Management Accounting Report: Excite Entertainment Ltd Analysis

VerifiedAdded on 2020/10/23

|18

|4921

|480

Report

AI Summary

This report provides a comprehensive analysis of management accounting principles, focusing on their application within Excite Entertainment Ltd, a company operating in the entertainment and leisure industry. It begins by defining management accounting, differentiating it from financial accounting, and outlining the essential requirements of various management accounting systems, including cost accounting and inventory management systems. The report delves into different methods used for management accounting reporting, such as budget reports, accounts receivable aging reports, and performance reports. It then demonstrates the calculation of costs using techniques of cost analysis, specifically marginal and absorption costing, to prepare an income statement. The report also discusses the advantages and disadvantages of different planning tools used for budgetary control and concludes with a comparison of how Excite Entertainment Ltd adapts management accounting systems to respond to financial problems. The report aims to provide a practical understanding of management accounting and its role in business decision-making.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

LO1..................................................................................................................................................1

P1 Management accounting and essential requirements of different types of management

accounting systems......................................................................................................................1

P2 Different methods used for management accounting reporting............................................4

LO2..................................................................................................................................................6

P3 Calculate costs using techniques of cost analysis to prepare an income statement using

marginal and absorption costs......................................................................................................6

LO3..................................................................................................................................................8

P4 The advantages and disadvantages of different types of planning tools used for budgetary

control..........................................................................................................................................8

LO4................................................................................................................................................11

P5 Excite Entertainment Ltd are adapting management accounting systems to respond to

financial problems......................................................................................................................11

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................1

LO1..................................................................................................................................................1

P1 Management accounting and essential requirements of different types of management

accounting systems......................................................................................................................1

P2 Different methods used for management accounting reporting............................................4

LO2..................................................................................................................................................6

P3 Calculate costs using techniques of cost analysis to prepare an income statement using

marginal and absorption costs......................................................................................................6

LO3..................................................................................................................................................8

P4 The advantages and disadvantages of different types of planning tools used for budgetary

control..........................................................................................................................................8

LO4................................................................................................................................................11

P5 Excite Entertainment Ltd are adapting management accounting systems to respond to

financial problems......................................................................................................................11

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

Management accounting is a process which analyses cost of business and operations in

order to prepare internal financial report to help managers in decision making and to achieve

their goals of business (Firk, Schrapp, and Wolff, 2016). In this report Excite Entertainment Ltd.

Company is taken for better understanding. Excite Entertainment Ltd is a company which

operates in entertainment and leisure industry in the country UK. The activity of promotion of

concerts and festivals emphasis on Management accounting and financial accounting. The

difference between both accounting will also explain in this report. The report will also

discussing about different methods used for management accounting report. Also, a calculation

based on appropriate techniques of cost analysis in order to prepare an income statement by the

use of absorption and marginal costing will be highlighted in this report. The advantages and

disadvantages on different types of tools for planning which is used for budgetary control will be

discussed in this report. A comparison on adapting management accounting system by Excite

Entertainment Ltd to respond financial problems will be discussed in the report.

LO1

P1 Management accounting and essential requirements of different types of management

accounting systems.

Management accounting

“The management accounting includes the concept and methods which are necessary for

planning in effective manner and to choose the best alternative action of business and also

control by the interpretation and evaluation of performance.”

Financial accounting

“It is a that specialized accounting branch which keeps on track of financial transactions

of a company. The transactions are firstly recording then summarized and at last presented in

financial statement or report which are Balance sheet or income statement.”

Difference between management accounting and financial accounting

Basis MANAGEMENT ACCOUNTING FINANCIAL ACCOUNTING

Legal

requirement

The reports are used internally in

the organisation and they does not

need any legal requirement.

The rules which are in financial

accounting prescribed by

Generally accepted accounting

1

Management accounting is a process which analyses cost of business and operations in

order to prepare internal financial report to help managers in decision making and to achieve

their goals of business (Firk, Schrapp, and Wolff, 2016). In this report Excite Entertainment Ltd.

Company is taken for better understanding. Excite Entertainment Ltd is a company which

operates in entertainment and leisure industry in the country UK. The activity of promotion of

concerts and festivals emphasis on Management accounting and financial accounting. The

difference between both accounting will also explain in this report. The report will also

discussing about different methods used for management accounting report. Also, a calculation

based on appropriate techniques of cost analysis in order to prepare an income statement by the

use of absorption and marginal costing will be highlighted in this report. The advantages and

disadvantages on different types of tools for planning which is used for budgetary control will be

discussed in this report. A comparison on adapting management accounting system by Excite

Entertainment Ltd to respond financial problems will be discussed in the report.

LO1

P1 Management accounting and essential requirements of different types of management

accounting systems.

Management accounting

“The management accounting includes the concept and methods which are necessary for

planning in effective manner and to choose the best alternative action of business and also

control by the interpretation and evaluation of performance.”

Financial accounting

“It is a that specialized accounting branch which keeps on track of financial transactions

of a company. The transactions are firstly recording then summarized and at last presented in

financial statement or report which are Balance sheet or income statement.”

Difference between management accounting and financial accounting

Basis MANAGEMENT ACCOUNTING FINANCIAL ACCOUNTING

Legal

requirement

The reports are used internally in

the organisation and they does not

need any legal requirement.

The rules which are in financial

accounting prescribed by

Generally accepted accounting

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

principles and International

financial reporting standard

Standards. Legal requirement are

there in financial accounting for

the companies like company

Excite entertainment follows these

legal requirements.

Format of

presentation

The management accounting

does not follow any format for

presentation of management

information.

The financial accounting in Excite

entertainment Ltd follows a

specific format for recording and

presenting information.

Area of

coverage within

the

organisation

Management accounting is

concerned with specific area for

analysis. The area may vary from

geography, product line,

manufacturing unit, etc.

