Management Accounting Report: Jeffery and Son's Case Study Analysis

VerifiedAdded on 2020/01/28

|23

|6068

|71

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles, focusing on cost classification, job costing, and absorption costing techniques. The report uses a case study of Jeffery and Son's to illustrate these concepts, calculating unit and total job costs. It further explores the purpose and nature of the budgeting process, including the preparation of different types of budgets and a cash budget. The report also delves into variance analysis, preparing a reconciliation operating statement and offering findings to management in accordance with identified responsibility centers. The analysis includes different types of cost classification based on element, function, nature, and behavior. The report also prepares a cost report, analyzing variances between budgeted and actual costs, and suggests ways to reduce costs and enhance value and quality. Overall, the report offers a practical application of management accounting concepts and provides insights into decision-making related to pricing strategies and cost management.

Management Accounting

Table of Contents

Table of Contents

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................4

TASK 1............................................................................................................................................4

1.1 Different types of cost classification.....................................................................................4

1.2 Calculating Unit cost and total job cost.................................................................................5

1.3 Calculating cost of Exquisite using absorption costing technique........................................5

1.4 Analyzing cost of Exquisite...................................................................................................7

TASK 2............................................................................................................................................8

2.1 Preparing and analyzing cost report.......................................................................................8

2.2 Using performance indicators to identify areas for potential improvement..........................9

2.3 Ways to reduce cost and enhance value, quality.................................................................10

Task 3.............................................................................................................................................11

3.1 Purpose and nature of budgeting process............................................................................11

3.2 Selecting appropriate budgeting methods for organization.................................................11

3.3 Preparation of different types of budget..............................................................................12

3.4 Preparing of cash budget......................................................................................................13

TASK 4..........................................................................................................................................15

4.1 Calculating of variance........................................................................................................15

4.2 Preparing of reconciliation operating statement..................................................................16

4.3 Findings to management in accordance with identified responsibility centers...................16

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

2

TASK 1............................................................................................................................................4

1.1 Different types of cost classification.....................................................................................4

1.2 Calculating Unit cost and total job cost.................................................................................5

1.3 Calculating cost of Exquisite using absorption costing technique........................................5

1.4 Analyzing cost of Exquisite...................................................................................................7

TASK 2............................................................................................................................................8

2.1 Preparing and analyzing cost report.......................................................................................8

2.2 Using performance indicators to identify areas for potential improvement..........................9

2.3 Ways to reduce cost and enhance value, quality.................................................................10

Task 3.............................................................................................................................................11

3.1 Purpose and nature of budgeting process............................................................................11

3.2 Selecting appropriate budgeting methods for organization.................................................11

3.3 Preparation of different types of budget..............................................................................12

3.4 Preparing of cash budget......................................................................................................13

TASK 4..........................................................................................................................................15

4.1 Calculating of variance........................................................................................................15

4.2 Preparing of reconciliation operating statement..................................................................16

4.3 Findings to management in accordance with identified responsibility centers...................16

CONCLUSION..............................................................................................................................17

REFERENCES..............................................................................................................................18

2

INTRODUCTION

Management accounting is a crucial aspect by which management can keep detail record

related to accounting information and accordingly, they can take decisions related to pricing

strategies. It is also extended in three areas such as strategic, performance and risk management

which provide support to business in order to determine secure position in the marketplace. The

present report is based on the case study of Jeffery and Son's which produces many popular and

branded products (Weygandt and et. al., 2009). This has basically two departments such as

service (stores and Maintenance) and production. In this regard, classification of cost has been

done on the basis of element, function, nature and behavior. Further, unit cost and total cost have

been calculated by using job costing method. In addition to this, purpose and nature of budgeting

process are also explained.

TASK 1

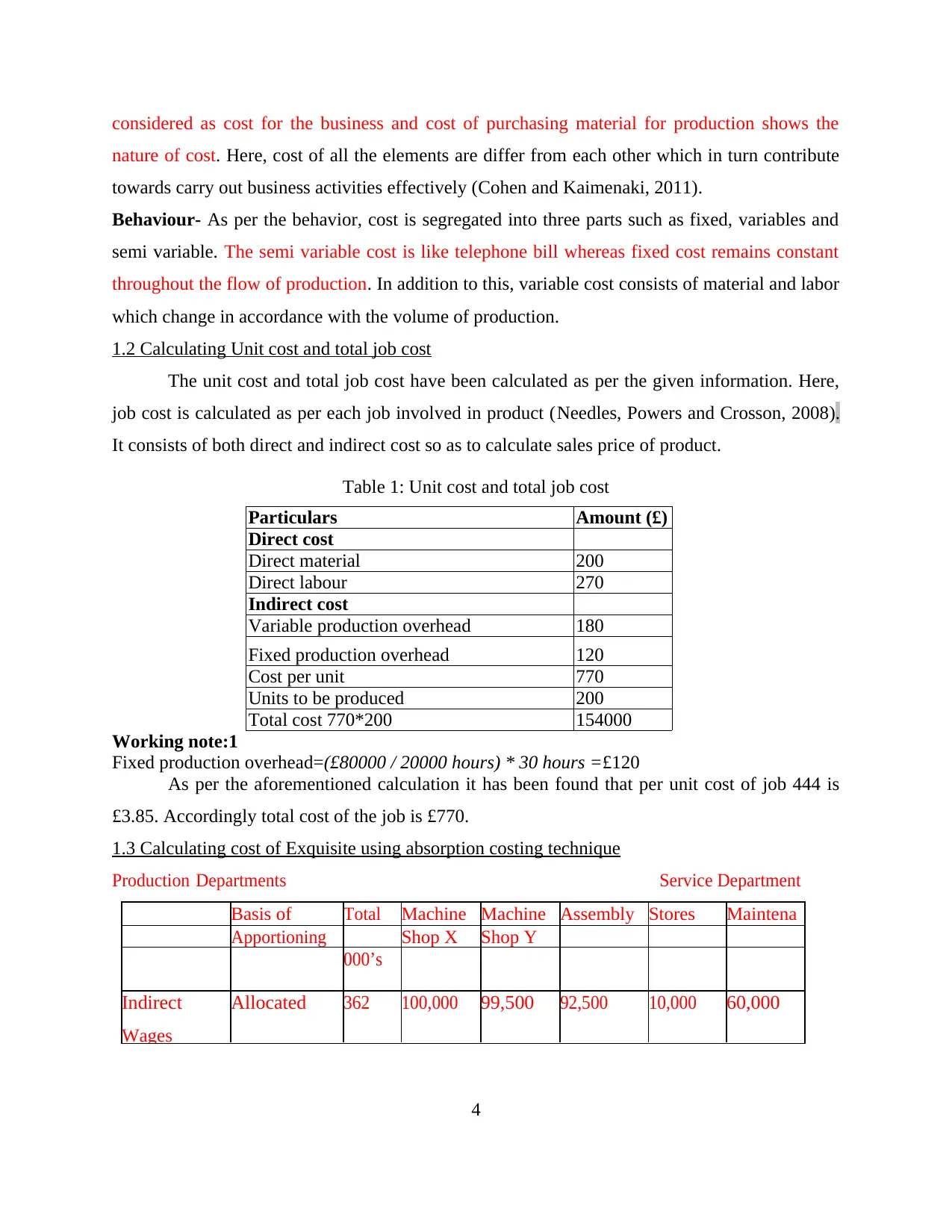

1.1 Different types of cost classification

There are different types of cost involved in the production of products and services.

