Management Accounting Report: Zylla, Financial Analysis and Strategies

VerifiedAdded on 2020/07/23

|19

|5588

|198

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices within Zylla, a small-scale business. It begins with an introduction to management accounting, its importance, and various system types, including price optimization and cost accounting. The report then explores different management accounting reporting systems, such as budget reports and performance reporting, highlighting their significance in business operations. The core of the report delves into costing methods, contrasting absorption and marginal costing, and their application in financial analysis. Furthermore, it examines the benefits and drawbacks of planning tools and techniques, and the adaptation of management accounting methods to address financial issues within the company. The report concludes with an overview of the findings, providing valuable insights into Zylla's financial management strategies.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Concept of Management accounting and various type of management accounting systems 1

P2 Various System used for management accounting reporting................................................3

M1 Merits of using management accounting approach..............................................................4

D1 Desegregation of management accounting systems and reporting.......................................5

TASK 2............................................................................................................................................5

P3 Compute cost using absorption and marginal costing...........................................................5

M2 Use of management accounting method...............................................................................9

D2 Financial reports that utilize for understand business activities............................................9

TASK 3............................................................................................................................................9

P4 Benefits and disadvantages of various kind of planning tools...............................................9

M3 Evaluation of planning techniques.....................................................................................11

D3 Planning tools or technique for respond financial issue......................................................11

TASK 4..........................................................................................................................................12

P5 Adaption of management accounting method to respond financial issue............................12

M4 Evaluation of financial problem.........................................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Concept of Management accounting and various type of management accounting systems 1

P2 Various System used for management accounting reporting................................................3

M1 Merits of using management accounting approach..............................................................4

D1 Desegregation of management accounting systems and reporting.......................................5

TASK 2............................................................................................................................................5

P3 Compute cost using absorption and marginal costing...........................................................5

M2 Use of management accounting method...............................................................................9

D2 Financial reports that utilize for understand business activities............................................9

TASK 3............................................................................................................................................9

P4 Benefits and disadvantages of various kind of planning tools...............................................9

M3 Evaluation of planning techniques.....................................................................................11

D3 Planning tools or technique for respond financial issue......................................................11

TASK 4..........................................................................................................................................12

P5 Adaption of management accounting method to respond financial issue............................12

M4 Evaluation of financial problem.........................................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is the analysis, communication and sourcing and use of decision

link to applicable financial and non-financial data to preserve and generate value for enterprise.

It is an effective techniques and processes that are emphasised on the proper use of business

resources in order to help administrators in their task or project of improving both shareholder

and customer value (Bebbington, Unerman and O'Dwyer, 2014). It is a system of collection and

demonstration of accurate economic information and data relating to an organisation for

monitoring, decision making and planning. This assignment is based on Zylla, it is a small scale

under which 50 employees are work together. This report also shown about management

accounting concepts and necessitate of various kind of accounting methods. Different types of

management accounting reporting and integration of company activity with the approach of

management accounting also determined in this study. Further, different approaches which an

enterprise use for measurement such as marginal and absorption costing is shown in this

assignment. Disadvantage and benefits of planning tool, and tools of management accounting

method also used in this project in order to decrees financial issues in the business entity.

TASK 1

P1 Concept of Management accounting and various type of management accounting systems

Management accounting: It is an essential process of accumulation, determination,

evaluation, analysis, interpretation, communication and preparation of information that supports

managers in certain decision creating within the structure of accomplishing the company goals

and objectives (What is management accounting system, 2018). According to American

Accounting Association; Management accounting consist of concepts and methods which are

necessary or essential for proper planning and selecting among alternative business activities for

control the evaluation of performances.

In Zylla, management accounting very important and necessary for the business entity to

mange their all financial and non-financial information systematically (Bennett and James,

2017). This system also useful and valuable for the organisation to accomplish their

predetermined goals and target in given time duration. There are some other importance of the

management accounting for the company to increase their sales and revenues, these are

determined as below:

1

Management accounting is the analysis, communication and sourcing and use of decision

link to applicable financial and non-financial data to preserve and generate value for enterprise.

It is an effective techniques and processes that are emphasised on the proper use of business

resources in order to help administrators in their task or project of improving both shareholder

and customer value (Bebbington, Unerman and O'Dwyer, 2014). It is a system of collection and

demonstration of accurate economic information and data relating to an organisation for

monitoring, decision making and planning. This assignment is based on Zylla, it is a small scale

under which 50 employees are work together. This report also shown about management

accounting concepts and necessitate of various kind of accounting methods. Different types of

management accounting reporting and integration of company activity with the approach of

management accounting also determined in this study. Further, different approaches which an

enterprise use for measurement such as marginal and absorption costing is shown in this

assignment. Disadvantage and benefits of planning tool, and tools of management accounting

method also used in this project in order to decrees financial issues in the business entity.

TASK 1

P1 Concept of Management accounting and various type of management accounting systems

Management accounting: It is an essential process of accumulation, determination,

evaluation, analysis, interpretation, communication and preparation of information that supports

managers in certain decision creating within the structure of accomplishing the company goals

and objectives (What is management accounting system, 2018). According to American

Accounting Association; Management accounting consist of concepts and methods which are

necessary or essential for proper planning and selecting among alternative business activities for

control the evaluation of performances.

