Management Accounting Report: Hospital Cost Analysis and Prediction

VerifiedAdded on 2020/01/21

|21

|3972

|102

Report

AI Summary

This report delves into a comprehensive management accounting analysis, focusing on a hospital's operational costs and financial performance. It begins with a scatter diagram and high-low method to analyze administrative costs against patient load, followed by regression analysis for cost prediction. The report explores the impact of emergency procedures on administrative costs, evaluating the suitability of different prediction tools. It then covers equivalent units, cost per unit, and assignment of production costs, including a weighted average cost analysis. Further, the report addresses overhead allocation, calculating overhead rates, comparing actual and budgeted costs, and assessing the accuracy of cost estimation methods. Activity-based costing (ABC) is applied to determine service pricing, cash receipts, and budget preparation. The report also examines cost reallocation using direct, step-down, and reciprocal service methods, followed by a linear programming (LPP) analysis for meal preparation. Finally, it concludes with a cost quality report and comments on quality cost performance.

MANAGEMENT

ACCCOUNTING

ACCCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

QUESTION 1..................................................................................................................................4

(1)Scatter diagram of administrative cost and patients load during first year of operations.......4

(2) High low method of management accounting for forecast....................................................4

(3) Prediction of administrative cost when 800 patients visit the hospital..................................5

(4) Regression analysis................................................................................................................5

(5) Impact of emergency procedures on the administrative cost.................................................7

(6) Suitability of tools used for predicting value of the variable.................................................8

QUESTION 2..................................................................................................................................9

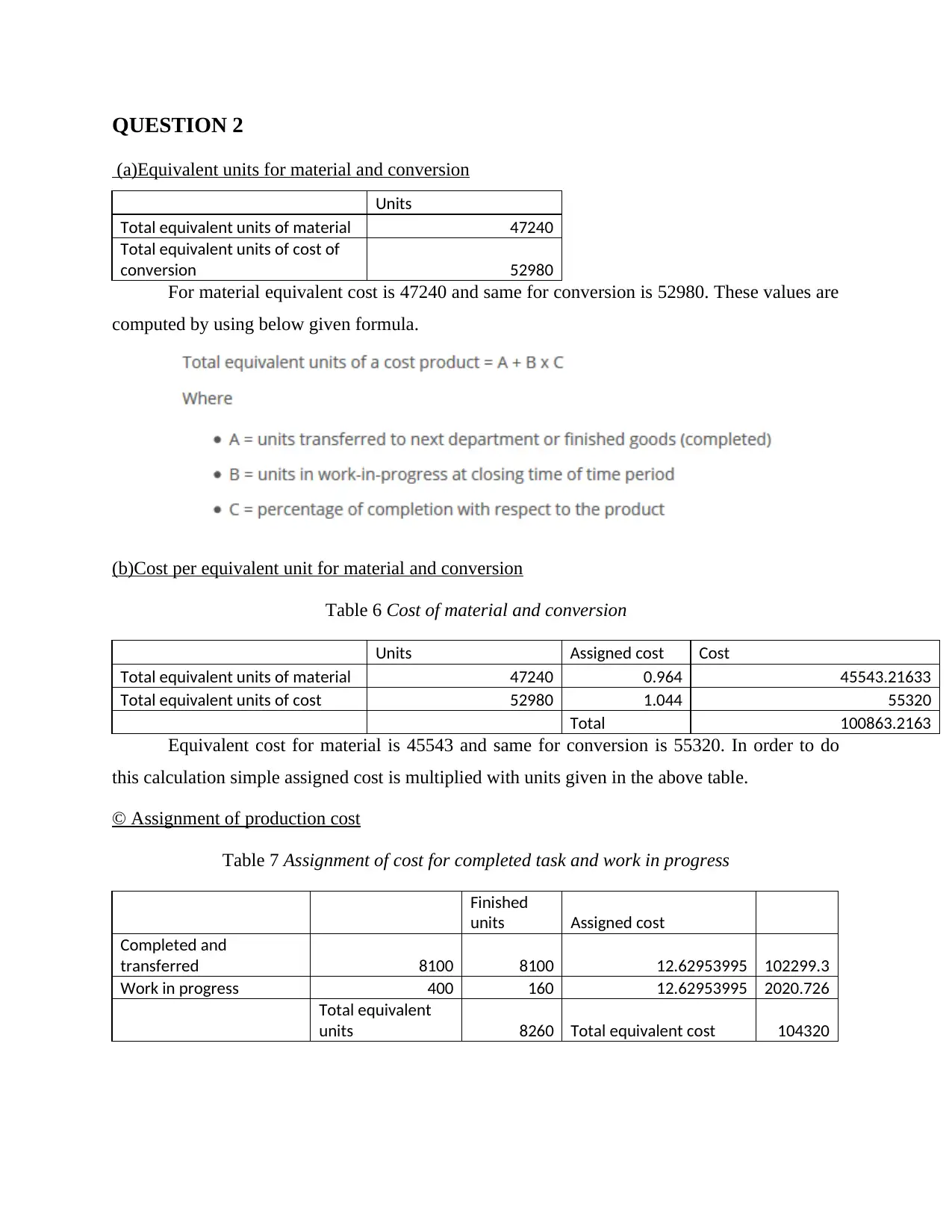

(a)Equivalent units for material and conversion..........................................................................9

(b)Cost per equivalent unit for material and conversion.............................................................9

© Assignment of production cost................................................................................................9

(d)Weighted average unit cost of leather belts completed and transferred to finished goods...10

(2) Comment of the cost per belt of 11.50 which firm used for planning and control..............10

QUESTION 3................................................................................................................................10

