Management Cost and Control Report - University Name, Semester 1

VerifiedAdded on 2020/12/31

|12

|2756

|306

Report

AI Summary

This report delves into the core concepts of management accounting and cost control. It begins by differentiating between financial and management accounting, outlining their key functions and relevance to concepts like panopticism, control, and discipline. The report then presents financial statements, including the cost of goods manufactured and profit and loss statements. It explores job order costing and various cost allocation methods such as direct, step-down, and reciprocal, with justifications for preferring budgeted costs. The report further examines activity-based costing (ABC), determining per-unit manufacturing costs, analyzing cost drivers, and extracting profitable segments. The analysis includes journal entries and practical examples, providing a comprehensive overview of cost management techniques.

MANAGEMENT COST AND

CONTROL

CONTROL

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

Q1................................................................................................................................................1

Q2................................................................................................................................................2

Q3................................................................................................................................................3

3.B Journal entries.......................................................................................................................4

3.D Presenting major cost for giving special focus ....................................................................4

Q4 Determination of allocation of service department...............................................................5

4.a Direct method for allocation..................................................................................................5

4.b Step down method for cost allocation...................................................................................5

4.c Reciprocal method for cost allocation...................................................................................6

4.d Reason for preferring budgeted instead of actual costs allocation ......................................7

Q5 Activity based costing...........................................................................................................7

5.a Determining total cost of manufacturing of per unit and along with this per unit................7

Deluxe.........................................................................................................................................8

5.b Reason for high manufacturing overhead cost as 120 for standard door as compared to

deluxe as 80.................................................................................................................................8

5.c Cost driver.............................................................................................................................8

5.d Computation of manufacturing overhead per unit ...............................................................9

5.e Extraction of profitable segment...........................................................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

INTRODUCTION...........................................................................................................................1

Q1................................................................................................................................................1

Q2................................................................................................................................................2

Q3................................................................................................................................................3

3.B Journal entries.......................................................................................................................4

3.D Presenting major cost for giving special focus ....................................................................4

Q4 Determination of allocation of service department...............................................................5

4.a Direct method for allocation..................................................................................................5

4.b Step down method for cost allocation...................................................................................5

4.c Reciprocal method for cost allocation...................................................................................6

4.d Reason for preferring budgeted instead of actual costs allocation ......................................7

Q5 Activity based costing...........................................................................................................7

5.a Determining total cost of manufacturing of per unit and along with this per unit................7

Deluxe.........................................................................................................................................8

5.b Reason for high manufacturing overhead cost as 120 for standard door as compared to

deluxe as 80.................................................................................................................................8

5.c Cost driver.............................................................................................................................8

5.d Computation of manufacturing overhead per unit ...............................................................9

5.e Extraction of profitable segment...........................................................................................9

CONCLUSION................................................................................................................................9

REFERENCES..............................................................................................................................10

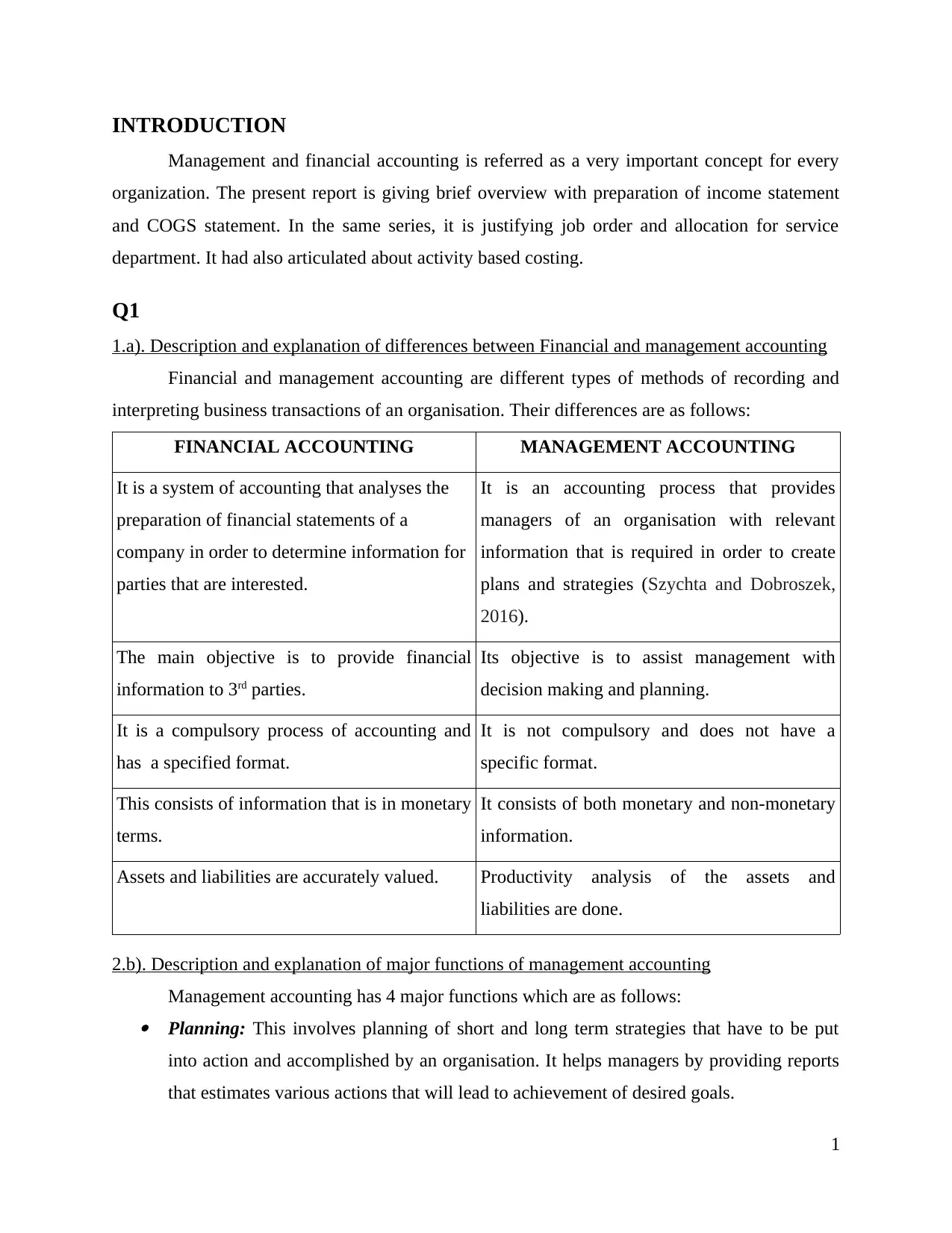

INTRODUCTION

Management and financial accounting is referred as a very important concept for every

organization. The present report is giving brief overview with preparation of income statement

and COGS statement. In the same series, it is justifying job order and allocation for service

department. It had also articulated about activity based costing.

