Evaluating Performance and Management Control Systems in Insurance

VerifiedAdded on 2020/02/24

|22

|4796

|380

Report

AI Summary

This report evaluates the performance and management control systems of three leading Australian insurance companies: AMP Limited, IAG Limited, and QBE Insurance Group, focusing on executive performance and remuneration policies. The analysis examines executive remuneration allocation, changes in reporting, company performance versus executive pay, and the mix of performance measures used. The report compares remuneration systems, summarizes findings, analyzes remuneration methods, and offers recommendations for improving reporting and performance measures. The study reveals insights into the relationship between financial performance and executive compensation, highlighting the strengths and weaknesses of each company's approach. The report concludes by assessing the efficacy of the overall organizational performance and providing recommendations for enhanced reporting and performance measurement.

Running head: MEASURING PERFORMANCE AND MANAGEMENT CONTROL

SYSTEMS

Measuring Performance and Management Control Systems

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

SYSTEMS

Measuring Performance and Management Control Systems

Name of the Student:

Name of the University:

Author’s Note:

Course ID:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1MEASURING PERFORMANCE AND MANAGEMENT CONTROL SYSTEMS

Executive Summary:

The current report aims to evaluate the performance and management control systems

of the three leading insurance companies in Australia in order to assess the effectiveness of

executive performance and remuneration policies. The three organisations that have selected

to fit the purpose of this report include AMP Limited, IAG Limited and QBE Insurance

Group. The remuneration systems for the three organisations have been evaluated as well to

assess the efficacy of the overall organisational performance. Finally, the report sheds light

on providing recommendations for improving the reporting along with widening the

performance measures of the organisation. It has been found that it could be stated that the

remuneration methods of AMP Limited are superior in contrast to the other two organisations

due to better financial performance in the Australian insurance industry.

Executive Summary:

The current report aims to evaluate the performance and management control systems

of the three leading insurance companies in Australia in order to assess the effectiveness of

executive performance and remuneration policies. The three organisations that have selected

to fit the purpose of this report include AMP Limited, IAG Limited and QBE Insurance

Group. The remuneration systems for the three organisations have been evaluated as well to

assess the efficacy of the overall organisational performance. Finally, the report sheds light

on providing recommendations for improving the reporting along with widening the

performance measures of the organisation. It has been found that it could be stated that the

remuneration methods of AMP Limited are superior in contrast to the other two organisations

due to better financial performance in the Australian insurance industry.

2MEASURING PERFORMANCE AND MANAGEMENT CONTROL SYSTEMS

Table of Contents

1. Introduction:...........................................................................................................................3

2. Company reviews:..................................................................................................................3

2.1 Allocation of executive remuneration:.............................................................................3

2.2 Change in executive remuneration reporting:..................................................................9

2.3 Company performance versus executive pay:................................................................10

2.4 Mix of performance measures used:..............................................................................12

3. Comparison of remuneration systems:.................................................................................15

4. Summary of findings:...........................................................................................................16

5. Analysis of remuneration methods used:.............................................................................16

6. Recommendations:...............................................................................................................17

7. Conclusion:..........................................................................................................................18

References and Bibliographies:................................................................................................19

Table of Contents

1. Introduction:...........................................................................................................................3

2. Company reviews:..................................................................................................................3

2.1 Allocation of executive remuneration:.............................................................................3

2.2 Change in executive remuneration reporting:..................................................................9

2.3 Company performance versus executive pay:................................................................10

2.4 Mix of performance measures used:..............................................................................12

3. Comparison of remuneration systems:.................................................................................15

4. Summary of findings:...........................................................................................................16

5. Analysis of remuneration methods used:.............................................................................16

6. Recommendations:...............................................................................................................17

7. Conclusion:..........................................................................................................................18

References and Bibliographies:................................................................................................19

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3MEASURING PERFORMANCE AND MANAGEMENT CONTROL SYSTEMS

1. Introduction:

The current report aims to evaluate the performance and management control systems

of the three leading insurance companies in Australia in order to assess the effectiveness of

executive performance and remuneration policies. The three organisations that have selected

to fit the purpose of this report include AMP Limited, IAG Limited and QBE Insurance

Group. In this report, the company reviews have been evaluated in terms of executive

remuneration apportionment, changes in remuneration reporting, company performance in

contrast to executive payment and combination of performance measures used. The

remuneration systems for the three organisations have been evaluated as well to assess the

efficacy of the overall organisational performance. Finally, the report sheds light on

providing recommendations for improving the reporting along with widening the

performance measures of the organisation.

