization at

the end of each day.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

• This supports the organization in fulfilling its business goals and making the effective

utilization of the capital of the company. It also helps to create standards for the stakeholders

concerned. When the study of variation presents a set of results that produce large variances in

the data, it may indicate that there have been significant issues with the preparation of budgets.

Concerns can make a contribution to the use of inaccurate data or information, or database

calculation errors which used to plan either a spending plan or a real variance evaluate may

occur. Variability measurement is also a helpful means of checking the budgeting method of the

company. The organization wants to become far more mobile by making efforts to improve the

budget plan (Pogodin and Lattimore, 2019).

• Evaluation of variation is a critical form of tracking as it stats areas where actual outcome

differs from planned activities. Another advantage is that identifying areas where services are not

being utilized efficiently and places where improvements are required may be helpful. The

analysis of heterogeneity therefore promotes organizational versatility. Examination of variances

can also be used to identify areas where costs exceed and to determine if the specified uniform

costs are acceptable.

Demerits:

• Accounting department collects variances at the end of every month before sending the reports

to management. Manager requires feedback even quicker on most cases and it tends to rely on

warning signals or on-site behaviour (Ceraolo and Giorgi, 2020).

• Certain variance / variance variables are not included in accounting records, and accounting

departments will study and evaluate information such as coordinating research, spending on

supplies and payroll data to identify the triggers of such variances. This add-on procedure is cost-

effective when the management have been able to resolve the problems effectively on the

grounds of the provided knowledge.

• If budgeting does not take place on the basis of a detailed analysis of each element, the

budgeting process can be treated arbitrarily, which may vary from the actual estimates. For such

a scenario it cannot make sense to evaluate variances.

• A variance analysis has a major drawback in that it takes longer to evaluate the effects of the

variability and can therefore delay the corrective steps. The tracking system leads to a

considerable delay in time-frame and therefore would significantly postpone the emergence of

preventive measures (Su, 2020).

utilization of the capital of the company. It also helps to create standards for the stakeholders

concerned. When the study of variation presents a set of results that produce large variances in

the data, it may indicate that there have been significant issues with the preparation of budgets.

Concerns can make a contribution to the use of inaccurate data or information, or database

calculation errors which used to plan either a spending plan or a real variance evaluate may

occur. Variability measurement is also a helpful means of checking the budgeting method of the

company. The organization wants to become far more mobile by making efforts to improve the

budget plan (Pogodin and Lattimore, 2019).

• Evaluation of variation is a critical form of tracking as it stats areas where actual outcome

differs from planned activities. Another advantage is that identifying areas where services are not

being utilized efficiently and places where improvements are required may be helpful. The

analysis of heterogeneity therefore promotes organizational versatility. Examination of variances

can also be used to identify areas where costs exceed and to determine if the specified uniform

costs are acceptable.

Demerits:

• Accounting department collects variances at the end of every month before sending the reports

to management. Manager requires feedback even quicker on most cases and it tends to rely on

warning signals or on-site behaviour (Ceraolo and Giorgi, 2020).

• Certain variance / variance variables are not included in accounting records, and accounting

departments will study and evaluate information such as coordinating research, spending on

supplies and payroll data to identify the triggers of such variances. This add-on procedure is cost-

effective when the management have been able to resolve the problems effectively on the

grounds of the provided knowledge.

• If budgeting does not take place on the basis of a detailed analysis of each element, the

budgeting process can be treated arbitrarily, which may vary from the actual estimates. For such

a scenario it cannot make sense to evaluate variances.

• A variance analysis has a major drawback in that it takes longer to evaluate the effects of the

variability and can therefore delay the corrective steps. The tracking system leads to a

considerable delay in time-frame and therefore would significantly postpone the emergence of

preventive measures (Su, 2020).

PART B

This is becoming extremely prevalent for purchasers to presume sellers to create binding

assurances that resale products bought from sellers would not violate third-party patents.

Vendors, as well as importers in specific, find themself in a complicated situation since they may

not realize whether solution applied in product is safeguarded by patent rights (Wang, Xu and

Feng, 2019). As here in case study given that XLG corporation that is cleaning

products corporation situated in eastern part, UK, it produces two major cleaning

agents, chemical name X and Y. XLG currently runs in a very competitive atmosphere;

Though, over years, they have sustained their market top position as a result of patent against

fama Q i.e. effective cleaning agent, implying that it could not be replicated by other competing

companies within industry. XLG has launched a number of stores throughout the UK and is also

selling their brands online, hosting a number of demonstration shows to attract buyers to their

brands. In the second half of year beginning in mar.2020, corona virus began to break out

and United Kingdom Government imposed a national lock-down to tackle the epidemic,

pressuring XLG to relocate all sales online.