Q1

1.a). Description and explanation of differences between Financial and management accounting

Financial and management accounting are different types of methods of recording and

interpreting business transactions of an organisation. Their differences are as follows:

FINANCIAL ACCOUNTING MANAGEMENT ACCOUNTING

It is a system of accounting that analyses the

preparation of financial statements of a

company in order to determine information for

parties that are interested.

It is an accounting process that provides

managers of an organisation with relevant

information that is required in order to create

plans and strategies (Szychta and Dobroszek,

2016).

The main objective is to provide financial

information to 3rd parties.

Its objective is to assist management with

decision making and planning.

It is a compulsory process of accounting and

has a specified format.

It is not compulsory and does not have a

specific format.

This consists of information that is in monetary

terms.

It consists of both monetary and non-monetary

information.

Assets and liabilities are accurately valued. Productivity analysis of the assets and

liabilities are done.

2.b). Description and explanation of major functions of management accounting

Management accounting has 4 major functions which are as follows: Planning: This involves planning of short and long term strategies that have to be put

into action and accomplished by an organisation. It helps managers by providing reports

that estimates various actions that will lead to achievement of desired goals.

1

Management and financial accounting is referred as a very important concept for every

organization. The present report is giving brief overview with preparation of income statement

and COGS statement. In the same series, it is justifying job order and allocation for service

department. It had also articulated about activity based costing.

Q1

1.a). Description and explanation of differences between Financial and management accounting

Financial and management accounting are different types of methods of recording and

interpreting business transactions of an organisation. Their differences are as follows:

FINANCIAL ACCOUNTING MANAGEMENT ACCOUNTING

It is a system of accounting that analyses the

preparation of financial statements of a

company in order to determine information for

parties that are interested.

It is an accounting process that provides

managers of an organisation with relevant

information that is required in order to create

plans and strategies (Szychta and Dobroszek,

2016).

The main objective is to provide financial

information to 3rd parties.

Its objective is to assist management with

decision making and planning.

It is a compulsory process of accounting and

has a specified format.

It is not compulsory and does not have a

specific format.

This consists of information that is in monetary

terms.

It consists of both monetary and non-monetary

information.

Assets and liabilities are accurately valued. Productivity analysis of the assets and

liabilities are done.

2.b). Description and explanation of major functions of management accounting

Management accounting has 4 major functions which are as follows: Planning: This involves planning of short and long term strategies that have to be put

into action and accomplished by an organisation. It helps managers by providing reports

that estimates various actions that will lead to achievement of desired goals.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Organising: It is a process that organises a framework and assigns responsibilities to

employees of an organisation (Hiebl, 2014). This helps in providing required reports and

information that will regulate operations and adjust in case changes are required. Controlling: It is the monitoring, measuring, evaluating and correcting of actual results in

order to make sure that organisation's plans and objectives are being achieved. It helps

analysing and controlling expected and actual results.

Decision making: This is a process which involves choosing from various alternatives,

regarding problems that have to be fixed and goals that have to be achieved (Shan, 2015).

3.c). Panopticism, control and discipline concept's relevance to management accounting

Panopticism is an experiment of power that deals with behaviour modification.

Management accounting uses it as a way of determining effects of decisions and evaluates them

even after discontinuation (Berry, Broadbent and Otley, 2016). This helps in finding new

methods to adopt. Control concept is helpful for maintaining performances of an organisation,

making management accounting easy. Discipline concept is required as proper principles can be

applied while assessing company's management.

Q2

Statement of cost of goods manufactured Details Amount

Direct materials used

Raw Material Inventory (1st July, 2016) 183000

Purchase of Raw Material 1200360

Less: Raw Material Inventory (30th June, 2017) 186000

Raw material used 1197360

less: Indirect material 52500

Used Direct material 1144860

Direct Labour 1284000

Manufacturing overhead

Indirect Labour 75000

Factory Rent 152820

Freight In 90000

2

employees of an organisation (Hiebl, 2014). This helps in providing required reports and

information that will regulate operations and adjust in case changes are required. Controlling: It is the monitoring, measuring, evaluating and correcting of actual results in

order to make sure that organisation's plans and objectives are being achieved. It helps

analysing and controlling expected and actual results.

Decision making: This is a process which involves choosing from various alternatives,

regarding problems that have to be fixed and goals that have to be achieved (Shan, 2015).

3.c). Panopticism, control and discipline concept's relevance to management accounting

Panopticism is an experiment of power that deals with behaviour modification.

Management accounting uses it as a way of determining effects of decisions and evaluates them

even after discontinuation (Berry, Broadbent and Otley, 2016). This helps in finding new

methods to adopt. Control concept is helpful for maintaining performances of an organisation,

making management accounting easy. Discipline concept is required as proper principles can be

applied while assessing company's management.

Q2

Statement of cost of goods manufactured Details Amount

Direct materials used

Raw Material Inventory (1st July, 2016) 183000

Purchase of Raw Material 1200360

Less: Raw Material Inventory (30th June, 2017) 186000

Raw material used 1197360

less: Indirect material 52500

Used Direct material 1144860

Direct Labour 1284000

Manufacturing overhead

Indirect Labour 75000

Factory Rent 152820

Freight In 90000

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Depreciation Expense - Factory Equipment 90000