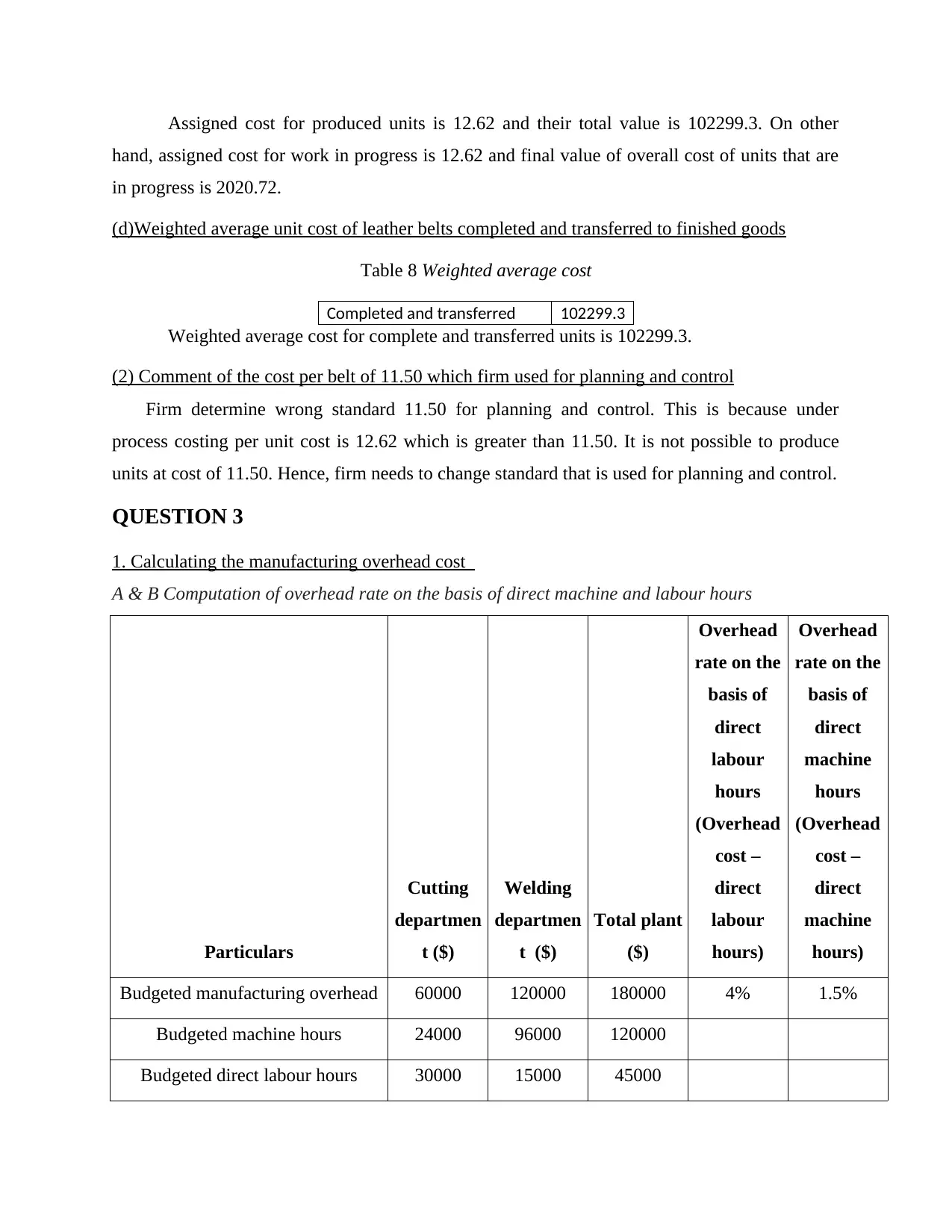

1. Calculating the manufacturing overhead cost........................................................................10

2. Stating the overhead estimation which is highly true............................................................11

3. Calculating actual manufacturing overhead cost...................................................................11

Actual cost.................................................................................................................................12

4. Estimating the cost of overhead which is more accurate.......................................................12

QUESTION 4................................................................................................................................12

1. Calculation of the activity rates.............................................................................................12

2. Using activity based costing to prepare the wages and salary as well as business tax return

...................................................................................................................................................13

3. Evaluating the pricing policy which is used by the firm.......................................................14

Question 5......................................................................................................................................14

(1)Scheduled budgeted cash receipts.........................................................................................14

(2)Budgeted P&L statement for month of December................................................................14

(3)Balance in account payable on 31st December......................................................................14

QUESTION 6................................................................................................................................15

1. Using direct method to reallocate the budgeted cost.............................................................15

QUESTION 1..................................................................................................................................4

(1)Scatter diagram of administrative cost and patients load during first year of operations.......4

(2) High low method of management accounting for forecast....................................................4

(3) Prediction of administrative cost when 800 patients visit the hospital..................................5

(4) Regression analysis................................................................................................................5

(5) Impact of emergency procedures on the administrative cost.................................................7

(6) Suitability of tools used for predicting value of the variable.................................................8

QUESTION 2..................................................................................................................................9

(a)Equivalent units for material and conversion..........................................................................9

(b)Cost per equivalent unit for material and conversion.............................................................9

© Assignment of production cost................................................................................................9

(d)Weighted average unit cost of leather belts completed and transferred to finished goods...10

(2) Comment of the cost per belt of 11.50 which firm used for planning and control..............10

QUESTION 3................................................................................................................................10

1. Calculating the manufacturing overhead cost........................................................................10

2. Stating the overhead estimation which is highly true............................................................11

3. Calculating actual manufacturing overhead cost...................................................................11

Actual cost.................................................................................................................................12

4. Estimating the cost of overhead which is more accurate.......................................................12

QUESTION 4................................................................................................................................12

1. Calculation of the activity rates.............................................................................................12

2. Using activity based costing to prepare the wages and salary as well as business tax return

...................................................................................................................................................13

3. Evaluating the pricing policy which is used by the firm.......................................................14

Question 5......................................................................................................................................14

(1)Scheduled budgeted cash receipts.........................................................................................14

(2)Budgeted P&L statement for month of December................................................................14

(3)Balance in account payable on 31st December......................................................................14

QUESTION 6................................................................................................................................15

1. Using direct method to reallocate the budgeted cost.............................................................15

2. Stating the reallocation of the cost of human resources and computing on the basis of step

down method.............................................................................................................................15

3. Using the reciprocal service method for the purpose of reallocation....................................16

Question 7......................................................................................................................................17

(1)Objective function and constraints........................................................................................18

(2) Graph on constraints of Madras curry kitchen meal preparation process............................18

(3) Number of units to be produced to achieve objective..........................................................19

(4) Value of Madras curry kitchen contribution margin............................................................19

QUESTION 8................................................................................................................................19

1. Preparing a cost quality report for model ABC.....................................................................19

2. Commenting on the quality cost performance.......................................................................19

Table 1Variables used in calculation in high low method...............................................................4

Table 2Calculation of cost...............................................................................................................4

Table 3Regression statistics.............................................................................................................7

Table 4ANNOVA table...................................................................................................................8

Table 5 Coefficient table.................................................................................................................8

Table 6 Cost of material and conversion.........................................................................................9

Table 7 Assignment of cost for completed task and work in progress............................................9

Table 8 Weighted average cost......................................................................................................10

Table 9Computation of actual overhead rate.................................................................................11

Table 10Cash receipts of business firm in the month of December..............................................14

Table 11Income statement.............................................................................................................14

Table 12Account payable..............................................................................................................15

Table 13Values of HR and computing used for allocation............................................................16

Table 14Allocation by using step down method...........................................................................16