Here, costs have been classified into following categories-

Element-According to the element, cost is divided into two different parts such as direct and

indirect cost. Main examples of direct cost are heating, lighting and material as well as labor

which play active role in production activities (Jones and Clatworthy, 2006). On the other hand,

indirect costs are those which are indirectly related to the production. It includes smooth tools

which support production activities indirectly.

Function-Cost of production is divided according to the functions to be performed. It consists of

finance, production and marketing as well as research and development. Here, cost of

corporation will be recorded functionally for example in production department overall cost is

segregated on the basis of manufacturing and large amount is being utilized for carrying out

production. Further, in marketing department cost is indulged for development of advertisement

and other promotional tools.

Nature-Under this, cost is divided into three main parts such as labor, overhead expense and

material. All these aspects are related to the overhead expenses. It assists corporation to carry out

production in a smooth manner. For instance if organization provides payment to labor then it is

3

Management accounting is a crucial aspect by which management can keep detail record

related to accounting information and accordingly, they can take decisions related to pricing

strategies. It is also extended in three areas such as strategic, performance and risk management

which provide support to business in order to determine secure position in the marketplace. The

present report is based on the case study of Jeffery and Son's which produces many popular and

branded products (Weygandt and et. al., 2009). This has basically two departments such as

service (stores and Maintenance) and production. In this regard, classification of cost has been

done on the basis of element, function, nature and behavior. Further, unit cost and total cost have

been calculated by using job costing method. In addition to this, purpose and nature of budgeting

process are also explained.

TASK 1

1.1 Different types of cost classification

There are different types of cost involved in the production of products and services.

Here, costs have been classified into following categories-

Element-According to the element, cost is divided into two different parts such as direct and

indirect cost. Main examples of direct cost are heating, lighting and material as well as labor

which play active role in production activities (Jones and Clatworthy, 2006). On the other hand,

indirect costs are those which are indirectly related to the production. It includes smooth tools

which support production activities indirectly.

Function-Cost of production is divided according to the functions to be performed. It consists of

finance, production and marketing as well as research and development. Here, cost of

corporation will be recorded functionally for example in production department overall cost is

segregated on the basis of manufacturing and large amount is being utilized for carrying out

production. Further, in marketing department cost is indulged for development of advertisement

and other promotional tools.

Nature-Under this, cost is divided into three main parts such as labor, overhead expense and

material. All these aspects are related to the overhead expenses. It assists corporation to carry out

production in a smooth manner. For instance if organization provides payment to labor then it is

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

considered as cost for the business and cost of purchasing material for production shows the

nature of cost. Here, cost of all the elements are differ from each other which in turn contribute

towards carry out business activities effectively (Cohen and Kaimenaki, 2011).

Behaviour- As per the behavior, cost is segregated into three parts such as fixed, variables and

semi variable. The semi variable cost is like telephone bill whereas fixed cost remains constant

throughout the flow of production. In addition to this, variable cost consists of material and labor

which change in accordance with the volume of production.

1.2 Calculating Unit cost and total job cost

The unit cost and total job cost have been calculated as per the given information. Here,

job cost is calculated as per each job involved in product (Needles, Powers and Crosson, 2008).

It consists of both direct and indirect cost so as to calculate sales price of product.

Table 1: Unit cost and total job cost

Particulars Amount (£)

Direct cost

Direct material 200

Direct labour 270

Indirect cost

Variable production overhead 180

Fixed production overhead 120

Cost per unit 770

Units to be produced 200

Total cost 770*200 154000

Working note:1

Fixed production overhead=(£80000 / 20000 hours) * 30 hours =£120

As per the aforementioned calculation it has been found that per unit cost of job 444 is

£3.85. Accordingly total cost of the job is £770.

1.3 Calculating cost of Exquisite using absorption costing technique

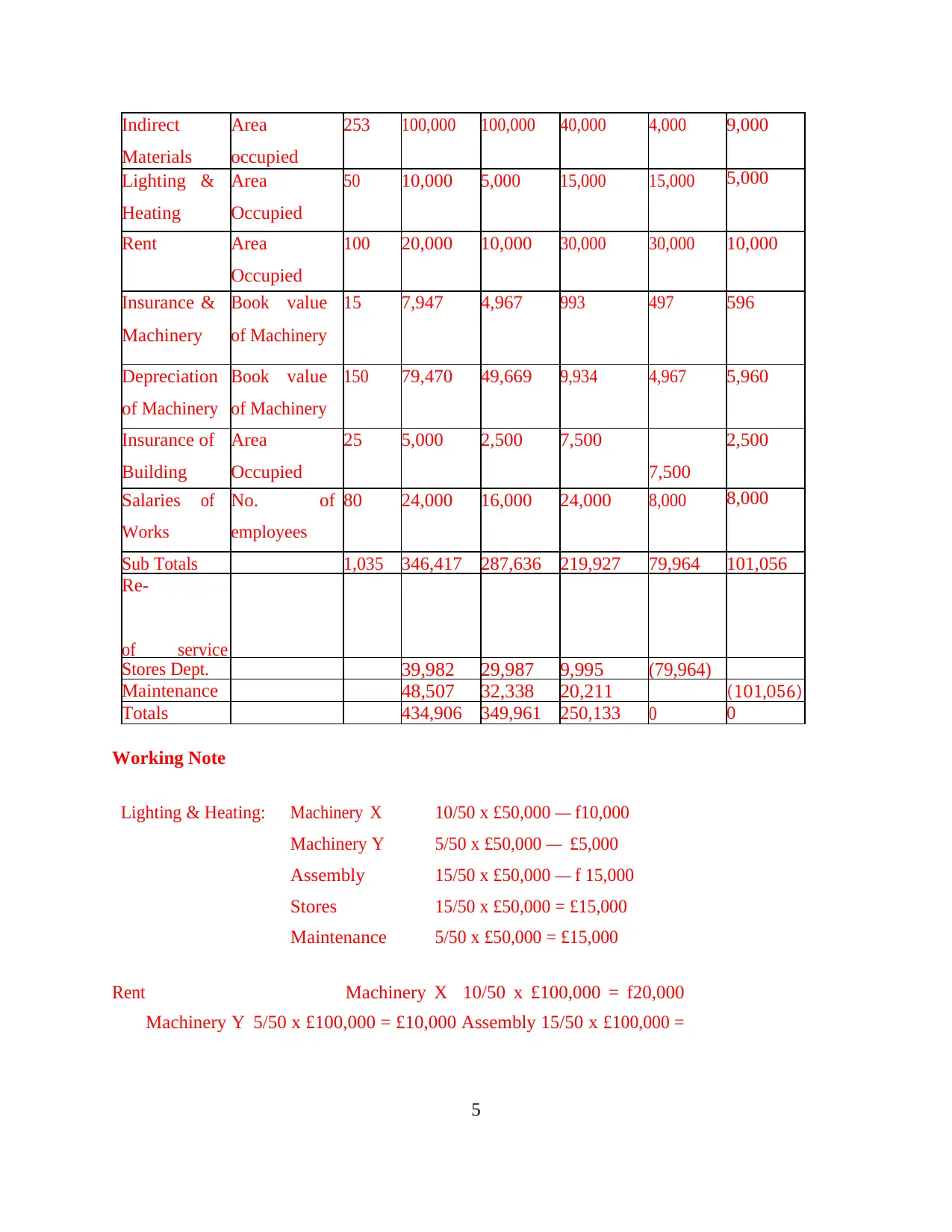

Production Departments Service Department

Basis of Total Machine Machine Assembly Stores Maintena

nceApportioning Shop X Shop Y

000’s

Indirect

Wages

Allocated 362 100,000 99,500 92,500 10,000 60,000

4

nature of cost. Here, cost of all the elements are differ from each other which in turn contribute

towards carry out business activities effectively (Cohen and Kaimenaki, 2011).

