Management Accounting Report: Williams Performance Tenders Analysis

VerifiedAdded on 2020/02/03

|19

|5003

|72

Report

AI Summary

This report analyzes management accounting practices within Williams Performance Tenders, a boat manufacturing company. It explores the essential requirements for different accounting systems, including cost accounting and inventory management. The report details various management accounting reporting methods, such as budget reports, job cost reports, and debtor/accounts receivable aging reports. It further delves into cost analysis techniques, comparing marginal and absorption costing methods for preparing income statements. The report also discusses the advantages and disadvantages of different planning tools used for budgetary control and examines how organizations adapt management accounting systems to address financial challenges. The content provides a comprehensive understanding of management accounting principles and their application in a business context.

MANAGEMENT

ACCOUUNTING

ACCOUUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................4

TASK 1............................................................................................................................................4

P1Explaining management accounting and essential requirement for different types of

accounting system........................................................................................................................4

P2 Different methods used for management accounting reporting.............................................6

TASK 2............................................................................................................................................8

P3 Calculating cost using appropriate techniques of cost analysis for preparing income

statement of marginal and absorption costing.............................................................................8

Difference between marginal and absorption costing................................................................11

TASK 3..........................................................................................................................................12

P4 Explaining advantages and disadvantages of different types of planning tools for budgetary

control of Williams Performance Tenders................................................................................12

P5 Comparing how organizations are adapting the management accounting system to respond

the financial problems................................................................................................................17

CONCLUSION..............................................................................................................................19

REFERENCES..............................................................................................................................20

INTRODUCTION...........................................................................................................................4

TASK 1............................................................................................................................................4

P1Explaining management accounting and essential requirement for different types of

accounting system........................................................................................................................4

P2 Different methods used for management accounting reporting.............................................6

TASK 2............................................................................................................................................8

P3 Calculating cost using appropriate techniques of cost analysis for preparing income

statement of marginal and absorption costing.............................................................................8

Difference between marginal and absorption costing................................................................11

TASK 3..........................................................................................................................................12

P4 Explaining advantages and disadvantages of different types of planning tools for budgetary

control of Williams Performance Tenders................................................................................12

P5 Comparing how organizations are adapting the management accounting system to respond

the financial problems................................................................................................................17

CONCLUSION..............................................................................................................................19

REFERENCES..............................................................................................................................20

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

The management accounting is developed to meet the specific internal management need

for taking quick decision, allocation of resources and capacity utilization. Along with that,

customer value and internal business processes are used under management accounting through

which business objectives can be accomplished. The present report is based on Williams

Performance Tenders which deals in boat manufacturing. This organization is operating with 36

workforce in financial year 2011. It applies several concept of management accounting and

varied methods applied for reporting of the same. In addition to this, advantages and

disadvantages of different types of planning tools applied under the budgetary control have been

explained. Moreover, ways to determine the success of the business by responding the financial

problem has been explained.

TASK 1

P1Explaining management accounting and essential requirement for different types of

accounting system

The management accounting refers tot he process of preparing management report so as

to fulfill the short ass well as long term objectives of the business. It is helpful for corporation to

take the financial and statistical decision whereby firm can identify, measure and internal as well

as communicate the information among respective parties to meet the set objectives. Williams

Performance Tenders applied management accounting to fulfill the below mentioned objectives- Forecasting the future-With the help of management accounting report, company

forecast related to investment activities and diversification as well as expansion in

another country. This proves to be effective to cater the requirement of all related parties

and support business to accomplish long as well as short term objectives (Kaplan and

Atkinson, 2015). Forecasting cash flows-The management accounting report of Williams Performance

Tenders aids to take the decision related to future cash flow on the basis of budgets, and

trend chart. This proves to be effective to allocate the financial resources on right

business activities and gather profitability to meet specific objectives of the business.

