Management Accounting Report: Alpha Ltd. and Planning Tools

VerifiedAdded on 2023/01/17

|19

|4858

|31

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on its application within the context of Alpha Ltd., a medium-sized pizza manufacturing company. The report begins by defining management accounting and outlining its essential systems, including cost accounting, inventory management, and price optimization. It then describes various management accounting reporting methods, such as budgetary reports, accounts receivable aging reports, performance reports, and cost management reports, and highlights their benefits. The report further delves into the application of management accounting techniques like marginal and absorption costing, and develops financial income statements. It also assesses different planning tools and their advantages and disadvantages, concluding with a comparative analysis of how management accounting systems can lead to sustainable success, critically evaluating the integration of these tools within the organization to solve financial problems. The report emphasizes the importance of management accounting for internal stakeholders in making informed decisions to enhance profitability and productivity.

Management Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Discussing management accounting and essential requirements of its systems....................3

P2 Describing various methods of management accounting reporting.......................................4

M1 Benefits of management accounting systems and their application......................................4

D1 Critically evaluating integration of management accounting systems and reporting within

organisation..................................................................................................................................4

TASK 2............................................................................................................................................4

P3 Developing financial income statement using marginal and absorption costs.......................4

M2 Applying management accounting techniques......................................................................4

D2 Interpretations........................................................................................................................4

TASK 3............................................................................................................................................4

P4 Explaining advantages and disadvantages of different types of planning tools along with

their use in an organisation..........................................................................................................4

M3 Stating the use and application of different planning tools for preparing and forecasting

budgets.........................................................................................................................................4

P5 Comparative analysis..............................................................................................................4

M4 Critically analysing how the organisations use management accounting systems to lead to

sustainable success.......................................................................................................................4

D3 Critically evaluating the ways by which planning tools for accounting respond

appropriately to solving financial problems to lead organisations to sustainable success..........4

CONCLUSION................................................................................................................................4

REFERENCES................................................................................................................................4

2

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1 Discussing management accounting and essential requirements of its systems....................3

P2 Describing various methods of management accounting reporting.......................................4

M1 Benefits of management accounting systems and their application......................................4

D1 Critically evaluating integration of management accounting systems and reporting within

organisation..................................................................................................................................4

TASK 2............................................................................................................................................4

P3 Developing financial income statement using marginal and absorption costs.......................4

M2 Applying management accounting techniques......................................................................4

D2 Interpretations........................................................................................................................4

TASK 3............................................................................................................................................4

P4 Explaining advantages and disadvantages of different types of planning tools along with

their use in an organisation..........................................................................................................4

M3 Stating the use and application of different planning tools for preparing and forecasting

budgets.........................................................................................................................................4

P5 Comparative analysis..............................................................................................................4

M4 Critically analysing how the organisations use management accounting systems to lead to

sustainable success.......................................................................................................................4

D3 Critically evaluating the ways by which planning tools for accounting respond

appropriately to solving financial problems to lead organisations to sustainable success..........4

CONCLUSION................................................................................................................................4

REFERENCES................................................................................................................................4

2

INTRODUCTION

Management accounting is a concept of analysing the internal financial and non financial

information of an organisation in order to make relevant decisions for the growth and

development of the organisation (Almaktoom, 2017). This concept is an area of study which

facilitate management accountants to analyse the information by which they can enhance

profitability of the organisation (Carlsson-Wall, Kraus and Messner, 2016). The main aim of this

report is to develop understanding about the concepts and systems of management accounting. In

this report, a medium sized organisation is selected which is Alpha Ltd. This is a medium sized

manufacturing organisation which manufacturers local pizza. This organisation has 50 staff

members and annual turnover of £500000.

In this report, the concept of management accounting is explained in detail along with the

description and application of its systems in context of Alpha Ltd. Besides this, various

management accounting reporting methods are evaluated along with its integration with system

within the organisation. Management accounting techniques such as marginal costing, absorption

costing and CVP analysis are used to develop income statements for Alpha Ltd. In the second

part of this report, various budgetary tools are assessed along with their advantages and

disadvantages. In the last, a comparative analysis is used to compare the ways by which

management accounting techniques can be adopted.

TASK 1

P1 Discussing management accounting and essential requirements of its systems

Management accounting is a procedure of presenting the financial information using

management accounting techniques so they can be used by management accountants to make

reliable decisions for an organisation. This accounting concept involves recording to the

transactions of regular course of an organisation. This accounting procedure is collection of

various techniques and methods which require special knowledge and ability which ultimately

aims of enhance profit making ability of an organisation (Chenhall and Moers, 2015). Alpha Ltd.

is a medium scale organisation which manufacturers and then sell local pizza. The operations of

this organisation includes day to day activities due to which it is important for this organisation

to consider appropriate usage of management accounting techniques so that growth and

development of this organisation can be ensured. Apart from financial accounting, it is important

3

Management accounting is a concept of analysing the internal financial and non financial

information of an organisation in order to make relevant decisions for the growth and

development of the organisation (Almaktoom, 2017). This concept is an area of study which

facilitate management accountants to analyse the information by which they can enhance

profitability of the organisation (Carlsson-Wall, Kraus and Messner, 2016). The main aim of this

report is to develop understanding about the concepts and systems of management accounting. In

this report, a medium sized organisation is selected which is Alpha Ltd. This is a medium sized

manufacturing organisation which manufacturers local pizza. This organisation has 50 staff

members and annual turnover of £500000.