Behaviour- As per the behavior, cost is segregated into three parts such as fixed, variables and

semi variable. The semi variable cost is like telephone bill whereas fixed cost remains constant

throughout the flow of production. In addition to this, variable cost consists of material and labor

which change in accordance with the volume of production.

1.2 Calculating Unit cost and total job cost

The unit cost and total job cost have been calculated as per the given information. Here,

job cost is calculated as per each job involved in product (Needles, Powers and Crosson, 2008).

It consists of both direct and indirect cost so as to calculate sales price of product.

Table 1: Unit cost and total job cost

Particulars Amount (£)

Direct cost

Direct material 200

Direct labour 270

Indirect cost

Variable production overhead 180

Fixed production overhead 120

Cost per unit 770

Units to be produced 200

Total cost 770*200 154000

Working note:1

Fixed production overhead=(£80000 / 20000 hours) * 30 hours =£120

As per the aforementioned calculation it has been found that per unit cost of job 444 is

£3.85. Accordingly total cost of the job is £770.

1.3 Calculating cost of Exquisite using absorption costing technique

Production Departments Service Department

Basis of Total Machine Machine Assembly Stores Maintena

nceApportioning Shop X Shop Y

000’s

Indirect

Wages

Allocated 362 100,000 99,500 92,500 10,000 60,000

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Indirect

Materials

Area

occupied

253 100,000 100,000 40,000 4,000 9,000

Lighting

Heating

& Area

Occupied

50 10,000 5,000 15,000 15,000 5,000

Rent Area

Occupied

100 20,000 10,000 30,000 30,000 10,000

Insurance &

Machinery

Book value

of Machinery

15 7,947 4,967 993 497 596

Depreciation

of Machinery

Book value

of Machinery

150 79,470 49,669 9,934 4,967 5,960

Insurance of

Building

Area

Occupied

25 5,000 2,500 7,500

7,500

2,500

Salaries

Works

of No.

employees

of 80 24,000 16,000 24,000 8,000 8,000

Sub Totals 1,035 346,417 287,636 219,927 79,964 101,056

Re-

of service

Stores Dept. 39,982 29,987 9,995 (79,964)

Maintenance 48,507 32,338 20,211 (101,056)

Totals 434,906 349,961 250,133 0 0

Working Note

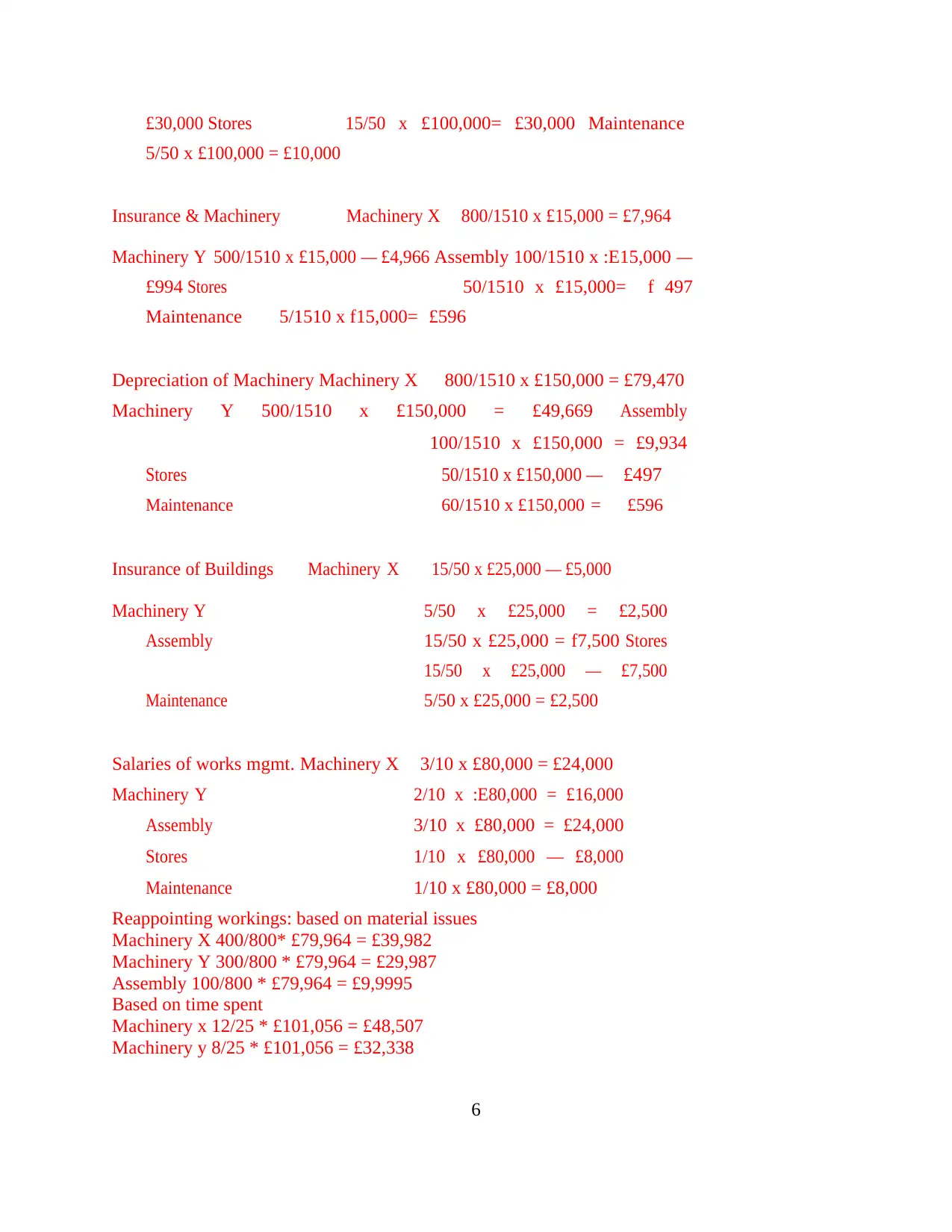

Lighting & Heating: Machinery X 10/50 x £50,000 — f10,000

Machinery Y 5/50 x £50,000 — £5,000

Assembly 15/50 x £50,000 — f 15,000

Stores 15/50 x £50,000 = £15,000

Maintenance 5/50 x £50,000 = £15,000

Rent Machinery X 10/50 x £100,000 = f20,000

Machinery Y 5/50 x £100,000 = £10,000 Assembly 15/50 x £100,000 =

5

Materials

Area

occupied

253 100,000 100,000 40,000 4,000 9,000

Lighting

Heating

& Area

Occupied

50 10,000 5,000 15,000 15,000 5,000

Rent Area

Occupied

100 20,000 10,000 30,000 30,000 10,000

Insurance &

Machinery

Book value

of Machinery

15 7,947 4,967 993 497 596

Depreciation

of Machinery

Book value

of Machinery

150 79,470 49,669 9,934 4,967 5,960

Insurance of

Building

Area

Occupied

25 5,000 2,500 7,500

7,500

2,500

Salaries

Works

of No.