The management accounting is developed to meet the specific internal management need

for taking quick decision, allocation of resources and capacity utilization. Along with that,

customer value and internal business processes are used under management accounting through

which business objectives can be accomplished. The present report is based on Williams

Performance Tenders which deals in boat manufacturing. This organization is operating with 36

workforce in financial year 2011. It applies several concept of management accounting and

varied methods applied for reporting of the same. In addition to this, advantages and

disadvantages of different types of planning tools applied under the budgetary control have been

explained. Moreover, ways to determine the success of the business by responding the financial

problem has been explained.

TASK 1

P1Explaining management accounting and essential requirement for different types of

accounting system

The management accounting refers tot he process of preparing management report so as

to fulfill the short ass well as long term objectives of the business. It is helpful for corporation to

take the financial and statistical decision whereby firm can identify, measure and internal as well

as communicate the information among respective parties to meet the set objectives. Williams

Performance Tenders applied management accounting to fulfill the below mentioned objectives- Forecasting the future-With the help of management accounting report, company

forecast related to investment activities and diversification as well as expansion in

another country. This proves to be effective to cater the requirement of all related parties

and support business to accomplish long as well as short term objectives (Kaplan and

Atkinson, 2015). Forecasting cash flows-The management accounting report of Williams Performance

Tenders aids to take the decision related to future cash flow on the basis of budgets, and

trend chart. This proves to be effective to allocate the financial resources on right

business activities and gather profitability to meet specific objectives of the business.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Analyzing rate of return-Every company has to analyze the internal performance in term

of resources for the purpose of getting expected rate of return out of the operational

activities. This can be made possible only with the help of estimating the requirement of

finance of business project (DRURY, 2013).

Performance variance-Use of management accounting makes it possible for Williams

Performance Tenders to understand the negative and positive variance exist in the

financial figures and accordingly reach to the valid decision. This contributes towards

determining the success of firm and deliver good quality of services to large number of

buyers effectively (What is Management Accounting and its Importance, 2017)

There are several kind of accounting system applied under Williams Performance

Tenders so as to meet the essential requirement. It has been explained as follows- Cost accounting system-The cost accounting management system is applied under

Williams Performance Tenders in order to track the process and job cost associated with

each product and services. For this purpose, data are recorded effectively with the help of

appropriate record keeping standard (Renz, 2016). Job costing system-It is another accounting system under which cost is allocated on

labour, material and overhead so as to find the input provided for each single product or

service. This proves to be effective for catering requirement of all related parties and

determining the long run success of the business in the marketplace. Inventory management system-There are different approaches used for the purpose of

inventory management with the application of tools such as Jit in Time and LIFO or

FIFO so as to manage the stock effectively and produce valid outcome in the direction of

growhr and success of the business (Brierley, 2016). In addition to this, tools or

application of management accounting is applied for effective management of inventory.

Price optimization-It is another management accounting system which is required by

Williams Performance Tenders to take the appropriate decision related to price of the

product or services in order to determine the rate of return. It facilitates to integrate all

business activities and meet the expectations of parties associated with the firm.

Therefore, price optimization is based on cost of inventory and other input used for

production of goods.

of resources for the purpose of getting expected rate of return out of the operational

activities. This can be made possible only with the help of estimating the requirement of

finance of business project (DRURY, 2013).

Performance variance-Use of management accounting makes it possible for Williams

Performance Tenders to understand the negative and positive variance exist in the

financial figures and accordingly reach to the valid decision. This contributes towards

determining the success of firm and deliver good quality of services to large number of

buyers effectively (What is Management Accounting and its Importance, 2017)

There are several kind of accounting system applied under Williams Performance

Tenders so as to meet the essential requirement. It has been explained as follows- Cost accounting system-The cost accounting management system is applied under

Williams Performance Tenders in order to track the process and job cost associated with

each product and services. For this purpose, data are recorded effectively with the help of

appropriate record keeping standard (Renz, 2016). Job costing system-It is another accounting system under which cost is allocated on

labour, material and overhead so as to find the input provided for each single product or

service. This proves to be effective for catering requirement of all related parties and

determining the long run success of the business in the marketplace. Inventory management system-There are different approaches used for the purpose of

inventory management with the application of tools such as Jit in Time and LIFO or

FIFO so as to manage the stock effectively and produce valid outcome in the direction of

growhr and success of the business (Brierley, 2016). In addition to this, tools or

application of management accounting is applied for effective management of inventory.

