Management Accounting Report: Cost Analysis, Budgeting and Variances

VerifiedAdded on 2019/12/04

|18

|4873

|178

Report

AI Summary

This report delves into the core principles of management accounting, examining cost classification, various costing methods (including variable and absorption costing), and techniques for analyzing cost data. The report includes case studies of companies like Bittern Ltd, Next plc, and others, illustrating the practical application of these concepts. It explores different types of costs, such as those classified by nature, function, and behavior. The report then moves on to preparing and analyzing cost reports, using performance indicators to identify areas for improvement, and suggesting methods for cost reduction and value enhancement. Furthermore, the report covers the budgeting process, including selecting appropriate budgeting methods, preparing budgets, and conducting variance analysis to identify causes and recommend corrective actions. The report concludes with an overview of reconciled operating statements and reporting findings to management.

Management Accounting

1

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................4

TASK 1............................................................................................................................................4

1.1 Preparing report and classifying different types of cost........................................................4

1.2 Using different costing methods ...........................................................................................5

1.3 Calculating cost using appropriate techniques.......................................................................6

1.4 Analysing cost data using appropriate techniques.................................................................6

TASK 2............................................................................................................................................6

2.1 Preparing and analysing cost reports.....................................................................................6

2.2 Using performance indicators to identify potential improvement.........................................7

2.3 Suggesting improvements to reduce cost, enhance value and quality...................................7

TASK 3............................................................................................................................................8

3.1 Purpose and nature of budgeting process..............................................................................8

3.2 Selecting appropriate budgeting methods for organization and its needs.............................9

3.3 Preparing budgets according to the chosen budgeting method..............................................9

3.4 Preparing cash budget............................................................................................................9

TASK 4............................................................................................................................................9

4.1 Calculating variances, identifying possible causes and recommending corrective action....9

4.2 Preparing reconciled operating statement............................................................................10

4.3 Reporting findings to management in accordance with responsibility center.....................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

2

INTRODUCTION...........................................................................................................................4

TASK 1............................................................................................................................................4

1.1 Preparing report and classifying different types of cost........................................................4

1.2 Using different costing methods ...........................................................................................5

1.3 Calculating cost using appropriate techniques.......................................................................6

1.4 Analysing cost data using appropriate techniques.................................................................6

TASK 2............................................................................................................................................6

2.1 Preparing and analysing cost reports.....................................................................................6

2.2 Using performance indicators to identify potential improvement.........................................7

2.3 Suggesting improvements to reduce cost, enhance value and quality...................................7

TASK 3............................................................................................................................................8

3.1 Purpose and nature of budgeting process..............................................................................8

3.2 Selecting appropriate budgeting methods for organization and its needs.............................9

3.3 Preparing budgets according to the chosen budgeting method..............................................9

3.4 Preparing cash budget............................................................................................................9

TASK 4............................................................................................................................................9

4.1 Calculating variances, identifying possible causes and recommending corrective action....9

4.2 Preparing reconciled operating statement............................................................................10

4.3 Reporting findings to management in accordance with responsibility center.....................11

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

2

Index of Tables

Table 1: Variance calculation of May............................................................................................10

Table 2: Reconciled operating statement of May..........................................................................11

Table 3: Variance at 10% reduction in demand.............................................................................11

3

Table 1: Variance calculation of May............................................................................................10

Table 2: Reconciled operating statement of May..........................................................................11

Table 3: Variance at 10% reduction in demand.............................................................................11

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is the most important field of study which assists organization

to minimize cost and maximise profitability. It is helpful for corporation in determining aim of

the business and support accounting personnel to preparing long term investment plan. Present

report is based on different case scenario such as Bittern Ltd, Antoonio ltd and Toscanini Ltd.

These corporation deals in several types of products and services and cost structure of the same

has been referred in report. Furthermore, current report covers classification of cost by using

different costing methods. Routine cost analysis has also been prepared which serves as path for

taking corrective action when required. Apart from this, budgeting process and variances

analysis are explained.

TASK 1

1.1 Preparing report and classifying different types of cost

Classification of cost is imperative task which is based on requirement of every business.

These different costing methods are explained as follows-

By nature

The cost classification on the basis of nature is based on elements like material, labour

and expenses. The examples of material cost are taxes & duties, freight and insurance as well as

rebates (Bellah and et. al., 2013). On the other hand, labour cost is directly associated with

production activities which consists of salaries & wages and fringe benefits like gratuity, bonus

and incentives. Other expenses such as job processing charges are also included in cost

classification by nature.

