Management Accounting: Systems, Reporting, Costing & Planning

VerifiedAdded on 2023/06/12

|20

|6530

|205

Report

AI Summary

This report delves into the realm of management accounting, examining various systems and methods employed by companies like XYZ Ltd for effective decision-making and financial control. It covers different types of management accounting systems, including costing accountancy, pricing management, and stock administration, along with methods for preparing accounting reports such as stock control, budgeting, efficiency, and accounts receivable reports. The report further analyzes costing techniques like marginal costing and absorption costing, highlighting their characteristics and impact on profitability. Additionally, it explores the advantages and disadvantages of various planning tools and their application in preparing and forecasting budgets. The study emphasizes how organizations adapt management accounting systems to address financial challenges and achieve sustainable success. This document, shared on Desklib, aims to provide students with valuable insights into the practical application of management accounting principles and techniques.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1. Different types of systems of management accounting and their application..................3

P2. Methods for preparing accounting reports.......................................................................4

M1. Benefits of systems with their applicability....................................................................5

TASK 2............................................................................................................................................7

P3. Calculation of cost with distinct costing techniques........................................................7

M2. Diverse management accounting techniques................................................................10

D2. Financial reports that accurately apply and interpret data.............................................10

Task 3.............................................................................................................................................11

P4 Advantages and disadvantages of different types of planning tools...............................11

M3 Use of planning tools and its application for preparing and forecasting budgets..........14

Task 4.............................................................................................................................................14

P5 Organizations are adopting management accounting system to respond financial problems

..............................................................................................................................................14

M4 Management accounting can lead to sustainable success..............................................17

D3 Planning tools for accounting respond by solving financial problems...........................17

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................19

Contents...........................................................................................................................................2

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1. Different types of systems of management accounting and their application..................3

P2. Methods for preparing accounting reports.......................................................................4

M1. Benefits of systems with their applicability....................................................................5

TASK 2............................................................................................................................................7

P3. Calculation of cost with distinct costing techniques........................................................7

M2. Diverse management accounting techniques................................................................10

D2. Financial reports that accurately apply and interpret data.............................................10

Task 3.............................................................................................................................................11

P4 Advantages and disadvantages of different types of planning tools...............................11

M3 Use of planning tools and its application for preparing and forecasting budgets..........14

Task 4.............................................................................................................................................14

P5 Organizations are adopting management accounting system to respond financial problems

..............................................................................................................................................14

M4 Management accounting can lead to sustainable success..............................................17

D3 Planning tools for accounting respond by solving financial problems...........................17

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................19

INTRODUCTION

Managerial bookkeeping is a method of gathering, evaluating, and tracking operating costs

and process in order for executives to make effective decisions (Altukhov, Predeus and Predeus,

2019). It is critical for a firm to concentrate on all corporate data and keep it in an efficient way

so that choices could be made quickly. Management accounting is also called as managerial

accounting it can be define as the process of giving finance related details and funds to the

managers for taking decision. Management accounting is only done by the internal group of the

company and this was the only that makes it separate from financial accounting. In this stage

financial details and projects such as invoice , financial balance sheet is shared by

finance(Altukhov, P. V., Predeus, N. V. and Predeus, J. V., 2019). department with the

management group of the business. Goal of management accounting is to use statics data and on

the basis of that data company take better and accurate decisions also control the business,

organization development and activities of the company. From the below report it discussed

about the various types and methods of management accounting, calculation of cost analysis and

prepare income statement, merits and demerits of various planning tools with the use of

budgetary control and organizing and adapting management accounting with respond to financial

barriers. This research is predicated on XYZ Ltd, a fashion retailer with a diverse range of

products. It employs managerial accountancy to make long-term business choices.

TASK 1

P1. Different types of systems of management accounting and their application

Managerial accountancy is concerned with measures that are linked to financial

information that is applied to generate business choices. This is utilised by executives of every

firm who effectively gather, evaluate, and oversee accounting transactions in order to sustain

prosperity. Executives at the XYZ Ltd business employ a variety of managerial accountancy

techniques that can aid in the analysis of the firm's earnings as well as its current financial status.

Beneath, we'll go over all of the main types of managerial accountancy processes:

Management use the costing accountancy method to examine expenses associated with

operational and company processes in order to increase competitiveness. It does have a

crucial necessity of identifying and eliminating superfluous costs whilst making items.

Managerial bookkeeping is a method of gathering, evaluating, and tracking operating costs

and process in order for executives to make effective decisions (Altukhov, Predeus and Predeus,

2019). It is critical for a firm to concentrate on all corporate data and keep it in an efficient way

so that choices could be made quickly. Management accounting is also called as managerial

accounting it can be define as the process of giving finance related details and funds to the

managers for taking decision. Management accounting is only done by the internal group of the

company and this was the only that makes it separate from financial accounting. In this stage

financial details and projects such as invoice , financial balance sheet is shared by

finance(Altukhov, P. V., Predeus, N. V. and Predeus, J. V., 2019). department with the

management group of the business. Goal of management accounting is to use statics data and on

the basis of that data company take better and accurate decisions also control the business,

organization development and activities of the company. From the below report it discussed

about the various types and methods of management accounting, calculation of cost analysis and

prepare income statement, merits and demerits of various planning tools with the use of

budgetary control and organizing and adapting management accounting with respond to financial

barriers. This research is predicated on XYZ Ltd, a fashion retailer with a diverse range of

products. It employs managerial accountancy to make long-term business choices.

