Management Accounting Assignment: Cost Analysis and CVP

VerifiedAdded on 2020/05/28

|6

|1178

|156

Homework Assignment

AI Summary

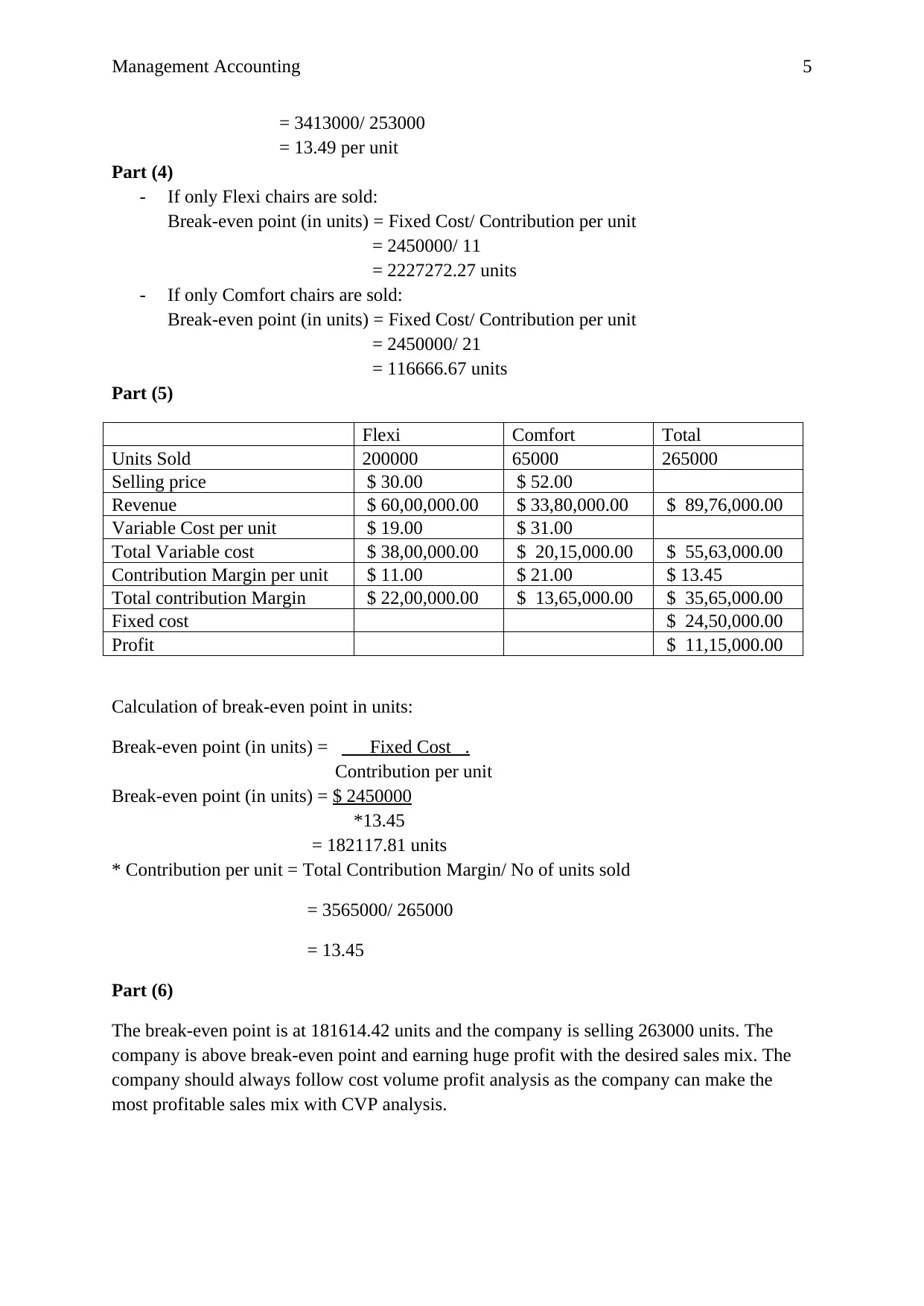

This document presents a comprehensive solution to a management accounting assignment. The solution begins with a detailed cost analysis using both traditional costing and activity-based costing (ABC) methods, comparing the results and explaining the differences in per-unit costs for two product lines, Xtreme and Wtreme. It then delves into cost-volume-profit (CVP) analysis, outlining its benefits, including profit planning and decision-making, and discussing the underlying assumptions. The solution includes calculations of the break-even point, considering different sales mixes and scenarios, providing insights into profitability and the impact of various factors on the company's financial performance. The assignment concludes with recommendations on the optimal sales mix and emphasizes the importance of using CVP analysis for informed business decisions. References from prominent accounting textbooks are also provided.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.