By functions

According to the functions cost are classified under different aspects like production,

selling, administration as well as distribution. Along with that research & development and

administration. Furthermore, production cost can be direct and indirect that consists of all

expenses such as quality control, labour welfare expenses and salaries for staff (Chapman,

Hopwood and Shields, 2011). Furthermore, administration cost consists of legal, bank charges as

well as salaries of accountant staff. Similarly, example of selling cost are; royalty on sales, legal

4

Management accounting is the most important field of study which assists organization

to minimize cost and maximise profitability. It is helpful for corporation in determining aim of

the business and support accounting personnel to preparing long term investment plan. Present

report is based on different case scenario such as Bittern Ltd, Antoonio ltd and Toscanini Ltd.

These corporation deals in several types of products and services and cost structure of the same

has been referred in report. Furthermore, current report covers classification of cost by using

different costing methods. Routine cost analysis has also been prepared which serves as path for

taking corrective action when required. Apart from this, budgeting process and variances

analysis are explained.

TASK 1

1.1 Preparing report and classifying different types of cost

Classification of cost is imperative task which is based on requirement of every business.

These different costing methods are explained as follows-

By nature

The cost classification on the basis of nature is based on elements like material, labour

and expenses. The examples of material cost are taxes & duties, freight and insurance as well as

rebates (Bellah and et. al., 2013). On the other hand, labour cost is directly associated with

production activities which consists of salaries & wages and fringe benefits like gratuity, bonus

and incentives. Other expenses such as job processing charges are also included in cost

classification by nature.

By functions

According to the functions cost are classified under different aspects like production,

selling, administration as well as distribution. Along with that research & development and

administration. Furthermore, production cost can be direct and indirect that consists of all

expenses such as quality control, labour welfare expenses and salaries for staff (Chapman,

Hopwood and Shields, 2011). Furthermore, administration cost consists of legal, bank charges as

well as salaries of accountant staff. Similarly, example of selling cost are; royalty on sales, legal

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

expenses and market research cost. In addition to this, distribution cost are related to

transportation and delivery of products and services (Gesimba, Alvar and Mante, 2014).

by Behaviour

The cost classification as per behaviour consists of fixed, variables and semi-variable

cost. Here, fixed cost varies in accordance with volume of production where variable cost does

not. Apart from this, semi-variable cost is partly fixed and partly variable. Example of semi-

variable cost is telephone bill (Łukaszewski and Wilk, 2016). It reflects that Bittern Ltd

classifies cost on the basis of behaviour as case study is showing different types of cost such as

variable, semi-variables and fixed cost. Here, variable cost of organization includes production

and distribution where semi-variables cost consists of labour and fixed overhead is also there.

1.2 Using different costing methods

There are different costing methods which assists businesses to keep record related to

cost. It is helpful in setting margin of profit on cost so as to enhance overall rate of return. Here,

job costing is done to recognize cost of each job of business. This type of cost is applied for

machine tool manufacturers and generally engineering workshop (McKevitt and Davis, 2013).

Job costing facilitates Bittern Ltd to set margin of profit in accordance with each job performed.

It provides realistic results which support organization to ensure optimum utilization of limited

resources. Furthermore, contract costing is also important cost method wherein big job require

extensive time to complete the same. It assists organization to keep separate account for contract

costing. The contract cost is decided on the basis of work to be done and time require. However,

information related to cost, labour and specific requirement of client also matters thereby cost

can be fluctuate. Apart from this contract cost be varied in accordance with external factors.

Owing to this, Bittern Ltd can should consider uncertainty and accordingly contract price is

decided with mutual consent of client and service providers.

The sector of civil engineering contractors and builders uses contract costing. Apart from

this, process cost applies in chemical, paper manufacturers and textile units (Shelby, 2013). This

is because in these industries products passes from different stages where it becomes important

to ascertain cost of each process. In addition to this, unit costing is another important method of

cost wherein cost of each unit produced in Bittern Ltd will be calculated.

5

transportation and delivery of products and services (Gesimba, Alvar and Mante, 2014).

by Behaviour

The cost classification as per behaviour consists of fixed, variables and semi-variable

cost. Here, fixed cost varies in accordance with volume of production where variable cost does

not. Apart from this, semi-variable cost is partly fixed and partly variable. Example of semi-

variable cost is telephone bill (Łukaszewski and Wilk, 2016). It reflects that Bittern Ltd

classifies cost on the basis of behaviour as case study is showing different types of cost such as

variable, semi-variables and fixed cost. Here, variable cost of organization includes production

and distribution where semi-variables cost consists of labour and fixed overhead is also there.