The financial accounting is

concerned with business as a

whole. Accounting standards

bound the organisations to

reporting in area in set formats.

Type of data

used

In management accounting

quantitative data as well as

qualitative data is used.

In financial accounting only

quantitative data of Excite

Entertainment Ltd is used.

Cost accounting systems – It is a framework which is used by different firms in order to estimate

cost of products for analysis of profitability, cost control and valuation of inventory. Cost

accounting system works through tracking of raw materials by going through stages of

production and turns slowly into finish goods (Janin, 2017). The accounting entry in Excite

Entertainment Ltd for whenever raw material put to production this system of cost accounting

records immediately use of materials through crediting raw material account and debit goods in

process account.

Direct cost is one of the type of cost which is related with production of goods and

services. It includes labour, distribution cost which is associated with product while production,

cost of materials used in production, direct expenses. This cost is easily traced by a project,

2

financial reporting standard

Standards. Legal requirement are

there in financial accounting for

the companies like company

Excite entertainment follows these

legal requirements.

Format of

presentation

The management accounting

does not follow any format for

presentation of management

information.

The financial accounting in Excite

entertainment Ltd follows a

specific format for recording and

presenting information.

Area of

coverage within

the

organisation

Management accounting is

concerned with specific area for

analysis. The area may vary from

geography, product line,

manufacturing unit, etc.

The financial accounting is

concerned with business as a

whole. Accounting standards

bound the organisations to

reporting in area in set formats.

Type of data

used

In management accounting

quantitative data as well as

qualitative data is used.

In financial accounting only

quantitative data of Excite

Entertainment Ltd is used.

Cost accounting systems – It is a framework which is used by different firms in order to estimate

cost of products for analysis of profitability, cost control and valuation of inventory. Cost

accounting system works through tracking of raw materials by going through stages of

production and turns slowly into finish goods (Janin, 2017). The accounting entry in Excite

Entertainment Ltd for whenever raw material put to production this system of cost accounting

records immediately use of materials through crediting raw material account and debit goods in

process account.

Direct cost is one of the type of cost which is related with production of goods and

services. It includes labour, distribution cost which is associated with product while production,

cost of materials used in production, direct expenses. This cost is easily traced by a project,

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

department or a product. In addition to direct cost derive inventory value and is not allowed

under International financial reporting standard (IFRS) and Generally accepted accounting

principles (GAAP) so that it did not provide a view to which the cost are incurred while creating

of product or promoting activities of Excite Entertainment Ltd.

Accounting standard cost is a cost which is occurred by evaluating the difference

between actual cost and budgeted cost. This type of accounting executes comparison between

actual cost of goods that are used in production and cost that estimated for production of goods.

The inventory ledger accounts and cost of goods sold contains standard cost. The standard cost

and actual cost is considered as variances and accounting standard cost uses these variances for

their outcomes.

Different types of costing techniques for ascertaining costs are :

Uniform costing – This technique of costing uses the same principles and practices of

costing by undertaking several times for comparison of costs or common control (Chen,

Delmas, and Lieberman, 2015).

Marginal costing – This costing technique is ascertained by differentiating between

variable and fixed cost. This cost is useful to ascertain the changes effect in type of

volume of output basically on profit.

Standard costing – This technique of costing is ascertained by comparing actual cost

with pre determined standard cost. The difference between them is their deviation and

also called variance. This enables the management to investigate reasons for variances

and to take corrective suitable action for them.

Historical costing – This cost is ascertained after they have incurred. This technique of

costing aim at ascertaining cost which is actually incurred on work which is done in past.

Direct costing – This technique of costing is charging all direct cost, fixed and variable

cost relating to process, operation and products which leave all other cost to be written

off against profit which they have arise. Absorption costing – This costing technique consists all cost which includes fixed and

variable costs to process and operate.

Inventory management systems – It track inventories through supply chain or the portion of

their business operates. Inventory management system includes retail to production, shipping to

3

under International financial reporting standard (IFRS) and Generally accepted accounting

principles (GAAP) so that it did not provide a view to which the cost are incurred while creating

of product or promoting activities of Excite Entertainment Ltd.

Accounting standard cost is a cost which is occurred by evaluating the difference

between actual cost and budgeted cost. This type of accounting executes comparison between

actual cost of goods that are used in production and cost that estimated for production of goods.

The inventory ledger accounts and cost of goods sold contains standard cost. The standard cost

and actual cost is considered as variances and accounting standard cost uses these variances for

their outcomes.

Different types of costing techniques for ascertaining costs are :

Uniform costing – This technique of costing uses the same principles and practices of

costing by undertaking several times for comparison of costs or common control (Chen,

Delmas, and Lieberman, 2015).

Marginal costing – This costing technique is ascertained by differentiating between

variable and fixed cost. This cost is useful to ascertain the changes effect in type of

volume of output basically on profit.

Standard costing – This technique of costing is ascertained by comparing actual cost

with pre determined standard cost. The difference between them is their deviation and

also called variance. This enables the management to investigate reasons for variances

and to take corrective suitable action for them.

Historical costing – This cost is ascertained after they have incurred. This technique of

costing aim at ascertaining cost which is actually incurred on work which is done in past.

Direct costing – This technique of costing is charging all direct cost, fixed and variable

cost relating to process, operation and products which leave all other cost to be written

off against profit which they have arise. Absorption costing – This costing technique consists all cost which includes fixed and

variable costs to process and operate.

Inventory management systems – It track inventories through supply chain or the portion of

their business operates. Inventory management system includes retail to production, shipping to

3

warehousing, etc. Inventory management is supervision of inventories and items of stocks

(Smith, 2017).

