Management Accounting Report: Financial Analysis of Cream Ltd

VerifiedAdded on 2023/01/12

|20

|5455

|55

Report

AI Summary

This report provides a comprehensive overview of management accounting principles and their application within Cream Ltd., a UK-based SME. The report begins with an introduction to management accounting, explaining its role in facilitating informed decision-making and its distinction from financial accounting. It then delves into various management accounting systems, including job costing, price optimization, cost accounting, and inventory management, highlighting their significance for internal departments. The report further explores different methods for managing accounting reports, such as budget reports, performance reports, and inventory management reports. A significant portion of the report is dedicated to the preparation of income statements using managerial accounting techniques, specifically absorption and marginal costing methods, and their impact on financial reporting documents. Additionally, the report examines the benefits and drawbacks of budgetary control techniques and assesses the influence of management accounting on resolving financial problems. The report concludes by summarizing the key findings and emphasizing the importance of management accounting in achieving organizational success. Overall, this report provides a solid foundation for understanding management accounting and its practical applications in a real-world business scenario.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1: Explanation of various management accounting and their system.......................................3

P2 Different method that can be used in management accounting reports..................................5

TASK2.............................................................................................................................................7

P3 Preparation of income statements using managerial accounting techniques..........................7

TASK3...........................................................................................................................................12

P4 Benefits and drawbacks of budgetary control techniques....................................................12

TASK4...........................................................................................................................................17

P5 Effect of management accounting technique in solving financial problems........................17

CONCLUSION..............................................................................................................................19

REFERENCES..............................................................................................................................21

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1: Explanation of various management accounting and their system.......................................3

P2 Different method that can be used in management accounting reports..................................5

TASK2.............................................................................................................................................7

P3 Preparation of income statements using managerial accounting techniques..........................7

TASK3...........................................................................................................................................12

P4 Benefits and drawbacks of budgetary control techniques....................................................12

TASK4...........................................................................................................................................17

P5 Effect of management accounting technique in solving financial problems........................17

CONCLUSION..............................................................................................................................19

REFERENCES..............................................................................................................................21

INTRODUCTION

Management accounting is terms as an activity of maintaining record of intrinsic

information about an organisation so that it makes easy for management to make a better and

profitable decisions for further growth and success of an organisation (Biondi, Gulluscio and et.

al., 2017). Keeping such report helps stakeholders such as customers, employees, shareholders

etc. to identify actual financial performance of an organisation so that they can decide whether to

stay with company or not. The present assignment report is based on Cream Ltd. Which is

engaged in provide wide range of products such as ice-cream, waffles, doughnuts etc. It is SME

operated in United Kingdom. The report explains the concepts of management accounting and its

systems and reporting. Along with this, use of different costing methods for the purpose of

calculations of net profit are also summarised under this report. The report also covers planning

tools to control budget and use of MA in resolving financial issues of an organisation.

TASK 1

P1: Explanation of various management accounting and their system

Management accounting: It is a branch of accounting in which transactions are

collected, measured and recorded for the purpose of taking essential financial decision. In other

words, it is a process of formulating managerial accounting policies with the use of accounting

data. Organization use this technique for optimum utilization of their resources by taking

effective decision. This tool of accounting is used by internal department of Cream Ltd..

Managers of Cream Ltd. uses different management accounting systems for the purpose of

taking necessary decisions. Success of plans and policies of internal department is depending on

how effectively their managers use management accounting system of their department

(Bromwich and Scapens, 2016)

Differences between management and financial accounting:

Basis Management accounting Financial accounting

Meaning It facilitate management to

make accurate profitable

decision and plans for

operating business more

effectively.

It mainly focuses on preparing

final accounts of business so as

to know their actual financial

stability in the market.

Management accounting is terms as an activity of maintaining record of intrinsic

information about an organisation so that it makes easy for management to make a better and

profitable decisions for further growth and success of an organisation (Biondi, Gulluscio and et.

al., 2017). Keeping such report helps stakeholders such as customers, employees, shareholders

etc. to identify actual financial performance of an organisation so that they can decide whether to

stay with company or not. The present assignment report is based on Cream Ltd. Which is

engaged in provide wide range of products such as ice-cream, waffles, doughnuts etc. It is SME

operated in United Kingdom. The report explains the concepts of management accounting and its

systems and reporting. Along with this, use of different costing methods for the purpose of

calculations of net profit are also summarised under this report. The report also covers planning

tools to control budget and use of MA in resolving financial issues of an organisation.