employees

of 80 24,000 16,000 24,000 8,000 8,000

Sub Totals 1,035 346,417 287,636 219,927 79,964 101,056

Re-

of service

Stores Dept. 39,982 29,987 9,995 (79,964)

Maintenance 48,507 32,338 20,211 (101,056)

Totals 434,906 349,961 250,133 0 0

Working Note

Lighting & Heating: Machinery X 10/50 x £50,000 — f10,000

Machinery Y 5/50 x £50,000 — £5,000

Assembly 15/50 x £50,000 — f 15,000

Stores 15/50 x £50,000 = £15,000

Maintenance 5/50 x £50,000 = £15,000

Rent Machinery X 10/50 x £100,000 = f20,000

Machinery Y 5/50 x £100,000 = £10,000 Assembly 15/50 x £100,000 =

5

£30,000 Stores 15/50 x £100,000= £30,000 Maintenance

5/50 x £100,000 = £10,000

Insurance & Machinery Machinery X 800/1510 x £15,000 = £7,964

Machinery Y 500/1510 x £15,000 — £4,966 Assembly 100/1510 x :E15,000 —

£994 Stores 50/1510 x £15,000= f 497

Maintenance 5/1510 x f15,000= £596

Depreciation of Machinery Machinery X 800/1510 x £150,000 = £79,470

Machinery Y 500/1510 x £150,000 = £49,669 Assembly

100/1510 x £150,000 = £9,934

Stores 50/1510 x £150,000 — £497

Maintenance 60/1510 x £150,000 = £596

Insurance of Buildings Machinery X 15/50 x £25,000 — £5,000

Machinery Y 5/50 x £25,000 = £2,500

Assembly 15/50 x £25,000 = f7,500 Stores

15/50 x £25,000 — £7,500

Maintenance 5/50 x £25,000 = £2,500

Salaries of works mgmt. Machinery X 3/10 x £80,000 = £24,000

Machinery Y 2/10 x :E80,000 = £16,000

Assembly 3/10 x £80,000 = £24,000

Stores 1/10 x £80,000 — £8,000

Maintenance 1/10 x £80,000 = £8,000

Reappointing workings: based on material issues

Machinery X 400/800* £79,964 = £39,982

Machinery Y 300/800 * £79,964 = £29,987

Assembly 100/800 * £79,964 = £9,9995

Based on time spent

Machinery x 12/25 * £101,056 = £48,507

Machinery y 8/25 * £101,056 = £32,338

6

5/50 x £100,000 = £10,000

Insurance & Machinery Machinery X 800/1510 x £15,000 = £7,964

Machinery Y 500/1510 x £15,000 — £4,966 Assembly 100/1510 x :E15,000 —

£994 Stores 50/1510 x £15,000= f 497

Maintenance 5/1510 x f15,000= £596

Depreciation of Machinery Machinery X 800/1510 x £150,000 = £79,470

Machinery Y 500/1510 x £150,000 = £49,669 Assembly

100/1510 x £150,000 = £9,934

Stores 50/1510 x £150,000 — £497

Maintenance 60/1510 x £150,000 = £596

Insurance of Buildings Machinery X 15/50 x £25,000 — £5,000

Machinery Y 5/50 x £25,000 = £2,500

Assembly 15/50 x £25,000 = f7,500 Stores

15/50 x £25,000 — £7,500

Maintenance 5/50 x £25,000 = £2,500

Salaries of works mgmt. Machinery X 3/10 x £80,000 = £24,000

Machinery Y 2/10 x :E80,000 = £16,000

Assembly 3/10 x £80,000 = £24,000

Stores 1/10 x £80,000 — £8,000

Maintenance 1/10 x £80,000 = £8,000

Reappointing workings: based on material issues

Machinery X 400/800* £79,964 = £39,982

Machinery Y 300/800 * £79,964 = £29,987