Table 15 LPP for Indian and Portuguese Cuisine..........................................................................17

Table 16Calculation for constraint 1.............................................................................................18

Table 17 Calculation for constraint 2............................................................................................18

Table 18 Computation for constraint 3..........................................................................................18

down method.............................................................................................................................15

3. Using the reciprocal service method for the purpose of reallocation....................................16

Question 7......................................................................................................................................17

(1)Objective function and constraints........................................................................................18

(2) Graph on constraints of Madras curry kitchen meal preparation process............................18

(3) Number of units to be produced to achieve objective..........................................................19

(4) Value of Madras curry kitchen contribution margin............................................................19

QUESTION 8................................................................................................................................19

1. Preparing a cost quality report for model ABC.....................................................................19

2. Commenting on the quality cost performance.......................................................................19

Table 1Variables used in calculation in high low method...............................................................4

Table 2Calculation of cost...............................................................................................................4

Table 3Regression statistics.............................................................................................................7

Table 4ANNOVA table...................................................................................................................8

Table 5 Coefficient table.................................................................................................................8

Table 6 Cost of material and conversion.........................................................................................9

Table 7 Assignment of cost for completed task and work in progress............................................9

Table 8 Weighted average cost......................................................................................................10

Table 9Computation of actual overhead rate.................................................................................11

Table 10Cash receipts of business firm in the month of December..............................................14

Table 11Income statement.............................................................................................................14

Table 12Account payable..............................................................................................................15

Table 13Values of HR and computing used for allocation............................................................16

Table 14Allocation by using step down method...........................................................................16

Table 15 LPP for Indian and Portuguese Cuisine..........................................................................17

Table 16Calculation for constraint 1.............................................................................................18

Table 17 Calculation for constraint 2............................................................................................18

Table 18 Computation for constraint 3..........................................................................................18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Figure 1Scatter diagram of patient load and administrative cost....................................................5

Figure 2Chart predicting administrative cost on the basis of patient load......................................6

Figure 3Equation for predicting the administrative cost on the basis of patient load.....................7

Figure 4Equation for patient load and chart....................................................................................8

Figure 5Charting on LPP...............................................................................................................20

Figure 2Chart predicting administrative cost on the basis of patient load......................................6

Figure 3Equation for predicting the administrative cost on the basis of patient load.....................7

Figure 4Equation for patient load and chart....................................................................................8

Figure 5Charting on LPP...............................................................................................................20

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QUESTION 1

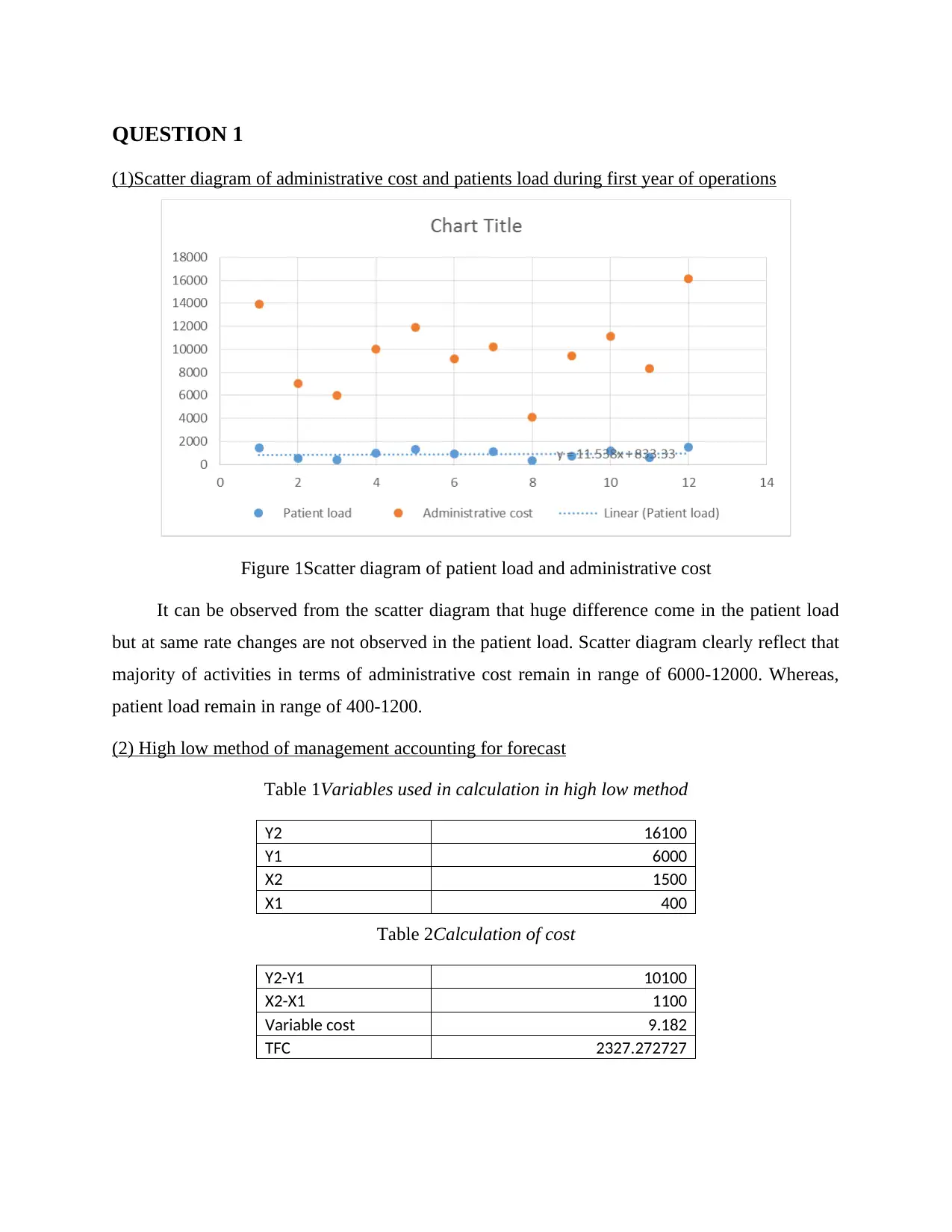

(1)Scatter diagram of administrative cost and patients load during first year of operations

Figure 1Scatter diagram of patient load and administrative cost

It can be observed from the scatter diagram that huge difference come in the patient load

but at same rate changes are not observed in the patient load. Scatter diagram clearly reflect that

majority of activities in terms of administrative cost remain in range of 6000-12000. Whereas,

patient load remain in range of 400-1200.

