Analysis of Management Accounting Systems and Reporting Methods

VerifiedAdded on 2020/11/23

|13

|4328

|154

Report

AI Summary

This report delves into the core principles and practical applications of management accounting within the context of George Lines, a concrete distribution company. It explores various management accounting systems, including cost accounting, price optimization, job costing, and inventory management, evaluating their benefits and applications. The report examines different management accounting reporting methods such as performance reports, accounts receivable reports, inventory management reports, and job cost reporting, highlighting their significance in decision-making. Furthermore, it analyzes cost calculation techniques like marginal costing and absorption costing, alongside break-even analysis and margin of safety calculations. The report also covers budgetary control and planning tools, assessing their role in financial planning and forecasting, and discusses how management accounting systems respond to and resolve financial problems. Overall, the report provides a comprehensive overview of how management accounting supports organizational planning, control, and financial success.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Management accounting and its types of management accounting systems...................1

P2: Different methods used for management accounting reporting.......................................2

M1: Evaluate the benefits of management accounting system and its applications...............3

D1: Management accounting system and its reporting are integrated within organisational

process....................................................................................................................................4

TASK 2............................................................................................................................................4

P3: Calculation of cost using an appropriate technique.........................................................4

M2 Accounting techniques.....................................................................................................6

D2: Data interpretation...........................................................................................................6

TASK 3............................................................................................................................................6

P4: Budgetary control and planning tools used in budgetary control with its advantages and

disadvantages..........................................................................................................................6

M3: Uses and applications of planning tools for preparing and forecasting budgets............8

TASK 4............................................................................................................................................8

P5: Responses of management accounting system to deal with financial problems..............8

M4: Management accounting lead organisation to sustainable success in responding to

financial problems................................................................................................................10

D3: Planning tools respond appropriately to resolve financial problems.............................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Management accounting and its types of management accounting systems...................1

P2: Different methods used for management accounting reporting.......................................2

M1: Evaluate the benefits of management accounting system and its applications...............3

D1: Management accounting system and its reporting are integrated within organisational

process....................................................................................................................................4

TASK 2............................................................................................................................................4

P3: Calculation of cost using an appropriate technique.........................................................4

M2 Accounting techniques.....................................................................................................6

D2: Data interpretation...........................................................................................................6

TASK 3............................................................................................................................................6

P4: Budgetary control and planning tools used in budgetary control with its advantages and

disadvantages..........................................................................................................................6

M3: Uses and applications of planning tools for preparing and forecasting budgets............8

TASK 4............................................................................................................................................8

P5: Responses of management accounting system to deal with financial problems..............8

M4: Management accounting lead organisation to sustainable success in responding to

financial problems................................................................................................................10

D3: Planning tools respond appropriately to resolve financial problems.............................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Management accounting is a process of identification, measurement, accumulation,

analysis, interpretation and communication of financial information used by management to

plan, control within an organisation and assures the use of accountability for its resources.

George Lines is a concrete distributors which is an autonomous civil and landscape

merchants settled in West London. In this project, company is dealing in groundwork of supply

materials like natural stone and concrete. Company uses efficient accounting framework to thrive

success. Company follows several management accounting systems, reporting tools, budgetary

control techniques and tools for identifying it's profitability status that would be discussed in the

report. It also uses various planning tools used in budgetary control and evaluate use different

management accounting systems for resolving financial issues that will be discussed in this

report.(Knežević, Rakočević and Đurić, 2011).

TASK 1

P1: Management accounting and its types of management accounting systems

Management accounting is an approach of analysing financial information and sets

guidelines use in the arrangement and development of company. The primary aim of

management accounting is to assist the management to take qualitative decision for controlling

the company's working effectively. Management accounting system refers to supply of more

meaningful information to all level of management with the use of various accounting systems.

George Lines uses various management accounting systems for translating its objectives into

achievements within a particular time period. Cost accounting, inventory management, job cost

and price optimisation system helps management in analysing and interpreting information that

company have to follow in achieving goals. Different management accounting systems are

explained below:

Cost accounting systems: This system is used by manufacturer for recording and

accumulating cost of raw materials in their production activities as they processed through

various production stages and then turned into finished goods in specific time. George Lines is

perpetually developing a variety of landscaping products like precast concrete and nature stone

which they supply to builders and merchants within country. Management uses various cost

accounting systems like actual costing for determining the actual cost of raw material, labour

and variable overheads and standard costing for estimating cost of manufacturing products under

1

Management accounting is a process of identification, measurement, accumulation,

analysis, interpretation and communication of financial information used by management to

plan, control within an organisation and assures the use of accountability for its resources.

George Lines is a concrete distributors which is an autonomous civil and landscape

merchants settled in West London. In this project, company is dealing in groundwork of supply

materials like natural stone and concrete. Company uses efficient accounting framework to thrive

success. Company follows several management accounting systems, reporting tools, budgetary

control techniques and tools for identifying it's profitability status that would be discussed in the

report. It also uses various planning tools used in budgetary control and evaluate use different

management accounting systems for resolving financial issues that will be discussed in this

report.(Knežević, Rakočević and Đurić, 2011).

TASK 1

P1: Management accounting and its types of management accounting systems

Management accounting is an approach of analysing financial information and sets

guidelines use in the arrangement and development of company. The primary aim of

management accounting is to assist the management to take qualitative decision for controlling

the company's working effectively. Management accounting system refers to supply of more

meaningful information to all level of management with the use of various accounting systems.

George Lines uses various management accounting systems for translating its objectives into

achievements within a particular time period. Cost accounting, inventory management, job cost

and price optimisation system helps management in analysing and interpreting information that

company have to follow in achieving goals. Different management accounting systems are

explained below:

Cost accounting systems: This system is used by manufacturer for recording and

accumulating cost of raw materials in their production activities as they processed through

various production stages and then turned into finished goods in specific time. George Lines is

perpetually developing a variety of landscaping products like precast concrete and nature stone

which they supply to builders and merchants within country. Management uses various cost

accounting systems like actual costing for determining the actual cost of raw material, labour

and variable overheads and standard costing for estimating cost of manufacturing products under

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

normal conditions so that they properly utilized their resources against future uncertainty

(Schuster, 2015).

Price optimisation systems: It is a systematic approach that calculate variation in

demand of product at different levels of price and combines that content with information on

costs and stock levels to recommend prices for future profitability. George Lines is a concrete

manufacturer and distributor which adopt price optimisation system for identifying it's product

effective price i.e. recommended for improving profits and is one of most preferred decisions

made by the management. With the help of this system George Lines identify its customer's

willingness to pay for their product.

Job costing systems: In this system, management assign the manufacturing costs that a

company incur for a particular job. This system is broadly used in preparing effective budgets.

George Lines is working in distribution of stone and concrete so they have to focus on both

levels of product. Company follow process costing which is a method of job costing system for

identifying single manufacturing cost at different levels and measures their performance.