Total manufacturing OH 407820

Cost of manufacturing 2836680

Add Work in Process (1st July, 2016) 60600

Less Work in Process (30th June, 2017) 57330

Manufactured cost of goods 2839950

Statement of profit and loss Details Amount

Sales 6751500

Cost of sales

Finished Goods (1st July, 2016) 264000

Cost of goods manufactured 2839550

Cost of goods for sale 3103550

Less: Finished Goods (30th June, 2017) 345000

Cost of goods sold 2758550

Gross profit 3992950

Operating expenses

Factory Rent 152820

Freight In 90000

Selling & Distribution Expenses 1200000

Administration Expenses 600000

Depreciation Expense - Factory Equipment 90000

Total operating expense 2132820

Income from operations 1860130

Add: depreciation 90000

Net income 1950130

Q3

Budgeted Department A Department B

Machine hours 4000

Direct manufacturing labour 8000

3

Total manufacturing OH 407820

Cost of manufacturing 2836680

Add Work in Process (1st July, 2016) 60600

Less Work in Process (30th June, 2017) 57330

Manufactured cost of goods 2839950

Statement of profit and loss Details Amount

Sales 6751500

Cost of sales

Finished Goods (1st July, 2016) 264000

Cost of goods manufactured 2839550

Cost of goods for sale 3103550

Less: Finished Goods (30th June, 2017) 345000

Cost of goods sold 2758550

Gross profit 3992950

Operating expenses

Factory Rent 152820

Freight In 90000

Selling & Distribution Expenses 1200000

Administration Expenses 600000

Depreciation Expense - Factory Equipment 90000

Total operating expense 2132820

Income from operations 1860130

Add: depreciation 90000

Net income 1950130

Q3

Budgeted Department A Department B

Machine hours 4000

Direct manufacturing labour 8000

3

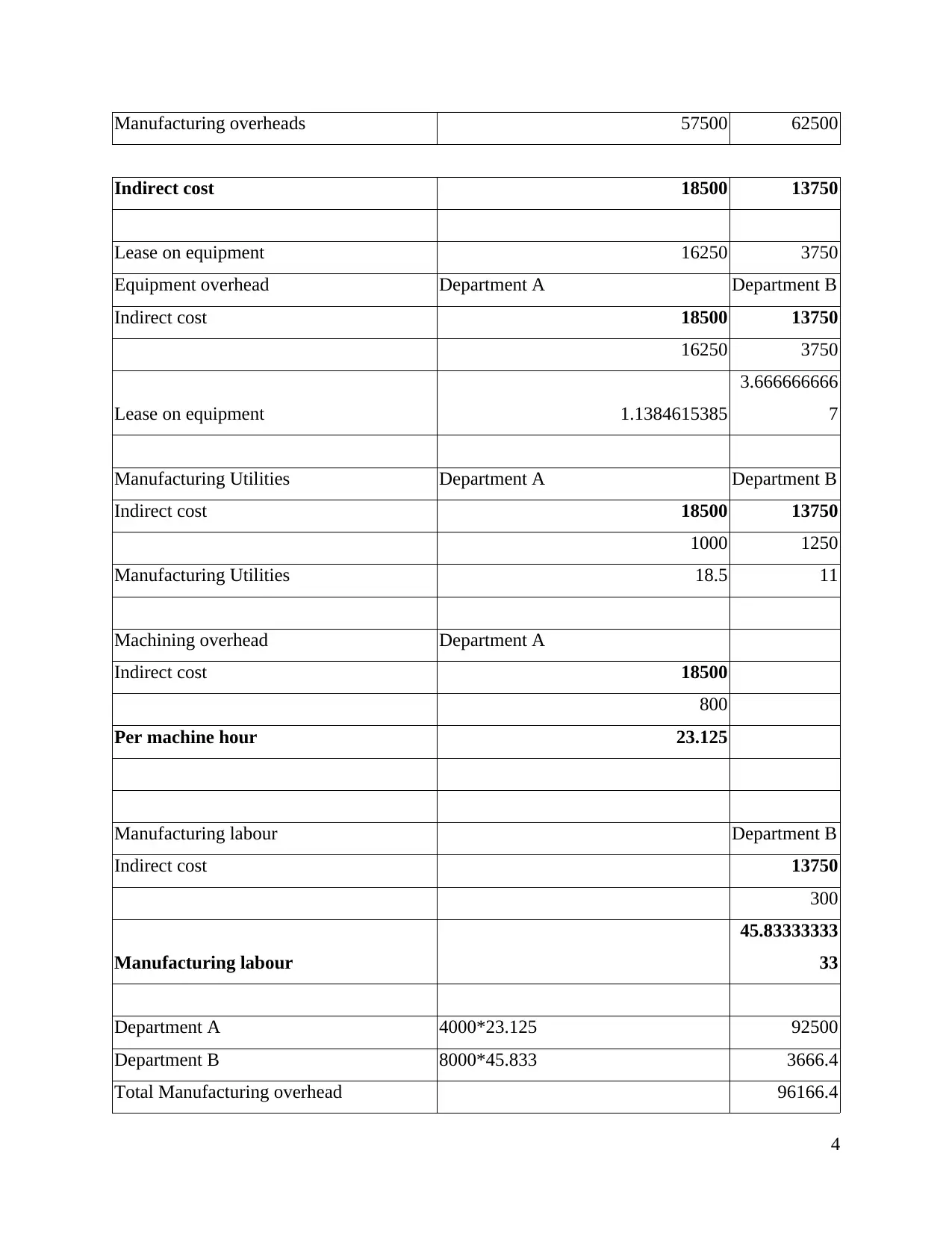

Manufacturing overheads 57500 62500

Indirect cost 18500 13750

Lease on equipment 16250 3750

Equipment overhead Department A Department B

Indirect cost 18500 13750

16250 3750

Lease on equipment 1.1384615385

3.666666666

7

Manufacturing Utilities Department A Department B

Indirect cost 18500 13750

1000 1250

Manufacturing Utilities 18.5 11

Machining overhead Department A

Indirect cost 18500

800

Per machine hour 23.125

Manufacturing labour Department B

Indirect cost 13750

300

Manufacturing labour

45.83333333

33

Department A 4000*23.125 92500

Department B 8000*45.833 3666.4

Total Manufacturing overhead 96166.4

4

Indirect cost 18500 13750

Lease on equipment 16250 3750

Equipment overhead Department A Department B