2. Company reviews:

2.1 Allocation of executive remuneration:

In order to determine the allocation of executive remuneration, it is necessary to

consider the fixed pay, short-term incentives and long-term incentives of the executive

directors (Arnaboldi, Lapsley and Steccolini, 2015).

AMP Limited:

1. Introduction:

The current report aims to evaluate the performance and management control systems

of the three leading insurance companies in Australia in order to assess the effectiveness of

executive performance and remuneration policies. The three organisations that have selected

to fit the purpose of this report include AMP Limited, IAG Limited and QBE Insurance

Group. In this report, the company reviews have been evaluated in terms of executive

remuneration apportionment, changes in remuneration reporting, company performance in

contrast to executive payment and combination of performance measures used. The

remuneration systems for the three organisations have been evaluated as well to assess the

efficacy of the overall organisational performance. Finally, the report sheds light on

providing recommendations for improving the reporting along with widening the

performance measures of the organisation.

2. Company reviews:

2.1 Allocation of executive remuneration:

In order to determine the allocation of executive remuneration, it is necessary to

consider the fixed pay, short-term incentives and long-term incentives of the executive

directors (Arnaboldi, Lapsley and Steccolini, 2015).

AMP Limited:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4MEASURING PERFORMANCE AND MANAGEMENT CONTROL SYSTEMS