Price optimization-It is another management accounting system which is required by

Williams Performance Tenders to take the appropriate decision related to price of the

product or services in order to determine the rate of return. It facilitates to integrate all

business activities and meet the expectations of parties associated with the firm.

Therefore, price optimization is based on cost of inventory and other input used for

production of goods.

All these mentioned management account system are essential to use in the business

through which cost of each product or service can be recorded effectively and valid outcome can

be derived in the right manner. This contributes towards improving the business performance and

assists management to reduce the cost of production (Fisher and Krumwiede, 2015). For

example, price optimization is used to track the inventory applied in the production of boat by

Williams Performance Tenders.

Moreover, job costing system will be beneficial to find the cost of product in the right

manner. Apart from this, several benefits are associated with management account as it increase

the efficiency of the business and maximize overall rate of return. In addition to this, business-

critical decisions are taken with the help of management account whereby all activities can be

integrated and higher rate of return can be derived so as to ensure better utilization of the

resource. This leads to create goodwill of the business and support the managerial activities

effectively (Rojas, Leiva, Wanke and Marchant, 2015). Thus, Williams Performance Tenders

applies all concept of management accounting effectively through which it becomes easy to

recover the cost of production and set the price of products and services effectively for

accomplishing the set objectives.

P2 Different methods used for management accounting reporting

The management accounting report is presentation of financial data in term of findings or

recording for the department of accounting. It helps management to understand the actual

performance of the business and accordingly take the corrective action for the issues which are

being faced by the business. The major reason behind preparing the management accounting

report is to keep the management informed regarding the performance of company and track the

performance in the light of stated objectives. For this purpose, accounting report is prepared in

accordance with specific period. This aids to meet the specific objectives of the firm and cater

requirement of all related parties in the right direction (Lawless, 2013). Basically, period of

management accounting report is weekly, monthly, daily or quarterly as per the requirement or

request of the management. On the other hand, management accounting report is prepared to

assess the that whether to employed resources are deriving valid outcome or not. This also

provide information regarding the efficiency of corporation that how effectively resources can be

utilized for increasing the rate of return and support the managerial activities. Moreover, with the

through which cost of each product or service can be recorded effectively and valid outcome can

be derived in the right manner. This contributes towards improving the business performance and

assists management to reduce the cost of production (Fisher and Krumwiede, 2015). For

example, price optimization is used to track the inventory applied in the production of boat by

Williams Performance Tenders.

Moreover, job costing system will be beneficial to find the cost of product in the right

manner. Apart from this, several benefits are associated with management account as it increase

the efficiency of the business and maximize overall rate of return. In addition to this, business-

critical decisions are taken with the help of management account whereby all activities can be

integrated and higher rate of return can be derived so as to ensure better utilization of the

resource. This leads to create goodwill of the business and support the managerial activities

effectively (Rojas, Leiva, Wanke and Marchant, 2015). Thus, Williams Performance Tenders

applies all concept of management accounting effectively through which it becomes easy to

recover the cost of production and set the price of products and services effectively for

accomplishing the set objectives.

P2 Different methods used for management accounting reporting

The management accounting report is presentation of financial data in term of findings or

recording for the department of accounting. It helps management to understand the actual

performance of the business and accordingly take the corrective action for the issues which are

being faced by the business. The major reason behind preparing the management accounting

report is to keep the management informed regarding the performance of company and track the

performance in the light of stated objectives. For this purpose, accounting report is prepared in

accordance with specific period. This aids to meet the specific objectives of the firm and cater

requirement of all related parties in the right direction (Lawless, 2013). Basically, period of

management accounting report is weekly, monthly, daily or quarterly as per the requirement or

request of the management. On the other hand, management accounting report is prepared to

assess the that whether to employed resources are deriving valid outcome or not. This also

provide information regarding the efficiency of corporation that how effectively resources can be

utilized for increasing the rate of return and support the managerial activities. Moreover, with the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

use of management accounting report it becomes easy to ensure the all resources are utilized in

an optimum manner and supporting corporation to accomplish the objectives set by the business.