Assembly 100/800 * £79,964 = £9,9995

Based on time spent

Machinery x 12/25 * £101,056 = £48,507

Machinery y 8/25 * £101,056 = £32,338

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

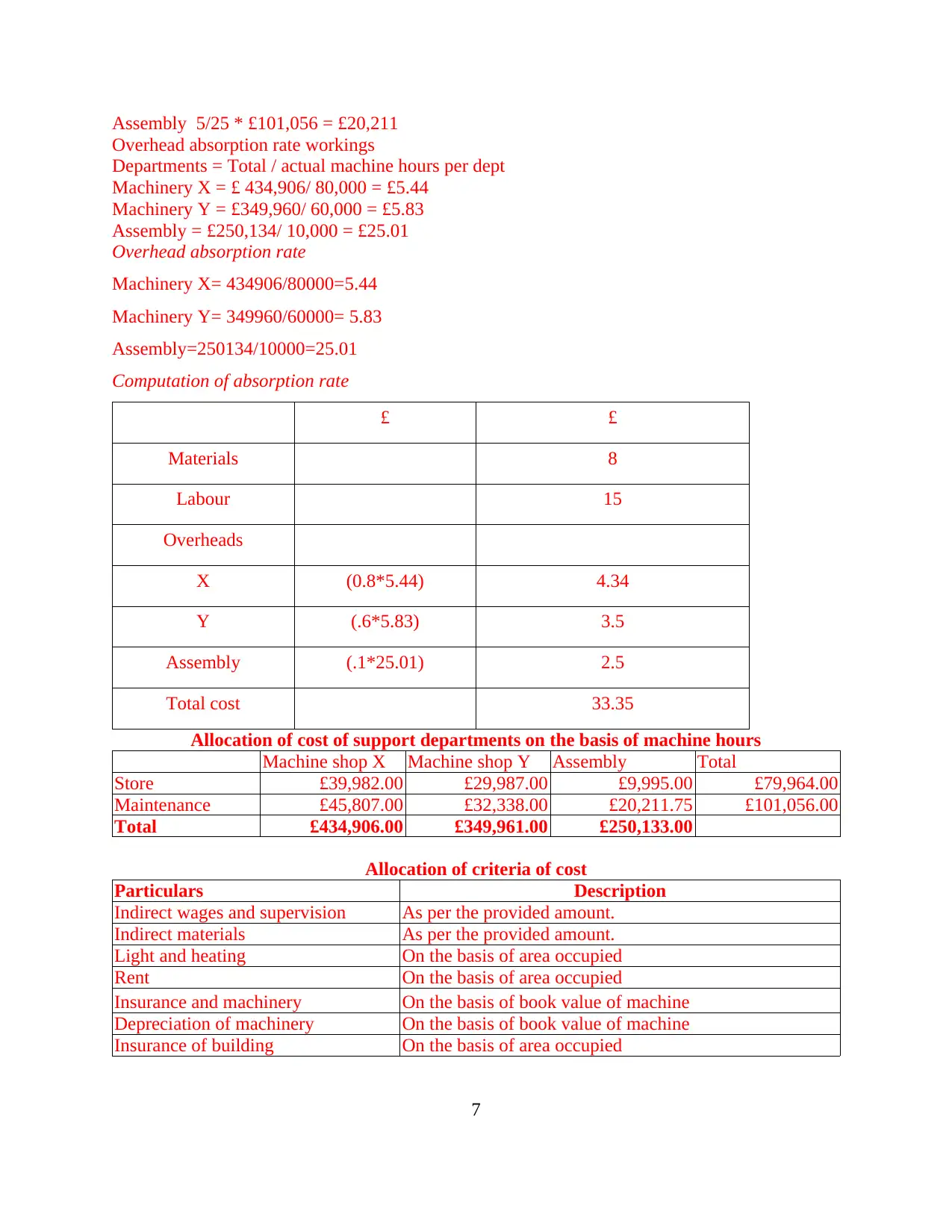

Assembly 5/25 * £101,056 = £20,211

Overhead absorption rate workings

Departments = Total / actual machine hours per dept

Machinery X = £ 434,906/ 80,000 = £5.44

Machinery Y = £349,960/ 60,000 = £5.83

Assembly = £250,134/ 10,000 = £25.01

Overhead absorption rate

Machinery X= 434906/80000=5.44

Machinery Y= 349960/60000= 5.83

Assembly=250134/10000=25.01

Computation of absorption rate

£ £

Materials 8

Labour 15

Overheads

X (0.8*5.44) 4.34

Y (.6*5.83) 3.5

Assembly (.1*25.01) 2.5

Total cost 33.35

Allocation of cost of support departments on the basis of machine hours

Machine shop X Machine shop Y Assembly Total

Store £39,982.00 £29,987.00 £9,995.00 £79,964.00

Maintenance £45,807.00 £32,338.00 £20,211.75 £101,056.00

Total £434,906.00 £349,961.00 £250,133.00

Allocation of criteria of cost

Particulars Description

Indirect wages and supervision As per the provided amount.

Indirect materials As per the provided amount.

Light and heating On the basis of area occupied

Rent On the basis of area occupied

Insurance and machinery On the basis of book value of machine

Depreciation of machinery On the basis of book value of machine

Insurance of building On the basis of area occupied

7

Overhead absorption rate workings

Departments = Total / actual machine hours per dept

Machinery X = £ 434,906/ 80,000 = £5.44

Machinery Y = £349,960/ 60,000 = £5.83

Assembly = £250,134/ 10,000 = £25.01

Overhead absorption rate

Machinery X= 434906/80000=5.44

Machinery Y= 349960/60000= 5.83

Assembly=250134/10000=25.01

Computation of absorption rate

£ £

Materials 8

Labour 15

Overheads

X (0.8*5.44) 4.34

Y (.6*5.83) 3.5

Assembly (.1*25.01) 2.5

Total cost 33.35

Allocation of cost of support departments on the basis of machine hours

Machine shop X Machine shop Y Assembly Total

Store £39,982.00 £29,987.00 £9,995.00 £79,964.00

Maintenance £45,807.00 £32,338.00 £20,211.75 £101,056.00

Total £434,906.00 £349,961.00 £250,133.00

Allocation of criteria of cost

Particulars Description

Indirect wages and supervision As per the provided amount.

Indirect materials As per the provided amount.

Light and heating On the basis of area occupied

Rent On the basis of area occupied

Insurance and machinery On the basis of book value of machine

Depreciation of machinery On the basis of book value of machine

Insurance of building On the basis of area occupied

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

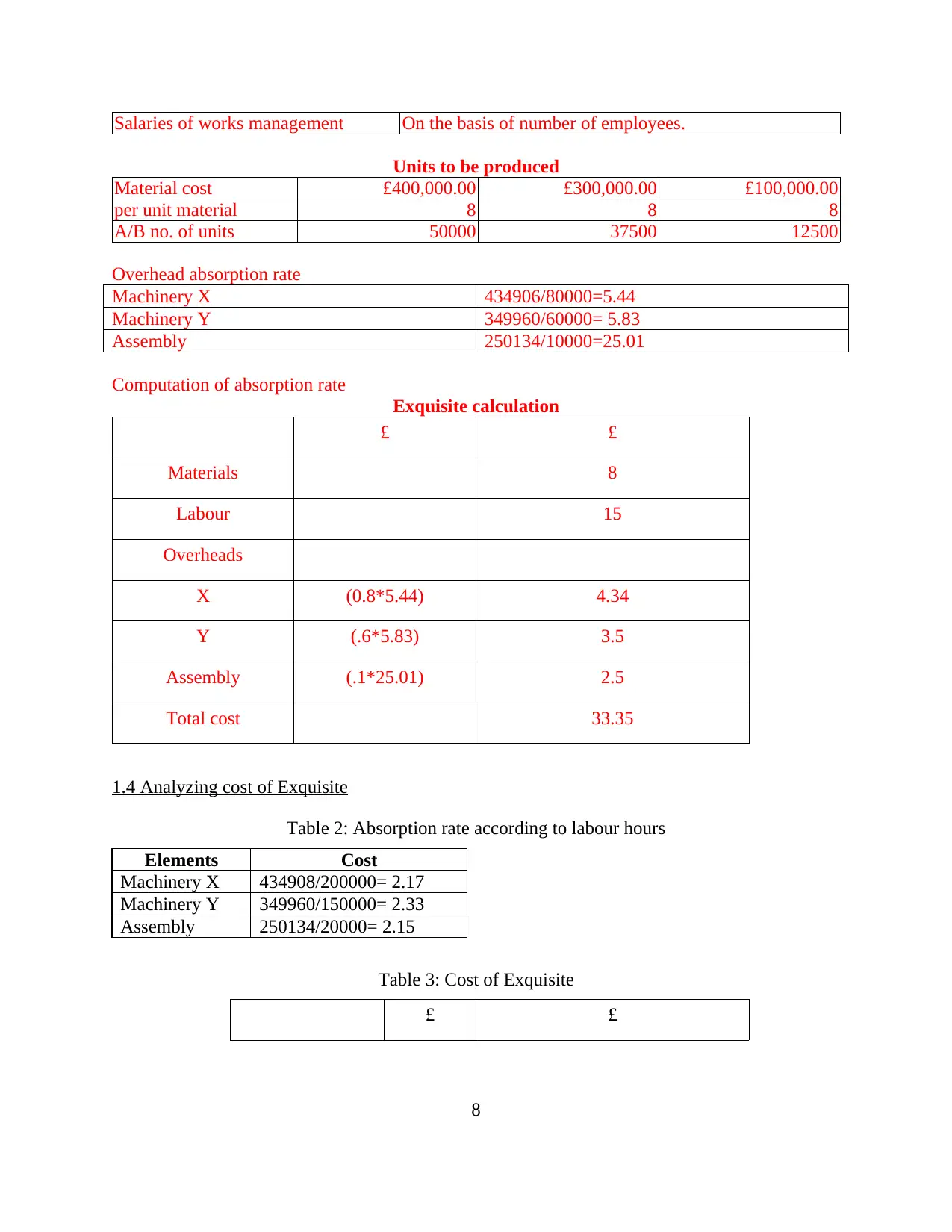

Salaries of works management On the basis of number of employees.