Executive remuneration in 2016

Executive remuneration in 2014

Executive remuneration in 2015

Executive remuneration in 2013

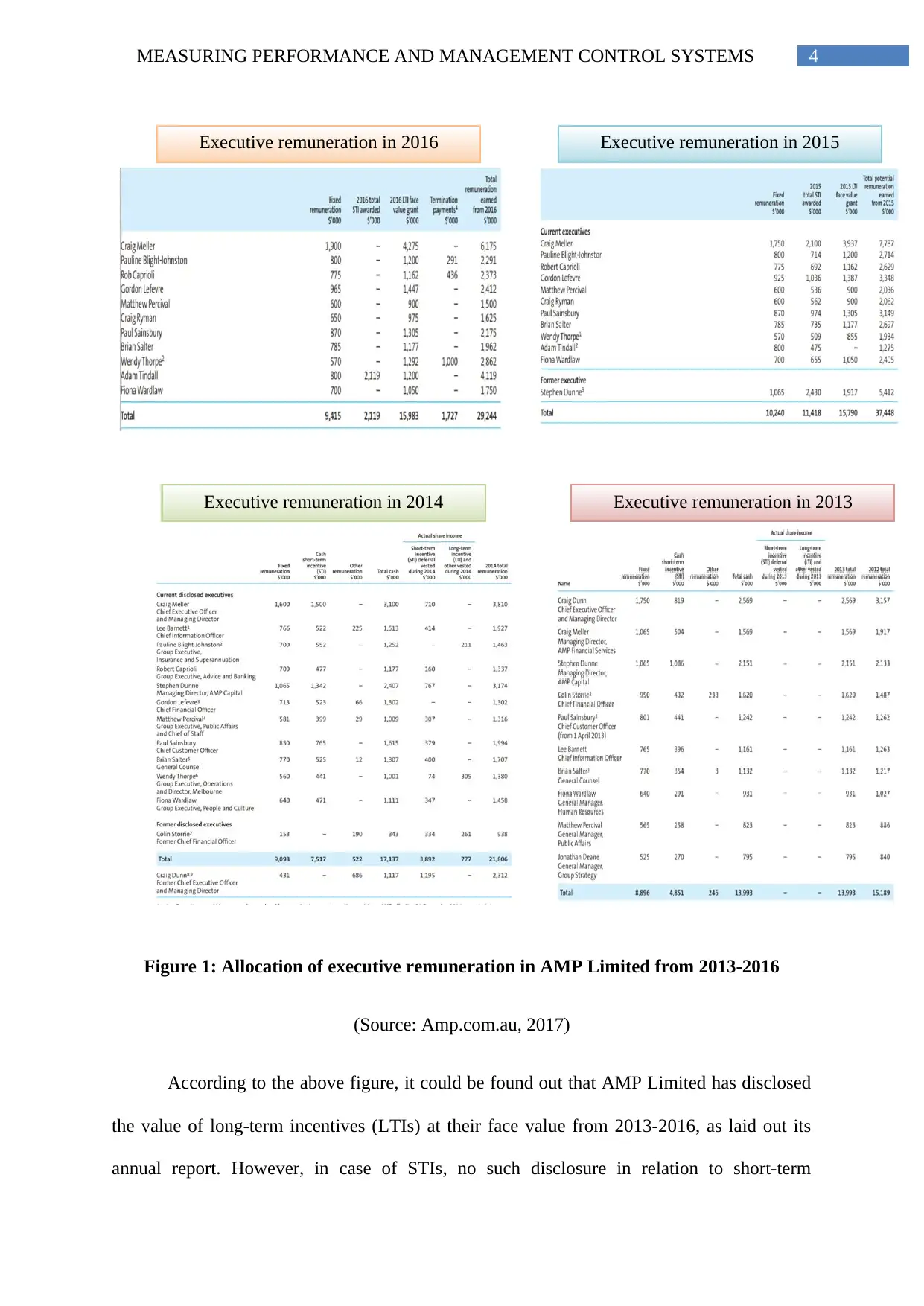

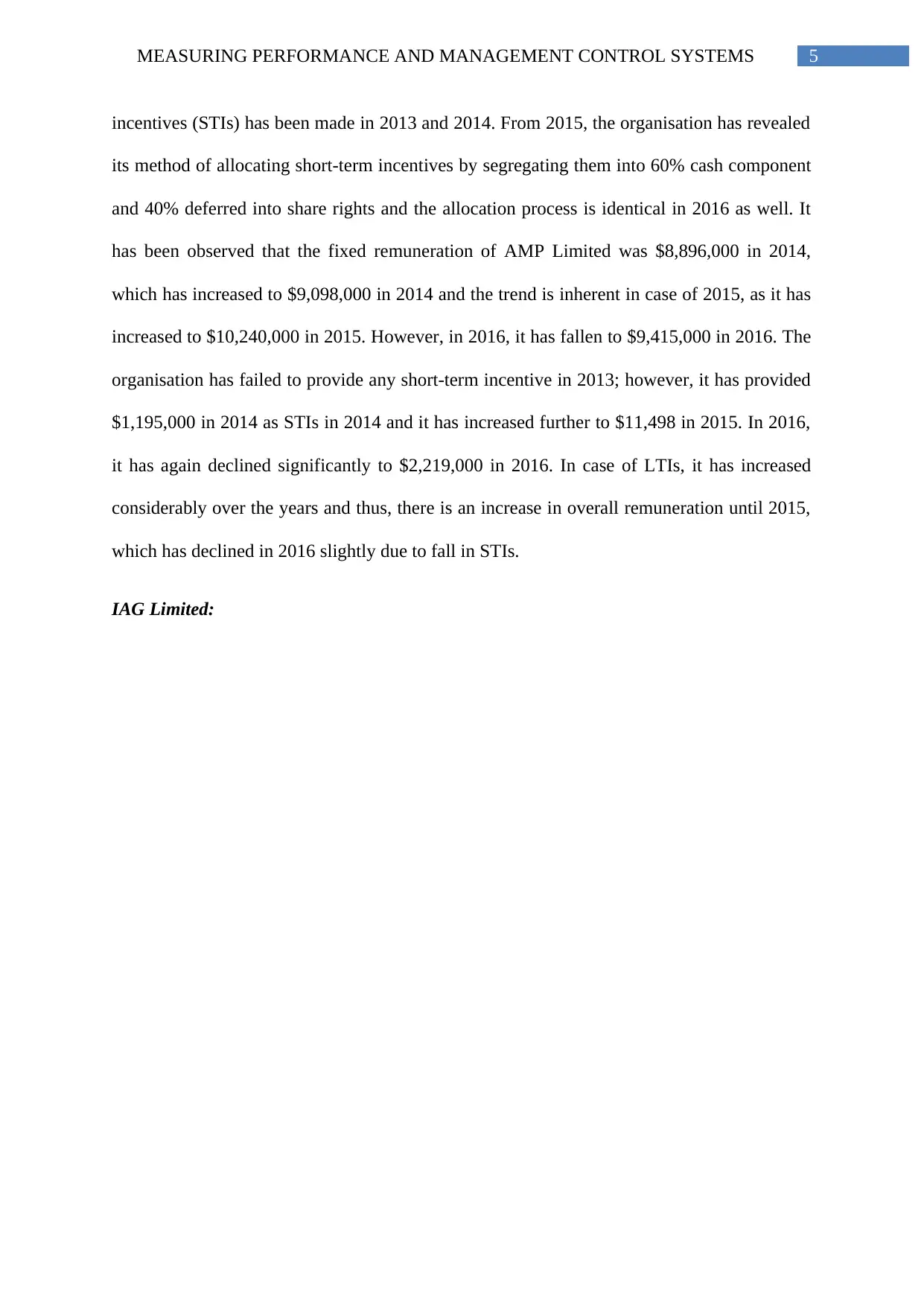

Figure 1: Allocation of executive remuneration in AMP Limited from 2013-2016

(Source: Amp.com.au, 2017)