1.2 Using different costing methods

There are different costing methods which assists businesses to keep record related to

cost. It is helpful in setting margin of profit on cost so as to enhance overall rate of return. Here,

job costing is done to recognize cost of each job of business. This type of cost is applied for

machine tool manufacturers and generally engineering workshop (McKevitt and Davis, 2013).

Job costing facilitates Bittern Ltd to set margin of profit in accordance with each job performed.

It provides realistic results which support organization to ensure optimum utilization of limited

resources. Furthermore, contract costing is also important cost method wherein big job require

extensive time to complete the same. It assists organization to keep separate account for contract

costing. The contract cost is decided on the basis of work to be done and time require. However,

information related to cost, labour and specific requirement of client also matters thereby cost

can be fluctuate. Apart from this contract cost be varied in accordance with external factors.

Owing to this, Bittern Ltd can should consider uncertainty and accordingly contract price is

decided with mutual consent of client and service providers.

The sector of civil engineering contractors and builders uses contract costing. Apart from

this, process cost applies in chemical, paper manufacturers and textile units (Shelby, 2013). This

is because in these industries products passes from different stages where it becomes important

to ascertain cost of each process. In addition to this, unit costing is another important method of

cost wherein cost of each unit produced in Bittern Ltd will be calculated.

5

1.3 Calculating cost using appropriate techniques

Cost calculation is a major aspect of deciding on the profits of a business entity and

taking pricing decision. There are various tactics used for the calculation of cost such as

activity based costing, variable costing and absorption costing system.

Here, two major cost calculation tactics are explained :

Variable costing method : This is also called as Direct Costing System. The cited

costing method is a managerial accounting cost concept which is used to calculate cost while

ignoring fixed cost incurred in the period that a product is produced.

Absorption costing: This is also called as full costing method. The use of absorption

costing allows production department to fixed costs, in calculating the cost of production. The

advantage of absorption costing is that it provides a more accurate accounting of net profitability,

however, it does not support CVP analysis because it treats fixed manufacturing expenses as

variable cost.

1.4 Analysing cost data using appropriate techniques

According to the given case scenario, Bittern Ltd manufactures and sells a single product

at the price of £25 per unit. Previously, it operated a system of variable costing for management

accounting purposes now decided to review the system and to compare it for management

accounting purposes with an absorption costing system. Here is the calculation of Bittern’s

profits in constant-price-level terms over a three-year period in three different hypothetical using

variable costing system and full-cost absorption costing system.(I) Stable unit levels of production, sales and inventory

Variable costing

Particular t1(£) t2 (£) t3 (£)

Production Materials

cost 10000 10000 10000

Distribution cost 1000 1000 1000

Labour Cost 2000 2000 2000

Total production

cost 13000 13000 13000

Selling price (25) 25000 25000 25000

Bittern’s Profit 12000 12000 12000

6

Cost calculation is a major aspect of deciding on the profits of a business entity and

taking pricing decision. There are various tactics used for the calculation of cost such as

activity based costing, variable costing and absorption costing system.

Here, two major cost calculation tactics are explained :

Variable costing method : This is also called as Direct Costing System. The cited

costing method is a managerial accounting cost concept which is used to calculate cost while

ignoring fixed cost incurred in the period that a product is produced.

Absorption costing: This is also called as full costing method. The use of absorption

costing allows production department to fixed costs, in calculating the cost of production. The

advantage of absorption costing is that it provides a more accurate accounting of net profitability,

however, it does not support CVP analysis because it treats fixed manufacturing expenses as

variable cost.

