Management Accounting Report: Variance Analysis for XLG plc (LCBB5002)

VerifiedAdded on 2023/01/07

|14

|3250

|75

Report

AI Summary

This report, prepared for a management accounting course (LCBB5002), delves into variance analysis and its application within a business context. It begins with an introduction to management accounting and the importance of variance analysis, a technique used to compare actual data with financial projections. The main body of the report is divided into two parts. Part A focuses on the computation of various variances, including sales price, sales volume contribution, material price planning, and operational variances. Part B examines the make-or-buy decision, presenting a case study on XLG plc and its choice regarding the production of a cleaning material, Fama Q. The report analyzes the costs and benefits associated with in-house manufacturing versus purchasing from an external supplier. The report concludes with a discussion of the merits and demerits of variance analysis in assessing managerial performance and offering recommendations for decision-making. References are included to support the analysis and findings presented.

LCBB5002

MANAGEMENT

ACCOUNTING – 2

MANAGEMENT

ACCOUNTING – 2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION.....................................................................................................................................3

MAIN BODY.............................................................................................................................................3

Part A......................................................................................................................................................3

Part B.....................................................................................................................................................10

CONCLUSION........................................................................................................................................13

REFERENCES........................................................................................................................................14

INTRODUCTION.....................................................................................................................................3

MAIN BODY.............................................................................................................................................3

Part A......................................................................................................................................................3

Part B.....................................................................................................................................................10

CONCLUSION........................................................................................................................................13

REFERENCES........................................................................................................................................14

INTRODUCTION

The management accounting (MA) is known as a form of accounting that is associated to

handling monetary and non-monetary resources in a manner so that corrective actions can be

carried out for decision making (Cescon, Costantini and Grassetti, 2019). This accounting

contains a range of techniques and variance analysis is considered as one of the key approach

which is connected to compare actual data with financial projections. Majority of executive of

companies, rely on this method in order to take viable financial judgments. In the report a case

study has been discussed which is based on calculation of variances and suggesting a suitable

alternative to XLG plc. The project report is based on two tasks which are A and B. The part A

contains information related to calculation of different kinds of variables have been done. While

in part B, detailed information regarding to selection of an alternative has been done by using

appropriate methods.