Patent infringement relates to any incident involving the usage or use, use, bid, sale

and/or importing of patented item for benefit or professional reasons without the permission

of patent proprietor. Right to restrict imports of patented product is fundamental right given

to patent owner. Here in given case case major risk posed due to import of famaQ is patent

infringement which also can lead to many legal issues such as litigation and claims. Also here

notable aspect is lock-down due to corona virus outbreak. This affected economy of UK

adversely but here considerable change is that companies are now forced to sell their products

online (Webster and Lark, 2019).

As given in case study of XLG, due to lock-down, there is significant increase in the

selling prices as the standard selling price of per unit of chemical X has been increased form £35

per unit to £45 per unit while in case of chemical Y, selling price has been reached to £37 per

unit from £30 per unit. Major cause of this increment in selling price is increase in price of fama

Q that is company's superior cleaning element which is mixed in its products. Because of lock-

down as well as prohibitions and restrictions on international travellings, it become necessary for

company to import fama Q from air transport system. This has increased import cost

significantly as air transport is too expensive as compared to sea transport. Due to this increase in

This is becoming extremely prevalent for purchasers to presume sellers to create binding

assurances that resale products bought from sellers would not violate third-party patents.

Vendors, as well as importers in specific, find themself in a complicated situation since they may

not realize whether solution applied in product is safeguarded by patent rights (Wang, Xu and

Feng, 2019). As here in case study given that XLG corporation that is cleaning

products corporation situated in eastern part, UK, it produces two major cleaning

agents, chemical name X and Y. XLG currently runs in a very competitive atmosphere;

Though, over years, they have sustained their market top position as a result of patent against

fama Q i.e. effective cleaning agent, implying that it could not be replicated by other competing

companies within industry. XLG has launched a number of stores throughout the UK and is also

selling their brands online, hosting a number of demonstration shows to attract buyers to their

brands. In the second half of year beginning in mar.2020, corona virus began to break out

and United Kingdom Government imposed a national lock-down to tackle the epidemic,

pressuring XLG to relocate all sales online.

Patent infringement relates to any incident involving the usage or use, use, bid, sale

and/or importing of patented item for benefit or professional reasons without the permission

of patent proprietor. Right to restrict imports of patented product is fundamental right given

to patent owner. Here in given case case major risk posed due to import of famaQ is patent

infringement which also can lead to many legal issues such as litigation and claims. Also here

notable aspect is lock-down due to corona virus outbreak. This affected economy of UK

adversely but here considerable change is that companies are now forced to sell their products

online (Webster and Lark, 2019).

As given in case study of XLG, due to lock-down, there is significant increase in the

selling prices as the standard selling price of per unit of chemical X has been increased form £35

per unit to £45 per unit while in case of chemical Y, selling price has been reached to £37 per

unit from £30 per unit. Major cause of this increment in selling price is increase in price of fama

Q that is company's superior cleaning element which is mixed in its products. Because of lock-

down as well as prohibitions and restrictions on international travellings, it become necessary for

company to import fama Q from air transport system. This has increased import cost

significantly as air transport is too expensive as compared to sea transport. Due to this increase in

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

transport costs, selling price of chemical X and Y has been increased. Fama Q's standard price

was £2.50 per unit that has been increased to £4.50 per unit but actually paid price by XLG is

£3.70 per unit. Here considerable impact is that company's overall profit margin would be

affected. Along with selling price, here a sudden increase has been reported in demand and

consumption of chemical X and Y. During second quarter, estimated total demand of chemical X

and Y i.e. 1190 units has been increased to 850 units and 750 respectively for chemical X and

chemical Y. This increment is favourable for company as this increased overall sell of its major

products. This is one of the major impact of lock-down. Reason behind such significant increase

is increased demand of cleaning products because now people have become more conscious

about cleanness and hygiene (Seaman, Riffe and Caswell, 2019).

Moreover, additional information provided in case study that if company makes single

unit of fama Q it will cost company to £3 per unit along with decreasing 15 days’ delivery time.

