University Finance: Management and Cost Accounting Exam Solution

VerifiedAdded on 2023/01/03

|17

|2620

|100

Homework Assignment

AI Summary

This document provides a comprehensive solution to an online exam in Management and Cost Accounting. The solution covers various topics, including activity-based costing (ABC) with calculations of activity rates, overhead allocation, and unit manufacturing costs. It also includes variance analysis for direct materials and labor, examining price and efficiency variances, and explores the impact of discounts on profitability. The solution further addresses break-even analysis, calculating the number of units needed to achieve a target after-tax profit and the required revenue. Finally, it presents a debtor schedule and a cash budget, analyzing cash inflows and outflows to assess the feasibility of a new project. The document includes detailed calculations, explanations, and journal entries where applicable, providing a thorough understanding of the concepts discussed.

Online Exam (Management and Cost Accounting)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

Main body...................................................................................................................................................3

Question 1...............................................................................................................................................3

Question 2...............................................................................................................................................8

Question 3...............................................................................................................................................9

Question 4.............................................................................................................................................11

Question 5.............................................................................................................................................13

REFERENCES..........................................................................................................................................17

Main body...................................................................................................................................................3

Question 1...............................................................................................................................................3

Question 2...............................................................................................................................................8

Question 3...............................................................................................................................................9

Question 4.............................................................................................................................................11

Question 5.............................................................................................................................................13

REFERENCES..........................................................................................................................................17

Main body

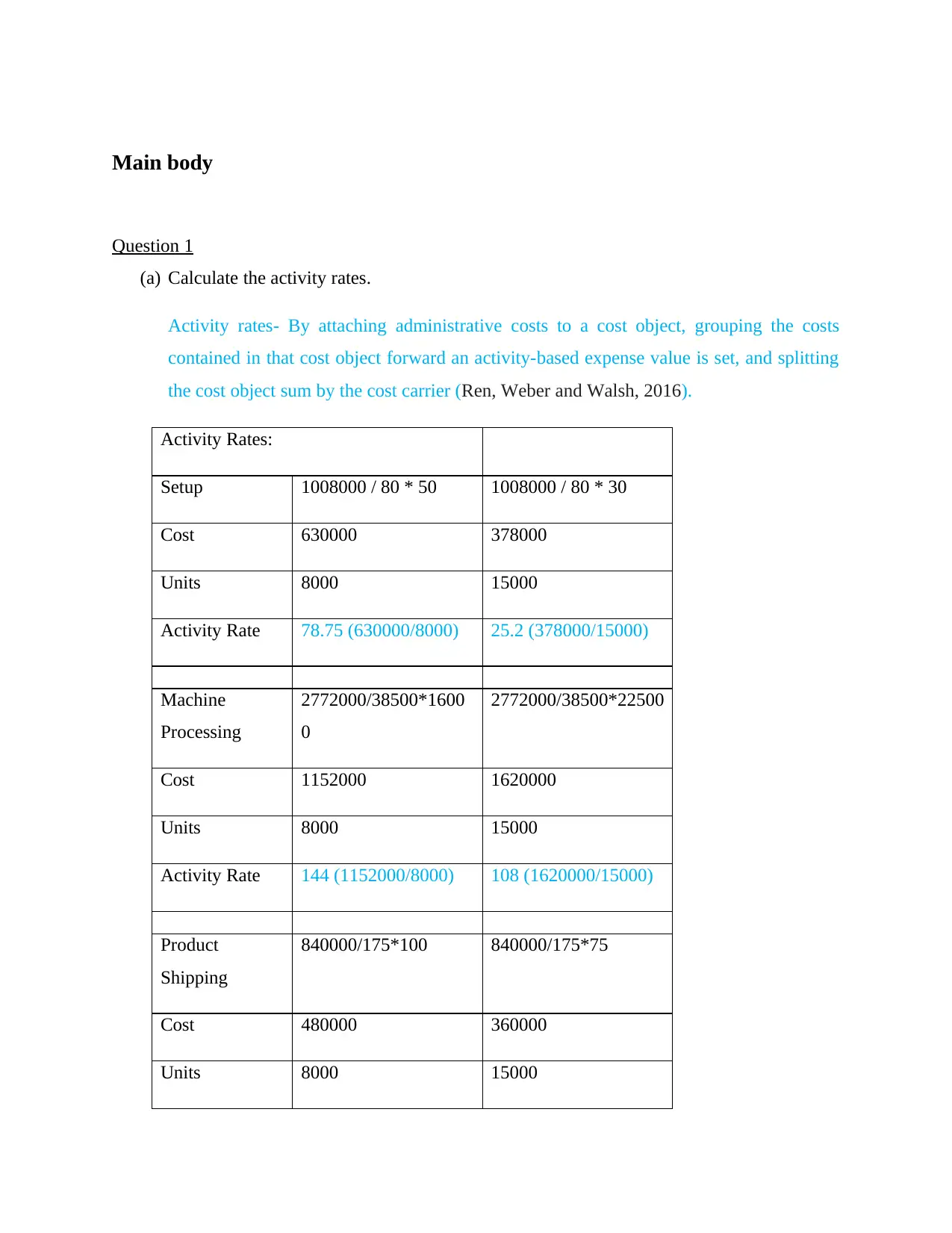

Question 1

(a) Calculate the activity rates.

Activity rates- By attaching administrative costs to a cost object, grouping the costs

contained in that cost object forward an activity-based expense value is set, and splitting

the cost object sum by the cost carrier (Ren, Weber and Walsh, 2016).