Indirect cost 18500 13750

16250 3750

Lease on equipment 1.1384615385

3.666666666

7

Manufacturing Utilities Department A Department B

Indirect cost 18500 13750

1000 1250

Manufacturing Utilities 18.5 11

Machining overhead Department A

Indirect cost 18500

800

Per machine hour 23.125

Manufacturing labour Department B

Indirect cost 13750

300

Manufacturing labour

45.83333333

33

Department A 4000*23.125 92500

Department B 8000*45.833 3666.4

Total Manufacturing overhead 96166.4

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

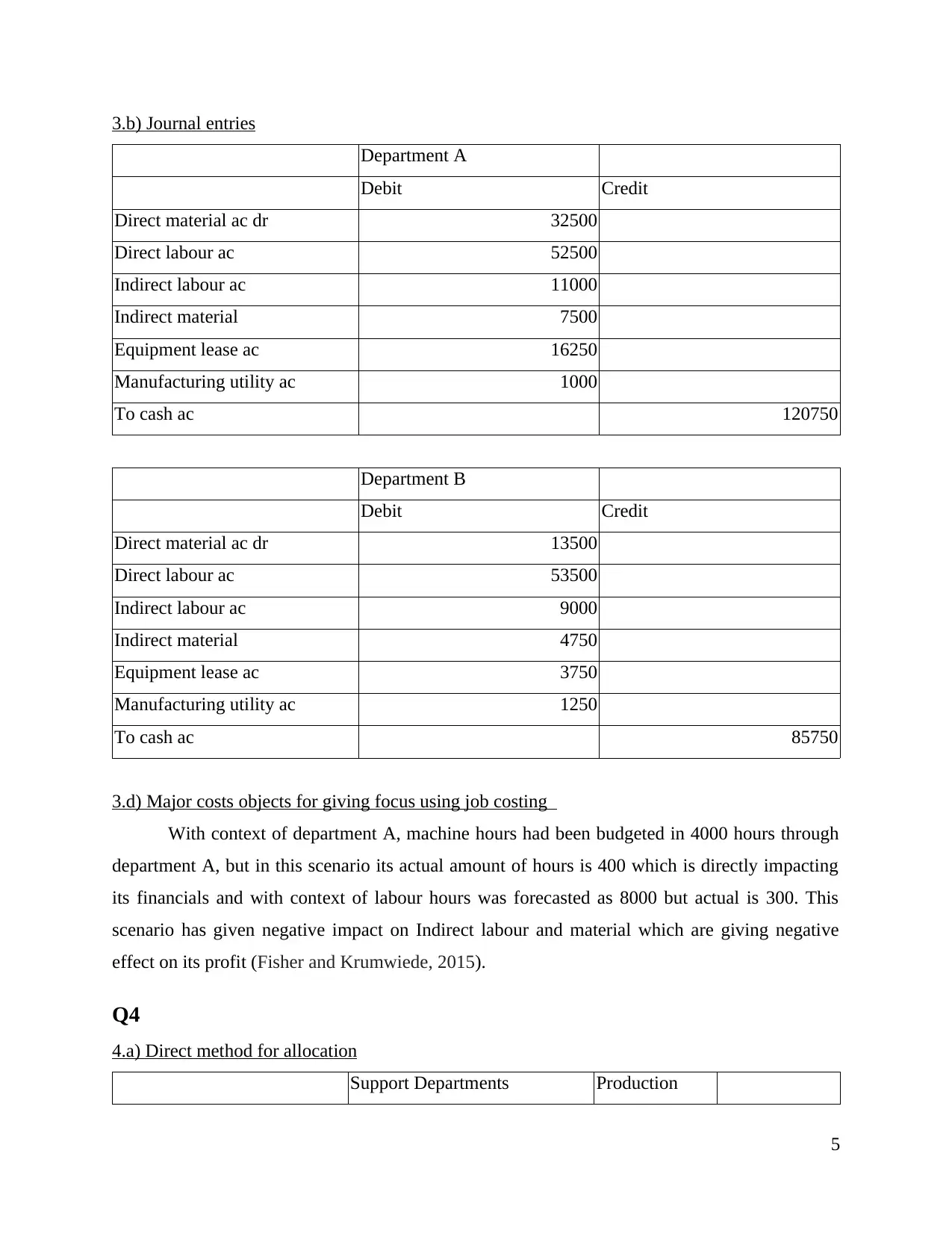

3.b) Journal entries

Department A

Debit Credit

Direct material ac dr 32500

Direct labour ac 52500

Indirect labour ac 11000

Indirect material 7500

Equipment lease ac 16250

Manufacturing utility ac 1000

To cash ac 120750

Department B

Debit Credit

Direct material ac dr 13500

Direct labour ac 53500

Indirect labour ac 9000

Indirect material 4750

Equipment lease ac 3750

Manufacturing utility ac 1250

To cash ac 85750

3.d) Major costs objects for giving focus using job costing

With context of department A, machine hours had been budgeted in 4000 hours through

department A, but in this scenario its actual amount of hours is 400 which is directly impacting

its financials and with context of labour hours was forecasted as 8000 but actual is 300. This

scenario has given negative impact on Indirect labour and material which are giving negative

effect on its profit (Fisher and Krumwiede, 2015).

Q4

4.a) Direct method for allocation

Support Departments Production

5

Department A

Debit Credit

Direct material ac dr 32500

Direct labour ac 52500

Indirect labour ac 11000

Indirect material 7500

Equipment lease ac 16250

Manufacturing utility ac 1000

To cash ac 120750

Department B

Debit Credit

Direct material ac dr 13500

Direct labour ac 53500

Indirect labour ac 9000

Indirect material 4750

Equipment lease ac 3750

Manufacturing utility ac 1250

To cash ac 85750

3.d) Major costs objects for giving focus using job costing

With context of department A, machine hours had been budgeted in 4000 hours through

department A, but in this scenario its actual amount of hours is 400 which is directly impacting

its financials and with context of labour hours was forecasted as 8000 but actual is 300. This

scenario has given negative impact on Indirect labour and material which are giving negative

effect on its profit (Fisher and Krumwiede, 2015).