In Zylla, management accounting very important and necessary for the business entity to

mange their all financial and non-financial information systematically (Bennett and James,

2017). This system also useful and valuable for the organisation to accomplish their

predetermined goals and target in given time duration. There are some other importance of the

management accounting for the company to increase their sales and revenues, these are

determined as below:

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Qualitative Data or information: For analysis all business activities and operations

effectively, manager of the company collect necessary information regarding company services

and products (Bovens, Goodin and Schillemans, 2014). It is essential for the enterprise to

increase their turnover and sales in limited duration. Management accounting assist in attain the

same and support in analysing the critical situation in easily.

Ongoing training or activities as well as data: It is essential for Zylla in order to

organise training activities for its workers so they can know and acquire regarding this approach.

Management accounting important for the company to handle daily basis activities and function

in an effective and efficient manner.

Give relevant information:Main benefits of this system is that it assists administrator in

gather and evaluate relevant data which support them in take appropriate judgement about

business operations and functions.

TYPES OF MANAGEMENT ACCOUNTING SYSTEM: There are some methods of

management accounting which are determined as below:

Price Optimisation System: It is a mathematical method which is use by each and every

organisation to evaluate how audience react to various prices or value of product (Brewer,

Sorensen and Stout, 2014). It is essential and beneficial tool for the Zylla and its administrator to

fix the accurate prices for the services and goods. It assist the business administrator to set

accurate cost of their products in a systematic manner. Therefore, company can easily attain their

desired and long term goals or objectives in allotted time period. Data which is use by

organisation for optimisation of price including historic prices, sales, operating cost and

inventory.

Cost Accounting System: It is an effective system of management accounting which

assist the manager to estimate and calculate the cost of services and goods. It is essential for the

company to analysis their profit and control cost effectively. Evaluate the accurate cost is not

easy for the enterprise success and development (Chiwamit, Modell and Yang, 2014). This

approach is used by the Zylla in order to create their business operations and activities more

profitable.

Inventory Management approach: Management accounting system support the business

administrator to maintain and keep the perfect level of cost. It assist in decrease entire cost or

value of business activities and operations. There are certain elements which are includes in this

2

effectively, manager of the company collect necessary information regarding company services

and products (Bovens, Goodin and Schillemans, 2014). It is essential for the enterprise to

increase their turnover and sales in limited duration. Management accounting assist in attain the

same and support in analysing the critical situation in easily.

Ongoing training or activities as well as data: It is essential for Zylla in order to

organise training activities for its workers so they can know and acquire regarding this approach.

Management accounting important for the company to handle daily basis activities and function

in an effective and efficient manner.

Give relevant information:Main benefits of this system is that it assists administrator in

gather and evaluate relevant data which support them in take appropriate judgement about

business operations and functions.

TYPES OF MANAGEMENT ACCOUNTING SYSTEM: There are some methods of

management accounting which are determined as below:

Price Optimisation System: It is a mathematical method which is use by each and every

organisation to evaluate how audience react to various prices or value of product (Brewer,

Sorensen and Stout, 2014). It is essential and beneficial tool for the Zylla and its administrator to

fix the accurate prices for the services and goods. It assist the business administrator to set

accurate cost of their products in a systematic manner. Therefore, company can easily attain their

desired and long term goals or objectives in allotted time period. Data which is use by

organisation for optimisation of price including historic prices, sales, operating cost and

inventory.

Cost Accounting System: It is an effective system of management accounting which

assist the manager to estimate and calculate the cost of services and goods. It is essential for the

company to analysis their profit and control cost effectively. Evaluate the accurate cost is not

easy for the enterprise success and development (Chiwamit, Modell and Yang, 2014). This

approach is used by the Zylla in order to create their business operations and activities more

profitable.

Inventory Management approach: Management accounting system support the business

administrator to maintain and keep the perfect level of cost. It assist in decrease entire cost or

value of business activities and operations. There are certain elements which are includes in this

2

approach such as just-in-time, Economic order quantity and many other. These are valuable for

the organisation maintain production process and accomplish predetermined objectives of

company.

Job costing system: This technique includes accumulation of different kind of cost like;

managerial, overhead, labour etc. Main purpose of company for applying this tool is to control

entire expanses of company and maximise sales of them (EBRAHIMI and MOGHADASPOUR,

2015). Zylla measure the production cost value which is chiefly classified into three parts such as

overhead, direct material and Labour cost.

P2 Various System used for management accounting reporting

Management accounting reporting: It is identify as a record of reporting forms which

including a set of non-financial and financial performance indicators. It provides necessary and

essential information to the different group of user. Reporting is also beneficial for the business

entity to introduce their all pictures in marketplace and in the customer's mind. It is critical for

the referred firm in order to derive their essential strategic and policy insights from these

important document. It is determine as a continues and essential activity which is highly

beneficial in the process of decision making (Klychova, Faskhutdinova and Sadrieva, 2014).

Effective and accurate report is important for the company to achieve best outcomes and results

in limited time duration.

Significance and essential of management accounting reporting: There are some importance of

accounting system which are described as below:

Essential in profitable operations of the business: Management accounting reporting is

the best and essential for the success and development of company. It also beneficial in

achievement of long term growth and accomplishment of predetermined goals of company. With

the use of these tool business entity easily organise their business operations and activities

effectively.

