Detailed Management Accounting System Report for Zylla Company

VerifiedAdded on 2020/06/06

|17

|4695

|51

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles applied to Zylla Company. It delves into the role of management accounting in decision-making and achieving organizational goals. The report covers various aspects, including different costing methods like cost accounting, inventory management, price optimization, and job costing, highlighting their importance for financial control and profitability. It also explores management accounting reporting methods, such as profit and loss statements and performance reports, crucial for internal stakeholders. The report further evaluates the merits of using a management accounting system and offers a critical assessment of reporting systems. Additionally, it examines different planning tools used in budgetary control, evaluating their advantages and disadvantages and analyzing financial problems. Finally, the report includes a comparison of Zylla Company with other companies regarding their financial challenges and provides a conclusion and references.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

FROM: MANAGEMENT ACCOUNTING OFFICER..................................................................1

TO,...................................................................................................................................................1

GENERAL MANAGER..................................................................................................................1

ZYLLA COMPANY.......................................................................................................................1

SUB: MANAGEMENT ACCOUNTING SYSTEM .....................................................................1

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting and essential requirements of its different accounting system.....1

P2: Method of management account reporting...........................................................................3

M1: Merits of using management accounting system.................................................................5

D1: Critical evaluation of reporting system ...............................................................................5

TASK 2............................................................................................................................................5

P3: Various costing method using in management accounting..................................................6

M2: Evaluation of accounting tools............................................................................................7

D2: Critical evaluation of income statements.............................................................................8

TASK 3............................................................................................................................................8

P4. Advantages and Disadvantage of different type of planning tools used in budgetary

control.........................................................................................................................................8

M3: Evaluation of planning techniques....................................................................................10

D3: Critical analysis of financial problem................................................................................11

TASK4...........................................................................................................................................11

P5: Comparison with various company regarding its financial problem..................................11

M4: Analysis of financial problem...........................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

FROM: MANAGEMENT ACCOUNTING OFFICER..................................................................1

TO,...................................................................................................................................................1

GENERAL MANAGER..................................................................................................................1

ZYLLA COMPANY.......................................................................................................................1

SUB: MANAGEMENT ACCOUNTING SYSTEM .....................................................................1

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Management accounting and essential requirements of its different accounting system.....1

P2: Method of management account reporting...........................................................................3

M1: Merits of using management accounting system.................................................................5

D1: Critical evaluation of reporting system ...............................................................................5

TASK 2............................................................................................................................................5

P3: Various costing method using in management accounting..................................................6

M2: Evaluation of accounting tools............................................................................................7

D2: Critical evaluation of income statements.............................................................................8

TASK 3............................................................................................................................................8

P4. Advantages and Disadvantage of different type of planning tools used in budgetary

control.........................................................................................................................................8

M3: Evaluation of planning techniques....................................................................................10

D3: Critical analysis of financial problem................................................................................11

TASK4...........................................................................................................................................11

P5: Comparison with various company regarding its financial problem..................................11

M4: Analysis of financial problem...........................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FROM: MANAGEMENT ACCOUNTING OFFICER

TO,

GENERAL MANAGER

ZYLLA COMPANY

SUB: MANAGEMENT ACCOUNTING SYSTEM

INTRODUCTION

Management accounting plays an important role in controlling and monitoring

accounting records and information which help managers in making an effective decision and

plans. Thus it is required in every organisation irrespective of the size whether small or large. As

every organisation need to identify their actual financial position through which they can

compete with their rivals. Therefore management accounting provides them relevant financial

records and statements which help them in forecasting the project activities in proper manner that

will bring positive result to company (Albelda, 2011).

The main purpose of this project reports is to provide the roles and importance of

management accounting in achieving desired goals and objectives. The project covers different

costing methods which help company in analysing the actual profitability of company.

Budgetary control techniques are also explained under this project which help in resolving

financial issues of company and achieve profitability. It also covers management accounting

system and reports which help in identifying the actual financial position of company. Company

named “ Zylla” is chosen for the purpose of preparing this report.

TASK 1

P1. Management accounting and essential requirements of its different accounting system

Management Accounting Practices Committee (MAPC) defines Management

accounting as “ the process of identifying, measuring, analysis, interpreting and communicating

financial information which is used by manager to formulate an effective business decision.

Institute of Management Accountants (IMA) defines MA as “ It is a profession that

involves partnering in management decision making, control and monitoring the financial

records and information in order to formulate an effective plans and strategies.

1

TO,

GENERAL MANAGER

ZYLLA COMPANY

SUB: MANAGEMENT ACCOUNTING SYSTEM

INTRODUCTION

Management accounting plays an important role in controlling and monitoring

accounting records and information which help managers in making an effective decision and

plans. Thus it is required in every organisation irrespective of the size whether small or large. As

every organisation need to identify their actual financial position through which they can

compete with their rivals. Therefore management accounting provides them relevant financial

records and statements which help them in forecasting the project activities in proper manner that

will bring positive result to company (Albelda, 2011).