In this report, the concept of management accounting is explained in detail along with the

description and application of its systems in context of Alpha Ltd. Besides this, various

management accounting reporting methods are evaluated along with its integration with system

within the organisation. Management accounting techniques such as marginal costing, absorption

costing and CVP analysis are used to develop income statements for Alpha Ltd. In the second

part of this report, various budgetary tools are assessed along with their advantages and

disadvantages. In the last, a comparative analysis is used to compare the ways by which

management accounting techniques can be adopted.

TASK 1

P1 Discussing management accounting and essential requirements of its systems

Management accounting is a procedure of presenting the financial information using

management accounting techniques so they can be used by management accountants to make

reliable decisions for an organisation. This accounting concept involves recording to the

transactions of regular course of an organisation. This accounting procedure is collection of

various techniques and methods which require special knowledge and ability which ultimately

aims of enhance profit making ability of an organisation (Chenhall and Moers, 2015). Alpha Ltd.

is a medium scale organisation which manufacturers and then sell local pizza. The operations of

this organisation includes day to day activities due to which it is important for this organisation

to consider appropriate usage of management accounting techniques so that growth and

development of this organisation can be ensured. Apart from financial accounting, it is important

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

for Alpha Ltd. to use management accounting as well because of these accounting procedures are

way different from each other.

Financial accounting is used for the purpose to serve external and internal stakeholders but

on the contrary management accounting can only be used by internal stakeholders such as

managers and board of directors. Management accounting is not regulated by any law due to

which skill requirement in the course of preparing management reports is less than financial

reports. Also the management accounting report does not need to be audited which even makes it

more important for Alpha Ltd. as they do not have to bear expense of auditor (Jamil and et.al.,

2015).

Alpha Ltd. is at its developing stage where they must consider using management

accounting systems so that they can effectively utilise their earnings. Management accounting

systems are the basis which assist in managing different variables of an organisation. There are

various types of management accounting systems which are discussed below along with their

essential requirement in context of Alpha Ltd.:

Cost accounting system

This management accounting system is used to estimate the cost which will be incurred

by an organisation. This provides a framework by which an organisation can estimate the cost for

the products manufactured by them which is further used for the purpose of cost control. There

are broadly two types of cost accounting system i.e., process costing and job order costing. In the

case of process costing, an organisation estimates the cost which can be incurred by completing

their whole manufacturing process. On the other hand, job order costing includes estimation of

cost of each job order. In context of Alpha Ltd. both of these cost accounting techniques are used

by which they predict cost expense in their manufacturing process and cost expense of special

pizza orders which they get. These techniques help them to first estimate their incurred cost and

then control that cost by using measures of economies of scale and optimum utilisation of

resources (Jukic and Hedi, 2014).

Inventory management system

In this management accounting system, an organisation develops a framework in which

they record all the transactions of ordering and storing the inventory. This inventory includes raw

material, semi finished goods and even finished goods. The aim behind sing this system is to

4

way different from each other.

Financial accounting is used for the purpose to serve external and internal stakeholders but

on the contrary management accounting can only be used by internal stakeholders such as

managers and board of directors. Management accounting is not regulated by any law due to

which skill requirement in the course of preparing management reports is less than financial

reports. Also the management accounting report does not need to be audited which even makes it

more important for Alpha Ltd. as they do not have to bear expense of auditor (Jamil and et.al.,

2015).

Alpha Ltd. is at its developing stage where they must consider using management

accounting systems so that they can effectively utilise their earnings. Management accounting

systems are the basis which assist in managing different variables of an organisation. There are

various types of management accounting systems which are discussed below along with their

essential requirement in context of Alpha Ltd.:

Cost accounting system

This management accounting system is used to estimate the cost which will be incurred

by an organisation. This provides a framework by which an organisation can estimate the cost for

the products manufactured by them which is further used for the purpose of cost control. There

are broadly two types of cost accounting system i.e., process costing and job order costing. In the

case of process costing, an organisation estimates the cost which can be incurred by completing

their whole manufacturing process. On the other hand, job order costing includes estimation of

cost of each job order. In context of Alpha Ltd. both of these cost accounting techniques are used

by which they predict cost expense in their manufacturing process and cost expense of special

pizza orders which they get. These techniques help them to first estimate their incurred cost and

then control that cost by using measures of economies of scale and optimum utilisation of

resources (Jukic and Hedi, 2014).

Inventory management system

In this management accounting system, an organisation develops a framework in which

they record all the transactions of ordering and storing the inventory. This inventory includes raw

material, semi finished goods and even finished goods. The aim behind sing this system is to

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

optimally use the available inventory. There are various techniques by which an organisation can

use manage their inventory. These techniques are FIFO, LIFO etc.

FIFO is a technique in which organisations first uses the inventory which is first bought

by them and in case of LIFO, organisation first uses the inventory which is last bought by them

(Kaplan and Atkinson, 2015). Alpha Ltd. is a pizza manufacturing company which develops

their products using raw material which is perishable in nature due to which they must use FIFO

method by which their raw material will be fully utilised and wastage will be minimised. These

are the essential requirements of this system for Alpha Ltd. due to which they must more

emphasise in effectively using management accounting and its systems.

Price optimisation system

This management accounting system is the based on mathematical and economic

equations which helps in analysing the demand for the products at various price levels. The aim

of using this system is to set optimised prices for products which can help in raising the demand

and profitability. In context of Alpha Ltd. which is a pizza manufacturing company must use this

management accounting system which is essentially required by them as by this, they can set

flexible prices for their produced pizzas which will increase the demand and as well

organisation’s profitability.