(2) High low method of management accounting for forecast

Table 1Variables used in calculation in high low method

Y2 16100

Y1 6000

X2 1500

X1 400

Table 2Calculation of cost

Y2-Y1 10100

X2-X1 1100

Variable cost 9.182

TFC 2327.272727

(1)Scatter diagram of administrative cost and patients load during first year of operations

Figure 1Scatter diagram of patient load and administrative cost

It can be observed from the scatter diagram that huge difference come in the patient load

but at same rate changes are not observed in the patient load. Scatter diagram clearly reflect that

majority of activities in terms of administrative cost remain in range of 6000-12000. Whereas,

patient load remain in range of 400-1200.

(2) High low method of management accounting for forecast

Table 1Variables used in calculation in high low method

Y2 16100

Y1 6000

X2 1500

X1 400

Table 2Calculation of cost

Y2-Y1 10100

X2-X1 1100

Variable cost 9.182

TFC 2327.272727

On the basis of high low method it is identified that variable cost for each patient load is 9.182

and fixed cost for same is 2327. This is computed by considering cost of high and low range of

business activities. Equation used in entire calculation is given below.

Variable cost= Y2-Y1/X2-X1

TFC= Y2-bX2

(3) Prediction of administrative cost when 800 patients visit the hospital

Regression equation in the above given scatter diagram is y=11538x+833.33. In order to

predict administrative cost on the basis of this equation number of patients that are expected to

arrive in the hospital are taken in to consideration. Hence, y= 11538*800+833.33 which means

y=10063. Thus, it is clear that administrative cost for 800 patients in the hospital will be 10063.

(4) Regression analysis

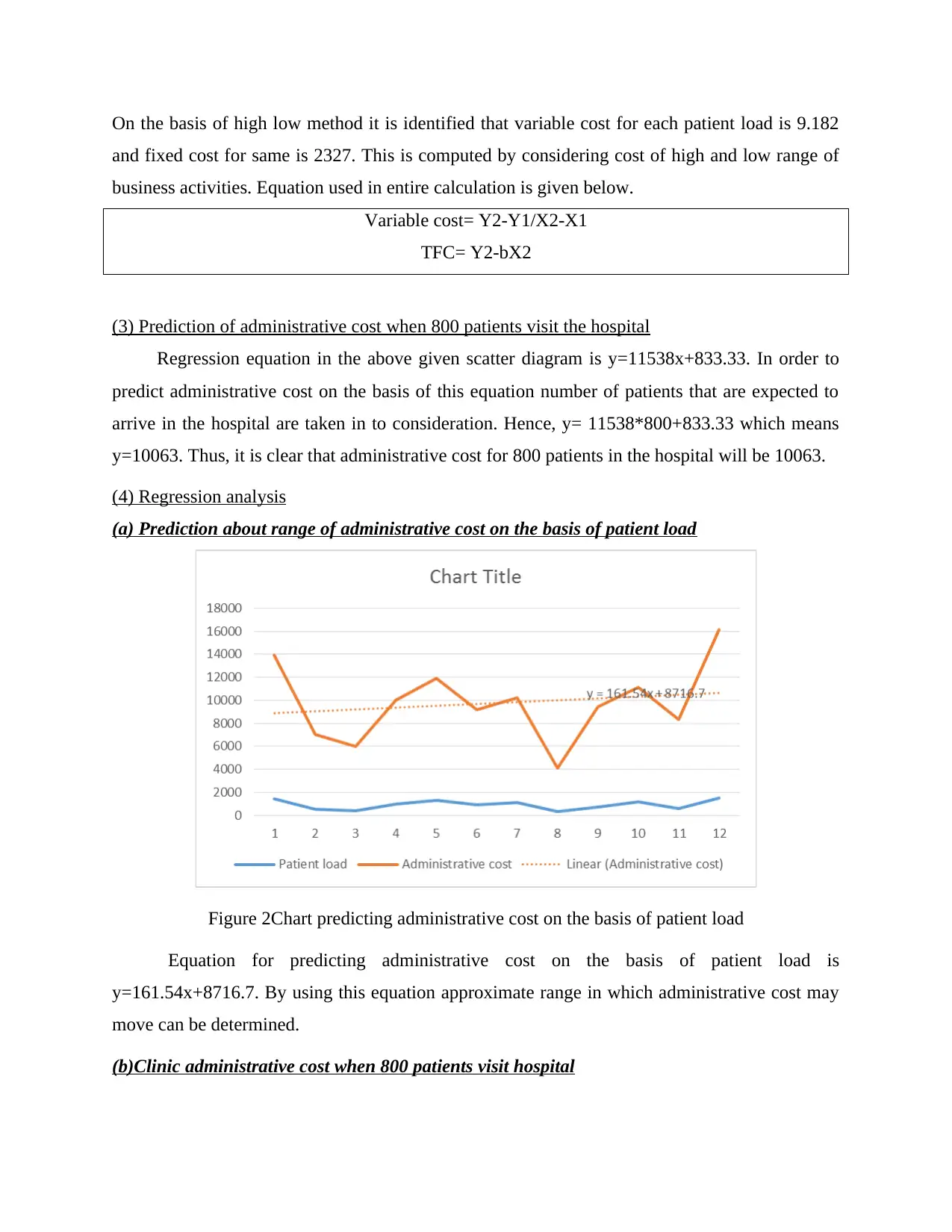

(a) Prediction about range of administrative cost on the basis of patient load

Figure 2Chart predicting administrative cost on the basis of patient load

Equation for predicting administrative cost on the basis of patient load is

y=161.54x+8716.7. By using this equation approximate range in which administrative cost may

move can be determined.

(b)Clinic administrative cost when 800 patients visit hospital

and fixed cost for same is 2327. This is computed by considering cost of high and low range of

business activities. Equation used in entire calculation is given below.

Variable cost= Y2-Y1/X2-X1

TFC= Y2-bX2

(3) Prediction of administrative cost when 800 patients visit the hospital

Regression equation in the above given scatter diagram is y=11538x+833.33. In order to

predict administrative cost on the basis of this equation number of patients that are expected to

arrive in the hospital are taken in to consideration. Hence, y= 11538*800+833.33 which means

y=10063. Thus, it is clear that administrative cost for 800 patients in the hospital will be 10063.

(4) Regression analysis

(a) Prediction about range of administrative cost on the basis of patient load

Figure 2Chart predicting administrative cost on the basis of patient load

Equation for predicting administrative cost on the basis of patient load is

y=161.54x+8716.7. By using this equation approximate range in which administrative cost may

move can be determined.