Inventory management system: This accounting system is planned for tracking the flow

of inventory continuously through different stages of production. George Lines is small scale

organisation and is expanding company for concrete distributor. Company use FIFO method for

valuation of inventory which help to determine the inflow and outflow of its inventory. With the

help of this system George Lines control its inventory and manage the product demand in future.

P2: Different methods used for management accounting reporting

Management accounting report is a tool used for understanding management reports that

is useful in decision making. Such reports includes company's quarterly or yearly performance in

the financial statements consist of income statements, balance sheet and cash flows statements

etc. George Lines uses different methods of reporting like performance reporting, job cost,

inventory management and account receivable reporting etc. for developing impressive plans

which improves company's performance so that they expand their market without any issues

(Venkatesh and Blaskovich, 2012).

Different types of management accounting reporting are explained below:

Performance report: This report measure continuous performance of organisation

which involves collecting and scattering project data, communicating its progress to

shareholders. It includes analysis of past performance, summary of alternation authorised in

2

(Schuster, 2015).

Price optimisation systems: It is a systematic approach that calculate variation in

demand of product at different levels of price and combines that content with information on

costs and stock levels to recommend prices for future profitability. George Lines is a concrete

manufacturer and distributor which adopt price optimisation system for identifying it's product

effective price i.e. recommended for improving profits and is one of most preferred decisions

made by the management. With the help of this system George Lines identify its customer's

willingness to pay for their product.

Job costing systems: In this system, management assign the manufacturing costs that a

company incur for a particular job. This system is broadly used in preparing effective budgets.

George Lines is working in distribution of stone and concrete so they have to focus on both

levels of product. Company follow process costing which is a method of job costing system for

identifying single manufacturing cost at different levels and measures their performance.

Inventory management system: This accounting system is planned for tracking the flow

of inventory continuously through different stages of production. George Lines is small scale

organisation and is expanding company for concrete distributor. Company use FIFO method for

valuation of inventory which help to determine the inflow and outflow of its inventory. With the

help of this system George Lines control its inventory and manage the product demand in future.

P2: Different methods used for management accounting reporting

Management accounting report is a tool used for understanding management reports that

is useful in decision making. Such reports includes company's quarterly or yearly performance in

the financial statements consist of income statements, balance sheet and cash flows statements

etc. George Lines uses different methods of reporting like performance reporting, job cost,

inventory management and account receivable reporting etc. for developing impressive plans

which improves company's performance so that they expand their market without any issues

(Venkatesh and Blaskovich, 2012).

Different types of management accounting reporting are explained below:

Performance report: This report measure continuous performance of organisation

which involves collecting and scattering project data, communicating its progress to

shareholders. It includes analysis of past performance, summary of alternation authorised in

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

reporting period, present status of risks and outcomes of variance analysis etc. George Lines

prepares performance report for evaluating it's current performance within various departments

and forecasting future progress by comparing actual production and distribution with budgeted.

Company set certain laws and guidelines for manages at all level of management so that they

identify errors and resolve issues in time.

Account receivable reports: This is also known as account receivable ageing because it

determines the age of definite items. This report includes both detailed and summarized form of

information regarding customer's present and past due bills, on account credits and cash

amounts, debit memos etc. Company provides many receivable reports like ageing by account,

amount, collector and salesperson. George Lines consider this tool as an important tool because

it is used in determining details about overdue customer's invoices, credit customers, average

collection period and it also identify frequency of collection period for increasing their

distribution practices.

Inventory management reports: This report is created for maintaining a physical

inventory or products used efficiently in manufacturing process. Inventory wastage, labour cost

per hour or overhead costs per unit etc. are various elements included in these reports. ABC

analysis and EOQ are the examples of inventory management reporting. Economic order

quantity is an important method for determining ordering and holding costs of inventory. George

Lines wants to manage their inventories and finds EOQ method is valuable for maintaining

optimum amount of inventory.

Job cost reporting: This reporting system refers to ongoing cost of a project maintained

correctly in order to work. It helps in identifying issues related to present job and avoid those

problems in future job. George Lines is a small scale company and wants to expand in future for

this company choose job cost reporting method for detects its expenses like cost of direct

material, labour, equipments etc. of a particular assignment related to current status and evaluate

its future profitability (Weygandt, Kimmel and Kieso, 2015).

M1: Evaluate the benefits of management accounting system and its applications

Management accounting system Benefits

Cost accounting system It leads to reduction in costs.

It eliminate losses and inefficiencies by

3

prepares performance report for evaluating it's current performance within various departments

and forecasting future progress by comparing actual production and distribution with budgeted.

Company set certain laws and guidelines for manages at all level of management so that they

identify errors and resolve issues in time.

Account receivable reports: This is also known as account receivable ageing because it

determines the age of definite items. This report includes both detailed and summarized form of

information regarding customer's present and past due bills, on account credits and cash

amounts, debit memos etc. Company provides many receivable reports like ageing by account,

amount, collector and salesperson. George Lines consider this tool as an important tool because

it is used in determining details about overdue customer's invoices, credit customers, average

collection period and it also identify frequency of collection period for increasing their

distribution practices.

Inventory management reports: This report is created for maintaining a physical

inventory or products used efficiently in manufacturing process. Inventory wastage, labour cost

per hour or overhead costs per unit etc. are various elements included in these reports. ABC

analysis and EOQ are the examples of inventory management reporting. Economic order

quantity is an important method for determining ordering and holding costs of inventory. George

Lines wants to manage their inventories and finds EOQ method is valuable for maintaining

optimum amount of inventory.

Job cost reporting: This reporting system refers to ongoing cost of a project maintained

correctly in order to work. It helps in identifying issues related to present job and avoid those

problems in future job. George Lines is a small scale company and wants to expand in future for

this company choose job cost reporting method for detects its expenses like cost of direct

material, labour, equipments etc. of a particular assignment related to current status and evaluate

its future profitability (Weygandt, Kimmel and Kieso, 2015).