According to the above figure, it could be found out that AMP Limited has disclosed

the value of long-term incentives (LTIs) at their face value from 2013-2016, as laid out its

annual report. However, in case of STIs, no such disclosure in relation to short-term

Executive remuneration in 2016

Executive remuneration in 2014

Executive remuneration in 2015

Executive remuneration in 2013

Figure 1: Allocation of executive remuneration in AMP Limited from 2013-2016

(Source: Amp.com.au, 2017)

According to the above figure, it could be found out that AMP Limited has disclosed

the value of long-term incentives (LTIs) at their face value from 2013-2016, as laid out its

annual report. However, in case of STIs, no such disclosure in relation to short-term

5MEASURING PERFORMANCE AND MANAGEMENT CONTROL SYSTEMS

incentives (STIs) has been made in 2013 and 2014. From 2015, the organisation has revealed

its method of allocating short-term incentives by segregating them into 60% cash component

and 40% deferred into share rights and the allocation process is identical in 2016 as well. It

has been observed that the fixed remuneration of AMP Limited was $8,896,000 in 2014,

which has increased to $9,098,000 in 2014 and the trend is inherent in case of 2015, as it has

increased to $10,240,000 in 2015. However, in 2016, it has fallen to $9,415,000 in 2016. The

organisation has failed to provide any short-term incentive in 2013; however, it has provided

$1,195,000 in 2014 as STIs in 2014 and it has increased further to $11,498 in 2015. In 2016,

it has again declined significantly to $2,219,000 in 2016. In case of LTIs, it has increased

considerably over the years and thus, there is an increase in overall remuneration until 2015,

which has declined in 2016 slightly due to fall in STIs.

IAG Limited:

incentives (STIs) has been made in 2013 and 2014. From 2015, the organisation has revealed

its method of allocating short-term incentives by segregating them into 60% cash component

and 40% deferred into share rights and the allocation process is identical in 2016 as well. It

has been observed that the fixed remuneration of AMP Limited was $8,896,000 in 2014,

which has increased to $9,098,000 in 2014 and the trend is inherent in case of 2015, as it has

increased to $10,240,000 in 2015. However, in 2016, it has fallen to $9,415,000 in 2016. The

organisation has failed to provide any short-term incentive in 2013; however, it has provided

$1,195,000 in 2014 as STIs in 2014 and it has increased further to $11,498 in 2015. In 2016,

it has again declined significantly to $2,219,000 in 2016. In case of LTIs, it has increased

considerably over the years and thus, there is an increase in overall remuneration until 2015,

which has declined in 2016 slightly due to fall in STIs.

IAG Limited:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6MEASURING PERFORMANCE AND MANAGEMENT CONTROL SYSTEMS

