Detailed Management Accounting Report Analysis for Zylla Company

VerifiedAdded on 2020/06/06

|14

|4373

|51

Report

AI Summary

This report provides a comprehensive overview of management accounting principles and their application within the context of Zylla Company, a multinational organization. It delves into various aspects of management accounting, including different types of accounting and their essential requirements. The report examines diverse costing approaches used to evaluate profitability, such as absorption costing and marginal costing, comparing their methodologies and impacts on financial outcomes. Furthermore, it explores the use of planning tools in budgetary control, crucial for financial problem-solving. The report also includes a comparative analysis with another business to address financial issues. The introduction defines management accounting and highlights its importance for accurate financial reporting and decision-making. The report emphasizes the role of accounting systems in managing inventory, optimizing prices, and determining batch sizes. It also covers different reporting systems like operating budgets and performance reporting. Overall, the report provides a detailed examination of accounting systems that support sound financial decision-making, with the goal of improving company sustainability and profitability.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Different kinds of management accounting and essential requirements of their different

types........................................................................................................................................1

P2. Different approaches of management accounting reporting............................................2

TASK 2............................................................................................................................................4

P3 Various costing approach used to evaluate profitability...................................................4

TASK 3............................................................................................................................................6

P4. Planning tool use in budgetary control.............................................................................6

TASK 4............................................................................................................................................9

P5 Comparison with another business's with purpose to solve financial issue......................9

CONCLUSION .............................................................................................................................10

REFERENCES..............................................................................................................................11

.......................................................................................................................................................12

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Different kinds of management accounting and essential requirements of their different

types........................................................................................................................................1

P2. Different approaches of management accounting reporting............................................2

TASK 2............................................................................................................................................4

P3 Various costing approach used to evaluate profitability...................................................4

TASK 3............................................................................................................................................6

P4. Planning tool use in budgetary control.............................................................................6

TASK 4............................................................................................................................................9

P5 Comparison with another business's with purpose to solve financial issue......................9

CONCLUSION .............................................................................................................................10

REFERENCES..............................................................................................................................11

.......................................................................................................................................................12

INTRODUCTION

Management accounting is a procedure of preparing accounts and reports that provide

proper and timely statistical as well as timely information. It is required by business managers in

order to make short term judgement in an accurate manner. Manager use accounting information

related to the provision which controls all the functions of business enterprise. These reports

mainly display the amount of present cash, outstanding debts, inventory, raw material and other

aspects (Bodie and et. al, 2014). Accounting is defined as a systematic recording, monitoring and

summarising of financial records and entries.

This project is based on Zylla Company which is a large multinational organisation. This

report consists of several tasks which lay on different accounting reports and systems. It will also

determine about the costing approach with an aim of evaluating business profitability. With the

use budgetary control, planning tools is very important to support in controlling all financial

problems. Overall, file is based on accounting system that helps in taking an accurate and

effective judgement regarding company’s sustainability in the future.

TASK 1

P1. Different kinds of management accounting and essential requirements of their different types

Management accounting is a approach which includes all those elements that are

beneficial for the financial department. They can support top level administration as well as other

departments in the execution and policy execution. Management is the main part of each and

every enterprise that is related with first task of controlling, executing and designing operational

activities of business. In order to make an impressive judgement, accounting information is

required and on the basis of same, position of firm is decided. In this accurate data is usually

right which output is uncertainty of fallible in decreased.

Management accounting is a beneficial part of the business that plays an essential role in

order to provide right direction to them. So, in this, business possibility of getting large number

of growth and profit of company (Burritt and et. al., 2011). In regards to evaluating Zylla

company performance, critical judgement are build to decrease its additional expenses and cost.

It is defined that scope & nature of accounting method is essential as well as wide due to its

correctiveness and accuracy. Aim and purpose of business managers in order to make accurate

financial report & entries so that objectives and aim can be achieved in an effective manner. In

1

Management accounting is a procedure of preparing accounts and reports that provide

proper and timely statistical as well as timely information. It is required by business managers in

order to make short term judgement in an accurate manner. Manager use accounting information

related to the provision which controls all the functions of business enterprise. These reports

mainly display the amount of present cash, outstanding debts, inventory, raw material and other

aspects (Bodie and et. al, 2014). Accounting is defined as a systematic recording, monitoring and

summarising of financial records and entries.

This project is based on Zylla Company which is a large multinational organisation. This

report consists of several tasks which lay on different accounting reports and systems. It will also

determine about the costing approach with an aim of evaluating business profitability. With the

use budgetary control, planning tools is very important to support in controlling all financial

problems. Overall, file is based on accounting system that helps in taking an accurate and

effective judgement regarding company’s sustainability in the future.

TASK 1

P1. Different kinds of management accounting and essential requirements of their different types

Management accounting is a approach which includes all those elements that are

beneficial for the financial department. They can support top level administration as well as other

departments in the execution and policy execution. Management is the main part of each and

every enterprise that is related with first task of controlling, executing and designing operational

activities of business. In order to make an impressive judgement, accounting information is

required and on the basis of same, position of firm is decided. In this accurate data is usually

right which output is uncertainty of fallible in decreased.

Management accounting is a beneficial part of the business that plays an essential role in

order to provide right direction to them. So, in this, business possibility of getting large number

of growth and profit of company (Burritt and et. al., 2011). In regards to evaluating Zylla

company performance, critical judgement are build to decrease its additional expenses and cost.

It is defined that scope & nature of accounting method is essential as well as wide due to its

correctiveness and accuracy. Aim and purpose of business managers in order to make accurate

financial report & entries so that objectives and aim can be achieved in an effective manner. In

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the case performance of the firm is impacting, so in this managers using various methods to

record business & financial transaction. Some kinds of accounting methods that can be essential

and supportive in monitoring business operations in an accurate manner. All these are

determined as:

Cost accounting: It is used by business organisation with an aim of evaluating cost that

firm is sustaining in their process of production. Main purpose of using this approach is to

identify the cost control, profitability and different parts related to costs which are obtained over

various activities. At the production point, project handler uses different aspects in costs like

standard, actual and normal cost.