MAIN BODY

Part A

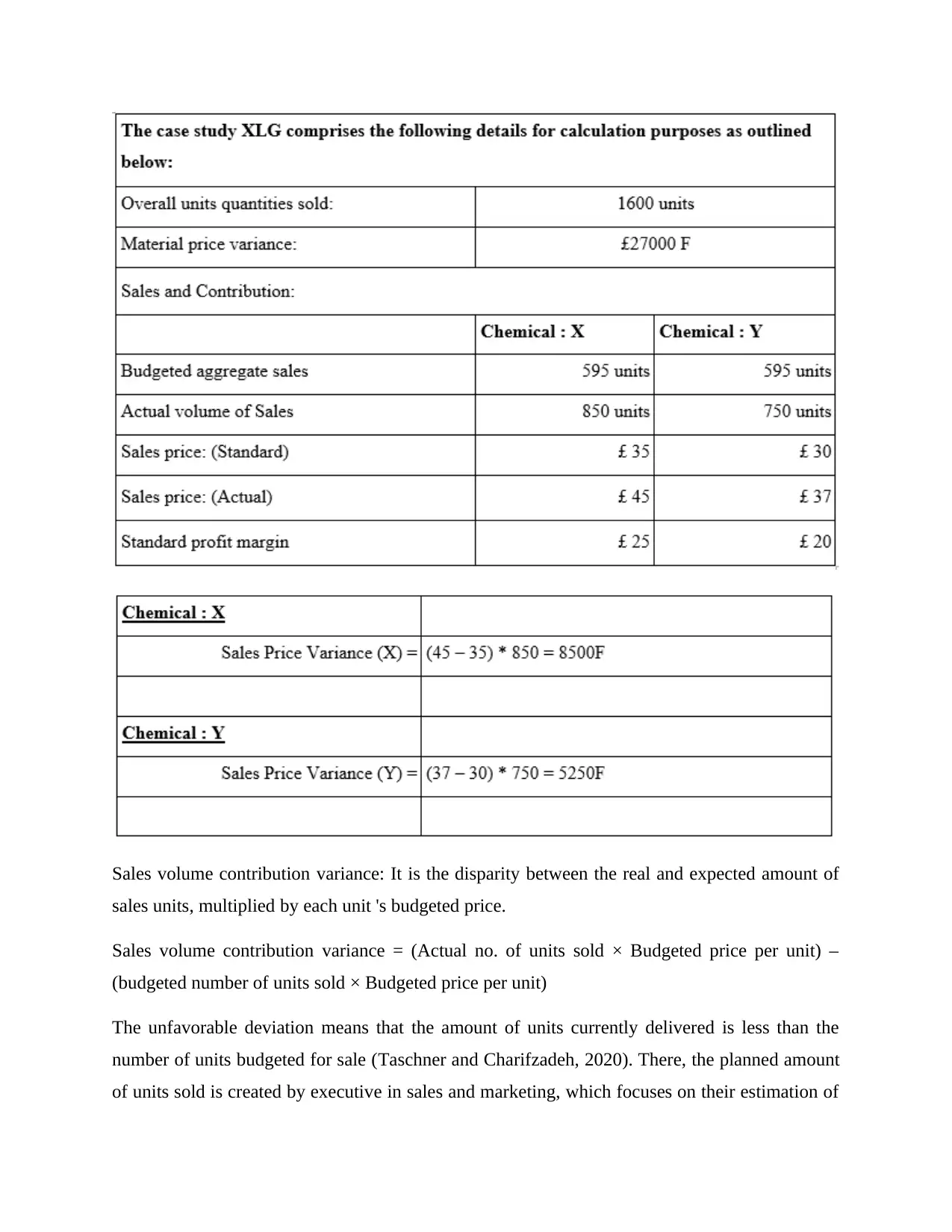

(i) Computation of the Sales price variances and sales volume contribution variances:

Sales price variance: The variance in the selling price means a discrepancy between real and

expected sales arising from a change in commodity price (Labrador and Olmo, 2019).

Sales price variance = (Actual Price – Standard Price) * Actual Unit

The value of negative variance indicates that actual price is shorter as compared to projected

prices. On the other hands, positive variance shows that actual prices are more than estimated

prices (Dai, Free and Gendron, 2019). By help of this variance, it becomes easier for companies

to know about level of price on which they can sell their items.

The management accounting (MA) is known as a form of accounting that is associated to

handling monetary and non-monetary resources in a manner so that corrective actions can be

carried out for decision making (Cescon, Costantini and Grassetti, 2019). This accounting

contains a range of techniques and variance analysis is considered as one of the key approach

which is connected to compare actual data with financial projections. Majority of executive of

companies, rely on this method in order to take viable financial judgments. In the report a case

study has been discussed which is based on calculation of variances and suggesting a suitable

alternative to XLG plc. The project report is based on two tasks which are A and B. The part A

contains information related to calculation of different kinds of variables have been done. While

in part B, detailed information regarding to selection of an alternative has been done by using

appropriate methods.

MAIN BODY

Part A

(i) Computation of the Sales price variances and sales volume contribution variances:

Sales price variance: The variance in the selling price means a discrepancy between real and

expected sales arising from a change in commodity price (Labrador and Olmo, 2019).

Sales price variance = (Actual Price – Standard Price) * Actual Unit

The value of negative variance indicates that actual price is shorter as compared to projected

prices. On the other hands, positive variance shows that actual prices are more than estimated

prices (Dai, Free and Gendron, 2019). By help of this variance, it becomes easier for companies

to know about level of price on which they can sell their items.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