TASK 1

P1. Different types of systems of management accounting and their application

Managerial accountancy is concerned with measures that are linked to financial

information that is applied to generate business choices. This is utilised by executives of every

firm who effectively gather, evaluate, and oversee accounting transactions in order to sustain

prosperity. Executives at the XYZ Ltd business employ a variety of managerial accountancy

techniques that can aid in the analysis of the firm's earnings as well as its current financial status.

Beneath, we'll go over all of the main types of managerial accountancy processes:

Management use the costing accountancy method to examine expenses associated with

operational and company processes in order to increase competitiveness. It does have a

crucial necessity of identifying and eliminating superfluous costs whilst making items.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management at XYZ Ltd use it to keep track of real expenses and basic materials used in

the company's fashion operations (Arroyo, 2012).

Pricing management method is also known as quantitative evaluation, this framework is

being utilized by businesses in various industries to evaluate how consumer response in

able to establish various prices for goods and activities. With the use of it, XYZ Ltd's

accounting adjusted the pricing of as well as other basic materials in order to entice

clients and achieve protracted objectives such as increased revenues, increased industry

proportion, and so forth.(Arroyo, 2012).

Stock administration systems is a framework keeps control of the supplies which are kept

in warehouses and factories. It is a necessary criterion since it aids in the management of

all inventories by defining which materials are in inventory and which are missing. XYZ

Ltd's management keeps track of every materials using application which enables him to

understand when a specific supply is available.

o FIFO: This strategy means that an organisation sells the things that were purchased

initially.

o LIFO: This concept means that an organisation sells things that were lately acquired

foremost, resulting in a gain.

o AVCO: According to this strategy, a company sells commodities at the mean price of

company commodities and concepts.

Another specific method is the job pricing method, which is utilized to monitor costs and

earnings by task in attempt to maximise work efficiency. XYZ Ltd's management

allocates costs to certain jobs, which aids in tracking spending and making selections in

addition to properly conduct corporate activities (Borthick and Pennington, 2017).

P2. Methods for preparing accounting reports

Managerial accountancy statements are studies created by executives that include strategy,

rules, productivity measurement, and judgement call company operations. It aids in the

management of all financial and non-financial recordings, as well as their conversion into

relevant knowledge for the organisation. XYZ Ltd's supervisor creates financial statements

which aid in making better-informed strategic choices. There seem to be a variety of techniques

for reporting managerial accountancy statistics that are detailed below:

the company's fashion operations (Arroyo, 2012).

Pricing management method is also known as quantitative evaluation, this framework is

being utilized by businesses in various industries to evaluate how consumer response in

able to establish various prices for goods and activities. With the use of it, XYZ Ltd's

accounting adjusted the pricing of as well as other basic materials in order to entice

clients and achieve protracted objectives such as increased revenues, increased industry

proportion, and so forth.(Arroyo, 2012).

Stock administration systems is a framework keeps control of the supplies which are kept

in warehouses and factories. It is a necessary criterion since it aids in the management of

all inventories by defining which materials are in inventory and which are missing. XYZ

Ltd's management keeps track of every materials using application which enables him to

understand when a specific supply is available.

o FIFO: This strategy means that an organisation sells the things that were purchased

initially.

o LIFO: This concept means that an organisation sells things that were lately acquired

foremost, resulting in a gain.

o AVCO: According to this strategy, a company sells commodities at the mean price of

company commodities and concepts.

Another specific method is the job pricing method, which is utilized to monitor costs and

earnings by task in attempt to maximise work efficiency. XYZ Ltd's management

allocates costs to certain jobs, which aids in tracking spending and making selections in

addition to properly conduct corporate activities (Borthick and Pennington, 2017).

P2. Methods for preparing accounting reports

Managerial accountancy statements are studies created by executives that include strategy,

rules, productivity measurement, and judgement call company operations. It aids in the

management of all financial and non-financial recordings, as well as their conversion into

relevant knowledge for the organisation. XYZ Ltd's supervisor creates financial statements

which aid in making better-informed strategic choices. There seem to be a variety of techniques

for reporting managerial accountancy statistics that are detailed below:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Stock control reports: An inventories administration reporting is a document that is

utilized to collect statistics regarding inventories or completed items. For example, the

administrator of XYZ Ltd prepares a stock control analysis in order to learn regarding the basic

materials that are utilized. It aids in stock management and ensures that stock is adequately

tracked by management.(Borthick, . and Pennington, 2017).

Budgeting report: This is a crucial record which determines a company's fiscal

performance. Budgeting analysis is a commercial company's information document which

organizations utilize to contrast development and planning to functional prototypes in attempt to

boost profitability. It aids in the creation of the budgeted amount by factoring in all expenditures

and income. Executives at XYZ Ltd establish an operating cost for apparel and compared it to

the real cost to determine how much extra the company decides to invest (Chathurangani and

Madhusanka, 2019).