Inventory management: It is an accounting system which is very effective in monitoring

closing and opening stocks (Cadez and Guilding, 2012). It is a big problem for the employer in

order to manage its inventory without having an accurate approach. For determining the stock

position, they can use stock turnover and ABC costing aspects.

Price optimisation: It is known as a systematic approach which helps business in

identifying the appropriate price. This aspect is supportive and beneficial in determining which

value is very much affordable for buyers for their commodities. It is used by Zylla with regard to

identify the profitability of them as well as create large chances for acquiring effective outputs in

quick period.

Job costing: Main purpose of using this approach is to determine batch size of products

and services manufacturing in the year. This aspect considers product date, number of

identification and quality of commodity.

P2. Different approaches of management accounting reporting

Reporting is defined as a financial transaction position in the accounts book. So, in this

way, final statements of business organisation can be built in an accurate and systematic manner.

It will include different necessary information linked with business operations . All data and

collection must be relevant before conveying into the statements. In this situation, upper level

management makes their own judgement through evaluating such entries in order to present and

give it to investors at the time (DRURY, 2013). So, it is a critical form of corporate governance.

Financial statements include cash-flows, income statements and balance sheet in order to pertain

regular transactions of company.

2

record business & financial transaction. Some kinds of accounting methods that can be essential

and supportive in monitoring business operations in an accurate manner. All these are

determined as:

Cost accounting: It is used by business organisation with an aim of evaluating cost that

firm is sustaining in their process of production. Main purpose of using this approach is to

identify the cost control, profitability and different parts related to costs which are obtained over

various activities. At the production point, project handler uses different aspects in costs like

standard, actual and normal cost.

Inventory management: It is an accounting system which is very effective in monitoring

closing and opening stocks (Cadez and Guilding, 2012). It is a big problem for the employer in

order to manage its inventory without having an accurate approach. For determining the stock

position, they can use stock turnover and ABC costing aspects.

Price optimisation: It is known as a systematic approach which helps business in

identifying the appropriate price. This aspect is supportive and beneficial in determining which

value is very much affordable for buyers for their commodities. It is used by Zylla with regard to

identify the profitability of them as well as create large chances for acquiring effective outputs in

quick period.

Job costing: Main purpose of using this approach is to determine batch size of products

and services manufacturing in the year. This aspect considers product date, number of

identification and quality of commodity.

P2. Different approaches of management accounting reporting

Reporting is defined as a financial transaction position in the accounts book. So, in this

way, final statements of business organisation can be built in an accurate and systematic manner.

It will include different necessary information linked with business operations . All data and

collection must be relevant before conveying into the statements. In this situation, upper level

management makes their own judgement through evaluating such entries in order to present and

give it to investors at the time (DRURY, 2013). So, it is a critical form of corporate governance.

Financial statements include cash-flows, income statements and balance sheet in order to pertain

regular transactions of company.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Main aim of using this report is to control and evaluate wastage of business organisation.

Which is complete in the unnecessary expenses and cost forms. In this situation investors and

administration can take future judgement on the report basis, it is formulated by accounts

division. After devising such report overlook is necessary and essential for making investment

plans decision. It will supportive and important for formatting performance appraisal & analysis

for group members as well as organisation. The sources of information and data gathered is non-

financial & financial. It will be collect from different division who are working in the enterprise

with the aim of achieving common interest (Fourie and et. al., 2015). There are several system

of reporting which is followed by Zylla managers, these are determined under this:

Operating budget: It is an accounting reporting system which is related with production process,

it is covers all expenditures and income which incur by business entity in the year. Main

objectives of applying this approach is to identify real price which is complete by firm over the

goods productions. So it is known as internal reporting which is beneficial for the production

department.

Performance reporting: This report considers the valuable and essential information about the

current and past year performance of the company which is use into consideration. So it is

support managers in order to evaluate a logical element where an accurate result can be given

regarding its effectiveness and performances.

Account receivable again report: It is also a essential part of the reporting which is beneficial

for the non-paying customers invoice as well as uncredited bills (Frezatti and et. al., 2011). Main

purpose of using this systems is to determine recovery period of due price.

Therefore, Management accounting approach is very essential and beneficial part of the

financial department in order to identify income and expenditure of the business. In this way,

business manager can safeguard and handle its financial statements. It will support in making

positive results with the present resources. In regrades to built more chances of receiving

revenues they require to use different system of accounting such as job costing, price

optimisation and other essential aspects which is impressive for the organisation. Main benefits

of using such kind of approach is to maximise business efficiency and effectiveness in a

systematic manner. Zylla enterprise is very much dependable for making their sustainability in

upcoming time. It is a reporting part which is linked with costs of production unites such as

overhead, raw material and labour etc. Main aim of using this, is to tract real value which is

3

Which is complete in the unnecessary expenses and cost forms. In this situation investors and

administration can take future judgement on the report basis, it is formulated by accounts

division. After devising such report overlook is necessary and essential for making investment

plans decision. It will supportive and important for formatting performance appraisal & analysis

for group members as well as organisation. The sources of information and data gathered is non-

financial & financial. It will be collect from different division who are working in the enterprise

with the aim of achieving common interest (Fourie and et. al., 2015). There are several system

of reporting which is followed by Zylla managers, these are determined under this:

Operating budget: It is an accounting reporting system which is related with production process,

it is covers all expenditures and income which incur by business entity in the year. Main

objectives of applying this approach is to identify real price which is complete by firm over the

goods productions. So it is known as internal reporting which is beneficial for the production

department.

Performance reporting: This report considers the valuable and essential information about the

current and past year performance of the company which is use into consideration. So it is

support managers in order to evaluate a logical element where an accurate result can be given

regarding its effectiveness and performances.