Williams Performance Tenders adopts the following management reporting system for assessing

the business performance effectively. All of these report are used with the basic purpose to

increase the efficiency and encouraging workforce to contribute their best towards achieving

long as well as short term objectives in the marketplace (Ueckerdt and et. al., 2013). Budget report-This report is used to assess the current performance of the business in

accordance with set standards. For example, a business find itself unable to cut the cost

then management revise their future budget by allocating more financial resources so as

to recover the cost of production and maintain the higher performance in the marketplace.

Furthermore, management and owners of the business refer the budget report for

encouraging employees and offering them incentives so as to determine the optimum

utilization of limited resources (DRURY, 2013.). For example, in case financial

performance of the business is good then workforce are provided monetary benefits.

Therefore, budget report facilitates to control the current as well as future performance of

corporation so as to cater requirement of all internals external parties in the right manner. Job cost report-This report is prepared by organizations like Williams Performance

Tenders to ascertain the cost of specific project. It is used for matching with estimation of

revenue in order to evaluate the profitability associated with that particular job. IN this

manner, business come to know about the higher earning or lower areas and then

accordingly form suitable strategies to meet the organization objectives in the right way

(Darghouth, Barbose and Wiser, 2014). For example, Williams Performance Tenders

might cancel to take the external contract for making small boats in case it does not

generate higher profit. This bring operational efficiency and ensure long term success of

the company in the marketplace. Not only this but job cost is also helpful to evaluate the

expenses incurred from project which provides an opportunity to correct those lacking

areas on right time. Inventory management report-The inventory management report is prepared by the

business for controlling the physical inventory and save the storage cost in the right

direction. The inventory management report basically covers, hourly labor cost, inventory

an optimum manner and supporting corporation to accomplish the objectives set by the business.

Williams Performance Tenders adopts the following management reporting system for assessing

the business performance effectively. All of these report are used with the basic purpose to

increase the efficiency and encouraging workforce to contribute their best towards achieving

long as well as short term objectives in the marketplace (Ueckerdt and et. al., 2013). Budget report-This report is used to assess the current performance of the business in

accordance with set standards. For example, a business find itself unable to cut the cost

then management revise their future budget by allocating more financial resources so as

to recover the cost of production and maintain the higher performance in the marketplace.

Furthermore, management and owners of the business refer the budget report for

encouraging employees and offering them incentives so as to determine the optimum

utilization of limited resources (DRURY, 2013.). For example, in case financial

performance of the business is good then workforce are provided monetary benefits.

Therefore, budget report facilitates to control the current as well as future performance of

corporation so as to cater requirement of all internals external parties in the right manner. Job cost report-This report is prepared by organizations like Williams Performance

Tenders to ascertain the cost of specific project. It is used for matching with estimation of

revenue in order to evaluate the profitability associated with that particular job. IN this

manner, business come to know about the higher earning or lower areas and then

accordingly form suitable strategies to meet the organization objectives in the right way

(Darghouth, Barbose and Wiser, 2014). For example, Williams Performance Tenders

might cancel to take the external contract for making small boats in case it does not

generate higher profit. This bring operational efficiency and ensure long term success of

the company in the marketplace. Not only this but job cost is also helpful to evaluate the

expenses incurred from project which provides an opportunity to correct those lacking

areas on right time. Inventory management report-The inventory management report is prepared by the

business for controlling the physical inventory and save the storage cost in the right

direction. The inventory management report basically covers, hourly labor cost, inventory

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

waste and overhead unit cost etc. This aids to compare the present performance of the

business in the light of set standard and accordingly derive valid outcome for entire

business. At this juncture, departmental performance can be assessed by Williams

Performance Tenders in order to get the information related to best performing

department and provide them timely bonus (Kaplan and Atkinson, 2015).