(b)Clinic administrative cost when 800 patients visit hospital

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

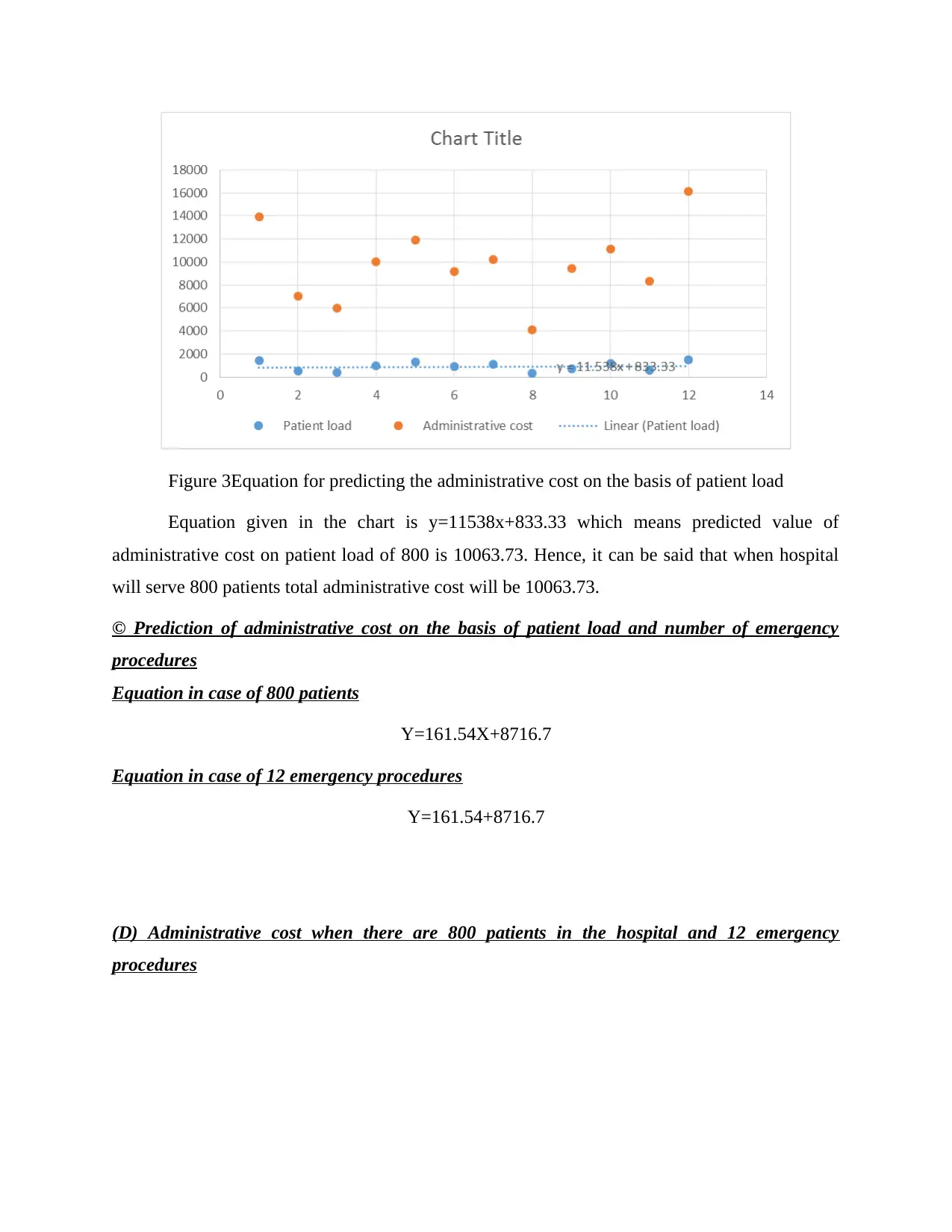

Figure 3Equation for predicting the administrative cost on the basis of patient load

Equation given in the chart is y=11538x+833.33 which means predicted value of

administrative cost on patient load of 800 is 10063.73. Hence, it can be said that when hospital

will serve 800 patients total administrative cost will be 10063.73.

© Prediction of administrative cost on the basis of patient load and number of emergency

procedures

Equation in case of 800 patients

Y=161.54X+8716.7

Equation in case of 12 emergency procedures

Y=161.54+8716.7

(D) Administrative cost when there are 800 patients in the hospital and 12 emergency

procedures

Equation given in the chart is y=11538x+833.33 which means predicted value of

administrative cost on patient load of 800 is 10063.73. Hence, it can be said that when hospital

will serve 800 patients total administrative cost will be 10063.73.

© Prediction of administrative cost on the basis of patient load and number of emergency

procedures

Equation in case of 800 patients

Y=161.54X+8716.7

Equation in case of 12 emergency procedures

Y=161.54+8716.7

(D) Administrative cost when there are 800 patients in the hospital and 12 emergency