TASK 1

P1: Explanation of various management accounting and their system

Management accounting: It is a branch of accounting in which transactions are

collected, measured and recorded for the purpose of taking essential financial decision. In other

words, it is a process of formulating managerial accounting policies with the use of accounting

data. Organization use this technique for optimum utilization of their resources by taking

effective decision. This tool of accounting is used by internal department of Cream Ltd..

Managers of Cream Ltd. uses different management accounting systems for the purpose of

taking necessary decisions. Success of plans and policies of internal department is depending on

how effectively their managers use management accounting system of their department

(Bromwich and Scapens, 2016)

Differences between management and financial accounting:

Basis Management accounting Financial accounting

Meaning It facilitate management to

make accurate profitable

decision and plans for

operating business more

effectively.

It mainly focuses on preparing

final accounts of business so as

to know their actual financial

stability in the market.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Compulsion It requires only when business

operations are not running

effectively.

It is compulsorily required for

company to prepare financial

statements so as to retain their

loyal stakeholders.

Prime motive Providing useful information

on various business matters so

as to make suitable plans and

policies.

To provide financial

information to interested

stakeholders.

Time frame Reports are prepared only if

there is requirement of

business

Annually

Types of management accounting system:

Job costing system: It is essential part of managerial amounting. Under job costing

system managers allocate cost of producing specific task products. Cost of each activity are

analysis and recorded in statements. These types of system is useful in those industries which

produced limited and specific products on demand of their customers. For example, producing

wide range of products such as ice-creams, waffles etc. by Cream Ltd., using such system helps

managers in allocating cost to different product according to the growth in their sales and

revenue(Eldenburg, Krishnan and Krishnan, 2017)

Price optimizing system: This system is applied by organizations to decide pricing rate

of their products. Managers decides price on the basis of analyzing entire market conditions.

They set price which gave satisfaction to customers and also provides financial gain to the

organization . Managers uses various strategies to set their price. Business organizations various

strategies of price like skimming, penetration and etc. They decide their price of product on the

basis of industrial life cycle product. In the context of Cream Ltd., identifying perception of

customers towards pricing policy of company, it makes easy for manager to make relevant

changes in their existing pricing policy which increases customer satisfaction level as revenue.

Cost accounting system: In management accounting tools cost accounting is also play

important role. Business organizations uses this system to analysis cost incurred in

manufacturing of products and then formulated polices which help in minimizing cost. This

operations are not running

effectively.

It is compulsorily required for

company to prepare financial

statements so as to retain their

loyal stakeholders.

Prime motive Providing useful information

on various business matters so

as to make suitable plans and

policies.

To provide financial

information to interested

stakeholders.

Time frame Reports are prepared only if

there is requirement of

business

Annually

Types of management accounting system:

Job costing system: It is essential part of managerial amounting. Under job costing

system managers allocate cost of producing specific task products. Cost of each activity are

analysis and recorded in statements. These types of system is useful in those industries which

produced limited and specific products on demand of their customers. For example, producing

wide range of products such as ice-creams, waffles etc. by Cream Ltd., using such system helps

managers in allocating cost to different product according to the growth in their sales and

revenue(Eldenburg, Krishnan and Krishnan, 2017)

Price optimizing system: This system is applied by organizations to decide pricing rate

of their products. Managers decides price on the basis of analyzing entire market conditions.

They set price which gave satisfaction to customers and also provides financial gain to the

organization . Managers uses various strategies to set their price. Business organizations various

strategies of price like skimming, penetration and etc. They decide their price of product on the

basis of industrial life cycle product. In the context of Cream Ltd., identifying perception of

customers towards pricing policy of company, it makes easy for manager to make relevant

changes in their existing pricing policy which increases customer satisfaction level as revenue.

Cost accounting system: In management accounting tools cost accounting is also play

important role. Business organizations uses this system to analysis cost incurred in

manufacturing of products and then formulated polices which help in minimizing cost. This

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

system is useful for every kind of industries either it is small or large size of enterprises. Cost

accounting system has very large criteria. In the context of Cream Ltd., analysing total cost

incurred in manufacturing of products makes easy for manager to set margin and charge prices

from customers accordingly (Ferdous, Adams and Boyce, 2019)

Inventory management system: Inventory management system is used to monitor and

control the stock products, which may be the asset, raw material, deliveries, supplies or product

which is ready to dispatched to the customers. This is a technological software used for tracking

the inventories of the company and as gives the information related to the stock which is helpful

for to control the stock or outages. There is a use of barcode scanning process which includes all

the detailing of product used to maintain the record. In the context of Cream Ltd., identifying

level of inventory reduces changes of failing customers needs and requirements which makes

strong brand image into the market .