Q4

4.a) Direct method for allocation

Support Departments Production

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

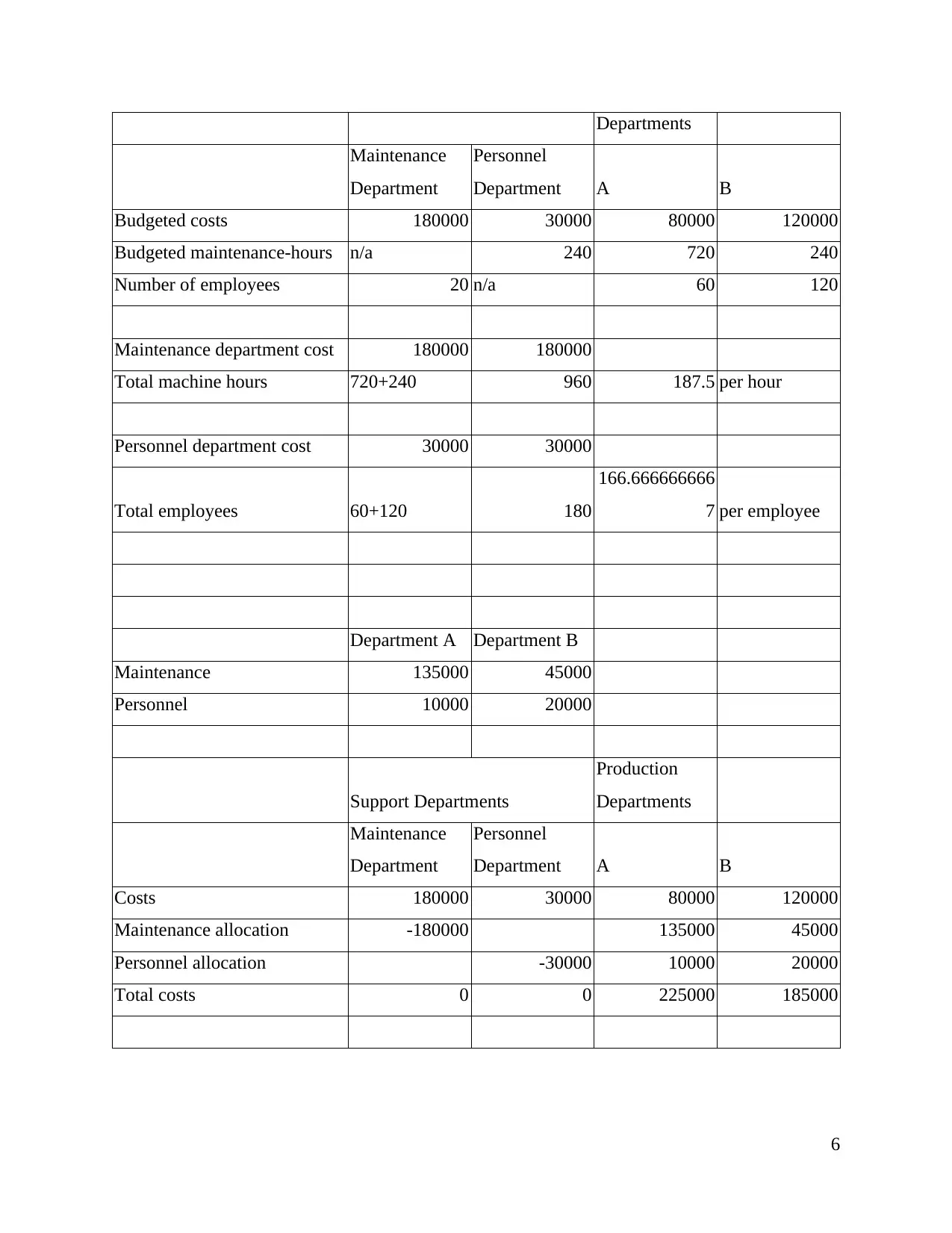

Departments

Maintenance

Department

Personnel

Department A B

Budgeted costs 180000 30000 80000 120000

Budgeted maintenance-hours n/a 240 720 240

Number of employees 20 n/a 60 120

Maintenance department cost 180000 180000

Total machine hours 720+240 960 187.5 per hour

Personnel department cost 30000 30000

Total employees 60+120 180

166.666666666

7 per employee

Department A Department B

Maintenance 135000 45000

Personnel 10000 20000

Support Departments

Production

Departments

Maintenance

Department

Personnel

Department A B

Costs 180000 30000 80000 120000

Maintenance allocation -180000 135000 45000

Personnel allocation -30000 10000 20000

Total costs 0 0 225000 185000

6

Maintenance

Department

Personnel

Department A B

Budgeted costs 180000 30000 80000 120000

Budgeted maintenance-hours n/a 240 720 240

Number of employees 20 n/a 60 120

Maintenance department cost 180000 180000

Total machine hours 720+240 960 187.5 per hour

Personnel department cost 30000 30000