Different method of inventory management are FIFO, LIFO and Weighted average. The

FIFO (First in First out) is an accounting method which relies on assumption of cash flow which

removes cost from accounts of inventory from the time when it is purchased. Then comes LIFO

(Last in First out) is method which matches with most recent cost on income statement with

sales. Weighted Average cost is utilized to assign average cost of production of a product. This

method of inventory management assumes that a store sells all their inventories simultaneously.

Job costing systems – It involves the accumulation process of information which is associated

with cost along with specific job of production and service (Florio, and Leoni, 2017). There are

three kinds of information needed by job cost system, which is direct labour, overhead and direct

materials. This system is useful for determining accuracy of estimation of company's system.

P2 Different methods used for management accounting reporting.

Managerial reports are those reports which are generated by the managers in order to

produce such reports which help the company's internal users in aiding their decision making

(Liu, Wei, and Xie, 2016). These reports emphasizing the internal information which is received

through the financial accounting by the auditors , these reports are generally used by the

company for effective planning, organising, regulation, decision making and also helps in

measuring the performance of the internal staff of the company. it is the reports under the

managerial accounting which focusing on the providing information to the internal users.

There are different types of managerial reports prepared by the organisation and some of them

are :

Budget reports

These are the reports considered to be very critical in measuring the organisation

performance and budget reports general prepared on the basis of the different departments in

order to manage all the operational activities and functions of that particular department

effectively.

The budget reports helps the organisation in comparing their actual performance with the

projected so that they can take the corrective actions to eliminate the deviations in between the

both. All the income and expenses are managed according to the budgets and that what is

4

(Smith, 2017).

Different method of inventory management are FIFO, LIFO and Weighted average. The

FIFO (First in First out) is an accounting method which relies on assumption of cash flow which

removes cost from accounts of inventory from the time when it is purchased. Then comes LIFO

(Last in First out) is method which matches with most recent cost on income statement with

sales. Weighted Average cost is utilized to assign average cost of production of a product. This

method of inventory management assumes that a store sells all their inventories simultaneously.

Job costing systems – It involves the accumulation process of information which is associated

with cost along with specific job of production and service (Florio, and Leoni, 2017). There are

three kinds of information needed by job cost system, which is direct labour, overhead and direct

materials. This system is useful for determining accuracy of estimation of company's system.

P2 Different methods used for management accounting reporting.

Managerial reports are those reports which are generated by the managers in order to

produce such reports which help the company's internal users in aiding their decision making

(Liu, Wei, and Xie, 2016). These reports emphasizing the internal information which is received

through the financial accounting by the auditors , these reports are generally used by the

company for effective planning, organising, regulation, decision making and also helps in

measuring the performance of the internal staff of the company. it is the reports under the

managerial accounting which focusing on the providing information to the internal users.

There are different types of managerial reports prepared by the organisation and some of them

are :

Budget reports

These are the reports considered to be very critical in measuring the organisation

performance and budget reports general prepared on the basis of the different departments in

order to manage all the operational activities and functions of that particular department

effectively.

The budget reports helps the organisation in comparing their actual performance with the

projected so that they can take the corrective actions to eliminate the deviations in between the

both. All the income and expenses are managed according to the budgets and that what is

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

reports does by informing the internal users about the inflow and outflow of cash as well as the

deviations in their performance (Massaro, Dumay, and Garlatti, 2015).

Advantages:

It is effective is measuring the performance

It helps in taking the corrective measures

It leads the organisation in ascertaining the most probable risk

budget reports helps investors to decide for further investments based on their

performances.

Account receivables Ageing reports

It is the report made by the business if they are involved in the activity of the extending

credit (Holm, 2018). The amount which is being given as credit to the customers for the specific

time periods helps the mangers in identifying their defaulters who would not pay the money and

also helps in finding the issues in the complete process of collection by the company. The

reports helps the business s organisation to ascertain that if there are many numbers of defaulters

than they need to transfer to more tighter credit policies in the company . There is always bad

debts in the company's reports which they are need to write off .hence, the account retrievable

ageing reports helps in many ways to manager for altering and changing in their credit policies

and strategies.

Advantages:

It helps the managers and top level management in deciding and restructuring the credit

policies (Ross, 2017)

this will lead the organisation in ascertaining the collection period of the company

internal users can make good and effective decisions regarding extending credit.

Performance Reports

These are the reports which are prepared for reviewing and analysing the performance

of the company of each staff members in order to take decisions regarding their appraisals, and

other organisation need (Lukka, and Modell, 2017).

Large organisation also prepare different number of performance report for each of the

department in order to analyse their performance towards the direction of the projected

performance and goal. This will help the organisation' in making the right decisions and taking

5

deviations in their performance (Massaro, Dumay, and Garlatti, 2015).

Advantages:

It is effective is measuring the performance

It helps in taking the corrective measures

It leads the organisation in ascertaining the most probable risk

budget reports helps investors to decide for further investments based on their

performances.

Account receivables Ageing reports

It is the report made by the business if they are involved in the activity of the extending

credit (Holm, 2018). The amount which is being given as credit to the customers for the specific

time periods helps the mangers in identifying their defaulters who would not pay the money and

also helps in finding the issues in the complete process of collection by the company. The

reports helps the business s organisation to ascertain that if there are many numbers of defaulters

than they need to transfer to more tighter credit policies in the company . There is always bad

debts in the company's reports which they are need to write off .hence, the account retrievable

ageing reports helps in many ways to manager for altering and changing in their credit policies

and strategies.

Advantages:

It helps the managers and top level management in deciding and restructuring the credit

policies (Ross, 2017)

this will lead the organisation in ascertaining the collection period of the company

internal users can make good and effective decisions regarding extending credit.

Performance Reports

These are the reports which are prepared for reviewing and analysing the performance

of the company of each staff members in order to take decisions regarding their appraisals, and

other organisation need (Lukka, and Modell, 2017).