Debtor/accounts receivable aging reports-This report is prepared by the business in case

it offers credit base services or products to customers. This report is prepared by showing

the break down structure related to customer balances and then is used for assess the

performance of the business for certain time span. Further, aging report provide

appropriate information in term of presenting the data or separate invoice columns for

late payment for 30, 90 or 60 days. This aids to management to improve the credit

collection policy and reduce the ratio of bad debts to a great extent. This is considered as

the effective approach to control the expenses and promote the higher rate of return of the

business for longer time span.

TASK 2

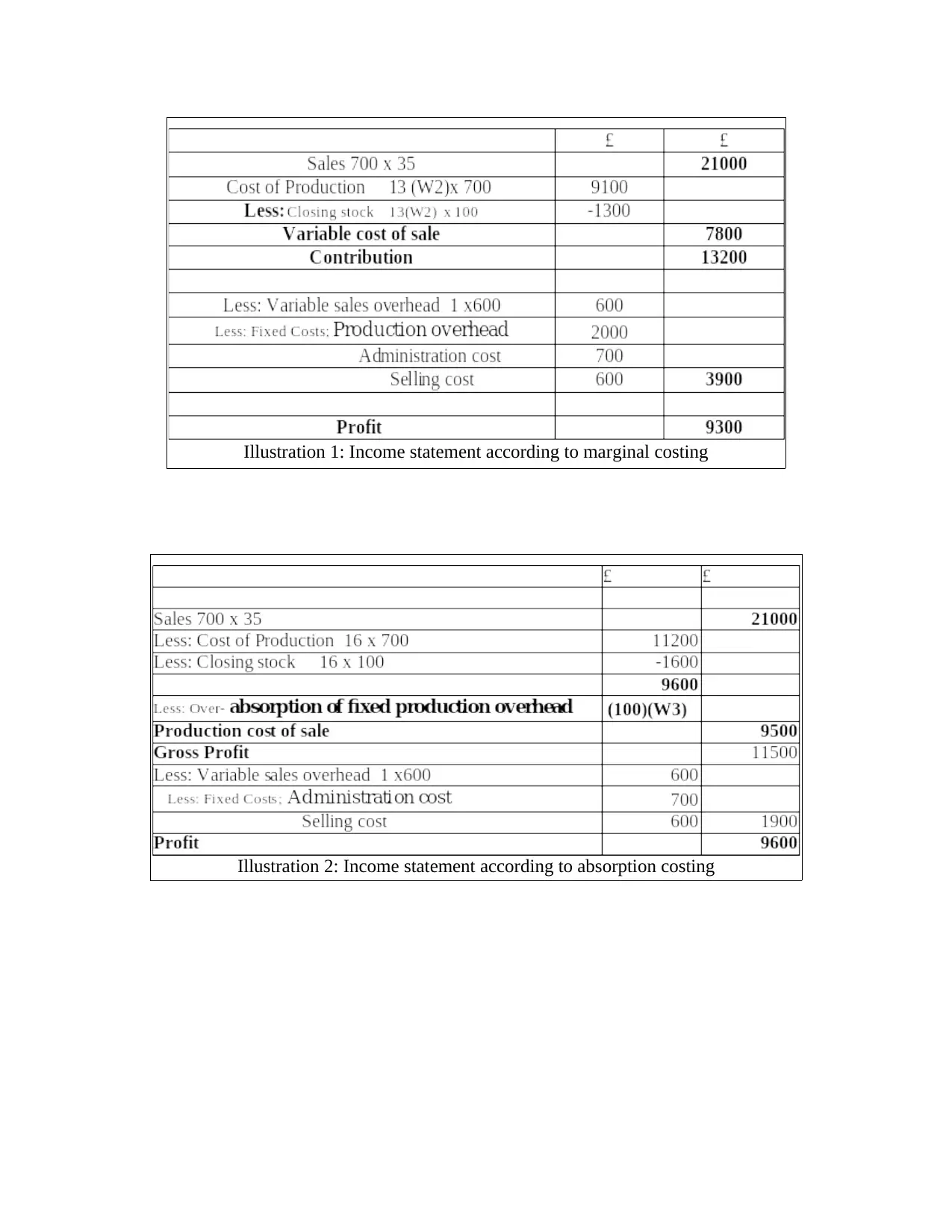

P3 Calculating cost using appropriate techniques of cost analysis for preparing income statement