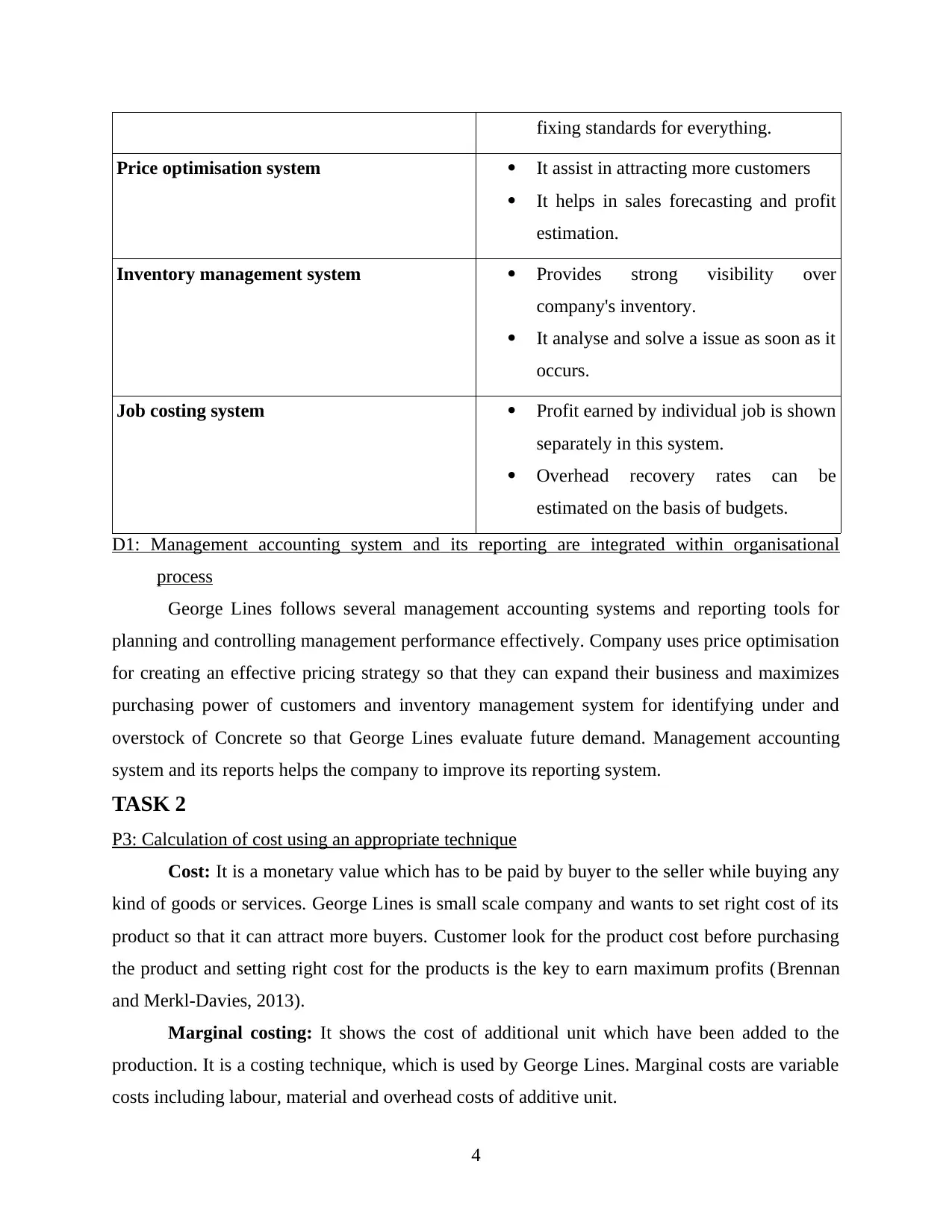

M1: Evaluate the benefits of management accounting system and its applications

Management accounting system Benefits

Cost accounting system It leads to reduction in costs.

It eliminate losses and inefficiencies by

3

fixing standards for everything.

Price optimisation system It assist in attracting more customers

It helps in sales forecasting and profit

estimation.

Inventory management system Provides strong visibility over

company's inventory.

It analyse and solve a issue as soon as it

occurs.

Job costing system Profit earned by individual job is shown

separately in this system.

Overhead recovery rates can be

estimated on the basis of budgets.

D1: Management accounting system and its reporting are integrated within organisational

process

George Lines follows several management accounting systems and reporting tools for

planning and controlling management performance effectively. Company uses price optimisation

for creating an effective pricing strategy so that they can expand their business and maximizes

purchasing power of customers and inventory management system for identifying under and

overstock of Concrete so that George Lines evaluate future demand. Management accounting

system and its reports helps the company to improve its reporting system.

TASK 2

P3: Calculation of cost using an appropriate technique

Cost: It is a monetary value which has to be paid by buyer to the seller while buying any

kind of goods or services. George Lines is small scale company and wants to set right cost of its

product so that it can attract more buyers. Customer look for the product cost before purchasing

the product and setting right cost for the products is the key to earn maximum profits (Brennan

and Merkl-Davies, 2013).

Marginal costing: It shows the cost of additional unit which have been added to the

production. It is a costing technique, which is used by George Lines. Marginal costs are variable

costs including labour, material and overhead costs of additive unit.

4

Price optimisation system It assist in attracting more customers

It helps in sales forecasting and profit

estimation.

Inventory management system Provides strong visibility over

company's inventory.

It analyse and solve a issue as soon as it

occurs.

Job costing system Profit earned by individual job is shown

separately in this system.

Overhead recovery rates can be

estimated on the basis of budgets.

D1: Management accounting system and its reporting are integrated within organisational

process

George Lines follows several management accounting systems and reporting tools for

planning and controlling management performance effectively. Company uses price optimisation

for creating an effective pricing strategy so that they can expand their business and maximizes

purchasing power of customers and inventory management system for identifying under and

overstock of Concrete so that George Lines evaluate future demand. Management accounting

system and its reports helps the company to improve its reporting system.

TASK 2

P3: Calculation of cost using an appropriate technique

Cost: It is a monetary value which has to be paid by buyer to the seller while buying any

kind of goods or services. George Lines is small scale company and wants to set right cost of its

product so that it can attract more buyers. Customer look for the product cost before purchasing

the product and setting right cost for the products is the key to earn maximum profits (Brennan

and Merkl-Davies, 2013).

Marginal costing: It shows the cost of additional unit which have been added to the

production. It is a costing technique, which is used by George Lines. Marginal costs are variable

costs including labour, material and overhead costs of additive unit.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Absorption costing: In this technique, all the manufacturing costs of the units are

absorbed from the sales of the same units. It includes all the direct material cost, direct labour

cost and overhead. It provides financial transparency to the investors of George Lines.

Calculation of net profit by using marginal costing method:

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 *

16) 3200

Contribution 23400

Fixed cost ( 3200 + 1200 + 1500 ) 5900

Net profit 17500

Computation of net income by using absorption costing method:

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

Break even analysis: It is a point where all variable and fixed costs are equal to all

revenues. George Lines uses this analysis to determine its break even point where business is in

the no profit and no loss state (Chen and et. al,. 2011).

A. Total number of product sold

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

B. Calculation of break even point in accordance to sales revenue

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution / sales * 100 30.00%

5

absorbed from the sales of the same units. It includes all the direct material cost, direct labour

cost and overhead. It provides financial transparency to the investors of George Lines.

