Management Accounting Report: Financial Analysis for Zylla Company

VerifiedAdded on 2020/06/03

|17

|4534

|55

Report

AI Summary

This report provides a comprehensive analysis of Zylla Company's management accounting system. It begins with an introduction to management accounting, its types, and the diverse methods employed by management accountants for reporting, including cost reports, budget reports, and performance reports. The report delves into the merits of implementing an effective accounting system and critically evaluates the reporting system. Task 2 focuses on the calculation of net profits using marginal costing and absorption costing methods, along with a discussion of different accounting techniques like financial planning, financial statement analysis, and budgetary control. Task 3 explores the benefits and limitations of planning tools and offers a critical evaluation of planning techniques, along with tools used for resolving financial issues. Finally, Task 4 addresses financial issues present in organizations and suggests measures to mitigate them, including an evaluation of financial issues. The report concludes with a summary of findings and recommendations for Zylla Company, emphasizing the importance of management accounting in achieving pre-set targets and sustainable development.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

FROM: MANAGEMENT ACCOUNTING OFFICER..................................................................1

TO,...................................................................................................................................................1

GENERAL MANAGER..................................................................................................................1

ZYLLA COMAPNY ......................................................................................................................1

SUB: MANAGEMENT ACCOUNTING SYSTEM .....................................................................1

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Management accounting and its types:............................................................................1

P2: Diverse methods implemented by the management accountant for management

accounting reporting:..............................................................................................................3

M1: Merits of implementing accounting:...............................................................................4

D1: Critically evaluate Reporting system...............................................................................4

TASK 2............................................................................................................................................4

P3: Net profits as per the marginal costing and absorption costing:......................................4

M2: Different accounting techniques.....................................................................................6

D2: Critical evaluation of income statements........................................................................6

TASK 3............................................................................................................................................7

P4: Benefits and limitation of using planning tools...............................................................7

M3: Critically evaluation of planning techniques..................................................................9

D3: Tools used for resolving financial issues.......................................................................10

TASK 4..........................................................................................................................................10

P5: Financial issues which are present in organisation and measures to reduce them.........10

M4: Evaluation of financial issues.......................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

Books and Journals...............................................................................................................13

FROM: MANAGEMENT ACCOUNTING OFFICER..................................................................1

TO,...................................................................................................................................................1

GENERAL MANAGER..................................................................................................................1

ZYLLA COMAPNY ......................................................................................................................1

SUB: MANAGEMENT ACCOUNTING SYSTEM .....................................................................1

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Management accounting and its types:............................................................................1

P2: Diverse methods implemented by the management accountant for management

accounting reporting:..............................................................................................................3

M1: Merits of implementing accounting:...............................................................................4

D1: Critically evaluate Reporting system...............................................................................4

TASK 2............................................................................................................................................4

P3: Net profits as per the marginal costing and absorption costing:......................................4

M2: Different accounting techniques.....................................................................................6

D2: Critical evaluation of income statements........................................................................6

TASK 3............................................................................................................................................7

P4: Benefits and limitation of using planning tools...............................................................7

M3: Critically evaluation of planning techniques..................................................................9

D3: Tools used for resolving financial issues.......................................................................10

TASK 4..........................................................................................................................................10

P5: Financial issues which are present in organisation and measures to reduce them.........10

M4: Evaluation of financial issues.......................................................................................12

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

Books and Journals...............................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FROM: MANAGEMENT ACCOUNTING OFFICER

TO,

GENERAL MANAGER

ZYLLA COMAPNY

SUB: MANAGEMENT ACCOUNTING SYSTEM

INTRODUCTION

Management accounting helps each and every firm to attains its pre-set targets with the

specified time limit. However, there are certain tools which are used by organisations for making

effective execution of the operational works. Although, the company needs to appoint a

management accountant who could know about the procedures for applying the management

accounting tools (Ahadiat, 2013). There is a need to adopt these tools that can create efficiency

for the firm. Under this report, the Zylla company is striving hard to improve their performance

by applying diverse management accounting in an effective manner. On the basis of these

management accounting tools, Zylla makes certain reports which would ultimately helps the

organisation for making effective decisions. Under this report, net profits is calculated by

implementing absorption and marginal costing. Various planning tools are going to discussed

under this so that the certain strategies can be made. Various management tools such as KPI,

Benchmarking, Financial governance are used under this for identifying and improving the

financial distress of the organisation.