Account receivable again report: It is also a essential part of the reporting which is beneficial

for the non-paying customers invoice as well as uncredited bills (Frezatti and et. al., 2011). Main

purpose of using this systems is to determine recovery period of due price.

Therefore, Management accounting approach is very essential and beneficial part of the

financial department in order to identify income and expenditure of the business. In this way,

business manager can safeguard and handle its financial statements. It will support in making

positive results with the present resources. In regrades to built more chances of receiving

revenues they require to use different system of accounting such as job costing, price

optimisation and other essential aspects which is impressive for the organisation. Main benefits

of using such kind of approach is to maximise business efficiency and effectiveness in a

systematic manner. Zylla enterprise is very much dependable for making their sustainability in

upcoming time. It is a reporting part which is linked with costs of production unites such as

overhead, raw material and labour etc. Main aim of using this, is to tract real value which is

3

charged on particular job as well as analysis them effectively and efficiently. Output of these is

to minimised cost. Reporting approach is beneficial for the firm for procuring positive outputs

with the present factors.

It can support them in order to evaluate financial transaction which result is maximised

profit. Main aim of using such methods is to analysis performance, growth, success and

sustainability of the company. It can be described by using necessary information and data

regarding future and current year performance. So in this, accurate plan can be evaluate

regarding Zylla company performance and efficiency. Main objectives of using these approach is

to taking investment idea in there future projects and tasks. Accounts receivable as well as

performance document are essential tools of reporting.

TASK 2

P3 Various costing approach used to evaluate profitability

Costing is an essential part which is used by business organisation with the purpose of

analysing total costs. It is invested on producing services and commodities to the clients in a

systematic manner. It is related either indirectly and directly with production price such as

overheads, labour and material etc. Company use this aspects in order to measuring monitory

value which is called as summary of resources (Fullerton and et. al., 2014). It is use by

administrator in regards to build accurate products transfer to its buyers. Such kind of costs are

impressive in process of judgement making which is given reliable and correct information

regarding actual values charge by the business entity (Zimmerman and Yahya-Zadeh, 2011).

There are some kind of costing approaches which is suitable and valuable for firm in regards to

evaluate net profits.

Absorption costing: It is a part of costing approach which the firm incurs in the production of an

additional units. Into the consideration, fixed cost contribution does not includes in this

approach.

Marginal costing: It is a part of cost which follow by business in the production process. It is

never includes fixed costs as per contribution unit.

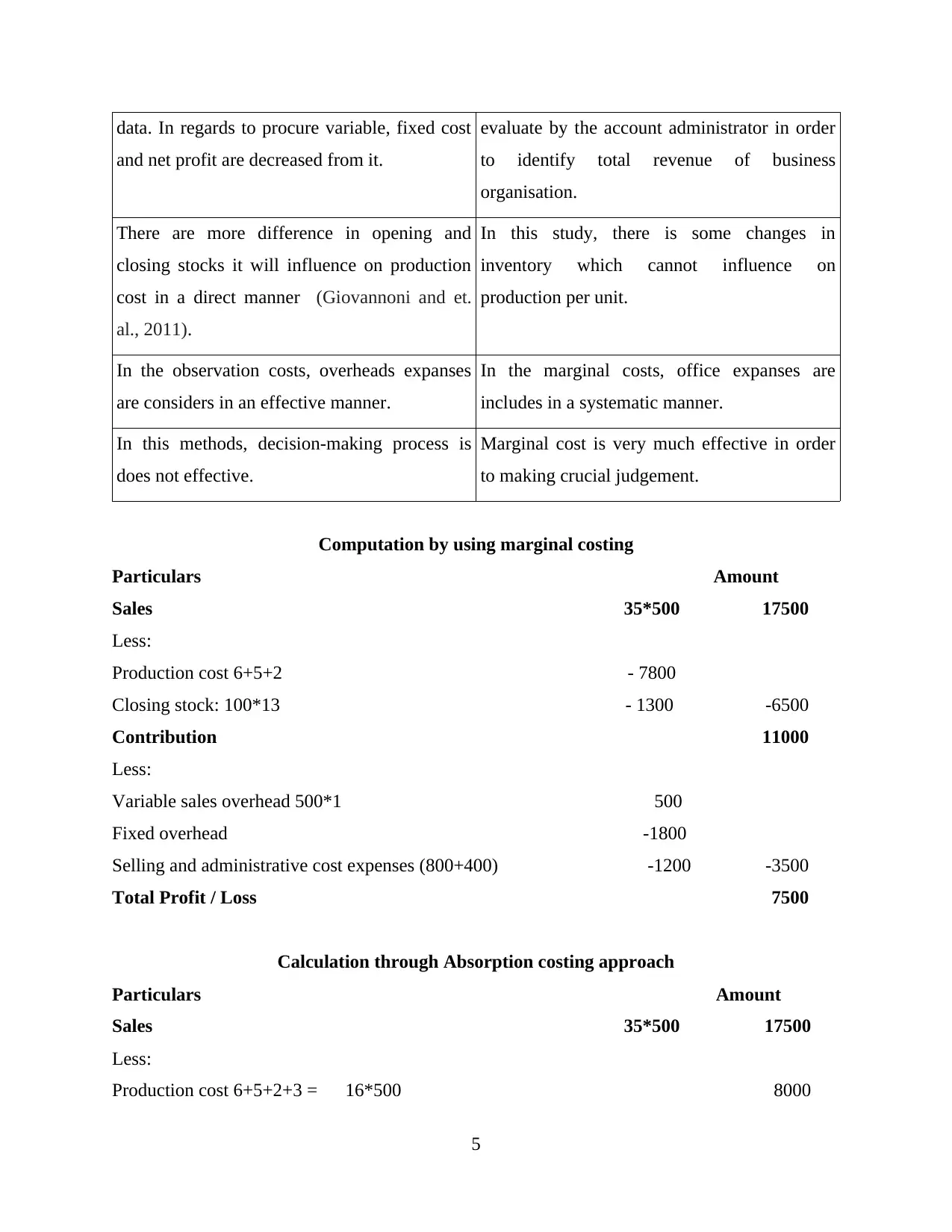

Difference between Marginal and Absorption costing

Absorption costing Marginal costing

This approach presented cost information and Calculation of per units contribution which is

4

to minimised cost. Reporting approach is beneficial for the firm for procuring positive outputs

with the present factors.

