Zylla Company: Management Accounting System and Analysis Report

VerifiedAdded on 2020/06/06

|15

|4843

|84

Report

AI Summary

This report provides a comprehensive analysis of the management accounting system employed by Zylla Company, a small to medium-sized retail entity. It explores various management accounting tools, including traditional accounting, cost accounting, and inventory management, emphasizing their role in gaining a competitive advantage. The report details specific tools like absorption costing, marginal costing, and budgetary controls, highlighting their application in maximizing profits and making effective decisions. Furthermore, it examines the merits of implementing management accounting systems, the use of planning tools, and the application of management accounting in responding to financial problems. The report underscores the importance of these tools in improving the company's performance and achieving its pre-set targets. It also includes discussions on cost reports, budget reports, and performance reports, providing insights into how Zylla Company utilizes these reports for internal decision-making and financial planning. The report concludes by emphasizing the significance of management accounting in ensuring sustainable development and achieving financial goals.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

FROM: MANAGEMENT ACCOUNTING OFFICER..................................................................1

TO,...................................................................................................................................................1

GENERAL MANAGER..................................................................................................................1

ZYLLA COMPANY.......................................................................................................................1

SUB: MANAGEMENT ACCOUNTING SYSTEM......................................................................1

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting tools and its various essential and its different types:...............1

P2. Various methods used by the management accounting officer for management accounting

reporting:................................................................................................................................3

M1: Merits of implementing accounting:...............................................................................4

P3 Net profits as per absorption costing and marginal costing:.............................................5

M2:.........................................................................................................................................6

D2:..........................................................................................................................................6

TASK 3............................................................................................................................................7

P4. Use of planning tools in the budgetary controls:..............................................................7

M3:.........................................................................................................................................8

D3:..........................................................................................................................................9

TASK 4............................................................................................................................................9

P5 Management accounting systems to respond financial problems.....................................1

M4:.........................................................................................................................................2

CONCLUSION................................................................................................................................2

REFERENCES................................................................................................................................3

FROM: MANAGEMENT ACCOUNTING OFFICER..................................................................1

TO,...................................................................................................................................................1

GENERAL MANAGER..................................................................................................................1

ZYLLA COMPANY.......................................................................................................................1

SUB: MANAGEMENT ACCOUNTING SYSTEM......................................................................1

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1 Management accounting tools and its various essential and its different types:...............1

P2. Various methods used by the management accounting officer for management accounting

reporting:................................................................................................................................3

M1: Merits of implementing accounting:...............................................................................4

P3 Net profits as per absorption costing and marginal costing:.............................................5

M2:.........................................................................................................................................6

D2:..........................................................................................................................................6

TASK 3............................................................................................................................................7

P4. Use of planning tools in the budgetary controls:..............................................................7

M3:.........................................................................................................................................8

D3:..........................................................................................................................................9

TASK 4............................................................................................................................................9

P5 Management accounting systems to respond financial problems.....................................1

M4:.........................................................................................................................................2

CONCLUSION................................................................................................................................2

REFERENCES................................................................................................................................3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

FROM: MANAGEMENT ACCOUNTING OFFICER

TO,

GENERAL MANAGER

ZYLLA COMPANY

SUB: MANAGEMENT ACCOUNTING SYSTEM

INTRODUCTION

Management accounting is the tool which is used by each firm in order to make

sustainable development. There are certain management accounting tools such as traditional

accounting, lean accounting, cost accounting, job costing, inventory management system, and

much more. With the help of these tools, any organisations can get the competitive advantage

over the others. Although, This report is made on the Zylla company which operated in the retail

trade. It is of small & medium size entity. By using management tools , firm can gain the

competitive advantage over the other rivals. However, this is observed that the company is using

these tools in order to improve the performance of the firm (Casini, Marone and Scozzafava,

2014). Various reports are made on the basis of these management tools so that they could take

effective strategy which is beneficial for the firm. Under this report, absorption and marginal

costing tools are used by the firm for maximising the firm's profits. In addition to this, various

planning tools, their advantages and disadvantages are used by the firm so that the business can

make effective decisions for the firm. However, this is the most effective tools which can be used

by each and every firms for gaining their pre-set targets. Various management accounting tools

such as, KPI, Financial governance, Benchmarking, Balance score care and so on, are used for

responding financial problems (Takeda and Boyns, 2014).