P2 Different method that can be used in management accounting reports

Management accounting reports defines the management of reports which provides

financial information. It has been preparing to analyse the profit, loss, gain, expense, etc. which

is needed to the company to increase its profitability index by increase its sale and reduces the

losses or to fulfil the loopholes that directly helps to grow even more faster. To manage the

reports it is more effective and efficient way for Cream Ltd. to keep the records of all the

activities perform in a particular period of time that is helpful in future forecasting. There are

several methods used to manage the reports by the management of Cream Ltd. these are as

follows as:

Budget reports - This is a report used for budgeting the certain task and hold back the

productivity by the management department. Budget reports is being used to compare the

performance or set the standards for every task. As it calculates the difference between the actual

and calculative cost thus it is helpful for Cream Ltd. to accomplish the task with more

consistency and improves the performance of the company. This is also used for forecasting the

future costing which is beneficial for the growth and development of the company (Hiebl and

Mayrleitner, 2019).

Performance report - Performance reports defines the individual, group or company

performance. It is useful to define the growth of individual by analysing the performance

because growth can only be achieved by better performance. Performance is being analysed to

accounting system has very large criteria. In the context of Cream Ltd., analysing total cost

incurred in manufacturing of products makes easy for manager to set margin and charge prices

from customers accordingly (Ferdous, Adams and Boyce, 2019)

Inventory management system: Inventory management system is used to monitor and

control the stock products, which may be the asset, raw material, deliveries, supplies or product

which is ready to dispatched to the customers. This is a technological software used for tracking

the inventories of the company and as gives the information related to the stock which is helpful

for to control the stock or outages. There is a use of barcode scanning process which includes all

the detailing of product used to maintain the record. In the context of Cream Ltd., identifying

level of inventory reduces changes of failing customers needs and requirements which makes

strong brand image into the market .

P2 Different method that can be used in management accounting reports

Management accounting reports defines the management of reports which provides

financial information. It has been preparing to analyse the profit, loss, gain, expense, etc. which

is needed to the company to increase its profitability index by increase its sale and reduces the

losses or to fulfil the loopholes that directly helps to grow even more faster. To manage the

reports it is more effective and efficient way for Cream Ltd. to keep the records of all the

activities perform in a particular period of time that is helpful in future forecasting. There are

several methods used to manage the reports by the management of Cream Ltd. these are as

follows as:

Budget reports - This is a report used for budgeting the certain task and hold back the

productivity by the management department. Budget reports is being used to compare the

performance or set the standards for every task. As it calculates the difference between the actual

and calculative cost thus it is helpful for Cream Ltd. to accomplish the task with more

consistency and improves the performance of the company. This is also used for forecasting the

future costing which is beneficial for the growth and development of the company (Hiebl and

Mayrleitner, 2019).

Performance report - Performance reports defines the individual, group or company

performance. It is useful to define the growth of individual by analysing the performance

because growth can only be achieved by better performance. Performance is being analysed to

provide bonus, incentives, perks, promotion, etc. to the employee which builds the motivation

and self-confidence to achieve the individual and company's goals and objectives. So

performance report is needed for Cream Ltd. to measure the growth of all.

Inventory management report – It is also necessary to control and manage the stock

reports as excess inventory or less inventory both is harmful for the company and in both the

cases company bears the loss. As every company such as Cream Ltd. deals with different product

and provide different services on that thus by which company manage to gain the profit for that

the control on production is much needed and that is control by inventory management reports.

Also manage according to the need and demand of customers as much the product is in demand

that much the stock is needed and if the product is not in demand the stock will also be not

needed (Thomas, 2016).

Accounting receivable report - Accounting receivable reports are the report of those

sale whose payment is not received by the company at a particular period of time. It is useful for

Cream Ltd. to compare the profit and loss of the company and also reflects company's

performance. It keep the record of credit sale and enlist those payments which is not pay at in

order to services ordered by the customer. This can be used by manager of Cream Ltd. to

measure the performance of the company as it defines the financial stability of the company and

also used to make budget and set target according to the previous reports.

The accounting management reports is used to measure the financial performance of the

company which involve the budgeting, inventory control, accounting receivable reports. It help

managers of Cream Ltd. in decision making, strategies, plan formation to gain the profit at a

certain period of time. Company need to prepare these reports to evaluate the performance and

deal with threats and grab the opportunities to enjoys the profit. This is also needed to present the

report in the market for the shareholders as they invest in the company and for market value as

well (Fiondella and et. al., 2016)

M1 Essential requirements of management accounting systems

Every organisation wants to sustain in competitive market for long duration which can be

possible only the suitable plans and policies formulates. In the context of Cream Ltd., it is

important for management to utilise different management accounting system for beneficial

purpose for an instance, using of price optimisation system drives managers to update their

existing pricing strategies after acknowledging perception of customers towards their existing

and self-confidence to achieve the individual and company's goals and objectives. So

performance report is needed for Cream Ltd. to measure the growth of all.