The main purpose of this project reports is to provide the roles and importance of

management accounting in achieving desired goals and objectives. The project covers different

costing methods which help company in analysing the actual profitability of company.

Budgetary control techniques are also explained under this project which help in resolving

financial issues of company and achieve profitability. It also covers management accounting

system and reports which help in identifying the actual financial position of company. Company

named “ Zylla” is chosen for the purpose of preparing this report.

TASK 1

P1. Management accounting and essential requirements of its different accounting system

Management Accounting Practices Committee (MAPC) defines Management

accounting as “ the process of identifying, measuring, analysis, interpreting and communicating

financial information which is used by manager to formulate an effective business decision.

Institute of Management Accountants (IMA) defines MA as “ It is a profession that

involves partnering in management decision making, control and monitoring the financial

records and information in order to formulate an effective plans and strategies.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management accounting: It refers to managing and monitoring the accounting and

financial recorded which help in making an effective decisions in order to achieve desired goals

and objectives of company. Through management accounting, Zylla can able to operate its

business operation in an effective way that will help them in increasing their financial position.

The accounting manager is held responsible to implement suitable management

accounting techniques which help them in dealing with uncertainty condition which directly

helps in improving their profitability situation (Advanced Management Accounting, 2017). The

manager need to guide and direct its employees to perform in such a way that will help in

meeting the desired result. In order to achieve growth ans success the manager of Zylla should

always keep their eyes on implementing new and advanced technology which helps in bringing

efficiency in their work and performance. If due to certain circumstances such as lack of

financial resources, lack of skilled employees etc. The company fails to implement changes in

existing technology then it will bring negative impact on their sustainability and profitability

(Arroyo, 2012).

Therefore the manager of Zylla need to implement various accounting systems through

which they can operate business functions and activities. Such accounting systems are as

follows:

Cost accounting system: This system is useful in determining the actual cost which will

be incurred in the production process. The main objective of adopting this system is to allocation

of cost on the basis of outcomes they received in near future. Thus the managers of Zylla should

focus on adopting such technique through which they can eliminate irrelevant cost and utilise

money in profitable manner. Through this they can ascertain net profitability, cost control and

other various factors which influences production and operational activities. For example the

product manager may use various cost such as normal, actual and standard price in order to

analyse expenses incurred in manufacturing process (Bennett, Schaltegger and Zvezdov, 2013).

Inventory management system: Through adopting this technique, the manager can able

to reduce the total cost of inventories with a motive of generating high return. Thus it is the

responsibility of manager of Zylla to carefully analyse the stock available and accordingly order

raw material which help them in avoiding the shortage situation. Ordering right quantity at right

time at right place will help company in meeting the demands of the targeted customers. It also

help in reduce the inventory storage cost through which they can able to provide product to

2

financial recorded which help in making an effective decisions in order to achieve desired goals

and objectives of company. Through management accounting, Zylla can able to operate its

business operation in an effective way that will help them in increasing their financial position.

The accounting manager is held responsible to implement suitable management

accounting techniques which help them in dealing with uncertainty condition which directly

helps in improving their profitability situation (Advanced Management Accounting, 2017). The

manager need to guide and direct its employees to perform in such a way that will help in

meeting the desired result. In order to achieve growth ans success the manager of Zylla should

always keep their eyes on implementing new and advanced technology which helps in bringing

efficiency in their work and performance. If due to certain circumstances such as lack of

financial resources, lack of skilled employees etc. The company fails to implement changes in

existing technology then it will bring negative impact on their sustainability and profitability

(Arroyo, 2012).

Therefore the manager of Zylla need to implement various accounting systems through

which they can operate business functions and activities. Such accounting systems are as

follows:

Cost accounting system: This system is useful in determining the actual cost which will

be incurred in the production process. The main objective of adopting this system is to allocation

of cost on the basis of outcomes they received in near future. Thus the managers of Zylla should

focus on adopting such technique through which they can eliminate irrelevant cost and utilise

money in profitable manner. Through this they can ascertain net profitability, cost control and

other various factors which influences production and operational activities. For example the

product manager may use various cost such as normal, actual and standard price in order to

analyse expenses incurred in manufacturing process (Bennett, Schaltegger and Zvezdov, 2013).

Inventory management system: Through adopting this technique, the manager can able

to reduce the total cost of inventories with a motive of generating high return. Thus it is the

responsibility of manager of Zylla to carefully analyse the stock available and accordingly order

raw material which help them in avoiding the shortage situation. Ordering right quantity at right

time at right place will help company in meeting the demands of the targeted customers. It also

help in reduce the inventory storage cost through which they can able to provide product to

2

customers at less prices. Therefore the manager of Zylla need to focus on managing and

monitoring inventory on regular basis so as to know the accurate position of stock through using

ABC costing and Stock turnover ratios.