TASK 1

P1 Management accounting tools and its various essential and its different types:

The management accounting is the process of making management reports which

ultimately aim to render exact and timely financial and statistical information needed by the

managers to for making daily and routine decisions. This is the brad term which covers all the

financial and non-financial information that ultimately provides deep information about the firm.

1

TO,

GENERAL MANAGER

ZYLLA COMPANY

SUB: MANAGEMENT ACCOUNTING SYSTEM

INTRODUCTION

Management accounting is the tool which is used by each firm in order to make

sustainable development. There are certain management accounting tools such as traditional

accounting, lean accounting, cost accounting, job costing, inventory management system, and

much more. With the help of these tools, any organisations can get the competitive advantage

over the others. Although, This report is made on the Zylla company which operated in the retail

trade. It is of small & medium size entity. By using management tools , firm can gain the

competitive advantage over the other rivals. However, this is observed that the company is using

these tools in order to improve the performance of the firm (Casini, Marone and Scozzafava,

2014). Various reports are made on the basis of these management tools so that they could take

effective strategy which is beneficial for the firm. Under this report, absorption and marginal

costing tools are used by the firm for maximising the firm's profits. In addition to this, various

planning tools, their advantages and disadvantages are used by the firm so that the business can

make effective decisions for the firm. However, this is the most effective tools which can be used

by each and every firms for gaining their pre-set targets. Various management accounting tools

such as, KPI, Financial governance, Benchmarking, Balance score care and so on, are used for

responding financial problems (Takeda and Boyns, 2014).

TASK 1

P1 Management accounting tools and its various essential and its different types:

The management accounting is the process of making management reports which

ultimately aim to render exact and timely financial and statistical information needed by the

managers to for making daily and routine decisions. This is the brad term which covers all the

financial and non-financial information that ultimately provides deep information about the firm.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

However, this is the most effective tool in any business form making effective decisions. There

is no legal requirement to serve this reports to the manager. This is totally depends on the

managers or top level authorities whether to serve the management accounting reports by the

management accounting officer or not. But on the other hand, financial accounting report is

required to be made as this is essential as per the law. Management accounting produces daily,

weekly or monthly reports for firm internal audiences. However, this report, typically reflects the

amount of cash available to the firm, sales revenue produced, amount of orders in hand, state of

debtors and credits, outstanding loans, raw material and stock and this might likewise covers

trend charts, variance analysis and other statistics, which will ultimately helps the firm to make

effective decisions for the firm (Malmmose, 2015). This is the tool which is used by the firm in

order to make cert

Management accounting includes accounting, finance and management along with the business

skills and tools which add real value to the firm. MA are qualified to work throughout the

business, not just in finance, assisting managers on the financial implications of huge decisions,

making business strategy and also controlling risks.

Management accountants implement management accounting reports for leading and

inform business strategy and drive sustainable success. The accounting officer of the Zylla

company use use management accounting information in such a manner so that the performance

of the cited firm can improve.

Cost accounting system: This is the accounting system which is used by the firm for

making production of good in an effective manner (Kotas, 2014). However, this is the most

effective tool for knowing the per unit cost. By using this tool, firm could bifurcate the per unit

cost and eliminate the wastage costs from the production costs. This is most useful for the firms

which are operating in the manufacturing sector. As, they would get to know about the costs of

various factors so that they can effectively add value to the firm. And make the product in an

appropriate value.

Inventory Management system: This is the management accounting tool which is used

in the firm for effectively using the available resource in an effective manner, however, this is

the most effective tool for optimising the value of the firm by managing the inventory in an

effective manner. Under this, the management effective manage the inventory so that no extra

costs can incur on the stock.

2

is no legal requirement to serve this reports to the manager. This is totally depends on the

managers or top level authorities whether to serve the management accounting reports by the

management accounting officer or not. But on the other hand, financial accounting report is

required to be made as this is essential as per the law. Management accounting produces daily,

weekly or monthly reports for firm internal audiences. However, this report, typically reflects the

amount of cash available to the firm, sales revenue produced, amount of orders in hand, state of

debtors and credits, outstanding loans, raw material and stock and this might likewise covers

trend charts, variance analysis and other statistics, which will ultimately helps the firm to make

effective decisions for the firm (Malmmose, 2015). This is the tool which is used by the firm in

order to make cert

Management accounting includes accounting, finance and management along with the business

skills and tools which add real value to the firm. MA are qualified to work throughout the

business, not just in finance, assisting managers on the financial implications of huge decisions,

making business strategy and also controlling risks.