Calculation of net profit by using marginal costing method:

Particulars Amount

Sales revenue = (selling price * no. of goods sold = 55 * 600) 33000

Marginal Cost of goods sold: 9600

Production = (units produced * marginal cost per unit = 800 * 16) 12800

closing stock = (closing stock units * marginal cost per unit = 200 *

16) 3200

Contribution 23400

Fixed cost ( 3200 + 1200 + 1500 ) 5900

Net profit 17500

Computation of net income by using absorption costing method:

Particulars Amount

Sales = (selling price * no. of units sold = 55 * 600) 33000

Cost of goods sold = (total expenses per unit * actual sales = 23.375 * 600) 14025

Gross profit 18975

Selling & Administrative expenses = (variable sales overhead * actual sales +

selling and administrative cost = 1 * 600 + 2700) 3300

Net profit/ operating income 15675

Break even analysis: It is a point where all variable and fixed costs are equal to all

revenues. George Lines uses this analysis to determine its break even point where business is in

the no profit and no loss state (Chen and et. al,. 2011).

A. Total number of product sold

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

BEP in units 500

B. Calculation of break even point in accordance to sales revenue

Sales per unit 40

Variable costs VC = DM + DL 28

Contribution 12

Fixed costs 6000

Profit volume ratio PVR = Contribution / sales * 100 30.00%

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

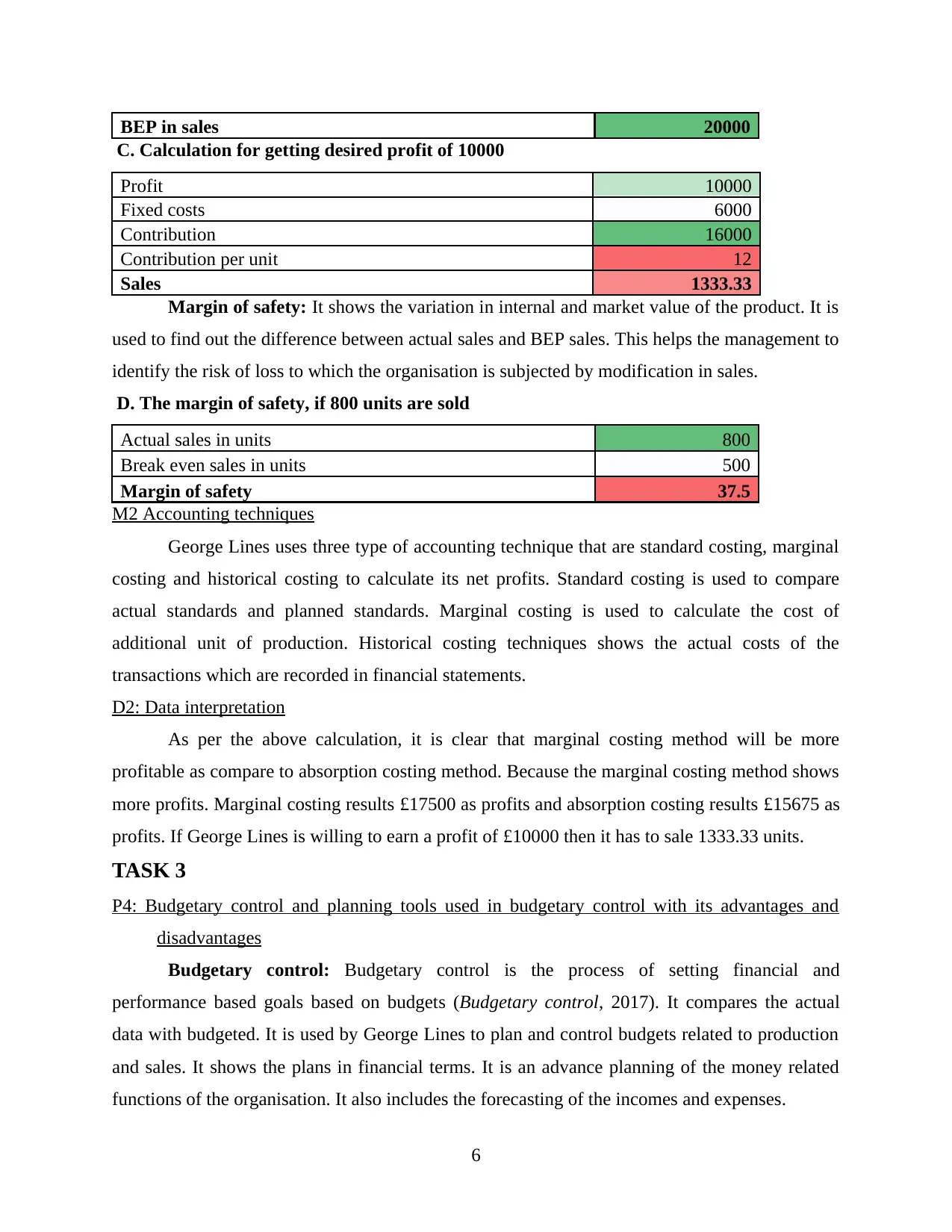

BEP in sales 20000

C. Calculation for getting desired profit of 10000

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

Margin of safety: It shows the variation in internal and market value of the product. It is

used to find out the difference between actual sales and BEP sales. This helps the management to

identify the risk of loss to which the organisation is subjected by modification in sales.

D. The margin of safety, if 800 units are sold

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

M2 Accounting techniques

George Lines uses three type of accounting technique that are standard costing, marginal

costing and historical costing to calculate its net profits. Standard costing is used to compare

actual standards and planned standards. Marginal costing is used to calculate the cost of

additional unit of production. Historical costing techniques shows the actual costs of the

transactions which are recorded in financial statements.

D2: Data interpretation

As per the above calculation, it is clear that marginal costing method will be more

profitable as compare to absorption costing method. Because the marginal costing method shows

more profits. Marginal costing results £17500 as profits and absorption costing results £15675 as

profits. If George Lines is willing to earn a profit of £10000 then it has to sale 1333.33 units.

TASK 3

P4: Budgetary control and planning tools used in budgetary control with its advantages and

disadvantages

Budgetary control: Budgetary control is the process of setting financial and

performance based goals based on budgets (Budgetary control, 2017). It compares the actual

data with budgeted. It is used by George Lines to plan and control budgets related to production

and sales. It shows the plans in financial terms. It is an advance planning of the money related

functions of the organisation. It also includes the forecasting of the incomes and expenses.

6

C. Calculation for getting desired profit of 10000

Profit 10000

Fixed costs 6000

Contribution 16000

Contribution per unit 12

Sales 1333.33

Margin of safety: It shows the variation in internal and market value of the product. It is

used to find out the difference between actual sales and BEP sales. This helps the management to

identify the risk of loss to which the organisation is subjected by modification in sales.

D. The margin of safety, if 800 units are sold

Actual sales in units 800

Break even sales in units 500

Margin of safety 37.5

M2 Accounting techniques

George Lines uses three type of accounting technique that are standard costing, marginal

costing and historical costing to calculate its net profits. Standard costing is used to compare

actual standards and planned standards. Marginal costing is used to calculate the cost of

additional unit of production. Historical costing techniques shows the actual costs of the

transactions which are recorded in financial statements.