Reporting on efficiency: Management create this analysis to evaluate the overall success

of the organisation as well as the success of every individual. It encourages workers to do well

by rewarding individuals for their efforts. XYZ Ltd's management prepares a summary sheet by

evaluating commercial activity and making crucial strategy selections for the company's growth.

Report on accounts receivable: Because each firm depends on creditworthiness, it's

critical that they produce an accounts receivables statement. This document aids in the

management of borrower details and also the repayment schedule, which specifies when

borrowers would reimburse the outstanding quantity. This analysis breaks apart the outstanding

amount into individual durations, allowing leaders to assess evaders and discuss problems that

need to be addressed during the data gathering. XYZ Ltd, for example, is a fashion shop that

produces clothing and sells it straight to stakeholders and clients on loan and money.

(Chathurangani,. and Madhusanka, , 2019.).

M1. Benefits of systems with their applicability

Managerial accountancy methods benefit organisations in the following ways:

Systems Advantages and applications

Stock control mechanism This method helps all businesses keep control of their stock

and arrange orders appropriately. This is used by XYZ Ltd's

management to keep track of input materials excess and

utilized to collect statistics regarding inventories or completed items. For example, the

administrator of XYZ Ltd prepares a stock control analysis in order to learn regarding the basic

materials that are utilized. It aids in stock management and ensures that stock is adequately

tracked by management.(Borthick, . and Pennington, 2017).

Budgeting report: This is a crucial record which determines a company's fiscal

performance. Budgeting analysis is a commercial company's information document which

organizations utilize to contrast development and planning to functional prototypes in attempt to

boost profitability. It aids in the creation of the budgeted amount by factoring in all expenditures

and income. Executives at XYZ Ltd establish an operating cost for apparel and compared it to

the real cost to determine how much extra the company decides to invest (Chathurangani and

Madhusanka, 2019).

Reporting on efficiency: Management create this analysis to evaluate the overall success

of the organisation as well as the success of every individual. It encourages workers to do well

by rewarding individuals for their efforts. XYZ Ltd's management prepares a summary sheet by

evaluating commercial activity and making crucial strategy selections for the company's growth.

Report on accounts receivable: Because each firm depends on creditworthiness, it's

critical that they produce an accounts receivables statement. This document aids in the

management of borrower details and also the repayment schedule, which specifies when

borrowers would reimburse the outstanding quantity. This analysis breaks apart the outstanding

amount into individual durations, allowing leaders to assess evaders and discuss problems that

need to be addressed during the data gathering. XYZ Ltd, for example, is a fashion shop that

produces clothing and sells it straight to stakeholders and clients on loan and money.

(Chathurangani,. and Madhusanka, , 2019.).

M1. Benefits of systems with their applicability

Managerial accountancy methods benefit organisations in the following ways:

Systems Advantages and applications

Stock control mechanism This method helps all businesses keep control of their stock

and arrange orders appropriately. This is used by XYZ Ltd's

management to keep track of input materials excess and

undervaluation (Cleve, 2017).

Method of costing framework This solution allows you to monitor costs and increase the

effectiveness of your company by keeping costs low.

Management at XYZ Ltd use it to aid them in lowering input

costs, maintaining supply quality, and expanding

manufacturing.

Mechanism for calculating

prices

It is advantageous for pricing items and solutions in a way

which motivates buyers to buy them. As the director of XYZ

Ltd, you determine the pricing in order to entice buyers to

shop through your company.(Cleve,, 2017).

Mechanism for calculating job

costs

This method provides a broad array of advantages to a

business, including the ability to assess income made on

actual tasks and assisting managers in allocating costs to

available positions. Its use is stated as XYZ Ltd's management

dividing costs into individual departments in the

manufacturing operation, allowing them to perform more

efficiently.

Organizational operations such as profitability and growth are connected with the

managerial accountancy framework and monitoring. The accountancy technology is being

utilized to evaluate and monitor productivity, while statistics are utilised to keep track of all

activities. XYZ Ltd, for example, uses a supplies control platform to keep monitor of existing

inventories and create inventories statistics so that orders can be placed properly. The pricing

optimizing technology assists XYZ Ltd in determining the pricing of as well as other basic

materials, as well as preparing financial statement for comparison with real expenditures. XYZ

Ltd can use a price accountancy platform and a work pricing database to keep track of all

expenditures and individual jobs in addition to stay profitable. As a result, financial activities and

reporting are linked with organisational processes, allowing all systems and data to assist gain

sustainable competitive advantage (Curtis and Taylor, 2018).

Method of costing framework This solution allows you to monitor costs and increase the

effectiveness of your company by keeping costs low.

Management at XYZ Ltd use it to aid them in lowering input

costs, maintaining supply quality, and expanding

manufacturing.

Mechanism for calculating

prices

It is advantageous for pricing items and solutions in a way

which motivates buyers to buy them. As the director of XYZ

Ltd, you determine the pricing in order to entice buyers to

shop through your company.(Cleve,, 2017).