Inventory management report – It is also necessary to control and manage the stock

reports as excess inventory or less inventory both is harmful for the company and in both the

cases company bears the loss. As every company such as Cream Ltd. deals with different product

and provide different services on that thus by which company manage to gain the profit for that

the control on production is much needed and that is control by inventory management reports.

Also manage according to the need and demand of customers as much the product is in demand

that much the stock is needed and if the product is not in demand the stock will also be not

needed (Thomas, 2016).

Accounting receivable report - Accounting receivable reports are the report of those

sale whose payment is not received by the company at a particular period of time. It is useful for

Cream Ltd. to compare the profit and loss of the company and also reflects company's

performance. It keep the record of credit sale and enlist those payments which is not pay at in

order to services ordered by the customer. This can be used by manager of Cream Ltd. to

measure the performance of the company as it defines the financial stability of the company and

also used to make budget and set target according to the previous reports.

The accounting management reports is used to measure the financial performance of the

company which involve the budgeting, inventory control, accounting receivable reports. It help

managers of Cream Ltd. in decision making, strategies, plan formation to gain the profit at a

certain period of time. Company need to prepare these reports to evaluate the performance and

deal with threats and grab the opportunities to enjoys the profit. This is also needed to present the

report in the market for the shareholders as they invest in the company and for market value as

well (Fiondella and et. al., 2016)

M1 Essential requirements of management accounting systems

Every organisation wants to sustain in competitive market for long duration which can be

possible only the suitable plans and policies formulates. In the context of Cream Ltd., it is

important for management to utilise different management accounting system for beneficial

purpose for an instance, using of price optimisation system drives managers to update their

existing pricing strategies after acknowledging perception of customers towards their existing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

pricining policy. This will retain loyal customers with company for longer duration. Another

instance of getting fruitful outcome for using management accounting system includes inventory

management system which communicates managers about the level of inventory available with

company at present so that further decision could be made regarding ordering further stock in

order to meet client’s requirements. This will increase brand image and loyalty in market.

D2 Management accounting system and management reporting system are integrated with

process of organisation

The management accounting and reporting systems of an organisation are integrated as

with the help of accounting system various reports of the company like financial statements etc.

can be produced which help in determining the financial position of a company. The accounting

system of a company help in recording the transactions that occur in company so that records can

be maintained. Thus it can be said that both the systems are integrated which help the company

in maintaining effective records of the company.