Activity Rates:

Setup 1008000 / 80 * 50 1008000 / 80 * 30

Cost 630000 378000

Units 8000 15000

Activity Rate 78.75 (630000/8000) 25.2 (378000/15000)

Machine

Processing

2772000/38500*1600

0

2772000/38500*22500

Cost 1152000 1620000

Units 8000 15000

Activity Rate 144 (1152000/8000) 108 (1620000/15000)

Product

Shipping

840000/175*100 840000/175*75

Cost 480000 360000

Units 8000 15000

Question 1

(a) Calculate the activity rates.

Activity rates- By attaching administrative costs to a cost object, grouping the costs

contained in that cost object forward an activity-based expense value is set, and splitting

the cost object sum by the cost carrier (Ren, Weber and Walsh, 2016).

Activity Rates:

Setup 1008000 / 80 * 50 1008000 / 80 * 30

Cost 630000 378000

Units 8000 15000

Activity Rate 78.75 (630000/8000) 25.2 (378000/15000)

Machine

Processing

2772000/38500*1600

0

2772000/38500*22500

Cost 1152000 1620000

Units 8000 15000

Activity Rate 144 (1152000/8000) 108 (1620000/15000)

Product

Shipping

840000/175*100 840000/175*75

Cost 480000 360000

Units 8000 15000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Activity Rate 60 (480000/8000) 24 (360000/15000)

(b) Calculate the total overhead costs allocated:

Deluxe Executive

Direct material cost 52.5 90

Direct labor cost 30 30

Total cost 82.5

(52.5+30)

120

(90+30)

Budgeted volume (units) 8000 15000

Total costs 660000

(8000*82.5)

1800000

(15000*120)

Ratio 0.27 0.73

Total Setup overhead costs

apportioned

270439 737561

Setups 50 30

Rate per setup activity 5408.78

(270439/50)

24585.37

(737561/30)

Machine Processing costs

apportioned

743707.3 2028293

Machine Hours 16000 22500

(b) Calculate the total overhead costs allocated:

Deluxe Executive

Direct material cost 52.5 90

Direct labor cost 30 30

Total cost 82.5

(52.5+30)

120

(90+30)

Budgeted volume (units) 8000 15000

Total costs 660000

(8000*82.5)

1800000

(15000*120)

Ratio 0.27 0.73

Total Setup overhead costs

apportioned

270439 737561

Setups 50 30

Rate per setup activity 5408.78

(270439/50)

24585.37

(737561/30)

Machine Processing costs

apportioned

743707.3 2028293

Machine Hours 16000 22500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

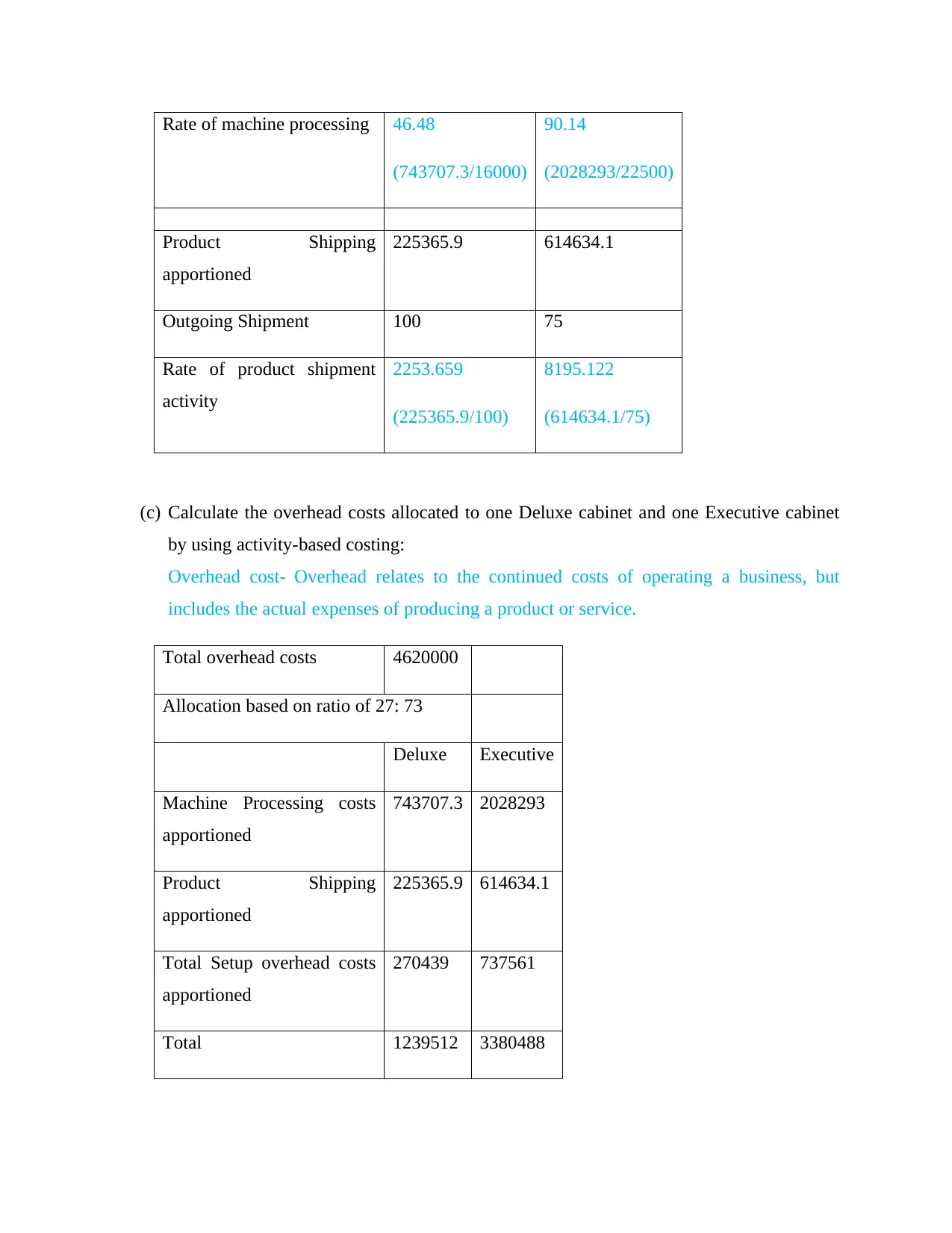

Rate of machine processing 46.48

(743707.3/16000)