Mechanism for calculating job

costs

This method provides a broad array of advantages to a

business, including the ability to assess income made on

actual tasks and assisting managers in allocating costs to

available positions. Its use is stated as XYZ Ltd's management

dividing costs into individual departments in the

manufacturing operation, allowing them to perform more

efficiently.

Organizational operations such as profitability and growth are connected with the

managerial accountancy framework and monitoring. The accountancy technology is being

utilized to evaluate and monitor productivity, while statistics are utilised to keep track of all

activities. XYZ Ltd, for example, uses a supplies control platform to keep monitor of existing

inventories and create inventories statistics so that orders can be placed properly. The pricing

optimizing technology assists XYZ Ltd in determining the pricing of as well as other basic

materials, as well as preparing financial statement for comparison with real expenditures. XYZ

Ltd can use a price accountancy platform and a work pricing database to keep track of all

expenditures and individual jobs in addition to stay profitable. As a result, financial activities and

reporting are linked with organisational processes, allowing all systems and data to assist gain

sustainable competitive advantage (Curtis and Taylor, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 2

P3. Calculation of cost with distinct costing techniques

Cost: It refers to the amount of cash required to develop or buy something, as well as the

profit made from the selling of such items. To put it differently, expenditure is basically a

measure of the worth of the effort, currency, time and goods, obligations, and other things that

should be expended in the execution of different business processes. Supplies, people, operating

expenditures, and other charges connected with production methods are included in those

expenses. During this whole instance, the organisation had several methods for calculating

operating earnings. Nasty Gal Vintage is a production company, thus this should assess the costs

of numerous marketing endeavours in order to achieve great fiscal efficiency and durability

profitability (Emiaso and Egbunike, 2018). It tells administrators to cut wastage as substantially

as feasible in order to enhance profits. The two more common costing methods are marginal

costing and absorption costing. It's also covered in the parts below:

The term "marginal costing" refers to a method of determining overall effectiveness

which only takes indirect costs into account. This method is beneficial whenever an

institution generates one extra item of output in contrast to the initial output. Based on

number of goods created, it may boost or decrease the total production cost. Staff and

commodities costs, and also a percentage of the predicted fixed price, make up marginal

expenditure, also known as adjustable price.

Characteristics of marginal costing:

1. categorization of fixed and variable cost: cost are divided into fixed and variable cost

. In fixed cost it will not be changed its fixed in every year and in variable it will be

changed it can be changed in every year.

2. Inventory valuation: In this point company valued finished goods and work in

progress in this company can only considered variable cost. In inventory valuation

selling and distribution overheads are not considered.

3. Price fixing: In this point company determined the price with the help of marginal

cost and contribution .

4. Profitability: determination of department and products profits is depend on the

contribution.

P3. Calculation of cost with distinct costing techniques

Cost: It refers to the amount of cash required to develop or buy something, as well as the

profit made from the selling of such items. To put it differently, expenditure is basically a

measure of the worth of the effort, currency, time and goods, obligations, and other things that

should be expended in the execution of different business processes. Supplies, people, operating

expenditures, and other charges connected with production methods are included in those

expenses. During this whole instance, the organisation had several methods for calculating

operating earnings. Nasty Gal Vintage is a production company, thus this should assess the costs

of numerous marketing endeavours in order to achieve great fiscal efficiency and durability

profitability (Emiaso and Egbunike, 2018). It tells administrators to cut wastage as substantially

as feasible in order to enhance profits. The two more common costing methods are marginal

costing and absorption costing. It's also covered in the parts below:

The term "marginal costing" refers to a method of determining overall effectiveness

which only takes indirect costs into account. This method is beneficial whenever an

institution generates one extra item of output in contrast to the initial output. Based on

number of goods created, it may boost or decrease the total production cost. Staff and

commodities costs, and also a percentage of the predicted fixed price, make up marginal

expenditure, also known as adjustable price.

Characteristics of marginal costing:

1. categorization of fixed and variable cost: cost are divided into fixed and variable cost

. In fixed cost it will not be changed its fixed in every year and in variable it will be

changed it can be changed in every year.

2. Inventory valuation: In this point company valued finished goods and work in

progress in this company can only considered variable cost. In inventory valuation

selling and distribution overheads are not considered.

3. Price fixing: In this point company determined the price with the help of marginal

cost and contribution .

4. Profitability: determination of department and products profits is depend on the

contribution.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Features of marginal cost:

1. Get to know the effect of variable cost and cost of production to find with the help

of marginal costing

2. Get to know the selling price its necessary to add variable cost and profit of the

year to contribution.

3. It's a support of valuation of stock of finished goods and work in progress.

4. Costs are divided into two costs one is variable and another is fixed costs. Semi –

fixed costs are also changed into either fixed cost or as variable costs.

Another important accountancy technique is absorption costing, which takes into

consideration all types of costs, both variable and fixed, which have an effect on earnings

revenue. It takes both variable and temporary inflation into consideration while

computing operating earnings. Operating costs, for example, include the cost of

personnel, the cost of basic products, and the cost of administration. Because of the

presence of fixed expenses, the company's operating earnings decreases, rendering it less

attractive among most enterprises.