It can support them in order to evaluate financial transaction which result is maximised

profit. Main aim of using such methods is to analysis performance, growth, success and

sustainability of the company. It can be described by using necessary information and data

regarding future and current year performance. So in this, accurate plan can be evaluate

regarding Zylla company performance and efficiency. Main objectives of using these approach is

to taking investment idea in there future projects and tasks. Accounts receivable as well as

performance document are essential tools of reporting.

TASK 2

P3 Various costing approach used to evaluate profitability

Costing is an essential part which is used by business organisation with the purpose of

analysing total costs. It is invested on producing services and commodities to the clients in a

systematic manner. It is related either indirectly and directly with production price such as

overheads, labour and material etc. Company use this aspects in order to measuring monitory

value which is called as summary of resources (Fullerton and et. al., 2014). It is use by

administrator in regards to build accurate products transfer to its buyers. Such kind of costs are

impressive in process of judgement making which is given reliable and correct information

regarding actual values charge by the business entity (Zimmerman and Yahya-Zadeh, 2011).

There are some kind of costing approaches which is suitable and valuable for firm in regards to

evaluate net profits.

Absorption costing: It is a part of costing approach which the firm incurs in the production of an

additional units. Into the consideration, fixed cost contribution does not includes in this

approach.

Marginal costing: It is a part of cost which follow by business in the production process. It is

never includes fixed costs as per contribution unit.

Difference between Marginal and Absorption costing

Absorption costing Marginal costing

This approach presented cost information and Calculation of per units contribution which is

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

data. In regards to procure variable, fixed cost

and net profit are decreased from it.

evaluate by the account administrator in order

to identify total revenue of business

organisation.

There are more difference in opening and

closing stocks it will influence on production

cost in a direct manner (Giovannoni and et.

al., 2011).

In this study, there is some changes in

inventory which cannot influence on

production per unit.

In the observation costs, overheads expanses

are considers in an effective manner.

In the marginal costs, office expanses are

includes in a systematic manner.

In this methods, decision-making process is

does not effective.

Marginal cost is very much effective in order

to making crucial judgement.

Computation by using marginal costing

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2 - 7800

Closing stock: 100*13 - 1300 -6500

Contribution 11000

Less:

Variable sales overhead 500*1 500

Fixed overhead -1800

Selling and administrative cost expenses (800+400) -1200 -3500

Total Profit / Loss 7500

Calculation through Absorption costing approach

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2+3 = 16*500 8000

5

and net profit are decreased from it.

evaluate by the account administrator in order

to identify total revenue of business

organisation.

There are more difference in opening and

closing stocks it will influence on production

cost in a direct manner (Giovannoni and et.

al., 2011).

In this study, there is some changes in

inventory which cannot influence on

production per unit.

In the observation costs, overheads expanses

are considers in an effective manner.

In the marginal costs, office expanses are

includes in a systematic manner.

In this methods, decision-making process is

does not effective.

Marginal cost is very much effective in order

to making crucial judgement.

Computation by using marginal costing

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2 - 7800

Closing stock: 100*13 - 1300 -6500

Contribution 11000

Less:

Variable sales overhead 500*1 500

Fixed overhead -1800

Selling and administrative cost expenses (800+400) -1200 -3500

Total Profit / Loss 7500

Calculation through Absorption costing approach

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2+3 = 16*500 8000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