90.14

(2028293/22500)

Product Shipping

apportioned

225365.9 614634.1

Outgoing Shipment 100 75

Rate of product shipment

activity

2253.659

(225365.9/100)

8195.122

(614634.1/75)

(c) Calculate the overhead costs allocated to one Deluxe cabinet and one Executive cabinet

by using activity-based costing:

Overhead cost- Overhead relates to the continued costs of operating a business, but

includes the actual expenses of producing a product or service.

Total overhead costs 4620000

Allocation based on ratio of 27: 73

Deluxe Executive

Machine Processing costs

apportioned

743707.3 2028293

Product Shipping

apportioned

225365.9 614634.1

Total Setup overhead costs

apportioned

270439 737561

Total 1239512 3380488

(743707.3/16000)

90.14

(2028293/22500)

Product Shipping

apportioned

225365.9 614634.1

Outgoing Shipment 100 75

Rate of product shipment

activity

2253.659

(225365.9/100)

8195.122

(614634.1/75)

(c) Calculate the overhead costs allocated to one Deluxe cabinet and one Executive cabinet

by using activity-based costing:

Overhead cost- Overhead relates to the continued costs of operating a business, but

includes the actual expenses of producing a product or service.

Total overhead costs 4620000

Allocation based on ratio of 27: 73

Deluxe Executive

Machine Processing costs

apportioned

743707.3 2028293

Product Shipping

apportioned

225365.9 614634.1

Total Setup overhead costs

apportioned

270439 737561

Total 1239512 3380488

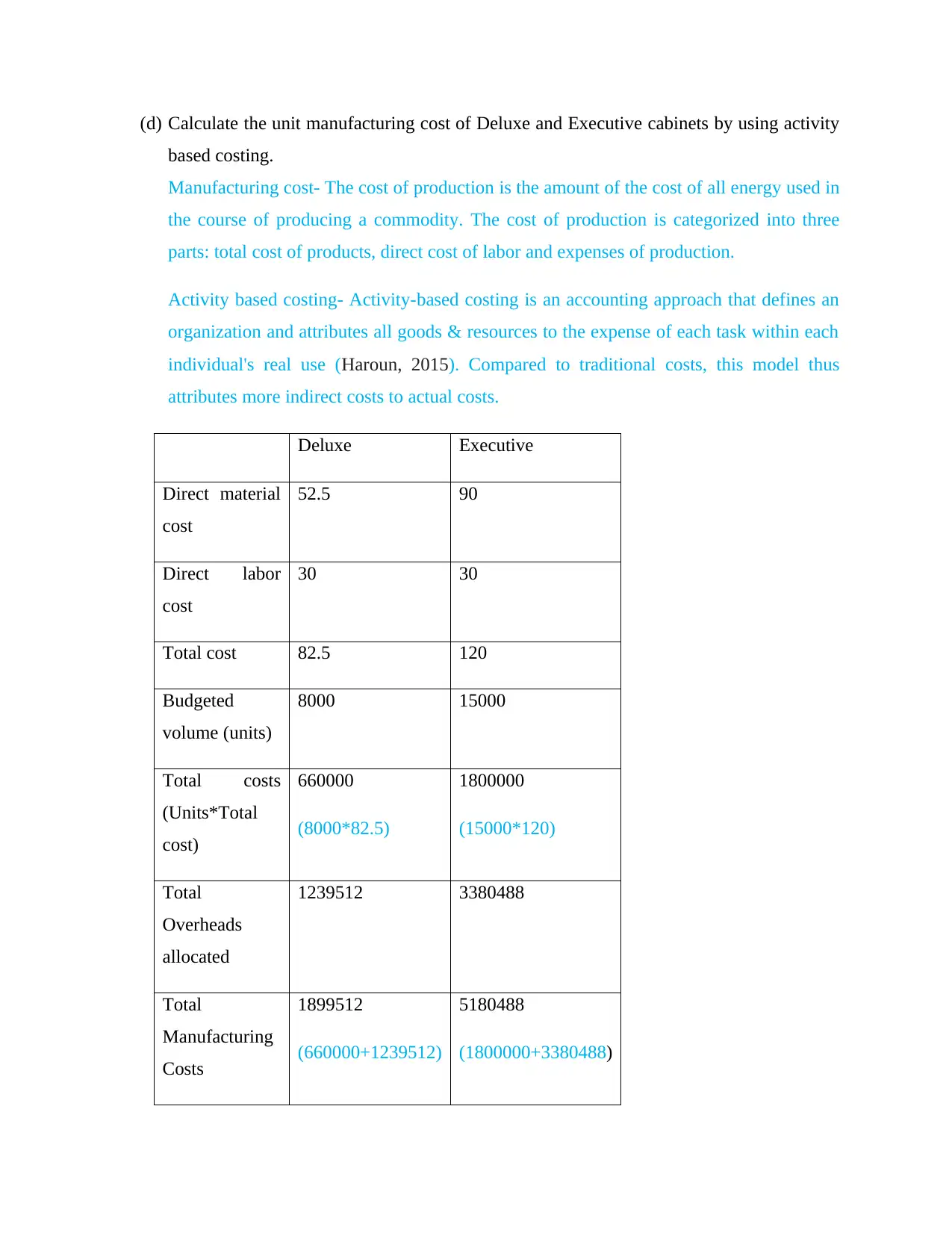

(d) Calculate the unit manufacturing cost of Deluxe and Executive cabinets by using activity

based costing.