TASK 1

P1: Management accounting and its types:

Management accounting is the process of knowing, calculating, assessing, evaluating and

communicating information for meeting the company's pre-set targets. This is the branch of

accounting which is also known as the name of cost accounting. In other words, this is the act of

forming sense of financial and costing data and changing that data into the useful information for

the management so that the managers could make strategies in such a manner by which they can

gain the sustainable development (Dillard and Roslender, 2011). This additionally means

1

TO,

GENERAL MANAGER

ZYLLA COMAPNY

SUB: MANAGEMENT ACCOUNTING SYSTEM

INTRODUCTION

Management accounting helps each and every firm to attains its pre-set targets with the

specified time limit. However, there are certain tools which are used by organisations for making

effective execution of the operational works. Although, the company needs to appoint a

management accountant who could know about the procedures for applying the management

accounting tools (Ahadiat, 2013). There is a need to adopt these tools that can create efficiency

for the firm. Under this report, the Zylla company is striving hard to improve their performance

by applying diverse management accounting in an effective manner. On the basis of these

management accounting tools, Zylla makes certain reports which would ultimately helps the

organisation for making effective decisions. Under this report, net profits is calculated by

implementing absorption and marginal costing. Various planning tools are going to discussed

under this so that the certain strategies can be made. Various management tools such as KPI,

Benchmarking, Financial governance are used under this for identifying and improving the

financial distress of the organisation.

TASK 1

P1: Management accounting and its types:

Management accounting is the process of knowing, calculating, assessing, evaluating and

communicating information for meeting the company's pre-set targets. This is the branch of

accounting which is also known as the name of cost accounting. In other words, this is the act of

forming sense of financial and costing data and changing that data into the useful information for

the management so that the managers could make strategies in such a manner by which they can

gain the sustainable development (Dillard and Roslender, 2011). This additionally means

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

assessing and recording business activities for the firm internal use in order to improve efficiency

and productivity. There are so many management accounting tools which are discussed as under:

Cost accounting: This is the cost accounting tool which are used by the firm for making

the product in a cost efficient manner. By which a firm could use this technique, so that the firm

could effectively use this tool for making the business objectives in an effective manner. With

the help of this tool, Zylla could eliminate the wastage costs from their per unit cost of

production. By eliminating costs of the product, company could gain the competitive advantage

and able to achieve its pre-set targets.

Job costing system: This is one of the management accounting system which are used by

the firm for recording the costs of manufacturing job, rather than process. By implementing job

costing system, a project manager can of track each job. Controlling data is highly related to the

operations of the firm. This resemble to the batch costing system.

Batch costing system: Under this system, each and every batch address independent

major costs units. This is the cluster of the costs that includes at the time of group of products or

services are formed and such can be determined to the most specific goods or services under the

group.

Price optimising system: Under this system, price is optimised in an effective manner so

that the prospective consumers are able to buy the products. And this would make effective

strategy for the firm operation (Morales,and Lambert, 2013). By having this system in the firm,

the management of the company will get to know the price on which they are willing to offer the

price of the product to the ultimate consumers.

Inventory management system: Under this system, the manager would manage its

inventory so that the firm can address this in an effective manner. However, there is a strong

need to manage for gaining sustainability, and this is the most effective tool for optimising the

value of the firm by controlling the inventory so effectively.

These are the management accounting tool which are implemented by the firm for achieving its

pre-set targets. Although these are the most crucial part that helps the manager and the top level

authorities for making effective decisions.

2

and productivity. There are so many management accounting tools which are discussed as under:

Cost accounting: This is the cost accounting tool which are used by the firm for making

the product in a cost efficient manner. By which a firm could use this technique, so that the firm

could effectively use this tool for making the business objectives in an effective manner. With

the help of this tool, Zylla could eliminate the wastage costs from their per unit cost of

production. By eliminating costs of the product, company could gain the competitive advantage

and able to achieve its pre-set targets.

Job costing system: This is one of the management accounting system which are used by

the firm for recording the costs of manufacturing job, rather than process. By implementing job

costing system, a project manager can of track each job. Controlling data is highly related to the

operations of the firm. This resemble to the batch costing system.

Batch costing system: Under this system, each and every batch address independent

major costs units. This is the cluster of the costs that includes at the time of group of products or

services are formed and such can be determined to the most specific goods or services under the

group.

Price optimising system: Under this system, price is optimised in an effective manner so

that the prospective consumers are able to buy the products. And this would make effective

strategy for the firm operation (Morales,and Lambert, 2013). By having this system in the firm,

the management of the company will get to know the price on which they are willing to offer the

price of the product to the ultimate consumers.

Inventory management system: Under this system, the manager would manage its

inventory so that the firm can address this in an effective manner. However, there is a strong

need to manage for gaining sustainability, and this is the most effective tool for optimising the

value of the firm by controlling the inventory so effectively.