TASK2

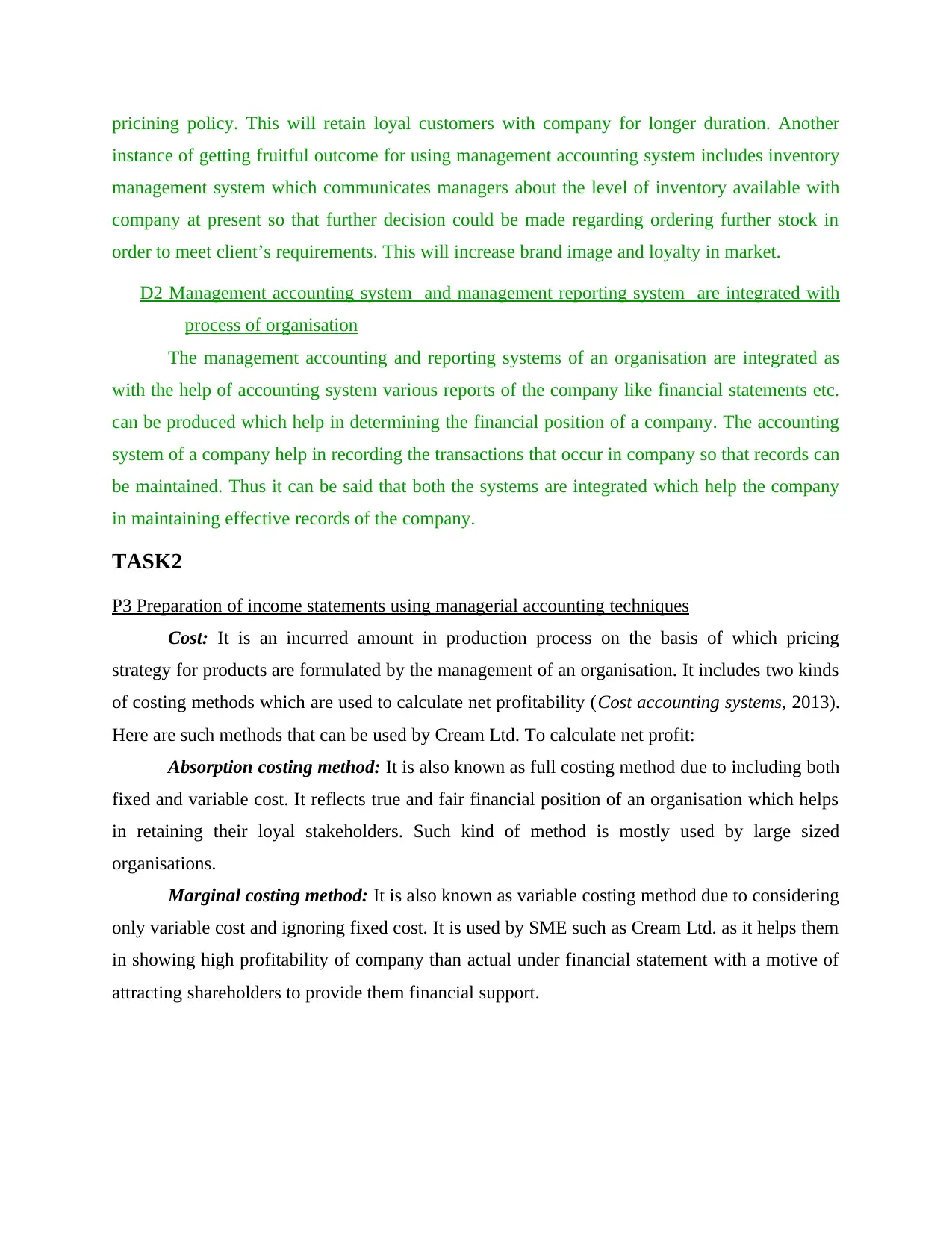

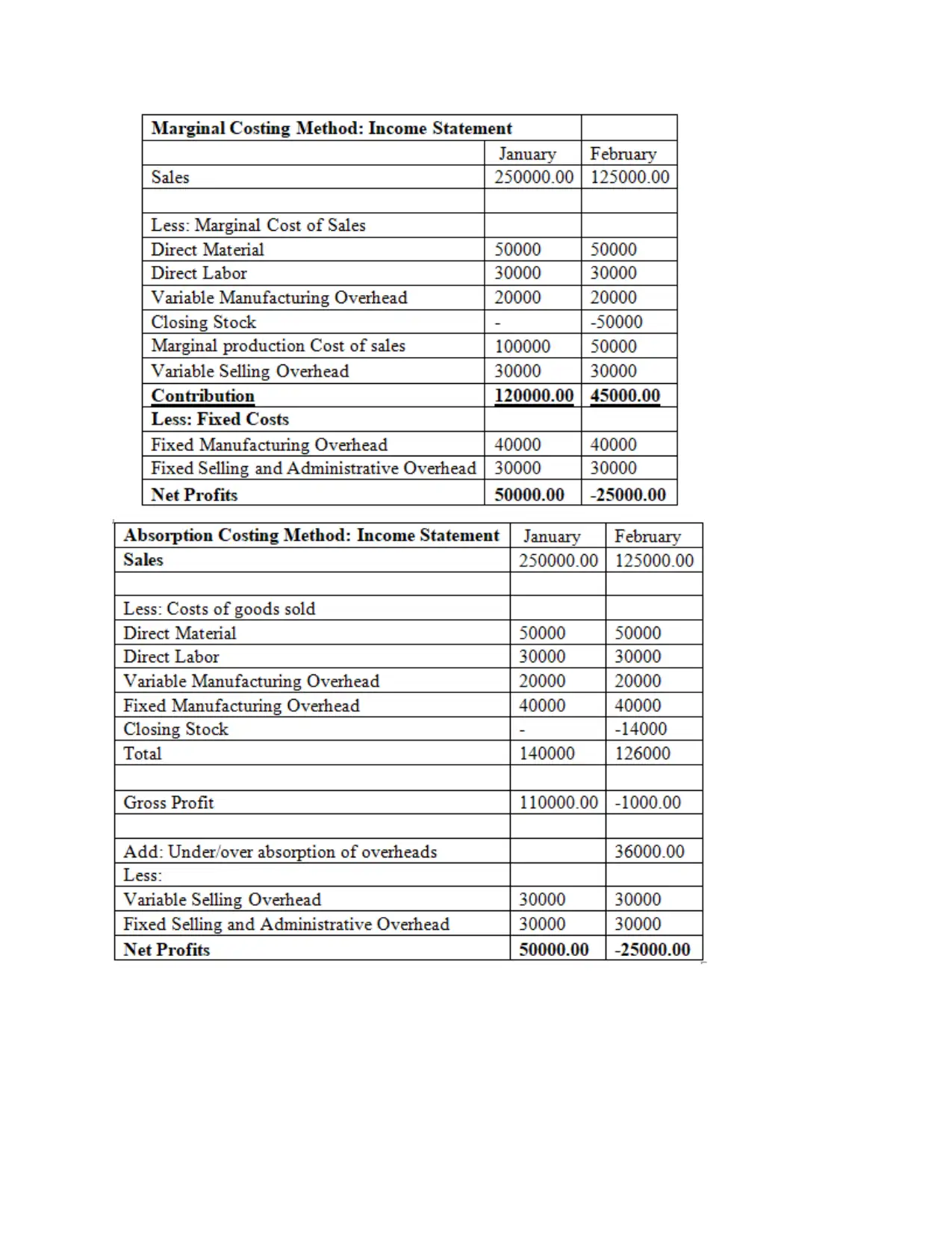

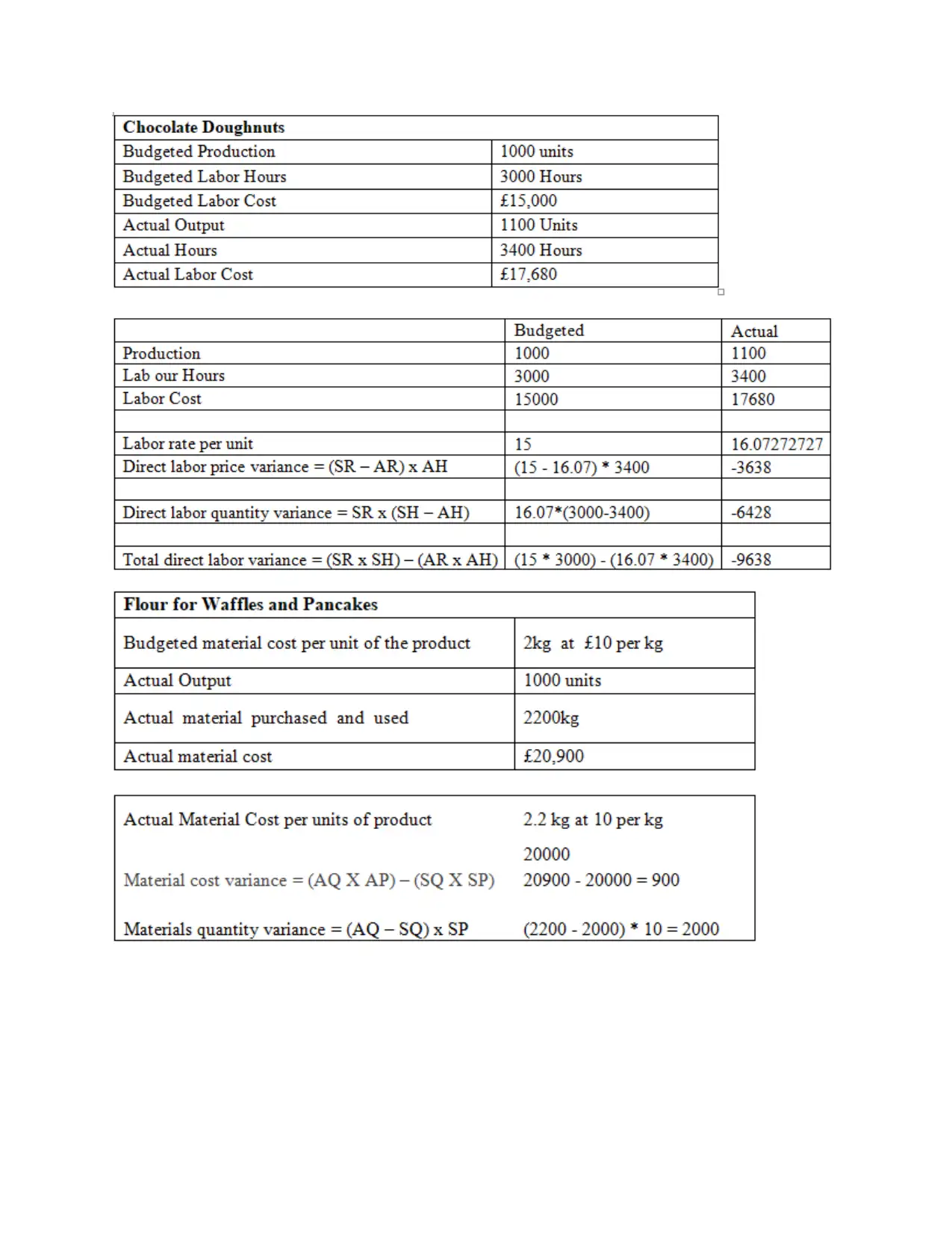

P3 Preparation of income statements using managerial accounting techniques

Cost: It is an incurred amount in production process on the basis of which pricing