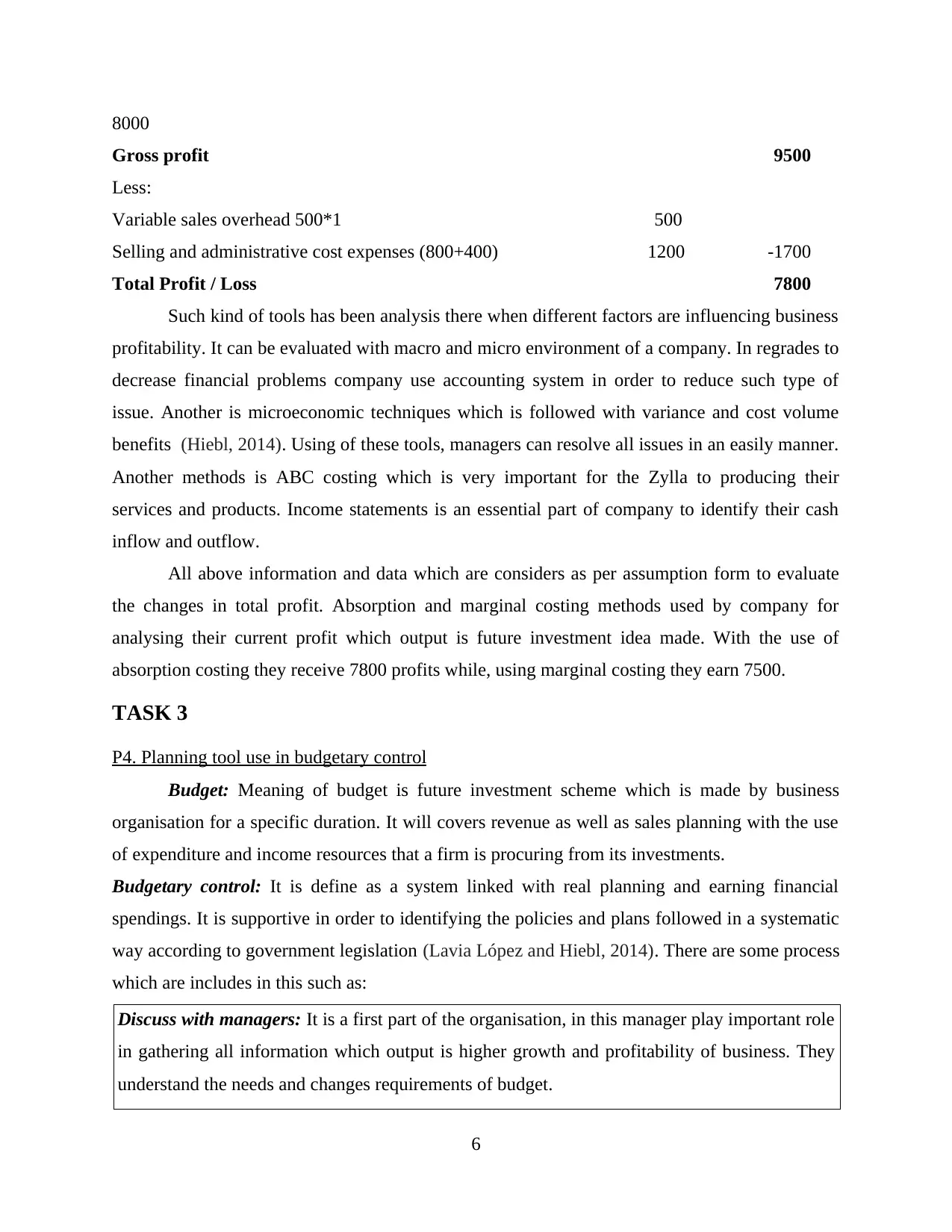

8000

Gross profit 9500

Less:

Variable sales overhead 500*1 500

Selling and administrative cost expenses (800+400) 1200 -1700

Total Profit / Loss 7800

Such kind of tools has been analysis there when different factors are influencing business

profitability. It can be evaluated with macro and micro environment of a company. In regrades to

decrease financial problems company use accounting system in order to reduce such type of

issue. Another is microeconomic techniques which is followed with variance and cost volume

benefits (Hiebl, 2014). Using of these tools, managers can resolve all issues in an easily manner.

Another methods is ABC costing which is very important for the Zylla to producing their

services and products. Income statements is an essential part of company to identify their cash

inflow and outflow.

All above information and data which are considers as per assumption form to evaluate

the changes in total profit. Absorption and marginal costing methods used by company for

analysing their current profit which output is future investment idea made. With the use of

absorption costing they receive 7800 profits while, using marginal costing they earn 7500.

TASK 3

P4. Planning tool use in budgetary control

Budget: Meaning of budget is future investment scheme which is made by business

organisation for a specific duration. It will covers revenue as well as sales planning with the use

of expenditure and income resources that a firm is procuring from its investments.

Budgetary control: It is define as a system linked with real planning and earning financial

spendings. It is supportive in order to identifying the policies and plans followed in a systematic

way according to government legislation (Lavia López and Hiebl, 2014). There are some process

which are includes in this such as:

Discuss with managers: It is a first part of the organisation, in this manager play important role

in gathering all information which output is higher growth and profitability of business. They

understand the needs and changes requirements of budget.

6

Gross profit 9500

Less:

Variable sales overhead 500*1 500

Selling and administrative cost expenses (800+400) 1200 -1700

Total Profit / Loss 7800

Such kind of tools has been analysis there when different factors are influencing business

profitability. It can be evaluated with macro and micro environment of a company. In regrades to

decrease financial problems company use accounting system in order to reduce such type of

issue. Another is microeconomic techniques which is followed with variance and cost volume

benefits (Hiebl, 2014). Using of these tools, managers can resolve all issues in an easily manner.

Another methods is ABC costing which is very important for the Zylla to producing their

services and products. Income statements is an essential part of company to identify their cash

inflow and outflow.

All above information and data which are considers as per assumption form to evaluate

the changes in total profit. Absorption and marginal costing methods used by company for

analysing their current profit which output is future investment idea made. With the use of

absorption costing they receive 7800 profits while, using marginal costing they earn 7500.

TASK 3

P4. Planning tool use in budgetary control

Budget: Meaning of budget is future investment scheme which is made by business

organisation for a specific duration. It will covers revenue as well as sales planning with the use

of expenditure and income resources that a firm is procuring from its investments.

Budgetary control: It is define as a system linked with real planning and earning financial

spendings. It is supportive in order to identifying the policies and plans followed in a systematic

way according to government legislation (Lavia López and Hiebl, 2014). There are some process

which are includes in this such as:

Discuss with managers: It is a first part of the organisation, in this manager play important role

in gathering all information which output is higher growth and profitability of business. They

understand the needs and changes requirements of budget.