P2 Describing various methods of management accounting reporting

Management accounting reporting is a process of creating various reports which helps an

organisation to present financial information in an effective way so that profitable decision can

be made. Methods of management accounting reporting includes various reports which are

developed by management accountants to record day to day activities of an organisation. These

management accounting reports or reporting methods are discussed below:

Budgetary report

A budget report is a record of estimated costs which an organisation estimates to plan

their expenses. This report includes prediction of future costs and revenues which can occur

within an organisation. The basic objective behind developing this report is to predict

contingencies which can be seen in future period so that provisions for those contingencies can

be developed and a prevention action plan can be prepared. Alpha Ltd. can prepare this report in

which they can list all future revenues and expenses which expect to be occurred. By this, they

can be prepared for future contingencies which might suffer their operations.

5

use manage their inventory. These techniques are FIFO, LIFO etc.

FIFO is a technique in which organisations first uses the inventory which is first bought

by them and in case of LIFO, organisation first uses the inventory which is last bought by them

(Kaplan and Atkinson, 2015). Alpha Ltd. is a pizza manufacturing company which develops

their products using raw material which is perishable in nature due to which they must use FIFO

method by which their raw material will be fully utilised and wastage will be minimised. These

are the essential requirements of this system for Alpha Ltd. due to which they must more

emphasise in effectively using management accounting and its systems.

Price optimisation system

This management accounting system is the based on mathematical and economic

equations which helps in analysing the demand for the products at various price levels. The aim

of using this system is to set optimised prices for products which can help in raising the demand

and profitability. In context of Alpha Ltd. which is a pizza manufacturing company must use this

management accounting system which is essentially required by them as by this, they can set

flexible prices for their produced pizzas which will increase the demand and as well

organisation’s profitability.

P2 Describing various methods of management accounting reporting

Management accounting reporting is a process of creating various reports which helps an

organisation to present financial information in an effective way so that profitable decision can

be made. Methods of management accounting reporting includes various reports which are

developed by management accountants to record day to day activities of an organisation. These

management accounting reports or reporting methods are discussed below:

Budgetary report

A budget report is a record of estimated costs which an organisation estimates to plan

their expenses. This report includes prediction of future costs and revenues which can occur

within an organisation. The basic objective behind developing this report is to predict

contingencies which can be seen in future period so that provisions for those contingencies can

be developed and a prevention action plan can be prepared. Alpha Ltd. can prepare this report in

which they can list all future revenues and expenses which expect to be occurred. By this, they

can be prepared for future contingencies which might suffer their operations.

5

Account Receivable Aging Report

According to this management accounting reporting method, every organisation must

develop a report which records all the transactions which are done on credit and organisation is

entitle to receive an amount (Karadag, 2015). The main aim behind developing this report is to

keep the track of the values which company is entitled to receive from its creditors. Using this

report, an organisation can also identify the defaulters and make suitable legal actions. Alpha

Ltd. is a medium scale organisation which manufactures and sells pizzas to local public. The

credit transactions of this organisation are comparatively less and this organisation does not

heavily rely upon extending credit. But in order to identify the defaulters, it is important for

Alpha Ltd. to use this reporting method and develop a report which can transact each and every

transaction which is done by providing or extending credit to their customers.

Performance report

It is one of the most influential reports which helps an organisation to improve overall

performance of the employees and the processes of an organisation. In this report, continuous

performance of each and every employee of an organisation is first recorded and then analysed

by comparing it to benchmarks. This report enables to review contribution of each employee

against fulfilment of the organisational objectives. In context of Alpha ltd., human resource

manager can analyse the performance of the employees of this organisation and then

communicate that information with management accountants so that they can record that

information in an understandable form and then continuously review their performance in order

to make sure their full potential to enhance productivity of the organisation.

Cost management report

This management accounting report is one of the most basic report which helps an

organisation to records all the costs which are incurred by them for producing their products. The

main aim of developing this report is to record all the cost transactions so that expense and

spending limit of an organisation can be managed and controlled. Alpha Ltd. can use this report

to analyse their cost expenses which are incurred by them regularly and then at the end of the

month they can compare their cost report which budgetary report to identify the variance.

All the above reports are usually developed by management accountants and are presented

effectively so that management decisions can be made. It is important for organisations like

Alpha Ltd. to develop these reports and present their managerial accounting information in them

6

According to this management accounting reporting method, every organisation must

develop a report which records all the transactions which are done on credit and organisation is

entitle to receive an amount (Karadag, 2015). The main aim behind developing this report is to

keep the track of the values which company is entitled to receive from its creditors. Using this

report, an organisation can also identify the defaulters and make suitable legal actions. Alpha

Ltd. is a medium scale organisation which manufactures and sells pizzas to local public. The

credit transactions of this organisation are comparatively less and this organisation does not

heavily rely upon extending credit. But in order to identify the defaulters, it is important for

Alpha Ltd. to use this reporting method and develop a report which can transact each and every

transaction which is done by providing or extending credit to their customers.

Performance report

It is one of the most influential reports which helps an organisation to improve overall

performance of the employees and the processes of an organisation. In this report, continuous

performance of each and every employee of an organisation is first recorded and then analysed

by comparing it to benchmarks. This report enables to review contribution of each employee

against fulfilment of the organisational objectives. In context of Alpha ltd., human resource

manager can analyse the performance of the employees of this organisation and then

communicate that information with management accountants so that they can record that

information in an understandable form and then continuously review their performance in order

to make sure their full potential to enhance productivity of the organisation.