Executive remuneration in 2016

Executive remuneration in 2014

Executive remuneration in 2015

Executive remuneration in 2013

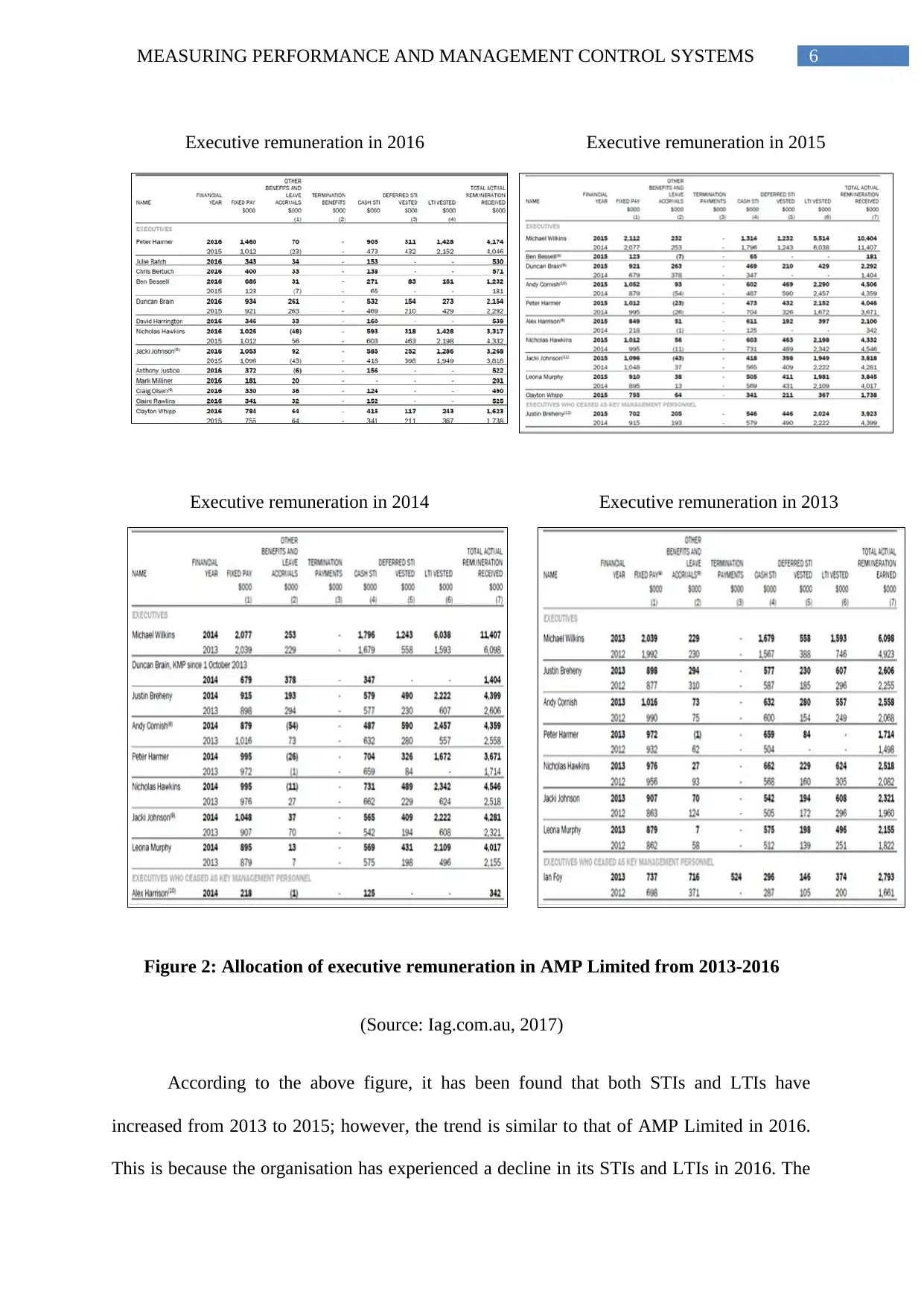

Figure 2: Allocation of executive remuneration in AMP Limited from 2013-2016

(Source: Iag.com.au, 2017)

According to the above figure, it has been found that both STIs and LTIs have

increased from 2013 to 2015; however, the trend is similar to that of AMP Limited in 2016.

This is because the organisation has experienced a decline in its STIs and LTIs in 2016. The

Executive remuneration in 2016

Executive remuneration in 2014

Executive remuneration in 2015

Executive remuneration in 2013

Figure 2: Allocation of executive remuneration in AMP Limited from 2013-2016

(Source: Iag.com.au, 2017)

According to the above figure, it has been found that both STIs and LTIs have

increased from 2013 to 2015; however, the trend is similar to that of AMP Limited in 2016.

This is because the organisation has experienced a decline in its STIs and LTIs in 2016. The

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7MEASURING PERFORMANCE AND MANAGEMENT CONTROL SYSTEMS

similar trend is observed in case of fixed remuneration as well and hence, there is a fall in

overall remuneration of the executives of AMP Limited in 2016, which has experienced a

steady increase from 2013 to 2015. Moreover, the allocation of STI has been made as 2/3rd of

cash STI and 1/3rd of deferred STI. The LTI has been allocated based on 95th percentile of the

peer group of the organisation.

QBE Insurance Group:

similar trend is observed in case of fixed remuneration as well and hence, there is a fall in

overall remuneration of the executives of AMP Limited in 2016, which has experienced a

steady increase from 2013 to 2015. Moreover, the allocation of STI has been made as 2/3rd of

cash STI and 1/3rd of deferred STI. The LTI has been allocated based on 95th percentile of the

peer group of the organisation.

