Management Accounting Report: Methods, Budgeting, and Analysis

VerifiedAdded on 2019/12/28

|15

|4142

|331

Report

AI Summary

This report provides a comprehensive overview of management accounting, focusing on its importance in decision-making processes. It delves into various management accounting methods, including marginal costing, absorption costing, and activity-based costing, highlighting their applications and merits. The report includes a comparative analysis of these methods, demonstrating their impact on profit calculations and financial statements. Furthermore, it discusses budgeting systems, their role in planning, and their comparison with other planning tools. The report also presents a critical evaluation of each method, emphasizing their practical applications within an organization and their role in cost analysis, make-or-buy decisions, and selling strategies. The report includes tables and illustrations to clarify the concepts and calculations. The report concludes with an examination of budget implications and reconciliation of profit and loss statements under different costing methods. Overall, the report aims to provide a solid understanding of management accounting principles and their practical application in business management.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

SECTION 1......................................................................................................................................1

1 Importance of management accounting in decision-making...............................................1

2 Different types of Management Accounting Methods........................................................2

3 Critical Evaluation of Management methods and their application ..................................3

4 Absorption and Marginal costing........................................................................................4

a) Comparative Income Statement ...............................................................................4

C) Reconciliation of Profit and Loss Statements..........................................................7

SECTION 2......................................................................................................................................8

PART A...........................................................................................................................................8

A budget is a forecast of which is expected to happen within the business during the next year

................................................................................................................................................8

Comparison and contrasting three planning tools used in management accounting .............9

Part B ............................................................................................................................................10

A...........................................................................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

ILLUSTRATION INDEX

Illustration 1: Table 1: Calculation of profits under Absorption Costing........................................5

Illustration 2: Table 2 : Calculation of cost per unit........................................................................5

Illustration 3: Table 3: Calculation of net profits as per Marginal Costing.....................................6

Illustration 4: Table 4 : Reconciliation under Marginal costing......................................................7

Illustration 5: Table 5 : Reconciliation as per Absorption costing..................................................7

INTRODUCTION...........................................................................................................................1

SECTION 1......................................................................................................................................1

1 Importance of management accounting in decision-making...............................................1

2 Different types of Management Accounting Methods........................................................2

3 Critical Evaluation of Management methods and their application ..................................3

4 Absorption and Marginal costing........................................................................................4

a) Comparative Income Statement ...............................................................................4

C) Reconciliation of Profit and Loss Statements..........................................................7

SECTION 2......................................................................................................................................8

PART A...........................................................................................................................................8

A budget is a forecast of which is expected to happen within the business during the next year

................................................................................................................................................8

Comparison and contrasting three planning tools used in management accounting .............9

Part B ............................................................................................................................................10

A...........................................................................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

ILLUSTRATION INDEX

Illustration 1: Table 1: Calculation of profits under Absorption Costing........................................5

Illustration 2: Table 2 : Calculation of cost per unit........................................................................5

Illustration 3: Table 3: Calculation of net profits as per Marginal Costing.....................................6

Illustration 4: Table 4 : Reconciliation under Marginal costing......................................................7

Illustration 5: Table 5 : Reconciliation as per Absorption costing..................................................7

INTRODUCTION

Management Accounting being one of the most crucial and critical functions of the organisation.

The decision-making process is highly supported by management accounting principles and

procedures further; there are various systems of management accounting. Systems are explained

with their merits and applications on the organisation. Further this report deals with the

comparison of profits under different methods and their interpretations. Moreover, budgeting

implications are discussed and compared with various planning tools. Various financial problems

can be assessed and solved with the help of management accounting.

SECTION 1

1 Importance of management accounting in decision-making

Management accounting is a process which provides data to take several decisions in the

business. It is a process helps to identify financial information's which leads to formulating better

plan and strategies to make the enterprise more profitable. The importance of the accounting

information's to take business decisions are as follows:

Analysing Growth: The management accounting information gives help to analyse business

performance as well as growth in the industry where the firm operates (Bowen, Call and

Rajgopal, 2010). If the firm is not growing in a better way and not profitable compared to a

previous year, then managers are making the proper strategies which lead to increase sales and

profit. Hence, the information is important to analyse growth and take corrective actions.

Make or Buy Analysis: the Primary importance of the management accounting information is

that components or raw material of products and services are whether to produce or buy from the

market. For example, in a small enterprise, a component of the product can be make and can buy.

From the Accounting, Information Company analyse that in making the component or in produce

the component, the high cost is incurred. Which strategy or which technique will incur less cost

that will be adopted in the production process. So, it helps to take decisions in the make or buy

component of goods and services.

Activity was Based Costing Technique: The technique is important to the business enterprise

to decide and appoint the best person who can sell the products and services effectively in the

business. As well as the accounting information's helpful for the firm to derive the cost incurred

1

Management Accounting being one of the most crucial and critical functions of the organisation.