Units to be produced

Material cost £400,000.00 £300,000.00 £100,000.00

per unit material 8 8 8

A/B no. of units 50000 37500 12500

Overhead absorption rate

Machinery X 434906/80000=5.44

Machinery Y 349960/60000= 5.83

Assembly 250134/10000=25.01

Computation of absorption rate

Exquisite calculation

£ £

Materials 8

Labour 15

Overheads

X (0.8*5.44) 4.34

Y (.6*5.83) 3.5

Assembly (.1*25.01) 2.5

Total cost 33.35

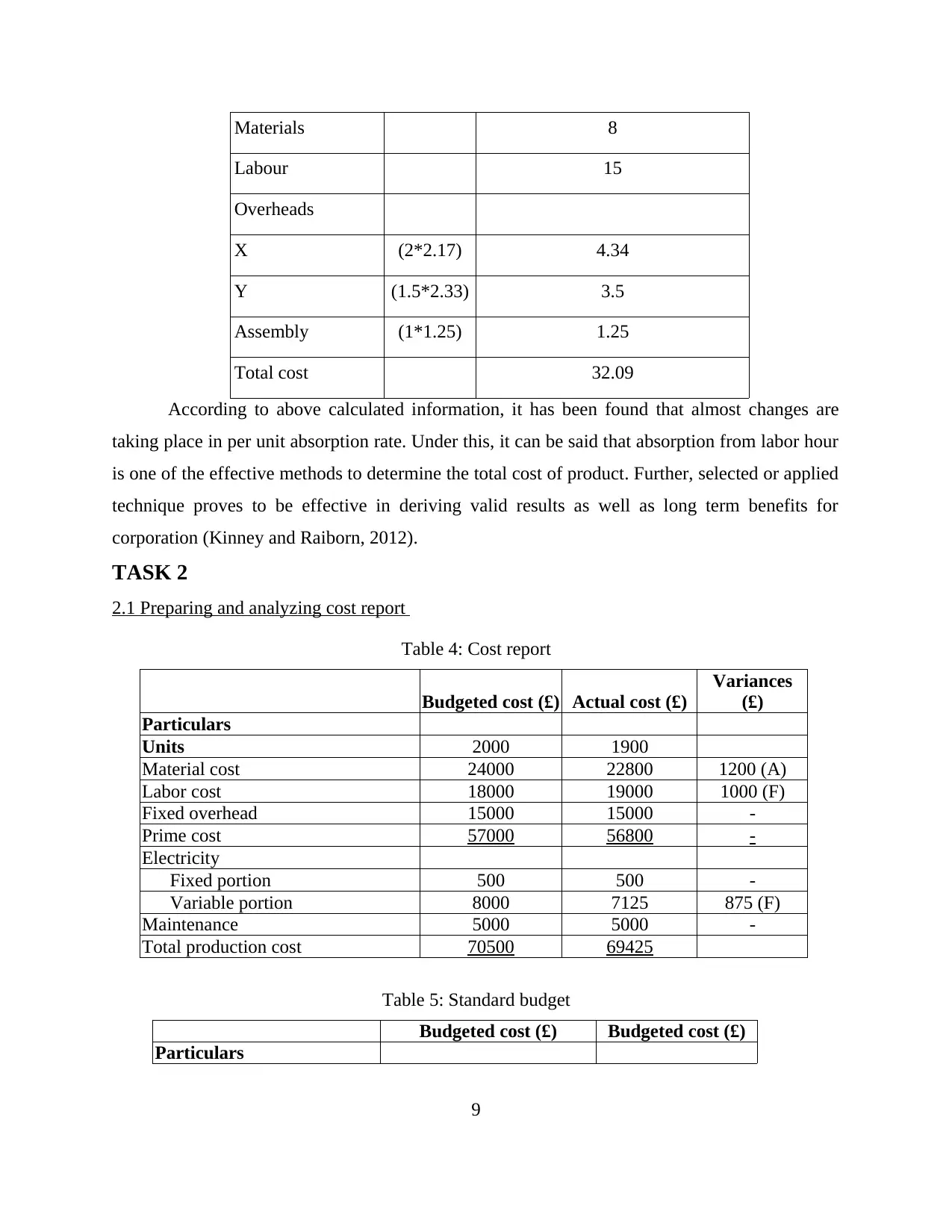

1.4 Analyzing cost of Exquisite

Table 2: Absorption rate according to labour hours

Elements Cost

Machinery X 434908/200000= 2.17

Machinery Y 349960/150000= 2.33

Assembly 250134/20000= 2.15

Table 3: Cost of Exquisite

£ £

8

Units to be produced

Material cost £400,000.00 £300,000.00 £100,000.00

per unit material 8 8 8

A/B no. of units 50000 37500 12500

Overhead absorption rate

Machinery X 434906/80000=5.44

Machinery Y 349960/60000= 5.83

Assembly 250134/10000=25.01

Computation of absorption rate

Exquisite calculation

£ £

Materials 8

Labour 15

Overheads

X (0.8*5.44) 4.34

Y (.6*5.83) 3.5

Assembly (.1*25.01) 2.5

Total cost 33.35

1.4 Analyzing cost of Exquisite

Table 2: Absorption rate according to labour hours

Elements Cost

Machinery X 434908/200000= 2.17

Machinery Y 349960/150000= 2.33

Assembly 250134/20000= 2.15

Table 3: Cost of Exquisite

£ £

8

Materials 8

Labour 15

Overheads

X (2*2.17) 4.34

Y (1.5*2.33) 3.5

Assembly (1*1.25) 1.25

Total cost 32.09

According to above calculated information, it has been found that almost changes are

taking place in per unit absorption rate. Under this, it can be said that absorption from labor hour

is one of the effective methods to determine the total cost of product. Further, selected or applied

technique proves to be effective in deriving valid results as well as long term benefits for

corporation (Kinney and Raiborn, 2012).