Here it is also provided that demand for chemical X and Y increased by 45 percent and

anticipated to be continue. Thus based on additional information and case study there are two

options available for company, as listed below:

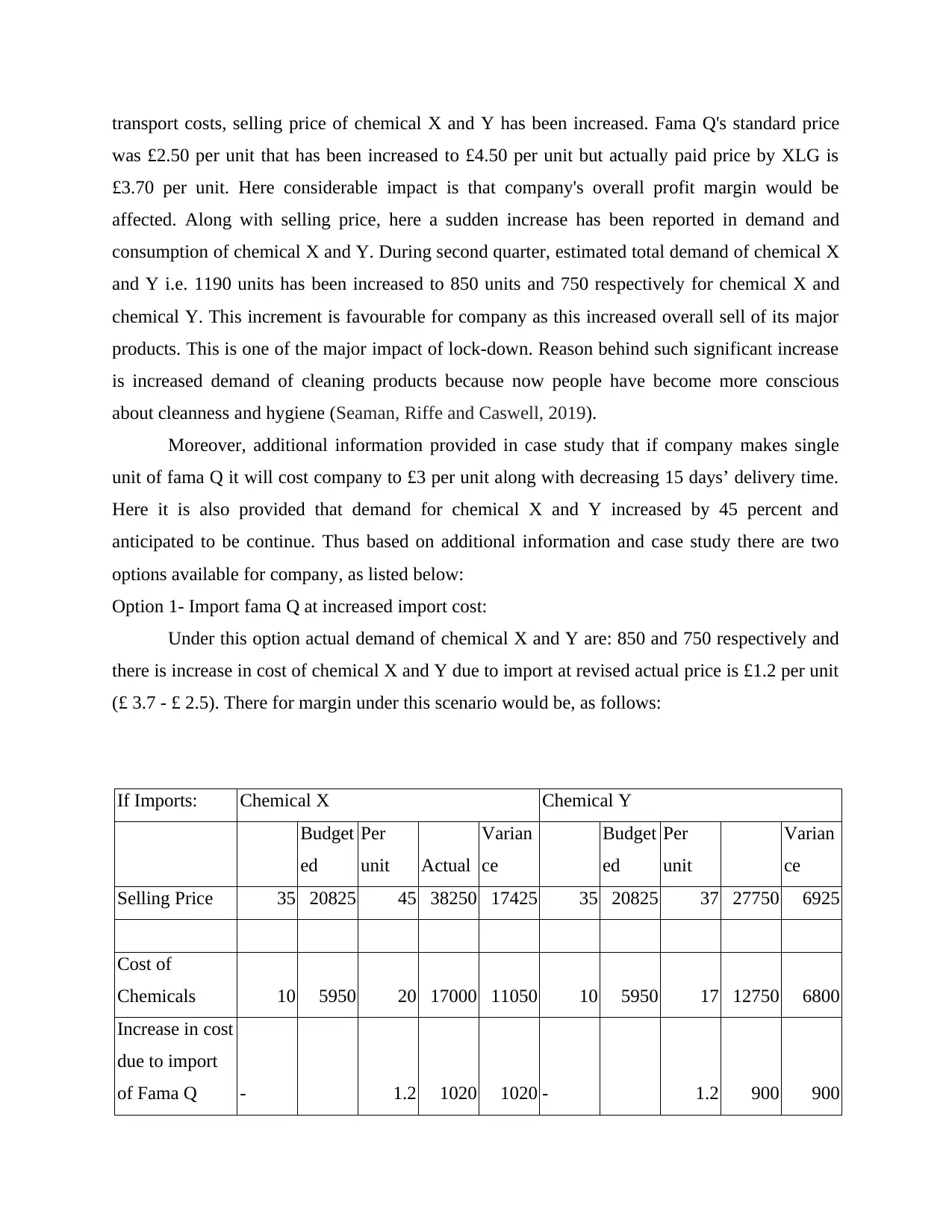

Option 1- Import fama Q at increased import cost:

Under this option actual demand of chemical X and Y are: 850 and 750 respectively and

there is increase in cost of chemical X and Y due to import at revised actual price is £1.2 per unit

(£ 3.7 - £ 2.5). There for margin under this scenario would be, as follows:

If Imports: Chemical X Chemical Y

Budget

ed

Per

unit Actual

Varian

ce

Budget

ed

Per

unit

Varian

ce

Selling Price 35 20825 45 38250 17425 35 20825 37 27750 6925

Cost of

Chemicals 10 5950 20 17000 11050 10 5950 17 12750 6800

Increase in cost

due to import

of Fama Q - 1.2 1020 1020 - 1.2 900 900

was £2.50 per unit that has been increased to £4.50 per unit but actually paid price by XLG is

£3.70 per unit. Here considerable impact is that company's overall profit margin would be

affected. Along with selling price, here a sudden increase has been reported in demand and

consumption of chemical X and Y. During second quarter, estimated total demand of chemical X

and Y i.e. 1190 units has been increased to 850 units and 750 respectively for chemical X and

chemical Y. This increment is favourable for company as this increased overall sell of its major

products. This is one of the major impact of lock-down. Reason behind such significant increase

is increased demand of cleaning products because now people have become more conscious

about cleanness and hygiene (Seaman, Riffe and Caswell, 2019).