Management accountants implement management accounting reports for leading and

inform business strategy and drive sustainable success. The accounting officer of the Zylla

company use use management accounting information in such a manner so that the performance

of the cited firm can improve.

Cost accounting system: This is the accounting system which is used by the firm for

making production of good in an effective manner (Kotas, 2014). However, this is the most

effective tool for knowing the per unit cost. By using this tool, firm could bifurcate the per unit

cost and eliminate the wastage costs from the production costs. This is most useful for the firms

which are operating in the manufacturing sector. As, they would get to know about the costs of

various factors so that they can effectively add value to the firm. And make the product in an

appropriate value.

Inventory Management system: This is the management accounting tool which is used

in the firm for effectively using the available resource in an effective manner, however, this is

the most effective tool for optimising the value of the firm by managing the inventory in an

effective manner. Under this, the management effective manage the inventory so that no extra

costs can incur on the stock.

2

Job cost system: This is the management accounting tool that are used by the firm for

recording the costs of producing job, instead of process (Fullerton, Kennedy and Widener, 2014).

With job costing system, a project manager or the management accounting officer could track

costs of the each job. Handling data that is more concerned to the operations of the business.

This is same as the batch costing system.

Batch costing system: Under this system, the batch costing is a kind of special order

costing. This is same as the job costing. Under the batch, each batch are a number of similar

units but each batch would be diverse. Each batch is addressing independent identifiable costs

unit. This is the cluster of the costs which are covered when a group of products or services are

made, and that could be identified to particular products or services within the group.

These are the management accounting tools that are used by the firm in order to attain

firm's pre-set objectives. However, this is the most essential part which are required to know by

the firm for making effective decisions.

P2. Various methods used by the management accounting officer for management accounting

reporting:

Management or Cost accounting concentrates internally on the information received via

financial accounting. Managerial accounting is implemented for planning, controlling and

decisions making. Management accountants depends upon the normal financial statements

covering the income statements, balance sheet and cash flow statements, but likewise

implement other kinds of management reports for assessing firm's information. These includes

product cost reports, budgets and performance reports.

Cost reports: Management accountants measures costs of products manufactured. This

is completed by considering all raw product costs, overheads, labour and any other extra costs

into consideration (Otley, and Emmanuel, 2013). The totals are divided by the amounts of goods

manufactured. Entire information related to this is briefly summarised under the cost report.

Such report enables managers the oversee the cost prices of products versus selling prices. This

enables the manager of the cited firm to plan and manage profits margin.

Budget reports: This is one of the most component of management accounting. Budgets

are mostly formed by implementing prior years' budgets and adjusting to future projections. A

firm's budget lists entire sources of revenues and expenses. A firm tries to complete its pre-set

targets and objectives at the time of staying within budgets amounts. Managers of the cited firm

3

recording the costs of producing job, instead of process (Fullerton, Kennedy and Widener, 2014).

With job costing system, a project manager or the management accounting officer could track

costs of the each job. Handling data that is more concerned to the operations of the business.

This is same as the batch costing system.

Batch costing system: Under this system, the batch costing is a kind of special order

costing. This is same as the job costing. Under the batch, each batch are a number of similar

units but each batch would be diverse. Each batch is addressing independent identifiable costs

unit. This is the cluster of the costs which are covered when a group of products or services are

made, and that could be identified to particular products or services within the group.

These are the management accounting tools that are used by the firm in order to attain

firm's pre-set objectives. However, this is the most essential part which are required to know by

the firm for making effective decisions.

P2. Various methods used by the management accounting officer for management accounting

reporting:

Management or Cost accounting concentrates internally on the information received via

financial accounting. Managerial accounting is implemented for planning, controlling and

decisions making. Management accountants depends upon the normal financial statements

covering the income statements, balance sheet and cash flow statements, but likewise

implement other kinds of management reports for assessing firm's information. These includes

product cost reports, budgets and performance reports.

Cost reports: Management accountants measures costs of products manufactured. This

is completed by considering all raw product costs, overheads, labour and any other extra costs

into consideration (Otley, and Emmanuel, 2013). The totals are divided by the amounts of goods

manufactured. Entire information related to this is briefly summarised under the cost report.