These are the management accounting tool which are implemented by the firm for achieving its

pre-set targets. Although these are the most crucial part that helps the manager and the top level

authorities for making effective decisions.

2

P2: Diverse methods implemented by the management accountant for management accounting

reporting:

Management accounting focuses inside on the data achieved by means of financial

accounting. This is made for arranging, controlling and decision making. Management

accounting relies on the typical income statements, cash flow statement, balance sheets, but also

uses different sorts of management reports for evaluating company's data. These incorporates

product cost reports, budgetary plans and performance reports.

Cost reports: Management accountants measures costs of products made. This is done

by considering raw material costs, overheads, labour and some other additional expenses into

consideration (Baldvinsdottir, Mitchell and Nørreklit,2010). The totals costs are separated by the

amount of products made. Effective informations are briefly summarised according to the cost

report. This report empowers managers to supervise the cost of items as opposed to selling

prices. This empowers the manager of the cited firm to design and oversee profits margin.

Budget reports: This is the most effective component of management accounting.

Budgets are mainly made by executing earlier years' financial plans and changing in accordance

with future projections. A company's budget lists whole sources of incomes and costs. A firm

tries to finish its pre-set targets while remaining with the planned sums. Manager of the cited

company to overlook into an advanced as the suppliers of the raw materials to protect money.

They also find various ways to enhance sales at the time of limiting expenses.

Performance Report: This is the report structure that reflects the performance of the

cited firm. Management accountants implement budgets to compare its actual expenses and

income to the budgeted amount. The variance is analysed during knowing the new budgets and

entire information which are connected to these amounts is listed on a performance report.

These are calculated on an yearly basis (Fullerton, Kennedy and Widener, 2013). However, so

many firms incorporates monthly or quarterly reports. These kinds of reports assists managers

to plan for future demand in producing and enhancing costs.

Other reports: there are diverse reports that assist for forming by the management

accountants. These reports show backlog information and if the orders are placed that were

highly needed. Such kind of reports also scrutinize if the vast number of orders were ordered.

Business situation reports also incorporates which assists the Zylla company to incorporates

decisions regarding existing and future firm conditions.

3

reporting:

Management accounting focuses inside on the data achieved by means of financial

accounting. This is made for arranging, controlling and decision making. Management

accounting relies on the typical income statements, cash flow statement, balance sheets, but also

uses different sorts of management reports for evaluating company's data. These incorporates

product cost reports, budgetary plans and performance reports.

Cost reports: Management accountants measures costs of products made. This is done

by considering raw material costs, overheads, labour and some other additional expenses into

consideration (Baldvinsdottir, Mitchell and Nørreklit,2010). The totals costs are separated by the

amount of products made. Effective informations are briefly summarised according to the cost

report. This report empowers managers to supervise the cost of items as opposed to selling

prices. This empowers the manager of the cited firm to design and oversee profits margin.

Budget reports: This is the most effective component of management accounting.

Budgets are mainly made by executing earlier years' financial plans and changing in accordance

with future projections. A company's budget lists whole sources of incomes and costs. A firm

tries to finish its pre-set targets while remaining with the planned sums. Manager of the cited

company to overlook into an advanced as the suppliers of the raw materials to protect money.

They also find various ways to enhance sales at the time of limiting expenses.

Performance Report: This is the report structure that reflects the performance of the

cited firm. Management accountants implement budgets to compare its actual expenses and

income to the budgeted amount. The variance is analysed during knowing the new budgets and

entire information which are connected to these amounts is listed on a performance report.

These are calculated on an yearly basis (Fullerton, Kennedy and Widener, 2013). However, so

many firms incorporates monthly or quarterly reports. These kinds of reports assists managers

to plan for future demand in producing and enhancing costs.

Other reports: there are diverse reports that assist for forming by the management

accountants. These reports show backlog information and if the orders are placed that were

highly needed. Such kind of reports also scrutinize if the vast number of orders were ordered.

Business situation reports also incorporates which assists the Zylla company to incorporates

decisions regarding existing and future firm conditions.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Job costs reports: As per this report, Job cost report is an introductory place for higher

of the data covered under other report. Under this report lists each job under which operations

and lists the total costs covered on the Job in earlier period. This job costs are costs broken down

into the mentioned categories: Labour costs, Materiel costs, Subcontractor costs. Field

overheads, Liquidated damages. By relying this report, Zylla firm could implement this in an

efficient manner.

These report are the crucial parts under which firm could gain the sustainable

development for the firm.