Price optimisation system: This system play an important role in fixing the prices of

product that will satisfy the customer's expectations. Therefore the manager need to first properly

analyse the demand of their product and accordingly made changes in prices in order to get huge

profitability as well as attain loyal customers. After considering all expenses incurred in

production and other business functions, the manager should decide the price of their products

which help them in recovering their actual cost and also maximises the level of satisfaction of

customers towards the prices the charged.

Job costing system: This method can be used when the products the company

manufactures are relatively different from each other. It is essentially required for manager to

record job cost for each and every items and accordingly allocate direct material and direct

labour to each and every job which brings efficiency in each item.

P2: Method of management account reporting

In every business organisation, management accounting is entirely different form final

accounting in which managers use to formulate reports for Zylla company's internal

stakeholders. Reports are one of the crucial aspects for the company which is used for the

purpose of recording various financial transaction on regular basis. The data recorded in it is

gather from various sources such as operational, financial and investing activities. There are

different reports those are been prepared by account managers. Such as profit and loss statement

which is one of the most crucial managerial reports prepare during the year (Bodie, 2013).

This will be provide more specific and reliable information about companies to total

income and revenue they are getting in an accounting year. Accounts officers and managers

generally use to write and develop income reports so that valuable decisions can be made

properly. This will be considered in order to identify total gross profits generated by the

company during the month as well as in a year. This monthly reports are use by managers in

order to inform supervisors about current projects performance. By the help of this, management

would use to track accountability and keep ensure that proper results would be attain with proper

utilisation of resources.

3

monitoring inventory on regular basis so as to know the accurate position of stock through using

ABC costing and Stock turnover ratios.

Price optimisation system: This system play an important role in fixing the prices of

product that will satisfy the customer's expectations. Therefore the manager need to first properly

analyse the demand of their product and accordingly made changes in prices in order to get huge

profitability as well as attain loyal customers. After considering all expenses incurred in

production and other business functions, the manager should decide the price of their products

which help them in recovering their actual cost and also maximises the level of satisfaction of

customers towards the prices the charged.

Job costing system: This method can be used when the products the company

manufactures are relatively different from each other. It is essentially required for manager to

record job cost for each and every items and accordingly allocate direct material and direct

labour to each and every job which brings efficiency in each item.

P2: Method of management account reporting

In every business organisation, management accounting is entirely different form final

accounting in which managers use to formulate reports for Zylla company's internal

stakeholders. Reports are one of the crucial aspects for the company which is used for the

purpose of recording various financial transaction on regular basis. The data recorded in it is

gather from various sources such as operational, financial and investing activities. There are

different reports those are been prepared by account managers. Such as profit and loss statement

which is one of the most crucial managerial reports prepare during the year (Bodie, 2013).

This will be provide more specific and reliable information about companies to total

income and revenue they are getting in an accounting year. Accounts officers and managers

generally use to write and develop income reports so that valuable decisions can be made

properly. This will be considered in order to identify total gross profits generated by the

company during the month as well as in a year. This monthly reports are use by managers in

order to inform supervisors about current projects performance. By the help of this, management

would use to track accountability and keep ensure that proper results would be attain with proper

utilisation of resources.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Reporting to management is a kind of systematic process of delivering data at various

level of the department in order to enable proper analysis of ongoing projects. If any things

required to be change then by using corrective tools this will be remove before completed the

task. Reporting is very complex, multiple stage activity that take place in accordance with other

business processes that provide crucial information about future profitability of an organisation.

The reports are more useful for Zylla company for future planning. This will be essentially

required to be implemented by managers in order to take corrective action for increasing

productivity of Zylla Ltd. In other way of reporting is operated at internal level (Boyns and

Edwards, 2013).

“Reporting in management is an organised techniques of delivering every manager with

all information only those data that is require crucial for future decision making”.

Objectives: A report is mainly an effective mode of upward communication. These are

more crucial for the purpose of making vital decision regarding formulation of any business

function. Some of the other aspects are related with the legal needs of the company. Managers

use to prepare annual reports which is to be effectively helpful during the time of audit.

Importance:

Provide valuable information: Reports are essential for delivering corrective

information to every possible level. Such as trend of business, fund flow and total amount

of cash they are getting during an accounting year.

Helps in selection process: There are plenty of information presented by the managers.

Out of which only relevant data in taken into consideration in an account.

Types of reporting system:

Performance report: This particular report is use to determine exact position of the

company. This can be analyse by using data from past and current year. It is necessary activity in

accounting. It consists of various collection of information such as utilisation of resources, future

progress and current status of company's stakeholders.