Large organisation also prepare different number of performance report for each of the

department in order to analyse their performance towards the direction of the projected

performance and goal. This will help the organisation' in making the right decisions and taking

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

corrective measures for eliminating the difference between the actual and projected

performance .

Advantages

It helps in making comparison between the actual and budgeted performance

This guide the organisation for making decisions regarding termination or promotion of

the employee

training and development programs are also implemented on the basis of analysing the

performances.

LO2

P3 Calculate costs using techniques of cost analysis to prepare an income statement using

marginal and absorption costs.

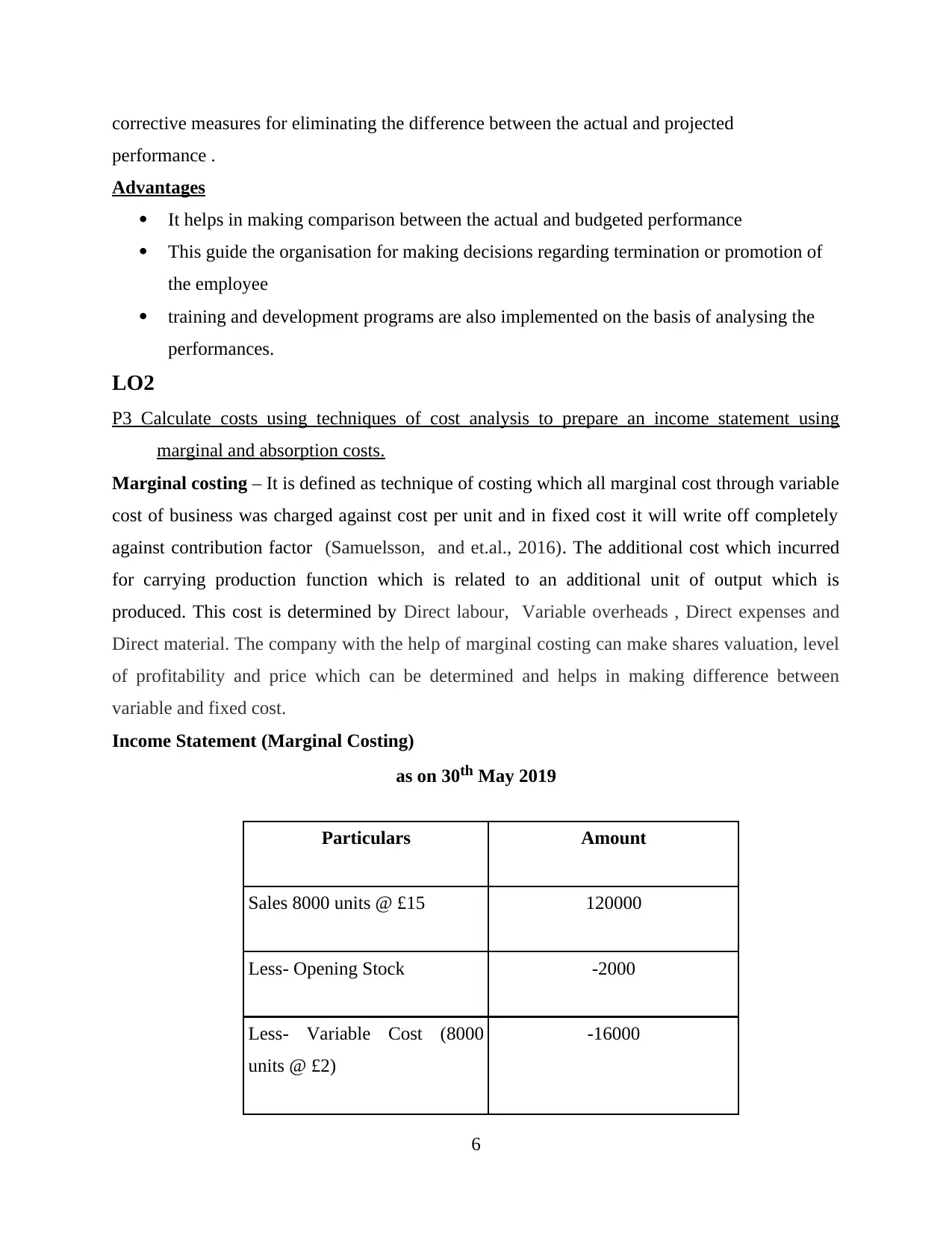

Marginal costing – It is defined as technique of costing which all marginal cost through variable

cost of business was charged against cost per unit and in fixed cost it will write off completely

against contribution factor (Samuelsson, and et.al., 2016). The additional cost which incurred

for carrying production function which is related to an additional unit of output which is

produced. This cost is determined by Direct labour, Variable overheads , Direct expenses and

Direct material. The company with the help of marginal costing can make shares valuation, level

of profitability and price which can be determined and helps in making difference between

variable and fixed cost.

