Icon College: Management Accounting Report - Zylla Company Analysis

VerifiedAdded on 2020/06/05

|19

|5958

|130

Report

AI Summary

This report analyzes management accounting practices, focusing on their application within Zylla Company. It defines management accounting, discusses its types, and outlines essential organizational requirements. The report explores various reporting methods, including segmental, performance, inventory management, accounts receivables ageing, and job cost reports. It delves into cost calculation techniques such as absorption and marginal costing, and examines the benefits and applications of management accounting systems. The report also explores different management accounting techniques, budgetary control tools, and planning tools for budget preparation and forecasting. It further compares how organizations adapt management accounting systems to address financial problems and discusses how these systems can lead to success. The report provides a comprehensive overview of how management accounting contributes to organizational efficiency, internal control, and strategic decision-making, supported by examples from Zylla Company.

Management Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

(P1) Define management accounting and discuss its types and essential requirements in

organisation............................................................................................................................1

(P2) Discuss different methods used for management accounting reporting.........................3

(M1) Discuss benefits of management accounting systems and their application.................5

(P3) Calculate costs by using tchniques of cost analysis eith help of absorption costing and

marginal costing.....................................................................................................................5

APPENDIX......................................................................................................................................8

Working Note 1......................................................................................................................8

Working Note 2......................................................................................................................8

(M2) Different management accounting techniques..............................................................8

(P4)Outilne avantafs and duadvantages of tools used in budgetary control..........................9

(M3) State the use of different planning tools and their application for preparing and

forecasting budgets...............................................................................................................11

(P5) Compare how organisations are adapting management accounting systems to respond to

financial problems................................................................................................................11

(M4) Discuss how, in responding to financial problems, management accounting can lead to

success..................................................................................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

2

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

(P1) Define management accounting and discuss its types and essential requirements in

organisation............................................................................................................................1

(P2) Discuss different methods used for management accounting reporting.........................3

(M1) Discuss benefits of management accounting systems and their application.................5

(P3) Calculate costs by using tchniques of cost analysis eith help of absorption costing and

marginal costing.....................................................................................................................5

APPENDIX......................................................................................................................................8

Working Note 1......................................................................................................................8

Working Note 2......................................................................................................................8

(M2) Different management accounting techniques..............................................................8

(P4)Outilne avantafs and duadvantages of tools used in budgetary control..........................9

(M3) State the use of different planning tools and their application for preparing and

forecasting budgets...............................................................................................................11

(P5) Compare how organisations are adapting management accounting systems to respond to

financial problems................................................................................................................11

(M4) Discuss how, in responding to financial problems, management accounting can lead to

success..................................................................................................................................13

CONCLUSION..............................................................................................................................13

REFERENCES..............................................................................................................................14

2

INTRODUCTION

Management accounting is useful tool for organization to have full control on the internal

factors of it so that if any deviations exist then it can be solved with the help of management

accounting techniques in effective way. This report deals with Zylla Company which is quite

successful in its set up from past few years (van der Steen, 2011). It is also good in its working

and is able to make good image in market. Management accounting information is essential for

firm as it jot down inefficiencies if exist in organization and suggest ways how to eradicate it

with the help of management accounting system by the firm. Several tools like cost accounting,

job costing, price optimisation and inventory management system are very much helpful for firm

to effectively meet its objectives and goals.

TASK 1

(P1) Define management accounting and discuss its types and essential requirements in

organisation

Management accounting is quite useful for organisation as it helps it to have internal

control in organisation itself. The management accounting information is required by

management to improve its performance, if deviations exist in organisation. It is an essential

requirement to managers so that they may take quick and timely decisions for betterment of

company. This will help organisation internally vibrant and will become capable of performing

competitive in market. Management accounting provides accurate and timely information about

financial statements. It also provides statistical data to provide support to managers to take

enhanced and better decisions for the company. Zylla Company also uses management

accounting information to improve upon its working to be competitive in market.

Management accounting is utmost important for managers as it measures the internal

strength and weaknesses of organisation in the way which help it to improve upon weaknesses.

When managers know strength and weaknesses then they can make enhanced decisions for

betterment of company (Albelda, 2011). This will produce more productivity to organisation and

will be more successful in its operations and working effectively so that it can achieve its

objectives and goals in effectual manner. Management only to make decisions internally uses

management accounting information. It is not made available to external users like stakeholders,

3

Management accounting is useful tool for organization to have full control on the internal

factors of it so that if any deviations exist then it can be solved with the help of management

accounting techniques in effective way. This report deals with Zylla Company which is quite

successful in its set up from past few years (van der Steen, 2011). It is also good in its working

and is able to make good image in market. Management accounting information is essential for

firm as it jot down inefficiencies if exist in organization and suggest ways how to eradicate it

with the help of management accounting system by the firm. Several tools like cost accounting,

job costing, price optimisation and inventory management system are very much helpful for firm

to effectively meet its objectives and goals.