QBE Insurance Group:

8MEASURING PERFORMANCE AND MANAGEMENT CONTROL SYSTEMS

Executive remuneration in 2016

Executive remuneration in 2014

Executive remuneration in 2015

Executive remuneration in 2013

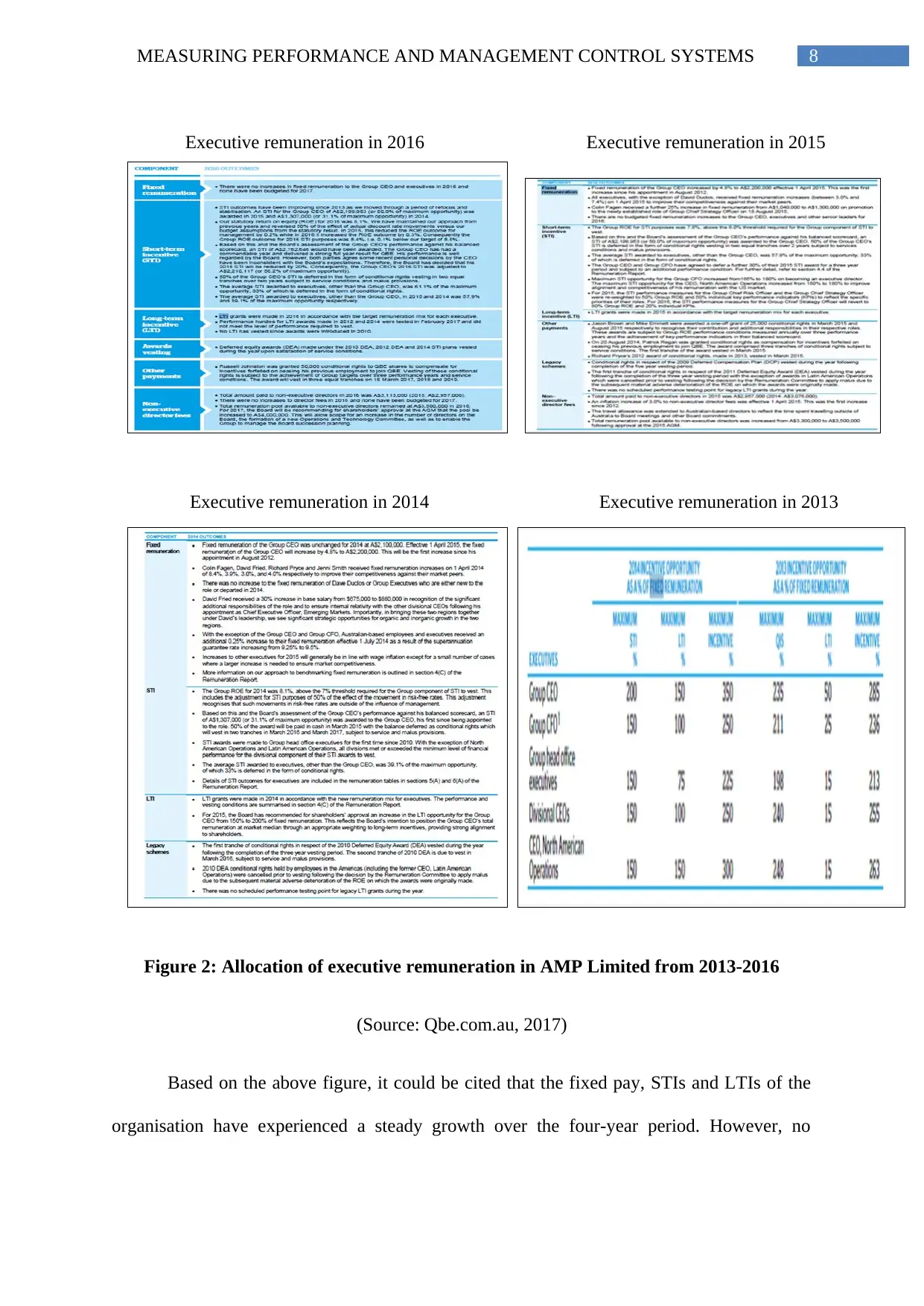

Figure 2: Allocation of executive remuneration in AMP Limited from 2013-2016

(Source: Qbe.com.au, 2017)

Based on the above figure, it could be cited that the fixed pay, STIs and LTIs of the

organisation have experienced a steady growth over the four-year period. However, no

Executive remuneration in 2016

Executive remuneration in 2014

Executive remuneration in 2015

Executive remuneration in 2013

Figure 2: Allocation of executive remuneration in AMP Limited from 2013-2016

(Source: Qbe.com.au, 2017)

Based on the above figure, it could be cited that the fixed pay, STIs and LTIs of the

organisation have experienced a steady growth over the four-year period. However, no

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9MEASURING PERFORMANCE AND MANAGEMENT CONTROL SYSTEMS

detailed breakdown regarding the allocation of STI has been depicted in the annual reports of

the organisation.