Cost management report

This management accounting report is one of the most basic report which helps an

organisation to records all the costs which are incurred by them for producing their products. The

main aim of developing this report is to record all the cost transactions so that expense and

spending limit of an organisation can be managed and controlled. Alpha Ltd. can use this report

to analyse their cost expenses which are incurred by them regularly and then at the end of the

month they can compare their cost report which budgetary report to identify the variance.

All the above reports are usually developed by management accountants and are presented

effectively so that management decisions can be made. It is important for organisations like

Alpha Ltd. to develop these reports and present their managerial accounting information in them

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

to assist stakeholders such as management and employees. Management and employees are the

internal stakeholders of an organisation which can analyse the true financial position of an

organisation using above mentioned reports and can make effective and suitable decisions so that

they can ensure organisation’s productivity and profitability.

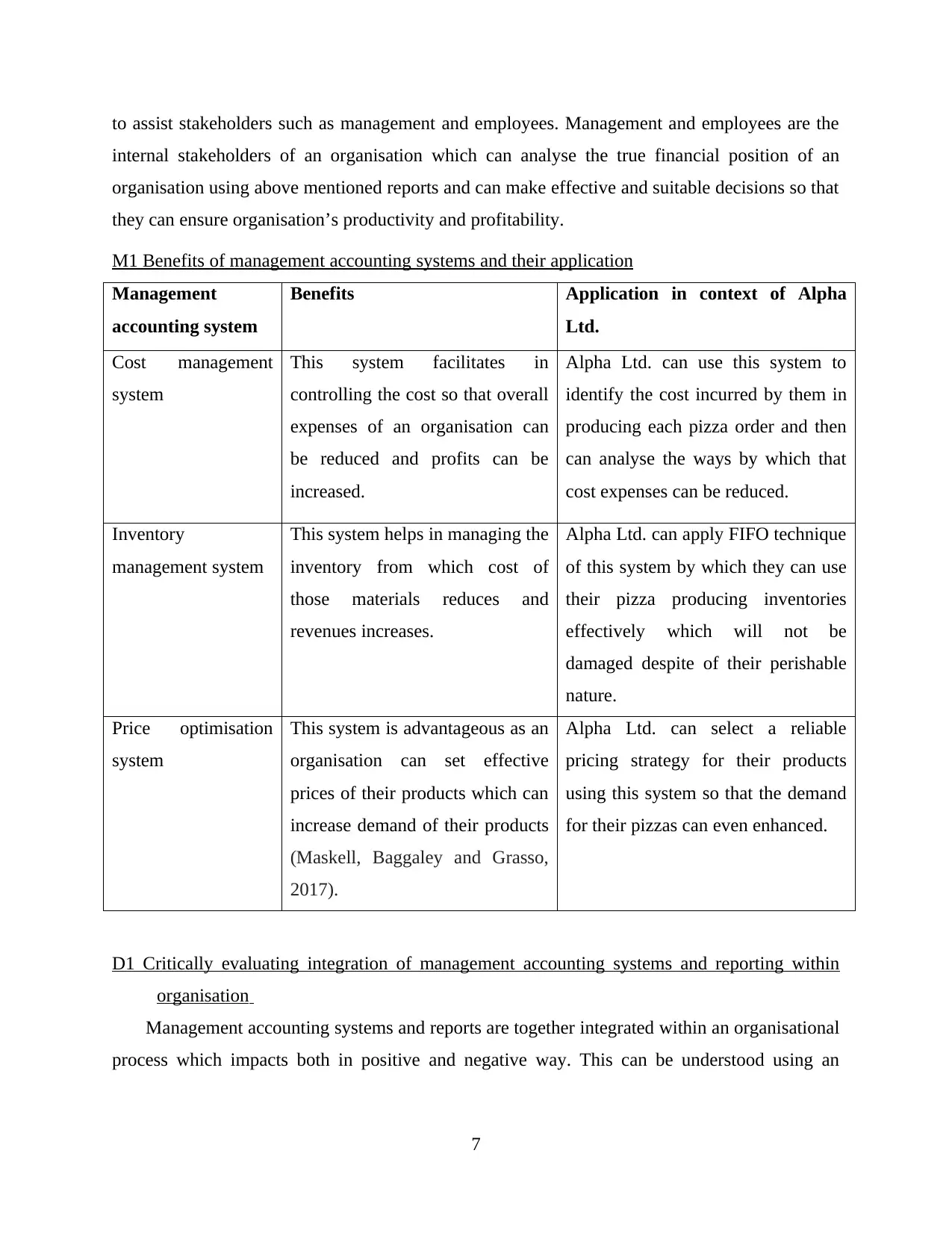

M1 Benefits of management accounting systems and their application

Management

accounting system

Benefits Application in context of Alpha

Ltd.

Cost management

system

This system facilitates in

controlling the cost so that overall

expenses of an organisation can

be reduced and profits can be

increased.

Alpha Ltd. can use this system to

identify the cost incurred by them in

producing each pizza order and then

can analyse the ways by which that

cost expenses can be reduced.

Inventory

management system

This system helps in managing the

inventory from which cost of

those materials reduces and

revenues increases.

Alpha Ltd. can apply FIFO technique

of this system by which they can use

their pizza producing inventories

effectively which will not be

damaged despite of their perishable

nature.