Moreover, additional information provided in case study that if company makes single

unit of fama Q it will cost company to £3 per unit along with decreasing 15 days’ delivery time.

Here it is also provided that demand for chemical X and Y increased by 45 percent and

anticipated to be continue. Thus based on additional information and case study there are two

options available for company, as listed below:

Option 1- Import fama Q at increased import cost:

Under this option actual demand of chemical X and Y are: 850 and 750 respectively and

there is increase in cost of chemical X and Y due to import at revised actual price is £1.2 per unit

(£ 3.7 - £ 2.5). There for margin under this scenario would be, as follows:

If Imports: Chemical X Chemical Y

Budget

ed

Per

unit Actual

Varian

ce

Budget

ed

Per

unit

Varian

ce

Selling Price 35 20825 45 38250 17425 35 20825 37 27750 6925

Cost of

Chemicals 10 5950 20 17000 11050 10 5950 17 12750 6800

Increase in cost

due to import

of Fama Q - 1.2 1020 1020 - 1.2 900 900

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Total Cost 10 5950 21.2 18020 12070 10 5950 18.2 13650 7700

Profit Margin 25 14875 23.8 20230 5355 25 14875 18.8 14100 -775

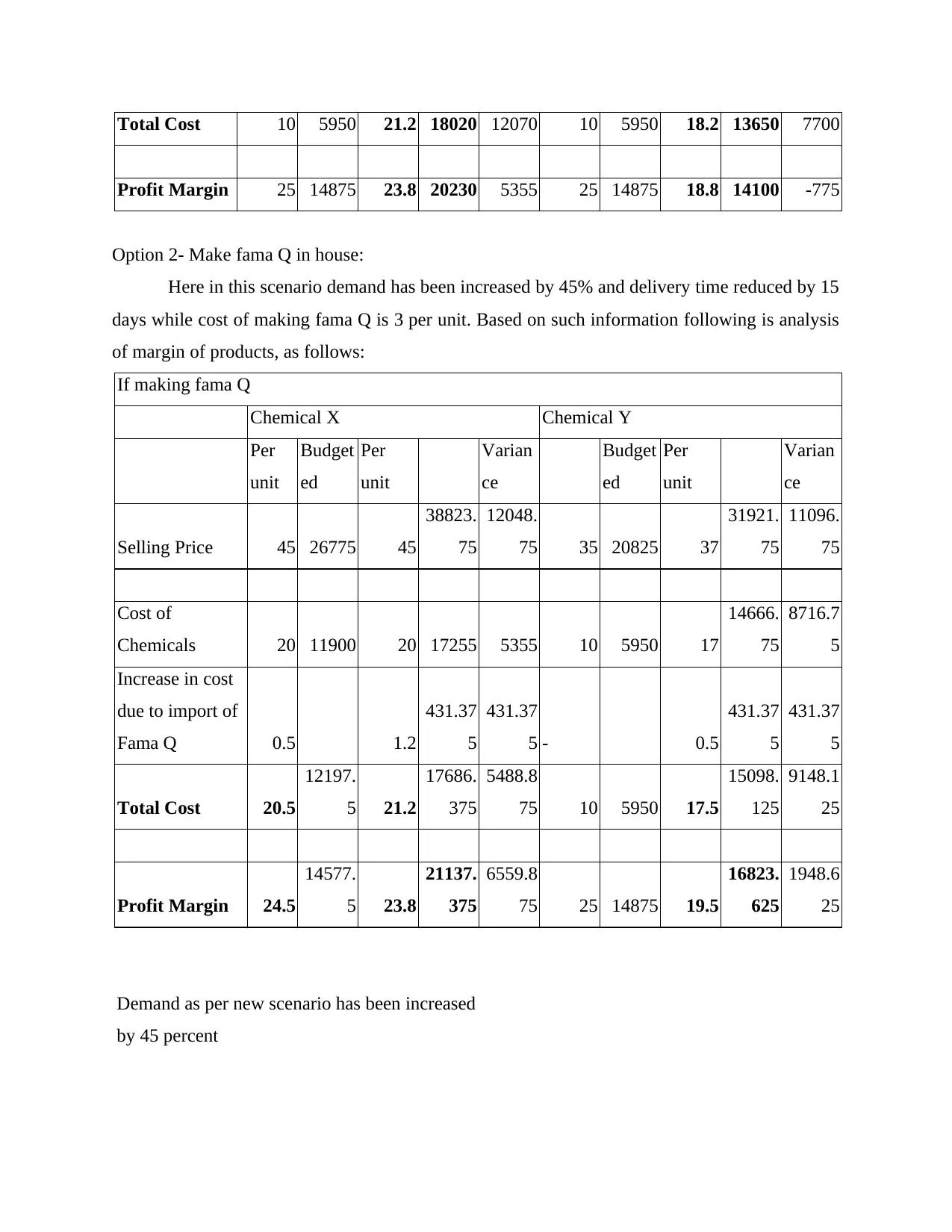

Option 2- Make fama Q in house:

Here in this scenario demand has been increased by 45% and delivery time reduced by 15

days while cost of making fama Q is 3 per unit. Based on such information following is analysis

of margin of products, as follows:

If making fama Q

Chemical X Chemical Y

Per

unit

Budget

ed

Per

unit

Varian

ce

Budget

ed

Per

unit

Varian

ce

Selling Price 45 26775 45

38823.

75

12048.

75 35 20825 37

31921.

75

11096.

75

Cost of

Chemicals 20 11900 20 17255 5355 10 5950 17

14666.

75

8716.7

5

Increase in cost

due to import of

Fama Q 0.5 1.2

431.37

5

431.37

5 - 0.5

431.37

5

431.37

5

Total Cost 20.5

12197.

5 21.2

17686.

375

5488.8

75 10 5950 17.5

15098.

125

9148.1

25

Profit Margin 24.5

14577.

5 23.8

21137.

375

6559.8

75 25 14875 19.5

16823.

625

1948.6

25

Demand as per new scenario has been increased

by 45 percent

Profit Margin 25 14875 23.8 20230 5355 25 14875 18.8 14100 -775

Option 2- Make fama Q in house:

Here in this scenario demand has been increased by 45% and delivery time reduced by 15

days while cost of making fama Q is 3 per unit. Based on such information following is analysis

of margin of products, as follows:

If making fama Q

Chemical X Chemical Y

Per

unit

Budget

ed

Per

unit

Varian

ce

Budget

ed

Per

unit

Varian

ce

Selling Price 45 26775 45

38823.

75

12048.

75 35 20825 37

31921.

75

11096.

75

Cost of

Chemicals 20 11900 20 17255 5355 10 5950 17

14666.

75

8716.7

5

Increase in cost

due to import of

Fama Q 0.5 1.2

431.37

5

431.37

5 - 0.5

431.37

5

431.37

5

Total Cost 20.5

12197.

5 21.2

17686.

375

5488.8

75 10 5950 17.5

15098.

125

9148.1

25

Profit Margin 24.5

14577.

5 23.8

21137.

375

6559.8

75 25 14875 19.5

16823.

625

1948.6

25

Demand as per new scenario has been increased

by 45 percent

So, new demand for Chemical X and Y would

be:

Chemical X 595+ 595*45% 862.75

Chemical Y 595+ 595 * 45% 862.75

Through the evaluation of both the options it has been analysed that making in-house

fama Q would be more viable for company (Underdal, 2019). As the in case of both Chemical X

and Y, margin is higher if company making famaQ itself instead of making import. Also it has

been analysed in comparison with budgeted figures that option of making famaQ would be more

beneficial for corporation.

CONCLUSION

From aforementioned study this has been evaluated that Management accounting is

valuable for enterprises to handle their operations. This contains the important tactics,

frameworks, reporting approaches and other practices that ultimately assist decision-making

tasks within a business. It is not compulsory for business entities to follow management

accounting frameworks but in real life it is not practical for a business entity which operating in

competitive to environment and deal with different issues. Further it proposes several techniques

which not only support key decisions of managing personnel but also offer a assistive framework

for formulation of strategies.

be:

Chemical X 595+ 595*45% 862.75

Chemical Y 595+ 595 * 45% 862.75

Through the evaluation of both the options it has been analysed that making in-house

fama Q would be more viable for company (Underdal, 2019). As the in case of both Chemical X

and Y, margin is higher if company making famaQ itself instead of making import. Also it has

been analysed in comparison with budgeted figures that option of making famaQ would be more

beneficial for corporation.

CONCLUSION

From aforementioned study this has been evaluated that Management accounting is

valuable for enterprises to handle their operations. This contains the important tactics,

frameworks, reporting approaches and other practices that ultimately assist decision-making

tasks within a business. It is not compulsory for business entities to follow management

accounting frameworks but in real life it is not practical for a business entity which operating in

competitive to environment and deal with different issues. Further it proposes several techniques

which not only support key decisions of managing personnel but also offer a assistive framework

for formulation of strategies.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.