TASK 1

(P1) Define management accounting and discuss its types and essential requirements in

organisation

Management accounting is quite useful for organisation as it helps it to have internal

control in organisation itself. The management accounting information is required by

management to improve its performance, if deviations exist in organisation. It is an essential

requirement to managers so that they may take quick and timely decisions for betterment of

company. This will help organisation internally vibrant and will become capable of performing

competitive in market. Management accounting provides accurate and timely information about

financial statements. It also provides statistical data to provide support to managers to take

enhanced and better decisions for the company. Zylla Company also uses management

accounting information to improve upon its working to be competitive in market.

Management accounting is utmost important for managers as it measures the internal

strength and weaknesses of organisation in the way which help it to improve upon weaknesses.

When managers know strength and weaknesses then they can make enhanced decisions for

betterment of company (Albelda, 2011). This will produce more productivity to organisation and

will be more successful in its operations and working effectively so that it can achieve its

objectives and goals in effectual manner. Management only to make decisions internally uses

management accounting information. It is not made available to external users like stakeholders,

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

government, tax authorities, customers, banks, labour unions, researchers and suppliers. Only

financial information is made available to them not internal information. Management

accounting is quite useful for managers so that they may be able to make enhanced and useful

decisions for company for betterment of it in effectual manner.

Management accounting is process of preparing management reports to make decisions

for company. It identifies measures and communicate information to enable organisation to

pursue its goals. Through financial accounting, which provides information regarding accounting

reports based on daily activities. Management accounting aids decision making through financial

accounting. Management accounting is useful to forecast the future of firm. It also helps to

predict cash flows and impact of cash flow on business. It also involves trends, budget charts and

tables; it helps managers to allocate money and resources in optimised way to generate growth

and projected revenue.

The different types of management accounting and their requirement in organisation is as

follows:

1. Inventory management system-

It is the ongoing process, which deals with moving parts and products into and out of

company location. Zylla company also manages effective inventory management as it clarifies

company that what amount of inventory is needed and how it can manage to get the products

timely produced and made available to final consumers. Company manages their inventory on

daily basis as they place new order for products and ship ordered goods to customers. It is

however important that business leaders gain grasp of everything involved in inventory

management process (Burritt, Schaltegger and Zvezdov, 2011). This will give them useful

insight, no wastage of stocks will be done, and no additional cost will be incurred. Thus, they can

find out ways to solve inventory management challenges by finding appropriate solutions for

company to flourish in bets possible way.

2. Cost accounting-

Cost accounting is the important phenomenon in organisation. It measures and controls

cost in the organization which helps them to keep a watch over its expenses and no additional

expenditure is incurred. It also provides measures to control. Estimating accurate cost is required

4

financial information is made available to them not internal information. Management

accounting is quite useful for managers so that they may be able to make enhanced and useful

decisions for company for betterment of it in effectual manner.

Management accounting is process of preparing management reports to make decisions

for company. It identifies measures and communicate information to enable organisation to

pursue its goals. Through financial accounting, which provides information regarding accounting

reports based on daily activities. Management accounting aids decision making through financial

accounting. Management accounting is useful to forecast the future of firm. It also helps to

predict cash flows and impact of cash flow on business. It also involves trends, budget charts and

tables; it helps managers to allocate money and resources in optimised way to generate growth

and projected revenue.

The different types of management accounting and their requirement in organisation is as

follows:

1. Inventory management system-

It is the ongoing process, which deals with moving parts and products into and out of

company location. Zylla company also manages effective inventory management as it clarifies

company that what amount of inventory is needed and how it can manage to get the products

timely produced and made available to final consumers. Company manages their inventory on

daily basis as they place new order for products and ship ordered goods to customers. It is

however important that business leaders gain grasp of everything involved in inventory

management process (Burritt, Schaltegger and Zvezdov, 2011). This will give them useful

insight, no wastage of stocks will be done, and no additional cost will be incurred. Thus, they can

find out ways to solve inventory management challenges by finding appropriate solutions for

company to flourish in bets possible way.

2. Cost accounting-

Cost accounting is the important phenomenon in organisation. It measures and controls

cost in the organization which helps them to keep a watch over its expenses and no additional

expenditure is incurred. It also provides measures to control. Estimating accurate cost is required

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

so as to arrive at profitable operations. Firm must know which products are profitable and which

are not. This can be ascertained by calculating correct cost of it. Further products costing system

helps in calculating and estimating closing value of materials inventory WIP (Work in Progress)

and finished goods for purpose of preparation of financial statements for organisation. It has

been divided in two parts such as process costing and activity based costing.

Process costing is cost accounting system that accumulate manufacturing expenses

separately for each process held in production of goods. It is more appropriate for products

whose production is assigned into different departments and cost flow from one department to

another department. Example, process involved in oil refineries and chemicals products. Activity

based costing involves calculation of activity rates and application of overhead expenses to

products based on their respective activity usage.

3. Job costing-

Job costing is the process, which involves accumulating information about costs associated

with specific production or service job. This information is quite helpful in order to submit

cost information to customer’s under contract where expenses are reimbursed (Caglio and

Ditillo, 2012). This information is also helpful for determining accuracy and transparency of

company estimating system regarding allocation of job to factors of production, which

should be able to quote price to allow reasonable profit to organization. It involves three

type of information such as direct materials, direct labour and overhead involved in carrying

out effective production by company.