M1: Merits of implementing accounting:

This is observed that the management accounting system is a productive framework that

are utilized by the association's for controlling and protecting its financial transactions. This sort

of frameworks could help them to get positive results with the accessible assets. For achieving

maximum results, management needs to embrace different management framework that could be

viable for the firm (Cinquini and Tenucci, 2010). The most basic for implementing these

framework is to improve productivity and proficiency for the firm. The Zylla organization turn

out to be more dependable or reliable for helping supportability.

D1: Critically evaluate Reporting system.

Evaluation of management accounting system provides the information which is used by

the management to satisfies the different needs of customer. These system provides the

opportunity to control different functions which are defined below:

Cost analysis: This evaluation provides the important information regarding different

costs which are incurred at different level of activities. This helps to reduces the process

which increase the cost of operations. This enables them to focus on important

procedures.

Activity based costing methods: This evaluation provides the information regarding cost

incurred on every task. This helps to focus on important tasks which are more profitable.

TASK 2

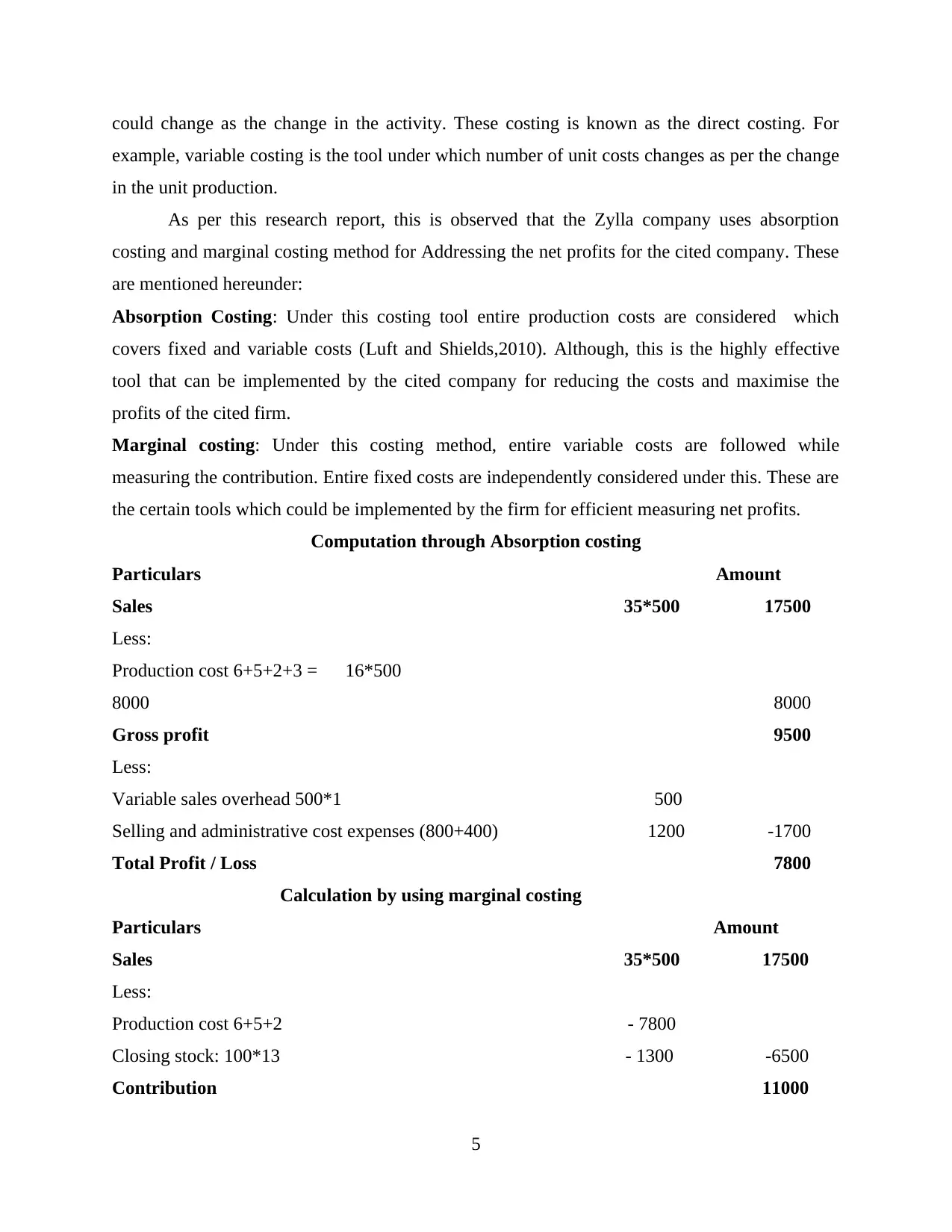

P3: Net profits as per the marginal costing and absorption costing:

Costing is the main tool that are used by the firm for asserting their per unit costs for the

organisation. This may includes the assignment of variable costs, which are those costs that

4

of the data covered under other report. Under this report lists each job under which operations

and lists the total costs covered on the Job in earlier period. This job costs are costs broken down

into the mentioned categories: Labour costs, Materiel costs, Subcontractor costs. Field

overheads, Liquidated damages. By relying this report, Zylla firm could implement this in an

efficient manner.