Account receivable aging report: This specific report is considered as complete list of

unpaid customers detail and unused credit memos through data ranges. This happens to be the

primary tools which is used for the purpose of collecting personnel to analyse which invoice is

overdue for commerce. There are certain causes in account receivable which is varies with

4

level of the department in order to enable proper analysis of ongoing projects. If any things

required to be change then by using corrective tools this will be remove before completed the

task. Reporting is very complex, multiple stage activity that take place in accordance with other

business processes that provide crucial information about future profitability of an organisation.

The reports are more useful for Zylla company for future planning. This will be essentially

required to be implemented by managers in order to take corrective action for increasing

productivity of Zylla Ltd. In other way of reporting is operated at internal level (Boyns and

Edwards, 2013).

“Reporting in management is an organised techniques of delivering every manager with

all information only those data that is require crucial for future decision making”.

Objectives: A report is mainly an effective mode of upward communication. These are

more crucial for the purpose of making vital decision regarding formulation of any business

function. Some of the other aspects are related with the legal needs of the company. Managers

use to prepare annual reports which is to be effectively helpful during the time of audit.

Importance:

Provide valuable information: Reports are essential for delivering corrective

information to every possible level. Such as trend of business, fund flow and total amount

of cash they are getting during an accounting year.

Helps in selection process: There are plenty of information presented by the managers.

Out of which only relevant data in taken into consideration in an account.

Types of reporting system:

Performance report: This particular report is use to determine exact position of the

company. This can be analyse by using data from past and current year. It is necessary activity in

accounting. It consists of various collection of information such as utilisation of resources, future

progress and current status of company's stakeholders.

Account receivable aging report: This specific report is considered as complete list of

unpaid customers detail and unused credit memos through data ranges. This happens to be the

primary tools which is used for the purpose of collecting personnel to analyse which invoice is

overdue for commerce. There are certain causes in account receivable which is varies with

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

increase and decrease in total cash owed by its clients. This will consists of balance sheet, bills

receivable etc.

Job cost report: This types of reports is mainly assigning to the costs which is incur for

a particular job in which owners and its business is associated with. This will be analyse by

recording, classifying and evaluating different alternatives aspects use for the purpose of

controlling costs.

Inventory management report: This is one of the main report that every business

managers uses to prepare. By the help of this, opening and closing stock details can be identified

during the time. There are various tools and techniques which is used from the purpose of

making proper of record of inventories such as EOQ, ABC costing and inventory turnover ratio.

The Zylla company can use this as primary tool to keep balance in their stock.

Operational budget report: The Zylla Business can implement various techniques in

order to estimate total income and expenses they are incurring during the production of each

units. This will summaries with sales, production and other curial budgets. In order to get more

effective results they need to prepare reports on a regular basis so the chances of getting more

effective results can be increased (DRURY, 2013).

M1: Merits of using management accounting system

Management accounting system has various benefits such as:

It helps company in reducing operational expenses through using management

accounting information.

It helps manager to make an effective business decision with the help of quantitative

analysis for various decision opportunities.

It also help in increasing financial returns of company through forecasting the customer's

demand and sales of products.

D1: Critical evaluation of reporting system

In case of Zylla company, each staffs and department is operating its roles and

responsibility in an effective manner. The use of accounting reporting techniques is an essential

aspects that can helpful in incur better results for the company. Reports are helpful for the

purpose of making crucial decision-making for future planning.

5

receivable etc.

Job cost report: This types of reports is mainly assigning to the costs which is incur for

a particular job in which owners and its business is associated with. This will be analyse by

recording, classifying and evaluating different alternatives aspects use for the purpose of

controlling costs.

Inventory management report: This is one of the main report that every business

managers uses to prepare. By the help of this, opening and closing stock details can be identified

during the time. There are various tools and techniques which is used from the purpose of

making proper of record of inventories such as EOQ, ABC costing and inventory turnover ratio.

The Zylla company can use this as primary tool to keep balance in their stock.

Operational budget report: The Zylla Business can implement various techniques in

order to estimate total income and expenses they are incurring during the production of each

units. This will summaries with sales, production and other curial budgets. In order to get more

effective results they need to prepare reports on a regular basis so the chances of getting more

effective results can be increased (DRURY, 2013).

M1: Merits of using management accounting system

Management accounting system has various benefits such as:

It helps company in reducing operational expenses through using management

accounting information.

It helps manager to make an effective business decision with the help of quantitative

analysis for various decision opportunities.

It also help in increasing financial returns of company through forecasting the customer's

demand and sales of products.

D1: Critical evaluation of reporting system

In case of Zylla company, each staffs and department is operating its roles and

responsibility in an effective manner. The use of accounting reporting techniques is an essential

aspects that can helpful in incur better results for the company. Reports are helpful for the

purpose of making crucial decision-making for future planning.