TASK 2

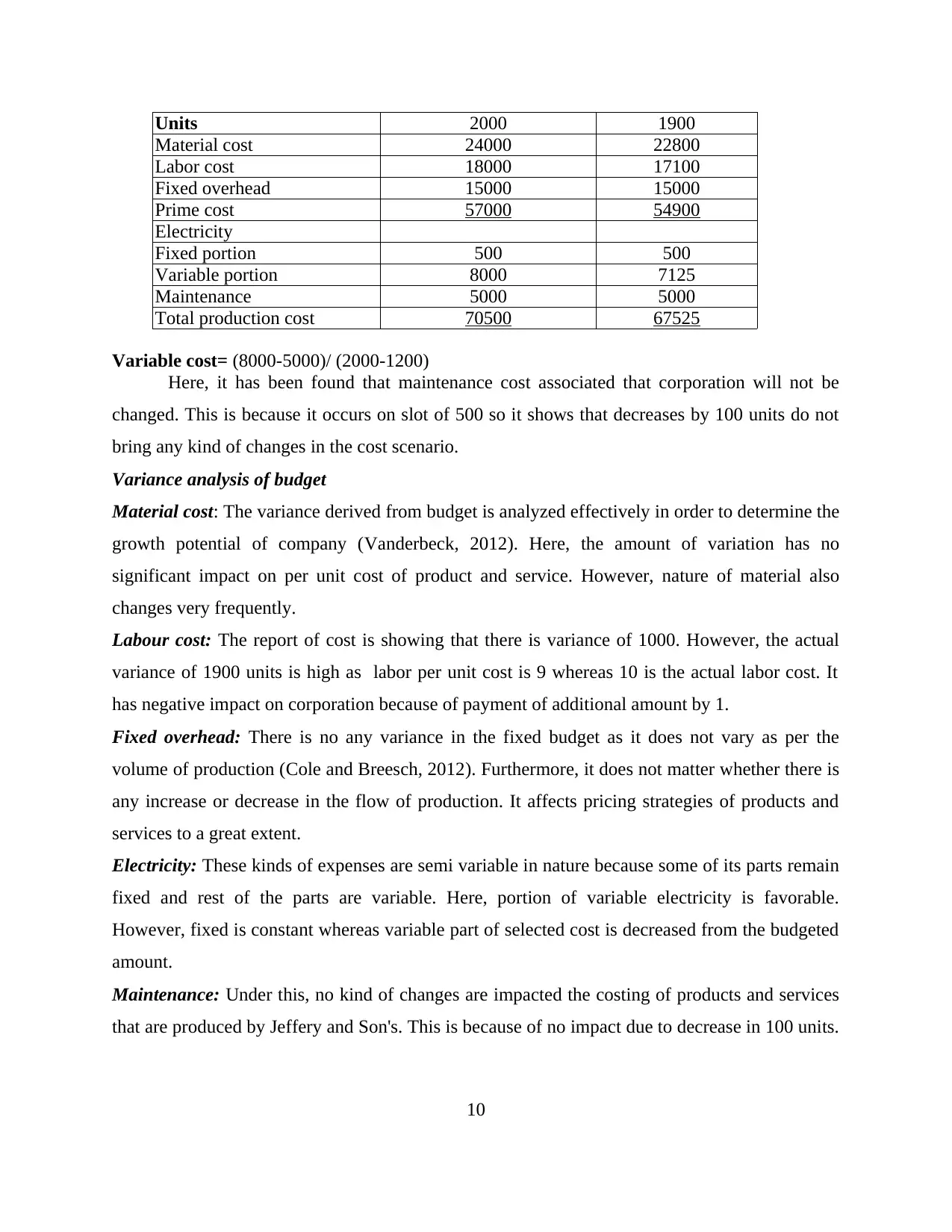

2.1 Preparing and analyzing cost report

Table 4: Cost report

Budgeted cost (£) Actual cost (£)

Variances

(£)

Particulars

Units 2000 1900

Material cost 24000 22800 1200 (A)

Labor cost 18000 19000 1000 (F)

Fixed overhead 15000 15000 -

Prime cost 57000 56800 -

Electricity

Fixed portion 500 500 -

Variable portion 8000 7125 875 (F)

Maintenance 5000 5000 -

Total production cost 70500 69425

Table 5: Standard budget

Budgeted cost (£) Budgeted cost (£)

Particulars

9

Labour 15

Overheads

X (2*2.17) 4.34

Y (1.5*2.33) 3.5

Assembly (1*1.25) 1.25

Total cost 32.09

According to above calculated information, it has been found that almost changes are

taking place in per unit absorption rate. Under this, it can be said that absorption from labor hour

is one of the effective methods to determine the total cost of product. Further, selected or applied

technique proves to be effective in deriving valid results as well as long term benefits for

corporation (Kinney and Raiborn, 2012).

TASK 2

2.1 Preparing and analyzing cost report

Table 4: Cost report

Budgeted cost (£) Actual cost (£)

Variances

(£)

Particulars

Units 2000 1900

Material cost 24000 22800 1200 (A)

Labor cost 18000 19000 1000 (F)

Fixed overhead 15000 15000 -

Prime cost 57000 56800 -

Electricity

Fixed portion 500 500 -

Variable portion 8000 7125 875 (F)

Maintenance 5000 5000 -

Total production cost 70500 69425

Table 5: Standard budget

Budgeted cost (£) Budgeted cost (£)

Particulars

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Units 2000 1900

Material cost 24000 22800

Labor cost 18000 17100

Fixed overhead 15000 15000

Prime cost 57000 54900

Electricity

Fixed portion 500 500

Variable portion 8000 7125

Maintenance 5000 5000

Total production cost 70500 67525

Variable cost= (8000-5000)/ (2000-1200)

Here, it has been found that maintenance cost associated that corporation will not be

changed. This is because it occurs on slot of 500 so it shows that decreases by 100 units do not

bring any kind of changes in the cost scenario.

Variance analysis of budget

Material cost: The variance derived from budget is analyzed effectively in order to determine the

growth potential of company (Vanderbeck, 2012). Here, the amount of variation has no

significant impact on per unit cost of product and service. However, nature of material also

changes very frequently.

Labour cost: The report of cost is showing that there is variance of 1000. However, the actual

variance of 1900 units is high as labor per unit cost is 9 whereas 10 is the actual labor cost. It

has negative impact on corporation because of payment of additional amount by 1.

Fixed overhead: There is no any variance in the fixed budget as it does not vary as per the

volume of production (Cole and Breesch, 2012). Furthermore, it does not matter whether there is

any increase or decrease in the flow of production. It affects pricing strategies of products and

services to a great extent.

Electricity: These kinds of expenses are semi variable in nature because some of its parts remain

fixed and rest of the parts are variable. Here, portion of variable electricity is favorable.

However, fixed is constant whereas variable part of selected cost is decreased from the budgeted

amount.

Maintenance: Under this, no kind of changes are impacted the costing of products and services

that are produced by Jeffery and Son's. This is because of no impact due to decrease in 100 units.

10

Material cost 24000 22800

Labor cost 18000 17100

Fixed overhead 15000 15000

Prime cost 57000 54900

Electricity

Fixed portion 500 500

Variable portion 8000 7125

Maintenance 5000 5000

Total production cost 70500 67525

Variable cost= (8000-5000)/ (2000-1200)

Here, it has been found that maintenance cost associated that corporation will not be

changed. This is because it occurs on slot of 500 so it shows that decreases by 100 units do not

bring any kind of changes in the cost scenario.

Variance analysis of budget

Material cost: The variance derived from budget is analyzed effectively in order to determine the

growth potential of company (Vanderbeck, 2012). Here, the amount of variation has no

significant impact on per unit cost of product and service. However, nature of material also

changes very frequently.

Labour cost: The report of cost is showing that there is variance of 1000. However, the actual

variance of 1900 units is high as labor per unit cost is 9 whereas 10 is the actual labor cost. It

has negative impact on corporation because of payment of additional amount by 1.

Fixed overhead: There is no any variance in the fixed budget as it does not vary as per the

volume of production (Cole and Breesch, 2012). Furthermore, it does not matter whether there is

any increase or decrease in the flow of production. It affects pricing strategies of products and

services to a great extent.

Electricity: These kinds of expenses are semi variable in nature because some of its parts remain

fixed and rest of the parts are variable. Here, portion of variable electricity is favorable.

However, fixed is constant whereas variable part of selected cost is decreased from the budgeted

amount.