Effective in handling system of control: It is also important for the organisation for

setting up long term objectives and goals. It is the main role of manager to observe after the

workers about attaining of objectives and goals effectively. In order to analysis accurate position

of the company, such type of tool highly supported.

Different methodologies of management accounting reporting: There are certain approach of

reporting which are followed by Zylla. All these are determined as below:

3

the organisation maintain production process and accomplish predetermined objectives of

company.

Job costing system: This technique includes accumulation of different kind of cost like;

managerial, overhead, labour etc. Main purpose of company for applying this tool is to control

entire expanses of company and maximise sales of them (EBRAHIMI and MOGHADASPOUR,

2015). Zylla measure the production cost value which is chiefly classified into three parts such as

overhead, direct material and Labour cost.

P2 Various System used for management accounting reporting

Management accounting reporting: It is identify as a record of reporting forms which

including a set of non-financial and financial performance indicators. It provides necessary and

essential information to the different group of user. Reporting is also beneficial for the business

entity to introduce their all pictures in marketplace and in the customer's mind. It is critical for

the referred firm in order to derive their essential strategic and policy insights from these

important document. It is determine as a continues and essential activity which is highly

beneficial in the process of decision making (Klychova, Faskhutdinova and Sadrieva, 2014).

Effective and accurate report is important for the company to achieve best outcomes and results

in limited time duration.

Significance and essential of management accounting reporting: There are some importance of

accounting system which are described as below:

Essential in profitable operations of the business: Management accounting reporting is

the best and essential for the success and development of company. It also beneficial in

achievement of long term growth and accomplishment of predetermined goals of company. With

the use of these tool business entity easily organise their business operations and activities

effectively.

Effective in handling system of control: It is also important for the organisation for

setting up long term objectives and goals. It is the main role of manager to observe after the

workers about attaining of objectives and goals effectively. In order to analysis accurate position

of the company, such type of tool highly supported.

Different methodologies of management accounting reporting: There are certain approach of

reporting which are followed by Zylla. All these are determined as below:

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Budget report: It is a best methodologies which is being followed by referred

organisation in the process of identifying the performance and profitability level of company. It

can be determine as necessary report or statement which is being applied by the upper level

administration in order to analysis budgeted project or task with the real level of performance, so

that objectives and targets can be accomplished easily (Lavia López and Hiebl, 2014).

Requirement of main chances is completed if the past year budget or fund has been allocated in

order to create accurate budget for the actual year as per the need of company.

Job costing reports: It is a part of accounting report which is important for the company

to shown their actual expanses related with specific task of company. In order to increase

profitability level, it is mainly significant that the expenditure should relate with the calculated

revenue of business. Main aim of the Zylla is to using this tool is to decreasing wastage and

maximising profit margin properly. Instead of activity, management costing reporting is linked

with the approach of production. With the use of this technique, manager of the business easily

track their all record and report of work which is completed along with the employees

performance.

Performance reporting approach: Main focus and aim of company for applying this tool

is to identifying the financial statement or report so that real performance of the company can be

developed effectively (Melnyk and et. al., 2014). It is essential to make an end report of business

and employee performance, so that proper judgement can be proceed for getting maximum

advantages. Measurement can be completed due to relevant information from the past and

current years.

Inventory and Manufacturing report: It is important tool for the management

accounting reporting that should be followed for creating an effective process of production. It is

mainly utilised by the company who have types of physical stock. It includes different kind of

cost such as overhead, labour, inventory, wastage and many other. Therefore manager of the

Zylla can control the availability of the inventory in the enterprise.

M1 Merits of using management accounting approach

Management accounting consists different methods such as Price Optimisation, Cost

Accounting, Inventory Management and Job costing. All these are important for the company to

maintain their performance and profitability in daily basis. All these are also assist the business

manager in order to achieve predetermined goals and targets of company in given time period.

4

organisation in the process of identifying the performance and profitability level of company. It

can be determine as necessary report or statement which is being applied by the upper level

administration in order to analysis budgeted project or task with the real level of performance, so

that objectives and targets can be accomplished easily (Lavia López and Hiebl, 2014).

Requirement of main chances is completed if the past year budget or fund has been allocated in

order to create accurate budget for the actual year as per the need of company.

Job costing reports: It is a part of accounting report which is important for the company

to shown their actual expanses related with specific task of company. In order to increase

profitability level, it is mainly significant that the expenditure should relate with the calculated

revenue of business. Main aim of the Zylla is to using this tool is to decreasing wastage and

maximising profit margin properly. Instead of activity, management costing reporting is linked

with the approach of production. With the use of this technique, manager of the business easily

track their all record and report of work which is completed along with the employees

performance.

Performance reporting approach: Main focus and aim of company for applying this tool

is to identifying the financial statement or report so that real performance of the company can be

developed effectively (Melnyk and et. al., 2014). It is essential to make an end report of business

and employee performance, so that proper judgement can be proceed for getting maximum

advantages. Measurement can be completed due to relevant information from the past and

current years.

Inventory and Manufacturing report: It is important tool for the management

accounting reporting that should be followed for creating an effective process of production. It is

mainly utilised by the company who have types of physical stock. It includes different kind of

cost such as overhead, labour, inventory, wastage and many other. Therefore manager of the

Zylla can control the availability of the inventory in the enterprise.