procedures

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

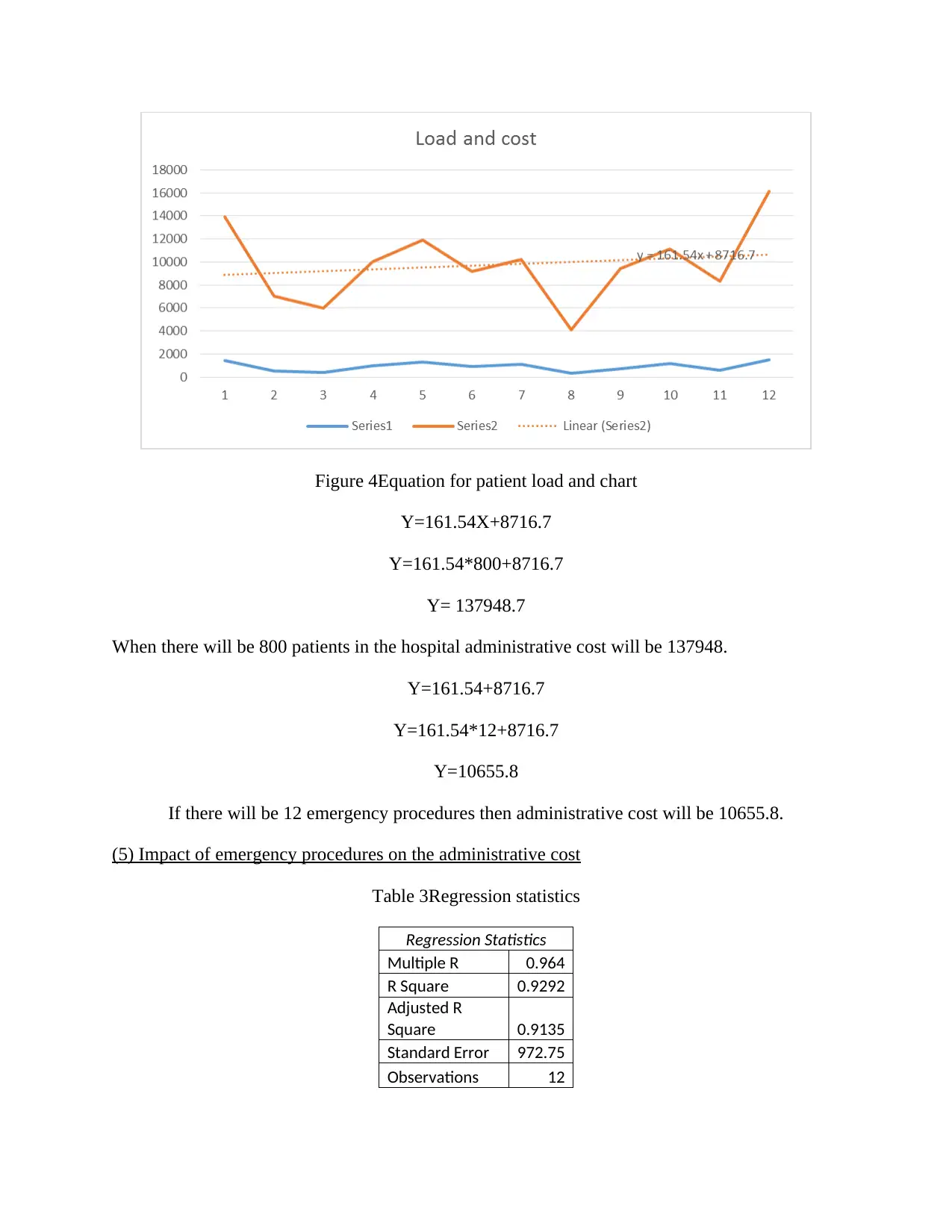

Figure 4Equation for patient load and chart

Y=161.54X+8716.7

Y=161.54*800+8716.7

Y= 137948.7

When there will be 800 patients in the hospital administrative cost will be 137948.

Y=161.54+8716.7

Y=161.54*12+8716.7

Y=10655.8

If there will be 12 emergency procedures then administrative cost will be 10655.8.

(5) Impact of emergency procedures on the administrative cost

Table 3Regression statistics

Regression Statistics

Multiple R 0.964

R Square 0.9292

Adjusted R

Square 0.9135

Standard Error 972.75

Observations 12

Y=161.54X+8716.7

Y=161.54*800+8716.7

Y= 137948.7

When there will be 800 patients in the hospital administrative cost will be 137948.

Y=161.54+8716.7

Y=161.54*12+8716.7

Y=10655.8

If there will be 12 emergency procedures then administrative cost will be 10655.8.

(5) Impact of emergency procedures on the administrative cost

Table 3Regression statistics

Regression Statistics

Multiple R 0.964

R Square 0.9292

Adjusted R

Square 0.9135

Standard Error 972.75

Observations 12

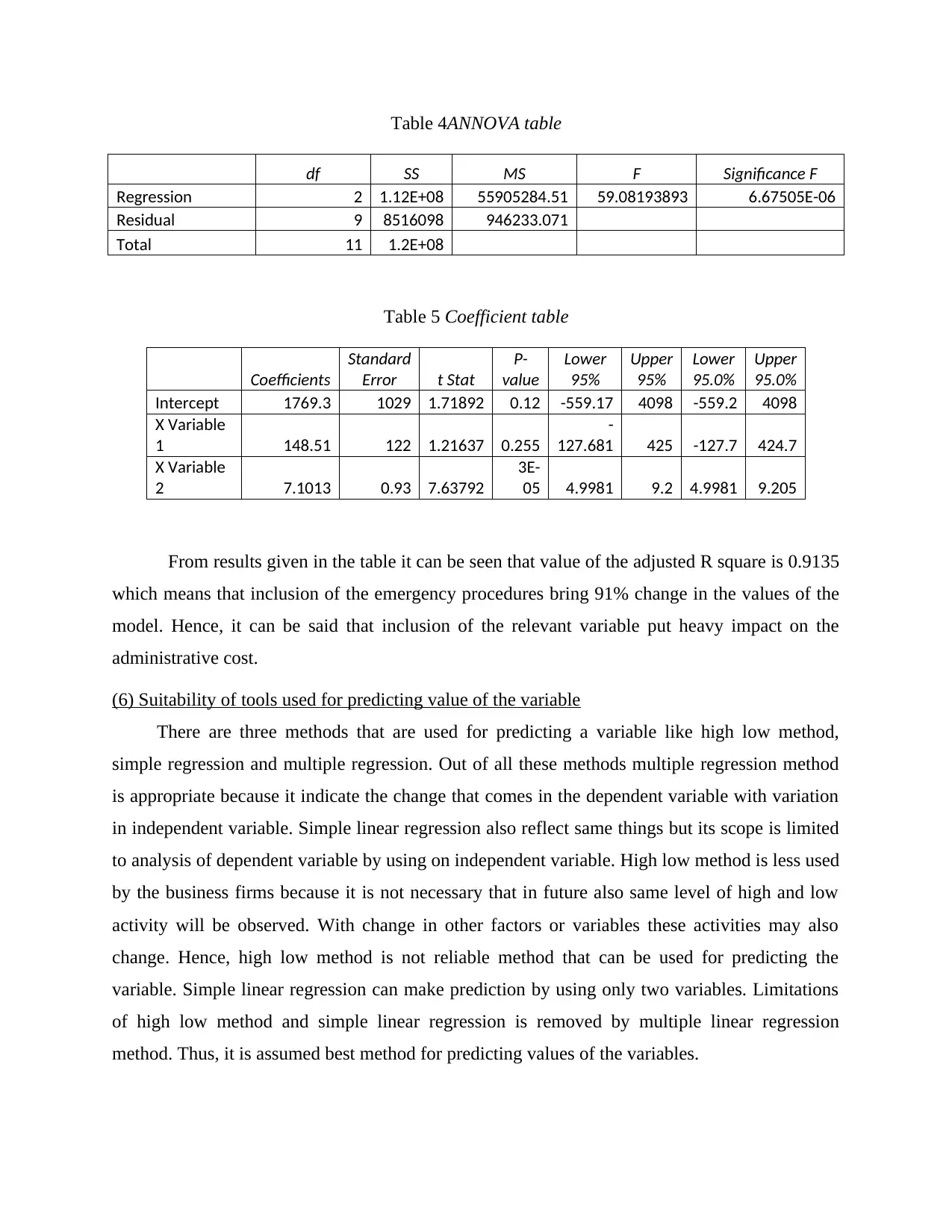

Table 4ANNOVA table

df SS MS F Significance F

Regression 2 1.12E+08 55905284.51 59.08193893 6.67505E-06

Residual 9 8516098 946233.071

Total 11 1.2E+08

Table 5 Coefficient table

Coefficients

Standard

Error t Stat

P-

value

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept 1769.3 1029 1.71892 0.12 -559.17 4098 -559.2 4098

X Variable

1 148.51 122 1.21637 0.255

-

127.681 425 -127.7 424.7

X Variable

2 7.1013 0.93 7.63792

3E-

05 4.9981 9.2 4.9981 9.205

From results given in the table it can be seen that value of the adjusted R square is 0.9135

which means that inclusion of the emergency procedures bring 91% change in the values of the

model. Hence, it can be said that inclusion of the relevant variable put heavy impact on the

administrative cost.