These report are the crucial parts under which firm could gain the sustainable

development for the firm.

M1: Merits of implementing accounting:

This is observed that the management accounting system is a productive framework that

are utilized by the association's for controlling and protecting its financial transactions. This sort

of frameworks could help them to get positive results with the accessible assets. For achieving

maximum results, management needs to embrace different management framework that could be

viable for the firm (Cinquini and Tenucci, 2010). The most basic for implementing these

framework is to improve productivity and proficiency for the firm. The Zylla organization turn

out to be more dependable or reliable for helping supportability.

D1: Critically evaluate Reporting system.

Evaluation of management accounting system provides the information which is used by

the management to satisfies the different needs of customer. These system provides the

opportunity to control different functions which are defined below:

Cost analysis: This evaluation provides the important information regarding different

costs which are incurred at different level of activities. This helps to reduces the process

which increase the cost of operations. This enables them to focus on important

procedures.

Activity based costing methods: This evaluation provides the information regarding cost

incurred on every task. This helps to focus on important tasks which are more profitable.

TASK 2

P3: Net profits as per the marginal costing and absorption costing:

Costing is the main tool that are used by the firm for asserting their per unit costs for the

organisation. This may includes the assignment of variable costs, which are those costs that

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

could change as the change in the activity. These costing is known as the direct costing. For

example, variable costing is the tool under which number of unit costs changes as per the change

in the unit production.

As per this research report, this is observed that the Zylla company uses absorption

costing and marginal costing method for Addressing the net profits for the cited company. These

are mentioned hereunder:

Absorption Costing: Under this costing tool entire production costs are considered which

covers fixed and variable costs (Luft and Shields,2010). Although, this is the highly effective

tool that can be implemented by the cited company for reducing the costs and maximise the

profits of the cited firm.

Marginal costing: Under this costing method, entire variable costs are followed while

measuring the contribution. Entire fixed costs are independently considered under this. These are

the certain tools which could be implemented by the firm for efficient measuring net profits.

Computation through Absorption costing

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2+3 = 16*500

8000 8000

Gross profit 9500

Less:

Variable sales overhead 500*1 500

Selling and administrative cost expenses (800+400) 1200 -1700

Total Profit / Loss 7800

Calculation by using marginal costing

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2 - 7800

Closing stock: 100*13 - 1300 -6500

Contribution 11000

5

example, variable costing is the tool under which number of unit costs changes as per the change

in the unit production.

As per this research report, this is observed that the Zylla company uses absorption

costing and marginal costing method for Addressing the net profits for the cited company. These

are mentioned hereunder:

Absorption Costing: Under this costing tool entire production costs are considered which

covers fixed and variable costs (Luft and Shields,2010). Although, this is the highly effective

tool that can be implemented by the cited company for reducing the costs and maximise the

profits of the cited firm.

Marginal costing: Under this costing method, entire variable costs are followed while

measuring the contribution. Entire fixed costs are independently considered under this. These are

the certain tools which could be implemented by the firm for efficient measuring net profits.

Computation through Absorption costing

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2+3 = 16*500

8000 8000

Gross profit 9500

Less:

Variable sales overhead 500*1 500

Selling and administrative cost expenses (800+400) 1200 -1700

Total Profit / Loss 7800

Calculation by using marginal costing

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2 - 7800

Closing stock: 100*13 - 1300 -6500

Contribution 11000

5

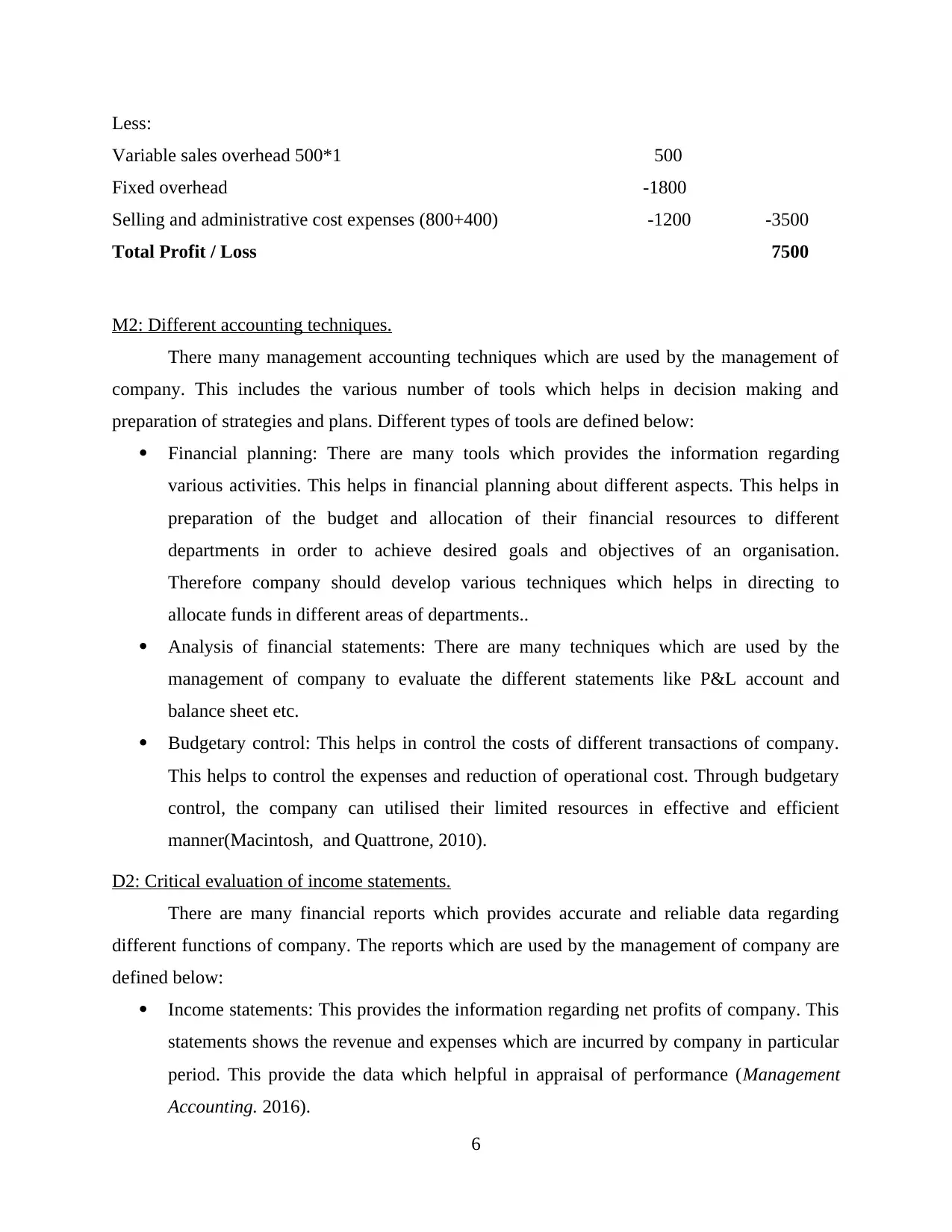

Less:

Variable sales overhead 500*1 500

Fixed overhead -1800

Selling and administrative cost expenses (800+400) -1200 -3500

Total Profit / Loss 7500

M2: Different accounting techniques.

There many management accounting techniques which are used by the management of

company. This includes the various number of tools which helps in decision making and

preparation of strategies and plans. Different types of tools are defined below:

Financial planning: There are many tools which provides the information regarding

various activities. This helps in financial planning about different aspects. This helps in

preparation of the budget and allocation of their financial resources to different

departments in order to achieve desired goals and objectives of an organisation.

Therefore company should develop various techniques which helps in directing to

allocate funds in different areas of departments..

Analysis of financial statements: There are many techniques which are used by the

management of company to evaluate the different statements like P&L account and

balance sheet etc.

Budgetary control: This helps in control the costs of different transactions of company.

This helps to control the expenses and reduction of operational cost. Through budgetary

control, the company can utilised their limited resources in effective and efficient

manner(Macintosh, and Quattrone, 2010).

D2: Critical evaluation of income statements.

There are many financial reports which provides accurate and reliable data regarding

different functions of company. The reports which are used by the management of company are

defined below:

Income statements: This provides the information regarding net profits of company. This

statements shows the revenue and expenses which are incurred by company in particular

period. This provide the data which helpful in appraisal of performance (Management

Accounting. 2016).

6

Variable sales overhead 500*1 500

Fixed overhead -1800

Selling and administrative cost expenses (800+400) -1200 -3500

Total Profit / Loss 7500

M2: Different accounting techniques.