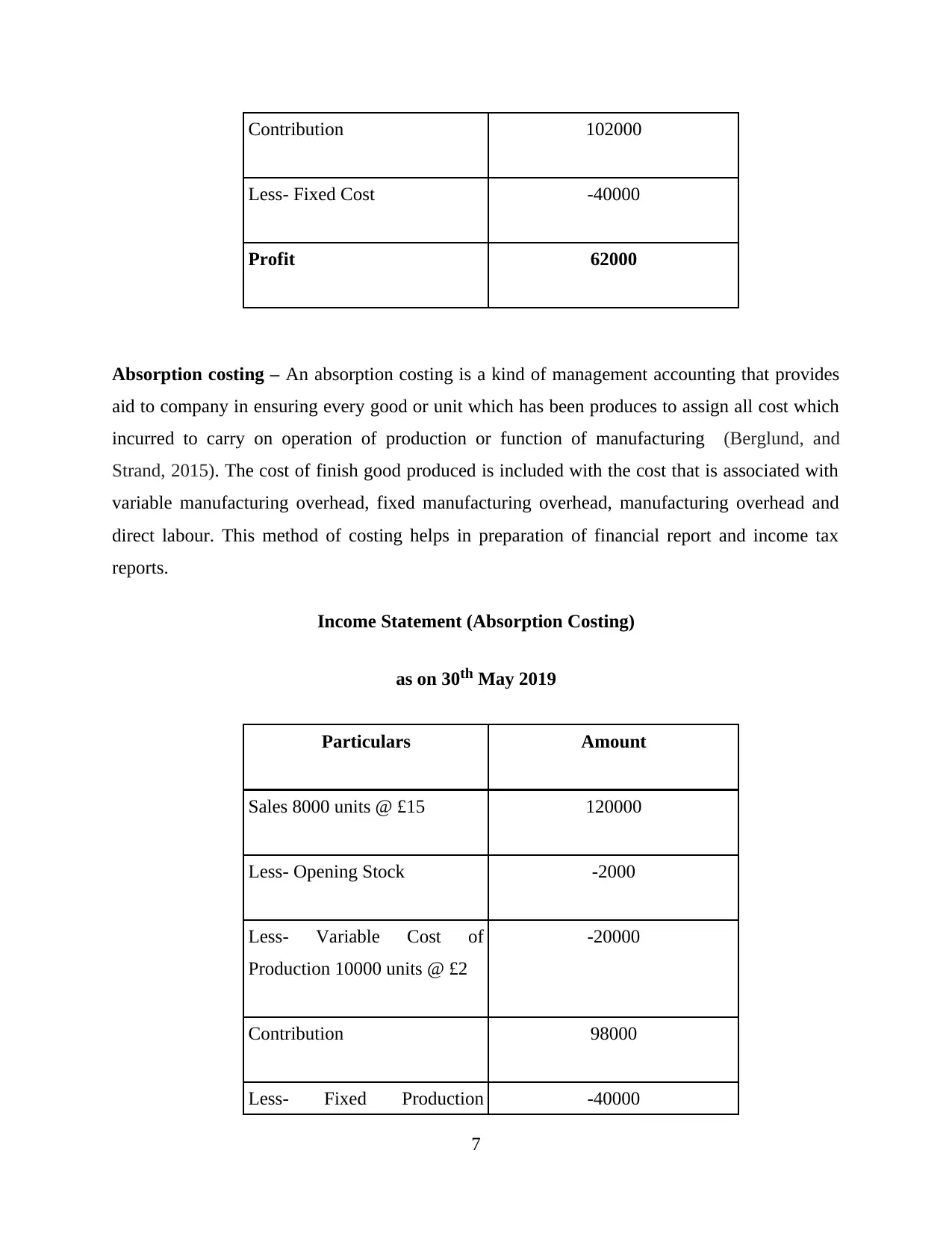

Income Statement (Marginal Costing)

as on 30th May 2019

Particulars Amount

Sales 8000 units @ £15 120000

Less- Opening Stock -2000

Less- Variable Cost (8000

units @ £2)

-16000

6

performance .

Advantages

It helps in making comparison between the actual and budgeted performance

This guide the organisation for making decisions regarding termination or promotion of

the employee

training and development programs are also implemented on the basis of analysing the

performances.

LO2

P3 Calculate costs using techniques of cost analysis to prepare an income statement using

marginal and absorption costs.

Marginal costing – It is defined as technique of costing which all marginal cost through variable

cost of business was charged against cost per unit and in fixed cost it will write off completely

against contribution factor (Samuelsson, and et.al., 2016). The additional cost which incurred

for carrying production function which is related to an additional unit of output which is

produced. This cost is determined by Direct labour, Variable overheads , Direct expenses and

Direct material. The company with the help of marginal costing can make shares valuation, level

of profitability and price which can be determined and helps in making difference between

variable and fixed cost.

Income Statement (Marginal Costing)

as on 30th May 2019

Particulars Amount

Sales 8000 units @ £15 120000

Less- Opening Stock -2000

Less- Variable Cost (8000

units @ £2)