4. Price optimisation-

This method is based on mathematical models to calculate how demand varies at

different price level and then resultant data combined with information on costs and stock levels

to recommend that amount of price, which will improve and provide more profits to firm in

effectual manner. This is done because if prices are too high, customers will not purchase and if

prices are too low, then firm will not earn profits. As such, price optimisation is used to improve

upon profits to company. So, formula of price optimisation is based on overall demand for

product in market, level of competition. Finding perfect balance between the price and profit is

essential part of this system. This will provide clarity to business on how much price is to be

5

are not. This can be ascertained by calculating correct cost of it. Further products costing system

helps in calculating and estimating closing value of materials inventory WIP (Work in Progress)

and finished goods for purpose of preparation of financial statements for organisation. It has

been divided in two parts such as process costing and activity based costing.

Process costing is cost accounting system that accumulate manufacturing expenses

separately for each process held in production of goods. It is more appropriate for products

whose production is assigned into different departments and cost flow from one department to

another department. Example, process involved in oil refineries and chemicals products. Activity

based costing involves calculation of activity rates and application of overhead expenses to

products based on their respective activity usage.

3. Job costing-

Job costing is the process, which involves accumulating information about costs associated

with specific production or service job. This information is quite helpful in order to submit

cost information to customer’s under contract where expenses are reimbursed (Caglio and

Ditillo, 2012). This information is also helpful for determining accuracy and transparency of

company estimating system regarding allocation of job to factors of production, which

should be able to quote price to allow reasonable profit to organization. It involves three

type of information such as direct materials, direct labour and overhead involved in carrying

out effective production by company.

4. Price optimisation-

This method is based on mathematical models to calculate how demand varies at

different price level and then resultant data combined with information on costs and stock levels

to recommend that amount of price, which will improve and provide more profits to firm in

effectual manner. This is done because if prices are too high, customers will not purchase and if

prices are too low, then firm will not earn profits. As such, price optimisation is used to improve

upon profits to company. So, formula of price optimisation is based on overall demand for

product in market, level of competition. Finding perfect balance between the price and profit is

essential part of this system. This will provide clarity to business on how much price is to be

5

quoted to gain more profits by analysing demand for the product in market and determine level

of competition from rivals. As such, this technique is quite useful for Zylla Company to target

high profits in effectual manner.

(P2) Discuss different methods used for management accounting reporting

Segmental report:

It is the report of operating segments of company in disclosures accompanying in its

financial statements. It is required for public held entities and not for the private ones for its use.

Creditors and investors regarding financial strength of operating departments of company use

segment reporting. Zylla Company prepares this report for providing information to them in

effective way as by relying on this report, they can make decisions regarding company. Segment

report includes information like factors used to identify reportable segments, types of products

sold by each segment, revenues and indirect expense, depreciation and amortisation. It also

includes information such as material expense items, income tax expense, non-cash items and

profit or loss incurred. As such, this all type of information is helpful for analysing strength of

financial position of company for investors and creditors for enhanced decision making.

Performance report:

This report is detailed statement that measures results of some activity in terms of its

success over a specific time (Christ and Burritt, 2013). For example, company regarding

employee’s performance in accomplishing tasks may produce annual report. Alternatively, such

report might help management assess success of project or product and how well budgetary

constraints are adhered to. The actual results are compared with budgeted standards obtained

under some conditional assumptions over same period. Variations from such budget or standards

are known as variance and may be favourable or unfavourable depending upon higher or lower

measurements relative to the standards. Thus, corrective action are taken if any deviations are

occurred in performance of various parameter such as employees performance report or other

such thing which provides business to improve and attain stated objectives in effectual manner.

Inventory management report:

6

of competition from rivals. As such, this technique is quite useful for Zylla Company to target

high profits in effectual manner.

(P2) Discuss different methods used for management accounting reporting

Segmental report:

It is the report of operating segments of company in disclosures accompanying in its

financial statements. It is required for public held entities and not for the private ones for its use.

Creditors and investors regarding financial strength of operating departments of company use

segment reporting. Zylla Company prepares this report for providing information to them in

effective way as by relying on this report, they can make decisions regarding company. Segment

report includes information like factors used to identify reportable segments, types of products

sold by each segment, revenues and indirect expense, depreciation and amortisation. It also

includes information such as material expense items, income tax expense, non-cash items and

profit or loss incurred. As such, this all type of information is helpful for analysing strength of

financial position of company for investors and creditors for enhanced decision making.

Performance report:

This report is detailed statement that measures results of some activity in terms of its

success over a specific time (Christ and Burritt, 2013). For example, company regarding

employee’s performance in accomplishing tasks may produce annual report. Alternatively, such

report might help management assess success of project or product and how well budgetary

constraints are adhered to. The actual results are compared with budgeted standards obtained

under some conditional assumptions over same period. Variations from such budget or standards

are known as variance and may be favourable or unfavourable depending upon higher or lower

measurements relative to the standards. Thus, corrective action are taken if any deviations are

occurred in performance of various parameter such as employees performance report or other

such thing which provides business to improve and attain stated objectives in effectual manner.