There many management accounting techniques which are used by the management of

company. This includes the various number of tools which helps in decision making and

preparation of strategies and plans. Different types of tools are defined below:

Financial planning: There are many tools which provides the information regarding

various activities. This helps in financial planning about different aspects. This helps in

preparation of the budget and allocation of their financial resources to different

departments in order to achieve desired goals and objectives of an organisation.

Therefore company should develop various techniques which helps in directing to

allocate funds in different areas of departments..

Analysis of financial statements: There are many techniques which are used by the

management of company to evaluate the different statements like P&L account and

balance sheet etc.

Budgetary control: This helps in control the costs of different transactions of company.

This helps to control the expenses and reduction of operational cost. Through budgetary

control, the company can utilised their limited resources in effective and efficient

manner(Macintosh, and Quattrone, 2010).

D2: Critical evaluation of income statements.

There are many financial reports which provides accurate and reliable data regarding

different functions of company. The reports which are used by the management of company are

defined below:

Income statements: This provides the information regarding net profits of company. This

statements shows the revenue and expenses which are incurred by company in particular

period. This provide the data which helpful in appraisal of performance (Management

Accounting. 2016).

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Balance sheet: Balance sheet shows the true and fair financial position of company. This

also provides the important information regarding assets and liabilities of company. This

helps in determination of their position in market.

TASK 3

P4: Benefits and limitation of using planning tools

Effective planning tools plays an important role in measuring performance of an

organisation and it also helps in decision making process. The financial statement which are

prepared using planning tools shows the stability and growth of an organisation therefore it is

important to understand about budget and its control measures before determining various

planning tools.

Budget: Budget refers to deciding and allocation of funds to complete certain activities in

effective and efficient manner. It can be decided after estimating all expenses and raw material

incurred in execution of project activities (Renz, 2016). The main objective of budget

preparation is to utilise resources and funds in optimum manner which helps in reducing wastage

of resources.

Budgetary control: It is related with controlling and monitoring usage of available funds

in different level of departments through planning, coordination and effective control. It

performs different activities such as :

It helps in dividing an organisation into various sub sections on the basis of their

functions which are considered as budget point.

Evaluate performance of employees as well as formulation of individual budgets for

every budget points.

The main objective of Zylla company is to maintaining balancing their actual performance with

the standard performance and also monitoring various operations in terms of utilizing available

funds in optimum manner.

Process of budgetary control: Discuss with managers: The first step is to discussing the material information with the

managers of company. Such material information are related with the probability and

stability of company And any changes required in budget should also need to be

discussed.

7

also provides the important information regarding assets and liabilities of company. This

helps in determination of their position in market.

TASK 3

P4: Benefits and limitation of using planning tools

Effective planning tools plays an important role in measuring performance of an

organisation and it also helps in decision making process. The financial statement which are

prepared using planning tools shows the stability and growth of an organisation therefore it is

important to understand about budget and its control measures before determining various

planning tools.

Budget: Budget refers to deciding and allocation of funds to complete certain activities in

effective and efficient manner. It can be decided after estimating all expenses and raw material

incurred in execution of project activities (Renz, 2016). The main objective of budget

preparation is to utilise resources and funds in optimum manner which helps in reducing wastage

of resources.

Budgetary control: It is related with controlling and monitoring usage of available funds

in different level of departments through planning, coordination and effective control. It

performs different activities such as :

It helps in dividing an organisation into various sub sections on the basis of their

functions which are considered as budget point.

Evaluate performance of employees as well as formulation of individual budgets for

every budget points.

The main objective of Zylla company is to maintaining balancing their actual performance with

the standard performance and also monitoring various operations in terms of utilizing available

funds in optimum manner.

Process of budgetary control: Discuss with managers: The first step is to discussing the material information with the

managers of company. Such material information are related with the probability and

stability of company And any changes required in budget should also need to be

discussed.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Make proper assumptions and declaration: As the budgets are prepared on the basis of

assumptions therefore it is required for the manager to analyse the profit which may

generated in future relating to project activities (Ward, 2012). Set systematic information for budget to achieve objectives: The manager should need to

prepare budget for each department after collecting all necessary details from members

perform in such departments. Measurement of actual with standard: The manager need to compare the actual

performance with their desired or standard performance through using actual data and

estimated data.

Review stages: This is the last and final stage in budgetary control in which manager of

Zylla company need to review analyse and implement corrective measures if any changes

need to be done on order to get positive outcomes.

