Management Accounting Report: Master Budget, Production Plan Analysis

VerifiedAdded on 2021/06/17

|16

|1993

|20

Report

AI Summary

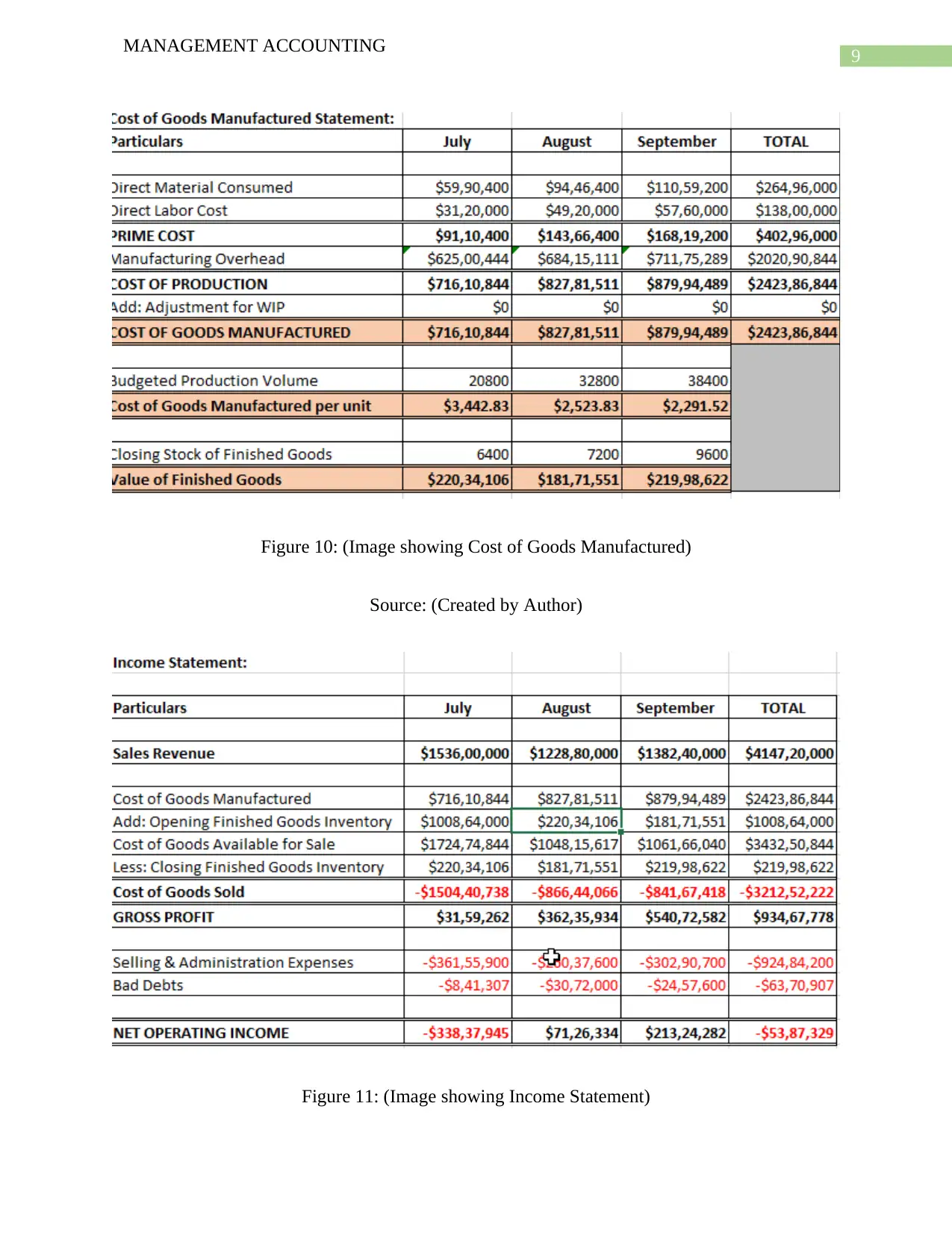

This management accounting report provides a detailed analysis of a company's production plan and budgetary processes. Part A focuses on the incorporation of a master budget, including sales, production, direct labor, purchase, direct material cost, manufacturing overhead, and cash budgets, culminating in an income statement. Part B analyzes a new production program, assessing its impact on production volume and costs, highlighting the use of budgetary approaches for cost and revenue estimation. The analysis includes key budget components like sales, production, direct labor, and manufacturing overhead. Part C compares and contrasts participative and imposed budgeting approaches, emphasizing the advantages of participative budgets in fostering employee collaboration and improving the quality of forecasts. The report recommends the adoption of a participative budget approach for the company, concluding with references to relevant academic literature.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.