2.2 Change in executive remuneration reporting:

The changes in reporting of executive remuneration could be evaluated with the

above-stated figures for all the three selected organisations. This is because they help in

revealing whether the organisations have made additional disclosures or eliminated some

disclosures over the four-year period (Buckingham and Goodall, 2015).

AMP Limited:

In 2013 and 2014, the remuneration strategy of the organisation is to match

remuneration with the creation of shareholder value by retaining and attracting staffs to

contribute to its success. However, in 2015 and 2016, the organisation has developed some

additional strategies for reporting its executive remuneration. These include formation of a

risk management framework along with a governance framework that enables in handling

conflicts of interest, precise responsibilities and ensuring effective checks and balances in

place.

In 2013 and 2014, the organisation has disclosed other remuneration in its executive

remuneration payment, which has been removed from the same in the annual reports of 2015

and 2016. This might be due to the fact that either the organisation has not paid any other

remuneration to its executives during these years or it has manipulated its financial

statements in these years for company benefits (De Waal and Kourtit, 2013). Moreover,

termination payment has been made as an additional disclosure in the annual report of 2016,

as two of its directors are about to part ways with the organisation in 2017.

IAG Limited:

detailed breakdown regarding the allocation of STI has been depicted in the annual reports of

the organisation.

2.2 Change in executive remuneration reporting:

The changes in reporting of executive remuneration could be evaluated with the

above-stated figures for all the three selected organisations. This is because they help in

revealing whether the organisations have made additional disclosures or eliminated some

disclosures over the four-year period (Buckingham and Goodall, 2015).

AMP Limited:

In 2013 and 2014, the remuneration strategy of the organisation is to match

remuneration with the creation of shareholder value by retaining and attracting staffs to

contribute to its success. However, in 2015 and 2016, the organisation has developed some

additional strategies for reporting its executive remuneration. These include formation of a

risk management framework along with a governance framework that enables in handling

conflicts of interest, precise responsibilities and ensuring effective checks and balances in

place.

In 2013 and 2014, the organisation has disclosed other remuneration in its executive

remuneration payment, which has been removed from the same in the annual reports of 2015

and 2016. This might be due to the fact that either the organisation has not paid any other

remuneration to its executives during these years or it has manipulated its financial

statements in these years for company benefits (De Waal and Kourtit, 2013). Moreover,

termination payment has been made as an additional disclosure in the annual report of 2016,

as two of its directors are about to part ways with the organisation in 2017.

IAG Limited:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10MEASURING PERFORMANCE AND MANAGEMENT CONTROL SYSTEMS

The remuneration strategy of IAG Limited is developed in such a manner that the

executive remuneration is aligned with the interests of its stakeholders. In addition, it aims to

maintain market competitiveness and risk-taking behaviour to maintain long-term financial

soundness (Mone and London, 2014). In 2016, it has appointed remuneration consultants for

providing the remuneration benchmarking. The reporting policy has remained the same over

the years, as no additional disclosures have been made or any disclosures have been

eliminated.

QBE Insurance Group:

The remuneration strategy of the organisation is to match remuneration with the

creation of shareholder value by retaining and attracting staffs to contribute to its success. In

addition, the organisation has disclosed other remuneration in its executive remuneration

payment, which has been removed from the same in the annual reports of 2015 and 2016.

This might be due to the fact that either the organisation has not paid any other remuneration

to its executives during these years or it has manipulated its financial statements in these

years for company benefits (Rausch, Sheta and Ayesh, 2013).

2.3 Company performance versus executive pay:

The organisational performance in contrast to executive payment could be assessed

with the help of contrasting the change in company price per share and dividends per share

with the executive payments (De Waal, 2013).

AMP Limited:

According to the annual report of the organisation, it has been found that the dividend

per share of the organisation has increased from $0.23 in 2013 to $0.26 in 2014 and it has

increased further to $0.28 in 2015. The dividend per share of the organisation has remained

The remuneration strategy of IAG Limited is developed in such a manner that the

executive remuneration is aligned with the interests of its stakeholders. In addition, it aims to

maintain market competitiveness and risk-taking behaviour to maintain long-term financial

soundness (Mone and London, 2014). In 2016, it has appointed remuneration consultants for

providing the remuneration benchmarking. The reporting policy has remained the same over

the years, as no additional disclosures have been made or any disclosures have been

eliminated.