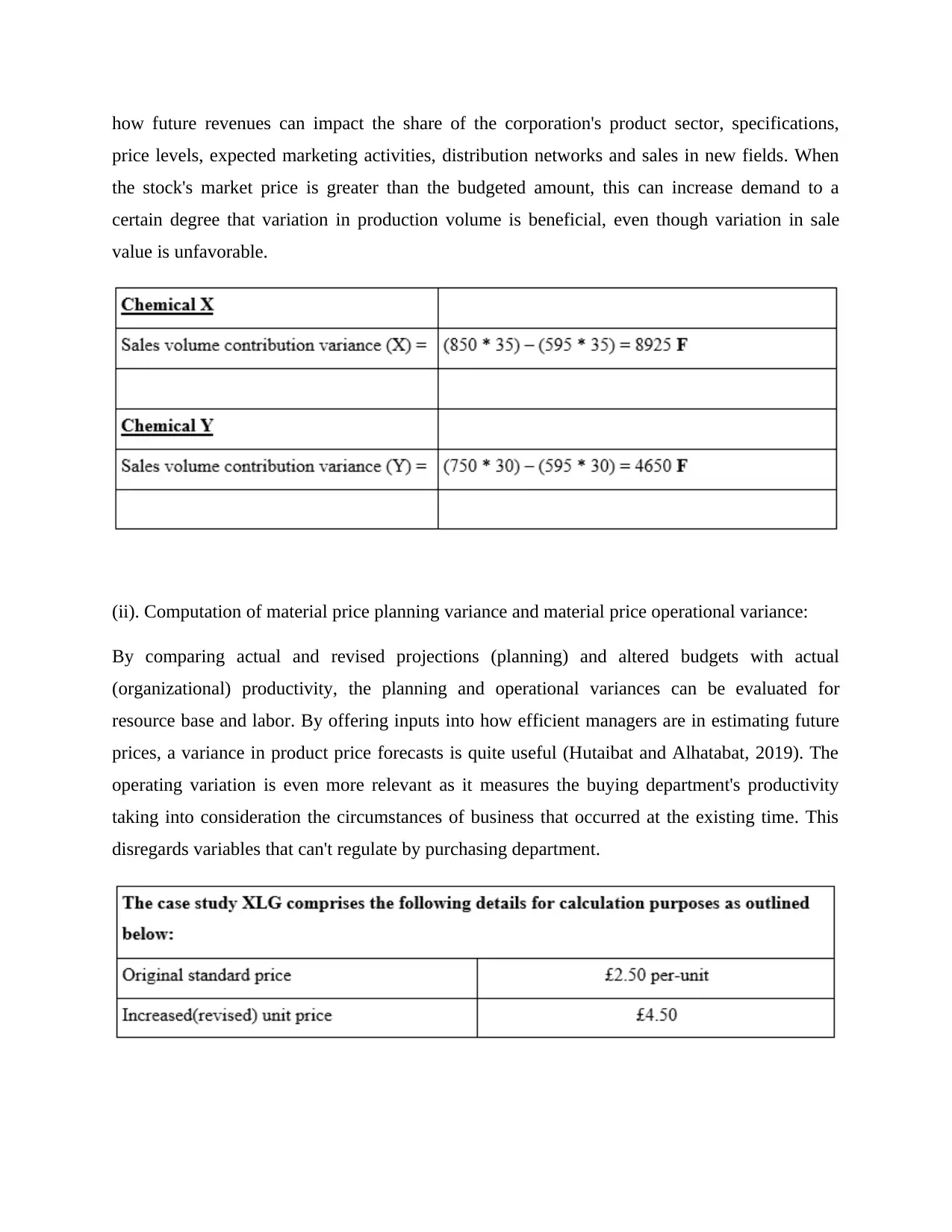

Sales volume contribution variance: It is the disparity between the real and expected amount of

sales units, multiplied by each unit 's budgeted price.

Sales volume contribution variance = (Actual no. of units sold × Budgeted price per unit) –

(budgeted number of units sold × Budgeted price per unit)

The unfavorable deviation means that the amount of units currently delivered is less than the

number of units budgeted for sale (Taschner and Charifzadeh, 2020). There, the planned amount

of units sold is created by executive in sales and marketing, which focuses on their estimation of

sales units, multiplied by each unit 's budgeted price.

Sales volume contribution variance = (Actual no. of units sold × Budgeted price per unit) –

(budgeted number of units sold × Budgeted price per unit)

The unfavorable deviation means that the amount of units currently delivered is less than the

number of units budgeted for sale (Taschner and Charifzadeh, 2020). There, the planned amount

of units sold is created by executive in sales and marketing, which focuses on their estimation of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

how future revenues can impact the share of the corporation's product sector, specifications,

price levels, expected marketing activities, distribution networks and sales in new fields. When

the stock's market price is greater than the budgeted amount, this can increase demand to a

certain degree that variation in production volume is beneficial, even though variation in sale

value is unfavorable.