1.4 Analysing cost data using appropriate techniques

According to the given case scenario, Bittern Ltd manufactures and sells a single product

at the price of £25 per unit. Previously, it operated a system of variable costing for management

accounting purposes now decided to review the system and to compare it for management

accounting purposes with an absorption costing system. Here is the calculation of Bittern’s

profits in constant-price-level terms over a three-year period in three different hypothetical using

variable costing system and full-cost absorption costing system.(I) Stable unit levels of production, sales and inventory

Variable costing

Particular t1(£) t2 (£) t3 (£)

Production Materials

cost 10000 10000 10000

Distribution cost 1000 1000 1000

Labour Cost 2000 2000 2000

Total production

cost 13000 13000 13000

Selling price (25) 25000 25000 25000

Bittern’s Profit 12000 12000 12000

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

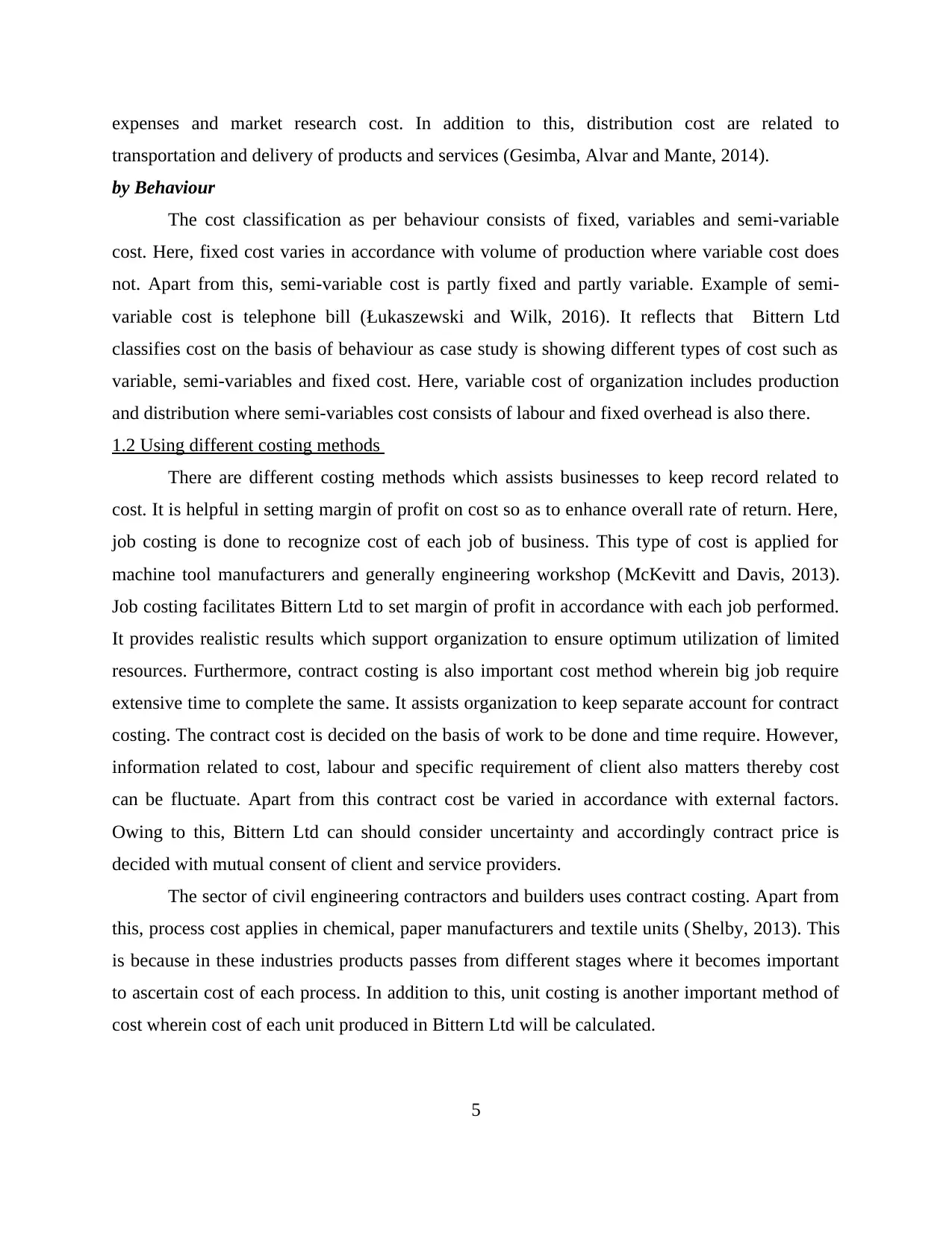

(Note : Here, considered £2 per unit as a variable cost and have avoided fixed one in variable

costing tactic)

Absorption costing

Particular t1(£) t2 (£) t3 (£)

