Management Accounting: Costing Methods and Decision-Making Report

VerifiedAdded on 2023/04/06

|13

|1176

|186

Report

AI Summary

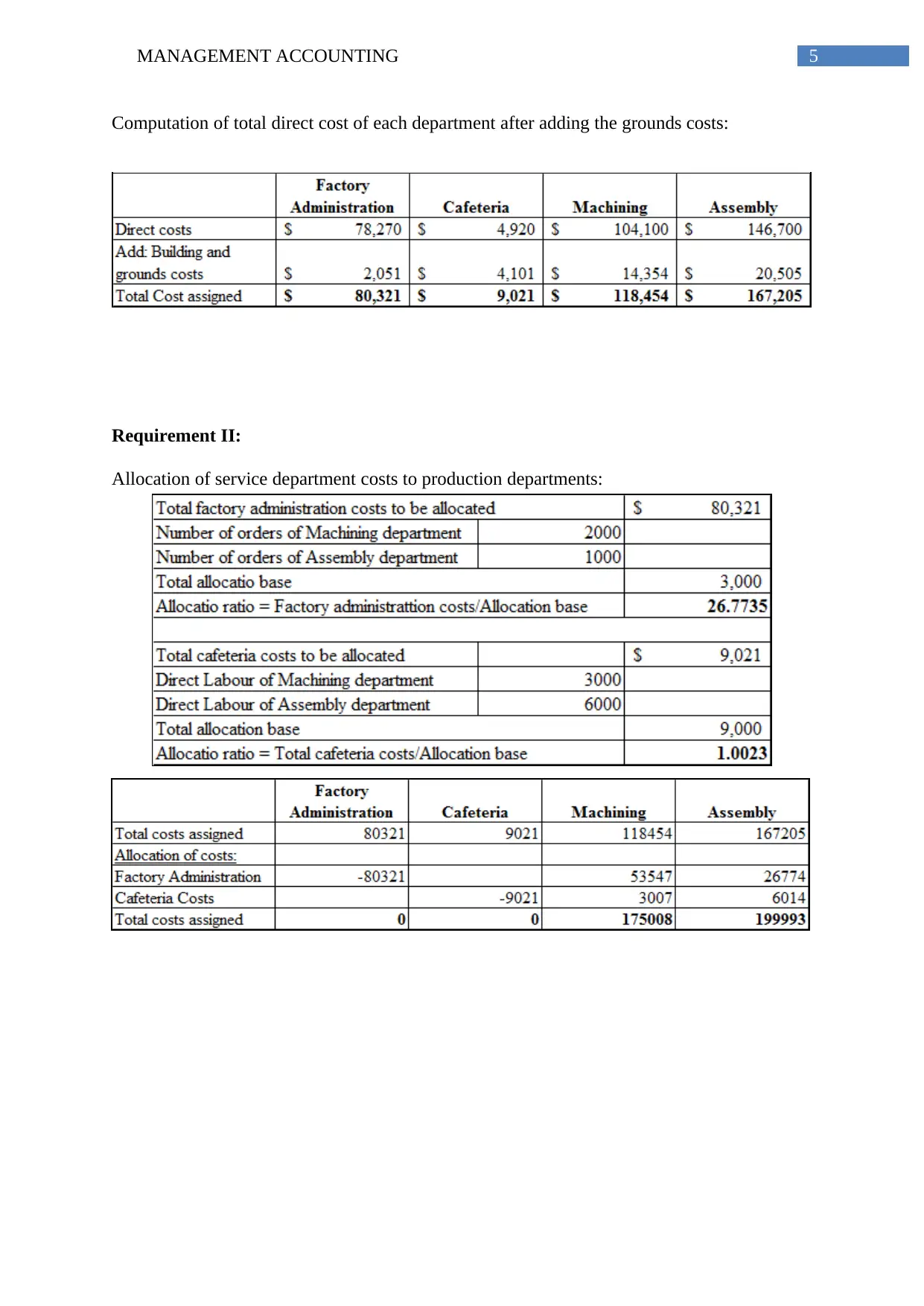

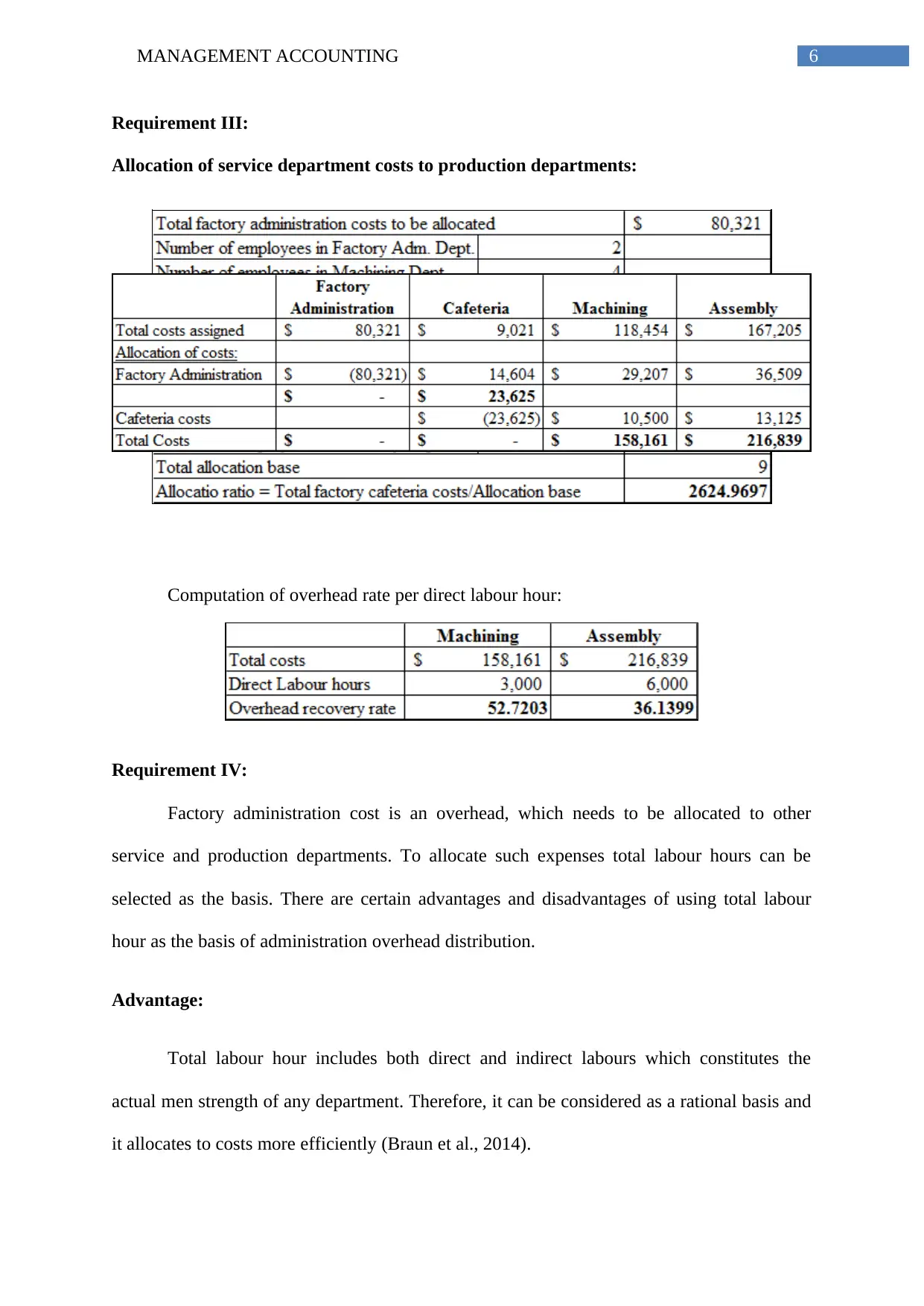