The decision-making process is highly supported by management accounting principles and

procedures further; there are various systems of management accounting. Systems are explained

with their merits and applications on the organisation. Further this report deals with the

comparison of profits under different methods and their interpretations. Moreover, budgeting

implications are discussed and compared with various planning tools. Various financial problems

can be assessed and solved with the help of management accounting.

SECTION 1

1 Importance of management accounting in decision-making

Management accounting is a process which provides data to take several decisions in the

business. It is a process helps to identify financial information's which leads to formulating better

plan and strategies to make the enterprise more profitable. The importance of the accounting

information's to take business decisions are as follows:

Analysing Growth: The management accounting information gives help to analyse business

performance as well as growth in the industry where the firm operates (Bowen, Call and

Rajgopal, 2010). If the firm is not growing in a better way and not profitable compared to a

previous year, then managers are making the proper strategies which lead to increase sales and

profit. Hence, the information is important to analyse growth and take corrective actions.

Make or Buy Analysis: the Primary importance of the management accounting information is

that components or raw material of products and services are whether to produce or buy from the

market. For example, in a small enterprise, a component of the product can be make and can buy.

From the Accounting, Information Company analyse that in making the component or in produce

the component, the high cost is incurred. Which strategy or which technique will incur less cost

that will be adopted in the production process. So, it helps to take decisions in the make or buy

component of goods and services.

Activity was Based Costing Technique: The technique is important to the business enterprise

to decide and appoint the best person who can sell the products and services effectively in the

business. As well as the accounting information's helpful for the firm to derive the cost incurred

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

in every activity of production process. By the information, the firm can know that which

activity is having the high cost of the amount.

The method of Selling: It is very necessary for a business that on which basis the products and

services are to be sold in the market (Schaltegger, Gibassier and Zvezdov, 2013). The

accounting information gives the data related to various direct and indirect cost associated with

the products. By costs, the firm takes the decision that how much percentage of margin has to be

charged and which selling method is to be selected. If the advertisement strategy is being used

then, the cost is also incurred in the price. So, it can be said that management accounting is very

important to decide selling method for sale the products and services.

Cost Analysis: Cost is the very sensitive factor of a business entity. Higher the cost and low

production are unfavourable for the firm. In the accounting, all the costs are recorded which are

incurred to produce goods and services. From the accounting information's management able to

derive costs and analyse that whether the cost is high or low. If the cost is unfavourable then the

management able to take the decision and formulate the strategies to increase sales and revenue

(Contrafatto and Burns, 2013). From the information's company able to know that where the

problem is occurring and what the corrective actions should be taken to overcome the problem of

cost increase.

2 Different types of Management Accounting Methods

There are various methods of Management accounting based on different assumptions and

following various streamlined processes. However, some of the major methods followed by the

majority of the manufacturing units are explained below:

Marginal System: Marginal costing is a method under which variable costs are only

associated with the units and fixed cost are not allocated. All the costs are classified into

fixed cost and variable cost. Marginal as the word depicts is an additional cost incurred

for every one unit produced additionally (Malmi, 2010). Therefore it shows the effect of

the change in volume on the profits of the firm. As per this method, fixed cost are

periodic cost and are charged directly to the profits for that period. The contribution is

arrived after deducting variable costs from the sales, and net profit is arrived after

deducting fixed costs from the contribution.

2

activity is having the high cost of the amount.

The method of Selling: It is very necessary for a business that on which basis the products and

services are to be sold in the market (Schaltegger, Gibassier and Zvezdov, 2013). The

accounting information gives the data related to various direct and indirect cost associated with

the products. By costs, the firm takes the decision that how much percentage of margin has to be

charged and which selling method is to be selected. If the advertisement strategy is being used

then, the cost is also incurred in the price. So, it can be said that management accounting is very

important to decide selling method for sale the products and services.

Cost Analysis: Cost is the very sensitive factor of a business entity. Higher the cost and low

production are unfavourable for the firm. In the accounting, all the costs are recorded which are

incurred to produce goods and services. From the accounting information's management able to

derive costs and analyse that whether the cost is high or low. If the cost is unfavourable then the

management able to take the decision and formulate the strategies to increase sales and revenue

(Contrafatto and Burns, 2013). From the information's company able to know that where the

problem is occurring and what the corrective actions should be taken to overcome the problem of

cost increase.

2 Different types of Management Accounting Methods

There are various methods of Management accounting based on different assumptions and

following various streamlined processes. However, some of the major methods followed by the

majority of the manufacturing units are explained below:

Marginal System: Marginal costing is a method under which variable costs are only

associated with the units and fixed cost are not allocated. All the costs are classified into

fixed cost and variable cost. Marginal as the word depicts is an additional cost incurred

for every one unit produced additionally (Malmi, 2010). Therefore it shows the effect of

the change in volume on the profits of the firm. As per this method, fixed cost are

periodic cost and are charged directly to the profits for that period. The contribution is

arrived after deducting variable costs from the sales, and net profit is arrived after

deducting fixed costs from the contribution.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Budgeting System: Budgeting is the process by which pre-planned budgets are prepared

and compared with the actual performance of the business and variances are analysed,

and corrective measures are undertaken to improve the situation. This is the most popular

system, as it compares the data and has the scope for improvement. Also, it gives a clear

picture about future expenses and incomes and also increases profitability by reducing

waste. Various budgets are prepared for monthly, quarterly or annual basis and compared

with actual results.