D2: Data interpretation

As per the above calculation, it is clear that marginal costing method will be more

profitable as compare to absorption costing method. Because the marginal costing method shows

more profits. Marginal costing results £17500 as profits and absorption costing results £15675 as

profits. If George Lines is willing to earn a profit of £10000 then it has to sale 1333.33 units.

TASK 3

P4: Budgetary control and planning tools used in budgetary control with its advantages and

disadvantages

Budgetary control: Budgetary control is the process of setting financial and

performance based goals based on budgets (Budgetary control, 2017). It compares the actual

data with budgeted. It is used by George Lines to plan and control budgets related to production

and sales. It shows the plans in financial terms. It is an advance planning of the money related

functions of the organisation. It also includes the forecasting of the incomes and expenses.

6

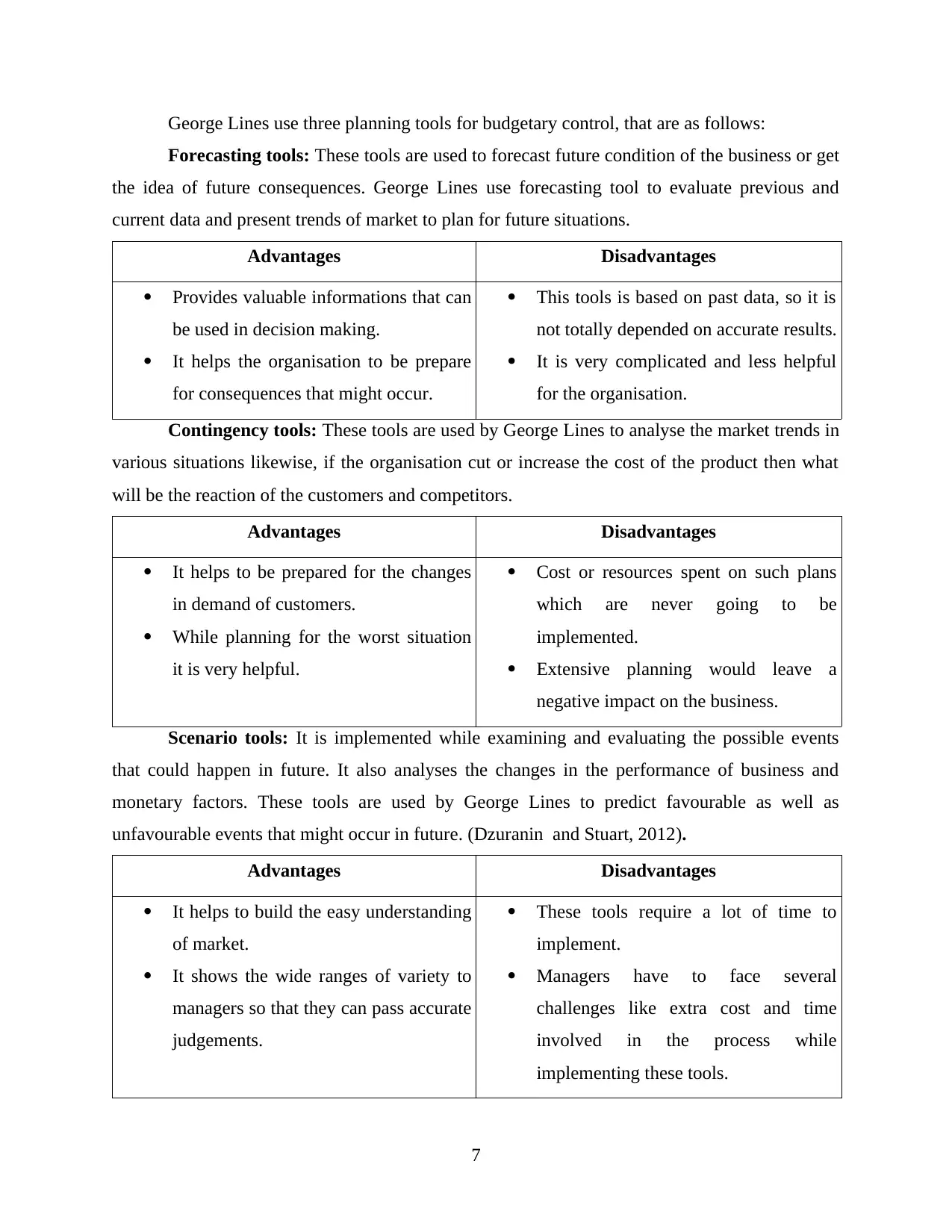

George Lines use three planning tools for budgetary control, that are as follows:

Forecasting tools: These tools are used to forecast future condition of the business or get

the idea of future consequences. George Lines use forecasting tool to evaluate previous and

current data and present trends of market to plan for future situations.

Advantages Disadvantages

Provides valuable informations that can

be used in decision making.

It helps the organisation to be prepare

for consequences that might occur.

This tools is based on past data, so it is

not totally depended on accurate results.

It is very complicated and less helpful

for the organisation.

Contingency tools: These tools are used by George Lines to analyse the market trends in

various situations likewise, if the organisation cut or increase the cost of the product then what

will be the reaction of the customers and competitors.

Advantages Disadvantages

It helps to be prepared for the changes

in demand of customers.

While planning for the worst situation

it is very helpful.

Cost or resources spent on such plans

which are never going to be

implemented.

Extensive planning would leave a

negative impact on the business.

Scenario tools: It is implemented while examining and evaluating the possible events

that could happen in future. It also analyses the changes in the performance of business and

monetary factors. These tools are used by George Lines to predict favourable as well as

unfavourable events that might occur in future. (Dzuranin and Stuart, 2012).

Advantages Disadvantages

It helps to build the easy understanding

of market.

It shows the wide ranges of variety to

managers so that they can pass accurate

judgements.

These tools require a lot of time to

implement.

Managers have to face several

challenges like extra cost and time

involved in the process while

implementing these tools.

7

Forecasting tools: These tools are used to forecast future condition of the business or get

the idea of future consequences. George Lines use forecasting tool to evaluate previous and

current data and present trends of market to plan for future situations.

Advantages Disadvantages

Provides valuable informations that can

be used in decision making.

It helps the organisation to be prepare

for consequences that might occur.

This tools is based on past data, so it is

not totally depended on accurate results.

It is very complicated and less helpful

for the organisation.

Contingency tools: These tools are used by George Lines to analyse the market trends in

various situations likewise, if the organisation cut or increase the cost of the product then what

will be the reaction of the customers and competitors.

Advantages Disadvantages

It helps to be prepared for the changes

in demand of customers.

While planning for the worst situation

it is very helpful.

Cost or resources spent on such plans

which are never going to be

implemented.

Extensive planning would leave a

negative impact on the business.

Scenario tools: It is implemented while examining and evaluating the possible events

that could happen in future. It also analyses the changes in the performance of business and

monetary factors. These tools are used by George Lines to predict favourable as well as

unfavourable events that might occur in future. (Dzuranin and Stuart, 2012).

Advantages Disadvantages

It helps to build the easy understanding

of market.