M1 Merits of using management accounting approach

Management accounting consists different methods such as Price Optimisation, Cost

Accounting, Inventory Management and Job costing. All these are important for the company to

maintain their performance and profitability in daily basis. All these are also assist the business

manager in order to achieve predetermined goals and targets of company in given time period.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

With the help of all tools of management accounting Zylla easily increase their performance in

marketplace.

D1 Desegregation of management accounting systems and reporting

According to the James, (2017) management accounting reporting and system both are

valuable tools for the business success and development. All those are includes some types are

beneficial; for the organisation to maximise their sales and turnover in limited duration.

On the other hand Bennett, (2017) those technique's are beneficial and essential for the

company to maximise their profitability and performance level in limited time duration.

TASK 2

P3 Compute cost using absorption and marginal costing

Cost: It is one of the valuable and necessary part of the every business entity in order to

do their all activities and functions in an appropriate manner. Without this aspect company can

not grow and develop their operation in different level.

Costing: It is also important and significant part of each and every company to measure

their performance and profitability ratio (Messner, 2016). It evaluate the cost of product and

process for the motive of controlling, budgeting and pricing. It is available in the business as the

form of direct and indirect cost, it is essential for the Zylla to calculate their productivity and

effectiveness level systematically. Costing is mainly classified into two parts which are

determined as below:

Absorption Costing: These is the essential tool for the company to designing and

preparing their financial report for external objective. Such type of cost mainly linked with the

manufacturing of products and services. It is important for the Zylla to measure their profitability

and performance as compare to other businesses. It assist the administrator to calculate their

turnover and revenue in an essential manner (Mistry, Sharma and Low, 2014). It is beneficial

method of costing a products in which both fixed and variable cost are provided systematically.

Marginal Costing: It is also important method of the company to evaluate their sales and

net profit systematically. With the help of this technique's business entity easily measure their

performance and effectiveness level in limited time period. With the use of this approach,

company view fixed expanses or expenditure on regular basis. This assist the manager to

decrease their addition cost and maximise cost of production. This methodologies is very

5

marketplace.

D1 Desegregation of management accounting systems and reporting

According to the James, (2017) management accounting reporting and system both are

valuable tools for the business success and development. All those are includes some types are

beneficial; for the organisation to maximise their sales and turnover in limited duration.

On the other hand Bennett, (2017) those technique's are beneficial and essential for the

company to maximise their profitability and performance level in limited time duration.

TASK 2

P3 Compute cost using absorption and marginal costing

Cost: It is one of the valuable and necessary part of the every business entity in order to

do their all activities and functions in an appropriate manner. Without this aspect company can

not grow and develop their operation in different level.

Costing: It is also important and significant part of each and every company to measure

their performance and profitability ratio (Messner, 2016). It evaluate the cost of product and

process for the motive of controlling, budgeting and pricing. It is available in the business as the

form of direct and indirect cost, it is essential for the Zylla to calculate their productivity and

effectiveness level systematically. Costing is mainly classified into two parts which are

determined as below:

Absorption Costing: These is the essential tool for the company to designing and

preparing their financial report for external objective. Such type of cost mainly linked with the

manufacturing of products and services. It is important for the Zylla to measure their profitability

and performance as compare to other businesses. It assist the administrator to calculate their

turnover and revenue in an essential manner (Mistry, Sharma and Low, 2014). It is beneficial

method of costing a products in which both fixed and variable cost are provided systematically.

Marginal Costing: It is also important method of the company to evaluate their sales and

net profit systematically. With the help of this technique's business entity easily measure their

performance and effectiveness level in limited time period. With the use of this approach,

company view fixed expanses or expenditure on regular basis. This assist the manager to

decrease their addition cost and maximise cost of production. This methodologies is very

5

effective in nature where both variable and fixed cost of value modify for particular time

(Nørreklit, 2014).