of marginal and absorption costing

Cost analysis is considered as the important aspect to assess the internal performance of

the business and contribute towards its success in the marketplace with the increased rate of

return. It facilitates to support operational activities of firm and accordingly create its

competitive edge in the marketplace. The cost report is prepared in accordance with the report

derived from the financial and management accounting. Generally, cost analysis is used for

estimated on the basis of cost and volume analysis through which corporation can effectively

find the valid information regarding the business and follow the specific guidelines of the firm. It

proves to be effective in managing the cost related data (Ismail and King, 2014).

business in the light of set standard and accordingly derive valid outcome for entire

business. At this juncture, departmental performance can be assessed by Williams

Performance Tenders in order to get the information related to best performing

department and provide them timely bonus (Kaplan and Atkinson, 2015).

Debtor/accounts receivable aging reports-This report is prepared by the business in case

it offers credit base services or products to customers. This report is prepared by showing

the break down structure related to customer balances and then is used for assess the

performance of the business for certain time span. Further, aging report provide

appropriate information in term of presenting the data or separate invoice columns for

late payment for 30, 90 or 60 days. This aids to management to improve the credit

collection policy and reduce the ratio of bad debts to a great extent. This is considered as

the effective approach to control the expenses and promote the higher rate of return of the

business for longer time span.

TASK 2

P3 Calculating cost using appropriate techniques of cost analysis for preparing income statement

of marginal and absorption costing

Cost analysis is considered as the important aspect to assess the internal performance of

the business and contribute towards its success in the marketplace with the increased rate of

return. It facilitates to support operational activities of firm and accordingly create its

competitive edge in the marketplace. The cost report is prepared in accordance with the report

derived from the financial and management accounting. Generally, cost analysis is used for

estimated on the basis of cost and volume analysis through which corporation can effectively

find the valid information regarding the business and follow the specific guidelines of the firm. It

proves to be effective in managing the cost related data (Ismail and King, 2014).

Illustration 1: Income statement according to marginal costing

Illustration 2: Income statement according to absorption costing

Illustration 2: Income statement according to absorption costing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Difference between marginal and absorption costing

Majorly, two approaches are there that are being used named Marginal Costing and Absorption

Costing for the valuation of inventory. Under marginal costing, by segregating the fixed and

variable cost marginal cost, determination of marginal costing is done. In this costing method,

only variable costs are charged for the operations done. However, in these operations, fixed cost

is excluded as it is already involved. But, fixed cost is charged to profit and loss account for the

particular period of time in which the operations are conducted (Fullerton Kennedy and Widener,

2014).

On the other hand. Absorption costing can be termed as full costing as under this method, the

total units produced engrosses all costs whether they are fixed or variable. It can be said that

these costs are mainly used for the purpose of reporting which means for the financial and tax

reporting. According to many, marginal costing is better than absorption but in order to

understand the same, it is important for one that he/she should have enough knowledge about the

difference between marginal and absorption costing for the purpose of reaching at final and

appropriate conclusion with regard to decide the better and preferred cost.

Marginal costing can be termed as the technique which is used by businesses for their decision

making process in order to ascertain the total cost of production. While, absorption costing is

nothing but the apportionment of total costs to cost center with the help of which total cost

involved in the production process is determined. Along with that, under marginal costing, the

variable cost is taken as the product cost by firms however, for calculating the period cost, fixed

cost is considered (Armstrong, 2014). On the other hand, under absorption costing, variable as

well as fixed; both the costs are considered as product cost.