Manufacturing cost- The cost of production is the amount of the cost of all energy used in

the course of producing a commodity. The cost of production is categorized into three

parts: total cost of products, direct cost of labor and expenses of production.

Activity based costing- Activity-based costing is an accounting approach that defines an

organization and attributes all goods & resources to the expense of each task within each

individual's real use (Haroun, 2015). Compared to traditional costs, this model thus

attributes more indirect costs to actual costs.

Deluxe Executive

Direct material

cost

52.5 90

Direct labor

cost

30 30

Total cost 82.5 120

Budgeted

volume (units)

8000 15000

Total costs

(Units*Total

cost)

660000

(8000*82.5)

1800000

(15000*120)

Total

Overheads

allocated

1239512 3380488

Total

Manufacturing

Costs

1899512

(660000+1239512)

5180488

(1800000+3380488)

based costing.

Manufacturing cost- The cost of production is the amount of the cost of all energy used in

the course of producing a commodity. The cost of production is categorized into three

parts: total cost of products, direct cost of labor and expenses of production.

Activity based costing- Activity-based costing is an accounting approach that defines an

organization and attributes all goods & resources to the expense of each task within each

individual's real use (Haroun, 2015). Compared to traditional costs, this model thus

attributes more indirect costs to actual costs.

Deluxe Executive

Direct material

cost

52.5 90

Direct labor

cost

30 30

Total cost 82.5 120

Budgeted

volume (units)

8000 15000

Total costs

(Units*Total

cost)

660000

(8000*82.5)

1800000

(15000*120)

Total

Overheads

allocated

1239512 3380488

Total

Manufacturing

Costs

1899512

(660000+1239512)

5180488

(1800000+3380488)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

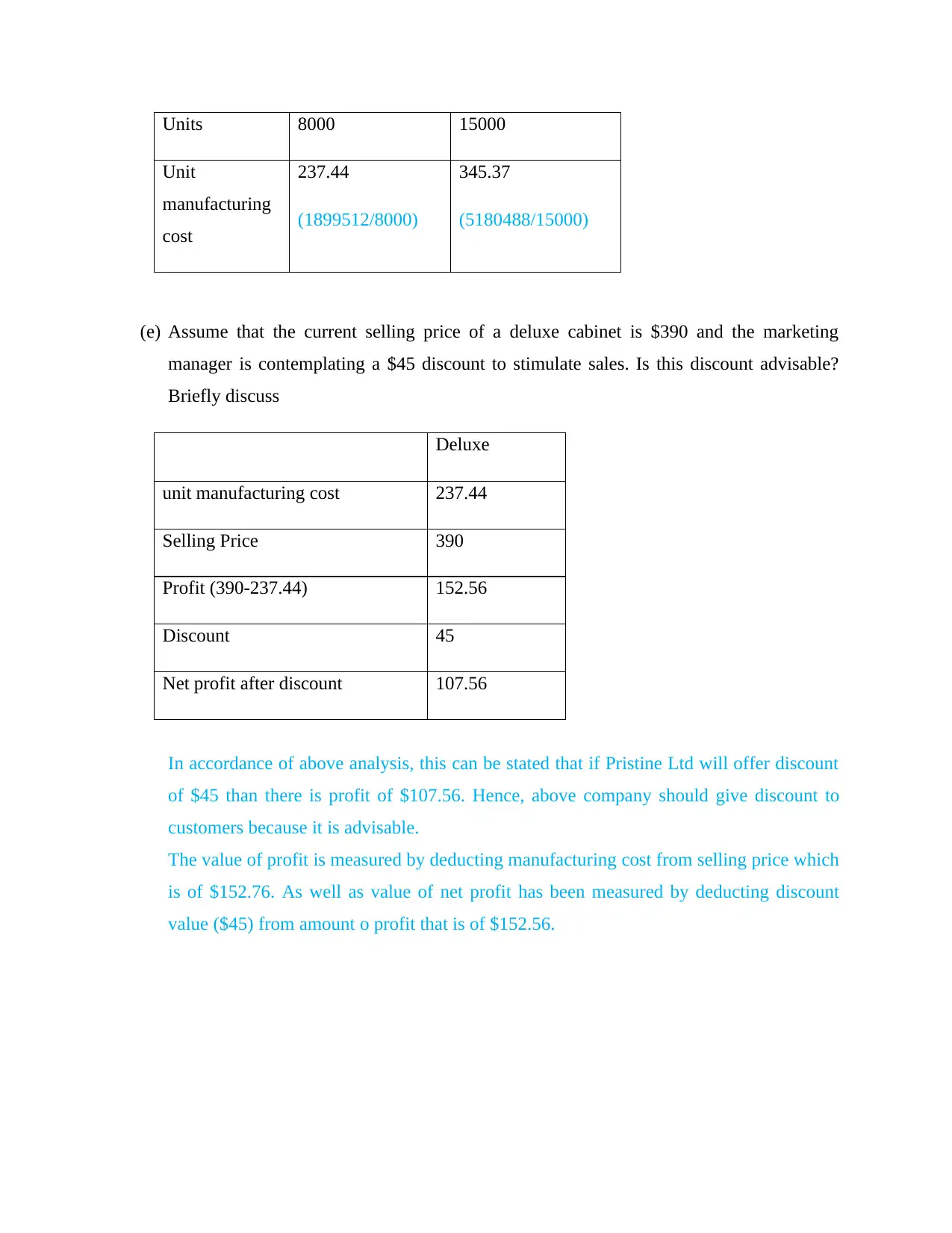

Units 8000 15000

Unit

manufacturing

cost

237.44

(1899512/8000)

345.37

(5180488/15000)

(e) Assume that the current selling price of a deluxe cabinet is $390 and the marketing

manager is contemplating a $45 discount to stimulate sales. Is this discount advisable?