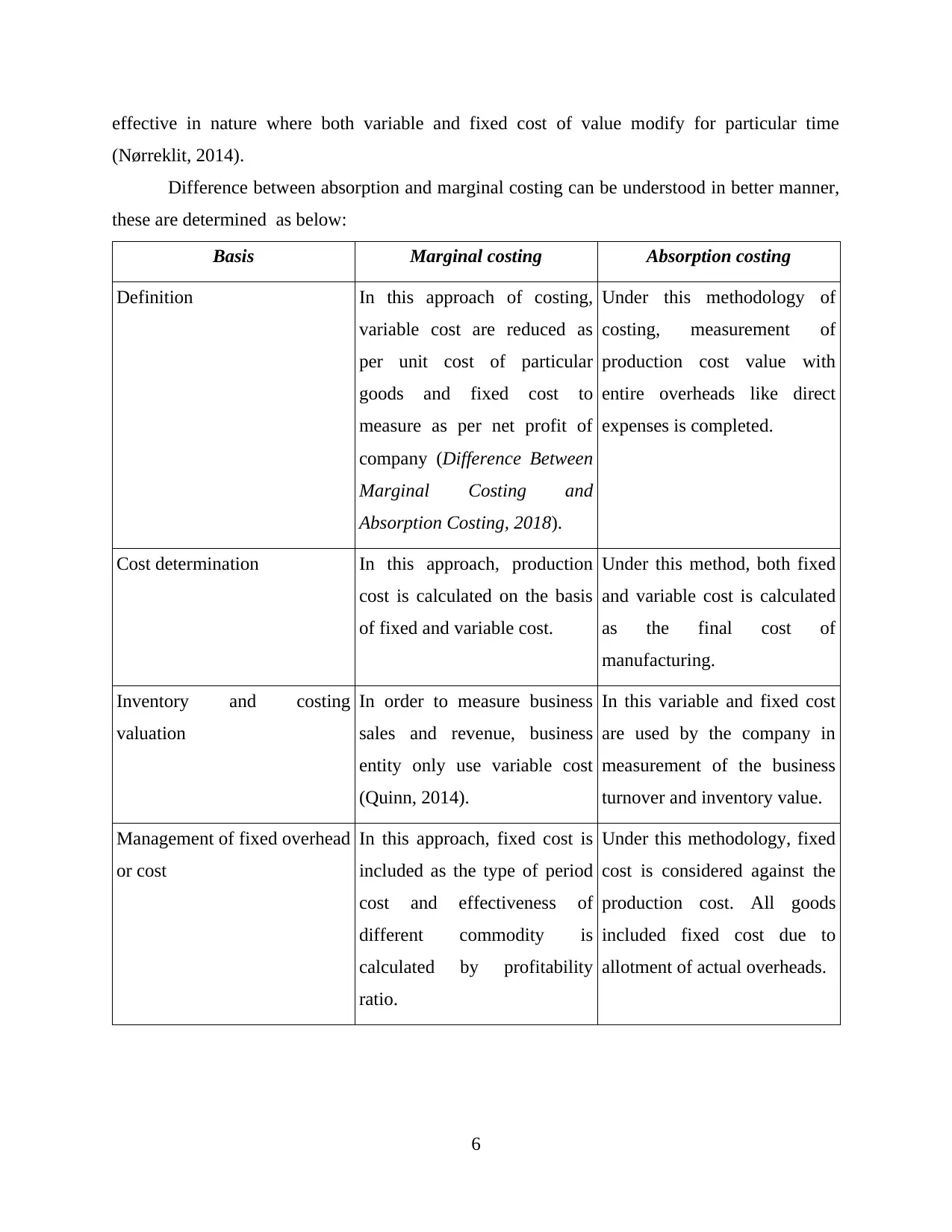

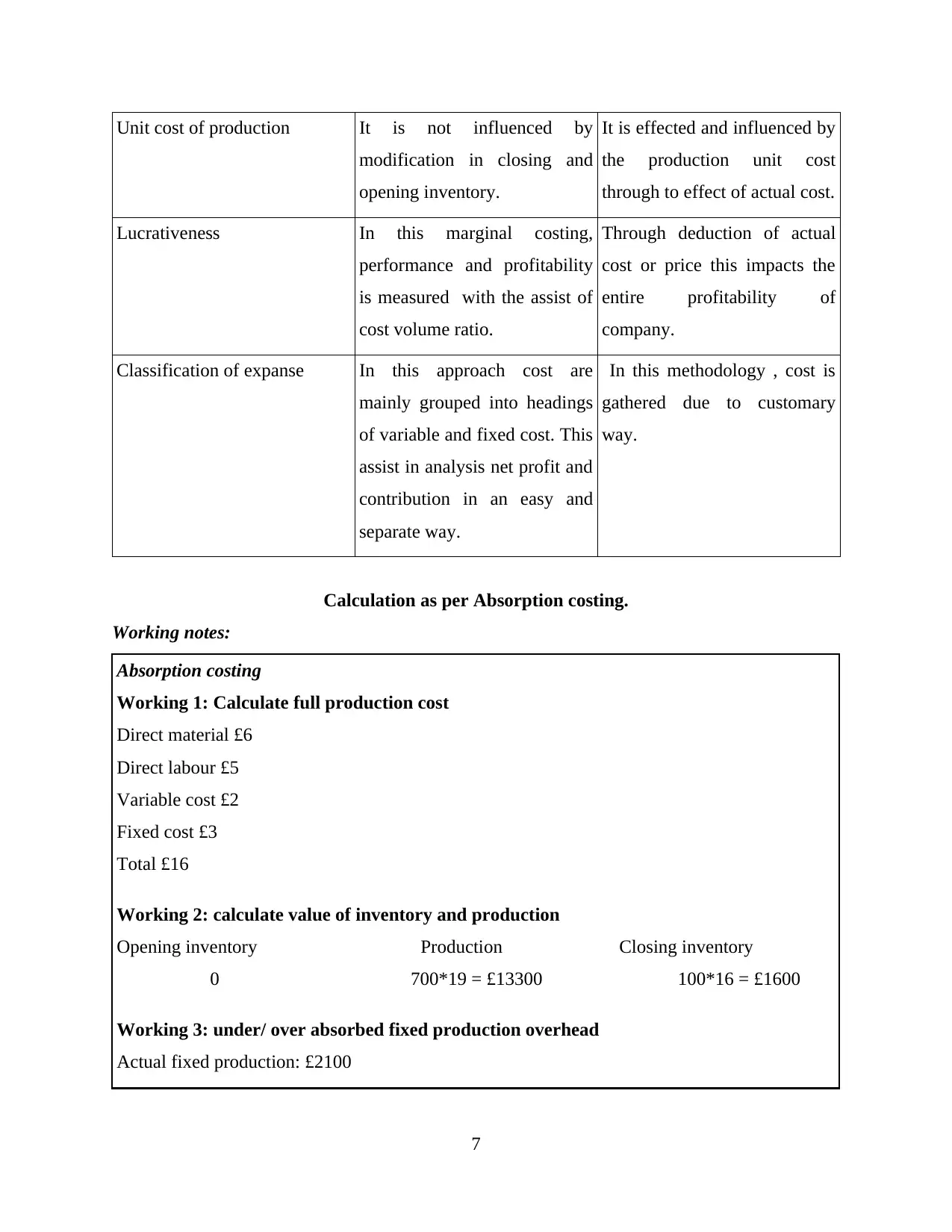

Difference between absorption and marginal costing can be understood in better manner,

these are determined as below:

Basis Marginal costing Absorption costing

Definition In this approach of costing,

variable cost are reduced as

per unit cost of particular

goods and fixed cost to

measure as per net profit of

company (Difference Between

Marginal Costing and

Absorption Costing, 2018).

Under this methodology of

costing, measurement of

production cost value with

entire overheads like direct

expenses is completed.

Cost determination In this approach, production

cost is calculated on the basis

of fixed and variable cost.

Under this method, both fixed

and variable cost is calculated

as the final cost of

manufacturing.

Inventory and costing

valuation

In order to measure business

sales and revenue, business

entity only use variable cost

(Quinn, 2014).

In this variable and fixed cost

are used by the company in

measurement of the business

turnover and inventory value.

Management of fixed overhead

or cost

In this approach, fixed cost is

included as the type of period

cost and effectiveness of

different commodity is

calculated by profitability

ratio.

Under this methodology, fixed

cost is considered against the

production cost. All goods

included fixed cost due to

allotment of actual overheads.

6

(Nørreklit, 2014).

Difference between absorption and marginal costing can be understood in better manner,

these are determined as below:

Basis Marginal costing Absorption costing

Definition In this approach of costing,

variable cost are reduced as

per unit cost of particular

goods and fixed cost to

measure as per net profit of

company (Difference Between

Marginal Costing and

Absorption Costing, 2018).

Under this methodology of

costing, measurement of

production cost value with

entire overheads like direct

expenses is completed.

Cost determination In this approach, production

cost is calculated on the basis

of fixed and variable cost.

Under this method, both fixed

and variable cost is calculated

as the final cost of

manufacturing.

Inventory and costing

valuation

In order to measure business

sales and revenue, business

entity only use variable cost

(Quinn, 2014).

In this variable and fixed cost

are used by the company in

measurement of the business