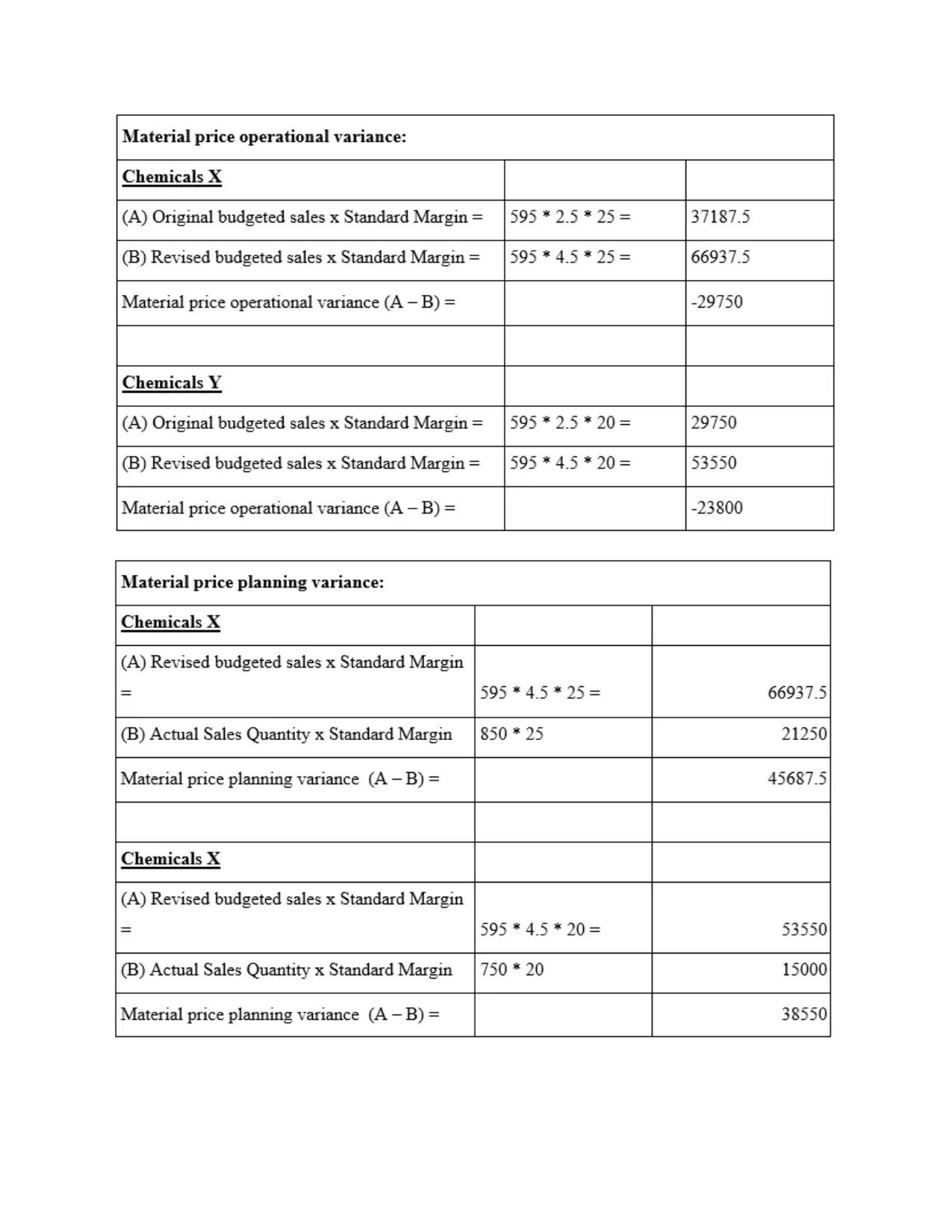

(ii). Computation of material price planning variance and material price operational variance:

By comparing actual and revised projections (planning) and altered budgets with actual

(organizational) productivity, the planning and operational variances can be evaluated for

resource base and labor. By offering inputs into how efficient managers are in estimating future

prices, a variance in product price forecasts is quite useful (Hutaibat and Alhatabat, 2019). The

operating variation is even more relevant as it measures the buying department's productivity

taking into consideration the circumstances of business that occurred at the existing time. This

disregards variables that can't regulate by purchasing department.

price levels, expected marketing activities, distribution networks and sales in new fields. When

the stock's market price is greater than the budgeted amount, this can increase demand to a

certain degree that variation in production volume is beneficial, even though variation in sale

value is unfavorable.

(ii). Computation of material price planning variance and material price operational variance:

By comparing actual and revised projections (planning) and altered budgets with actual

(organizational) productivity, the planning and operational variances can be evaluated for

resource base and labor. By offering inputs into how efficient managers are in estimating future

prices, a variance in product price forecasts is quite useful (Hutaibat and Alhatabat, 2019). The

operating variation is even more relevant as it measures the buying department's productivity

taking into consideration the circumstances of business that occurred at the existing time. This

disregards variables that can't regulate by purchasing department.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

(iii). Comprehend analysis of all substantial merits and demerits linked with variances use in

determining managers’ performance:

Variance analysis- A variance in the expenditure or income is a regular calculation utilized by

nations, companies or entities to compute the discrepancy between the expected and real

estimates within a certain form of accounting period (Pasch, 2019). A favorable variance in the

income or expense corresponds to positive variances or benefits; an adverse variance in the

income or expense defines negative variance which implies losses or shortages. The variances

exist as forecasters that cannot entirely reliable to foresee projected expenses and revenues.

Variance is determined by taking the variations between each variable in the data set and the

norm, then quadrating the variations to render them meaningful, and then separating the squares

by the amount of values in the data set. This is being computed by applying below mentioned

formula that is as follows:

Variance: Actual outcome – estimated outcome

This is a common formula to measure the variance which can be used by any individual in an

organization. Though, in statistics there are a range of other formulas which are being used by

companies to measure their performance related to different aspects. For instance, in the context

of above XLG plc different kinds of variances have been computed with an aim of assessing

their performance in terms of price, material and many more. This method has certain merits and

demerits that are explained below in such manner:

Merits-

Analysis of variance is an important monitoring tool, since it tends to focus on situations

where real activity varies from expected operations. The benefit is that variance analysis

can be valuable in finding places where assets are not used adequately and where changes

are needed. Therefore, variance analysis facilitates efficiency in management of

performance. Examination of variances may also be used to find situations where cost

overruns or actual income is too lower. In different kinds of companies, a range of

variances are computed which contributes to managers in order to track each activities’

performance individually. On the behalf of this, managers take suitable actions and

prepare strategies to overcome from adverse situations.

determining managers’ performance:

Variance analysis- A variance in the expenditure or income is a regular calculation utilized by

nations, companies or entities to compute the discrepancy between the expected and real

estimates within a certain form of accounting period (Pasch, 2019). A favorable variance in the

income or expense corresponds to positive variances or benefits; an adverse variance in the

income or expense defines negative variance which implies losses or shortages. The variances

exist as forecasters that cannot entirely reliable to foresee projected expenses and revenues.