6

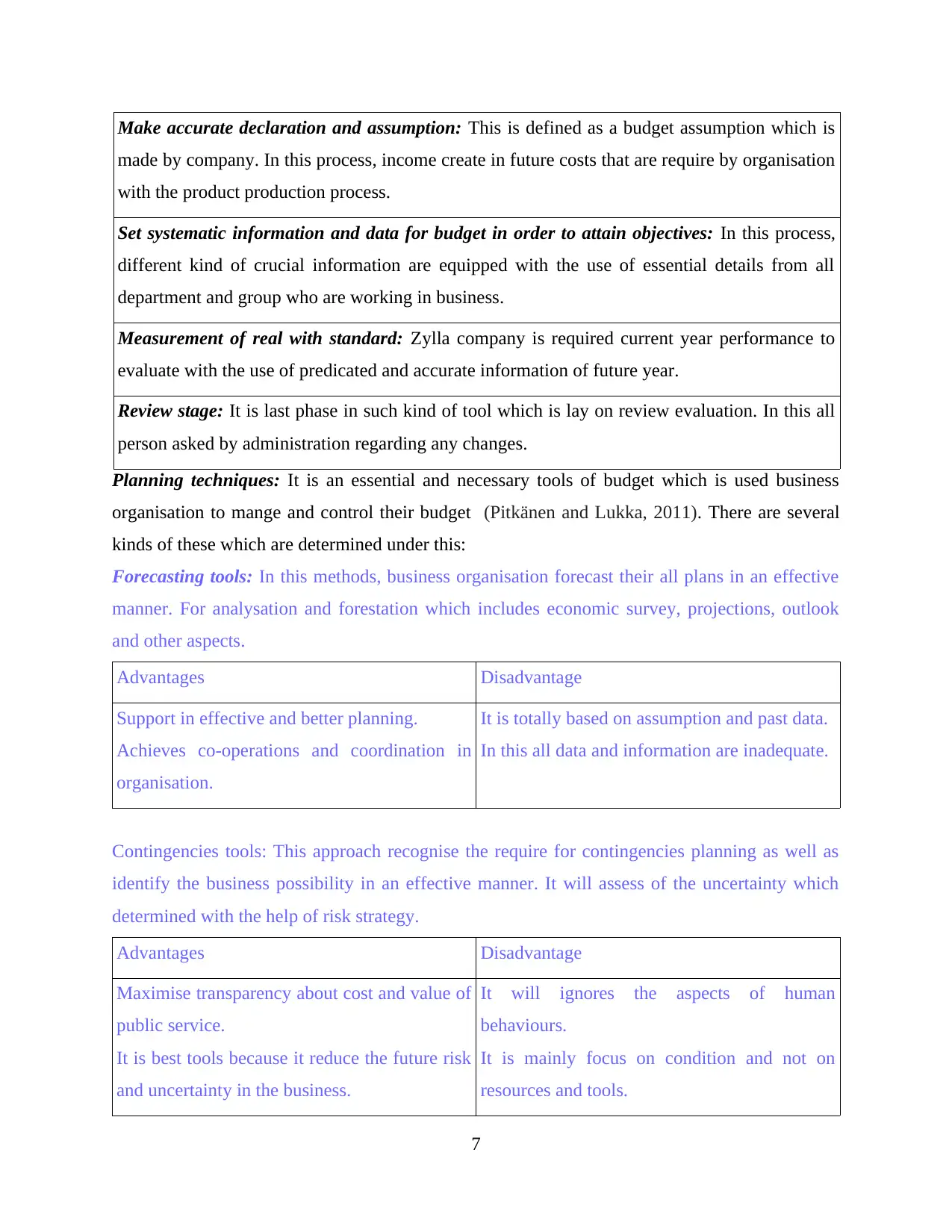

Make accurate declaration and assumption: This is defined as a budget assumption which is

made by company. In this process, income create in future costs that are require by organisation

with the product production process.

Set systematic information and data for budget in order to attain objectives: In this process,

different kind of crucial information are equipped with the use of essential details from all

department and group who are working in business.

Measurement of real with standard: Zylla company is required current year performance to

evaluate with the use of predicated and accurate information of future year.

Review stage: It is last phase in such kind of tool which is lay on review evaluation. In this all

person asked by administration regarding any changes.

Planning techniques: It is an essential and necessary tools of budget which is used business

organisation to mange and control their budget (Pitkänen and Lukka, 2011). There are several

kinds of these which are determined under this:

Forecasting tools: In this methods, business organisation forecast their all plans in an effective

manner. For analysation and forestation which includes economic survey, projections, outlook

and other aspects.

Advantages Disadvantage

Support in effective and better planning.

Achieves co-operations and coordination in

organisation.

It is totally based on assumption and past data.

In this all data and information are inadequate.

Contingencies tools: This approach recognise the require for contingencies planning as well as

identify the business possibility in an effective manner. It will assess of the uncertainty which

determined with the help of risk strategy.

Advantages Disadvantage

Maximise transparency about cost and value of

public service.

It is best tools because it reduce the future risk

and uncertainty in the business.

It will ignores the aspects of human

behaviours.

It is mainly focus on condition and not on

resources and tools.

7

made by company. In this process, income create in future costs that are require by organisation

with the product production process.

Set systematic information and data for budget in order to attain objectives: In this process,

different kind of crucial information are equipped with the use of essential details from all

department and group who are working in business.

Measurement of real with standard: Zylla company is required current year performance to

evaluate with the use of predicated and accurate information of future year.

Review stage: It is last phase in such kind of tool which is lay on review evaluation. In this all

person asked by administration regarding any changes.

Planning techniques: It is an essential and necessary tools of budget which is used business

organisation to mange and control their budget (Pitkänen and Lukka, 2011). There are several

kinds of these which are determined under this:

Forecasting tools: In this methods, business organisation forecast their all plans in an effective

manner. For analysation and forestation which includes economic survey, projections, outlook

and other aspects.

Advantages Disadvantage

Support in effective and better planning.

Achieves co-operations and coordination in

organisation.

It is totally based on assumption and past data.

In this all data and information are inadequate.

Contingencies tools: This approach recognise the require for contingencies planning as well as

identify the business possibility in an effective manner. It will assess of the uncertainty which

determined with the help of risk strategy.

Advantages Disadvantage

Maximise transparency about cost and value of

public service.

It is best tools because it reduce the future risk

and uncertainty in the business.

It will ignores the aspects of human

behaviours.