turnover and inventory value.

Management of fixed overhead

or cost

In this approach, fixed cost is

included as the type of period

cost and effectiveness of

different commodity is

calculated by profitability

ratio.

Under this methodology, fixed

cost is considered against the

production cost. All goods

included fixed cost due to

allotment of actual overheads.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Unit cost of production It is not influenced by

modification in closing and

opening inventory.

It is effected and influenced by

the production unit cost

through to effect of actual cost.

Lucrativeness In this marginal costing,

performance and profitability

is measured with the assist of

cost volume ratio.

Through deduction of actual

cost or price this impacts the

entire profitability of

company.

Classification of expanse In this approach cost are

mainly grouped into headings

of variable and fixed cost. This

assist in analysis net profit and

contribution in an easy and

separate way.

In this methodology , cost is

gathered due to customary

way.

Calculation as per Absorption costing.

Working notes:

Absorption costing

Working 1: Calculate full production cost

Direct material £6

Direct labour £5

Variable cost £2

Fixed cost £3

Total £16

Working 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*19 = £13300 100*16 = £1600

Working 3: under/ over absorbed fixed production overhead

Actual fixed production: £2100

7

modification in closing and

opening inventory.

It is effected and influenced by

the production unit cost

through to effect of actual cost.

Lucrativeness In this marginal costing,

performance and profitability

is measured with the assist of

cost volume ratio.

Through deduction of actual

cost or price this impacts the

entire profitability of

company.

Classification of expanse In this approach cost are

mainly grouped into headings

of variable and fixed cost. This

assist in analysis net profit and

contribution in an easy and

separate way.

In this methodology , cost is

gathered due to customary

way.

Calculation as per Absorption costing.

Working notes:

Absorption costing

Working 1: Calculate full production cost

Direct material £6

Direct labour £5

Variable cost £2

Fixed cost £3

Total £16

Working 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 700*19 = £13300 100*16 = £1600