In addition to this, for the classification of overheads, marginal costing involves fixed and

variable costs both but for absorption costing, overheads considered are production,

administration, selling as well as distribution. Marginal costing plays a significant role in

measuring the profitability through profit volume ratio whereas, under absorption costing,

profitability gets affected because of the inclusion of fixed cost. Apart from that, cost per unit

under marginal costing refers to the variances that are there in the opening and closing stock by

which cost per unit of output does not get impacted. On the contrary, if cost per unit is taken into

Majorly, two approaches are there that are being used named Marginal Costing and Absorption

Costing for the valuation of inventory. Under marginal costing, by segregating the fixed and

variable cost marginal cost, determination of marginal costing is done. In this costing method,

only variable costs are charged for the operations done. However, in these operations, fixed cost

is excluded as it is already involved. But, fixed cost is charged to profit and loss account for the

particular period of time in which the operations are conducted (Fullerton Kennedy and Widener,

2014).

On the other hand. Absorption costing can be termed as full costing as under this method, the

total units produced engrosses all costs whether they are fixed or variable. It can be said that

these costs are mainly used for the purpose of reporting which means for the financial and tax

reporting. According to many, marginal costing is better than absorption but in order to

understand the same, it is important for one that he/she should have enough knowledge about the

difference between marginal and absorption costing for the purpose of reaching at final and

appropriate conclusion with regard to decide the better and preferred cost.

Marginal costing can be termed as the technique which is used by businesses for their decision

making process in order to ascertain the total cost of production. While, absorption costing is

nothing but the apportionment of total costs to cost center with the help of which total cost

involved in the production process is determined. Along with that, under marginal costing, the

variable cost is taken as the product cost by firms however, for calculating the period cost, fixed

cost is considered (Armstrong, 2014). On the other hand, under absorption costing, variable as

well as fixed; both the costs are considered as product cost.

In addition to this, for the classification of overheads, marginal costing involves fixed and

variable costs both but for absorption costing, overheads considered are production,

administration, selling as well as distribution. Marginal costing plays a significant role in

measuring the profitability through profit volume ratio whereas, under absorption costing,

profitability gets affected because of the inclusion of fixed cost. Apart from that, cost per unit

under marginal costing refers to the variances that are there in the opening and closing stock by

which cost per unit of output does not get impacted. On the contrary, if cost per unit is taken into

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

consideration, cost per unit gets highly affected because of the variances present in opening and

closing stock. Further, contribution that per unit makes is the most highlighted aspect in marginal

costing however, in absorption costing, the major area to be focused is net profit per unit. Under

marginal costing, cost data is calculated in accordance with the contribution of each product

whereas, cost data in absorption costing is presented by the way of conventional way (Speklé and

Verbeeten, 2014).

For product costing and inventory valuation, marginal costing plays the significant role as for the

same only variable cost is considered. However, under absorption costing; in order to do

valuation of product costing and inventory valuation, the method considers both; fixed cost as

well as variable cost. Furthermore under marginal costing, fixed overhead are treated in a

different manner. Along with that, here, profitability of different products is judged through

period cost as well as by Profit/Volume ratio (P/V ratio). On the other hand, under absorption

costing system, from the cost of production, business charges the fixed cost which is borne by

each product but with reasonable share.

It can be said that there are differences in the profits generated in income statement by the

two costing system. It is because; fixed cost of production to the output is engrossed by the

absorption costing procedure. However, the fact is ignored by marginal costing system. In

addition to this, the absorption costing is done by the firms on the basis of budgeted levels of

output. However, the fact cannot be ignored that because of the reason; fixed overheads remain

same irrespective of the levels of output, actual and budgeted levels result in makes the to make

variances at the time of its recovery (Carmona, Ezzamel and Gutiérrez, 2016).

TASK 3

P4 Explaining advantages and disadvantages of different types of planning tools for budgetary

control of Williams Performance Tenders

Budgetary control refers to the process of allocation of financial resources on investing

activities with the estimation of certain ratio of profitability. It enables corporation to integrate

the current business activities effectively so as to derive valid outcome and create competitive

edge of the corporation. The planning tools consists of varied kind of budgets and techniques

such as capital budgeting. This proves to be effective to reduce the cost of operation or

production for deriving higher rate of return. The budgetary control procedure refers to the

closing stock. Further, contribution that per unit makes is the most highlighted aspect in marginal

costing however, in absorption costing, the major area to be focused is net profit per unit. Under

marginal costing, cost data is calculated in accordance with the contribution of each product

whereas, cost data in absorption costing is presented by the way of conventional way (Speklé and

Verbeeten, 2014).