(6) Suitability of tools used for predicting value of the variable

There are three methods that are used for predicting a variable like high low method,

simple regression and multiple regression. Out of all these methods multiple regression method

is appropriate because it indicate the change that comes in the dependent variable with variation

in independent variable. Simple linear regression also reflect same things but its scope is limited

to analysis of dependent variable by using on independent variable. High low method is less used

by the business firms because it is not necessary that in future also same level of high and low

activity will be observed. With change in other factors or variables these activities may also

change. Hence, high low method is not reliable method that can be used for predicting the

variable. Simple linear regression can make prediction by using only two variables. Limitations

of high low method and simple linear regression is removed by multiple linear regression

method. Thus, it is assumed best method for predicting values of the variables.

df SS MS F Significance F

Regression 2 1.12E+08 55905284.51 59.08193893 6.67505E-06

Residual 9 8516098 946233.071

Total 11 1.2E+08

Table 5 Coefficient table

Coefficients

Standard

Error t Stat

P-

value

Lower

95%

Upper

95%

Lower

95.0%

Upper

95.0%

Intercept 1769.3 1029 1.71892 0.12 -559.17 4098 -559.2 4098

X Variable

1 148.51 122 1.21637 0.255

-

127.681 425 -127.7 424.7

X Variable

2 7.1013 0.93 7.63792

3E-

05 4.9981 9.2 4.9981 9.205

From results given in the table it can be seen that value of the adjusted R square is 0.9135

which means that inclusion of the emergency procedures bring 91% change in the values of the

model. Hence, it can be said that inclusion of the relevant variable put heavy impact on the

administrative cost.

(6) Suitability of tools used for predicting value of the variable

There are three methods that are used for predicting a variable like high low method,

simple regression and multiple regression. Out of all these methods multiple regression method

is appropriate because it indicate the change that comes in the dependent variable with variation

in independent variable. Simple linear regression also reflect same things but its scope is limited

to analysis of dependent variable by using on independent variable. High low method is less used

by the business firms because it is not necessary that in future also same level of high and low

activity will be observed. With change in other factors or variables these activities may also

change. Hence, high low method is not reliable method that can be used for predicting the

variable. Simple linear regression can make prediction by using only two variables. Limitations

of high low method and simple linear regression is removed by multiple linear regression

method. Thus, it is assumed best method for predicting values of the variables.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

QUESTION 2

(a)Equivalent units for material and conversion

Units

Total equivalent units of material 47240

Total equivalent units of cost of

conversion 52980

For material equivalent cost is 47240 and same for conversion is 52980. These values are

computed by using below given formula.

(b)Cost per equivalent unit for material and conversion

Table 6 Cost of material and conversion

Units Assigned cost Cost

Total equivalent units of material 47240 0.964 45543.21633

Total equivalent units of cost 52980 1.044 55320

Total 100863.2163

Equivalent cost for material is 45543 and same for conversion is 55320. In order to do

this calculation simple assigned cost is multiplied with units given in the above table.

© Assignment of production cost

Table 7 Assignment of cost for completed task and work in progress

Finished

units Assigned cost

Completed and

transferred 8100 8100 12.62953995 102299.3

Work in progress 400 160 12.62953995 2020.726

Total equivalent

units 8260 Total equivalent cost 104320

(a)Equivalent units for material and conversion

Units

Total equivalent units of material 47240

Total equivalent units of cost of

conversion 52980

For material equivalent cost is 47240 and same for conversion is 52980. These values are

computed by using below given formula.

(b)Cost per equivalent unit for material and conversion

Table 6 Cost of material and conversion

Units Assigned cost Cost

Total equivalent units of material 47240 0.964 45543.21633

Total equivalent units of cost 52980 1.044 55320

Total 100863.2163

Equivalent cost for material is 45543 and same for conversion is 55320. In order to do

this calculation simple assigned cost is multiplied with units given in the above table.

© Assignment of production cost

Table 7 Assignment of cost for completed task and work in progress

Finished

units Assigned cost

Completed and

transferred 8100 8100 12.62953995 102299.3

Work in progress 400 160 12.62953995 2020.726

Total equivalent

units 8260 Total equivalent cost 104320

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Assigned cost for produced units is 12.62 and their total value is 102299.3. On other

hand, assigned cost for work in progress is 12.62 and final value of overall cost of units that are

in progress is 2020.72.

(d)Weighted average unit cost of leather belts completed and transferred to finished goods

Table 8 Weighted average cost

Completed and transferred 102299.3

Weighted average cost for complete and transferred units is 102299.3.

(2) Comment of the cost per belt of 11.50 which firm used for planning and control

Firm determine wrong standard 11.50 for planning and control. This is because under

process costing per unit cost is 12.62 which is greater than 11.50. It is not possible to produce

units at cost of 11.50. Hence, firm needs to change standard that is used for planning and control.

QUESTION 3

1. Calculating the manufacturing overhead cost

A & B Computation of overhead rate on the basis of direct machine and labour hours

Particulars

Cutting

departmen

t ($)

Welding

departmen

t ($)

Total plant

($)

Overhead

rate on the

basis of

direct

labour

hours

(Overhead

cost –

direct

labour

hours)

Overhead

rate on the

basis of

direct

machine

hours

(Overhead

cost –

direct

machine

hours)

Budgeted manufacturing overhead 60000 120000 180000 4% 1.5%

Budgeted machine hours 24000 96000 120000

Budgeted direct labour hours 30000 15000 45000

hand, assigned cost for work in progress is 12.62 and final value of overall cost of units that are

in progress is 2020.72.

(d)Weighted average unit cost of leather belts completed and transferred to finished goods

Table 8 Weighted average cost

Completed and transferred 102299.3

Weighted average cost for complete and transferred units is 102299.3.