Characteristics of absorption costing:

1. direct and indirect costs: In this type of costs absorption costing includes both the

costs in direct costs its equally go with the stage of production means its directly into

the production of the company and indirect cost not change with the stage of

production.

2. Identification of direct costs: In this point direct costs directly into the product that is

direct labour and direct material. So, its easy to find direct cost in the product its

clearly shown into the product.

3. Indirect costs are occupied: In this point indirect cost are absorbed. This is the main

reason for the use of absorption rate because it cant be directly find and identified

into the product.

4. Appropriate absorption rate: In this point indirect cost or overhead are occupied by

the use of suitable absorption rate.

1. Get to know the effect of variable cost and cost of production to find with the help

of marginal costing

2. Get to know the selling price its necessary to add variable cost and profit of the

year to contribution.

3. It's a support of valuation of stock of finished goods and work in progress.

4. Costs are divided into two costs one is variable and another is fixed costs. Semi –

fixed costs are also changed into either fixed cost or as variable costs.

Another important accountancy technique is absorption costing, which takes into

consideration all types of costs, both variable and fixed, which have an effect on earnings

revenue. It takes both variable and temporary inflation into consideration while

computing operating earnings. Operating costs, for example, include the cost of

personnel, the cost of basic products, and the cost of administration. Because of the

presence of fixed expenses, the company's operating earnings decreases, rendering it less

attractive among most enterprises.

Characteristics of absorption costing:

1. direct and indirect costs: In this type of costs absorption costing includes both the

costs in direct costs its equally go with the stage of production means its directly into

the production of the company and indirect cost not change with the stage of

production.

2. Identification of direct costs: In this point direct costs directly into the product that is

direct labour and direct material. So, its easy to find direct cost in the product its

clearly shown into the product.

3. Indirect costs are occupied: In this point indirect cost are absorbed. This is the main

reason for the use of absorption rate because it cant be directly find and identified

into the product.

4. Appropriate absorption rate: In this point indirect cost or overhead are occupied by

the use of suitable absorption rate.