QBE Insurance Group:

The remuneration strategy of the organisation is to match remuneration with the

creation of shareholder value by retaining and attracting staffs to contribute to its success. In

addition, the organisation has disclosed other remuneration in its executive remuneration

payment, which has been removed from the same in the annual reports of 2015 and 2016.

This might be due to the fact that either the organisation has not paid any other remuneration

to its executives during these years or it has manipulated its financial statements in these

years for company benefits (Rausch, Sheta and Ayesh, 2013).

2.3 Company performance versus executive pay:

The organisational performance in contrast to executive payment could be assessed

with the help of contrasting the change in company price per share and dividends per share

with the executive payments (De Waal, 2013).

AMP Limited:

According to the annual report of the organisation, it has been found that the dividend

per share of the organisation has increased from $0.23 in 2013 to $0.26 in 2014 and it has

increased further to $0.28 in 2015. The dividend per share of the organisation has remained

11MEASURING PERFORMANCE AND MANAGEMENT CONTROL SYSTEMS

constant at $0.28 in 2016 as well compared to that of the previous year. In addition, the share

price of AMP Limited has increased from $4.39 in 2013 to $5.50 in 2014 and it has increased

further to $5.83 in 2015. The share price of the organisation; however, has fallen sharply to

$5.04 in 2016 possibly due to the declining net income and falling market demand (Gerrish,

2016).

From the information depicted in the annual report, it has been found that the STI

pool as a percentage of underlying profit has been 9.8% in 2013, which has increased to

11.3% in 2014. However, it has declined to 9.4% in 2015 and the decline is further inherent

to 7.1% in 2016. This denotes that despite the increase in profit margin in 2015, the

organisation has reduced its executive payments in relation to STIs and LTIs for maximising

its base of retained earnings (Hatry, 2013).

IAG Limited:

As observed from the annual report of the organisation, the dividend per share has

increased from $0.36 in 2013 to $0.39 in 2014; however, it has fallen to $0.29 in 2015. In

2016, it has risen sharply to $0.36 despite the fall in overall profit margin. This denotes that

the organisation has focused on providing greater dividends to the shareholders in 2016

despite increased profit level in 2015. The share price of the organisation has increased

sharply from $5.44 in 2013 to $5.84 in 2014. However, it has fallen considerably to $5.58 in

2015 and the decline is further evident in 2016 to $5.45.

In accordance with the executive payments of the organisation, there is an increase in

their payments, as the profit margin has increased from 2013 to 2015. However, it has fallen

significantly in 2016 with the fall in net income despite the increase for dividends distributed.

Moreover, IAG Limited has not disclosed the STI pool as a percentage of underlying profits

in 2016 in its annual reports.

constant at $0.28 in 2016 as well compared to that of the previous year. In addition, the share

price of AMP Limited has increased from $4.39 in 2013 to $5.50 in 2014 and it has increased

further to $5.83 in 2015. The share price of the organisation; however, has fallen sharply to

$5.04 in 2016 possibly due to the declining net income and falling market demand (Gerrish,

2016).

From the information depicted in the annual report, it has been found that the STI

pool as a percentage of underlying profit has been 9.8% in 2013, which has increased to

11.3% in 2014. However, it has declined to 9.4% in 2015 and the decline is further inherent

to 7.1% in 2016. This denotes that despite the increase in profit margin in 2015, the

organisation has reduced its executive payments in relation to STIs and LTIs for maximising

its base of retained earnings (Hatry, 2013).

IAG Limited:

As observed from the annual report of the organisation, the dividend per share has

increased from $0.36 in 2013 to $0.39 in 2014; however, it has fallen to $0.29 in 2015. In

2016, it has risen sharply to $0.36 despite the fall in overall profit margin. This denotes that

the organisation has focused on providing greater dividends to the shareholders in 2016

despite increased profit level in 2015. The share price of the organisation has increased

sharply from $5.44 in 2013 to $5.84 in 2014. However, it has fallen considerably to $5.58 in

2015 and the decline is further evident in 2016 to $5.45.

In accordance with the executive payments of the organisation, there is an increase in

their payments, as the profit margin has increased from 2013 to 2015. However, it has fallen

significantly in 2016 with the fall in net income despite the increase for dividends distributed.

Moreover, IAG Limited has not disclosed the STI pool as a percentage of underlying profits

in 2016 in its annual reports.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.