Price optimisation

system

This system is advantageous as an

organisation can set effective

prices of their products which can

increase demand of their products

(Maskell, Baggaley and Grasso,

2017).

Alpha Ltd. can select a reliable

pricing strategy for their products

using this system so that the demand

for their pizzas can even enhanced.

D1 Critically evaluating integration of management accounting systems and reporting within

organisation

Management accounting systems and reports are together integrated within an organisational

process which impacts both in positive and negative way. This can be understood using an

7

internal stakeholders of an organisation which can analyse the true financial position of an

organisation using above mentioned reports and can make effective and suitable decisions so that

they can ensure organisation’s productivity and profitability.

M1 Benefits of management accounting systems and their application

Management

accounting system

Benefits Application in context of Alpha

Ltd.

Cost management

system

This system facilitates in

controlling the cost so that overall

expenses of an organisation can

be reduced and profits can be

increased.

Alpha Ltd. can use this system to

identify the cost incurred by them in

producing each pizza order and then

can analyse the ways by which that

cost expenses can be reduced.

Inventory

management system

This system helps in managing the

inventory from which cost of

those materials reduces and

revenues increases.

Alpha Ltd. can apply FIFO technique

of this system by which they can use

their pizza producing inventories

effectively which will not be

damaged despite of their perishable

nature.

Price optimisation

system

This system is advantageous as an

organisation can set effective

prices of their products which can

increase demand of their products

(Maskell, Baggaley and Grasso,

2017).

Alpha Ltd. can select a reliable

pricing strategy for their products

using this system so that the demand

for their pizzas can even enhanced.

D1 Critically evaluating integration of management accounting systems and reporting within

organisation

Management accounting systems and reports are together integrated within an organisational

process which impacts both in positive and negative way. This can be understood using an

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

example of cost accounting system and cost management report in the process of manufacturing

of Alpha Ltd.

Management accountants first use the management accounting system to identify all the cost

incurred by manufacturing unit of Alpha Ltd in producing pizzas for all the orders. After this,

they use management accounting report to record all these costs in a presentable way. By this,

Alpha Ltd. can control their spending level. But by this, much time and money of the

organisation’s employees will be utilised.