It is mainly focus on condition and not on

resources and tools.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

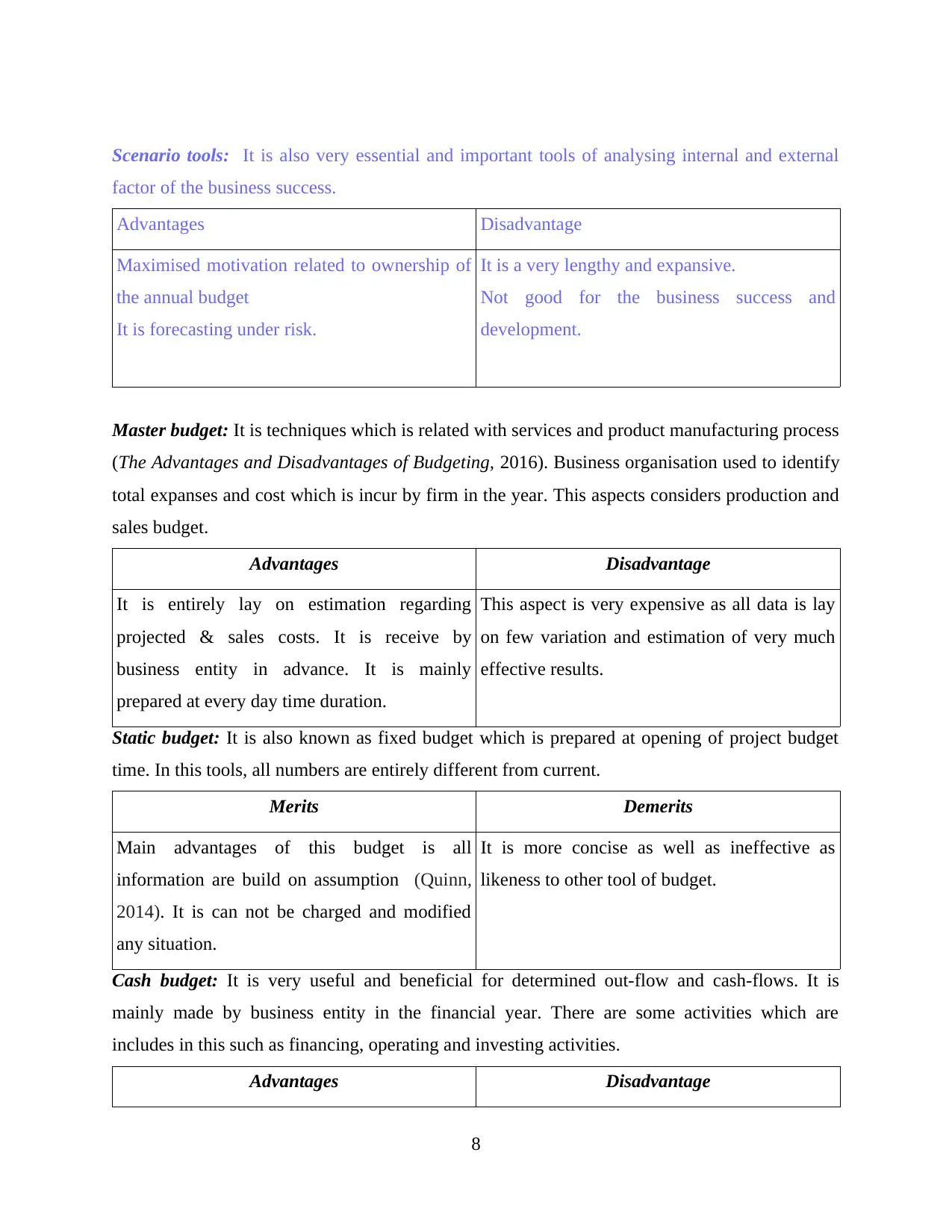

Scenario tools: It is also very essential and important tools of analysing internal and external

factor of the business success.

Advantages Disadvantage

Maximised motivation related to ownership of

the annual budget

It is forecasting under risk.

It is a very lengthy and expansive.

Not good for the business success and

development.

Master budget: It is techniques which is related with services and product manufacturing process

(The Advantages and Disadvantages of Budgeting, 2016). Business organisation used to identify

total expanses and cost which is incur by firm in the year. This aspects considers production and

sales budget.

Advantages Disadvantage

It is entirely lay on estimation regarding

projected & sales costs. It is receive by

business entity in advance. It is mainly

prepared at every day time duration.

This aspect is very expensive as all data is lay

on few variation and estimation of very much

effective results.

Static budget: It is also known as fixed budget which is prepared at opening of project budget

time. In this tools, all numbers are entirely different from current.

Merits Demerits

Main advantages of this budget is all

information are build on assumption (Quinn,

2014). It is can not be charged and modified

any situation.

It is more concise as well as ineffective as

likeness to other tool of budget.

Cash budget: It is very useful and beneficial for determined out-flow and cash-flows. It is

mainly made by business entity in the financial year. There are some activities which are

includes in this such as financing, operating and investing activities.

Advantages Disadvantage

8

factor of the business success.

Advantages Disadvantage

Maximised motivation related to ownership of

the annual budget

It is forecasting under risk.

It is a very lengthy and expansive.

Not good for the business success and

development.

Master budget: It is techniques which is related with services and product manufacturing process

(The Advantages and Disadvantages of Budgeting, 2016). Business organisation used to identify

total expanses and cost which is incur by firm in the year. This aspects considers production and

sales budget.

Advantages Disadvantage

It is entirely lay on estimation regarding

projected & sales costs. It is receive by

business entity in advance. It is mainly

prepared at every day time duration.

This aspect is very expensive as all data is lay

on few variation and estimation of very much

effective results.

Static budget: It is also known as fixed budget which is prepared at opening of project budget

time. In this tools, all numbers are entirely different from current.

Merits Demerits

Main advantages of this budget is all

information are build on assumption (Quinn,

2014). It is can not be charged and modified

any situation.

It is more concise as well as ineffective as

likeness to other tool of budget.

Cash budget: It is very useful and beneficial for determined out-flow and cash-flows. It is

mainly made by business entity in the financial year. There are some activities which are

includes in this such as financing, operating and investing activities.

Advantages Disadvantage

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

This budget support business in order to

evaluate net profit which is incurred by firm

from its different activities. It is identify by

company with the use of these budget in an

essential manner.

