Management Accounting Report: Cost Analysis and Budgeting Techniques

VerifiedAdded on 2020/07/22

|17

|4413

|32

Report

AI Summary

This report delves into the core concepts of management accounting, encompassing cost classification, various costing methods, and budgeting processes. It begins with an introduction to accounting and its role in budget estimation and cost control, followed by a detailed examination of cost types, including direct, indirect, manufacturing, and period costs. The report then explores various costing methods such as job costing, batch costing, process costing, and service costing, with a focus on their application. Furthermore, the report analyzes different costing techniques like absorption costing, marginal costing, and activity-based costing, providing calculations and examples. The report also covers the aims, objectives, and methods of the budgeting process, along with a case study demonstrating budget formulation. Finally, it calculates and analyzes variances, providing findings from case studies and offering recommendations.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1.1 classification of cost.........................................................................................................3

1.2 various costing methods...................................................................................................4

1.3 calculation of costing techniques......................................................................................5

1.4 Analysis of cost data used by the company......................................................................5

TASK 2............................................................................................................................................8

2.1 PPT...................................................................................................................................8

2.2 PPT...................................................................................................................................9

2.3 PPT.................................................................................................................................10

TASK 3..........................................................................................................................................11

3.1Aims and objectives of budgeting process .....................................................................11

3.2 Methods of budgeting process .......................................................................................11

3.3 Budget formulation by using appropriate method..........................................................12

3.4 Case study of Antonio Ltd as on 6 month .....................................................................13

TASK 4..........................................................................................................................................15

4.1 calculation of variances .................................................................................................15

4.2 calculate variances from the case studies.......................................................................15

4.3 Findings of case study ...................................................................................................16

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

1.1 classification of cost.........................................................................................................3

1.2 various costing methods...................................................................................................4

1.3 calculation of costing techniques......................................................................................5

1.4 Analysis of cost data used by the company......................................................................5

TASK 2............................................................................................................................................8

2.1 PPT...................................................................................................................................8

2.2 PPT...................................................................................................................................9

2.3 PPT.................................................................................................................................10

TASK 3..........................................................................................................................................11

3.1Aims and objectives of budgeting process .....................................................................11

3.2 Methods of budgeting process .......................................................................................11

3.3 Budget formulation by using appropriate method..........................................................12

3.4 Case study of Antonio Ltd as on 6 month .....................................................................13

TASK 4..........................................................................................................................................15

4.1 calculation of variances .................................................................................................15

4.2 calculate variances from the case studies.......................................................................15

4.3 Findings of case study ...................................................................................................16

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION

The project report contain description of management accounting. Under this various

case studies are mentioned that consist detail of companies management system. Accounting is

the process by which company can estimate its budget estimation and cost control for a particular

year (Arroyo, 2012). There are different types of cost and methods which are used by the

companies in its daily business operations. Under this report we have calculate and forecasted

budget has been made to estimate annual budget cash forecast during the year.

Various performance indicator are explain in appropriate manner and on the basis of this

we have done certain recommendation and generate valuable feedback. Nature and purpose of

budgeting process adopted by the company.

TASK 1

1.1 classification of cost

Cost : It refer to an amount paid or needed in payment for a material that are required

during the production process (Bodie, 2013). Research,retail and cost accounting under this cost

is total value of money that has been used to produce products and thus, is not gettable for any

use any longer for any business, the cost might be one of acquisition, in case the sum of fund

spent to adopt it is counted as cost for the company.

Types of costs and classification:

According to traceability

1. Direct cost which is related to manufacturing of goods and services. It may includes

material , labour ,expenses or distribution cost those are included in production process.

2. Indirect cost that are not incurred directly in manufacturing process. These may be fixed

or variable (Burritt and et. al., 2011).

Classification of costs

Manufacturing cost are often classified as under :

a) Direct Material b) Direct labour c) Manufacturing overhead

Prime cost = Direct cost of material + Direct cost of labour

Conversion cost =Cost of direct labour + manufacturing overhead

According to time of charge against Revenue

The project report contain description of management accounting. Under this various

case studies are mentioned that consist detail of companies management system. Accounting is

the process by which company can estimate its budget estimation and cost control for a particular

year (Arroyo, 2012). There are different types of cost and methods which are used by the

companies in its daily business operations. Under this report we have calculate and forecasted

budget has been made to estimate annual budget cash forecast during the year.

Various performance indicator are explain in appropriate manner and on the basis of this

we have done certain recommendation and generate valuable feedback. Nature and purpose of

budgeting process adopted by the company.