Total employees 60+120 180

166.666666666

7 per employee

Department A Department B

Maintenance 135000 45000

Personnel 10000 20000

Support Departments

Production

Departments

Maintenance

Department

Personnel

Department A B

Costs 180000 30000 80000 120000

Maintenance allocation -180000 135000 45000

Personnel allocation -30000 10000 20000

Total costs 0 0 225000 185000

6

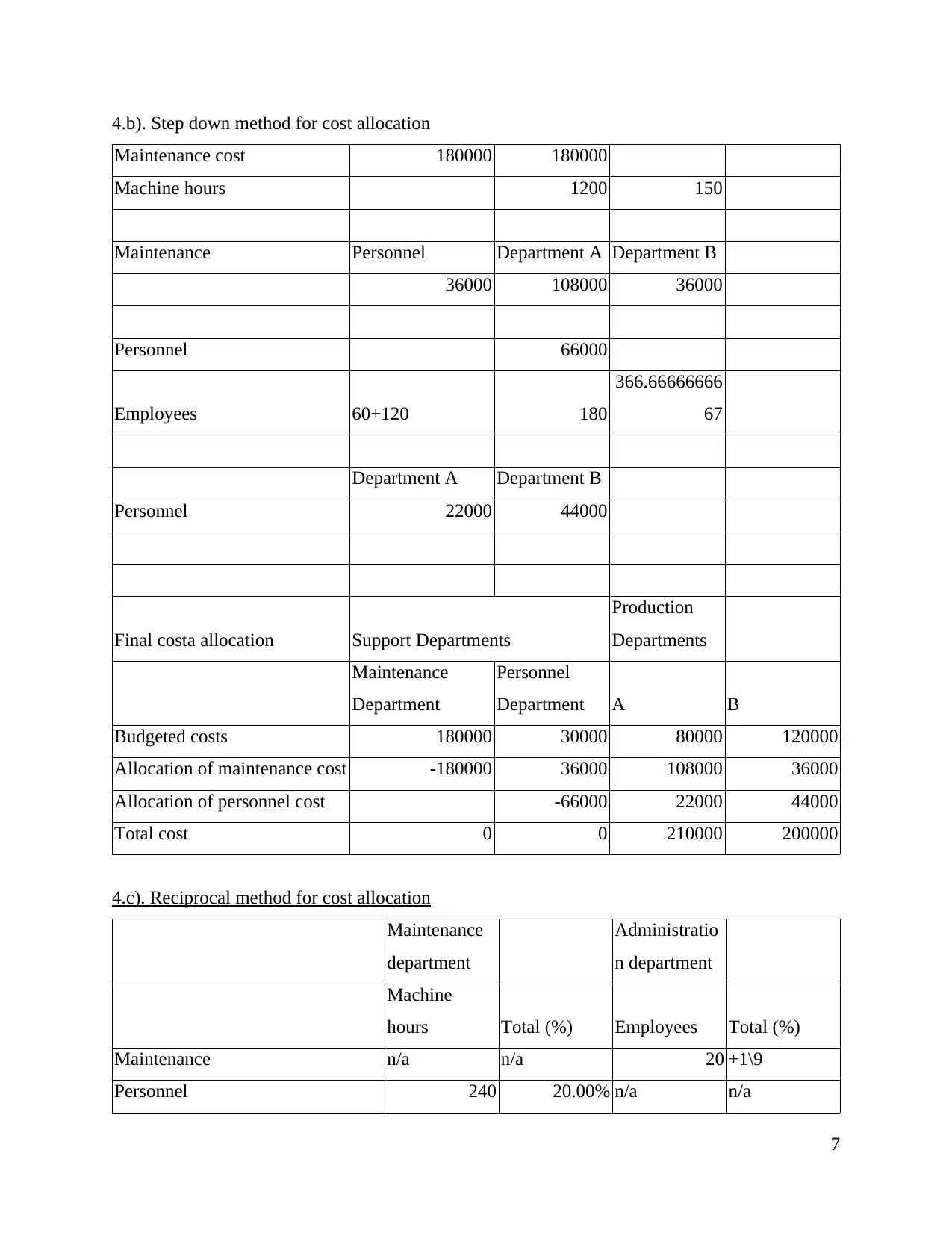

4.b). Step down method for cost allocation

Maintenance cost 180000 180000

Machine hours 1200 150

Maintenance Personnel Department A Department B

36000 108000 36000

Personnel 66000

Employees 60+120 180

366.66666666

67

Department A Department B

Personnel 22000 44000

Final costa allocation Support Departments

Production

Departments

Maintenance

Department

Personnel

Department A B

Budgeted costs 180000 30000 80000 120000

Allocation of maintenance cost -180000 36000 108000 36000

Allocation of personnel cost -66000 22000 44000

Total cost 0 0 210000 200000

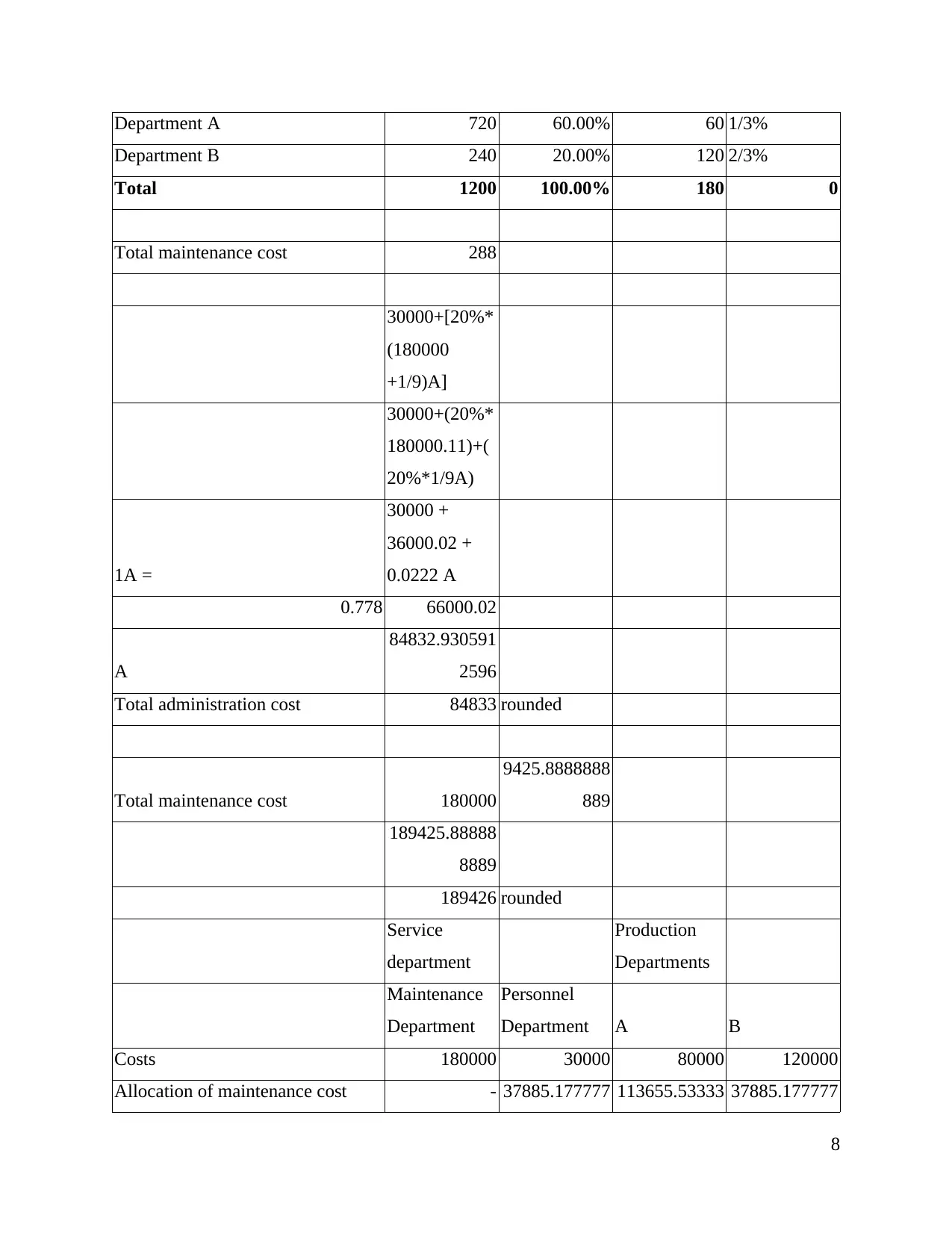

4.c). Reciprocal method for cost allocation

Maintenance

department

Administratio

n department

Machine

hours Total (%) Employees Total (%)