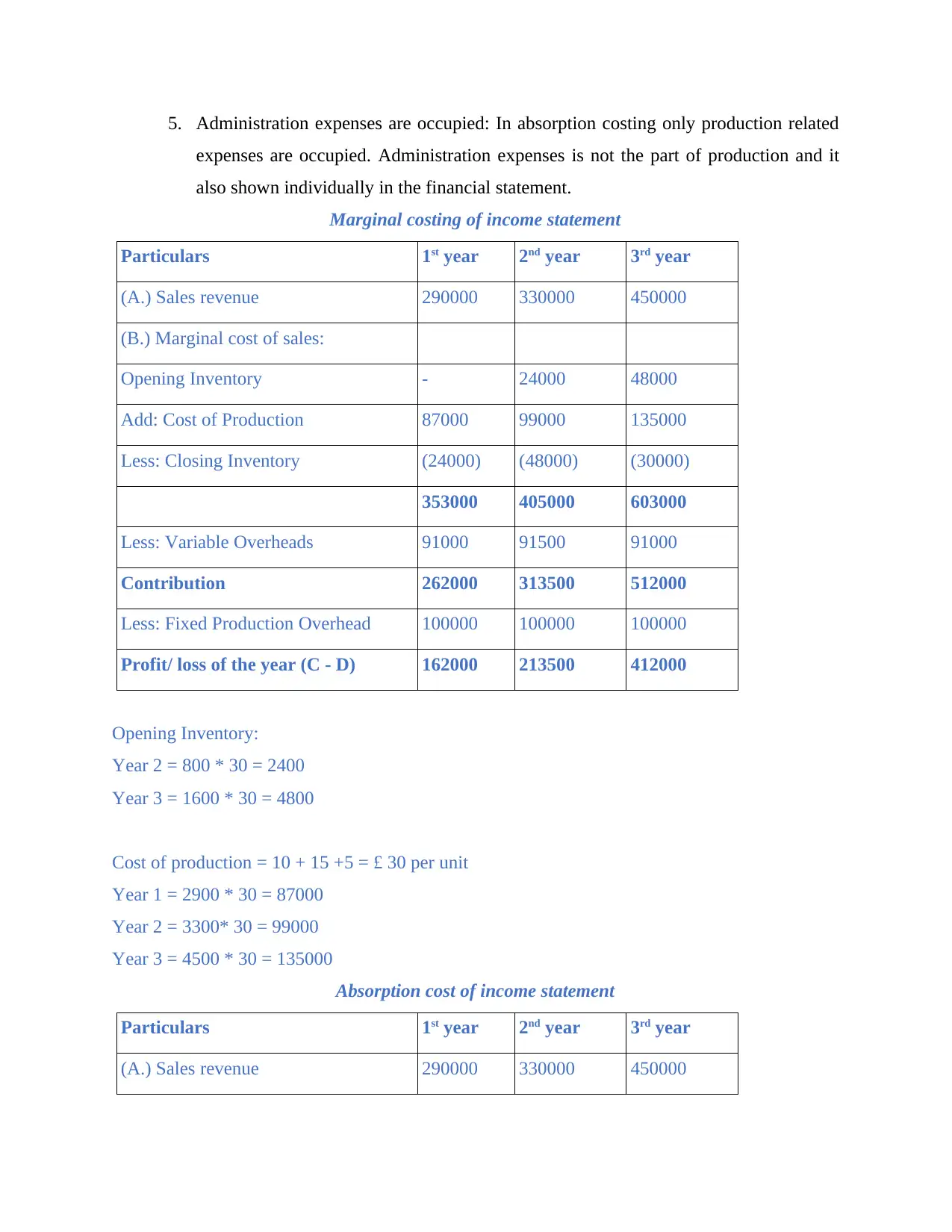

5. Administration expenses are occupied: In absorption costing only production related

expenses are occupied. Administration expenses is not the part of production and it

also shown individually in the financial statement.

Marginal costing of income statement

Particulars 1st year 2nd year 3rd year

(A.) Sales revenue 290000 330000 450000

(B.) Marginal cost of sales:

Opening Inventory - 24000 48000

Add: Cost of Production 87000 99000 135000

Less: Closing Inventory (24000) (48000) (30000)

353000 405000 603000

Less: Variable Overheads 91000 91500 91000

Contribution 262000 313500 512000

Less: Fixed Production Overhead 100000 100000 100000

Profit/ loss of the year (C - D) 162000 213500 412000

Opening Inventory:

Year 2 = 800 * 30 = 2400

Year 3 = 1600 * 30 = 4800

Cost of production = 10 + 15 +5 = £ 30 per unit

Year 1 = 2900 * 30 = 87000

Year 2 = 3300* 30 = 99000

Year 3 = 4500 * 30 = 135000

Absorption cost of income statement

Particulars 1st year 2nd year 3rd year

(A.) Sales revenue 290000 330000 450000

expenses are occupied. Administration expenses is not the part of production and it

also shown individually in the financial statement.

Marginal costing of income statement

Particulars 1st year 2nd year 3rd year

(A.) Sales revenue 290000 330000 450000

(B.) Marginal cost of sales:

Opening Inventory - 24000 48000

Add: Cost of Production 87000 99000 135000

Less: Closing Inventory (24000) (48000) (30000)

353000 405000 603000

Less: Variable Overheads 91000 91500 91000

Contribution 262000 313500 512000

Less: Fixed Production Overhead 100000 100000 100000

Profit/ loss of the year (C - D) 162000 213500 412000

Opening Inventory:

Year 2 = 800 * 30 = 2400

Year 3 = 1600 * 30 = 4800

Cost of production = 10 + 15 +5 = £ 30 per unit

Year 1 = 2900 * 30 = 87000

Year 2 = 3300* 30 = 99000

Year 3 = 4500 * 30 = 135000

Absorption cost of income statement

Particulars 1st year 2nd year 3rd year

(A.) Sales revenue 290000 330000 450000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