(2) Comment of the cost per belt of 11.50 which firm used for planning and control

Firm determine wrong standard 11.50 for planning and control. This is because under

process costing per unit cost is 12.62 which is greater than 11.50. It is not possible to produce

units at cost of 11.50. Hence, firm needs to change standard that is used for planning and control.

QUESTION 3

1. Calculating the manufacturing overhead cost

A & B Computation of overhead rate on the basis of direct machine and labour hours

Particulars

Cutting

departmen

t ($)

Welding

departmen

t ($)

Total plant

($)

Overhead

rate on the

basis of

direct

labour

hours

(Overhead

cost –

direct

labour

hours)

Overhead

rate on the

basis of

direct

machine

hours

(Overhead

cost –

direct

machine

hours)

Budgeted manufacturing overhead 60000 120000 180000 4% 1.5%

Budgeted machine hours 24000 96000 120000

Budgeted direct labour hours 30000 15000 45000

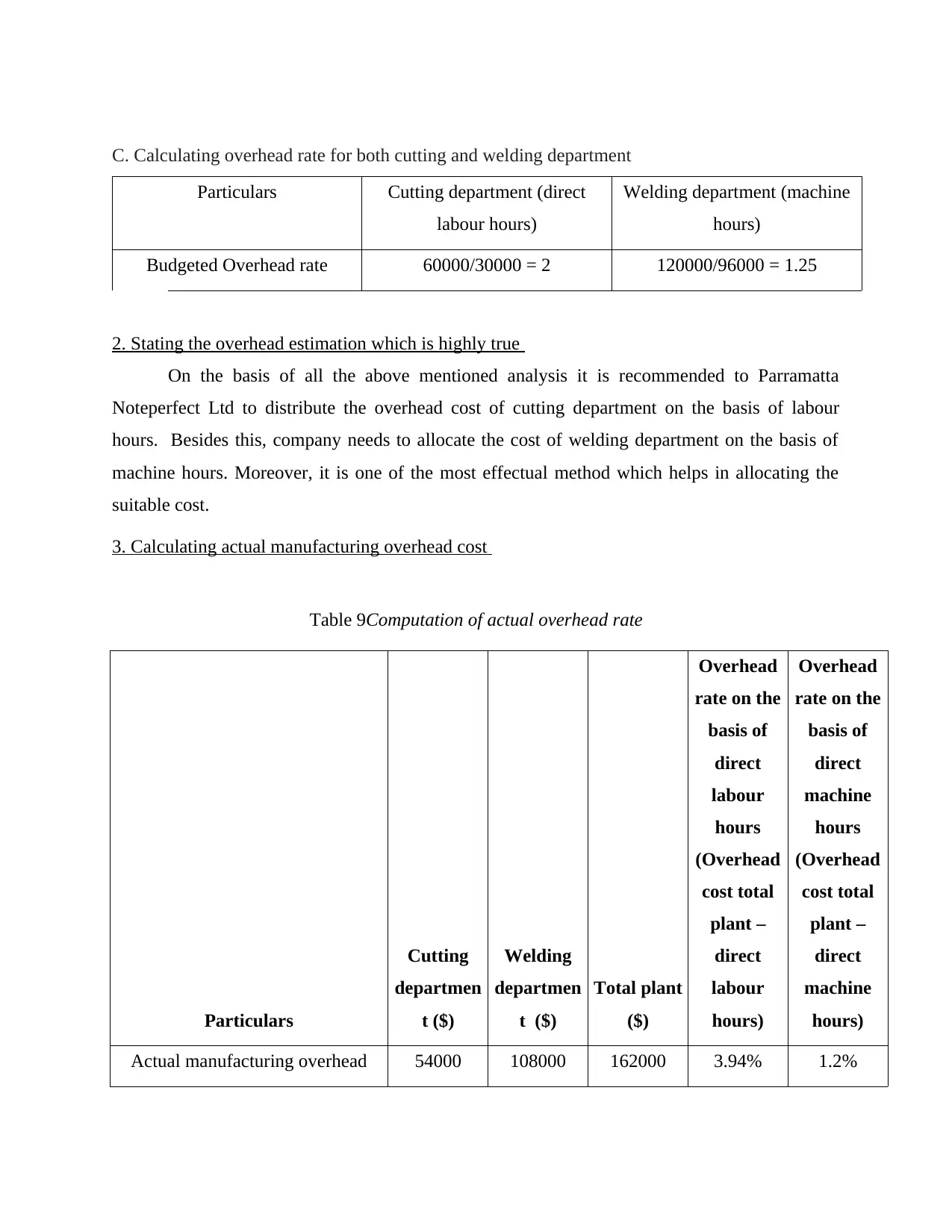

C. Calculating overhead rate for both cutting and welding department

Particulars Cutting department (direct

labour hours)

Welding department (machine

hours)

Budgeted Overhead rate 60000/30000 = 2 120000/96000 = 1.25

2. Stating the overhead estimation which is highly true

On the basis of all the above mentioned analysis it is recommended to Parramatta

Noteperfect Ltd to distribute the overhead cost of cutting department on the basis of labour

hours. Besides this, company needs to allocate the cost of welding department on the basis of

machine hours. Moreover, it is one of the most effectual method which helps in allocating the

suitable cost.

3. Calculating actual manufacturing overhead cost

Table 9Computation of actual overhead rate

Particulars

Cutting

departmen

t ($)

Welding

departmen

t ($)

Total plant

($)

Overhead

rate on the

basis of

direct

labour

hours

(Overhead

cost total

plant –

direct

labour

hours)

Overhead

rate on the

basis of

direct

machine

hours

(Overhead

cost total

plant –

direct

machine

hours)

Actual manufacturing overhead 54000 108000 162000 3.94% 1.2%

Particulars Cutting department (direct

labour hours)

Welding department (machine

hours)

Budgeted Overhead rate 60000/30000 = 2 120000/96000 = 1.25

2. Stating the overhead estimation which is highly true

On the basis of all the above mentioned analysis it is recommended to Parramatta

Noteperfect Ltd to distribute the overhead cost of cutting department on the basis of labour

hours. Besides this, company needs to allocate the cost of welding department on the basis of

machine hours. Moreover, it is one of the most effectual method which helps in allocating the

suitable cost.

3. Calculating actual manufacturing overhead cost

Table 9Computation of actual overhead rate

Particulars

Cutting

departmen

t ($)

Welding

departmen

t ($)

Total plant

($)

Overhead

rate on the

basis of

direct

labour

hours

(Overhead

cost total

plant –

direct

labour

hours)

Overhead

rate on the

basis of

direct

machine

hours

(Overhead

cost total

plant –

direct

machine

hours)

Actual manufacturing overhead 54000 108000 162000 3.94% 1.2%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.