Maintenance n/a n/a 20 +1\9

Personnel 240 20.00% n/a n/a

7

Maintenance cost 180000 180000

Machine hours 1200 150

Maintenance Personnel Department A Department B

36000 108000 36000

Personnel 66000

Employees 60+120 180

366.66666666

67

Department A Department B

Personnel 22000 44000

Final costa allocation Support Departments

Production

Departments

Maintenance

Department

Personnel

Department A B

Budgeted costs 180000 30000 80000 120000

Allocation of maintenance cost -180000 36000 108000 36000

Allocation of personnel cost -66000 22000 44000

Total cost 0 0 210000 200000

4.c). Reciprocal method for cost allocation

Maintenance

department

Administratio

n department

Machine

hours Total (%) Employees Total (%)

Maintenance n/a n/a 20 +1\9

Personnel 240 20.00% n/a n/a

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Department A 720 60.00% 60 1/3%

Department B 240 20.00% 120 2/3%

Total 1200 100.00% 180 0

Total maintenance cost 288

30000+[20%*

(180000

+1/9)A]

30000+(20%*

180000.11)+(

20%*1/9A)

1A =

30000 +

36000.02 +

0.0222 A

0.778 66000.02

A

84832.930591

2596

Total administration cost 84833 rounded

Total maintenance cost 180000

9425.8888888

889

189425.88888

8889

189426 rounded

Service

department

Production

Departments

Maintenance

Department

Personnel

Department A B

Costs 180000 30000 80000 120000

Allocation of maintenance cost - 37885.177777 113655.53333 37885.177777

8

Department B 240 20.00% 120 2/3%

Total 1200 100.00% 180 0

Total maintenance cost 288

30000+[20%*

(180000

+1/9)A]

30000+(20%*

180000.11)+(

20%*1/9A)

1A =

30000 +

36000.02 +

0.0222 A

0.778 66000.02

A

84832.930591

2596

Total administration cost 84833 rounded

Total maintenance cost 180000

9425.8888888

889

189425.88888

8889

189426 rounded

Service

department

Production

Departments

Maintenance

Department

Personnel

Department A B

Costs 180000 30000 80000 120000

Allocation of maintenance cost - 37885.177777 113655.53333 37885.177777

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

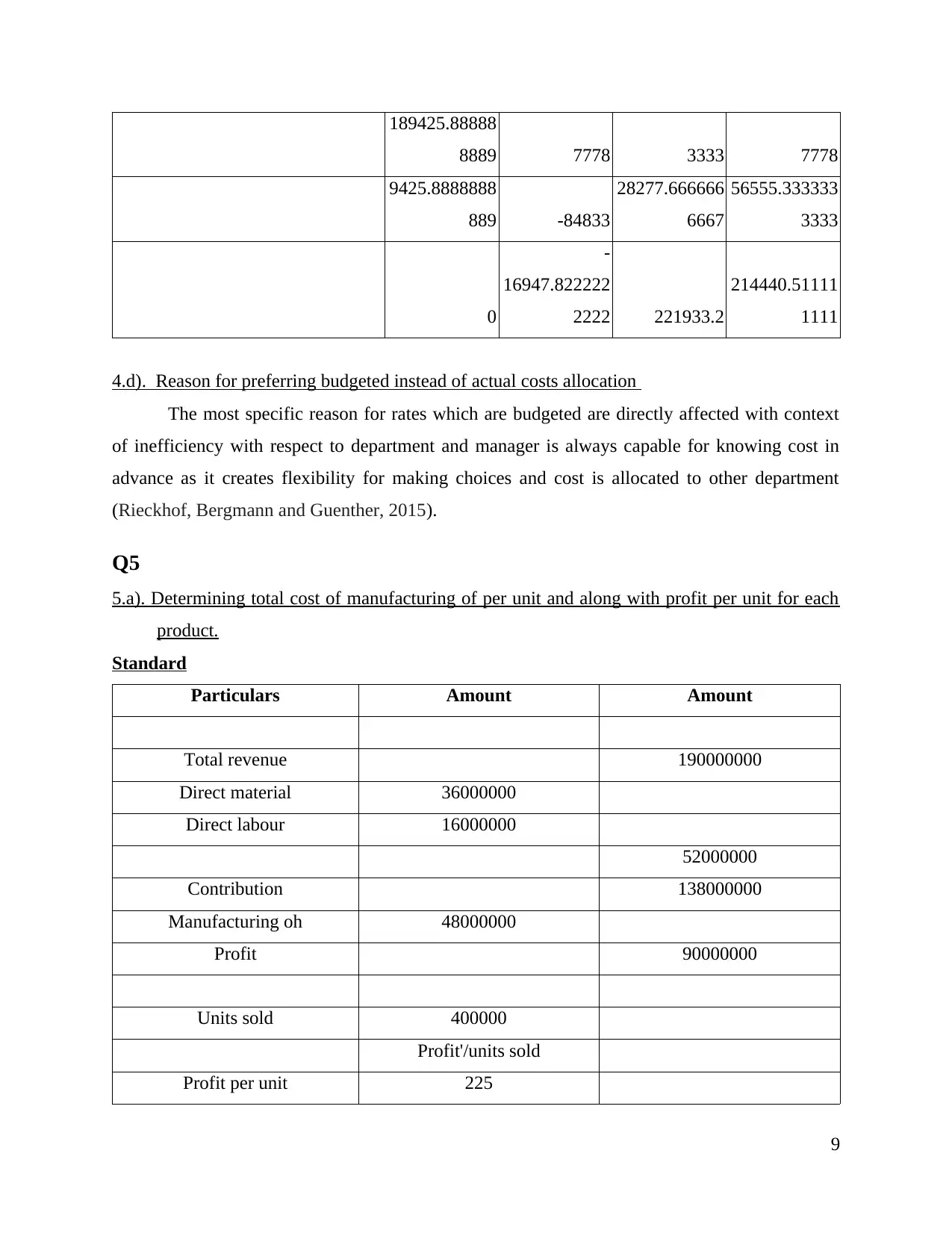

189425.88888

8889 7778 3333 7778

9425.8888888

889 -84833

28277.666666

6667

56555.333333

3333

0

-

16947.822222

2222 221933.2

214440.51111

1111

4.d). Reason for preferring budgeted instead of actual costs allocation

The most specific reason for rates which are budgeted are directly affected with context

of inefficiency with respect to department and manager is always capable for knowing cost in

advance as it creates flexibility for making choices and cost is allocated to other department

(Rieckhof, Bergmann and Guenther, 2015).

Q5

5.a). Determining total cost of manufacturing of per unit and along with profit per unit for each

product.