-16000

6

Contribution 102000

Less- Fixed Cost -40000

Profit 62000

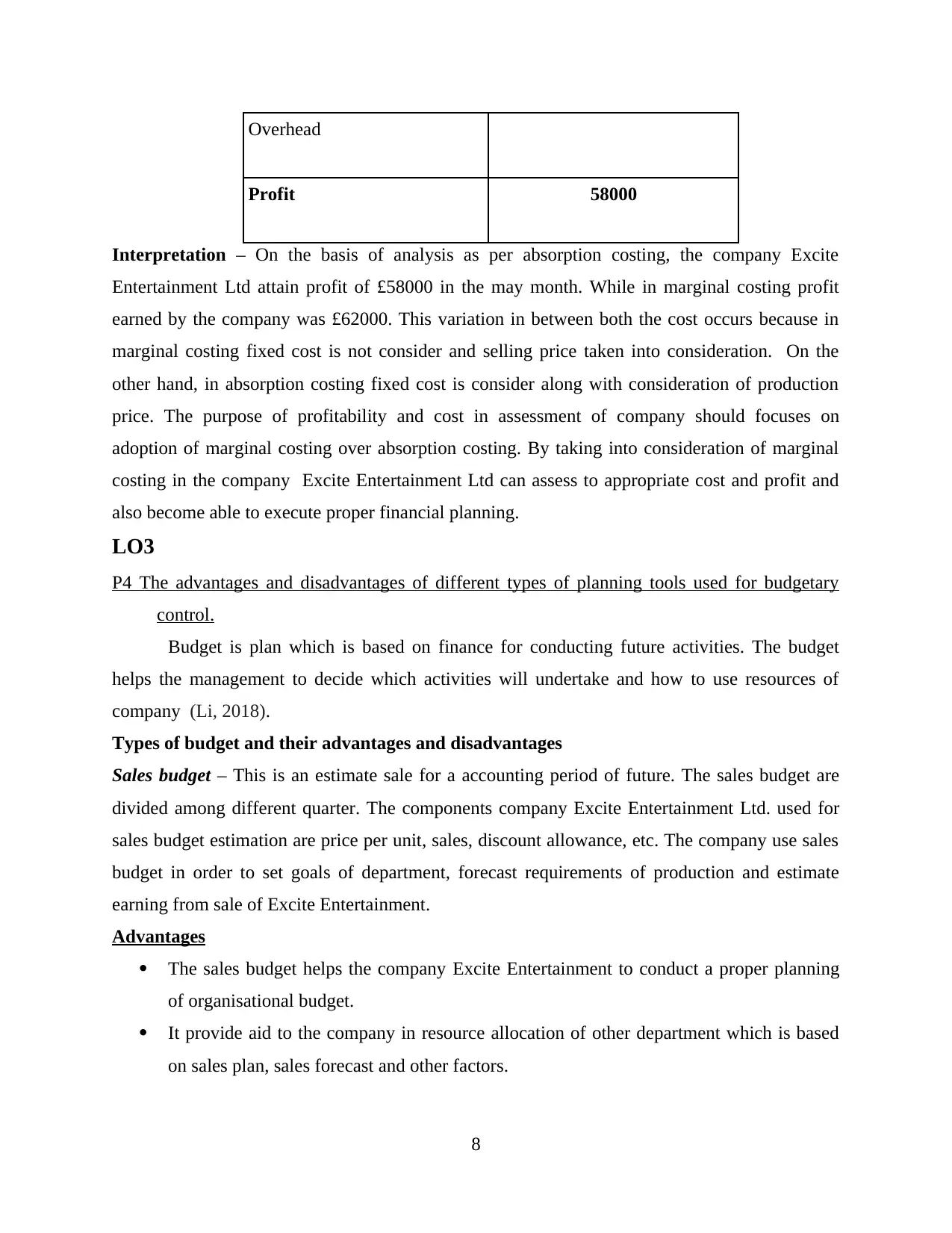

Absorption costing – An absorption costing is a kind of management accounting that provides

aid to company in ensuring every good or unit which has been produces to assign all cost which

incurred to carry on operation of production or function of manufacturing (Berglund, and

Strand, 2015). The cost of finish good produced is included with the cost that is associated with

variable manufacturing overhead, fixed manufacturing overhead, manufacturing overhead and

direct labour. This method of costing helps in preparation of financial report and income tax

reports.

Income Statement (Absorption Costing)

as on 30th May 2019

Particulars Amount

Sales 8000 units @ £15 120000

Less- Opening Stock -2000

Less- Variable Cost of

Production 10000 units @ £2

-20000

Contribution 98000

Less- Fixed Production -40000

7

Less- Fixed Cost -40000

Profit 62000

Absorption costing – An absorption costing is a kind of management accounting that provides

aid to company in ensuring every good or unit which has been produces to assign all cost which

incurred to carry on operation of production or function of manufacturing (Berglund, and

Strand, 2015). The cost of finish good produced is included with the cost that is associated with

variable manufacturing overhead, fixed manufacturing overhead, manufacturing overhead and

direct labour. This method of costing helps in preparation of financial report and income tax

reports.

Income Statement (Absorption Costing)