Main demerits of this budget disregard cash-

flows. So in this investment recovery time will

be fulfilled.

Therefore, In order to procure accurate and correct data, business may use different kinds

of budget tools. So planning techniques is more beneficial to observe business information

regarding financial situation (Renz, 2016). Operating budget, is another tool which is used by

company in order to see total expanses and costs in the year. For development of organisation

performance, all financial tools are require in a specific and systematic manner. In this chance

and new opportunities plenty are procuring in an accurate outputs. It is use where, there different

financial problems are available. It will make large effect on company profitability ratio. It is

define the duty of managers in order to analysis all problems and make better process to reduce

difficulties.

TASK 4

P5 Comparison with another business's with purpose to solve financial issue

In each and every enterprise are observed financial problems that can influence on

organisation growth and productivity in direct way. Main aim of the manager is to accurate plan

with the purpose of achieving long term objectives and profitability. It will impacted business

performance and its profitability at large. There are also several issues such as short duration

liabilities, lack of financial aspects and cash inability (Schaltegger and et. al., 2013). There are

several kinds of tools which has been reduce all issues in a systematic manner are as follows:

KPI: It is known as Key performance indicators which is very important and essential

techniques. It is used by company with the purpose of reducing all financial problem. Main aim

of using this approach is to evaluate organisation and team performance in the year.

Financial governance: This aspects is made by legal authorities which is followed by each and

every organisation. It will support them in order to analysis stability as well as durability of firm

in the past. It is very essential tools that control all financial risk in the business. In this all

transaction related to the company profit and loss account, balance sheet and other.

9

evaluate net profit which is incurred by firm

from its different activities. It is identify by

company with the use of these budget in an

essential manner.

Main demerits of this budget disregard cash-

flows. So in this investment recovery time will

be fulfilled.

Therefore, In order to procure accurate and correct data, business may use different kinds

of budget tools. So planning techniques is more beneficial to observe business information

regarding financial situation (Renz, 2016). Operating budget, is another tool which is used by

company in order to see total expanses and costs in the year. For development of organisation

performance, all financial tools are require in a specific and systematic manner. In this chance

and new opportunities plenty are procuring in an accurate outputs. It is use where, there different

financial problems are available. It will make large effect on company profitability ratio. It is

define the duty of managers in order to analysis all problems and make better process to reduce

difficulties.

TASK 4

P5 Comparison with another business's with purpose to solve financial issue

In each and every enterprise are observed financial problems that can influence on

organisation growth and productivity in direct way. Main aim of the manager is to accurate plan

with the purpose of achieving long term objectives and profitability. It will impacted business

performance and its profitability at large. There are also several issues such as short duration

liabilities, lack of financial aspects and cash inability (Schaltegger and et. al., 2013). There are

several kinds of tools which has been reduce all issues in a systematic manner are as follows:

KPI: It is known as Key performance indicators which is very important and essential

techniques. It is used by company with the purpose of reducing all financial problem. Main aim

of using this approach is to evaluate organisation and team performance in the year.

Financial governance: This aspects is made by legal authorities which is followed by each and

every organisation. It will support them in order to analysis stability as well as durability of firm

in the past. It is very essential tools that control all financial risk in the business. In this all

transaction related to the company profit and loss account, balance sheet and other.

9

Such kind of company is small business organisation which is dealing in electronic

equipments. In a middle level, 4com is operating in successfully. With the use of Key

performance indicators, they can easily analysis team and business performance. Another is Such

kind of company is a big organisation which dealing in multiple products. They required to have

accurate and effective system of accounting, with the help of these tool they can easily handle

their regular expanses. They use benchmarking and financial governance with the aim of

reducing financial problems. Such type of issue is identify the each and every organisation, so in

this situation they use accurate accounting methods to reduce these issue. It will make large

effects on company profitability and growth (Vosselman, 2014). In order to control entire

financial difficulties, business entity use various approaches which is profitable from acquiring

hamper. In this situation, business entity can achieve positive results, in this they adopt outdated

approach. With the use of key performance indicators & financial governance, firm can manger

their regular risk in a systematic manner.

CONCLUSION

As per the above mentioned report, it can be determined that management accounting is

important apart of the each and every organisation. With the help of these tools is to monitor

financial transactions in an effective manner. This study gives necessary and essential

information regarding different accounting approach as well as reporting tool. All those are more

valuable and beneficial for crucial judgement. Several tools and techniques are determined by the

company with the aim of achieving higher profitability and growth. Business organisation also

use planning methods which is used them in budgetary process. These tool give the accurate

information to firm in regrades to solve all financial problems.

10

equipments. In a middle level, 4com is operating in successfully. With the use of Key

performance indicators, they can easily analysis team and business performance. Another is Such

kind of company is a big organisation which dealing in multiple products. They required to have

accurate and effective system of accounting, with the help of these tool they can easily handle

their regular expanses. They use benchmarking and financial governance with the aim of

reducing financial problems. Such type of issue is identify the each and every organisation, so in

this situation they use accurate accounting methods to reduce these issue. It will make large

effects on company profitability and growth (Vosselman, 2014). In order to control entire

financial difficulties, business entity use various approaches which is profitable from acquiring

hamper. In this situation, business entity can achieve positive results, in this they adopt outdated

approach. With the use of key performance indicators & financial governance, firm can manger

their regular risk in a systematic manner.

CONCLUSION

As per the above mentioned report, it can be determined that management accounting is

important apart of the each and every organisation. With the help of these tools is to monitor

financial transactions in an effective manner. This study gives necessary and essential

information regarding different accounting approach as well as reporting tool. All those are more

valuable and beneficial for crucial judgement. Several tools and techniques are determined by the

company with the aim of achieving higher profitability and growth. Business organisation also

use planning methods which is used them in budgetary process. These tool give the accurate

information to firm in regrades to solve all financial problems.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.