Such report enables managers the oversee the cost prices of products versus selling prices. This

enables the manager of the cited firm to plan and manage profits margin.

Budget reports: This is one of the most component of management accounting. Budgets

are mostly formed by implementing prior years' budgets and adjusting to future projections. A

firm's budget lists entire sources of revenues and expenses. A firm tries to complete its pre-set

targets and objectives at the time of staying within budgets amounts. Managers of the cited firm

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

oversee into advanced vendors to implement as suppliers of raw materials to protect money.

They likewise find the ways to enhance sales while reducing expenses.

Performance Report: This is the report which reflects the performance of the firm.

Management accounting officer apply budgets to compare the actual expenses and incomes to

the budgeted amount. The variance is assessed at the time of identifying new budgets and and

whole information related to these amounts is listed on a performance report. Performance

reports are measured on an yearly basis. Although, few firms form them monthly or quarterly.

Such reports assists the managers plan for future demand in manufacturing and increasing costs.

Other reports: There are so many reports which are formed by managerial accountants.

Order information reports are used to compare orders placed to orders achieved. These reports

reflects backlog information and if the orders are placed were sufficiently required. These kind

of reports likewise summarize if huge number of orders were placed were specific were ordered,

henceforth, forcing the firm to sit on unused goods not required during the time. Business

situation reports likewise incorporated, that assists the managers to form decisions relating to

current and future firm conditions.

Job cost reports: Under this report, job cost report is the introductory place for much of

the data covered in other reports. Such report lists each job under which working on and lists the

total costs covered on the job in the previous period (Macintosh and Quattrone, 2010). The job

costs are costs broken down into the mentioned categories: Labour costs, Material costs,

Subcontractor costs, Field Overheads, Liquidated Damages. On the basis of this report, the Zylla

company can use this in effective manner. Although this is the most effective manner.

These reports are the essential parts by which firm can gain the sustainable development

for the firm.

M1: Merits of implementing accounting:

This is observed that the management accounting system is an efficient system that are

used by the firm's to control and safeguards its financial transactions. This kind of systems could

assist them to get positive outcomes with the available resources. For attaining optimum

advantages, managers needs to adopt diverse accounting system that could be effective for the

firm. The most imperative for implementing these system is to enhance profitability and

efficiency for the firm. The Zylla company become more reliable for assisting sustainability.

4

They likewise find the ways to enhance sales while reducing expenses.

Performance Report: This is the report which reflects the performance of the firm.

Management accounting officer apply budgets to compare the actual expenses and incomes to

the budgeted amount. The variance is assessed at the time of identifying new budgets and and

whole information related to these amounts is listed on a performance report. Performance

reports are measured on an yearly basis. Although, few firms form them monthly or quarterly.

Such reports assists the managers plan for future demand in manufacturing and increasing costs.

Other reports: There are so many reports which are formed by managerial accountants.

Order information reports are used to compare orders placed to orders achieved. These reports

reflects backlog information and if the orders are placed were sufficiently required. These kind

of reports likewise summarize if huge number of orders were placed were specific were ordered,

henceforth, forcing the firm to sit on unused goods not required during the time. Business

situation reports likewise incorporated, that assists the managers to form decisions relating to

current and future firm conditions.

Job cost reports: Under this report, job cost report is the introductory place for much of

the data covered in other reports. Such report lists each job under which working on and lists the

total costs covered on the job in the previous period (Macintosh and Quattrone, 2010). The job

costs are costs broken down into the mentioned categories: Labour costs, Material costs,

Subcontractor costs, Field Overheads, Liquidated Damages. On the basis of this report, the Zylla

company can use this in effective manner. Although this is the most effective manner.

These reports are the essential parts by which firm can gain the sustainable development

for the firm.