It shows the wide ranges of variety to

managers so that they can pass accurate

judgements.

These tools require a lot of time to

implement.

Managers have to face several

challenges like extra cost and time

involved in the process while

implementing these tools.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

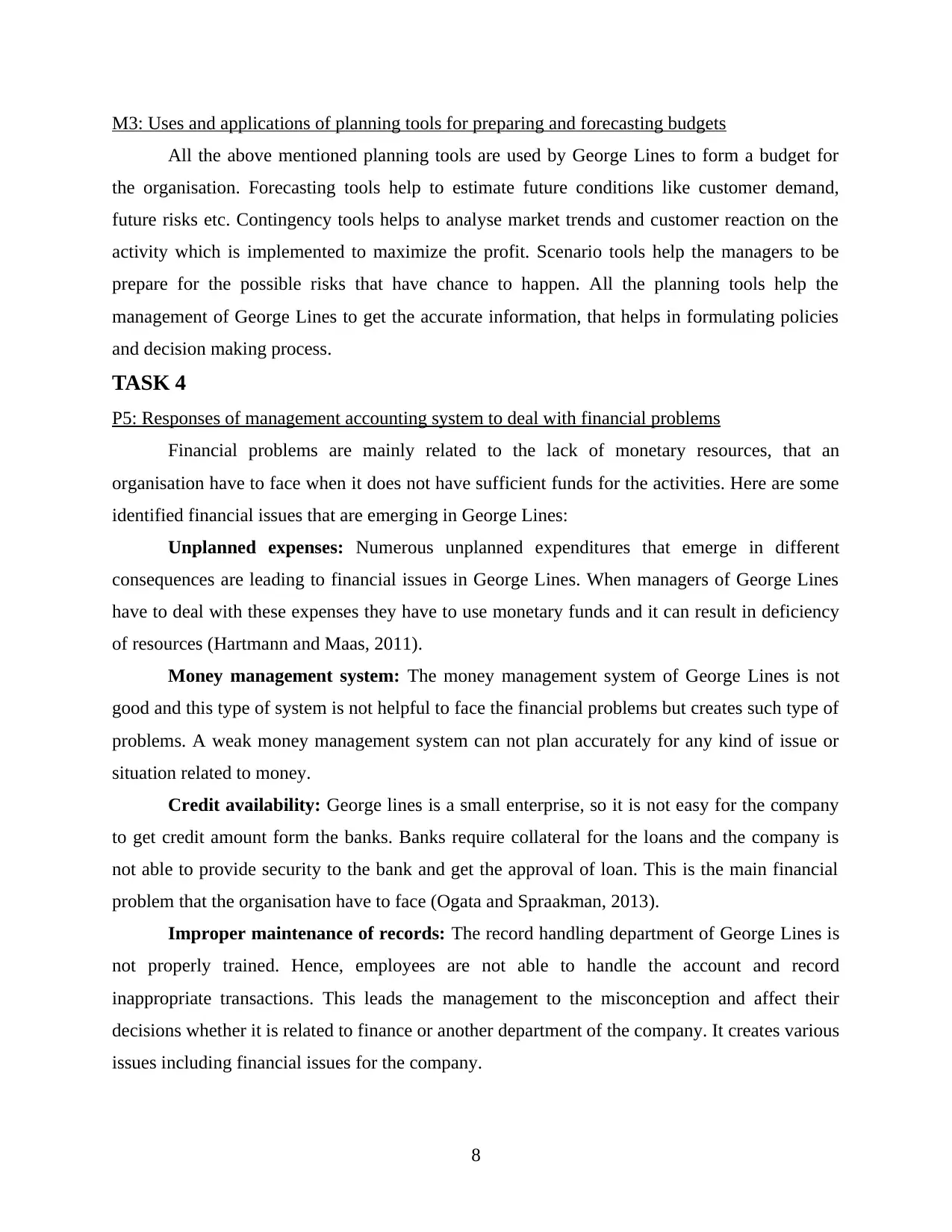

M3: Uses and applications of planning tools for preparing and forecasting budgets

All the above mentioned planning tools are used by George Lines to form a budget for

the organisation. Forecasting tools help to estimate future conditions like customer demand,

future risks etc. Contingency tools helps to analyse market trends and customer reaction on the

activity which is implemented to maximize the profit. Scenario tools help the managers to be

prepare for the possible risks that have chance to happen. All the planning tools help the

management of George Lines to get the accurate information, that helps in formulating policies

and decision making process.

TASK 4

P5: Responses of management accounting system to deal with financial problems

Financial problems are mainly related to the lack of monetary resources, that an

organisation have to face when it does not have sufficient funds for the activities. Here are some

identified financial issues that are emerging in George Lines:

Unplanned expenses: Numerous unplanned expenditures that emerge in different

consequences are leading to financial issues in George Lines. When managers of George Lines

have to deal with these expenses they have to use monetary funds and it can result in deficiency

of resources (Hartmann and Maas, 2011).

Money management system: The money management system of George Lines is not

good and this type of system is not helpful to face the financial problems but creates such type of

problems. A weak money management system can not plan accurately for any kind of issue or

situation related to money.

Credit availability: George lines is a small enterprise, so it is not easy for the company

to get credit amount form the banks. Banks require collateral for the loans and the company is

not able to provide security to the bank and get the approval of loan. This is the main financial

problem that the organisation have to face (Ogata and Spraakman, 2013).

Improper maintenance of records: The record handling department of George Lines is

not properly trained. Hence, employees are not able to handle the account and record

inappropriate transactions. This leads the management to the misconception and affect their

decisions whether it is related to finance or another department of the company. It creates various

issues including financial issues for the company.

8

All the above mentioned planning tools are used by George Lines to form a budget for

the organisation. Forecasting tools help to estimate future conditions like customer demand,

future risks etc. Contingency tools helps to analyse market trends and customer reaction on the

activity which is implemented to maximize the profit. Scenario tools help the managers to be

prepare for the possible risks that have chance to happen. All the planning tools help the

management of George Lines to get the accurate information, that helps in formulating policies

and decision making process.

TASK 4

P5: Responses of management accounting system to deal with financial problems

Financial problems are mainly related to the lack of monetary resources, that an

organisation have to face when it does not have sufficient funds for the activities. Here are some

identified financial issues that are emerging in George Lines:

Unplanned expenses: Numerous unplanned expenditures that emerge in different

consequences are leading to financial issues in George Lines. When managers of George Lines

have to deal with these expenses they have to use monetary funds and it can result in deficiency

of resources (Hartmann and Maas, 2011).

Money management system: The money management system of George Lines is not

good and this type of system is not helpful to face the financial problems but creates such type of

problems. A weak money management system can not plan accurately for any kind of issue or

situation related to money.

Credit availability: George lines is a small enterprise, so it is not easy for the company

to get credit amount form the banks. Banks require collateral for the loans and the company is

not able to provide security to the bank and get the approval of loan. This is the main financial

problem that the organisation have to face (Ogata and Spraakman, 2013).