Working 3: under/ over absorbed fixed production overhead

Actual fixed production: £2100

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

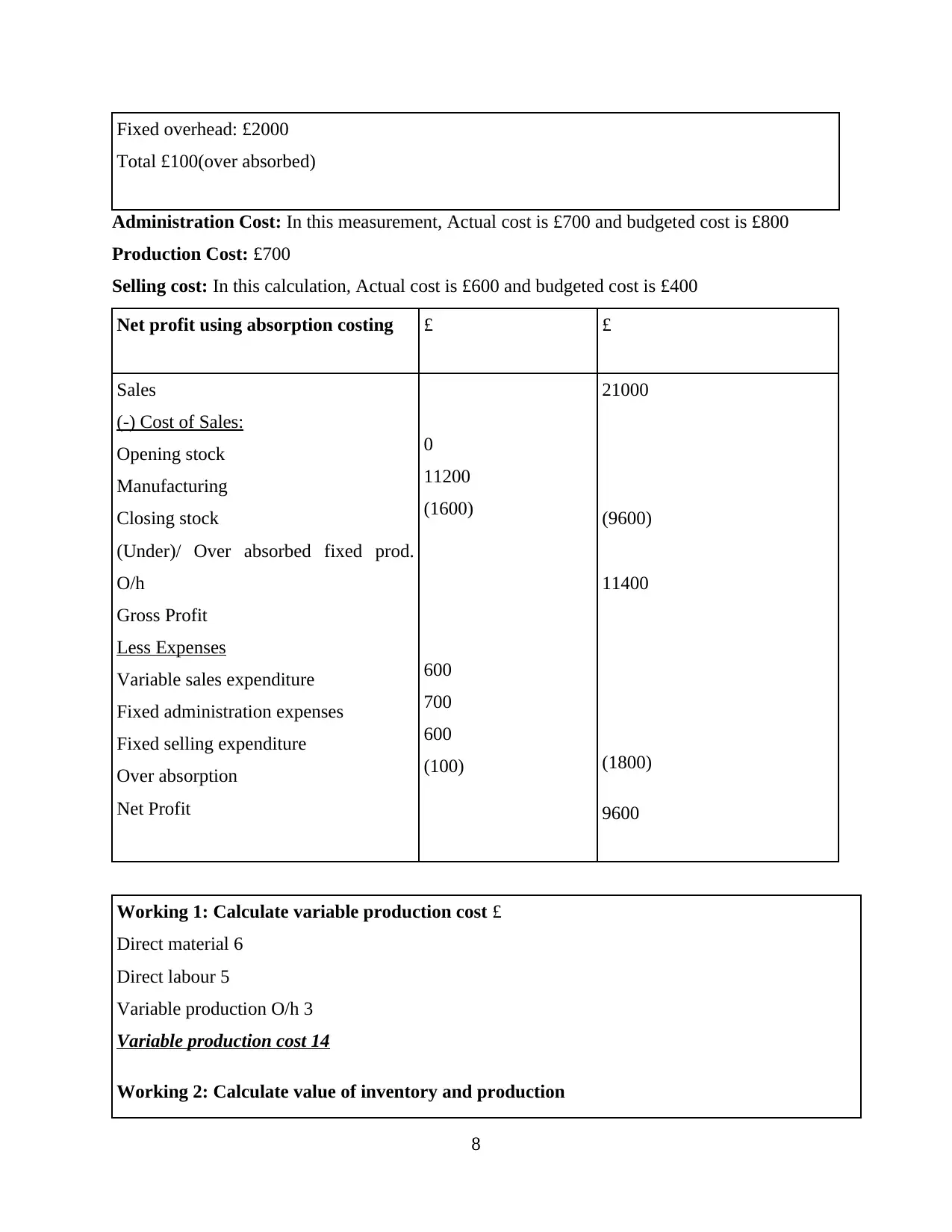

Fixed overhead: £2000

Total £100(over absorbed)

Administration Cost: In this measurement, Actual cost is £700 and budgeted cost is £800

Production Cost: £700

Selling cost: In this calculation, Actual cost is £600 and budgeted cost is £400

Net profit using absorption costing £ £

Sales

(-) Cost of Sales:

Opening stock

Manufacturing

Closing stock

(Under)/ Over absorbed fixed prod.

O/h

Gross Profit

Less Expenses

Variable sales expenditure

Fixed administration expenses

Fixed selling expenditure

Over absorption

Net Profit

0

11200

(1600)

600

700

600

(100)

21000

(9600)

11400

(1800)

9600

Working 1: Calculate variable production cost £

Direct material 6

Direct labour 5

Variable production O/h 3

Variable production cost 14

Working 2: Calculate value of inventory and production

8

Total £100(over absorbed)

Administration Cost: In this measurement, Actual cost is £700 and budgeted cost is £800

Production Cost: £700

Selling cost: In this calculation, Actual cost is £600 and budgeted cost is £400

Net profit using absorption costing £ £

Sales

(-) Cost of Sales:

Opening stock

Manufacturing

Closing stock

(Under)/ Over absorbed fixed prod.

O/h

Gross Profit

Less Expenses

Variable sales expenditure

Fixed administration expenses

Fixed selling expenditure

Over absorption

Net Profit

0

11200

(1600)

600

700

600

(100)

21000

(9600)

11400

(1800)