as on 30th May 2019

Particulars Amount

Sales 8000 units @ £15 120000

Less- Opening Stock -2000

Less- Variable Cost of

Production 10000 units @ £2

-20000

Contribution 98000

Less- Fixed Production -40000

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

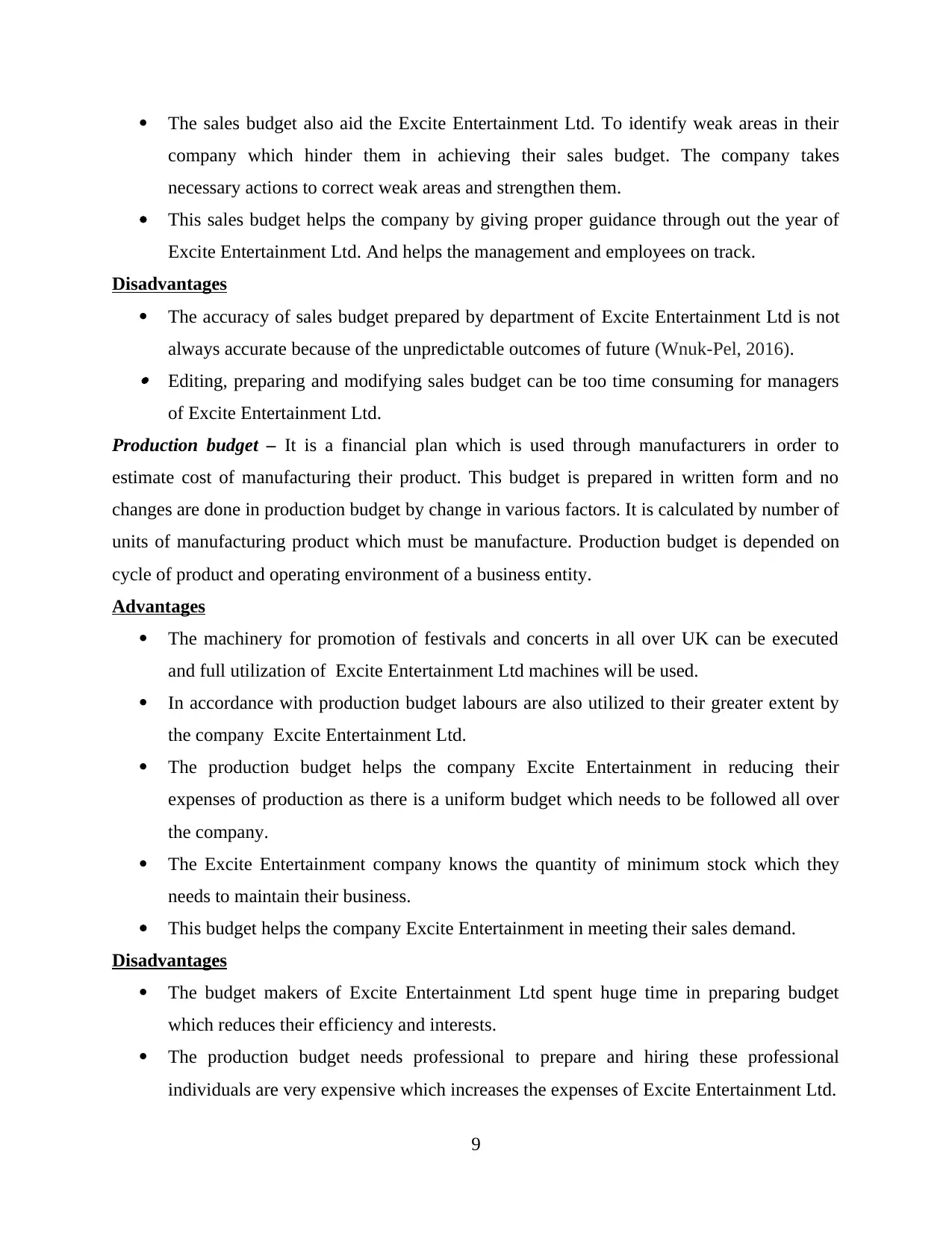

Overhead

Profit 58000

Interpretation – On the basis of analysis as per absorption costing, the company Excite

Entertainment Ltd attain profit of £58000 in the may month. While in marginal costing profit

earned by the company was £62000. This variation in between both the cost occurs because in

marginal costing fixed cost is not consider and selling price taken into consideration. On the

other hand, in absorption costing fixed cost is consider along with consideration of production

price. The purpose of profitability and cost in assessment of company should focuses on

adoption of marginal costing over absorption costing. By taking into consideration of marginal

costing in the company Excite Entertainment Ltd can assess to appropriate cost and profit and

also become able to execute proper financial planning.

LO3

P4 The advantages and disadvantages of different types of planning tools used for budgetary

control.

Budget is plan which is based on finance for conducting future activities. The budget

helps the management to decide which activities will undertake and how to use resources of

company (Li, 2018).

Types of budget and their advantages and disadvantages

Sales budget – This is an estimate sale for a accounting period of future. The sales budget are

divided among different quarter. The components company Excite Entertainment Ltd. used for

sales budget estimation are price per unit, sales, discount allowance, etc. The company use sales

budget in order to set goals of department, forecast requirements of production and estimate

earning from sale of Excite Entertainment.

Advantages

The sales budget helps the company Excite Entertainment to conduct a proper planning

of organisational budget.

It provide aid to the company in resource allocation of other department which is based

on sales plan, sales forecast and other factors.

8

Profit 58000

Interpretation – On the basis of analysis as per absorption costing, the company Excite

Entertainment Ltd attain profit of £58000 in the may month. While in marginal costing profit

earned by the company was £62000. This variation in between both the cost occurs because in

marginal costing fixed cost is not consider and selling price taken into consideration. On the

other hand, in absorption costing fixed cost is consider along with consideration of production

price. The purpose of profitability and cost in assessment of company should focuses on

adoption of marginal costing over absorption costing. By taking into consideration of marginal

costing in the company Excite Entertainment Ltd can assess to appropriate cost and profit and

also become able to execute proper financial planning.

LO3

P4 The advantages and disadvantages of different types of planning tools used for budgetary

control.

Budget is plan which is based on finance for conducting future activities. The budget

helps the management to decide which activities will undertake and how to use resources of

company (Li, 2018).

Types of budget and their advantages and disadvantages

Sales budget – This is an estimate sale for a accounting period of future. The sales budget are

divided among different quarter. The components company Excite Entertainment Ltd. used for

sales budget estimation are price per unit, sales, discount allowance, etc. The company use sales

budget in order to set goals of department, forecast requirements of production and estimate

earning from sale of Excite Entertainment.

Advantages

The sales budget helps the company Excite Entertainment to conduct a proper planning

of organisational budget.

It provide aid to the company in resource allocation of other department which is based

on sales plan, sales forecast and other factors.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The sales budget also aid the Excite Entertainment Ltd. To identify weak areas in their

company which hinder them in achieving their sales budget. The company takes

necessary actions to correct weak areas and strengthen them.

This sales budget helps the company by giving proper guidance through out the year of

Excite Entertainment Ltd. And helps the management and employees on track.

Disadvantages

The accuracy of sales budget prepared by department of Excite Entertainment Ltd is not

always accurate because of the unpredictable outcomes of future (Wnuk-Pel, 2016). Editing, preparing and modifying sales budget can be too time consuming for managers

of Excite Entertainment Ltd.

Production budget – It is a financial plan which is used through manufacturers in order to

estimate cost of manufacturing their product. This budget is prepared in written form and no

changes are done in production budget by change in various factors. It is calculated by number of

units of manufacturing product which must be manufacture. Production budget is depended on

cycle of product and operating environment of a business entity.

Advantages

The machinery for promotion of festivals and concerts in all over UK can be executed

and full utilization of Excite Entertainment Ltd machines will be used.