M1: Merits of implementing accounting:

This is observed that the management accounting system is an efficient system that are

used by the firm's to control and safeguards its financial transactions. This kind of systems could

assist them to get positive outcomes with the available resources. For attaining optimum

advantages, managers needs to adopt diverse accounting system that could be effective for the

firm. The most imperative for implementing these system is to enhance profitability and

efficiency for the firm. The Zylla company become more reliable for assisting sustainability.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

P3 Net profits as per absorption costing and marginal costing:

Costing is the most crucial part for assessing the per unit cost for the firm. This might

covers the assignment of variable costs, that are those costs which can vary with few forms of

activity. Such kind of costing is called as the direct costing. For instance. The cost of material

changes with the number of unit manufactured, and hence is a variable cost. Costing does not

only covers variable costs but also fixed costs, that are those costs which stay the same, instead

of the level of activity. Such kind of costing is known as the absorption costing. This is the

costing is implemented for two purposes:

Internal reporting: Management implements costing to learn about the cost of operations,

henceforth, this could improve operations for enhancing profitability (Kotas, 2014). This kinds

of information can likewise implement as the basis for emerging product prices.

External reporting: Diverse accounting systems needs that costs be apportioned to the stock

recorded in a firm's balance sheet at the end of the year. This is likewise known as the use of a

cost allocation system, consistently applied.

Under this research report, this is concluded that the cited company uses absorption

costing and marginal costing method for knowing the net profits for the firm. These are

mentioned hereunder:

Absorption Costing: This is the costing tool under which all the manufacturing costs including

fixed and variable costs, are considered while calculating net profits. However, this is one of the

most effective tool which is used by the firm for lowering the costs and optimise the profits of

the firm.

Marginal costing: Under this costing methods all the variable costs are considered while

calculating the contribution. And all the fixed costs are separately treated under this. Thee are

certain tools that can be used by the firm for effective calculating the net profits.

Computation through Absorption costing

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2+3 = 16*500

8000 8000

Gross profit 9500

5

Costing is the most crucial part for assessing the per unit cost for the firm. This might

covers the assignment of variable costs, that are those costs which can vary with few forms of

activity. Such kind of costing is called as the direct costing. For instance. The cost of material

changes with the number of unit manufactured, and hence is a variable cost. Costing does not

only covers variable costs but also fixed costs, that are those costs which stay the same, instead

of the level of activity. Such kind of costing is known as the absorption costing. This is the

costing is implemented for two purposes:

Internal reporting: Management implements costing to learn about the cost of operations,

henceforth, this could improve operations for enhancing profitability (Kotas, 2014). This kinds

of information can likewise implement as the basis for emerging product prices.

External reporting: Diverse accounting systems needs that costs be apportioned to the stock

recorded in a firm's balance sheet at the end of the year. This is likewise known as the use of a

cost allocation system, consistently applied.

Under this research report, this is concluded that the cited company uses absorption

costing and marginal costing method for knowing the net profits for the firm. These are

mentioned hereunder:

Absorption Costing: This is the costing tool under which all the manufacturing costs including

fixed and variable costs, are considered while calculating net profits. However, this is one of the

most effective tool which is used by the firm for lowering the costs and optimise the profits of

the firm.

Marginal costing: Under this costing methods all the variable costs are considered while

calculating the contribution. And all the fixed costs are separately treated under this. Thee are

certain tools that can be used by the firm for effective calculating the net profits.