Briefly discuss

Deluxe

unit manufacturing cost 237.44

Selling Price 390

Profit (390-237.44) 152.56

Discount 45

Net profit after discount 107.56

In accordance of above analysis, this can be stated that if Pristine Ltd will offer discount

of $45 than there is profit of $107.56. Hence, above company should give discount to

customers because it is advisable.

The value of profit is measured by deducting manufacturing cost from selling price which

is of $152.76. As well as value of net profit has been measured by deducting discount

value ($45) from amount o profit that is of $152.56.

Unit

manufacturing

cost

237.44

(1899512/8000)

345.37

(5180488/15000)

(e) Assume that the current selling price of a deluxe cabinet is $390 and the marketing

manager is contemplating a $45 discount to stimulate sales. Is this discount advisable?

Briefly discuss

Deluxe

unit manufacturing cost 237.44

Selling Price 390

Profit (390-237.44) 152.56

Discount 45

Net profit after discount 107.56

In accordance of above analysis, this can be stated that if Pristine Ltd will offer discount

of $45 than there is profit of $107.56. Hence, above company should give discount to

customers because it is advisable.

The value of profit is measured by deducting manufacturing cost from selling price which

is of $152.76. As well as value of net profit has been measured by deducting discount

value ($45) from amount o profit that is of $152.56.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

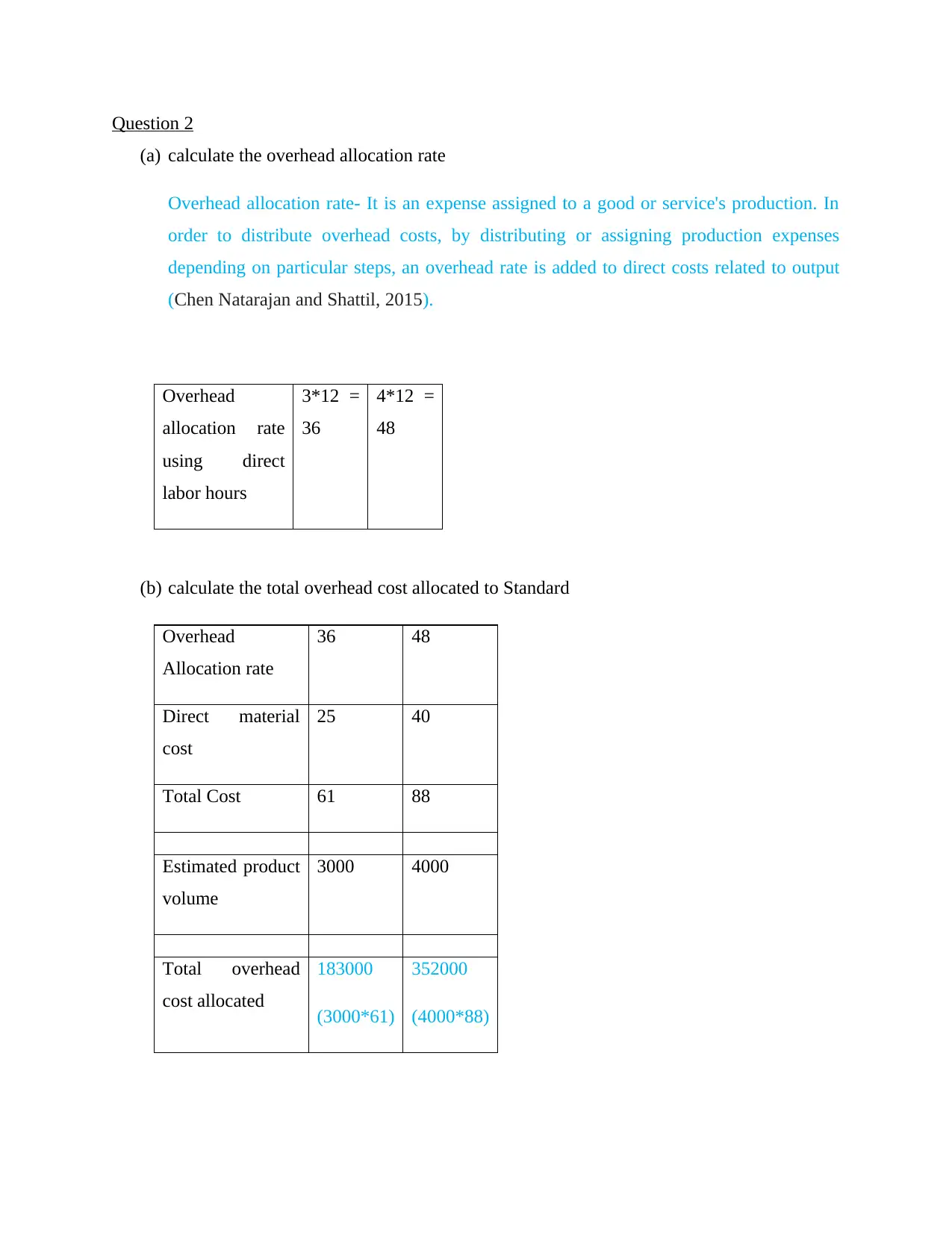

Question 2

(a) calculate the overhead allocation rate

Overhead allocation rate- It is an expense assigned to a good or service's production. In

order to distribute overhead costs, by distributing or assigning production expenses

depending on particular steps, an overhead rate is added to direct costs related to output

(Chen Natarajan and Shattil, 2015).