Inventory management report:

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inventory means stock of goods which are held in company warehouse for the purpose of

future production or sales. The stock of goods can be retained by company in for of raw

materials, spare parts, partly finished goods or finished goods in its godown or future sales or

production purpose. By inventorying stock in effective manner, company requires inventory

management report. This report deals with figures and facts about inventory currently in hand in

company’s warehouse. It provides managers useful information as how much amount of

inventory is used for production purpose and how much more is required to complete production

of specific items. This ensures that stock is not overestimated or underestimated and no

additional cost is incurred and production process is carried out in effective manner. Managers

do this as unnecessary stock in godown results in additional expense to company, which can be

clarified by inventory management report.

Accounts receivables ageing report:

This report lists down all the unpaid invoices, which are overdue for payments for

customers. This involve all such information, which is required by company to jot down lists of

unpaid invoices from customers (Dillard, J. and Roslender, 2011). It also includes unused credit

memos by date ranges. The ageing report is primary tool for company’s personnel’s to determine

invoices of customers, which are overdue for payment. This report can be used to configure to

also contain contact information for each of customers liable for payment of invoices. This report

is also used by management to determine effectiveness of credit and control functions of

company in effectual manner. The report is sorted by customer name with all invoices for each

customer directly below its name usually sorted by either of invoice number or invoice date on it.

It is very powerful tool for management as it provides them useful information regarding the

overdue payment, which should be taken in time by the company. By analysing this information,

company gains payments on time from the customers, which is needed for company’s effective

functioning.

Job cost report:

Job cost report shows expenses incurred by company in specific project. They are

usually matched with estimate of revenue so that company can evaluate its job profitability.

Zylla company effe5ctively shows its expenses through job cost report. This report helps to

identify high earning areas of business so that company can focus its efforts on those high

7

future production or sales. The stock of goods can be retained by company in for of raw

materials, spare parts, partly finished goods or finished goods in its godown or future sales or

production purpose. By inventorying stock in effective manner, company requires inventory

management report. This report deals with figures and facts about inventory currently in hand in

company’s warehouse. It provides managers useful information as how much amount of

inventory is used for production purpose and how much more is required to complete production

of specific items. This ensures that stock is not overestimated or underestimated and no

additional cost is incurred and production process is carried out in effective manner. Managers

do this as unnecessary stock in godown results in additional expense to company, which can be

clarified by inventory management report.

Accounts receivables ageing report:

This report lists down all the unpaid invoices, which are overdue for payments for

customers. This involve all such information, which is required by company to jot down lists of

unpaid invoices from customers (Dillard, J. and Roslender, 2011). It also includes unused credit

memos by date ranges. The ageing report is primary tool for company’s personnel’s to determine

invoices of customers, which are overdue for payment. This report can be used to configure to

also contain contact information for each of customers liable for payment of invoices. This report

is also used by management to determine effectiveness of credit and control functions of

company in effectual manner. The report is sorted by customer name with all invoices for each

customer directly below its name usually sorted by either of invoice number or invoice date on it.

It is very powerful tool for management as it provides them useful information regarding the

overdue payment, which should be taken in time by the company. By analysing this information,

company gains payments on time from the customers, which is needed for company’s effective

functioning.

Job cost report:

Job cost report shows expenses incurred by company in specific project. They are

usually matched with estimate of revenue so that company can evaluate its job profitability.

Zylla company effe5ctively shows its expenses through job cost report. This report helps to

identify high earning areas of business so that company can focus its efforts on those high

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

earning areas instead of wasting time and money on jobs which yield low profit margins to

company. These reports are also used to analyse expenses while project is in process so that

managers can correct areas before expense is incurred on particular project. This helps company

to establish those jobs, which yield them high revenue margins so that it may flourish in manner

so that it can achieve its objectives and goals in effectual manner (Fullerton, Kennedy and

Widener., 2013).

The benefits of management accounting systems and their application are:

Management accounting system helps business to reduce unwanted expenses, which may

not be incur by company as it reduces their profits and impact their overall efficiency.

Operational expenses can be lower down by managers by using this system in effective way.

This also provide clarity to business what resources are being used to carry out production. As

such, expenses are controlled and management accounting system in company observes wastage

of money and tom.

(P3) Calculate costs by using techniques of cost analysis with help of absorption costing and

marginal costing.

Marginal costing-

Marginal costing is the increase or decrease in total production cost by producing one

more unit of product or of service to customer. In manufacturing concern, marginal cost of

production decreases as the volume of output increases because of economies of scale in

production. Expenses are lower down because company take advantage of discounts for bulk

purchases of raw materials, optimise full use of equipment’s and engage more specialised labour

in carrying out production. However, production will reach point where diseconomies of scale

will enter marginal expenses will begin to rise. Cost may be aroused as company will hire more

management, more labour and more use of machinery will be made by it (Giovannoni,

Maraghini and Riccaboni, 2011). This will increase marginal cost to company. Marginal costs

can be used by management for production decisions.