Variance is determined by taking the variations between each variable in the data set and the

norm, then quadrating the variations to render them meaningful, and then separating the squares

by the amount of values in the data set. This is being computed by applying below mentioned

formula that is as follows:

Variance: Actual outcome – estimated outcome

This is a common formula to measure the variance which can be used by any individual in an

organization. Though, in statistics there are a range of other formulas which are being used by

companies to measure their performance related to different aspects. For instance, in the context

of above XLG plc different kinds of variances have been computed with an aim of assessing

their performance in terms of price, material and many more. This method has certain merits and

demerits that are explained below in such manner:

Merits-

Analysis of variance is an important monitoring tool, since it tends to focus on situations

where real activity varies from expected operations. The benefit is that variance analysis

can be valuable in finding places where assets are not used adequately and where changes

are needed. Therefore, variance analysis facilitates efficiency in management of

performance. Examination of variances may also be used to find situations where cost

overruns or actual income is too lower. In different kinds of companies, a range of

variances are computed which contributes to managers in order to track each activities’

performance individually. On the behalf of this, managers take suitable actions and

prepare strategies to overcome from adverse situations.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Analysis of variances leads to encourage the transfer of liability and activates monitoring

structures on divisions where they are needed. For instance, if labor performance

variation is seen as undesirable or raw material cost variance is undesirable then

companies can enhance control of such departments to improve output. Such as in the

context of above XLG plc, their performance is too lower as some variances are

producing unfavorable outcome then the managers can apply suitable framework in order

to deal with financial issues in an effective manner. This technique helps to prevent

negative impact on companies’ performance.

Variance analysis may even often offer way about how effectively an enterprise can be

handled. In the case of purchases, for example, the inability to negotiate product price or

to secure competitive tenders could imply organizational challenges within the

purchasing department (Tekathen, 2019). Furthermore, poor sales may also be a sign that

sales departments’ employees are not well trained or have lack inspiration. These all

aspects are useful for companies in order to deduct poor performance of any particular or

specific department. On the behalf of gathered information, managers can prepare

effective policies and plans to deal with raised issues.

The finance departments collect information that they need to grasp the explanations for

uncontrollable external variances, utilizing variance analysis. If they become informed of

these variation, then they can enforce strategies to minimize these uncertainties resulting

from these variances. Eventually, by help of variance analysis it becomes feasible for

managers to know about all unfavorable conditions. Mainly, the variance analysis is

useful for finance department as they can gather key details about different kinds of

activities which are resulting as higher expense or producing lower revenues as compared

to estimation.

Demerits:

In majority of situations, the variances are not visible in accounting reports, and due to

which accounting managers need to look over documents such as work routings,

inventory payments, and recorded overtime to ascertain the causes for these variances.

These add-on operation is cost-effective only when the management has been able to

structures on divisions where they are needed. For instance, if labor performance

variation is seen as undesirable or raw material cost variance is undesirable then

companies can enhance control of such departments to improve output. Such as in the

context of above XLG plc, their performance is too lower as some variances are

producing unfavorable outcome then the managers can apply suitable framework in order

to deal with financial issues in an effective manner. This technique helps to prevent

negative impact on companies’ performance.

Variance analysis may even often offer way about how effectively an enterprise can be

handled. In the case of purchases, for example, the inability to negotiate product price or

to secure competitive tenders could imply organizational challenges within the

purchasing department (Tekathen, 2019). Furthermore, poor sales may also be a sign that

sales departments’ employees are not well trained or have lack inspiration. These all

aspects are useful for companies in order to deduct poor performance of any particular or

specific department. On the behalf of gathered information, managers can prepare

effective policies and plans to deal with raised issues.

The finance departments collect information that they need to grasp the explanations for

uncontrollable external variances, utilizing variance analysis. If they become informed of

these variation, then they can enforce strategies to minimize these uncertainties resulting

from these variances. Eventually, by help of variance analysis it becomes feasible for

managers to know about all unfavorable conditions. Mainly, the variance analysis is

useful for finance department as they can gather key details about different kinds of

activities which are resulting as higher expense or producing lower revenues as compared

to estimation.

Demerits:

In majority of situations, the variances are not visible in accounting reports, and due to

which accounting managers need to look over documents such as work routings,

inventory payments, and recorded overtime to ascertain the causes for these variances.