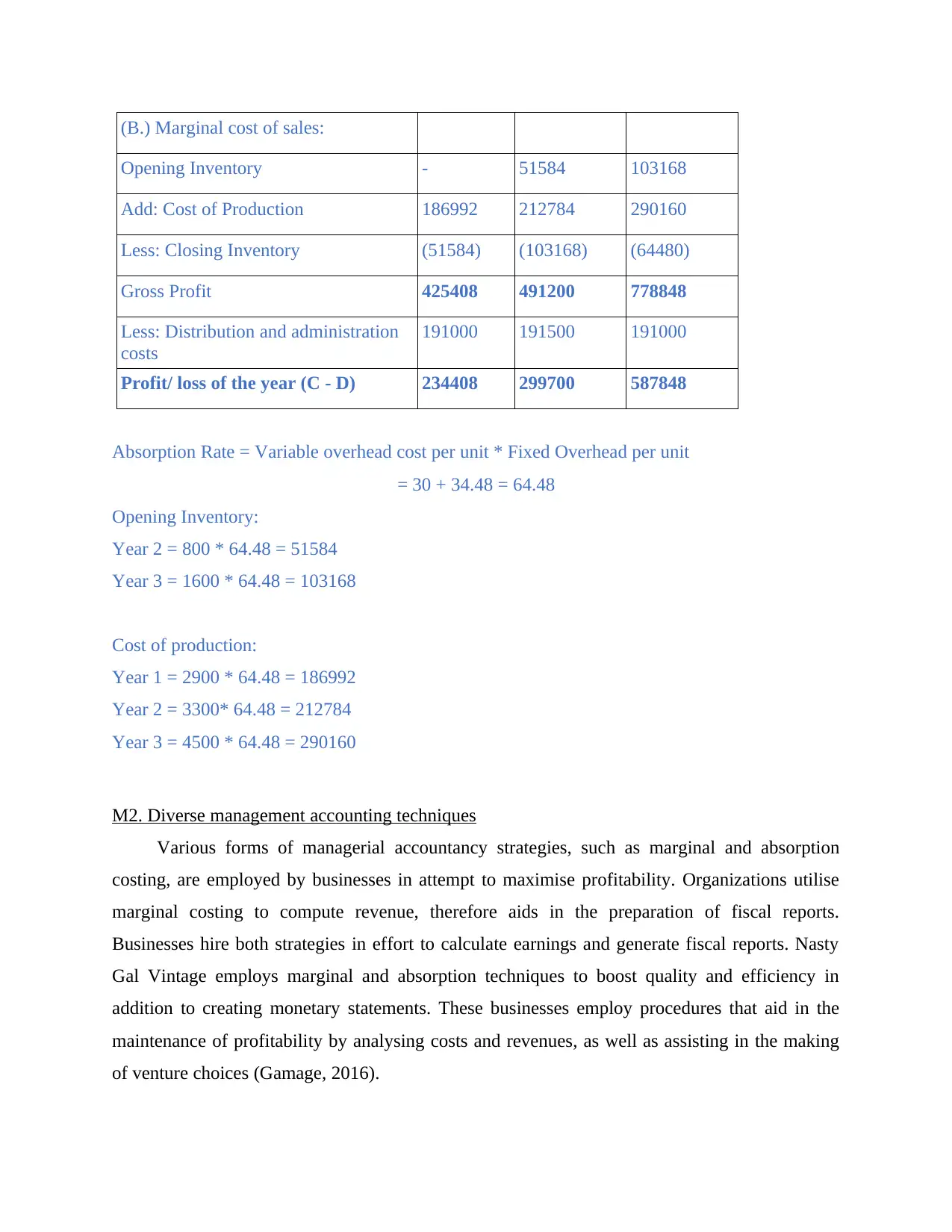

(B.) Marginal cost of sales:

Opening Inventory - 51584 103168

Add: Cost of Production 186992 212784 290160

Less: Closing Inventory (51584) (103168) (64480)

Gross Profit 425408 491200 778848

Less: Distribution and administration

costs

191000 191500 191000

Profit/ loss of the year (C - D) 234408 299700 587848

Absorption Rate = Variable overhead cost per unit * Fixed Overhead per unit

= 30 + 34.48 = 64.48

Opening Inventory:

Year 2 = 800 * 64.48 = 51584

Year 3 = 1600 * 64.48 = 103168

Cost of production:

Year 1 = 2900 * 64.48 = 186992

Year 2 = 3300* 64.48 = 212784

Year 3 = 4500 * 64.48 = 290160

M2. Diverse management accounting techniques

Various forms of managerial accountancy strategies, such as marginal and absorption

costing, are employed by businesses in attempt to maximise profitability. Organizations utilise

marginal costing to compute revenue, therefore aids in the preparation of fiscal reports.

Businesses hire both strategies in effort to calculate earnings and generate fiscal reports. Nasty

Gal Vintage employs marginal and absorption techniques to boost quality and efficiency in

addition to creating monetary statements. These businesses employ procedures that aid in the

maintenance of profitability by analysing costs and revenues, as well as assisting in the making

of venture choices (Gamage, 2016).

Opening Inventory - 51584 103168

Add: Cost of Production 186992 212784 290160

Less: Closing Inventory (51584) (103168) (64480)

Gross Profit 425408 491200 778848

Less: Distribution and administration

costs

191000 191500 191000

Profit/ loss of the year (C - D) 234408 299700 587848

Absorption Rate = Variable overhead cost per unit * Fixed Overhead per unit

= 30 + 34.48 = 64.48

Opening Inventory:

Year 2 = 800 * 64.48 = 51584

Year 3 = 1600 * 64.48 = 103168

Cost of production:

Year 1 = 2900 * 64.48 = 186992

Year 2 = 3300* 64.48 = 212784

Year 3 = 4500 * 64.48 = 290160

M2. Diverse management accounting techniques

Various forms of managerial accountancy strategies, such as marginal and absorption

costing, are employed by businesses in attempt to maximise profitability. Organizations utilise

marginal costing to compute revenue, therefore aids in the preparation of fiscal reports.

Businesses hire both strategies in effort to calculate earnings and generate fiscal reports. Nasty

Gal Vintage employs marginal and absorption techniques to boost quality and efficiency in

addition to creating monetary statements. These businesses employ procedures that aid in the

maintenance of profitability by analysing costs and revenues, as well as assisting in the making

of venture choices (Gamage, 2016).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

D2. Financial reports that accurately apply and interpret data

Finance statements are critical for any market because they assist in understanding a

corporation's monetary status and making commercial strategies. Management generate this

analysis to show income and expenses when operating a company. It uses both marginal and

absorption costing strategies to assist preserve profitability over time. Nasty Gal Vintage

produces a variety of goods and solutions in order to increase earnings.

Task 3

P4 Advantages and disadvantages of different types of planning tools

Budget- A plan is a detailed document that represents fiscal projections of costs and

revenues for a specified duration. In attempt to make a gain, XYZ Ltd's management prepares a

strategy based on the previous year's expenditure In other words budget can be define as its use

to predict the financial outcomes and a financial position of the business for a future period of

time. Its basically use for the plan and performance estimation purpose it can involve spend in

fixed assets, trained employees knowledge and skills, establishment of bonus plans and for

controlling operations.