5

TASK 2

P3: Various costing method using in management accounting

Cost is an amount which has to be paid in order to acquire something. In any business,

cost is mainly related with monetary evaluation of total material, labour, resources and workers

involve in delivery of products or services. It is a value of money which has been used up to

manufacture or deliver some specific products and services. A costing is the amount of

estimation which is forecasted by the managers for producing a product. This happens to be the

systematic process of identifying total cost of producing one units (Herzig and et. al. 2012).

It will provide perfect relationship among profit and capacity of a product. There are

various costing method those are directly or indirectly affecting the profitability of an

organisation. They consists of direct labour, material and other overhead costs those are

associated during the time of production. Some of them are discuss underneath:

Absorption costing: These are considers as all those costs which is related with the

production process. Those are absorbed by every units produced during the time. It

consists of both fixed or variable costs in order to get net profit during the year. It is

determine as full costing techniques.

Marginal costing: It is known as one of the effective costing method which is incur by

Zylla company for the production of one extra units. It will considered only variable costs

and fixed costs are ignore under this method. Hence, marginal cost involves prime costs

plus total variable overheads. In this, stocks values are much higher than using marginal

costing.

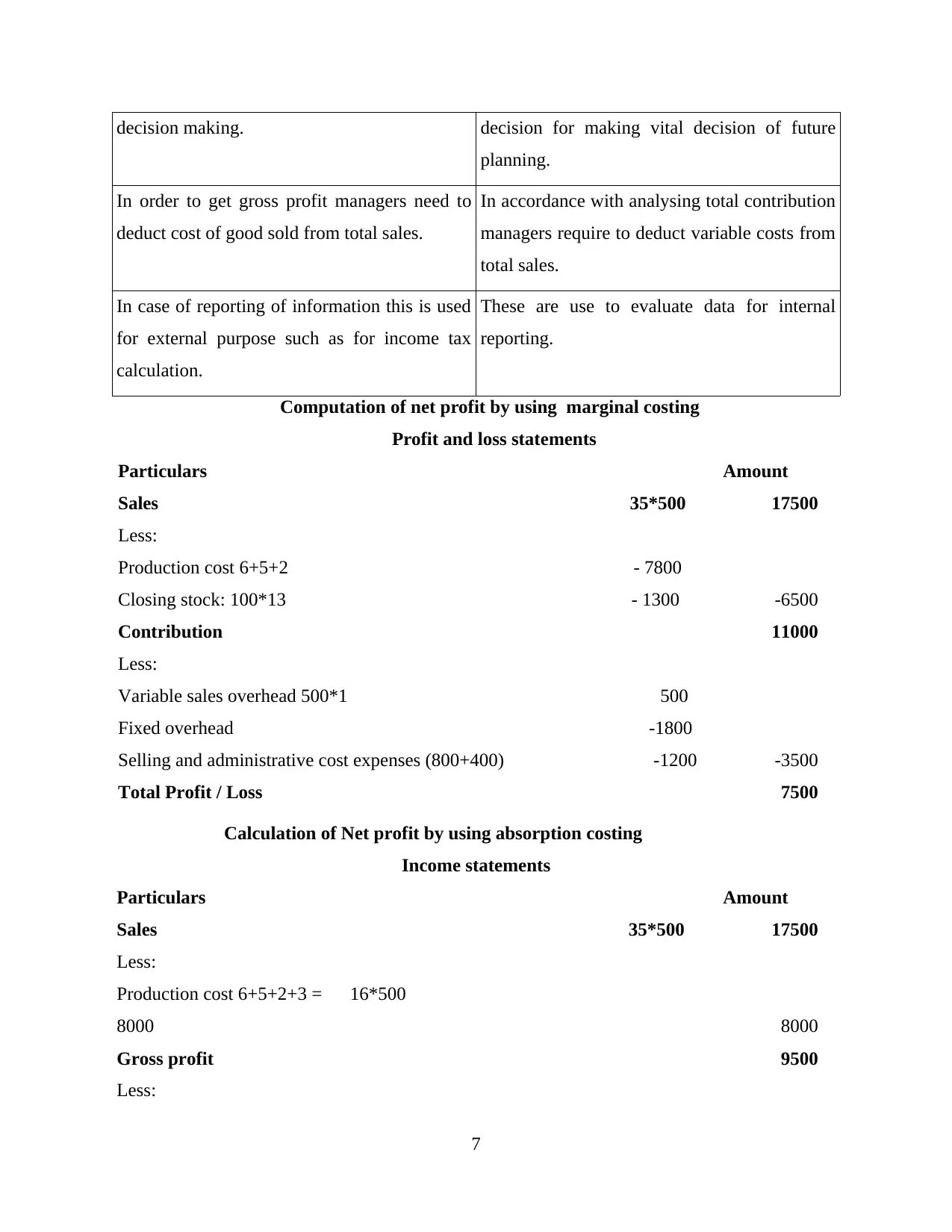

Absorption costing Marginal costing

Under this fixed costs are incur to the total cost

of production.