Activity Based System: As per activity based system all the costs are pooled, and cost

drivers are assigned and then by cost drivers all the costs are classified for different

products as per the resources utilised by the products (Caglio and Ditillo, 2012). Cost

objects are charged cost and it depicts clear picture based on the activities performed in

the context of particular products. Unlike traditional costing, it makes the cost allocation

more understandable and appropriate. This is best suited for complex scenarios where

many processes and techniques are applied for the production process.

3 Critical Evaluation of Management methods and their application

Every method has some merits and demerits attached to it. However, application and merits of

the system make it widely acceptable and appropriate. Benefits and applications of various

systems are explained here below:

Marginal system

Merits

It depicts the interrelationship between cost, price and volume. As marginal costing is

based on calculating the contribution and arriving at profitability therefore clearly.

A further contribution is used as an effective tool in decision making and helps in making

various transfer pricing decisions for internal pricing decisions.

Marginal costing is simple and easy to understand and apply (Kachelmeier. and

Williamson, 2010). Since it involves no fixed cost and therefore absorption of fixed cost

is not performed under marginal costing.

Marginal costing is applicable for the above mentioned organisation since3 it works in various

departments. Therefore, fixed cost need not be apportioned separately and can be deducted from

contribution to arrive at net profit.

3

and compared with the actual performance of the business and variances are analysed,

and corrective measures are undertaken to improve the situation. This is the most popular

system, as it compares the data and has the scope for improvement. Also, it gives a clear

picture about future expenses and incomes and also increases profitability by reducing

waste. Various budgets are prepared for monthly, quarterly or annual basis and compared

with actual results.

Activity Based System: As per activity based system all the costs are pooled, and cost

drivers are assigned and then by cost drivers all the costs are classified for different

products as per the resources utilised by the products (Caglio and Ditillo, 2012). Cost

objects are charged cost and it depicts clear picture based on the activities performed in

the context of particular products. Unlike traditional costing, it makes the cost allocation

more understandable and appropriate. This is best suited for complex scenarios where

many processes and techniques are applied for the production process.

3 Critical Evaluation of Management methods and their application

Every method has some merits and demerits attached to it. However, application and merits of

the system make it widely acceptable and appropriate. Benefits and applications of various

systems are explained here below:

Marginal system

Merits

It depicts the interrelationship between cost, price and volume. As marginal costing is

based on calculating the contribution and arriving at profitability therefore clearly.

A further contribution is used as an effective tool in decision making and helps in making

various transfer pricing decisions for internal pricing decisions.

Marginal costing is simple and easy to understand and apply (Kachelmeier. and

Williamson, 2010). Since it involves no fixed cost and therefore absorption of fixed cost

is not performed under marginal costing.

Marginal costing is applicable for the above mentioned organisation since3 it works in various

departments. Therefore, fixed cost need not be apportioned separately and can be deducted from

contribution to arrive at net profit.

3

Budgeting System

Merits

It defines the targets and objectives to be attained by various departments which are

necessary for success and growth.

Further, if the performance is detected below the targets controlling measures are adopted

for the same and therefore budget brings efficiency and effectiveness in management

(Papaspyropoulos and et.al., 2012).

Moreover, Budget controls facilitate the controlling the organisations from a single

central point even in the case of decentralised functions.

Since the organisation is working in the department and is medium sized therefore for effective

utilisation of resources and removing the duplication budgeting is crucial.

Activity Based Budgeting

Merits

Be effective controlling of cost fixed and variable costs can be reduced and controlled

easily.

Activity based budgeting establishes cause and effect relationships between various

factors and therefore is very scientific and technical (Tucker and D. Lowe, 2014).

Decision making is prospered by activity based system as it depicts clear profitability

devoted to the particular product.

Since the organisation is complex and have many departments, therefore, the allocation of costs

by activities will present clear picture about profitability.

4 Absorption and Marginal costing

a) Comparative Income Statement

4

Merits

It defines the targets and objectives to be attained by various departments which are

necessary for success and growth.

Further, if the performance is detected below the targets controlling measures are adopted

for the same and therefore budget brings efficiency and effectiveness in management

(Papaspyropoulos and et.al., 2012).

Moreover, Budget controls facilitate the controlling the organisations from a single

central point even in the case of decentralised functions.

Since the organisation is working in the department and is medium sized therefore for effective

utilisation of resources and removing the duplication budgeting is crucial.

Activity Based Budgeting

Merits

Be effective controlling of cost fixed and variable costs can be reduced and controlled

easily.