Marginal costs ae bifurcated on basis of variability into fixed and variable costs. It helps

to determine prices n basis of marginal contribution. Marginal cost = Direct Material + Direct

Labour + Direct Expenses + Overheads. It also helps in determining and valuing stock. It helps

8

company. These reports are also used to analyse expenses while project is in process so that

managers can correct areas before expense is incurred on particular project. This helps company

to establish those jobs, which yield them high revenue margins so that it may flourish in manner

so that it can achieve its objectives and goals in effectual manner (Fullerton, Kennedy and

Widener., 2013).

The benefits of management accounting systems and their application are:

Management accounting system helps business to reduce unwanted expenses, which may

not be incur by company as it reduces their profits and impact their overall efficiency.

Operational expenses can be lower down by managers by using this system in effective way.

This also provide clarity to business what resources are being used to carry out production. As

such, expenses are controlled and management accounting system in company observes wastage

of money and tom.

(P3) Calculate costs by using techniques of cost analysis with help of absorption costing and

marginal costing.

Marginal costing-

Marginal costing is the increase or decrease in total production cost by producing one

more unit of product or of service to customer. In manufacturing concern, marginal cost of

production decreases as the volume of output increases because of economies of scale in

production. Expenses are lower down because company take advantage of discounts for bulk

purchases of raw materials, optimise full use of equipment’s and engage more specialised labour

in carrying out production. However, production will reach point where diseconomies of scale

will enter marginal expenses will begin to rise. Cost may be aroused as company will hire more

management, more labour and more use of machinery will be made by it (Giovannoni,

Maraghini and Riccaboni, 2011). This will increase marginal cost to company. Marginal costs

can be used by management for production decisions.

Marginal costs ae bifurcated on basis of variability into fixed and variable costs. It helps

to determine prices n basis of marginal contribution. Marginal cost = Direct Material + Direct

Labour + Direct Expenses + Overheads. It also helps in determining and valuing stock. It helps

8

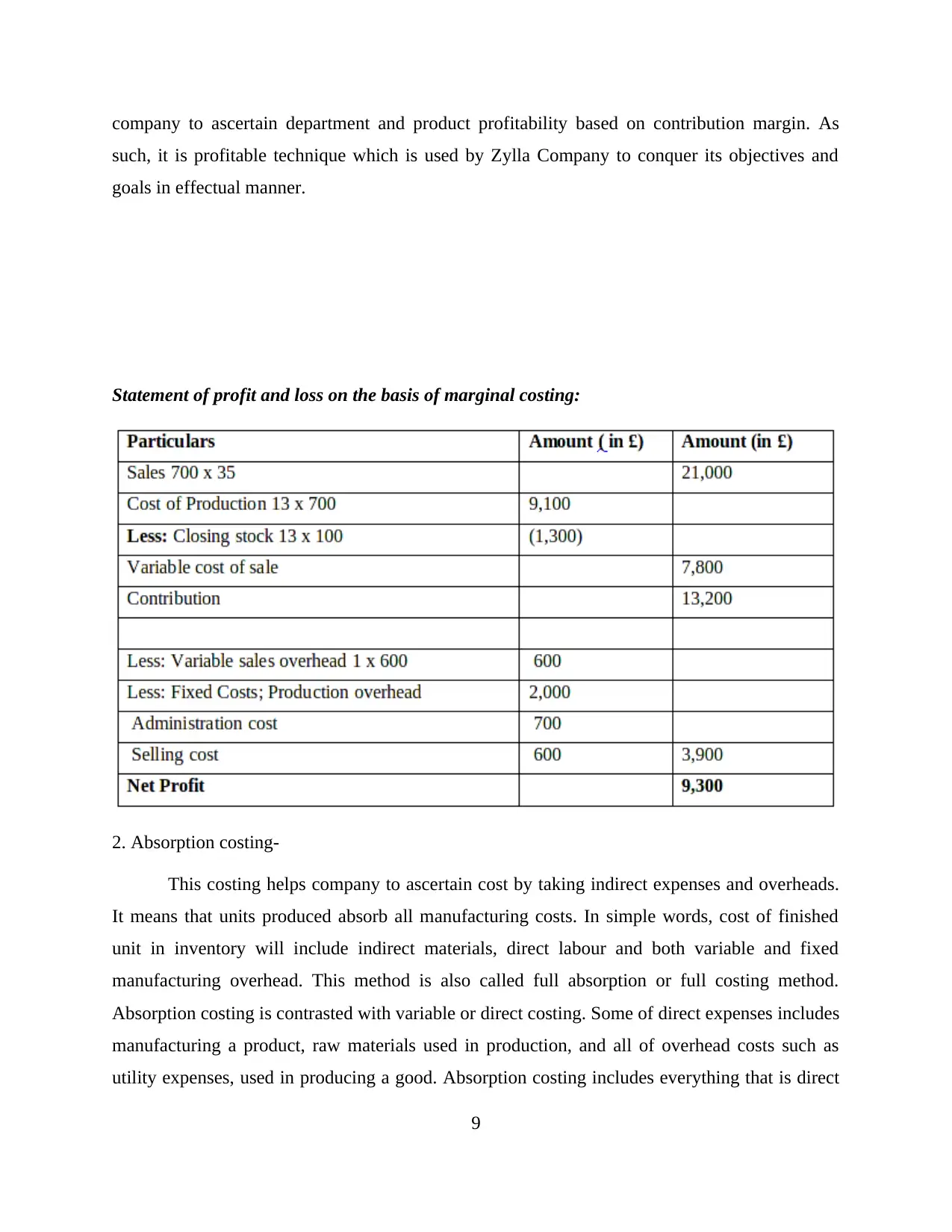

company to ascertain department and product profitability based on contribution margin. As