Improper maintenance of records: The record handling department of George Lines is

not properly trained. Hence, employees are not able to handle the account and record

inappropriate transactions. This leads the management to the misconception and affect their

decisions whether it is related to finance or another department of the company. It creates various

issues including financial issues for the company.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

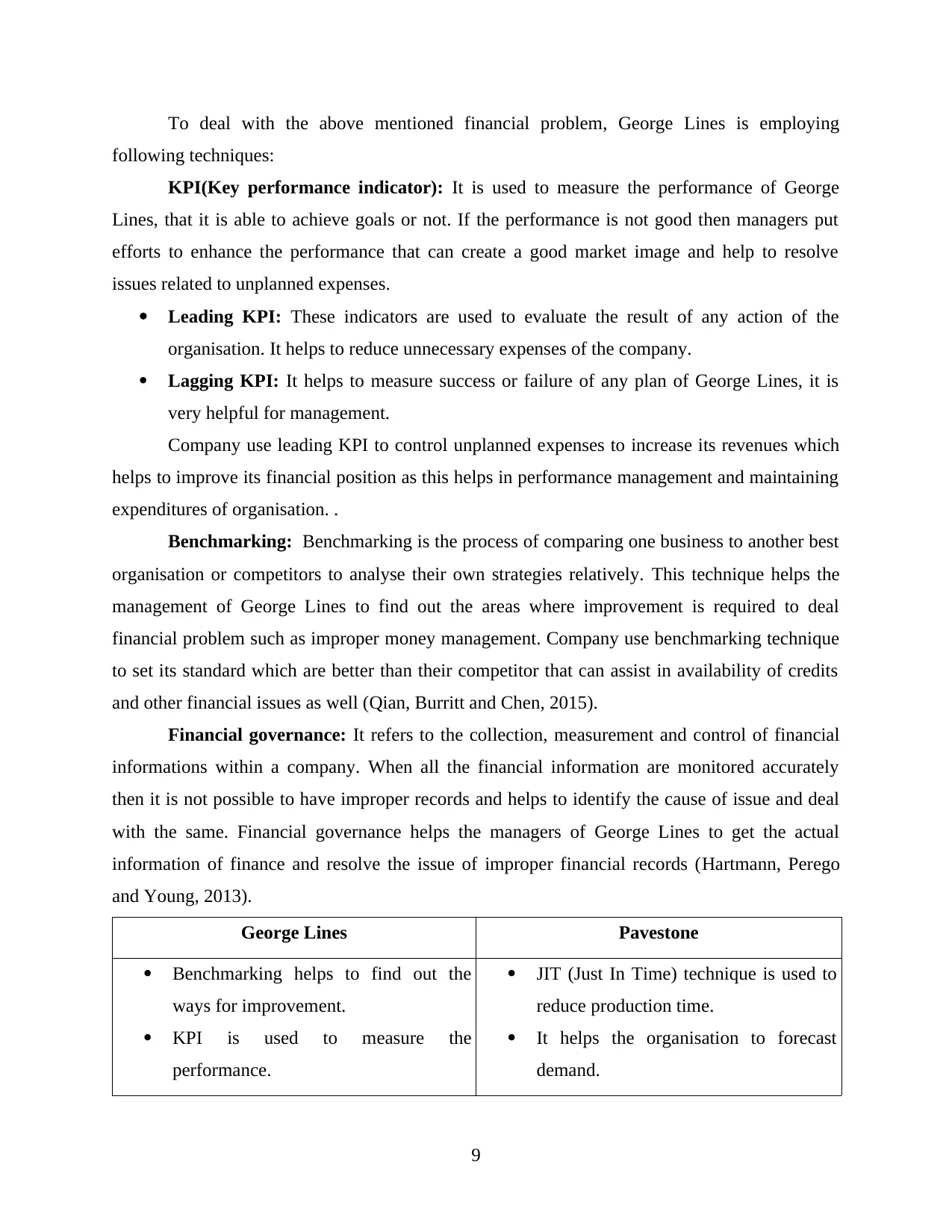

To deal with the above mentioned financial problem, George Lines is employing

following techniques:

KPI(Key performance indicator): It is used to measure the performance of George

Lines, that it is able to achieve goals or not. If the performance is not good then managers put

efforts to enhance the performance that can create a good market image and help to resolve

issues related to unplanned expenses.

Leading KPI: These indicators are used to evaluate the result of any action of the

organisation. It helps to reduce unnecessary expenses of the company.

Lagging KPI: It helps to measure success or failure of any plan of George Lines, it is

very helpful for management.

Company use leading KPI to control unplanned expenses to increase its revenues which

helps to improve its financial position as this helps in performance management and maintaining

expenditures of organisation. .

Benchmarking: Benchmarking is the process of comparing one business to another best

organisation or competitors to analyse their own strategies relatively. This technique helps the

management of George Lines to find out the areas where improvement is required to deal

financial problem such as improper money management. Company use benchmarking technique

to set its standard which are better than their competitor that can assist in availability of credits

and other financial issues as well (Qian, Burritt and Chen, 2015).

Financial governance: It refers to the collection, measurement and control of financial

informations within a company. When all the financial information are monitored accurately

then it is not possible to have improper records and helps to identify the cause of issue and deal

with the same. Financial governance helps the managers of George Lines to get the actual

information of finance and resolve the issue of improper financial records (Hartmann, Perego

and Young, 2013).

George Lines Pavestone

Benchmarking helps to find out the

ways for improvement.

KPI is used to measure the

performance.

JIT (Just In Time) technique is used to

reduce production time.

It helps the organisation to forecast

demand.

9

following techniques:

KPI(Key performance indicator): It is used to measure the performance of George

Lines, that it is able to achieve goals or not. If the performance is not good then managers put

efforts to enhance the performance that can create a good market image and help to resolve

issues related to unplanned expenses.

Leading KPI: These indicators are used to evaluate the result of any action of the

organisation. It helps to reduce unnecessary expenses of the company.

Lagging KPI: It helps to measure success or failure of any plan of George Lines, it is

very helpful for management.

Company use leading KPI to control unplanned expenses to increase its revenues which

helps to improve its financial position as this helps in performance management and maintaining

expenditures of organisation. .

Benchmarking: Benchmarking is the process of comparing one business to another best

organisation or competitors to analyse their own strategies relatively. This technique helps the

management of George Lines to find out the areas where improvement is required to deal

financial problem such as improper money management. Company use benchmarking technique

to set its standard which are better than their competitor that can assist in availability of credits

and other financial issues as well (Qian, Burritt and Chen, 2015).

Financial governance: It refers to the collection, measurement and control of financial

informations within a company. When all the financial information are monitored accurately

then it is not possible to have improper records and helps to identify the cause of issue and deal

with the same. Financial governance helps the managers of George Lines to get the actual

information of finance and resolve the issue of improper financial records (Hartmann, Perego

and Young, 2013).