Computation through Absorption costing

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2+3 = 16*500

8000 8000

Gross profit 9500

5

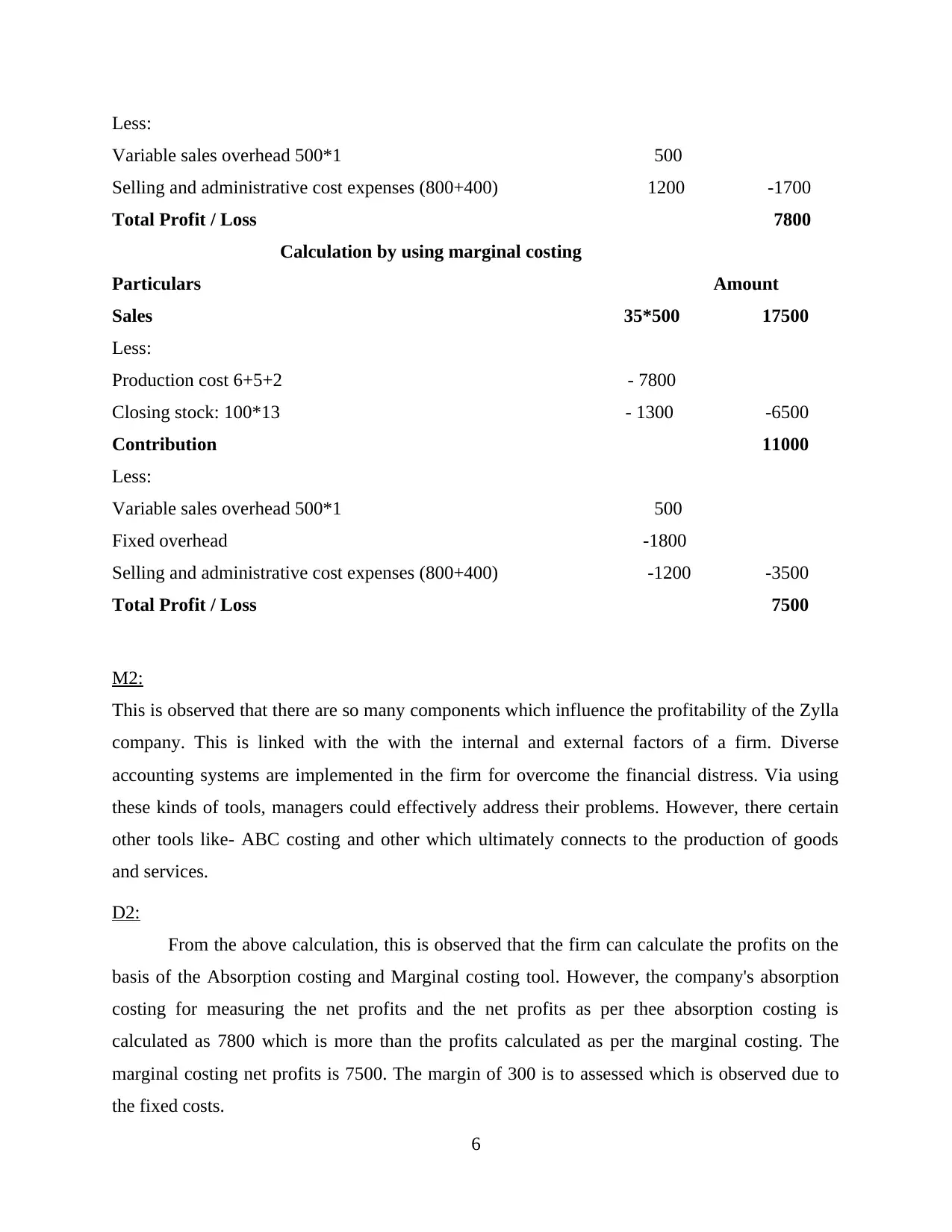

Less:

Variable sales overhead 500*1 500

Selling and administrative cost expenses (800+400) 1200 -1700

Total Profit / Loss 7800

Calculation by using marginal costing

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2 - 7800

Closing stock: 100*13 - 1300 -6500

Contribution 11000

Less:

Variable sales overhead 500*1 500

Fixed overhead -1800

Selling and administrative cost expenses (800+400) -1200 -3500

Total Profit / Loss 7500

M2:

This is observed that there are so many components which influence the profitability of the Zylla

company. This is linked with the with the internal and external factors of a firm. Diverse

accounting systems are implemented in the firm for overcome the financial distress. Via using

these kinds of tools, managers could effectively address their problems. However, there certain

other tools like- ABC costing and other which ultimately connects to the production of goods

and services.

D2:

From the above calculation, this is observed that the firm can calculate the profits on the

basis of the Absorption costing and Marginal costing tool. However, the company's absorption

costing for measuring the net profits and the net profits as per thee absorption costing is

calculated as 7800 which is more than the profits calculated as per the marginal costing. The

marginal costing net profits is 7500. The margin of 300 is to assessed which is observed due to

the fixed costs.

6

Variable sales overhead 500*1 500

Selling and administrative cost expenses (800+400) 1200 -1700

Total Profit / Loss 7800

Calculation by using marginal costing

Particulars Amount

Sales 35*500 17500

Less:

Production cost 6+5+2 - 7800

Closing stock: 100*13 - 1300 -6500

Contribution 11000

Less:

Variable sales overhead 500*1 500

Fixed overhead -1800

Selling and administrative cost expenses (800+400) -1200 -3500

Total Profit / Loss 7500

M2:

This is observed that there are so many components which influence the profitability of the Zylla

company. This is linked with the with the internal and external factors of a firm. Diverse

accounting systems are implemented in the firm for overcome the financial distress. Via using

these kinds of tools, managers could effectively address their problems. However, there certain

other tools like- ABC costing and other which ultimately connects to the production of goods

and services.