strategy for products are formulated by the management of an organisation. It includes two kinds

of costing methods which are used to calculate net profitability (Cost accounting systems, 2013).

Here are such methods that can be used by Cream Ltd. To calculate net profit:

Absorption costing method: It is also known as full costing method due to including both

fixed and variable cost. It reflects true and fair financial position of an organisation which helps

in retaining their loyal stakeholders. Such kind of method is mostly used by large sized

organisations.

Marginal costing method: It is also known as variable costing method due to considering

only variable cost and ignoring fixed cost. It is used by SME such as Cream Ltd. as it helps them

in showing high profitability of company than actual under financial statement with a motive of

attracting shareholders to provide them financial support.

instance of getting fruitful outcome for using management accounting system includes inventory

management system which communicates managers about the level of inventory available with

company at present so that further decision could be made regarding ordering further stock in

order to meet client’s requirements. This will increase brand image and loyalty in market.

D2 Management accounting system and management reporting system are integrated with

process of organisation

The management accounting and reporting systems of an organisation are integrated as

with the help of accounting system various reports of the company like financial statements etc.

can be produced which help in determining the financial position of a company. The accounting

system of a company help in recording the transactions that occur in company so that records can

be maintained. Thus it can be said that both the systems are integrated which help the company

in maintaining effective records of the company.

TASK2

P3 Preparation of income statements using managerial accounting techniques

Cost: It is an incurred amount in production process on the basis of which pricing

strategy for products are formulated by the management of an organisation. It includes two kinds

of costing methods which are used to calculate net profitability (Cost accounting systems, 2013).

Here are such methods that can be used by Cream Ltd. To calculate net profit:

Absorption costing method: It is also known as full costing method due to including both

fixed and variable cost. It reflects true and fair financial position of an organisation which helps

in retaining their loyal stakeholders. Such kind of method is mostly used by large sized

organisations.

Marginal costing method: It is also known as variable costing method due to considering

only variable cost and ignoring fixed cost. It is used by SME such as Cream Ltd. as it helps them

in showing high profitability of company than actual under financial statement with a motive of

attracting shareholders to provide them financial support.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

M2 Management accounting technique and financial reporting documents

With the help of management accounting techniques like marginal and absorption costing

the management of an organisation can effectively mange the budget so that sufficient funds can

be available wit the company in achieving its goals and objectives. The company can identify its

With the help of management accounting techniques like marginal and absorption costing

the management of an organisation can effectively mange the budget so that sufficient funds can

be available wit the company in achieving its goals and objectives. The company can identify its

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

financial position with the help of these tools so that the monetary data can be effectively

managed.

D2 Financial report which apply to interpret business activities

Various types of financial reports like budget reports, account receivable ageing reports,

cost accounting managerial reports etc. help the managers of company in identifying the

deficiencies and variances in an organisation (Ndemewah, Menges and Hiebl, 2019). This help

the management in identifying the effectiveness of business activities so that company goals can

be achieved so that efficient decisions can be made through strategic planning in order to achieve

long-term benefits.

TASK3

P4 Benefits and drawbacks of budgetary control techniques

Budget: budget is a process which defines the calculated and estimated result of funds as where

to invest and how much to invest for specified period of time in future. budget can be made by a

family, an individual, a group, by company, etc. It is for to manage the financial funds.

Types of Budget:

Cash budget: -

Cash budget is a forecast of the total amount of receipts and payments made by a company in a

financial year. This is a demonstration of inflow and outflow of cash in an entity in a specific

time, so that the estimation for working capital and other expenditure can be made to sound

working of an organisation. This is the budget which is prepared by Creams Ltd. primarily

before any of the budget so that close estimation can be made for other budgets and any cash

discrepancies can be found this will help the company to maintain ample cash balances (Lowe,

2019).

Objective of preparing cash budget:-

To forecast liquidity position of company.

To predict cash position of Creams Ltd. whether shortfall or surplus.

To estimate the time when cash will be required so that source of finance can be selected

accordingly.

To control over expenditure cash where funds are at shortfalls.