Overhead

allocation rate

using direct

labor hours

3*12 =

36

4*12 =

48

(b) calculate the total overhead cost allocated to Standard

Overhead

Allocation rate

36 48

Direct material

cost

25 40

Total Cost 61 88

Estimated product

volume

3000 4000

Total overhead

cost allocated

183000

(3000*61)

352000

(4000*88)

(a) calculate the overhead allocation rate

Overhead allocation rate- It is an expense assigned to a good or service's production. In

order to distribute overhead costs, by distributing or assigning production expenses

depending on particular steps, an overhead rate is added to direct costs related to output

(Chen Natarajan and Shattil, 2015).

Overhead

allocation rate

using direct

labor hours

3*12 =

36

4*12 =

48

(b) calculate the total overhead cost allocated to Standard

Overhead

Allocation rate

36 48

Direct material

cost

25 40

Total Cost 61 88

Estimated product

volume

3000 4000

Total overhead

cost allocated

183000

(3000*61)

352000

(4000*88)

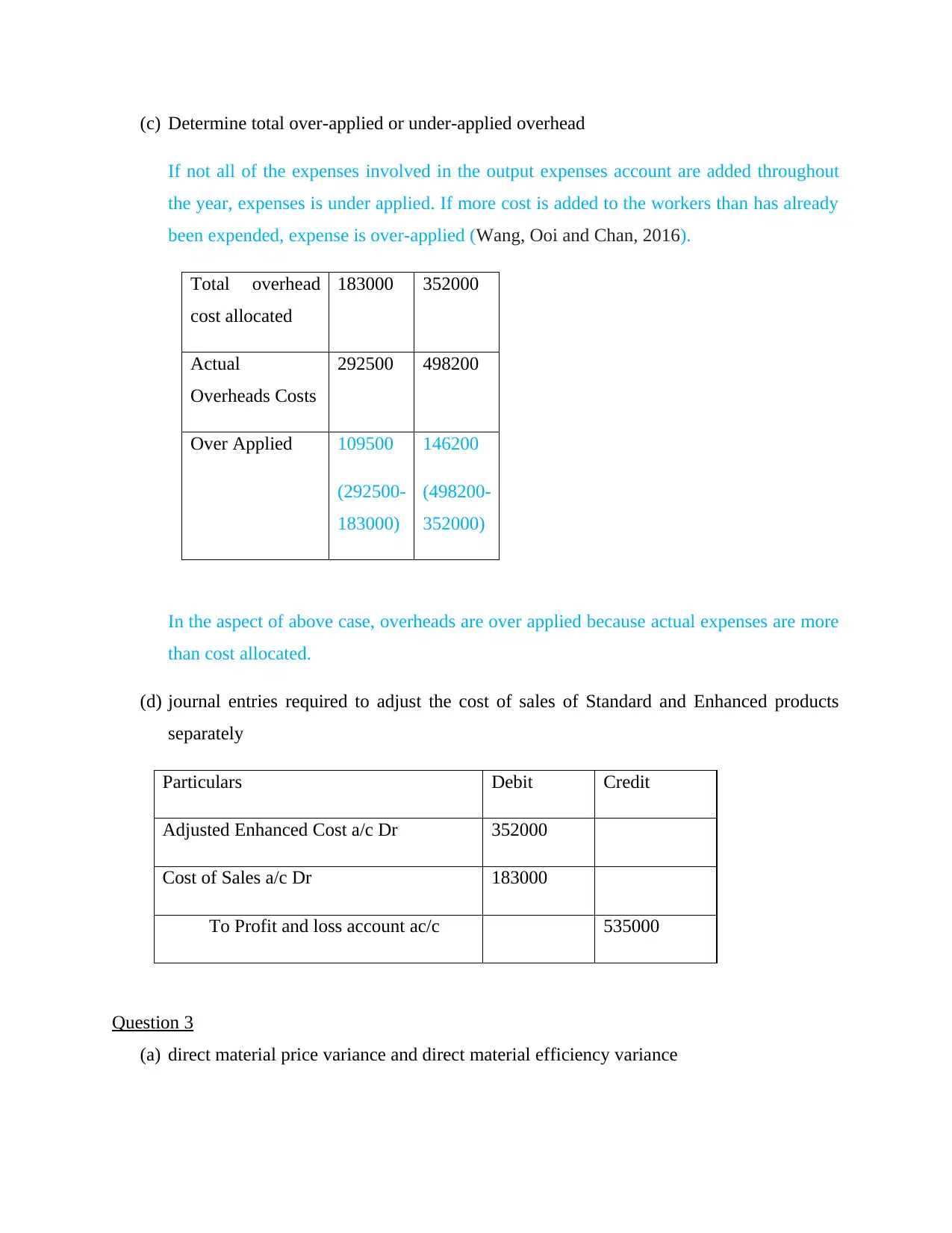

(c) Determine total over-applied or under-applied overhead

If not all of the expenses involved in the output expenses account are added throughout

the year, expenses is under applied. If more cost is added to the workers than has already

been expended, expense is over-applied (Wang, Ooi and Chan, 2016).

Total overhead

cost allocated

183000 352000

Actual

Overheads Costs

292500 498200

Over Applied 109500

(292500-

183000)

146200

(498200-

352000)

In the aspect of above case, overheads are over applied because actual expenses are more

than cost allocated.