TASK 1

1.1 classification of cost

Cost : It refer to an amount paid or needed in payment for a material that are required

during the production process (Bodie, 2013). Research,retail and cost accounting under this cost

is total value of money that has been used to produce products and thus, is not gettable for any

use any longer for any business, the cost might be one of acquisition, in case the sum of fund

spent to adopt it is counted as cost for the company.

Types of costs and classification:

According to traceability

1. Direct cost which is related to manufacturing of goods and services. It may includes

material , labour ,expenses or distribution cost those are included in production process.

2. Indirect cost that are not incurred directly in manufacturing process. These may be fixed

or variable (Burritt and et. al., 2011).

Classification of costs

Manufacturing cost are often classified as under :

a) Direct Material b) Direct labour c) Manufacturing overhead

Prime cost = Direct cost of material + Direct cost of labour

Conversion cost =Cost of direct labour + manufacturing overhead

According to time of charge against Revenue

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Product cost – it is said to be inventory cost which is that form of stock that are charged

against revenue only when it is sold.

Period cost : these are charged directly against revenue. It includes non-manufacturing

cost (Burritt and Schaltegger, 2010).

According to behaviour with activity

Variable cost : These are those cost which are incurred while producing one extra unit of

product . It varies according to production done in units.

Fixed cost : those cost that remain constant ,they can not affected with changes in unit

for manufactured products.

Mixed cost : all those combination cost which consist of variable and fixed cost at the

same time (Busco and Scapens, 2011).

1.2 various costing methods

Costing methods are recording and maintaining the record in which parent company

invest in subsidiary that is shown in cost, without having any kind of effect of profit and loss on

investments to its subsidiary. There are various costing method that help to evaluate cost for the

company :

1. Job costing method : The another name of this method is job order costing which are

linked with the cost of production one single unit or accumulation of products.

Basically,these are mainly used only those condition when the product manufactured are

good enough and various from each other.

2. Batch costing method :It is a kind of order costing. It is mostly similar to job costing

under which each product have given a unique code number to identified it with year of

production and its serial number. (Cadez and Guilding, 2012).

3. Process costing : under this methods of distribution cost to a particular unit that are

produce by large number homogeneous products. It is that type of costing which is used

to determine the cost at each level of processing.

4. Service costing : under this costing method all the cost calculated in production of

services are added equally and together. The are divided as total number of services units

rendered.

against revenue only when it is sold.

Period cost : these are charged directly against revenue. It includes non-manufacturing

cost (Burritt and Schaltegger, 2010).

According to behaviour with activity

Variable cost : These are those cost which are incurred while producing one extra unit of

product . It varies according to production done in units.

Fixed cost : those cost that remain constant ,they can not affected with changes in unit

for manufactured products.

Mixed cost : all those combination cost which consist of variable and fixed cost at the

same time (Busco and Scapens, 2011).

1.2 various costing methods

Costing methods are recording and maintaining the record in which parent company

invest in subsidiary that is shown in cost, without having any kind of effect of profit and loss on

investments to its subsidiary. There are various costing method that help to evaluate cost for the

company :

1. Job costing method : The another name of this method is job order costing which are

linked with the cost of production one single unit or accumulation of products.

Basically,these are mainly used only those condition when the product manufactured are

good enough and various from each other.

2. Batch costing method :It is a kind of order costing. It is mostly similar to job costing

under which each product have given a unique code number to identified it with year of

production and its serial number. (Cadez and Guilding, 2012).

3. Process costing : under this methods of distribution cost to a particular unit that are

produce by large number homogeneous products. It is that type of costing which is used

to determine the cost at each level of processing.

4. Service costing : under this costing method all the cost calculated in production of

services are added equally and together. The are divided as total number of services units

rendered.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5. Contract costing : It is said to be tracking of cost which are associated to certain contact

done with customer. It is way of providing funds to large and small business projects that

are involve during the period (Cullen and Whelan, 2011).

As from all the methods we have find out that Bittern Ltd company is using process costing

method as they are involved in manufacturing product.

1.3 calculation of costing techniques

Various costing techniques : most of important techniques used by the company are as

follows :

Absorption costing : It refers those method which are used to calculate cost of indirect expenses

that are produce during production process. Marginal costing can be said as added cost of

producing one extra unit of product or services.(DRURY, 2013).

Activity based costing : under this costing methods managers identified the activity and allot cost

of each activity with resources to goods and services.

Costing plus pricing : It is cost based methods used to set price of product and services. under

this methods all the direct costs that are incurred during production process are added to markup

percentages.