Planning tools used by manager:

To manage budget in effective and efficient manner there are certain various tools or

techniques which need to be used by Zylla company. Some tools are:

Operating Budget: It is related with determining cost and expenses which will be

incurred in manufacturing product and services (Quinn, 2014). It is prepared on weekly,

monthly, quarterly or yearly basis (Budgetary Control. 2017). It ensures the manager that which

area of department has large scope of work and accordingly allocate the amount of funds in

proportion. Through this the performance of manager can also be analysed and evaluated by

company.

Merits:

By preparing regular report on monthly, yearly basis, the company can achieve growth

and profitability.

Demerits:

As the information is based on the estimation therefore there is less chance of getting

more effective outcomes.

Static budget: Static budget which is also categorise by other name as fixed budget, is

prepared in beginning of project budget period and are completely different than actual.

Merits:

8

assumptions therefore it is required for the manager to analyse the profit which may

generated in future relating to project activities (Ward, 2012). Set systematic information for budget to achieve objectives: The manager should need to

prepare budget for each department after collecting all necessary details from members

perform in such departments. Measurement of actual with standard: The manager need to compare the actual

performance with their desired or standard performance through using actual data and

estimated data.

Review stages: This is the last and final stage in budgetary control in which manager of

Zylla company need to review analyse and implement corrective measures if any changes

need to be done on order to get positive outcomes.

Planning tools used by manager:

To manage budget in effective and efficient manner there are certain various tools or

techniques which need to be used by Zylla company. Some tools are:

Operating Budget: It is related with determining cost and expenses which will be

incurred in manufacturing product and services (Quinn, 2014). It is prepared on weekly,

monthly, quarterly or yearly basis (Budgetary Control. 2017). It ensures the manager that which

area of department has large scope of work and accordingly allocate the amount of funds in

proportion. Through this the performance of manager can also be analysed and evaluated by

company.

Merits:

By preparing regular report on monthly, yearly basis, the company can achieve growth

and profitability.

Demerits:

As the information is based on the estimation therefore there is less chance of getting

more effective outcomes.

Static budget: Static budget which is also categorise by other name as fixed budget, is

prepared in beginning of project budget period and are completely different than actual.

Merits:

8

As static budgets do not need to update regularly during accounting period therefore it is

easy to implement and follow.

It helps the company to control and monitor costs and make effective spending decisions.

Demerits:

Adverse impact on company's profitability because if company found underperforming

areas then it cannot allocate additional resources to help (Nixon and Burns, 2012). As static budgets are depend on the past data therefore company may face difficulties in

establishing and implementing them.

Cash budget: It is an estimation of cash inflow and outflow for successful operation of

business and its main objective is to assess whether the company have sufficient cash or funds to

operate or not. This budget guide the manager in determining the period of cash shortage and

thereafter taking corrective actions towards resolving such problems.

Merits:

It helps in reducing the cost and profit maximisation through concentrating on significant

matters of company.

It helps in enhancing better understanding and healthy relationship with the employees.

Demerits:

It is very expensive for company to operate a budget and may take longer time to achieve desired

objectives.

It can decreases the productivity and morale of employees if desired targets are not realistic.

Master budget: It is the sum of the total budget that company have and require to allocate

the funds to different activities of business (Herzig and et. al., 2012). This budget can be

developed through different factors such as sales, working capital, operating expenses etc.

Merits:

It helps in achieving estimated profit of an organisation and also provides material

information regarding forecast balance sheet.

Demerits:

It is difficult for the manager to determine how much portion of company's funds spend

on different departments on monthly basis.

9

easy to implement and follow.

It helps the company to control and monitor costs and make effective spending decisions.

Demerits:

Adverse impact on company's profitability because if company found underperforming

areas then it cannot allocate additional resources to help (Nixon and Burns, 2012). As static budgets are depend on the past data therefore company may face difficulties in

establishing and implementing them.

Cash budget: It is an estimation of cash inflow and outflow for successful operation of

business and its main objective is to assess whether the company have sufficient cash or funds to

operate or not. This budget guide the manager in determining the period of cash shortage and

thereafter taking corrective actions towards resolving such problems.

Merits:

It helps in reducing the cost and profit maximisation through concentrating on significant

matters of company.

It helps in enhancing better understanding and healthy relationship with the employees.

Demerits:

It is very expensive for company to operate a budget and may take longer time to achieve desired

objectives.

It can decreases the productivity and morale of employees if desired targets are not realistic.

Master budget: It is the sum of the total budget that company have and require to allocate

the funds to different activities of business (Herzig and et. al., 2012). This budget can be

developed through different factors such as sales, working capital, operating expenses etc.

Merits:

It helps in achieving estimated profit of an organisation and also provides material

information regarding forecast balance sheet.

Demerits:

It is difficult for the manager to determine how much portion of company's funds spend

on different departments on monthly basis.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.