(d) journal entries required to adjust the cost of sales of Standard and Enhanced products

separately

Particulars Debit Credit

Adjusted Enhanced Cost a/c Dr 352000

Cost of Sales a/c Dr 183000

To Profit and loss account ac/c 535000

Question 3

(a) direct material price variance and direct material efficiency variance

If not all of the expenses involved in the output expenses account are added throughout

the year, expenses is under applied. If more cost is added to the workers than has already

been expended, expense is over-applied (Wang, Ooi and Chan, 2016).

Total overhead

cost allocated

183000 352000

Actual

Overheads Costs

292500 498200

Over Applied 109500

(292500-

183000)

146200

(498200-

352000)

In the aspect of above case, overheads are over applied because actual expenses are more

than cost allocated.

(d) journal entries required to adjust the cost of sales of Standard and Enhanced products

separately

Particulars Debit Credit

Adjusted Enhanced Cost a/c Dr 352000

Cost of Sales a/c Dr 183000

To Profit and loss account ac/c 535000

Question 3

(a) direct material price variance and direct material efficiency variance

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Direct material price variance: It varies between the surplus cash expended on direct sales

of merchandise over a specific time and the sum expended if the product had been bought

at the normal price (Filipović, Gourier and Mancini, 2016).

Actual quantity of material purchased at actual price- Actual quantity of material

purchased at budgeted price

= 240000*0.62-240000*0.60

= 148800-144000

=$ 4800 Favorable

Direct material efficiency variance: In the measurement of variance, the discrepancy

between the typical amount of products that can then be used for the amount of units

currently manufactured versus the real amount of products used, priced at the average

unit cost of product, is the direct expenses utilization (effectiveness, volume) variance.

(Actual quantity – standard quantity)*Standard cost

= (210000-4)*0.60

= 125,997.6 Favorable

(b) Direct labor rate variance and direct labor efficiency variance:

Direct labor rate variance: Unless the wage paid is more than much less than the regular

rate is calculated by the direct labor rate difference. The direct difference in labor time

defines if the real hours utilized are more than which is less than the criteria that would

otherwise be used.

Actual hour (Actual rate-Standard rate)

= 13000(23-22)

= 13000 Favorable

Labor efficiency variance: The discrepancy in labor productivity is the change in the total

amount of direct working hours employed and the expected direct working hours that

could have been performed on the basis of expectations (Yao, 2015).

Actual hours*Standard rate-Standard hour*standard rate

of merchandise over a specific time and the sum expended if the product had been bought

at the normal price (Filipović, Gourier and Mancini, 2016).

Actual quantity of material purchased at actual price- Actual quantity of material

purchased at budgeted price

= 240000*0.62-240000*0.60

= 148800-144000

=$ 4800 Favorable

Direct material efficiency variance: In the measurement of variance, the discrepancy

between the typical amount of products that can then be used for the amount of units

currently manufactured versus the real amount of products used, priced at the average

unit cost of product, is the direct expenses utilization (effectiveness, volume) variance.

(Actual quantity – standard quantity)*Standard cost

= (210000-4)*0.60

= 125,997.6 Favorable

(b) Direct labor rate variance and direct labor efficiency variance:

Direct labor rate variance: Unless the wage paid is more than much less than the regular

rate is calculated by the direct labor rate difference. The direct difference in labor time

defines if the real hours utilized are more than which is less than the criteria that would

otherwise be used.

Actual hour (Actual rate-Standard rate)

= 13000(23-22)

= 13000 Favorable

Labor efficiency variance: The discrepancy in labor productivity is the change in the total

amount of direct working hours employed and the expected direct working hours that

could have been performed on the basis of expectations (Yao, 2015).

Actual hours*Standard rate-Standard hour*standard rate

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

= 13000*22-0.25*22

= 286000-5.5

= 285,994.5 Favorable

(c) Reasons for variation in material use include the procurement of effective quality goods

than the norm (this will be reflected in a favorable material price variance). Application

of unskilled labor. Boost of material wastage due to machinery and equipment depletion.

(d) Reason for variance:

Recruitment of more skilled labor than required in the Norm.

Inefficient recruitment by the department of HR.

Successful negotiations by trade unions

Question 4

(a) Total number of units that must be sold to achieve the targeted after-tax profit of $100

000:

Step one: In order to find out number of units to achieve targeted profit of 100000, first

we need to find out exact value of desired profit that is as follows:

Desired profit: It is defined as a form of profit which a company wants to achieve from

selling of different units or services (Baral, 2016). In relation to above aspect, calculation

of desired profit is done below:

= $100000*100/70

= $142,857.14

Step two: After measuring desired profit, next part is to find out contribution per unit

which is computed in combined manner for different products.

= 286000-5.5

= 285,994.5 Favorable

(c) Reasons for variation in material use include the procurement of effective quality goods

than the norm (this will be reflected in a favorable material price variance). Application

of unskilled labor. Boost of material wastage due to machinery and equipment depletion.

(d) Reason for variance:

Recruitment of more skilled labor than required in the Norm.

Inefficient recruitment by the department of HR.

Successful negotiations by trade unions

Question 4

(a) Total number of units that must be sold to achieve the targeted after-tax profit of $100

000:

Step one: In order to find out number of units to achieve targeted profit of 100000, first

we need to find out exact value of desired profit that is as follows:

Desired profit: It is defined as a form of profit which a company wants to achieve from

selling of different units or services (Baral, 2016). In relation to above aspect, calculation

of desired profit is done below:

= $100000*100/70

= $142,857.14

Step two: After measuring desired profit, next part is to find out contribution per unit

which is computed in combined manner for different products.