To perpetuate balance between cash, working capital needs, loans and advances made.

managed.

D2 Financial report which apply to interpret business activities

Various types of financial reports like budget reports, account receivable ageing reports,

cost accounting managerial reports etc. help the managers of company in identifying the

deficiencies and variances in an organisation (Ndemewah, Menges and Hiebl, 2019). This help

the management in identifying the effectiveness of business activities so that company goals can

be achieved so that efficient decisions can be made through strategic planning in order to achieve

long-term benefits.

TASK3

P4 Benefits and drawbacks of budgetary control techniques

Budget: budget is a process which defines the calculated and estimated result of funds as where

to invest and how much to invest for specified period of time in future. budget can be made by a

family, an individual, a group, by company, etc. It is for to manage the financial funds.

Types of Budget:

Cash budget: -

Cash budget is a forecast of the total amount of receipts and payments made by a company in a

financial year. This is a demonstration of inflow and outflow of cash in an entity in a specific

time, so that the estimation for working capital and other expenditure can be made to sound

working of an organisation. This is the budget which is prepared by Creams Ltd. primarily

before any of the budget so that close estimation can be made for other budgets and any cash

discrepancies can be found this will help the company to maintain ample cash balances (Lowe,

2019).

Objective of preparing cash budget:-

To forecast liquidity position of company.

To predict cash position of Creams Ltd. whether shortfall or surplus.

To estimate the time when cash will be required so that source of finance can be selected

accordingly.

To control over expenditure cash where funds are at shortfalls.

To perpetuate balance between cash, working capital needs, loans and advances made.

It depicts monthly cash requirement so that finance manager can wisely use funds and by

this funds will not be idle and cash will be in reserve when required.

Static budget:-

A static budget is prepared before commencement of a new financial year and on the

basis of revenue generated in last year. It is forecast of expenditure and income over an

upcoming financial year irrespective of the change in level of activity i.e. it remain unchanged

even if sales volume and production quantity fluctuates. Static budgets are made to evaluate

financial soundness of a company over a span of time (Chenhall and Moers, 2015)

Objective of preparing static budget:-

To mark costs, expenditure, income of a company and to determine financial position of

company.

To ensure that all the subdivision are under the budget by this companies can keep all the

department on proper track and prevent from deviation.

It leads to the proper management of cash flow in the organisation so that cash can be

obtained on time when needed.

To maintain record of field where amount is spent, from where money is coming and

what are the future expectations of flow of funds.

It helps in calculating performance for a period of time since the amount of expenditure is

evenly spread and hence it become easier to evaluate performance since it is easier because sum

of money apportioned to each month is the same.

It creates roadmap of income and expenditure of a company so that it can be followed

accordingly.

Planning tools to control budget

1. Master budget:

A master budget is the combination of all the budgets prepared by all the divisions. It is the

concise form of all divisional budgets made, this is not the biggest budget but it is a summarised

form of all the budgets. Master budget can be used in enlargement of business because it covers

all the aspects of business and makes the process of decision making easy (Endenich, Trapp and

Brandau, 2017) Master budget anticipates detailed knowledge about sales capacity, production

this funds will not be idle and cash will be in reserve when required.

Static budget:-

A static budget is prepared before commencement of a new financial year and on the

basis of revenue generated in last year. It is forecast of expenditure and income over an

upcoming financial year irrespective of the change in level of activity i.e. it remain unchanged

even if sales volume and production quantity fluctuates. Static budgets are made to evaluate

financial soundness of a company over a span of time (Chenhall and Moers, 2015)

Objective of preparing static budget:-

To mark costs, expenditure, income of a company and to determine financial position of

company.

To ensure that all the subdivision are under the budget by this companies can keep all the

department on proper track and prevent from deviation.

It leads to the proper management of cash flow in the organisation so that cash can be

obtained on time when needed.

To maintain record of field where amount is spent, from where money is coming and

what are the future expectations of flow of funds.

It helps in calculating performance for a period of time since the amount of expenditure is

evenly spread and hence it become easier to evaluate performance since it is easier because sum

of money apportioned to each month is the same.

It creates roadmap of income and expenditure of a company so that it can be followed

accordingly.

Planning tools to control budget

1. Master budget:

A master budget is the combination of all the budgets prepared by all the divisions. It is the

concise form of all divisional budgets made, this is not the biggest budget but it is a summarised

form of all the budgets. Master budget can be used in enlargement of business because it covers

all the aspects of business and makes the process of decision making easy (Endenich, Trapp and

Brandau, 2017) Master budget anticipates detailed knowledge about sales capacity, production

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.