These add-on operation is cost-effective only when the management has been able to

effectively address issues based on the knowledge provided. On the other hands, this may

lead to higher consumption of cost along with time. As well as it is necessary for

managers to get information in less time so that they can prepare strategies to beat their

competitors but in variance analysis needed information is offered in more time.

Evaluation of variance as an operation is focused on annual statements, which are

published far longer after quarterly closure; there could be a time delay that might have

an effect on remedial action to a certain degree (Zandi, Khalid and Islam, 2019). In this

competitive environment, only those companies can sustain who prepare their strategies

and policies in less time with higher effectiveness. Due to higher reliability on variances,

there can be lot of delay in process of managing different kinds of activities and

operations. Basically, it is one of the main issue of this technique as companies cannot

bear lose due to delay in strategy formulation.

The another drawback of variance analysis is that under it, calculations are done in

accordance of standard data related to income and expenses. These standard data are

prepared on the basis of assumptions of managers. Due to this, the provided outcome

under each variance become less reliable and effective. As well as in each company, this

assumption of income and expenses is done in accordance of own knowledge and skills

of managers. As a result, it becomes difficult to make comparison between performance

of two companies by help of this method.

In addition to this, the variance analysis is not suitable for those companies which are

involved in service sector. It is so because of higher number of overheads as compared to

direct expenses. Eventually, the variances can be computed only if there is complete

information about various kinds of expenses. While in service organizations, there are

lack of data about direct expenses (Ahmad and Al-Shbiel, 2019). Due to these causes,

variance analysis is not suitable for small companies and for those that are involved in

service sector instead of product manufacturing.

So these are some merits and demerits of variance analysis which are faced by companies that

apply it as a performance measurement tool.

lead to higher consumption of cost along with time. As well as it is necessary for

managers to get information in less time so that they can prepare strategies to beat their

competitors but in variance analysis needed information is offered in more time.

Evaluation of variance as an operation is focused on annual statements, which are

published far longer after quarterly closure; there could be a time delay that might have

an effect on remedial action to a certain degree (Zandi, Khalid and Islam, 2019). In this

competitive environment, only those companies can sustain who prepare their strategies

and policies in less time with higher effectiveness. Due to higher reliability on variances,

there can be lot of delay in process of managing different kinds of activities and

operations. Basically, it is one of the main issue of this technique as companies cannot

bear lose due to delay in strategy formulation.

The another drawback of variance analysis is that under it, calculations are done in

accordance of standard data related to income and expenses. These standard data are

prepared on the basis of assumptions of managers. Due to this, the provided outcome

under each variance become less reliable and effective. As well as in each company, this

assumption of income and expenses is done in accordance of own knowledge and skills

of managers. As a result, it becomes difficult to make comparison between performance

of two companies by help of this method.

In addition to this, the variance analysis is not suitable for those companies which are

involved in service sector. It is so because of higher number of overheads as compared to

direct expenses. Eventually, the variances can be computed only if there is complete

information about various kinds of expenses. While in service organizations, there are

lack of data about direct expenses (Ahmad and Al-Shbiel, 2019). Due to these causes,

variance analysis is not suitable for small companies and for those that are involved in

service sector instead of product manufacturing.

So these are some merits and demerits of variance analysis which are faced by companies that

apply it as a performance measurement tool.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Part B

Make-or - buy decisions is a mechanism whereby an organization opts for in-house

manufacturing or the purchasing of a commodity (Łada, Kozarkiewicz and Haslam, 2020).

Make-or - buy judgments, also relates to a procurement process that aligns with benefits and

costs connected with making a quality output internally or choosing an external supplier for

product lines. In order to calculate costs accurately, a company must consider certain aspects

relevant to the procurement and processing of the goods over the production of products in-

house.

In the context of in house production, a business must include costs connected to the sourcing of

the manufactured product and the output costs. The related expenditures may include extra labor

needed to create the products, storage requirements, total storage costs, material cost and many

more. On the other hands the purchasing costs involved with the procurement of the product

from a supplier may include the price of the item itself, other distribution or production charges

and the local taxes applicable. Furthermore, spending relating to the managing of received items

and labor costs associated with obtaining items in stock is also included in the aspect of buying

goods from suppliers.

The case-study discussed on XLG company reflects on making-or-buy choices. In the respective

case-study situations, management wants to paint a make-or - buy decision regarding the fama Q.

It is a cleaning material for managing high quality in manufacturing of fama Q for company.

This item is protected by patent, and XLG company plans to manufacture it in-house. Business

imports fama Q from Brazil and it was expensive to import such items for the company because

of country-wide lock-downs decided by UK authorities and government. Importing this product

into the company has been expensive. It cannot be shipped by air but instead by ship transport

from the lock-down, which has increased the retail price of fama Q to 4.5 per product as well as

the previous price was 3.7 per item.