Production materials

cost 10000 10000 10000

Distribution cost 1000 1000 1000

Labour cost 5000 5000 5000

Fixed cost 5000 5000 5000

Total production

cost 21000 21000 21000

Selling price (25) 25000 25000 25000

Bittern’s Profit 4000 4000 4000

(Note : Here, considered semi variable expenses to be £5000)

(II)Stable unit level of sales, but fluctuating unit levels of production and inventory

Variable costing

Particular t1(£) t2 (£) t3 (£)

Production materials

cost 15000 8000 7000

Distribution cost 1000 1000 1000

Labour cost 3000 1600 1400

Total production

cost 19000 10600 9400

Selling price (25) 25000 25000 25000

Profit 6000 14400 15600

Absorption costing

Particular t1(£) t2 (£) t3 (£)

Production materials

cost 15000 8000 7000

Distribution cost 1000 1000 1000

Labour cost 6000 1600 1400

Fixed cost 5000 5000 5000

Total production 27000 15600 14400

7

costing tactic)

Absorption costing

Particular t1(£) t2 (£) t3 (£)

Production materials

cost 10000 10000 10000

Distribution cost 1000 1000 1000

Labour cost 5000 5000 5000

Fixed cost 5000 5000 5000

Total production

cost 21000 21000 21000

Selling price (25) 25000 25000 25000

Bittern’s Profit 4000 4000 4000

(Note : Here, considered semi variable expenses to be £5000)

(II)Stable unit level of sales, but fluctuating unit levels of production and inventory

Variable costing

Particular t1(£) t2 (£) t3 (£)

Production materials

cost 15000 8000 7000

Distribution cost 1000 1000 1000

Labour cost 3000 1600 1400

Total production

cost 19000 10600 9400

Selling price (25) 25000 25000 25000

Profit 6000 14400 15600

Absorption costing

Particular t1(£) t2 (£) t3 (£)