Activity based budgeting establishes cause and effect relationships between various

factors and therefore is very scientific and technical (Tucker and D. Lowe, 2014).

Decision making is prospered by activity based system as it depicts clear profitability

devoted to the particular product.

Since the organisation is complex and have many departments, therefore, the allocation of costs

by activities will present clear picture about profitability.

4 Absorption and Marginal costing

a) Comparative Income Statement

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

5

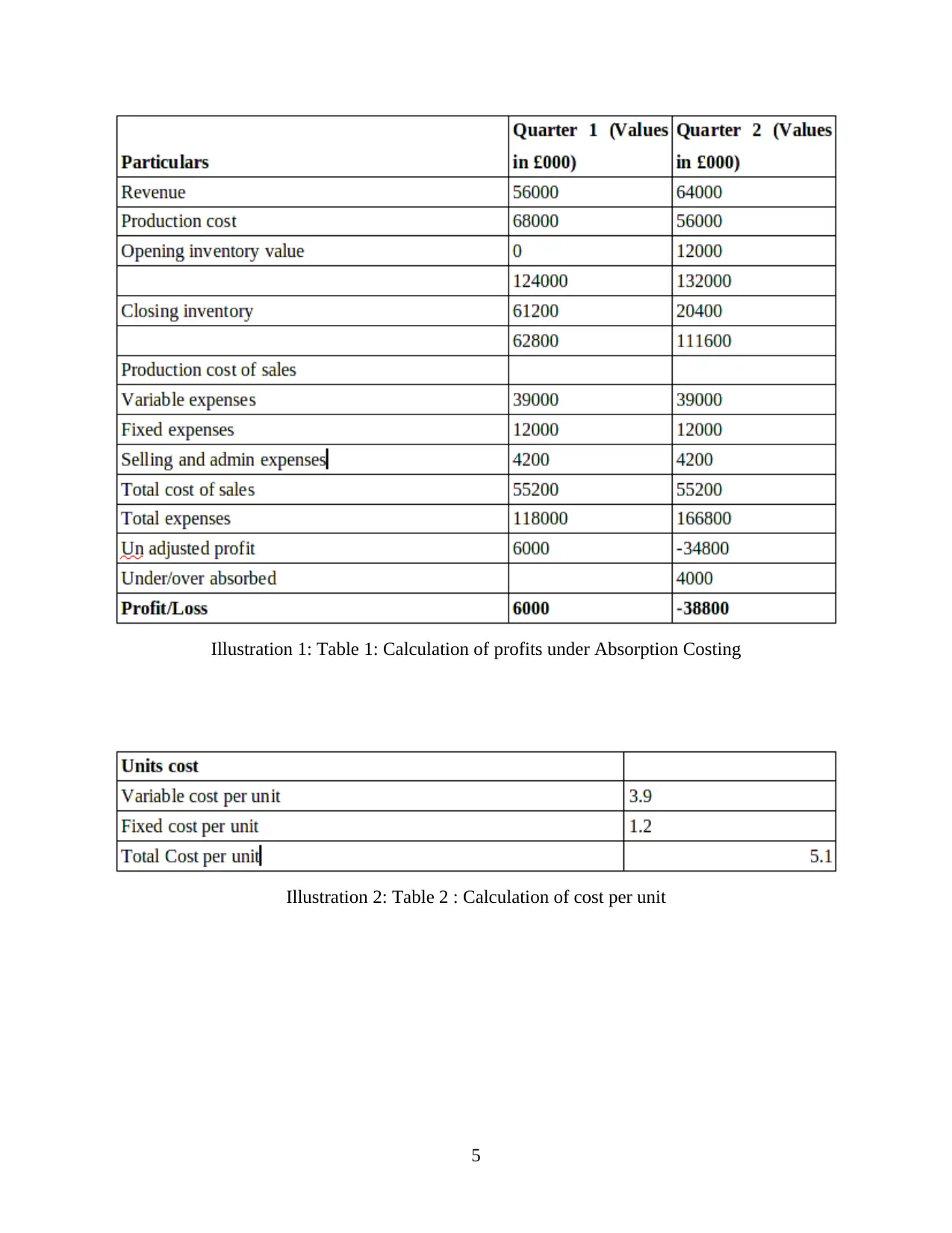

Illustration 1: Table 1: Calculation of profits under Absorption Costing

Illustration 2: Table 2 : Calculation of cost per unit

Illustration 1: Table 1: Calculation of profits under Absorption Costing

Illustration 2: Table 2 : Calculation of cost per unit

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

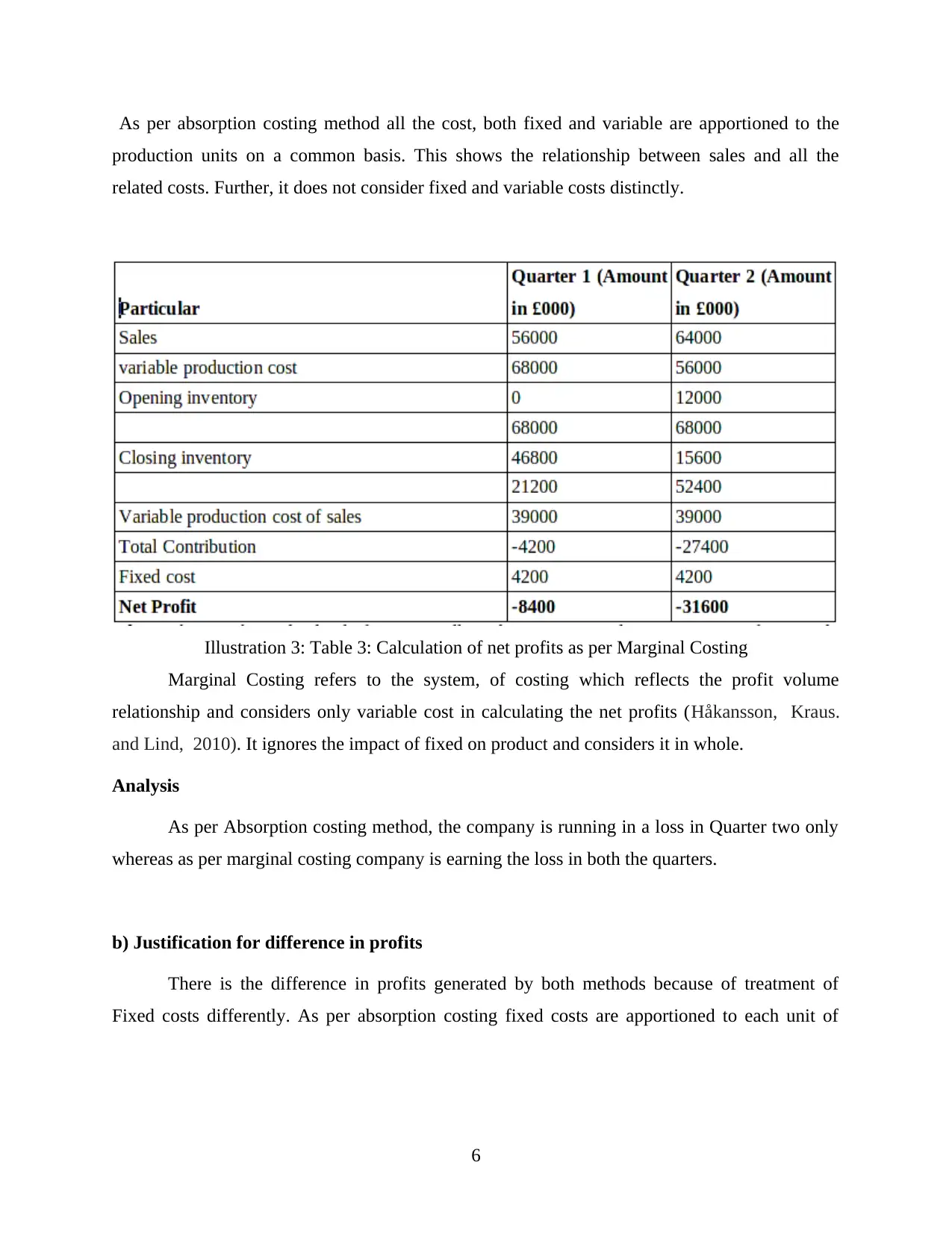

As per absorption costing method all the cost, both fixed and variable are apportioned to the

production units on a common basis. This shows the relationship between sales and all the

related costs. Further, it does not consider fixed and variable costs distinctly.

Marginal Costing refers to the system, of costing which reflects the profit volume

relationship and considers only variable cost in calculating the net profits (Håkansson, Kraus.

and Lind, 2010). It ignores the impact of fixed on product and considers it in whole.

Analysis

As per Absorption costing method, the company is running in a loss in Quarter two only

whereas as per marginal costing company is earning the loss in both the quarters.

b) Justification for difference in profits

There is the difference in profits generated by both methods because of treatment of

Fixed costs differently. As per absorption costing fixed costs are apportioned to each unit of

6

Illustration 3: Table 3: Calculation of net profits as per Marginal Costing

production units on a common basis. This shows the relationship between sales and all the

related costs. Further, it does not consider fixed and variable costs distinctly.

Marginal Costing refers to the system, of costing which reflects the profit volume

relationship and considers only variable cost in calculating the net profits (Håkansson, Kraus.

and Lind, 2010). It ignores the impact of fixed on product and considers it in whole.

Analysis

As per Absorption costing method, the company is running in a loss in Quarter two only

whereas as per marginal costing company is earning the loss in both the quarters.

b) Justification for difference in profits

There is the difference in profits generated by both methods because of treatment of

Fixed costs differently. As per absorption costing fixed costs are apportioned to each unit of

6

Illustration 3: Table 3: Calculation of net profits as per Marginal Costing

production whereas as marginal costing supports the deduction of total fixed costs from the

contribution derived (Zaleha Abdul Rasid. and et.al., 2011).