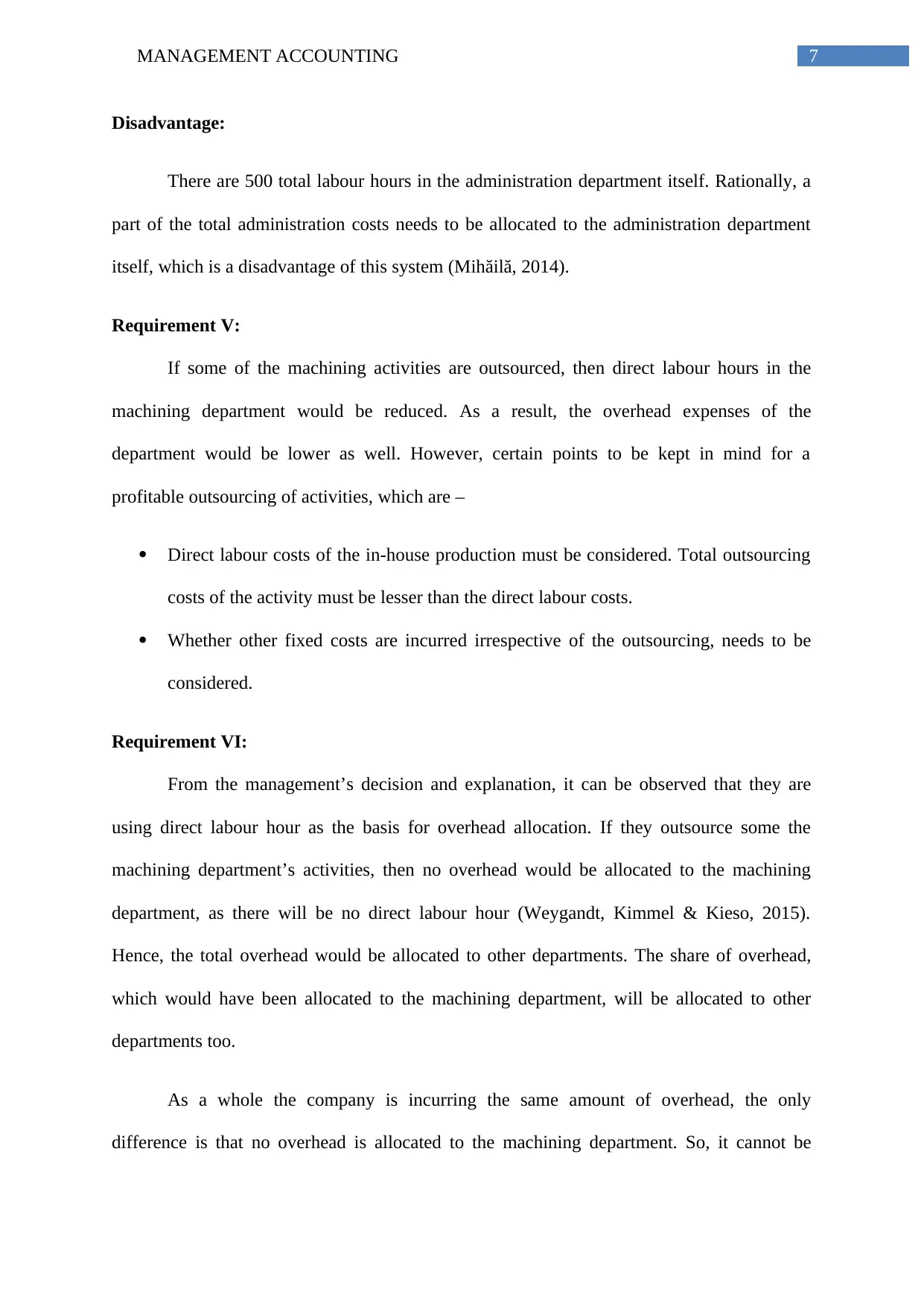

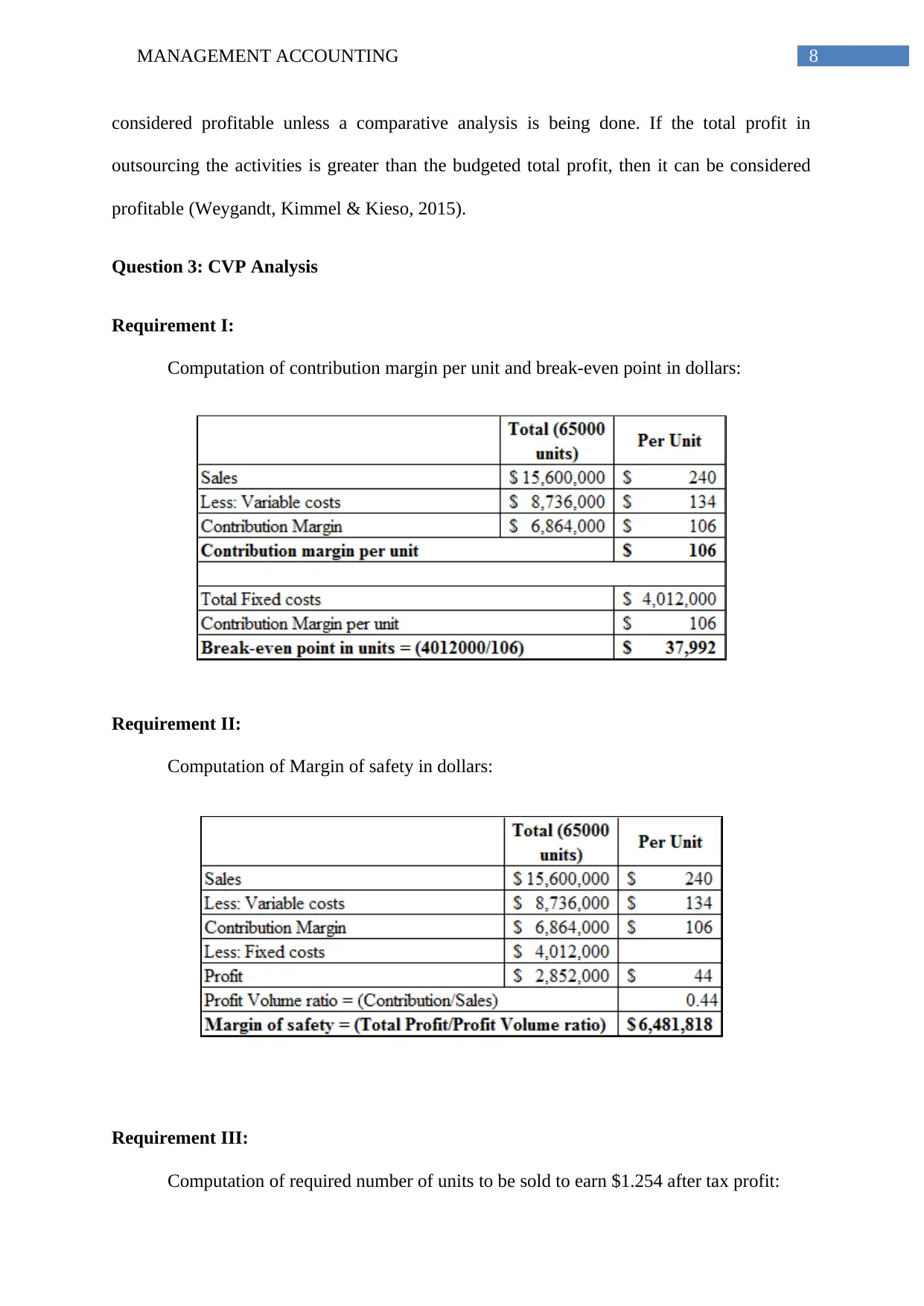

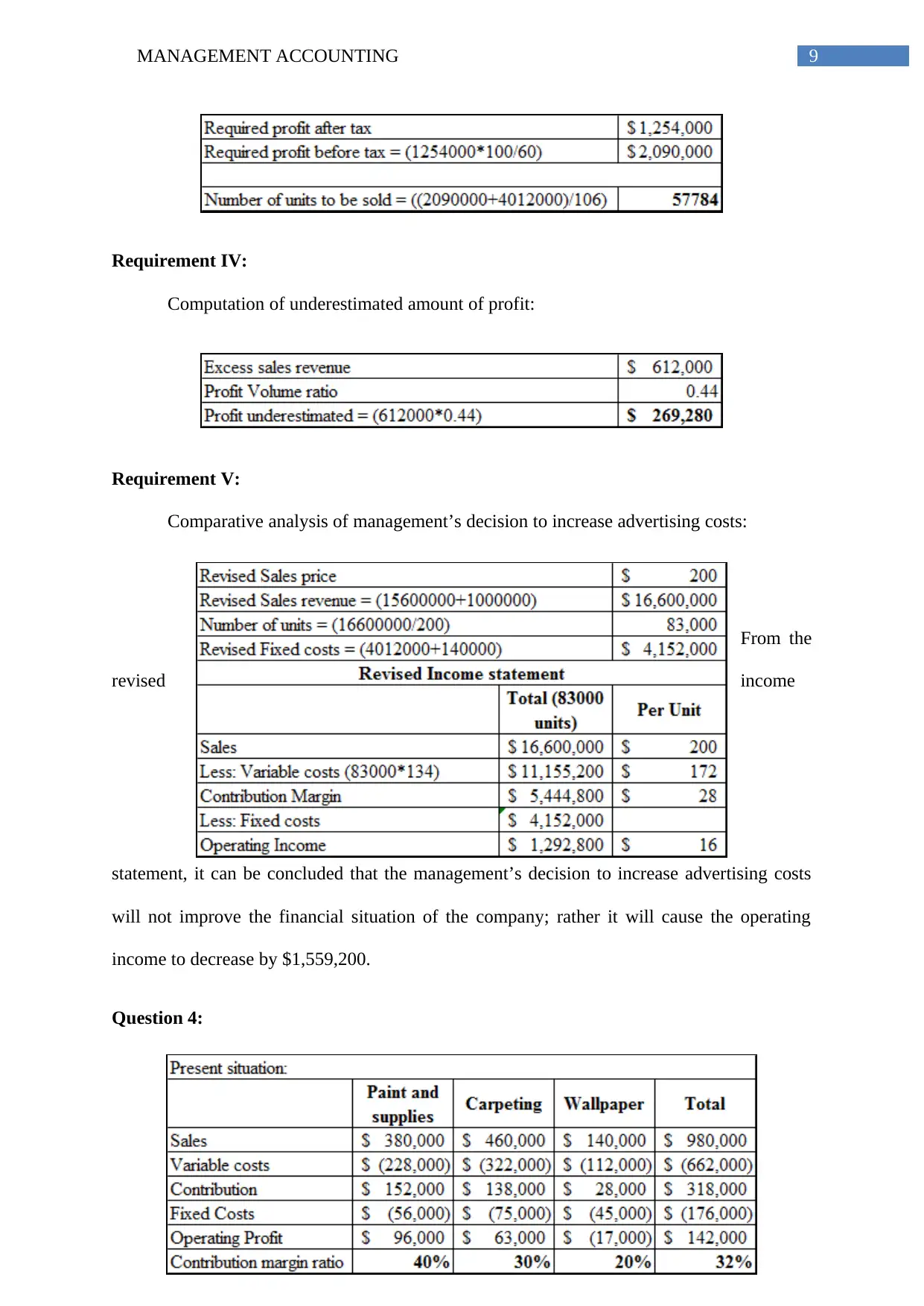

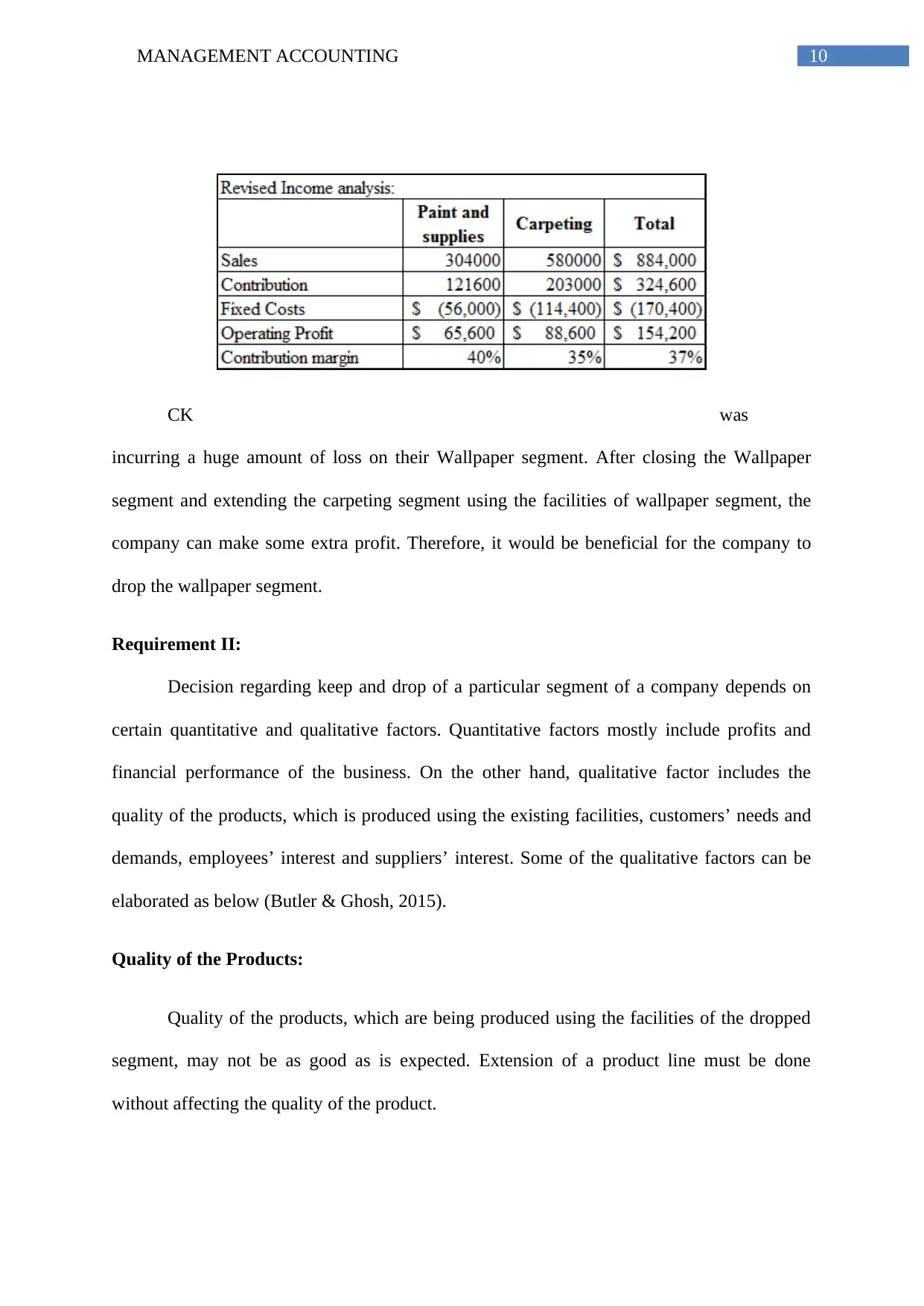

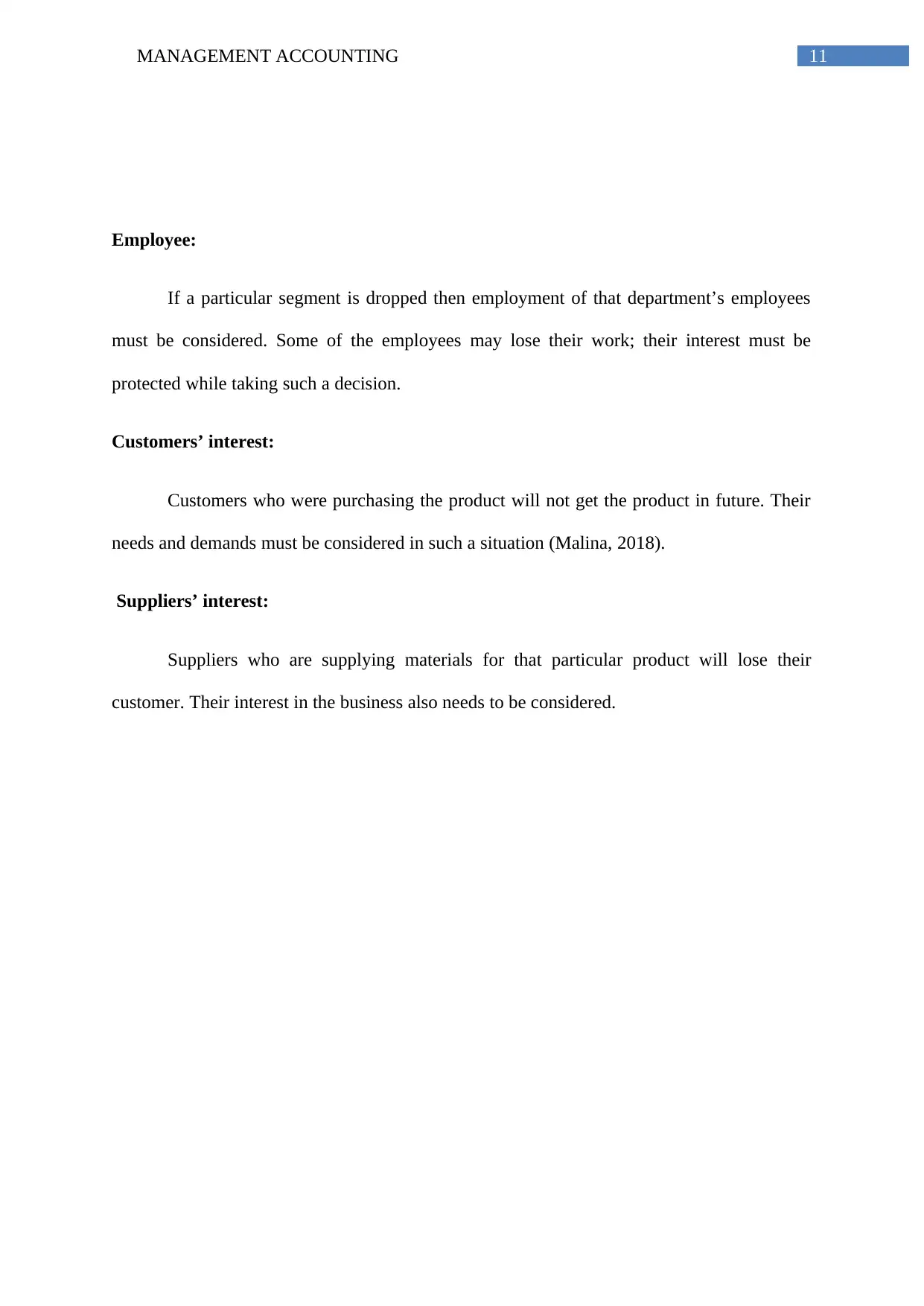

This management accounting assignment solution covers various key concepts and techniques. Part A focuses on cost assignment to cost pools, specifically for Mia's animal shelter, categorizing costs into housing, training, and healthcare services. Part B includes several questions addressing activity-based costing (ABC), support department cost allocation, cost-volume-profit (CVP) analysis, and decision-making related to segment profitability. The ABC analysis identifies appropriate activity drivers for different cost pools. The cost allocation section examines direct, step-down, and reciprocal methods, highlighting the advantages and disadvantages of different allocation bases. The CVP analysis computes break-even points, margin of safety, and sales volume required to achieve target profits, also evaluating the impact of increased advertising costs. Finally, the report assesses the decision to drop a business segment, considering both quantitative and qualitative factors influencing such strategic choices. Desklib provides similar solved assignments and resources for students.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.