Production materials

cost 15000 8000 7000

Distribution cost 1000 1000 1000

Labour cost 6000 1600 1400

Fixed cost 5000 5000 5000

Total production 27000 15600 14400

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

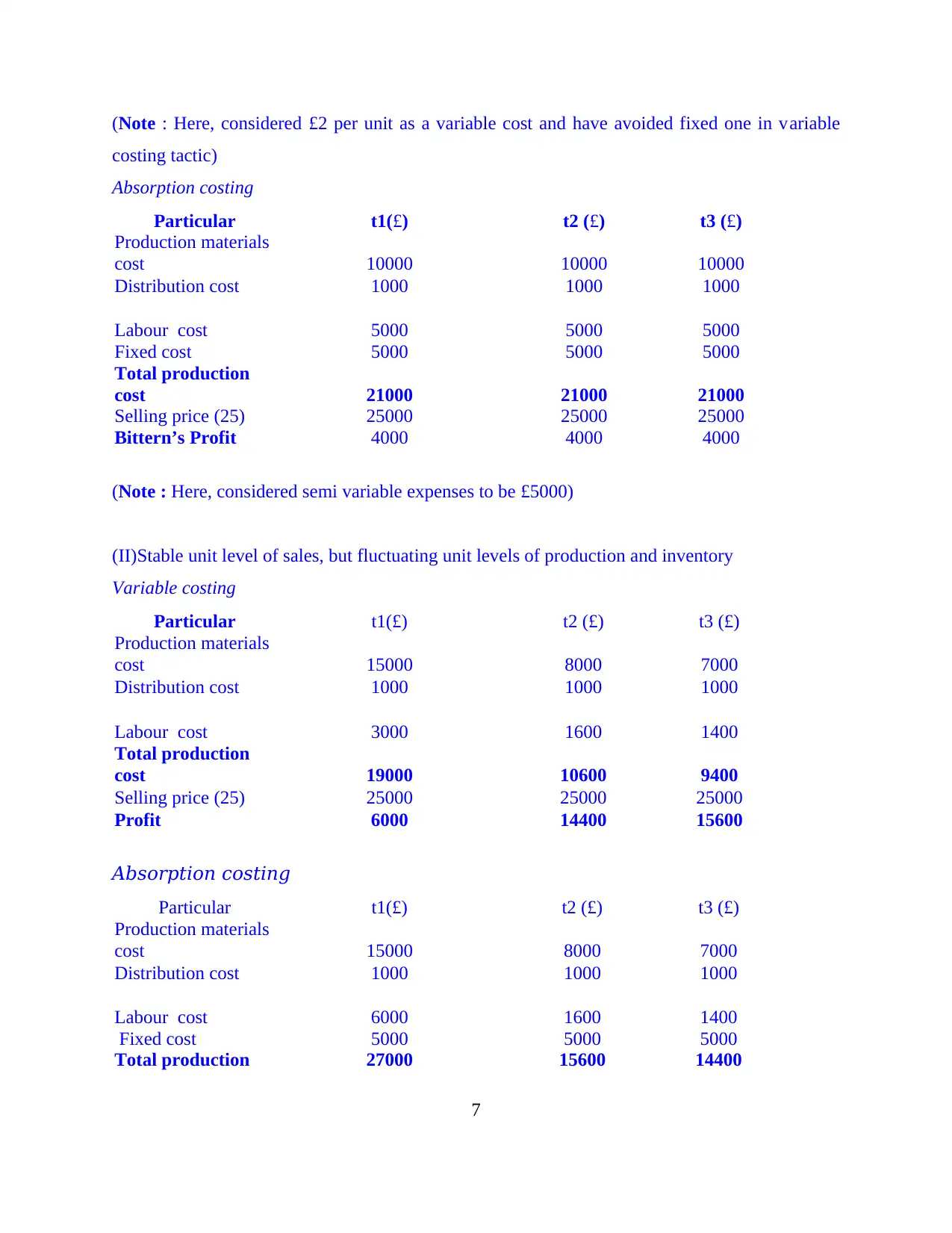

cost

Selling price (25) 25000 25000 25000

Profit -2000 9400 10600

(III) Stable unit level of production, but fluctuating unit levels of sales and

Inventory

Variable costing

Particular t1(£) t2 (£) t3 (£)

Production materials

cost 10000 10000 10000

Distribution cost 1000 1000 1000

Labour cost 2000 2000 2000

Total production

cost 13000 13000 13000

Selling price (25) 12500 30000 32500

Profit -500 17000 19500

Absorption costing

Particular t1(£) t2 (£) t3 (£)

Production materials

cost 10000 10000 10000

Distribution cost 1000 1000 1000

Labour cost 5000 5000 5000

Fixed cost 5000 5000 5000

Total production

cost 21000 21000 21000

Selling price (25) 12500 30000 32500

Profit -8500 9000 11500

TASK 2

Note: (Presentation is available separately)

2.1 Preparing and analysing cost reports

The preparation and analysis of cost report ensure inclusion of following aspects. The

selected organization for this task is Next plc, multinational clothing company. It also provides

home products and footwear to large number of buyers. This organization has around 700 stores.

8

Selling price (25) 25000 25000 25000

Profit -2000 9400 10600

(III) Stable unit level of production, but fluctuating unit levels of sales and

Inventory

Variable costing

Particular t1(£) t2 (£) t3 (£)

Production materials

cost 10000 10000 10000

Distribution cost 1000 1000 1000

Labour cost 2000 2000 2000

Total production

cost 13000 13000 13000

Selling price (25) 12500 30000 32500

Profit -500 17000 19500

Absorption costing

Particular t1(£) t2 (£) t3 (£)

Production materials

cost 10000 10000 10000

Distribution cost 1000 1000 1000

Labour cost 5000 5000 5000

Fixed cost 5000 5000 5000

Total production

cost 21000 21000 21000

Selling price (25) 12500 30000 32500

Profit -8500 9000 11500

TASK 2

Note: (Presentation is available separately)

2.1 Preparing and analysing cost reports

The preparation and analysis of cost report ensure inclusion of following aspects. The

selected organization for this task is Next plc, multinational clothing company. It also provides

home products and footwear to large number of buyers. This organization has around 700 stores.

8

Gathering information-Under this, management of Next plc will collect all important

information related to cost. For this purpose, total sales turnover can be taken into

account so as to refer number of units sold during particular time span. Itemize tangible cost-This point deals with tangible cost such as labour, material ad other

related stock incurred during production process. It assists management of Next plc to

keep record related to actual expenses incurred during particular time span. Categorize intangible cost-Under this part intangible cost will be recorded such as

expenses made for goodwill of business. It enables Next plc to calculate cost in right

manner so as to set margin of profit accordingly. Preparing structure of report-This segment deals with structure of cost wherein all

aspects are described in detail. Here, production cost, distribution and selling expenses

will be recorded. It proves to be effective in showing overall calculation related to

products and services. Conduct cost benefit analysis-This is the section for analysing cost data wherein finance

personnel analyse the cost in the light of benefit derived. It assists company to analyse

financial performance against objectives of corporation which leads create strong position

of Next plc in the marketplace.