Marketing pricing : It is the Economic price of product that are used in marketplace. Market

value are equal under these conditions of market equilibrium .

Target costing : It is used to determine product life cycle cost that are well enough to produce

specified function and quality to its desire profits (Englund and Gerdin, 2011).

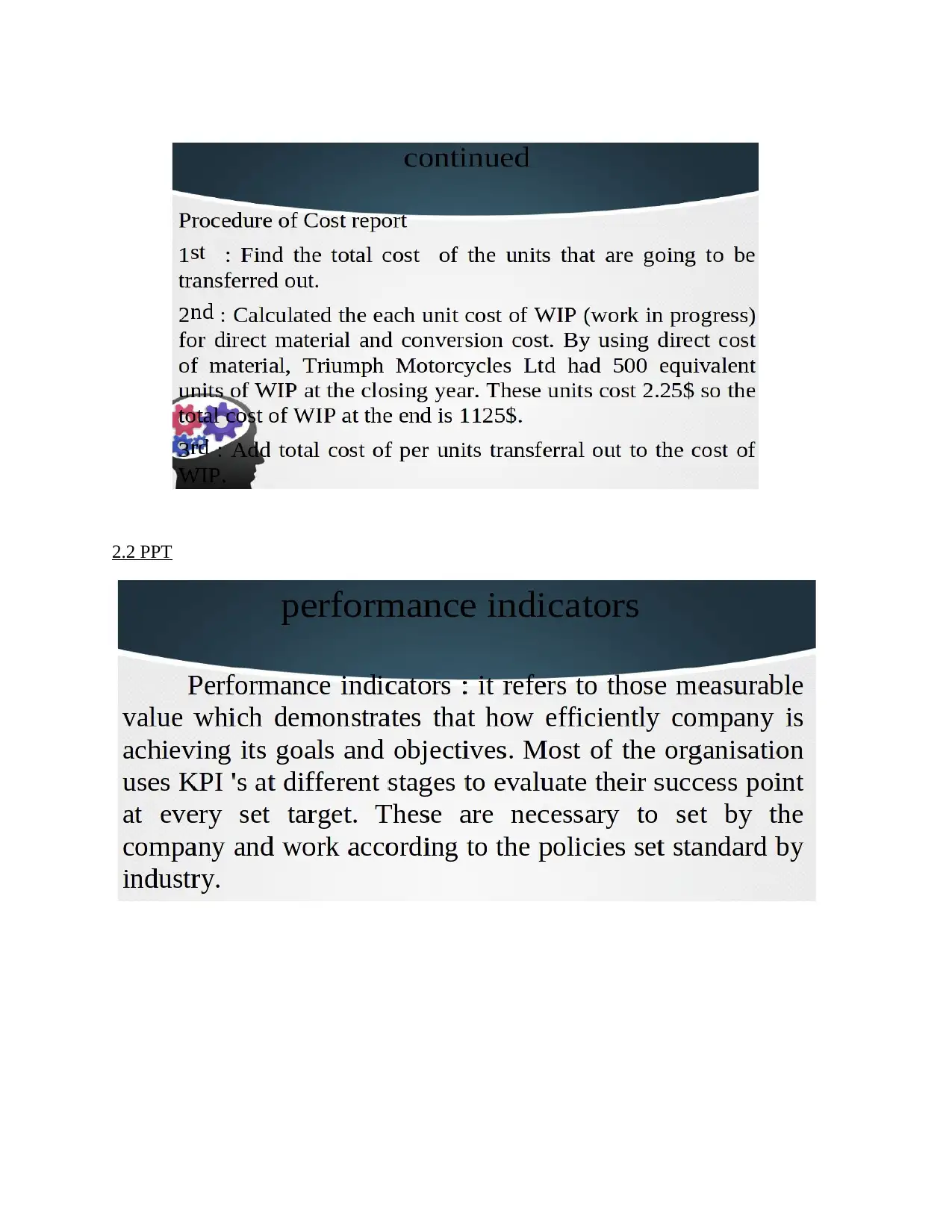

1.4 Analysis of cost data used by the company

A) allocation and apportion overhead to major departments.

Overheads : These are said to be overall current expenses that are associated with direct

material, direct labour and other expenses. Calculation of overhead :

Net profits as per marginal costing t1 t2 t3

SALES VALUE (25*1000) 25000 25000 25000

LESS- COST OF PRODUCTION

material produced (1000*12) =12000

less- closing stock (100*12)=1200

done with customer. It is way of providing funds to large and small business projects that

are involve during the period (Cullen and Whelan, 2011).