Maintenance: Under this, no kind of changes are impacted the costing of products and services

that are produced by Jeffery and Son's. This is because of no impact due to decrease in 100 units.

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It depicts that corporation can easily evaluate performance and select decision related to pricing

policy (Kate-Riin Kont, 2012).

2.2 Using performance indicators to identify areas for potential improvement

The performance indicators are most imperative aspect through which Jeffrey and Son's

ltd can recognize the areas where improvement are needed. Here, following indicator are major

which are considered in order to bring improvement in the current performance of corporation.

These are explained as follows-

Financial statement-It is the most important aspect to assess the performance of organization.

Under this if management find that ratio of profitability is going down and liquidity is not

maintained (Weygandt and et. al., 2009). In that case management can lay emphasis on assessing

the causes behind poor performance and accordingly effective strategies need to be taken. It

assists corporation to change the internal environment of organization and maintain liquidity.

Increasing base of customers-In this management increasing customer base is effective

indicator which shows that corporation is performing good in the marketplace. On the other

hand, if numbers of customers are decreasing then it depicts that company need improvement in

its product and services (Key Performance Indicators. 2014). Also, focusing enhancing customer

base of business can have positive impact on firm and stronger customer base represents that

business is performing efficiently and all its customers are satisfied with the range of products

being offered to them. Apart from this, corrective measures can be easily taken with the motive

to improve customer base of the business and this will be beneficial for organization in near

future also (Vanderbeck, 2012).

High sales turnover: It can be an effective performance indicator for business enterprise where

rise in sales volume can support enterprise in knowing that overall performance of company is

increasing at faster pace. Further, with the help of this it is possible for management to identify

the major areas where improvement is required in terms of performance. High sales turnover not

only represent efficiency of business also helps in knowing the appropriate areas where

improvement is possible so that organization can enhance its sales volume. By focusing on

improvement company can easily gain competitive advantage and it is possible to utilize all the

resources in effective manner and in turn it can act as development tool for enterprise (Needles

and Crosson, 2008).

11

policy (Kate-Riin Kont, 2012).

2.2 Using performance indicators to identify areas for potential improvement

The performance indicators are most imperative aspect through which Jeffrey and Son's

ltd can recognize the areas where improvement are needed. Here, following indicator are major

which are considered in order to bring improvement in the current performance of corporation.

These are explained as follows-

Financial statement-It is the most important aspect to assess the performance of organization.

Under this if management find that ratio of profitability is going down and liquidity is not

maintained (Weygandt and et. al., 2009). In that case management can lay emphasis on assessing

the causes behind poor performance and accordingly effective strategies need to be taken. It

assists corporation to change the internal environment of organization and maintain liquidity.

Increasing base of customers-In this management increasing customer base is effective

indicator which shows that corporation is performing good in the marketplace. On the other

hand, if numbers of customers are decreasing then it depicts that company need improvement in

its product and services (Key Performance Indicators. 2014). Also, focusing enhancing customer

base of business can have positive impact on firm and stronger customer base represents that

business is performing efficiently and all its customers are satisfied with the range of products

being offered to them. Apart from this, corrective measures can be easily taken with the motive

to improve customer base of the business and this will be beneficial for organization in near

future also (Vanderbeck, 2012).

High sales turnover: It can be an effective performance indicator for business enterprise where

rise in sales volume can support enterprise in knowing that overall performance of company is

increasing at faster pace. Further, with the help of this it is possible for management to identify

the major areas where improvement is required in terms of performance. High sales turnover not

only represent efficiency of business also helps in knowing the appropriate areas where

improvement is possible so that organization can enhance its sales volume. By focusing on

improvement company can easily gain competitive advantage and it is possible to utilize all the

resources in effective manner and in turn it can act as development tool for enterprise (Needles

and Crosson, 2008).

11

Gross profit ratio: This ratio is also regarded as one of the most effective performance indicator

for business through which it is possible for management to know about the profits earned by

business and in turn it can be ensured whether all the resources are utilized in efficient manner or

not (Vance, 2002).

ROCE: This ratio is also one of the indicators which represents efficiency of the business and

supports in knowing the overall return which has been obtained by business by employing

capital. In short, it can be known whether all the financial resources are utilized efficiently by

Jeffrey and Sons or not.

EPS: This ratio supports business in knowing the efficiency of business and it is the portion of

firm’s profit which is allocated to each outstanding share of common stock (Kinney and Raiborn,

2012). It shows the profitability level of the business and provides information the stakeholders

regarding overall performance of Jeffrey and Sons in the market.

Debtor collection period: It supports in highlighting the average time taken to collect trade debts

by business. Further, this ratio can support Jeffrey and Sons to know overall efficiency of the

business.

2.3 Ways to reduce cost and enhance value, quality

Different effective ways are present with Jeffrey and Son's ltd which business can

undertake with the motive to reduce overall cost and enhancing value along with quality of the

commodity. Such ways are as follows:

Kaizen costing: This technique assists enterprise in enhancing overall level of the operations

being carried out. Further, it becomes easy for management to accomplish desired goals along

with objectives if proper costing method is employed. Moreover, business can easily enhance

motivation level of its workforce and they will prefer to take more initiative for welfare of the

business (Theeke and Mitchell, 2008). On the other hand, major costs can be saved which is

linked with wastage in the production process.

Total quality management: This technique supports management in enhancing the quality level

of the product along with major cost associated with production can be saved easily. Through

this, it is possible for business to identify the major areas where improvement is possible and in

turn it acts as development tool for enterprise. Further, it can assist Jeffrey and Son's ltd in

12

for business through which it is possible for management to know about the profits earned by

business and in turn it can be ensured whether all the resources are utilized in efficient manner or

not (Vance, 2002).

ROCE: This ratio is also one of the indicators which represents efficiency of the business and

supports in knowing the overall return which has been obtained by business by employing

capital. In short, it can be known whether all the financial resources are utilized efficiently by

Jeffrey and Sons or not.

EPS: This ratio supports business in knowing the efficiency of business and it is the portion of

firm’s profit which is allocated to each outstanding share of common stock (Kinney and Raiborn,

2012). It shows the profitability level of the business and provides information the stakeholders

regarding overall performance of Jeffrey and Sons in the market.

Debtor collection period: It supports in highlighting the average time taken to collect trade debts

by business. Further, this ratio can support Jeffrey and Sons to know overall efficiency of the

business.

2.3 Ways to reduce cost and enhance value, quality

Different effective ways are present with Jeffrey and Son's ltd which business can

undertake with the motive to reduce overall cost and enhancing value along with quality of the

commodity. Such ways are as follows:

Kaizen costing: This technique assists enterprise in enhancing overall level of the operations

being carried out. Further, it becomes easy for management to accomplish desired goals along

with objectives if proper costing method is employed. Moreover, business can easily enhance

motivation level of its workforce and they will prefer to take more initiative for welfare of the

business (Theeke and Mitchell, 2008). On the other hand, major costs can be saved which is

linked with wastage in the production process.

Total quality management: This technique supports management in enhancing the quality level

of the product along with major cost associated with production can be saved easily. Through

this, it is possible for business to identify the major areas where improvement is possible and in

turn it acts as development tool for enterprise. Further, it can assist Jeffrey and Son's ltd in

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.