For product costing and inventory valuation, marginal costing plays the significant role as for the

same only variable cost is considered. However, under absorption costing; in order to do

valuation of product costing and inventory valuation, the method considers both; fixed cost as

well as variable cost. Furthermore under marginal costing, fixed overhead are treated in a

different manner. Along with that, here, profitability of different products is judged through

period cost as well as by Profit/Volume ratio (P/V ratio). On the other hand, under absorption

costing system, from the cost of production, business charges the fixed cost which is borne by

each product but with reasonable share.

It can be said that there are differences in the profits generated in income statement by the

two costing system. It is because; fixed cost of production to the output is engrossed by the

absorption costing procedure. However, the fact is ignored by marginal costing system. In

addition to this, the absorption costing is done by the firms on the basis of budgeted levels of

output. However, the fact cannot be ignored that because of the reason; fixed overheads remain

same irrespective of the levels of output, actual and budgeted levels result in makes the to make

variances at the time of its recovery (Carmona, Ezzamel and Gutiérrez, 2016).

TASK 3

P4 Explaining advantages and disadvantages of different types of planning tools for budgetary

control of Williams Performance Tenders

Budgetary control refers to the process of allocation of financial resources on investing

activities with the estimation of certain ratio of profitability. It enables corporation to integrate

the current business activities effectively so as to derive valid outcome and create competitive

edge of the corporation. The planning tools consists of varied kind of budgets and techniques

such as capital budgeting. This proves to be effective to reduce the cost of operation or

production for deriving higher rate of return. The budgetary control procedure refers to the

process of making budget or allocating the financial resources on different major business

activities and then comparing the same with the actual results (Kaplan and Atkinson, 2015). This

in turn business get to know about the variances and apply suitable strategies to overcome such

kind of situation.

Capital budgeting

Capital planning is also used as the budgeting control under which varied techniques are

applied by the business. The first technique of net present value method under which

management understand the requirement of finance for investment in the specific project. This

project is evaluated in accordance with net present value and then comparison is made to

understand the ratio of profitability derived to business from the same project. Apart from this,

payback period method as another technique is applied so as to get the information related to

time period required to recover the cost or initial cost of project (DRURY, 2013). For this

purpose, business expected cash flow is evaluated in term of initial investment and then

comparison is made for better decision. For this purpose, a project taking less time to complete to

cover the initial investment is selected and other is rejected. It leads to support all managerial

activities of firm and cater requirement of all related parties in the right direction. Moreover,

internal rate of return is also covered under the capital budgeting method through which return

generated from each project is considered for the selection of the most suitable one. It shows that

capital budgeting is the most effective method for calculating the rate of return for the business.

activities and then comparing the same with the actual results (Kaplan and Atkinson, 2015). This

in turn business get to know about the variances and apply suitable strategies to overcome such

kind of situation.

Capital budgeting

Capital planning is also used as the budgeting control under which varied techniques are

applied by the business. The first technique of net present value method under which

management understand the requirement of finance for investment in the specific project. This

project is evaluated in accordance with net present value and then comparison is made to

understand the ratio of profitability derived to business from the same project. Apart from this,

payback period method as another technique is applied so as to get the information related to

time period required to recover the cost or initial cost of project (DRURY, 2013). For this

purpose, business expected cash flow is evaluated in term of initial investment and then

comparison is made for better decision. For this purpose, a project taking less time to complete to

cover the initial investment is selected and other is rejected. It leads to support all managerial

activities of firm and cater requirement of all related parties in the right direction. Moreover,

internal rate of return is also covered under the capital budgeting method through which return

generated from each project is considered for the selection of the most suitable one. It shows that

capital budgeting is the most effective method for calculating the rate of return for the business.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.