As from all the methods we have find out that Bittern Ltd company is using process costing

method as they are involved in manufacturing product.

1.3 calculation of costing techniques

Various costing techniques : most of important techniques used by the company are as

follows :

Absorption costing : It refers those method which are used to calculate cost of indirect expenses

that are produce during production process. Marginal costing can be said as added cost of

producing one extra unit of product or services.(DRURY, 2013).

Activity based costing : under this costing methods managers identified the activity and allot cost

of each activity with resources to goods and services.

Costing plus pricing : It is cost based methods used to set price of product and services. under

this methods all the direct costs that are incurred during production process are added to markup

percentages.

Marketing pricing : It is the Economic price of product that are used in marketplace. Market

value are equal under these conditions of market equilibrium .

Target costing : It is used to determine product life cycle cost that are well enough to produce

specified function and quality to its desire profits (Englund and Gerdin, 2011).

1.4 Analysis of cost data used by the company

A) allocation and apportion overhead to major departments.

Overheads : These are said to be overall current expenses that are associated with direct

material, direct labour and other expenses. Calculation of overhead :

Net profits as per marginal costing t1 t2 t3

SALES VALUE (25*1000) 25000 25000 25000

LESS- COST OF PRODUCTION

material produced (1000*12) =12000

less- closing stock (100*12)=1200

variable cost -10800 -10800 -10800

Contribution 14200 14200 14200

less:

variable sales overhead (1000*1)=1000

fixed overheads =5000

fixed labour cost=5000

11000 11000 11000

Net Income as per marginal costing 3200 3200 3200

Net Income as per absorption costing

SALES VALUE (25*1000) 25000 25000 25000

LESS- COST OF PRODUCTION 13000 13000 13000

gross profit 12000 12000 12000

less:

fixed cost (5000+5000) 10000 10000 10000

Net Income as per absorption costing 2000 2000 2000

Meintenance cost is distributed on 15%,75%and10%. All the expenses are divided in

ratios 4:3:2:1.

B)

Net profits as per marginal costing t1 t2 t3

SALES VALUE (25*1000) 25000 25000 25000

LESS- COST OF PRODUCTION

material produced -18000 -9600 -8400

less- closing stock -7200 -4800 -1200

variable cost -25200 -14400 -9600

Contribution -200 10600 15400

less:

variable sales overhead

(1000*1)=1000

Contribution 14200 14200 14200

less:

variable sales overhead (1000*1)=1000

fixed overheads =5000

fixed labour cost=5000

11000 11000 11000

Net Income as per marginal costing 3200 3200 3200

Net Income as per absorption costing

SALES VALUE (25*1000) 25000 25000 25000

LESS- COST OF PRODUCTION 13000 13000 13000

gross profit 12000 12000 12000

less:

fixed cost (5000+5000) 10000 10000 10000

Net Income as per absorption costing 2000 2000 2000

Meintenance cost is distributed on 15%,75%and10%. All the expenses are divided in

ratios 4:3:2:1.

B)

Net profits as per marginal costing t1 t2 t3

SALES VALUE (25*1000) 25000 25000 25000

LESS- COST OF PRODUCTION

material produced -18000 -9600 -8400

less- closing stock -7200 -4800 -1200

variable cost -25200 -14400 -9600

Contribution -200 10600 15400

less:

variable sales overhead

(1000*1)=1000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

fixed overheads =5000

fixed labour cost=5000

11000 11000 11000

Net Income as per marginal costing -11200 -400 4400

Net Income as per absorption

costing

SALES VALUE (25*1000) 25000 25000 25000

LESS- COST OF PRODUCTION 19500 10400 9100

gross profit 5500 14600 15900

less:

fixed cost (5000+5000) 10000 10000 10000

Net Income as per absorption

costing -4500 4600 5900

c)

Net profits as per marginal costing T1 T2 T3

SALES VALUE (25*1000) 25000 25000 25000

LESS- COST OF PRODUCTION

material produced -12000 -12000 -12000

less- closing stock -7200 -4800 -1200

variable cost -19200 -16800 -13200

Contribution -200 8200 11800

less:

variable sales overhead

(1000*1)=1000

fixed overheads =5000

fixed labour cost=5000

11000 11000 11000

fixed labour cost=5000

11000 11000 11000

Net Income as per marginal costing -11200 -400 4400

Net Income as per absorption

costing

SALES VALUE (25*1000) 25000 25000 25000

LESS- COST OF PRODUCTION 19500 10400 9100

gross profit 5500 14600 15900

less:

fixed cost (5000+5000) 10000 10000 10000

Net Income as per absorption

costing -4500 4600 5900

c)