This will considers fixed costs as period costs.

These are identified through using P/v ratio.

All the costs information are marked as

conventional pattern.

Here, cost data is shown through total

contribution incur from each products.

Difference is determine because of the impacts

made on opening and closing stock.

They does not get affected.

It is not considered suitable for the purpose of Most of the managers uses to make valuable

6

P3: Various costing method using in management accounting

Cost is an amount which has to be paid in order to acquire something. In any business,

cost is mainly related with monetary evaluation of total material, labour, resources and workers

involve in delivery of products or services. It is a value of money which has been used up to

manufacture or deliver some specific products and services. A costing is the amount of

estimation which is forecasted by the managers for producing a product. This happens to be the

systematic process of identifying total cost of producing one units (Herzig and et. al. 2012).

It will provide perfect relationship among profit and capacity of a product. There are

various costing method those are directly or indirectly affecting the profitability of an

organisation. They consists of direct labour, material and other overhead costs those are

associated during the time of production. Some of them are discuss underneath:

Absorption costing: These are considers as all those costs which is related with the

production process. Those are absorbed by every units produced during the time. It

consists of both fixed or variable costs in order to get net profit during the year. It is

determine as full costing techniques.

Marginal costing: It is known as one of the effective costing method which is incur by

Zylla company for the production of one extra units. It will considered only variable costs

and fixed costs are ignore under this method. Hence, marginal cost involves prime costs

plus total variable overheads. In this, stocks values are much higher than using marginal

costing.

Absorption costing Marginal costing

Under this fixed costs are incur to the total cost

of production.

This will considers fixed costs as period costs.

These are identified through using P/v ratio.

All the costs information are marked as

conventional pattern.

Here, cost data is shown through total

contribution incur from each products.

Difference is determine because of the impacts

made on opening and closing stock.

They does not get affected.

It is not considered suitable for the purpose of Most of the managers uses to make valuable

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

decision making. decision for making vital decision of future

planning.

In order to get gross profit managers need to

deduct cost of good sold from total sales.

In accordance with analysing total contribution

managers require to deduct variable costs from

total sales.

In case of reporting of information this is used

for external purpose such as for income tax

calculation.

These are use to evaluate data for internal

reporting.

Computation of net profit by using marginal costing

Profit and loss statements

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2 - 7800

Closing stock: 100*13 - 1300 -6500

Contribution 11000

Less:

Variable sales overhead 500*1 500

Fixed overhead -1800

Selling and administrative cost expenses (800+400) -1200 -3500

Total Profit / Loss 7500

Calculation of Net profit by using absorption costing

Income statements

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2+3 = 16*500

8000 8000

Gross profit 9500

Less:

7

planning.

In order to get gross profit managers need to

deduct cost of good sold from total sales.

In accordance with analysing total contribution

managers require to deduct variable costs from

total sales.

In case of reporting of information this is used

for external purpose such as for income tax

calculation.

These are use to evaluate data for internal

reporting.

Computation of net profit by using marginal costing

Profit and loss statements

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2 - 7800

Closing stock: 100*13 - 1300 -6500

Contribution 11000

Less:

Variable sales overhead 500*1 500

Fixed overhead -1800

Selling and administrative cost expenses (800+400) -1200 -3500

Total Profit / Loss 7500

Calculation of Net profit by using absorption costing

Income statements

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2+3 = 16*500

8000 8000

Gross profit 9500

Less:

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

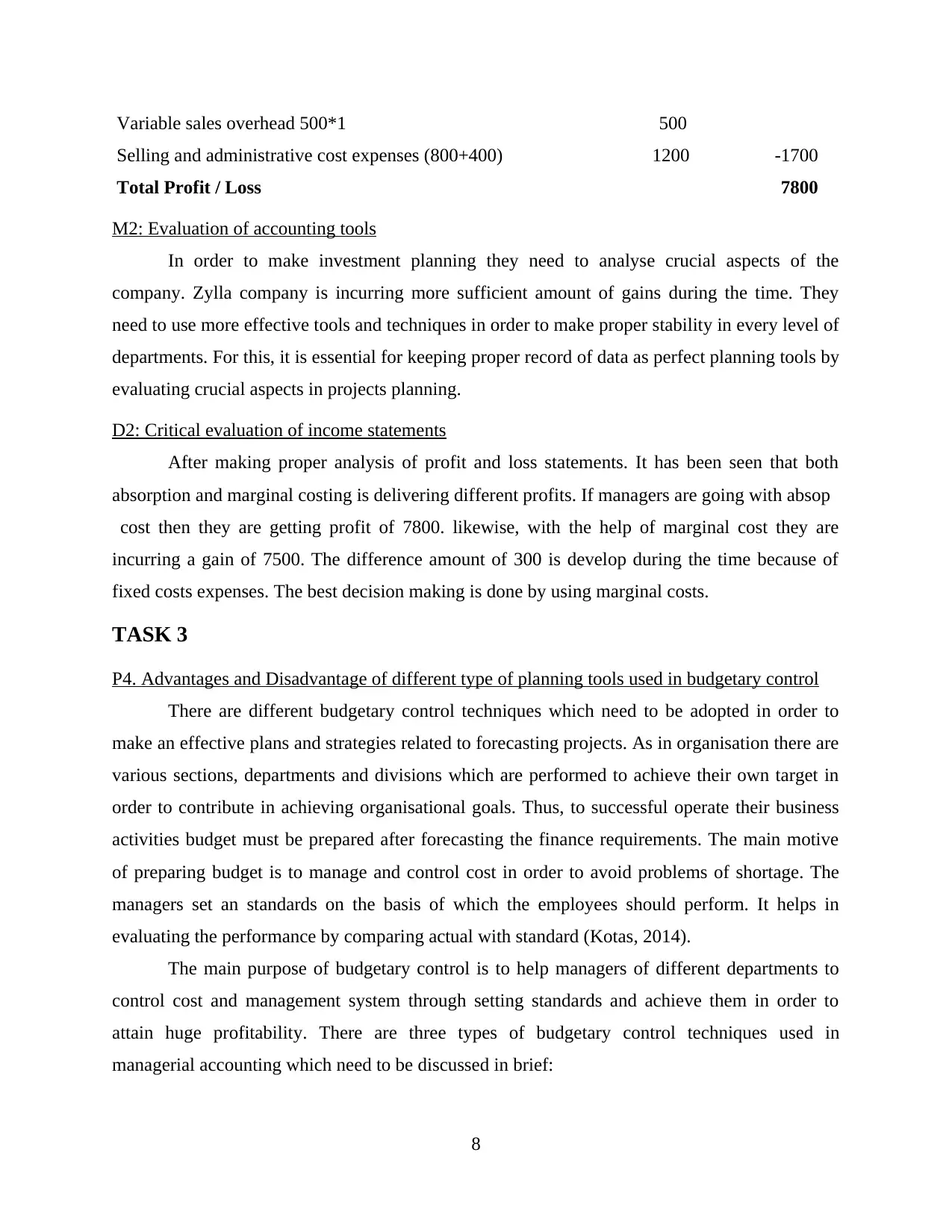

Variable sales overhead 500*1 500

Selling and administrative cost expenses (800+400) 1200 -1700

Total Profit / Loss 7800

M2: Evaluation of accounting tools

In order to make investment planning they need to analyse crucial aspects of the

company. Zylla company is incurring more sufficient amount of gains during the time. They

need to use more effective tools and techniques in order to make proper stability in every level of

departments. For this, it is essential for keeping proper record of data as perfect planning tools by

evaluating crucial aspects in projects planning.

D2: Critical evaluation of income statements

After making proper analysis of profit and loss statements. It has been seen that both

absorption and marginal costing is delivering different profits. If managers are going with absop

cost then they are getting profit of 7800. likewise, with the help of marginal cost they are

incurring a gain of 7500. The difference amount of 300 is develop during the time because of

fixed costs expenses. The best decision making is done by using marginal costs.

TASK 3

P4. Advantages and Disadvantage of different type of planning tools used in budgetary control

There are different budgetary control techniques which need to be adopted in order to

make an effective plans and strategies related to forecasting projects. As in organisation there are

various sections, departments and divisions which are performed to achieve their own target in

order to contribute in achieving organisational goals. Thus, to successful operate their business

activities budget must be prepared after forecasting the finance requirements. The main motive

of preparing budget is to manage and control cost in order to avoid problems of shortage. The

managers set an standards on the basis of which the employees should perform. It helps in

evaluating the performance by comparing actual with standard (Kotas, 2014).

The main purpose of budgetary control is to help managers of different departments to

control cost and management system through setting standards and achieve them in order to

attain huge profitability. There are three types of budgetary control techniques used in

managerial accounting which need to be discussed in brief:

8

Selling and administrative cost expenses (800+400) 1200 -1700

Total Profit / Loss 7800

M2: Evaluation of accounting tools

In order to make investment planning they need to analyse crucial aspects of the

company. Zylla company is incurring more sufficient amount of gains during the time. They

need to use more effective tools and techniques in order to make proper stability in every level of

departments. For this, it is essential for keeping proper record of data as perfect planning tools by

evaluating crucial aspects in projects planning.