In accordance with production budget labours are also utilized to their greater extent by

the company Excite Entertainment Ltd.

The production budget helps the company Excite Entertainment in reducing their

expenses of production as there is a uniform budget which needs to be followed all over

the company.

The Excite Entertainment company knows the quantity of minimum stock which they

needs to maintain their business.

This budget helps the company Excite Entertainment in meeting their sales demand.

Disadvantages

The budget makers of Excite Entertainment Ltd spent huge time in preparing budget

which reduces their efficiency and interests.

The production budget needs professional to prepare and hiring these professional

individuals are very expensive which increases the expenses of Excite Entertainment Ltd.

9

company which hinder them in achieving their sales budget. The company takes

necessary actions to correct weak areas and strengthen them.

This sales budget helps the company by giving proper guidance through out the year of

Excite Entertainment Ltd. And helps the management and employees on track.

Disadvantages

The accuracy of sales budget prepared by department of Excite Entertainment Ltd is not

always accurate because of the unpredictable outcomes of future (Wnuk-Pel, 2016). Editing, preparing and modifying sales budget can be too time consuming for managers

of Excite Entertainment Ltd.

Production budget – It is a financial plan which is used through manufacturers in order to

estimate cost of manufacturing their product. This budget is prepared in written form and no

changes are done in production budget by change in various factors. It is calculated by number of

units of manufacturing product which must be manufacture. Production budget is depended on

cycle of product and operating environment of a business entity.

Advantages

The machinery for promotion of festivals and concerts in all over UK can be executed

and full utilization of Excite Entertainment Ltd machines will be used.

In accordance with production budget labours are also utilized to their greater extent by

the company Excite Entertainment Ltd.

The production budget helps the company Excite Entertainment in reducing their

expenses of production as there is a uniform budget which needs to be followed all over

the company.

The Excite Entertainment company knows the quantity of minimum stock which they

needs to maintain their business.

This budget helps the company Excite Entertainment in meeting their sales demand.

Disadvantages

The budget makers of Excite Entertainment Ltd spent huge time in preparing budget

which reduces their efficiency and interests.

The production budget needs professional to prepare and hiring these professional

individuals are very expensive which increases the expenses of Excite Entertainment Ltd.

9

The process of budgeting only focuses on attention of management team and

implementation in actual is very difficult for the company Excite Entertainment Ltd.

Cash flow budget – It is an estimation of receipts of cash and expenditures which are expected

on a certain period of time. The estimates are made in this budget on the basis on bimonthly,

monthly and quarterly. The cash flow budget is useful to prepare for measuring performance of

businesses.

Advantages

The cash flow budget helps to avoid cash shortage in which company Excite

Entertainment Ltd bears high expenses.

The budget formulation is very easy and it helps the company Excite Entertainment Ltd

to attain success and growth in prevailing industry.

By cash flow budget Excite Entertainment Ltd can predict inflow and outflow of cash

within their business (Agu, Nweze, and Enekwe, 2016).

The need of cash identified by company Excite Entertainment Ltd which enables the

company to mange overall expenses and revenue they incur by the help of cash flow

budget.

Disadvantages

The company observes that the value of cash is uncertain so the cash flow budget

prepared by managers can lead them away from the target. The cash flow budget is a full wastage of time because it is not possible to predict future

and this also increase the expenses of the company Excite Entertainment Ltd.

About budget variance and their significance to the Excite Entertainment Ltd.

The budget variance is a difference between baseline or budgeted amount of revenue or

expenses and the actual amount. It is favorable only when actual revenue is greater than

budgeted and when actual expenses are less than budgeted. The company Excite Entertainment

also uses this technique of budget variance in order to measure their performance which is in line

with prepared budget. Any variance measured by managers for Excite Entertainment lead to take

effective measures to overcome these variance in the company to attain budgeted performance.

Budget variance plays a significant role on Excite Entertainment. The company measures

their performance of sales, production and cash flow by the use of these budgets (Uyar,

Gungormus, and Kuzey, 2017). Also, it provides aid to company Excite Entertainment Ltd to

10

implementation in actual is very difficult for the company Excite Entertainment Ltd.

Cash flow budget – It is an estimation of receipts of cash and expenditures which are expected

on a certain period of time. The estimates are made in this budget on the basis on bimonthly,

monthly and quarterly. The cash flow budget is useful to prepare for measuring performance of

businesses.

Advantages

The cash flow budget helps to avoid cash shortage in which company Excite

Entertainment Ltd bears high expenses.

The budget formulation is very easy and it helps the company Excite Entertainment Ltd

to attain success and growth in prevailing industry.

By cash flow budget Excite Entertainment Ltd can predict inflow and outflow of cash

within their business (Agu, Nweze, and Enekwe, 2016).

The need of cash identified by company Excite Entertainment Ltd which enables the

company to mange overall expenses and revenue they incur by the help of cash flow

budget.

Disadvantages

The company observes that the value of cash is uncertain so the cash flow budget

prepared by managers can lead them away from the target. The cash flow budget is a full wastage of time because it is not possible to predict future

and this also increase the expenses of the company Excite Entertainment Ltd.

About budget variance and their significance to the Excite Entertainment Ltd.

The budget variance is a difference between baseline or budgeted amount of revenue or

expenses and the actual amount. It is favorable only when actual revenue is greater than

budgeted and when actual expenses are less than budgeted. The company Excite Entertainment

also uses this technique of budget variance in order to measure their performance which is in line

with prepared budget. Any variance measured by managers for Excite Entertainment lead to take

effective measures to overcome these variance in the company to attain budgeted performance.

Budget variance plays a significant role on Excite Entertainment. The company measures

their performance of sales, production and cash flow by the use of these budgets (Uyar,

Gungormus, and Kuzey, 2017). Also, it provides aid to company Excite Entertainment Ltd to

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.