Standard

Particulars Amount Amount

Total revenue 190000000

Direct material 36000000

Direct labour 16000000

52000000

Contribution 138000000

Manufacturing oh 48000000

Profit 90000000

Units sold 400000

Profit'/units sold

Profit per unit 225

9

8889 7778 3333 7778

9425.8888888

889 -84833

28277.666666

6667

56555.333333

3333

0

-

16947.822222

2222 221933.2

214440.51111

1111

4.d). Reason for preferring budgeted instead of actual costs allocation

The most specific reason for rates which are budgeted are directly affected with context

of inefficiency with respect to department and manager is always capable for knowing cost in

advance as it creates flexibility for making choices and cost is allocated to other department

(Rieckhof, Bergmann and Guenther, 2015).

Q5

5.a). Determining total cost of manufacturing of per unit and along with profit per unit for each

product.

Standard

Particulars Amount Amount

Total revenue 190000000

Direct material 36000000

Direct labour 16000000

52000000

Contribution 138000000

Manufacturing oh 48000000

Profit 90000000

Units sold 400000

Profit'/units sold

Profit per unit 225

9

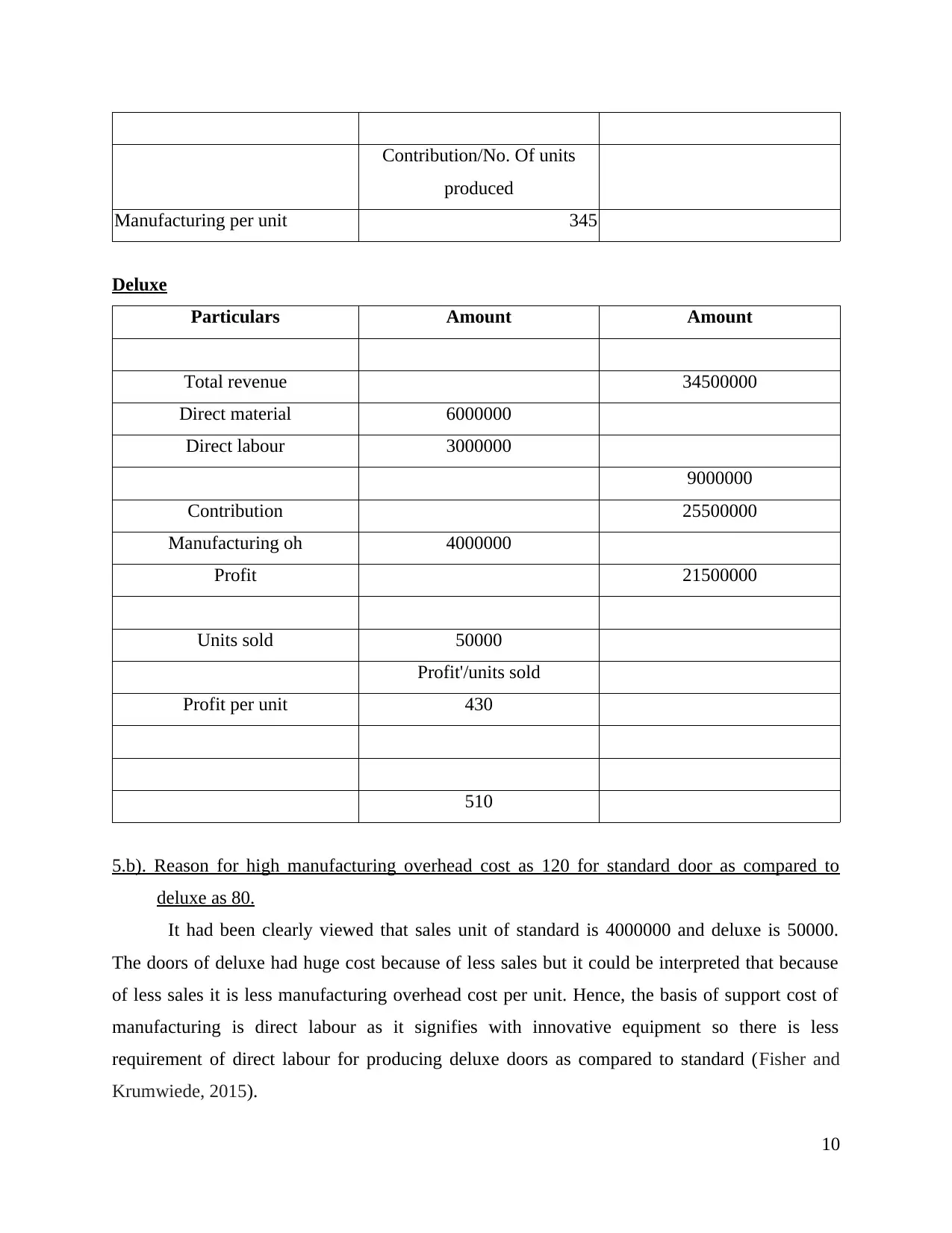

Contribution/No. Of units

produced

Manufacturing per unit 345

Deluxe

Particulars Amount Amount

Total revenue 34500000

Direct material 6000000

Direct labour 3000000

9000000

Contribution 25500000

Manufacturing oh 4000000

Profit 21500000

Units sold 50000

Profit'/units sold

Profit per unit 430

510

5.b). Reason for high manufacturing overhead cost as 120 for standard door as compared to

deluxe as 80.

It had been clearly viewed that sales unit of standard is 4000000 and deluxe is 50000.

The doors of deluxe had huge cost because of less sales but it could be interpreted that because

of less sales it is less manufacturing overhead cost per unit. Hence, the basis of support cost of

manufacturing is direct labour as it signifies with innovative equipment so there is less

requirement of direct labour for producing deluxe doors as compared to standard (Fisher and

Krumwiede, 2015).

10

produced

Manufacturing per unit 345

Deluxe

Particulars Amount Amount

Total revenue 34500000

Direct material 6000000

Direct labour 3000000

9000000

Contribution 25500000

Manufacturing oh 4000000

Profit 21500000

Units sold 50000

Profit'/units sold

Profit per unit 430

510

5.b). Reason for high manufacturing overhead cost as 120 for standard door as compared to

deluxe as 80.

It had been clearly viewed that sales unit of standard is 4000000 and deluxe is 50000.

The doors of deluxe had huge cost because of less sales but it could be interpreted that because

of less sales it is less manufacturing overhead cost per unit. Hence, the basis of support cost of

manufacturing is direct labour as it signifies with innovative equipment so there is less

requirement of direct labour for producing deluxe doors as compared to standard (Fisher and

Krumwiede, 2015).

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.