Net profits as per marginal costing T1 T2 T3

SALES VALUE (25*1000) 25000 25000 25000

LESS- COST OF PRODUCTION

material produced -12000 -12000 -12000

less- closing stock -7200 -4800 -1200

variable cost -19200 -16800 -13200

Contribution -200 8200 11800

less:

variable sales overhead

(1000*1)=1000

fixed overheads =5000

fixed labour cost=5000

11000 11000 11000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Net Income as per marginal costing -11200 -2800 800

Net Income as per absorption

costing

SALES VALUE (25*1000) 25000 25000 25000

LESS- COST OF PRODUCTION -13000 -13000 -13000

gross profit 12000 12000 12000

less:

fixed cost (5000+5000) 10000 10000 10000

Net Income as per absorption

costing 2000 2000 2000

TASK 2

2.1 PPT

Net Income as per absorption

costing

SALES VALUE (25*1000) 25000 25000 25000

LESS- COST OF PRODUCTION -13000 -13000 -13000

gross profit 12000 12000 12000

less:

fixed cost (5000+5000) 10000 10000 10000

Net Income as per absorption

costing 2000 2000 2000

TASK 2

2.1 PPT

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2.2 PPT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2.3 PPT

TASK 3

3.1Aims and objectives of budgeting process

In current era where there is huge competition regarding financial stability which are

directly impact on the resources which are available with the company that are used during

manufacturing process . To increase organisation effectiveness company may need to structure a

appropriate budget which can help in future forecasting.

Purpose of budgeting process :

Controlling the total spending : the main objective of budgeting is to control extra

spending of business. Once budgeting is don all the activities has to be done keeping in

mind the budget given against it.

Wealth maximising : the budgeted income can save the company and help them to

invest in different activities. The saved amount would be used in future that will provide

valuable interest (Pipan and Czarniawska, 2010).

Fulfilling organisation goal : This may open up various new doors for the business

which help them to achieve companies objectives.

Nature of budgeting process:

Determining the requirement of expenditure : The budgeting process help us to determine total

requirement of expenses that are need at the time of manufacturing. it will help to meet future

and current objective of the company.

Rigid in nature : Budgets are prepared after estimation of all cost and expenses that a company

is going used in a financial statements (Macintosh and Quattrone, 2010).

Time consuming : The budgeting can be time consuming to also . As we know that all the

estimation can be identified in a particular period unless any impact of this has not shown.

It is continuous process : These are not one time project because every year we have to revise the

company data and each department on the basis of its effectiveness in the profitability.

3.2 Methods of budgeting process

Important budgeting methods used under the case study is functional budgeting as we can

separate each budget's associated with financial situation like,sale,cash flows , income statements

of financial departments. These budget is estimation for the company who try to manage out its

3.1Aims and objectives of budgeting process

In current era where there is huge competition regarding financial stability which are

directly impact on the resources which are available with the company that are used during

manufacturing process . To increase organisation effectiveness company may need to structure a

appropriate budget which can help in future forecasting.

Purpose of budgeting process :

Controlling the total spending : the main objective of budgeting is to control extra

spending of business. Once budgeting is don all the activities has to be done keeping in

mind the budget given against it.

Wealth maximising : the budgeted income can save the company and help them to

invest in different activities. The saved amount would be used in future that will provide

valuable interest (Pipan and Czarniawska, 2010).

Fulfilling organisation goal : This may open up various new doors for the business

which help them to achieve companies objectives.

Nature of budgeting process:

Determining the requirement of expenditure : The budgeting process help us to determine total

requirement of expenses that are need at the time of manufacturing. it will help to meet future

and current objective of the company.

Rigid in nature : Budgets are prepared after estimation of all cost and expenses that a company

is going used in a financial statements (Macintosh and Quattrone, 2010).

Time consuming : The budgeting can be time consuming to also . As we know that all the

estimation can be identified in a particular period unless any impact of this has not shown.

It is continuous process : These are not one time project because every year we have to revise the

company data and each department on the basis of its effectiveness in the profitability.

3.2 Methods of budgeting process

Important budgeting methods used under the case study is functional budgeting as we can

separate each budget's associated with financial situation like,sale,cash flows , income statements

of financial departments. These budget is estimation for the company who try to manage out its

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.