D2:

From the above calculation, this is observed that the firm can calculate the profits on the

basis of the Absorption costing and Marginal costing tool. However, the company's absorption

costing for measuring the net profits and the net profits as per thee absorption costing is

calculated as 7800 which is more than the profits calculated as per the marginal costing. The

marginal costing net profits is 7500. The margin of 300 is to assessed which is observed due to

the fixed costs.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 3

P4. Use of planning tools in the budgetary controls:

Planning tools are the most crucial tools which are used for budgetary controls. These are

the most effective tool for gaining the sustainability for the firm. There are certain tools which

are used by the firm effective operations (Bodie, 2013). There are few of the planning tools

which are mentioned hereunder:

Forecasting tools: This is the planning tool which assists the firm's management in its

attempts to co-relate with the contingencies of the future, based on the data from the previous

and current analysis of trends. This begins with the particular hypothesis that are relied on the

management's experience, knowledge, and judgement. Such forecasting are projected into the

forthcoming months, years implementing one or higher tools like- Box-Jenkins models, Delphi

method, regression analysis and trend projection. As, any error or problems in the hypothesis

would outcomes in a same or important problems in estimating, the tools of sensitivity analysis is

implemented that allocates a range of values the uncertain components. This is the tool which is

used by the cited firm for budgetary controls.

Advantages:

Forecasting is the main tool which is used by the firm that could be used by the firm for

meeting the pre-set targets. However, the forecasting tools helps the firm to predicts the amounts

of the revenues and expenses so that the firm could use them for budgetary control.

Disadvantages:

Forecasting does not always renders the accurate prediction of the firm's revenues and

expenses for the pre-set targets and objectives (DRURY, 2013). If the company will use this tool,

then the company will make wrong budgets which will ultimately affects the objectives for the

firm in a negative manner. By applying this tool, firm pre-set objectives can not be achieved due

to its wrongful projection.

Scenario tools: This is planning tool which renders a stranded tool for managers for

evaluating alternative views of what might occurred in the future as this assist to strategic,

functional, and financial planning. This planning tool concentrates highly on responding three

questions: what could happened?, what will be affect on our strategies, plans and budgets?, how

must the company respond? On the basis of these tools, firm is able to respond these problems.

Advantages:

7

P4. Use of planning tools in the budgetary controls:

Planning tools are the most crucial tools which are used for budgetary controls. These are

the most effective tool for gaining the sustainability for the firm. There are certain tools which

are used by the firm effective operations (Bodie, 2013). There are few of the planning tools

which are mentioned hereunder:

Forecasting tools: This is the planning tool which assists the firm's management in its

attempts to co-relate with the contingencies of the future, based on the data from the previous

and current analysis of trends. This begins with the particular hypothesis that are relied on the

management's experience, knowledge, and judgement. Such forecasting are projected into the

forthcoming months, years implementing one or higher tools like- Box-Jenkins models, Delphi

method, regression analysis and trend projection. As, any error or problems in the hypothesis

would outcomes in a same or important problems in estimating, the tools of sensitivity analysis is

implemented that allocates a range of values the uncertain components. This is the tool which is

used by the cited firm for budgetary controls.

Advantages:

Forecasting is the main tool which is used by the firm that could be used by the firm for

meeting the pre-set targets. However, the forecasting tools helps the firm to predicts the amounts

of the revenues and expenses so that the firm could use them for budgetary control.

Disadvantages:

Forecasting does not always renders the accurate prediction of the firm's revenues and

expenses for the pre-set targets and objectives (DRURY, 2013). If the company will use this tool,

then the company will make wrong budgets which will ultimately affects the objectives for the

firm in a negative manner. By applying this tool, firm pre-set objectives can not be achieved due

to its wrongful projection.

Scenario tools: This is planning tool which renders a stranded tool for managers for

evaluating alternative views of what might occurred in the future as this assist to strategic,

functional, and financial planning. This planning tool concentrates highly on responding three

questions: what could happened?, what will be affect on our strategies, plans and budgets?, how

must the company respond? On the basis of these tools, firm is able to respond these problems.

Advantages:

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

With the help of scenario planning, firm managers get the investigates about the choices,

opportunities and execution which uncertainty presents. This introduce improved quality strategy

plans, budgets and estimates, and it permits a clearer apprehension of the sensitivity of the main

drivers of the firm and possible impacts of the future outcomes.