George Lines Pavestone

Benchmarking helps to find out the

ways for improvement.

KPI is used to measure the

performance.

JIT (Just In Time) technique is used to

reduce production time.

It helps the organisation to forecast

demand.

9

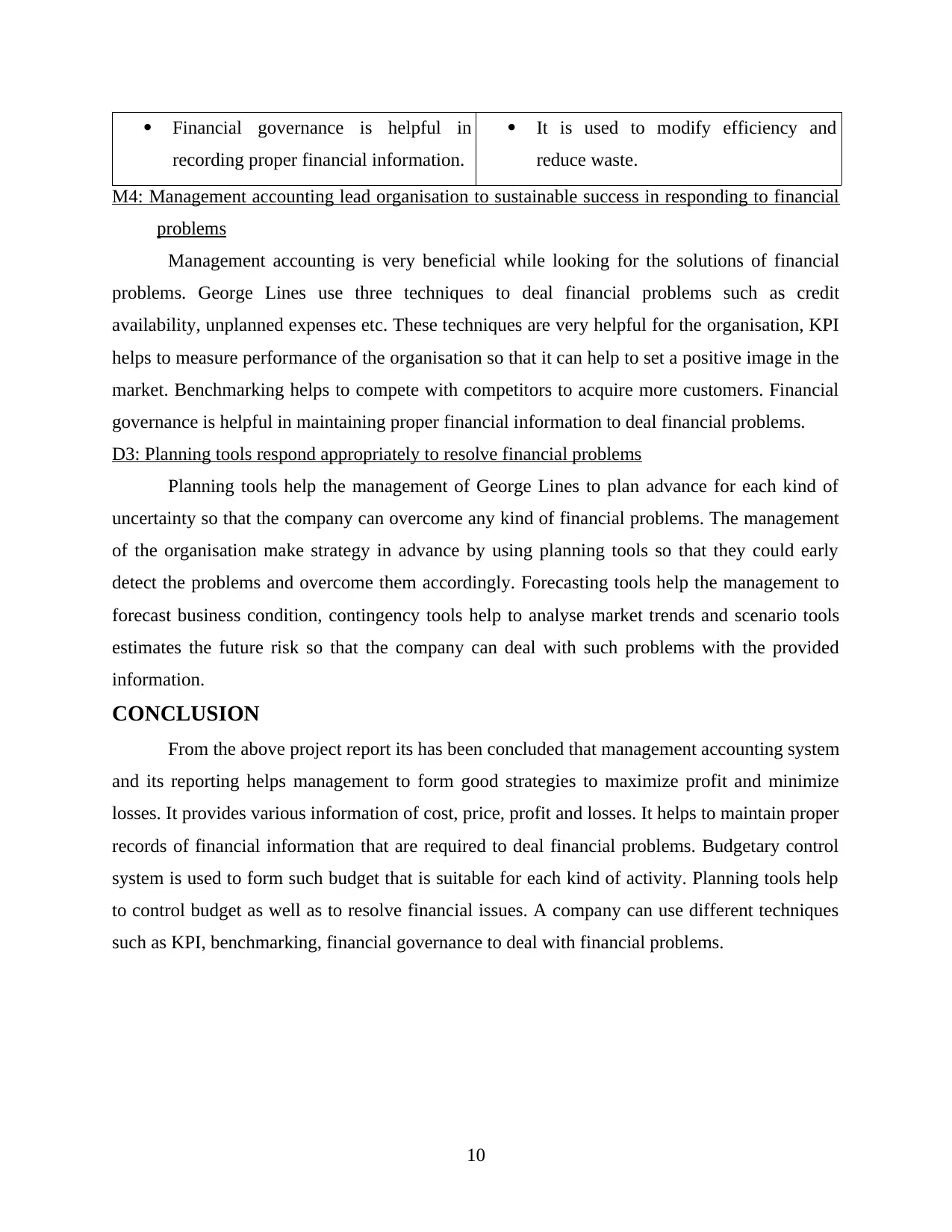

Financial governance is helpful in

recording proper financial information.

It is used to modify efficiency and

reduce waste.

M4: Management accounting lead organisation to sustainable success in responding to financial

problems

Management accounting is very beneficial while looking for the solutions of financial

problems. George Lines use three techniques to deal financial problems such as credit

availability, unplanned expenses etc. These techniques are very helpful for the organisation, KPI

helps to measure performance of the organisation so that it can help to set a positive image in the

market. Benchmarking helps to compete with competitors to acquire more customers. Financial

governance is helpful in maintaining proper financial information to deal financial problems.

D3: Planning tools respond appropriately to resolve financial problems

Planning tools help the management of George Lines to plan advance for each kind of

uncertainty so that the company can overcome any kind of financial problems. The management

of the organisation make strategy in advance by using planning tools so that they could early

detect the problems and overcome them accordingly. Forecasting tools help the management to

forecast business condition, contingency tools help to analyse market trends and scenario tools

estimates the future risk so that the company can deal with such problems with the provided

information.

CONCLUSION

From the above project report its has been concluded that management accounting system

and its reporting helps management to form good strategies to maximize profit and minimize

losses. It provides various information of cost, price, profit and losses. It helps to maintain proper

records of financial information that are required to deal financial problems. Budgetary control

system is used to form such budget that is suitable for each kind of activity. Planning tools help

to control budget as well as to resolve financial issues. A company can use different techniques

such as KPI, benchmarking, financial governance to deal with financial problems.

10

recording proper financial information.

It is used to modify efficiency and

reduce waste.

M4: Management accounting lead organisation to sustainable success in responding to financial

problems

Management accounting is very beneficial while looking for the solutions of financial

problems. George Lines use three techniques to deal financial problems such as credit

availability, unplanned expenses etc. These techniques are very helpful for the organisation, KPI

helps to measure performance of the organisation so that it can help to set a positive image in the

market. Benchmarking helps to compete with competitors to acquire more customers. Financial

governance is helpful in maintaining proper financial information to deal financial problems.

D3: Planning tools respond appropriately to resolve financial problems

Planning tools help the management of George Lines to plan advance for each kind of

uncertainty so that the company can overcome any kind of financial problems. The management

of the organisation make strategy in advance by using planning tools so that they could early

detect the problems and overcome them accordingly. Forecasting tools help the management to

forecast business condition, contingency tools help to analyse market trends and scenario tools

estimates the future risk so that the company can deal with such problems with the provided

information.

CONCLUSION

From the above project report its has been concluded that management accounting system

and its reporting helps management to form good strategies to maximize profit and minimize

losses. It provides various information of cost, price, profit and losses. It helps to maintain proper

records of financial information that are required to deal financial problems. Budgetary control

system is used to form such budget that is suitable for each kind of activity. Planning tools help

to control budget as well as to resolve financial issues. A company can use different techniques

such as KPI, benchmarking, financial governance to deal with financial problems.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.