such, it is profitable technique which is used by Zylla Company to conquer its objectives and

goals in effectual manner.

Statement of profit and loss on the basis of marginal costing:

2. Absorption costing-

This costing helps company to ascertain cost by taking indirect expenses and overheads.

It means that units produced absorb all manufacturing costs. In simple words, cost of finished

unit in inventory will include indirect materials, direct labour and both variable and fixed

manufacturing overhead. This method is also called full absorption or full costing method.

Absorption costing is contrasted with variable or direct costing. Some of direct expenses includes

manufacturing a product, raw materials used in production, and all of overhead costs such as

utility expenses, used in producing a good. Absorption costing includes everything that is direct

9

such, it is profitable technique which is used by Zylla Company to conquer its objectives and

goals in effectual manner.

Statement of profit and loss on the basis of marginal costing:

2. Absorption costing-

This costing helps company to ascertain cost by taking indirect expenses and overheads.

It means that units produced absorb all manufacturing costs. In simple words, cost of finished

unit in inventory will include indirect materials, direct labour and both variable and fixed

manufacturing overhead. This method is also called full absorption or full costing method.

Absorption costing is contrasted with variable or direct costing. Some of direct expenses includes

manufacturing a product, raw materials used in production, and all of overhead costs such as

utility expenses, used in producing a good. Absorption costing includes everything that is direct

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

expense in producing a good at the cost base. It also includes fixed overhead charges are

included as product expense.