As per absorption costing if the closing stock increases the profitability also increases whereas in

marginal costing if the closing stock increases the profitability will reduce.

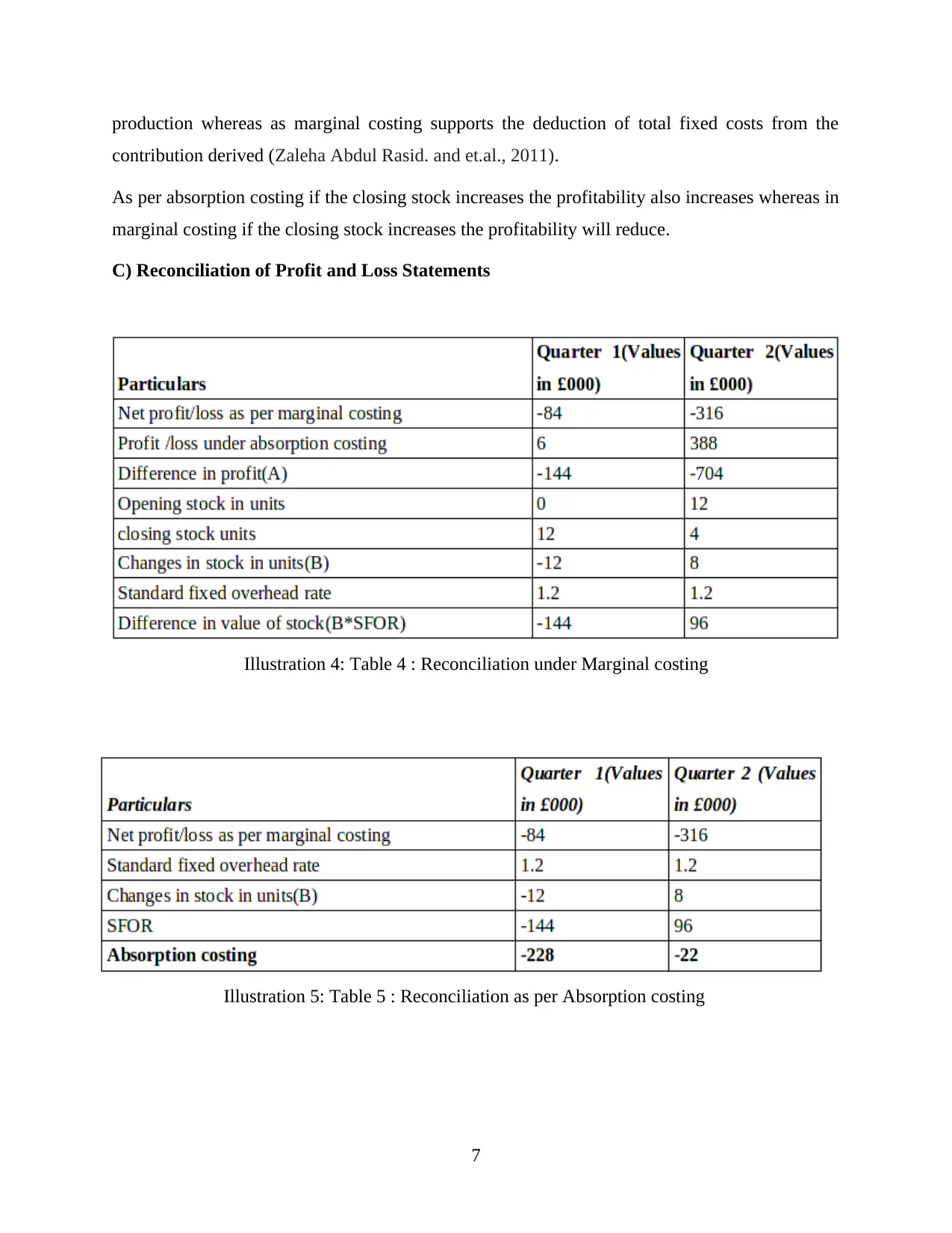

C) Reconciliation of Profit and Loss Statements

7

Illustration 4: Table 4 : Reconciliation under Marginal costing

Illustration 5: Table 5 : Reconciliation as per Absorption costing

contribution derived (Zaleha Abdul Rasid. and et.al., 2011).

As per absorption costing if the closing stock increases the profitability also increases whereas in

marginal costing if the closing stock increases the profitability will reduce.

C) Reconciliation of Profit and Loss Statements

7

Illustration 4: Table 4 : Reconciliation under Marginal costing

Illustration 5: Table 5 : Reconciliation as per Absorption costing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

As per marginal costing difference in value comes to £144000 in quarter 1 in contrast to

£96000 in Quarter 2 whereas absorption costing lays the difference in quarter one as negative

£228000 and -£22000 in Quarter 2.