Despite of this complex situation, company now plans to produce fama Q in-house. The price of

an object is mainly a major element in decision taking or purchasing. For each unit the original

standard fama-Q price is 2.5 Pounds. The expense of making fama Q is 3 Pounds. The related

evidence given herein is that there will be a 15-day reduction in shipping period for in-house

production alternative.

Make-or - buy decisions is a mechanism whereby an organization opts for in-house

manufacturing or the purchasing of a commodity (Łada, Kozarkiewicz and Haslam, 2020).

Make-or - buy judgments, also relates to a procurement process that aligns with benefits and

costs connected with making a quality output internally or choosing an external supplier for

product lines. In order to calculate costs accurately, a company must consider certain aspects

relevant to the procurement and processing of the goods over the production of products in-

house.

In the context of in house production, a business must include costs connected to the sourcing of

the manufactured product and the output costs. The related expenditures may include extra labor

needed to create the products, storage requirements, total storage costs, material cost and many

more. On the other hands the purchasing costs involved with the procurement of the product

from a supplier may include the price of the item itself, other distribution or production charges

and the local taxes applicable. Furthermore, spending relating to the managing of received items

and labor costs associated with obtaining items in stock is also included in the aspect of buying

goods from suppliers.

The case-study discussed on XLG company reflects on making-or-buy choices. In the respective

case-study situations, management wants to paint a make-or - buy decision regarding the fama Q.

It is a cleaning material for managing high quality in manufacturing of fama Q for company.

This item is protected by patent, and XLG company plans to manufacture it in-house. Business

imports fama Q from Brazil and it was expensive to import such items for the company because

of country-wide lock-downs decided by UK authorities and government. Importing this product

into the company has been expensive. It cannot be shipped by air but instead by ship transport

from the lock-down, which has increased the retail price of fama Q to 4.5 per product as well as

the previous price was 3.7 per item.

Despite of this complex situation, company now plans to produce fama Q in-house. The price of

an object is mainly a major element in decision taking or purchasing. For each unit the original

standard fama-Q price is 2.5 Pounds. The expense of making fama Q is 3 Pounds. The related

evidence given herein is that there will be a 15-day reduction in shipping period for in-house

production alternative.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Analysis of Making Decision:

The table termed below shows the outcome of business decision of in-housing of the fama Q in

such manner:

If In-housing

production of

fama Q: Chemical X Chemical Y

Budgeted (595

units)

Actual (862.75

units)

Varian

ce

Budgeted (595

units)

Actual (862.75

units)

Varian

ce

Selling Price 45 26775 45

38823.

75

12048.

75 35 20825 37

31921.

75

11096.

75

Cost of

Chemicals 20 11900 20 17255 5355 10 5950 17

14666.

75

8716.7

5

Increase in

cost due to in-

house of

production of

Fama Q 0.5

431.37

5

431.37

5 - 0.5

431.37

5

431.37

5

Total Cost 20.5

12197.

5 21.2

17686.

375

5488.8

75 10 5950 17.5

15098.

125

9148.1

25

Profit Margin 24.5

14577.

5 23.8

21137.

375

6559.8

75 25 14875 19.5

16823.

625

1948.6

25

The table termed below shows the outcome of business decision of in-housing of the fama Q in

such manner:

If In-housing

production of

fama Q: Chemical X Chemical Y

Budgeted (595

units)

Actual (862.75

units)

Varian

ce

Budgeted (595

units)

Actual (862.75

units)

Varian

ce

Selling Price 45 26775 45

38823.

75

12048.

75 35 20825 37

31921.

75

11096.

75

Cost of

Chemicals 20 11900 20 17255 5355 10 5950 17

14666.

75

8716.7

5

Increase in

cost due to in-

house of

production of

Fama Q 0.5

431.37

5

431.37

5 - 0.5

431.37

5

431.37

5

Total Cost 20.5

12197.

5 21.2

17686.

375

5488.8

75 10 5950 17.5

15098.

125

9148.1

25

Profit Margin 24.5

14577.

5 23.8

21137.

375

6559.8

75 25 14875 19.5

16823.

625

1948.6

25

Working Note:

Computation of Demand(units) based on the new scenario: (Demand expected to be risen

by 45 percent)

Chemical X 595 units + 595 units *45% = 862.75

Chemical Y 595 units + 595 units * 45% = 862.75

By analyzing the decision to buy fama Q, it can be stated that profit rates would rise by about

6559.87 and 1948.62 respectively in the light of both chemical X and Y production.

Consequently, under all situations the real earnings will exceed the total sum of income

budgeted.