Disadvantages:

This planning tool does not always renders an accurate forecasting values which can be

used by the firm. This is the time consuming process as this takes most of the time for

formulating planning tool.

Contingency planning tools: This is planning tool which is specially made for making a firm to

respond in an effective manner to an emergency and this possible impact (Herzig and et.al.

2012). Emerging a contingency plan covers forming decisions in advance about the management

of the human and financial resource, cope up and communications processes, and being aware of

a range of tools and logical references. These kind of planning is a management tool, covering

whole sectors, that could assist the firm to timely and efficient provision of humanitarian aid to

those highly in requirement at the time of disaster occurs.

Advantages:

The main advantage of the this planning tool is to minimise the costs so that the extra

cost can be eliminated. A contingency plan assists to lower the loss of production. A contingency

plan might covers of rerouting data, emergency producers for power, escape routine for

employees and management duties for contingency team members (Arroyo, 2012).

Disadvantages:

This is the most complicated plan as this takes highest time to calculate the planning tools.

While making this tool, company can make certain objectives in an effective manner. However,

this is the reactive approach instead of proactive approach.

M3:

In order to increase the efficiency and attain maximum advantage from the resources,

Zylla company is using various planning tools which can overcome the issues and make

necessary decision by using appropriate budgets. Some of the effective planning tools are

forecasting which can help the organisation to plan for the future sales and profits. Other are

contingency tools is based on situation, under this the company some reserve so that they can use

8

opportunities and execution which uncertainty presents. This introduce improved quality strategy

plans, budgets and estimates, and it permits a clearer apprehension of the sensitivity of the main

drivers of the firm and possible impacts of the future outcomes.

Disadvantages:

This planning tool does not always renders an accurate forecasting values which can be

used by the firm. This is the time consuming process as this takes most of the time for

formulating planning tool.

Contingency planning tools: This is planning tool which is specially made for making a firm to

respond in an effective manner to an emergency and this possible impact (Herzig and et.al.

2012). Emerging a contingency plan covers forming decisions in advance about the management

of the human and financial resource, cope up and communications processes, and being aware of

a range of tools and logical references. These kind of planning is a management tool, covering

whole sectors, that could assist the firm to timely and efficient provision of humanitarian aid to

those highly in requirement at the time of disaster occurs.

Advantages:

The main advantage of the this planning tool is to minimise the costs so that the extra

cost can be eliminated. A contingency plan assists to lower the loss of production. A contingency

plan might covers of rerouting data, emergency producers for power, escape routine for

employees and management duties for contingency team members (Arroyo, 2012).

Disadvantages:

This is the most complicated plan as this takes highest time to calculate the planning tools.

While making this tool, company can make certain objectives in an effective manner. However,

this is the reactive approach instead of proactive approach.

M3:

In order to increase the efficiency and attain maximum advantage from the resources,

Zylla company is using various planning tools which can overcome the issues and make

necessary decision by using appropriate budgets. Some of the effective planning tools are

forecasting which can help the organisation to plan for the future sales and profits. Other are

contingency tools is based on situation, under this the company some reserve so that they can use

8

it if any contingency occurs during year. All these tools help the company to increase their

market share and control extra cost which are incur during the year (Albelda, 2011).

D3:

In relation to manage Zylla company's performance finance department is entirely

responsible. They can take decision on the basis of current and previous year performance of the

company. It has been analyse that financial problems can affect the performance as well as

growth. It is utmost necessary for the managers to detect all those financial issues and make

necessary steps in attaining future sustainability for the company. Balance scorecard is an

essential system that can be used for the purpose of solving financial issues those are arises in an

organisation. Some issues are related with credit for living expenses on reduced income.

TASK 4

9

market share and control extra cost which are incur during the year (Albelda, 2011).

D3:

In relation to manage Zylla company's performance finance department is entirely

responsible. They can take decision on the basis of current and previous year performance of the

company. It has been analyse that financial problems can affect the performance as well as

growth. It is utmost necessary for the managers to detect all those financial issues and make

necessary steps in attaining future sustainability for the company. Balance scorecard is an

essential system that can be used for the purpose of solving financial issues those are arises in an

organisation. Some issues are related with credit for living expenses on reduced income.

TASK 4

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.