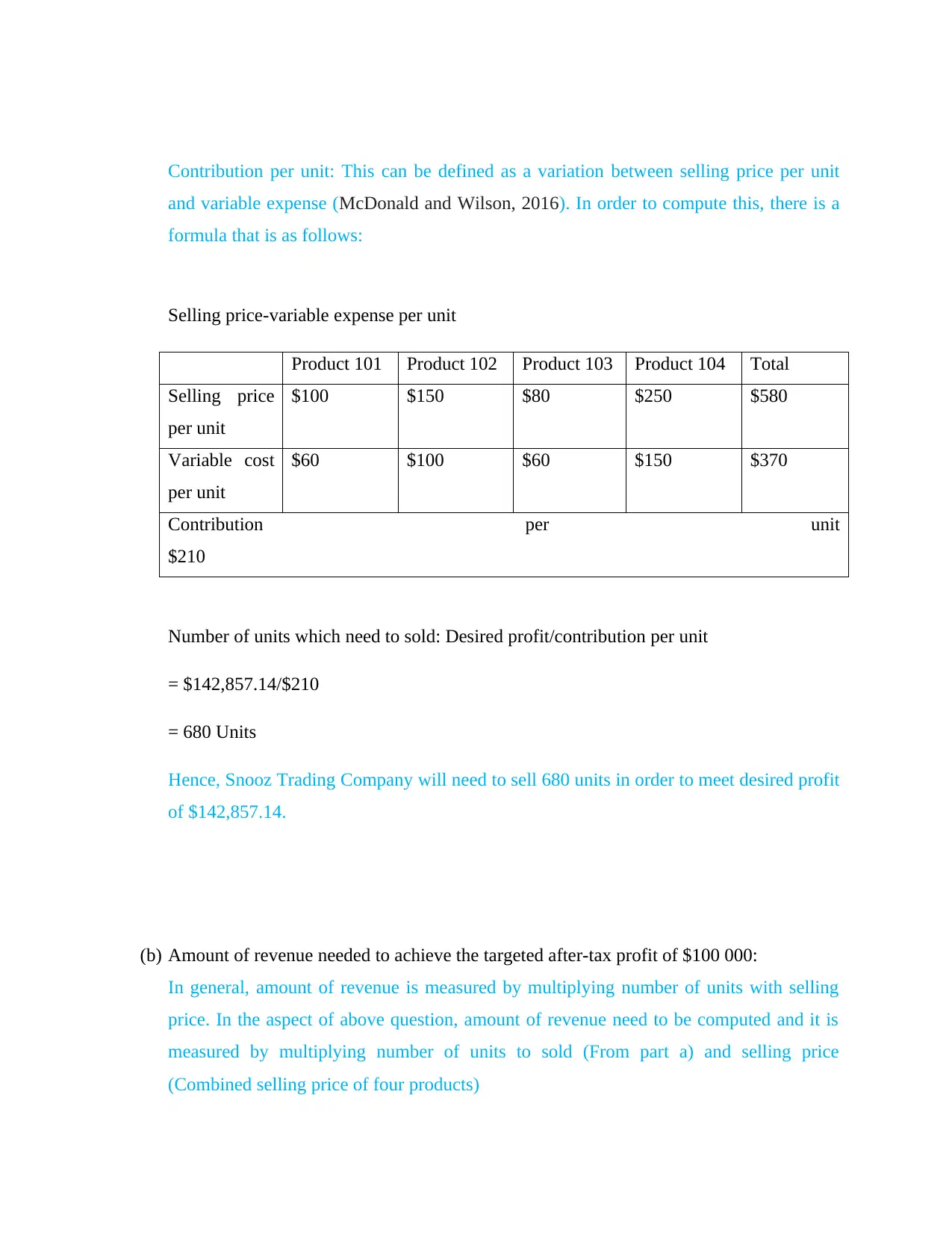

Contribution per unit: This can be defined as a variation between selling price per unit

and variable expense (McDonald and Wilson, 2016). In order to compute this, there is a

formula that is as follows:

Selling price-variable expense per unit

Product 101 Product 102 Product 103 Product 104 Total

Selling price

per unit

$100 $150 $80 $250 $580

Variable cost

per unit

$60 $100 $60 $150 $370

Contribution per unit

$210

Number of units which need to sold: Desired profit/contribution per unit

= $142,857.14/$210

= 680 Units

Hence, Snooz Trading Company will need to sell 680 units in order to meet desired profit

of $142,857.14.

(b) Amount of revenue needed to achieve the targeted after-tax profit of $100 000:

In general, amount of revenue is measured by multiplying number of units with selling

price. In the aspect of above question, amount of revenue need to be computed and it is

measured by multiplying number of units to sold (From part a) and selling price

(Combined selling price of four products)

and variable expense (McDonald and Wilson, 2016). In order to compute this, there is a

formula that is as follows:

Selling price-variable expense per unit

Product 101 Product 102 Product 103 Product 104 Total

Selling price

per unit

$100 $150 $80 $250 $580

Variable cost

per unit

$60 $100 $60 $150 $370

Contribution per unit

$210

Number of units which need to sold: Desired profit/contribution per unit

= $142,857.14/$210

= 680 Units

Hence, Snooz Trading Company will need to sell 680 units in order to meet desired profit

of $142,857.14.

(b) Amount of revenue needed to achieve the targeted after-tax profit of $100 000:

In general, amount of revenue is measured by multiplying number of units with selling

price. In the aspect of above question, amount of revenue need to be computed and it is

measured by multiplying number of units to sold (From part a) and selling price

(Combined selling price of four products)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.