Reconciliation is an effective tool to reconcile and evaluate various items of the cost-

profit analysis and their relationships (Jansen, 2011). Further costs under marginal and

absorption costing are calculated differently. Since valuation of the stock is a matter of concern

under two different methods, therefore, reconciliation makes the clear line of difference between

them. Increase and decrease in a level of closing stock affect the profitability of the business.

SECTION 2

PART A

A budget is a forecast of which is expected to happen within the business during the next year

Budget is regarded as an important tool that is being used by the management in making

prediction of overall expenses so that plans can be developed in reducing the expenses and

increasing the revenues in an effective manner. A budget is regarded as a plan that offers

financial data to all the users of the firm in offering guidance to the existing business through

offering sufficient path within the organisation (Wu and Boateng, 2010). The present financial

resources are being tested on varied parameters for setting a specific plan for the future course of

time. The accuracy of all the transactions emerges within the organisation would get automated.

There is presence of main form of budgeting that assist the individual in setting structure of the

business to develop sound decisions in the present firm that are enumerated as under:

Zero base budgeting: The particular budget is being developed for each year as it does

not carry out estimation by base year, so the as to carry out the organisational operations.

It takes into consideration all the components relates with the venture that is comprised of

income as well as expenditure (Jinga. and et.al., 2010). The specific element would be

analysed for the purpose of making a determination of its significance within the firm.

There is the presence of greater significance of each and every expenditure as there is the

lack of interdependency of any factor on other.

8

£96000 in Quarter 2 whereas absorption costing lays the difference in quarter one as negative

£228000 and -£22000 in Quarter 2.

Reconciliation is an effective tool to reconcile and evaluate various items of the cost-

profit analysis and their relationships (Jansen, 2011). Further costs under marginal and

absorption costing are calculated differently. Since valuation of the stock is a matter of concern

under two different methods, therefore, reconciliation makes the clear line of difference between

them. Increase and decrease in a level of closing stock affect the profitability of the business.

SECTION 2

PART A

A budget is a forecast of which is expected to happen within the business during the next year

Budget is regarded as an important tool that is being used by the management in making

prediction of overall expenses so that plans can be developed in reducing the expenses and

increasing the revenues in an effective manner. A budget is regarded as a plan that offers

financial data to all the users of the firm in offering guidance to the existing business through

offering sufficient path within the organisation (Wu and Boateng, 2010). The present financial

resources are being tested on varied parameters for setting a specific plan for the future course of

time. The accuracy of all the transactions emerges within the organisation would get automated.

There is presence of main form of budgeting that assist the individual in setting structure of the

business to develop sound decisions in the present firm that are enumerated as under:

Zero base budgeting: The particular budget is being developed for each year as it does

not carry out estimation by base year, so the as to carry out the organisational operations.

It takes into consideration all the components relates with the venture that is comprised of

income as well as expenditure (Jinga. and et.al., 2010). The specific element would be

analysed for the purpose of making a determination of its significance within the firm.

There is the presence of greater significance of each and every expenditure as there is the

lack of interdependency of any factor on other.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Incremental budgeting: The traditional approach is being complied with by varied

business who makes an analysis of the present efficiency of the firm by previous year

facts as well as figures. Such budget is in total dependent on another budget through

comparison of actual performance with the previous year so as to gain insight to the

increase as well as decrease that exists over the period (Coyne and et.al., 2010). The

budget is effective in making the forecast of the future expenses and losses to increase the

present performance. The accurate, as well as valid approach, would assist the statement

which presents that zero base budgeting has main motive towards seeking future business

opportunities through emphasising on present strength as well as weakness.

Comparison and contrasting three planning tools used in management accounting

There are several management accounting tools that are being utilized in planning

regarding increasing the current financial conditions of the firm that are enumerated in the

manner as under:

Throughput accounting: This is regarded as an important tool which is being utilised in

management accounting for the purpose of enhancing the power of decision making of all the

users within the firm (Harris and Durden, 2012). It is considered as the package of decision-

making that stress on several factors like dynamic, integration, principle based as well as a

comprehensive management tool for accounting.

Financial statement analysis: The financial statements are being prepared by the organisation

for the purpose of demonstrating the existing capabilities. The financial statement assists as

minor that demonstrates the image of the business in front of the external market for the purpose

of gaining an advantage over competitors (Faÿ, Introna and Puyou, 2010). The major emphasis

of such business is towards communication only financial performance through commenting on

the several streams like profitability, liquidity, and efficiency as well as investor ratio.

Decision accounting: This is a form of management accounting tools assisting in making

decisions to offers benefits of the firm. This form of accounting tool is being utilised in

enhancing the firm as it emphasises on a recording of the decisions that are being taken by the

owner in general course of business. The present approach would offer decision support system

that offers owner to make the selection of the appropriate option.

9

business who makes an analysis of the present efficiency of the firm by previous year

facts as well as figures. Such budget is in total dependent on another budget through

comparison of actual performance with the previous year so as to gain insight to the

increase as well as decrease that exists over the period (Coyne and et.al., 2010). The

budget is effective in making the forecast of the future expenses and losses to increase the

present performance. The accurate, as well as valid approach, would assist the statement

which presents that zero base budgeting has main motive towards seeking future business

opportunities through emphasising on present strength as well as weakness.