D2: Critical evaluation of income statements

After making proper analysis of profit and loss statements. It has been seen that both

absorption and marginal costing is delivering different profits. If managers are going with absop

cost then they are getting profit of 7800. likewise, with the help of marginal cost they are

incurring a gain of 7500. The difference amount of 300 is develop during the time because of

fixed costs expenses. The best decision making is done by using marginal costs.

TASK 3

P4. Advantages and Disadvantage of different type of planning tools used in budgetary control

There are different budgetary control techniques which need to be adopted in order to

make an effective plans and strategies related to forecasting projects. As in organisation there are

various sections, departments and divisions which are performed to achieve their own target in

order to contribute in achieving organisational goals. Thus, to successful operate their business

activities budget must be prepared after forecasting the finance requirements. The main motive

of preparing budget is to manage and control cost in order to avoid problems of shortage. The

managers set an standards on the basis of which the employees should perform. It helps in

evaluating the performance by comparing actual with standard (Kotas, 2014).

The main purpose of budgetary control is to help managers of different departments to

control cost and management system through setting standards and achieve them in order to

attain huge profitability. There are three types of budgetary control techniques used in

managerial accounting which need to be discussed in brief:

8

1. Finance budget: Cash is an important and crucial sources which is used in daily operational

activities. Thus it is responsibility of manager to prepare an estimated requirements of cash in

near future. This will help company in executing business activities in an effective manner with

the help of utilizing available resources at an optimum manner (Lukka and Vinnari, 2014).

Cash Budget: It is prepared to analyse the cash requirements used in operating business

functions and departmental activities of an organisation. There are various sources which help in

making an effective cash budget and plans such as cash receipts, fund flow and cash flow

requirements. These cash budget shall be prepared on the basis of weekly, monthly and quarterly

basis. It helps in ensuring proper utilisation financial resources in an optimum manner that will

help in getting profitable result.

Capital expenditure budget: This budget is prepared with a motive of analysing the

capital requirements which are needed in order to operate their business activities in an effective

manner. Capital expenditure refers to expenditure incurred in acquiring assets such as new plant

and machinery, land and building etc. This budget is helpful as capital assets are essentially

required in operating every business activities.

Balance sheet budget: This budget is prepared with a motive of identifying overall

expenditures incurred and incomes generated during all business activities and accordingly

formulate a budget in order to find out the actual financial position of company in competitive

world.

2. Operating budgets:

Sales and revenue budget: These type of budget is helpful in analysing the estimated sales and

revenue generated in near future from their business activates.

Expense budget: This budget is prepared with a motive of controlling unnecessary cost

incurred while executing business operations. This budget directed the manager to allocate funds

in such areas of department where they get positive outcomes. Profit and loss accounts and

income statements are such sources which represents expenditures incurred in business

operations (Macintosh and Quattrone, 2010).

Project Budget: This budget is prepared with a motive of analysing the difference

between the sales and revenue and expensed incurred in whole project activities. If the profit is

generated more than expected then it extra can be used to recover the extra expenses incurred in

project activities.

9

activities. Thus it is responsibility of manager to prepare an estimated requirements of cash in

near future. This will help company in executing business activities in an effective manner with

the help of utilizing available resources at an optimum manner (Lukka and Vinnari, 2014).

Cash Budget: It is prepared to analyse the cash requirements used in operating business

functions and departmental activities of an organisation. There are various sources which help in

making an effective cash budget and plans such as cash receipts, fund flow and cash flow

requirements. These cash budget shall be prepared on the basis of weekly, monthly and quarterly

basis. It helps in ensuring proper utilisation financial resources in an optimum manner that will

help in getting profitable result.

Capital expenditure budget: This budget is prepared with a motive of analysing the

capital requirements which are needed in order to operate their business activities in an effective

manner. Capital expenditure refers to expenditure incurred in acquiring assets such as new plant

and machinery, land and building etc. This budget is helpful as capital assets are essentially

required in operating every business activities.

Balance sheet budget: This budget is prepared with a motive of identifying overall

expenditures incurred and incomes generated during all business activities and accordingly

formulate a budget in order to find out the actual financial position of company in competitive

world.

2. Operating budgets:

Sales and revenue budget: These type of budget is helpful in analysing the estimated sales and

revenue generated in near future from their business activates.

Expense budget: This budget is prepared with a motive of controlling unnecessary cost

incurred while executing business operations. This budget directed the manager to allocate funds

in such areas of department where they get positive outcomes. Profit and loss accounts and

income statements are such sources which represents expenditures incurred in business

operations (Macintosh and Quattrone, 2010).

Project Budget: This budget is prepared with a motive of analysing the difference

between the sales and revenue and expensed incurred in whole project activities. If the profit is

generated more than expected then it extra can be used to recover the extra expenses incurred in

project activities.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.