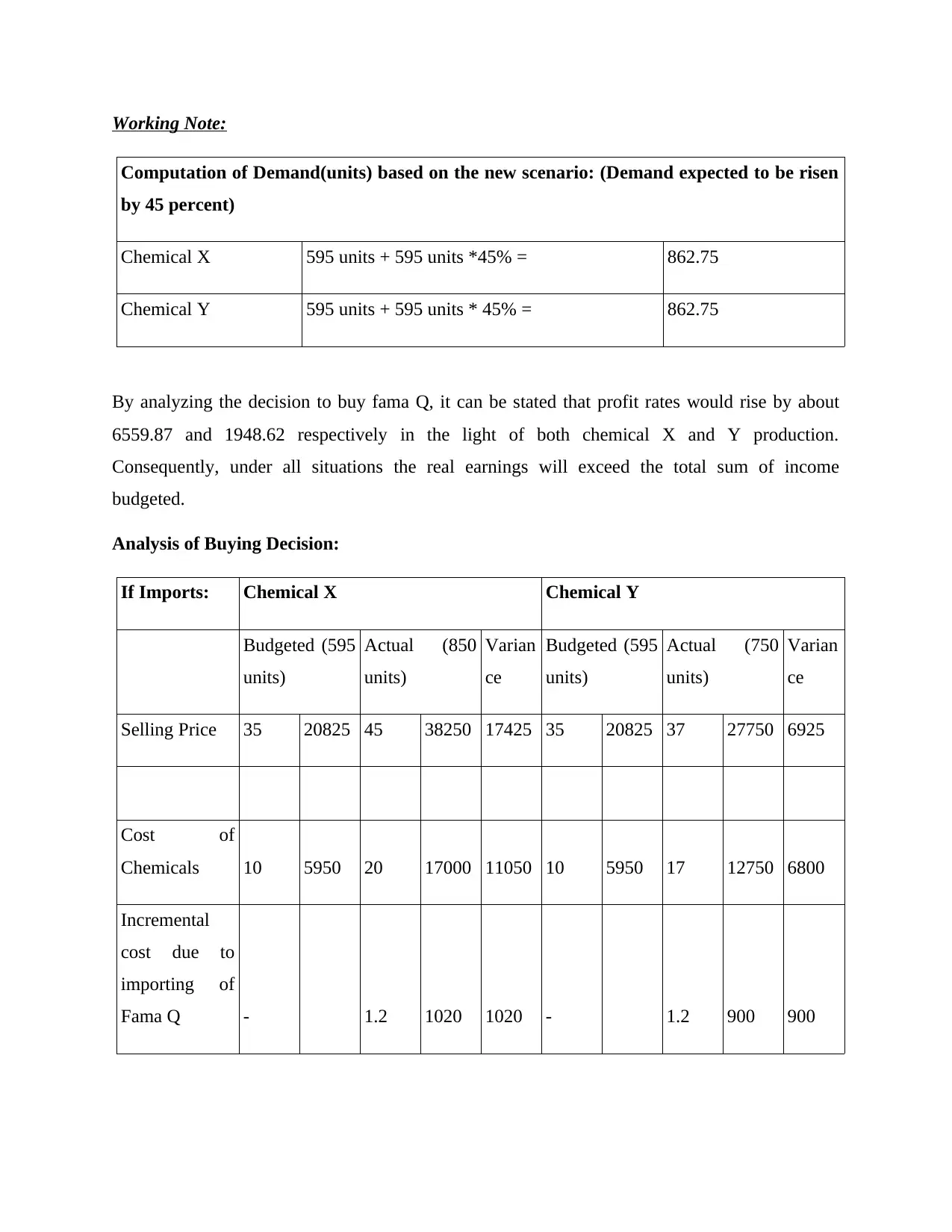

Analysis of Buying Decision:

If Imports: Chemical X Chemical Y

Budgeted (595

units)

Actual (850

units)

Varian

ce

Budgeted (595

units)

Actual (750

units)

Varian

ce

Selling Price 35 20825 45 38250 17425 35 20825 37 27750 6925

Cost of

Chemicals 10 5950 20 17000 11050 10 5950 17 12750 6800

Incremental

cost due to

importing of

Fama Q - 1.2 1020 1020 - 1.2 900 900

Computation of Demand(units) based on the new scenario: (Demand expected to be risen

by 45 percent)

Chemical X 595 units + 595 units *45% = 862.75

Chemical Y 595 units + 595 units * 45% = 862.75

By analyzing the decision to buy fama Q, it can be stated that profit rates would rise by about

6559.87 and 1948.62 respectively in the light of both chemical X and Y production.

Consequently, under all situations the real earnings will exceed the total sum of income

budgeted.

Analysis of Buying Decision:

If Imports: Chemical X Chemical Y

Budgeted (595

units)

Actual (850

units)

Varian

ce

Budgeted (595

units)

Actual (750

units)

Varian

ce

Selling Price 35 20825 45 38250 17425 35 20825 37 27750 6925

Cost of

Chemicals 10 5950 20 17000 11050 10 5950 17 12750 6800

Incremental

cost due to

importing of

Fama Q - 1.2 1020 1020 - 1.2 900 900

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.