Advantage of budgeting:

It helps to make plan: In this point its help the company to make plan for the

formation of budget so, that it easier for the company to spend money according to

the budget.

Budget communicate and helps in coordinating: It helps to maintain a discipline in

the organization and ensure that all department perform their task for achieving the

objectives.

It assist the company to take decision: Budget helps the firm to make planning as well

as taking decisions regarding the problem create while performing the function of

budget.

Budget utilize to direct an control: Its most important part of budget it helps the

organization to monitor and compare the actual performance.

It use to instigate and control: Budget involve motivational factor also it provide the

supervisor and other employees predetermined objectives.

Disadvantages of budgeting:

Finance statements are critical for any market because they assist in understanding a

corporation's monetary status and making commercial strategies. Management generate this

analysis to show income and expenses when operating a company. It uses both marginal and

absorption costing strategies to assist preserve profitability over time. Nasty Gal Vintage

produces a variety of goods and solutions in order to increase earnings.

Task 3

P4 Advantages and disadvantages of different types of planning tools

Budget- A plan is a detailed document that represents fiscal projections of costs and

revenues for a specified duration. In attempt to make a gain, XYZ Ltd's management prepares a

strategy based on the previous year's expenditure In other words budget can be define as its use

to predict the financial outcomes and a financial position of the business for a future period of

time. Its basically use for the plan and performance estimation purpose it can involve spend in

fixed assets, trained employees knowledge and skills, establishment of bonus plans and for

controlling operations.

Advantage of budgeting:

It helps to make plan: In this point its help the company to make plan for the

formation of budget so, that it easier for the company to spend money according to

the budget.

Budget communicate and helps in coordinating: It helps to maintain a discipline in

the organization and ensure that all department perform their task for achieving the

objectives.

It assist the company to take decision: Budget helps the firm to make planning as well

as taking decisions regarding the problem create while performing the function of

budget.

Budget utilize to direct an control: Its most important part of budget it helps the

organization to monitor and compare the actual performance.

It use to instigate and control: Budget involve motivational factor also it provide the

supervisor and other employees predetermined objectives.

Disadvantages of budgeting:

Increment in budget increase the expenses of budget: if a company try to change its

budget or include some additional machinery to purchase then the cost of budget also

increases.

Sometimes it shows imperfection in budget: In this point firm is highly based on the

budget and if any wrong information put across then it creates wrong efficiency in

budget.

Sometimes budget get demotivated: if employees in the organization not achieving

the target then it reduce the efficiency of employees and create demotivation factor on

them

Budget create disruption in department: if employees in the organization achieve

more that the targets then its create disruptions for the other department to handle.

It prepare at too low stage: if a business prepared budget at too low level then its not

provide any advantage to the company and its provide low output level with higher

cost.

Organizing budget

Budget carry an evaluated income statement for a future period of time. Complex budget

carry sales prediction, cost of goods sold and expenses necessary to help the projected

sales, evaluation of working capital requirements, purchases of fixed assets, prediction of

company cash flow and estimation of financial needs.

So, Much budgets are prepared in electronic spreadsheets, big businesses are in favour to

use specific software for the budgets which is more organized and less chances of

computation error.

XYZ Ltd's management employs a range of forecasting methods, as detailed below:

Variation assessment: There is a difference among an exact value and a projected

quantity; variability occurs whenever the allocated number varies from the real value.

Variation occurs whenever economic conditions fluctuate, if production is incorrectly

anticipated, and so forth. It is utilized by XYZ Ltd company to examine the differences

among real and budgeted statistics.

budget or include some additional machinery to purchase then the cost of budget also

increases.

Sometimes it shows imperfection in budget: In this point firm is highly based on the

budget and if any wrong information put across then it creates wrong efficiency in

budget.

Sometimes budget get demotivated: if employees in the organization not achieving

the target then it reduce the efficiency of employees and create demotivation factor on

them

Budget create disruption in department: if employees in the organization achieve

more that the targets then its create disruptions for the other department to handle.

It prepare at too low stage: if a business prepared budget at too low level then its not

provide any advantage to the company and its provide low output level with higher

cost.

Organizing budget

Budget carry an evaluated income statement for a future period of time. Complex budget

carry sales prediction, cost of goods sold and expenses necessary to help the projected

sales, evaluation of working capital requirements, purchases of fixed assets, prediction of

company cash flow and estimation of financial needs.

So, Much budgets are prepared in electronic spreadsheets, big businesses are in favour to

use specific software for the budgets which is more organized and less chances of

computation error.

XYZ Ltd's management employs a range of forecasting methods, as detailed below:

Variation assessment: There is a difference among an exact value and a projected

quantity; variability occurs whenever the allocated number varies from the real value.

Variation occurs whenever economic conditions fluctuate, if production is incorrectly

anticipated, and so forth. It is utilized by XYZ Ltd company to examine the differences

among real and budgeted statistics.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.