9600

Working 1: Calculate variable production cost £

Direct material 6

Direct labour 5

Variable production O/h 3

Variable production cost 14

Working 2: Calculate value of inventory and production

8

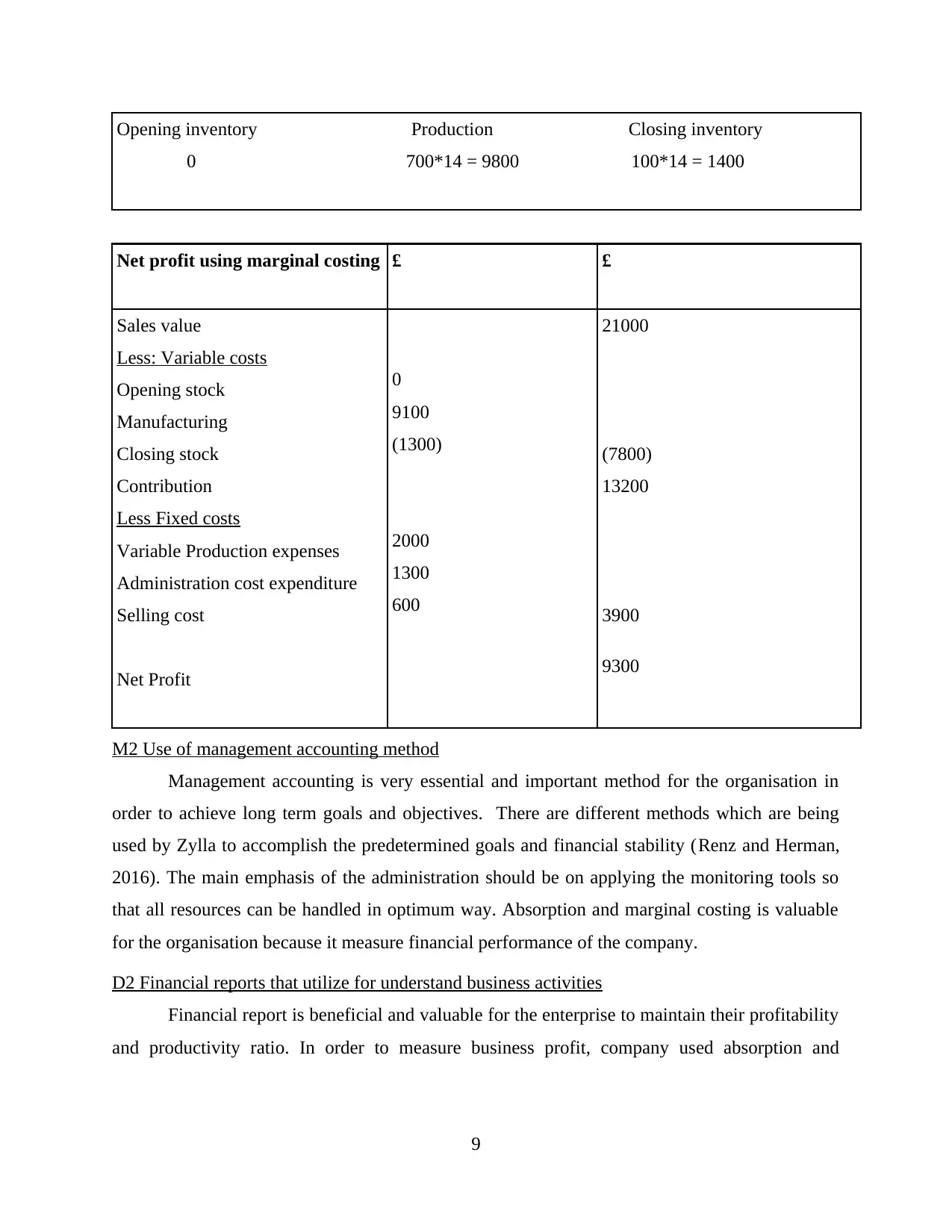

Opening inventory Production Closing inventory

0 700*14 = 9800 100*14 = 1400

Net profit using marginal costing £ £

Sales value

Less: Variable costs

Opening stock

Manufacturing

Closing stock

Contribution

Less Fixed costs

Variable Production expenses

Administration cost expenditure

Selling cost

Net Profit

0

9100

(1300)

2000

1300

600

21000

(7800)

13200

3900

9300

M2 Use of management accounting method

Management accounting is very essential and important method for the organisation in

order to achieve long term goals and objectives. There are different methods which are being

used by Zylla to accomplish the predetermined goals and financial stability (Renz and Herman,

2016). The main emphasis of the administration should be on applying the monitoring tools so

that all resources can be handled in optimum way. Absorption and marginal costing is valuable

for the organisation because it measure financial performance of the company.

D2 Financial reports that utilize for understand business activities

Financial report is beneficial and valuable for the enterprise to maintain their profitability

and productivity ratio. In order to measure business profit, company used absorption and

9

0 700*14 = 9800 100*14 = 1400

Net profit using marginal costing £ £

Sales value

Less: Variable costs

Opening stock

Manufacturing

Closing stock

Contribution

Less Fixed costs

Variable Production expenses

Administration cost expenditure

Selling cost

Net Profit

0

9100

(1300)

2000

1300

600

21000

(7800)

13200

3900

9300

M2 Use of management accounting method

Management accounting is very essential and important method for the organisation in

order to achieve long term goals and objectives. There are different methods which are being

used by Zylla to accomplish the predetermined goals and financial stability (Renz and Herman,

2016). The main emphasis of the administration should be on applying the monitoring tools so

that all resources can be handled in optimum way. Absorption and marginal costing is valuable

for the organisation because it measure financial performance of the company.

D2 Financial reports that utilize for understand business activities

Financial report is beneficial and valuable for the enterprise to maintain their profitability

and productivity ratio. In order to measure business profit, company used absorption and

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.