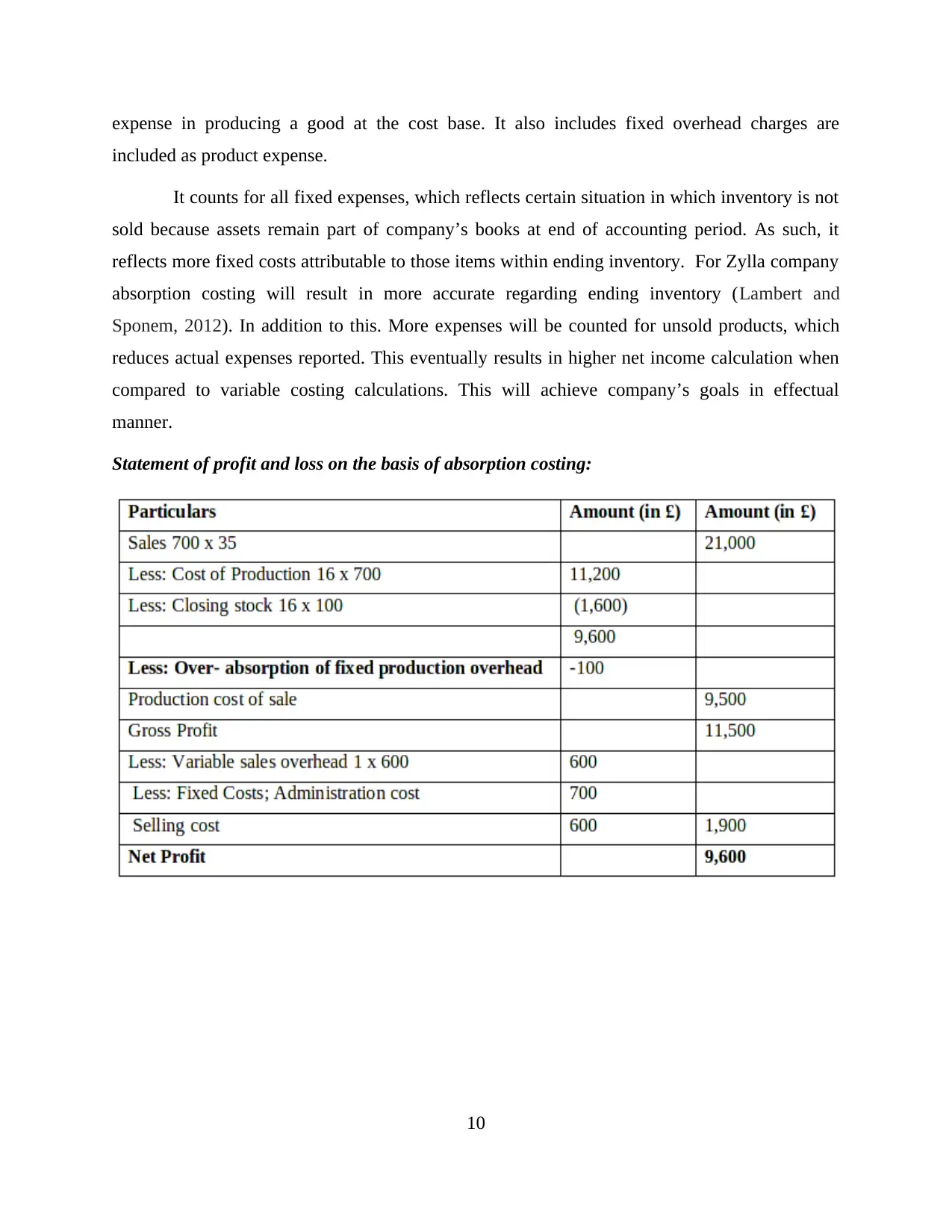

It counts for all fixed expenses, which reflects certain situation in which inventory is not

sold because assets remain part of company’s books at end of accounting period. As such, it

reflects more fixed costs attributable to those items within ending inventory. For Zylla company

absorption costing will result in more accurate regarding ending inventory (Lambert and

Sponem, 2012). In addition to this. More expenses will be counted for unsold products, which

reduces actual expenses reported. This eventually results in higher net income calculation when

compared to variable costing calculations. This will achieve company’s goals in effectual

manner.

Statement of profit and loss on the basis of absorption costing:

10

included as product expense.

It counts for all fixed expenses, which reflects certain situation in which inventory is not

sold because assets remain part of company’s books at end of accounting period. As such, it

reflects more fixed costs attributable to those items within ending inventory. For Zylla company

absorption costing will result in more accurate regarding ending inventory (Lambert and

Sponem, 2012). In addition to this. More expenses will be counted for unsold products, which

reduces actual expenses reported. This eventually results in higher net income calculation when

compared to variable costing calculations. This will achieve company’s goals in effectual

manner.

Statement of profit and loss on the basis of absorption costing:

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

APPENDIX

WORKINGS OF P3

Working Note 1

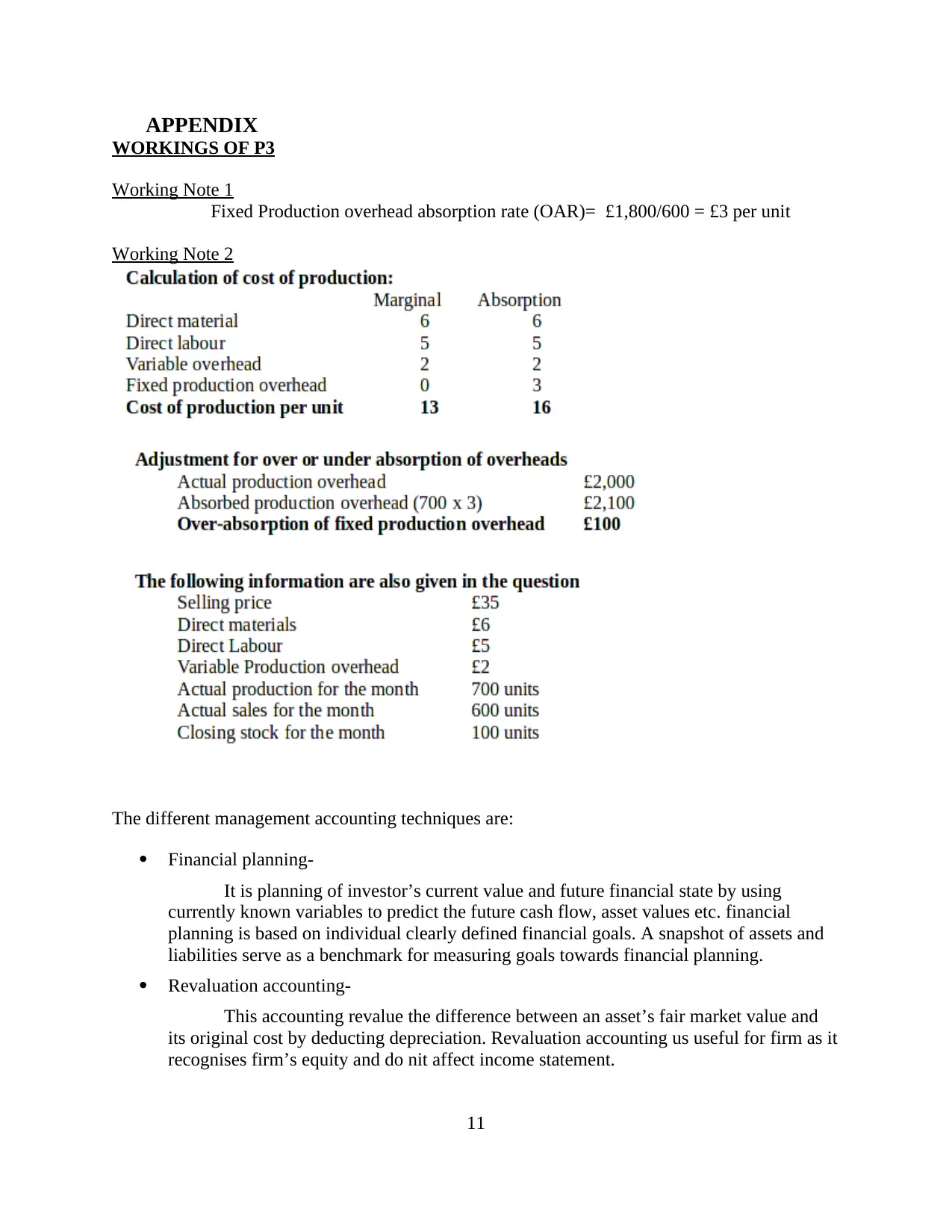

Fixed Production overhead absorption rate (OAR)= £1,800/600 = £3 per unit

Working Note 2

The different management accounting techniques are:

Financial planning-

It is planning of investor’s current value and future financial state by using

currently known variables to predict the future cash flow, asset values etc. financial

planning is based on individual clearly defined financial goals. A snapshot of assets and

liabilities serve as a benchmark for measuring goals towards financial planning.

Revaluation accounting-

This accounting revalue the difference between an asset’s fair market value and

its original cost by deducting depreciation. Revaluation accounting us useful for firm as it

recognises firm’s equity and do nit affect income statement.

11

WORKINGS OF P3

Working Note 1

Fixed Production overhead absorption rate (OAR)= £1,800/600 = £3 per unit

Working Note 2

The different management accounting techniques are:

Financial planning-

It is planning of investor’s current value and future financial state by using

currently known variables to predict the future cash flow, asset values etc. financial

planning is based on individual clearly defined financial goals. A snapshot of assets and

liabilities serve as a benchmark for measuring goals towards financial planning.

Revaluation accounting-

This accounting revalue the difference between an asset’s fair market value and

its original cost by deducting depreciation. Revaluation accounting us useful for firm as it

recognises firm’s equity and do nit affect income statement.

11

(P4)Outline advantages and disadvantages of tools used in budgetary control

Zero based budgeting-

This type of budgeting tool is based on zero base. In which all expenses must be justified

foe each new period. It means that no previous year data is used to make budget. Zero base

budgeting start from zero and every function within firm is organised for its needs and costs.

Budget is then prepared about what is needed for upcoming period by organization regardless of

previous budget whether it was higher or lower.

Advantages:

1. zero based budget are flexible budgets, focused operations. As it is based on zero basis,

flexibility is obtained in preparing budgets as no previous data is used in preparing budgets of

organization.

2. More disciplined execution can be observed in zero-based budgeting. It is useful technique to

prepare and forecast future budget for organization so that they may execute budget in enhanced

way which fulfils its goals and objectives in effectual manner.

3. Lower costs are obtained in implementing zero based budgeting. This is far better budget to

forecast best efficiency in organization. Firm need not incur additional expenses regarding

budget. It attains cost effective benefit in effectual manner.

Disadvantages:

1. It is quite resource intensive (Tucker and Lowe, 2014). It takes lot of time and effort to draw

up budget from scratch rather than using existing budget to modify it.

2. It can be gamed by managers as they get more resources into their departments. This makes

biasness among department. As such, it is not useful tool for organization.

2. Incremental budgeting-

This type of budgeting is based on simple basis. In this budget, only incremental values

are added to the existing budget to arrive at a new budget. Budget used for current fiscal year

becomes base for working on forthcoming year’s budgetary allocation. Management estimates

and assumes that all the departments will continue to operate at their current level of expenditure

12

Zero based budgeting-

This type of budgeting tool is based on zero base. In which all expenses must be justified

foe each new period. It means that no previous year data is used to make budget. Zero base

budgeting start from zero and every function within firm is organised for its needs and costs.

Budget is then prepared about what is needed for upcoming period by organization regardless of

previous budget whether it was higher or lower.

Advantages:

1. zero based budget are flexible budgets, focused operations. As it is based on zero basis,

flexibility is obtained in preparing budgets as no previous data is used in preparing budgets of

organization.

2. More disciplined execution can be observed in zero-based budgeting. It is useful technique to

prepare and forecast future budget for organization so that they may execute budget in enhanced

way which fulfils its goals and objectives in effectual manner.

3. Lower costs are obtained in implementing zero based budgeting. This is far better budget to

forecast best efficiency in organization. Firm need not incur additional expenses regarding

budget. It attains cost effective benefit in effectual manner.

Disadvantages:

1. It is quite resource intensive (Tucker and Lowe, 2014). It takes lot of time and effort to draw

up budget from scratch rather than using existing budget to modify it.

2. It can be gamed by managers as they get more resources into their departments. This makes

biasness among department. As such, it is not useful tool for organization.

2. Incremental budgeting-

This type of budgeting is based on simple basis. In this budget, only incremental values

are added to the existing budget to arrive at a new budget. Budget used for current fiscal year

becomes base for working on forthcoming year’s budgetary allocation. Management estimates

and assumes that all the departments will continue to operate at their current level of expenditure

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.