Comparison and contrasting three planning tools used in management accounting

There are several management accounting tools that are being utilized in planning

regarding increasing the current financial conditions of the firm that are enumerated in the

manner as under:

Throughput accounting: This is regarded as an important tool which is being utilised in

management accounting for the purpose of enhancing the power of decision making of all the

users within the firm (Harris and Durden, 2012). It is considered as the package of decision-

making that stress on several factors like dynamic, integration, principle based as well as a

comprehensive management tool for accounting.

Financial statement analysis: The financial statements are being prepared by the organisation

for the purpose of demonstrating the existing capabilities. The financial statement assists as

minor that demonstrates the image of the business in front of the external market for the purpose

of gaining an advantage over competitors (Faÿ, Introna and Puyou, 2010). The major emphasis

of such business is towards communication only financial performance through commenting on

the several streams like profitability, liquidity, and efficiency as well as investor ratio.

Decision accounting: This is a form of management accounting tools assisting in making

decisions to offers benefits of the firm. This form of accounting tool is being utilised in

enhancing the firm as it emphasises on a recording of the decisions that are being taken by the

owner in general course of business. The present approach would offer decision support system

that offers owner to make the selection of the appropriate option.

9

Part B

A

Varied management accounting methods that are applied and their effectiveness in dealing

with the financial problem are given below. Variance analysis: It is the one of the most important tool of the management accounting

that is used by the managers at the workplace. By using this tool firm performance is

measured and areas, where it is not good, are identified (Hansen, 2011). To apply

variance analysis method at the workplace first of all standards are determined and then

actual performance of the firm is measured. By comparing both firm performances is

accessed and areas where there is a need to deal with financial problems are identified. Ratio analysis: In the present era, companies have to examine and evaluate their

performance regularly to examine their operational performance as well as financial

strength. Ratio analysis is one of the best and effective tools that assist Nero Ltd and

other business organisations to analyse their effectiveness of operations. There is a

different kind of ratios that can be used by the firm such as profitability, liquidity,

solvency and efficiency ratios (Ratio analysis, 2016). Every ratio quantifies a relationship

between two monetary elements which helps Nero Ltd to determine their performance. It

is considered as an effective way which can be incorporated by Nero Ltd to examine their

performance excellence and financial position. This technique aware company about their

threats and monetary challenges due to which, the company has not reported excellent

performance. In such respect, profitability ratios enable Nero Ltd to determine that

whether the company has generated enough profit or yield or not on their turnover.

Liquidity ratios guide firm about their capabilities to repay their deferral payments to

suppliers by identifying the relationship between current assets and current liabilities. On

the other hand, efficiency ratio reveals that how effectively managers of the firm had

utilised corporate assets to generate a greater amount of revenues. However, solvency

ratios reveal information about the corporate ability to manage financial risk by the

optimum and effective mix of debt and equity capital. Through all the ratios, Nero Ltd

can determine their financial difficulties and challenges and take appropriate decisions to

overcome the same and drive success.

10

A

Varied management accounting methods that are applied and their effectiveness in dealing

with the financial problem are given below. Variance analysis: It is the one of the most important tool of the management accounting

that is used by the managers at the workplace. By using this tool firm performance is

measured and areas, where it is not good, are identified (Hansen, 2011). To apply

variance analysis method at the workplace first of all standards are determined and then

actual performance of the firm is measured. By comparing both firm performances is

accessed and areas where there is a need to deal with financial problems are identified. Ratio analysis: In the present era, companies have to examine and evaluate their

performance regularly to examine their operational performance as well as financial

strength. Ratio analysis is one of the best and effective tools that assist Nero Ltd and

other business organisations to analyse their effectiveness of operations. There is a

different kind of ratios that can be used by the firm such as profitability, liquidity,

solvency and efficiency ratios (Ratio analysis, 2016). Every ratio quantifies a relationship

between two monetary elements which helps Nero Ltd to determine their performance. It

is considered as an effective way which can be incorporated by Nero Ltd to examine their

performance excellence and financial position. This technique aware company about their

threats and monetary challenges due to which, the company has not reported excellent

performance. In such respect, profitability ratios enable Nero Ltd to determine that

whether the company has generated enough profit or yield or not on their turnover.

Liquidity ratios guide firm about their capabilities to repay their deferral payments to

suppliers by identifying the relationship between current assets and current liabilities. On

the other hand, efficiency ratio reveals that how effectively managers of the firm had

utilised corporate assets to generate a greater amount of revenues. However, solvency

ratios reveal information about the corporate ability to manage financial risk by the

optimum and effective mix of debt and equity capital. Through all the ratios, Nero Ltd

can determine their financial difficulties and challenges and take appropriate decisions to

overcome the same and drive success.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.