TASK 2

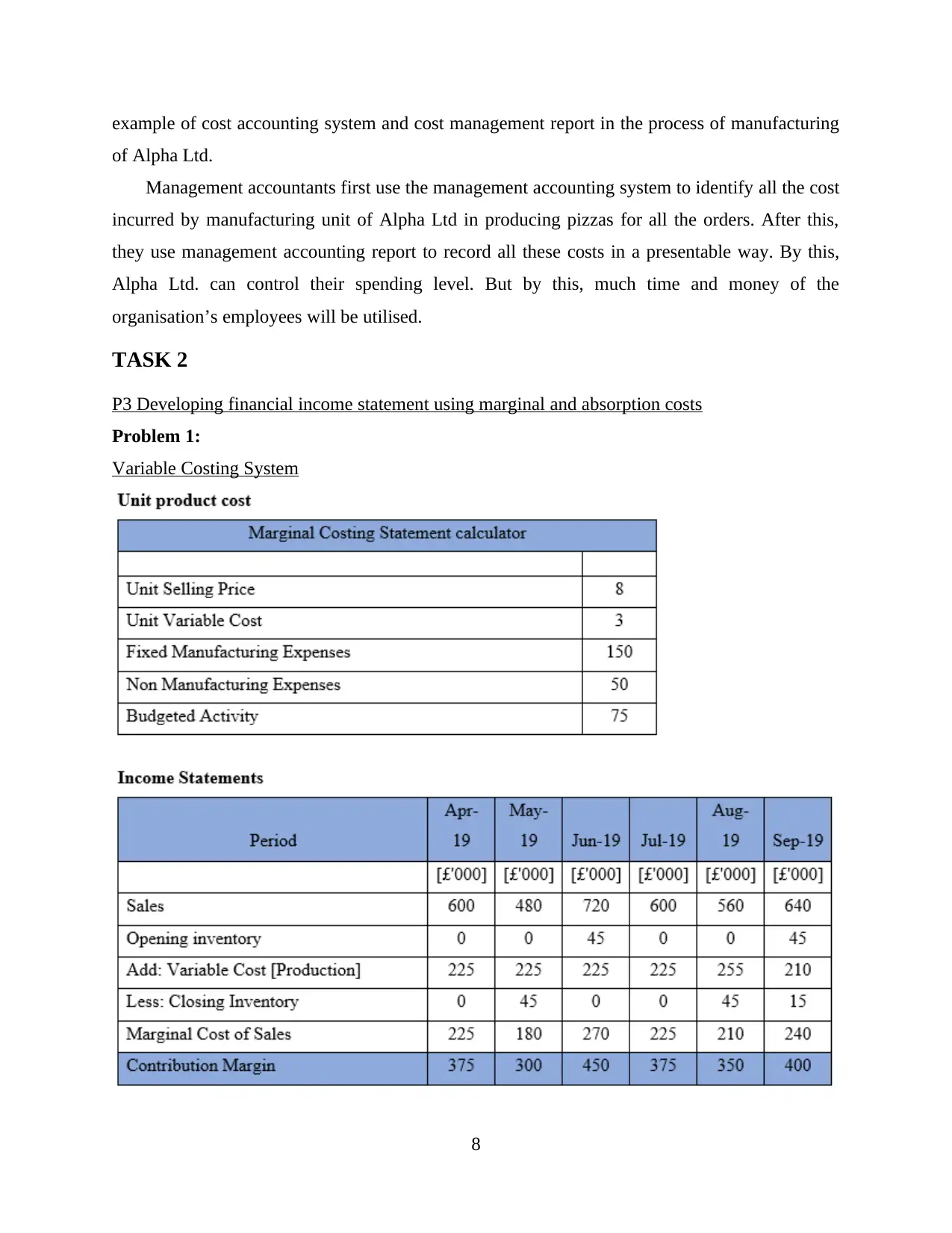

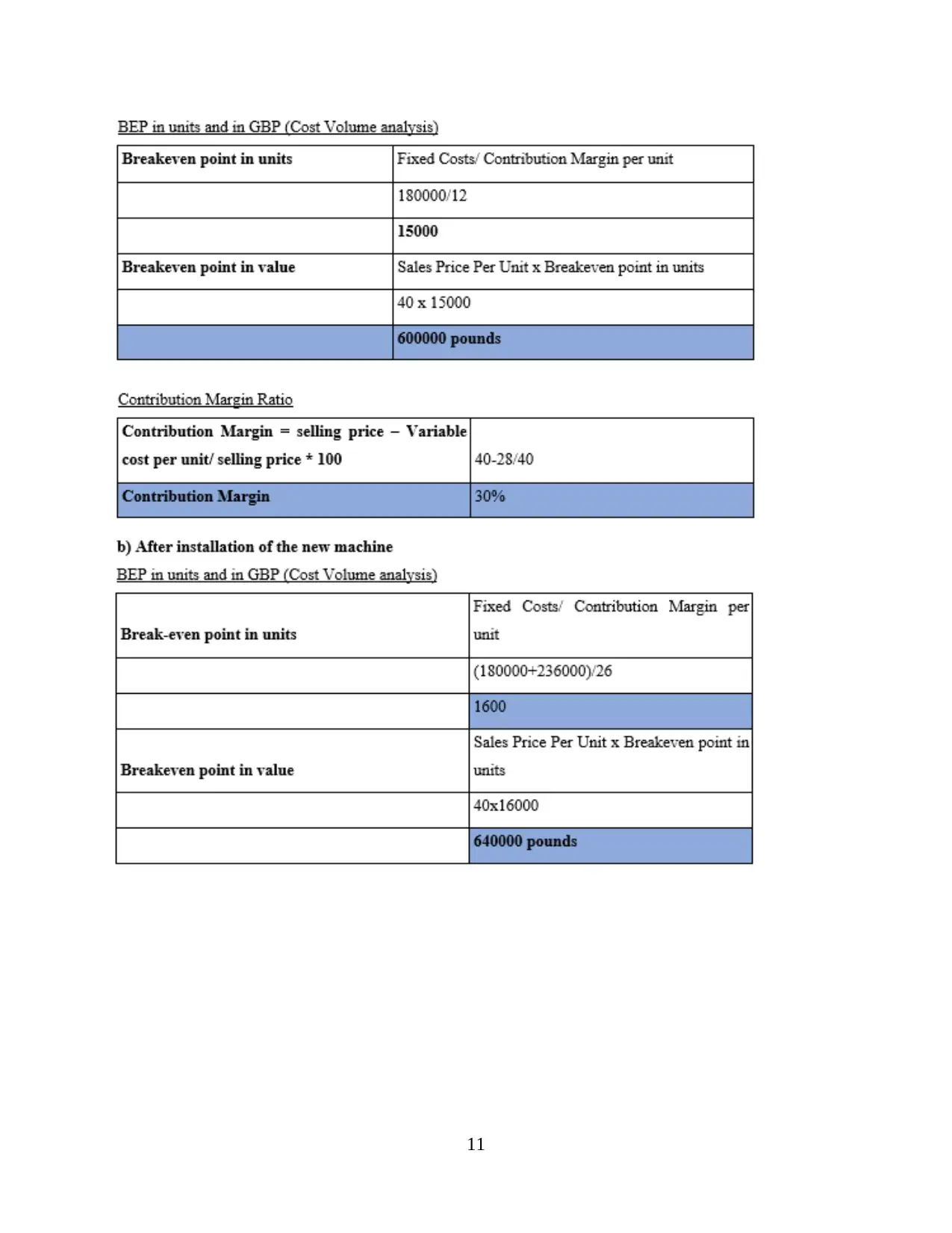

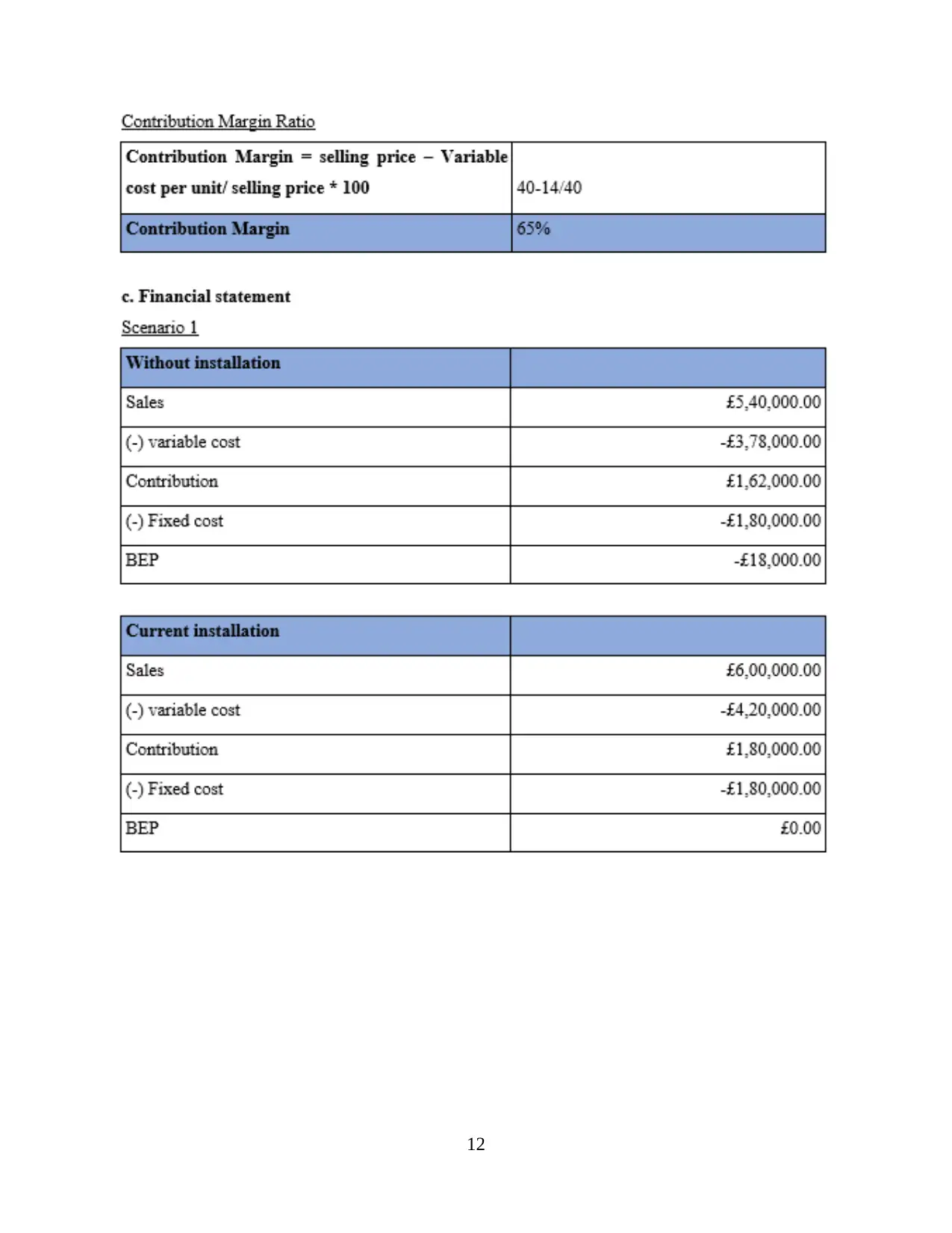

P3 Developing financial income statement using marginal and absorption costs

Problem 1:

Variable Costing System

8

of Alpha Ltd.

Management accountants first use the management accounting system to identify all the cost

incurred by manufacturing unit of Alpha Ltd in producing pizzas for all the orders. After this,

they use management accounting report to record all these costs in a presentable way. By this,

Alpha Ltd. can control their spending level. But by this, much time and money of the

organisation’s employees will be utilised.

TASK 2

P3 Developing financial income statement using marginal and absorption costs

Problem 1:

Variable Costing System

8

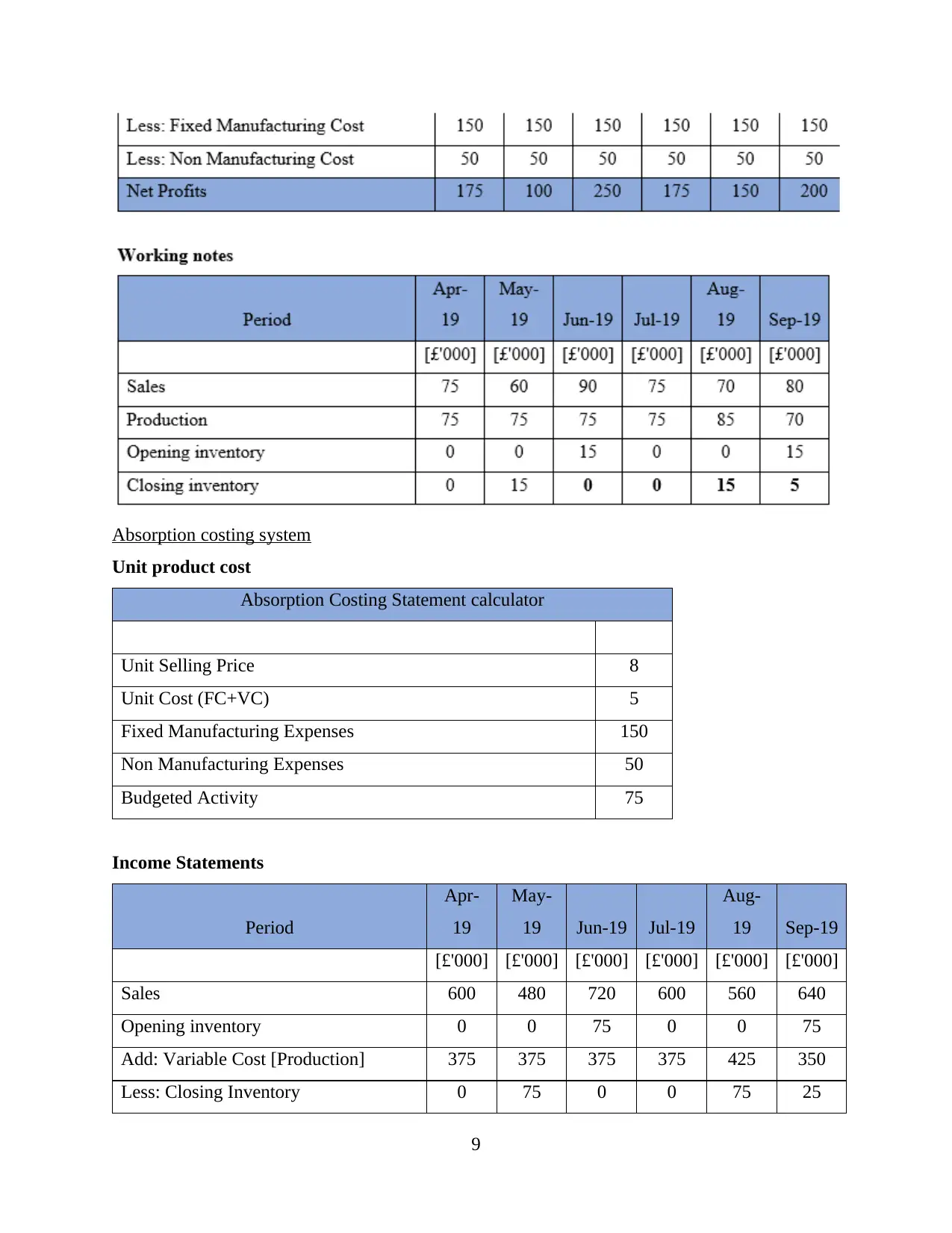

Absorption costing system

Unit product cost

Absorption Costing Statement calculator

Unit Selling Price 8

Unit Cost (FC+VC) 5

Fixed Manufacturing Expenses 150

Non Manufacturing Expenses 50

Budgeted Activity 75

Income Statements

Period

Apr-

19

May-

19 Jun-19 Jul-19

Aug-

19 Sep-19

[£'000] [£'000] [£'000] [£'000] [£'000] [£'000]

Sales 600 480 720 600 560 640

Opening inventory 0 0 75 0 0 75

Add: Variable Cost [Production] 375 375 375 375 425 350

Less: Closing Inventory 0 75 0 0 75 25

9

Unit product cost

Absorption Costing Statement calculator

Unit Selling Price 8

Unit Cost (FC+VC) 5

Fixed Manufacturing Expenses 150

Non Manufacturing Expenses 50

Budgeted Activity 75

Income Statements

Period

Apr-

19

May-

19 Jun-19 Jul-19

Aug-

19 Sep-19

[£'000] [£'000] [£'000] [£'000] [£'000] [£'000]

Sales 600 480 720 600 560 640

Opening inventory 0 0 75 0 0 75

Add: Variable Cost [Production] 375 375 375 375 425 350

Less: Closing Inventory 0 75 0 0 75 25

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Marginal Cost of Sales 375 300 450 375 350 400

Gross Profit 225 180 270 225 210 240

Adjustment for Overheads 0 0 0 0 -20 10

Less: Non Manufacturing Cost 50 50 50 50 50 50

Net Profits 175 130 220 175 180 180

Working notes

Period

Apr-

19

May-

19 Jun-19 Jul-19

Aug-

19 Sep-19

[£'000] [£'000] [£'000] [£'000] [£'000] [£'000]

Sales 75 60 90 75 70 80

Production 75 75 75 75 85 70

Opening inventory 0 0 15 0 0 15

Closing inventory 0 15 0 0 15 5

Schedule of reconciliation

Period Apr-19 May-19

Jun-

19 Jul-19

Aug-

19 Sep-19

[£'000 ] [£'000 ]

[£'00

0 ]

[£'00

0 ]

[£'00

0 ]

[£'000

]

Net Profits under Absorption Costing 175 130 220 175 180 180

ADD : Fixed Overheads in opening 0 0 30 0 0 30

LESS: Fixed Overheads in closing 0 30 0 0 30 10

Net Profits under Marginal Costing 175 100 250 175 150 200

M2 Applying management accounting techniques

Problem 2:

a) Before installation of the new machine

10

Gross Profit 225 180 270 225 210 240

Adjustment for Overheads 0 0 0 0 -20 10

Less: Non Manufacturing Cost 50 50 50 50 50 50

Net Profits 175 130 220 175 180 180

Working notes

Period

Apr-

19

May-

19 Jun-19 Jul-19

Aug-

19 Sep-19

[£'000] [£'000] [£'000] [£'000] [£'000] [£'000]

Sales 75 60 90 75 70 80

Production 75 75 75 75 85 70

Opening inventory 0 0 15 0 0 15

Closing inventory 0 15 0 0 15 5

Schedule of reconciliation

Period Apr-19 May-19

Jun-

19 Jul-19

Aug-

19 Sep-19

[£'000 ] [£'000 ]

[£'00

0 ]

[£'00

0 ]

[£'00

0 ]

[£'000

]

Net Profits under Absorption Costing 175 130 220 175 180 180

ADD : Fixed Overheads in opening 0 0 30 0 0 30

LESS: Fixed Overheads in closing 0 30 0 0 30 10

Net Profits under Marginal Costing 175 100 250 175 150 200

M2 Applying management accounting techniques

Problem 2:

a) Before installation of the new machine

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

11

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.