Calculating payback time- This is part of analysis of cost data under which finance

department tends to assess the benefits derived after recovering initial cost. It facilitates

Next plc to accomplish its long as well as short term objectives.

2.2 Using performance indicators to identify potential improvement

The performance indicators plays important role for any organization because it helps

management to take corrective action in accordance with derived outcome. These are explained

as follows- High profitability-Profitability is one of the most performance indicator that provide

detail information to management regarding decrease and increase in earning per share

(Brigham and Houston, 2011). For example in case Next plc is having higher profitability

then it indicates favourable results for organization. It facilitates to increase overall rate

of return. In case corporation is not generating enough profitability then company will

take necessary action to improve its performance.

9

information related to cost. For this purpose, total sales turnover can be taken into

account so as to refer number of units sold during particular time span. Itemize tangible cost-This point deals with tangible cost such as labour, material ad other

related stock incurred during production process. It assists management of Next plc to

keep record related to actual expenses incurred during particular time span. Categorize intangible cost-Under this part intangible cost will be recorded such as

expenses made for goodwill of business. It enables Next plc to calculate cost in right

manner so as to set margin of profit accordingly. Preparing structure of report-This segment deals with structure of cost wherein all

aspects are described in detail. Here, production cost, distribution and selling expenses

will be recorded. It proves to be effective in showing overall calculation related to

products and services. Conduct cost benefit analysis-This is the section for analysing cost data wherein finance

personnel analyse the cost in the light of benefit derived. It assists company to analyse

financial performance against objectives of corporation which leads create strong position

of Next plc in the marketplace.

Calculating payback time- This is part of analysis of cost data under which finance

department tends to assess the benefits derived after recovering initial cost. It facilitates

Next plc to accomplish its long as well as short term objectives.

2.2 Using performance indicators to identify potential improvement

The performance indicators plays important role for any organization because it helps

management to take corrective action in accordance with derived outcome. These are explained

as follows- High profitability-Profitability is one of the most performance indicator that provide

detail information to management regarding decrease and increase in earning per share

(Brigham and Houston, 2011). For example in case Next plc is having higher profitability

then it indicates favourable results for organization. It facilitates to increase overall rate

of return. In case corporation is not generating enough profitability then company will

take necessary action to improve its performance.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Sales turnover-Sales turnover is also important performance indicator through which

corporation can implement effective strategies for increasing the same (Chandra, 2011).

In case of high sales turnover company can take decision related to appropriate

investment project. On the other hand, low sales turnover is the sign of Next plc can take

appropriate measures for increase overall flow of production. Customer retention-This customer retention in Next plc is also effective or favourable

performance indicator. It reflects that customers are satisfied and they want to take

frequent repeat purchase decision (Hult, Craighead and Ketchen Jr,2010). On the

contrary, lower satisfaction level of buyers reflects that organization must take initiative

to improve product or service quality.

Cost reduction-Significant reduction in cost of products and services is also favourable

aspect which depicts that organization can easily operate its business at global level. This

tends to enhance profitability (Kaplan and Atkinson, 2015).

2.3 Suggesting improvements to reduce cost, enhance value and quality

There are several measures can be taken by organization to reduce cost and enhance

value as well as quality of products and services. These improvements are listed as follows- Cost reduction-The most effective method for reduction in reducing cost through

restructuring production process (Malhotra and Temponi, 2010). Under this organization

can review overall process of production which in turn company can easily reduce cost of

production. Effective management-For reducing cost, effective management can be ensued in term of

material, workforce and other related factors (Swayne, Duncan and Ginter, 2012). Here,

Next plc can provide training for its workforce so as enhance their skills and knowledge

so as to support production activities. Similarly, material should be managed in such a

manner that it saves storage cost and maintain consistent flow of production.

Value enhancement and Improvement in service quality

For value enhancement of business competent workforce must be there in organization

which tends to improve service quality (Talke, Salomo and Rost, 2010). However, management

must communicate regarding requirement of consumers so they can effectively increase

satisfaction level of the same. Furthermore, research and development activities should be

10

corporation can implement effective strategies for increasing the same (Chandra, 2011).

In case of high sales turnover company can take decision related to appropriate

investment project. On the other hand, low sales turnover is the sign of Next plc can take

appropriate measures for increase overall flow of production. Customer retention-This customer retention in Next plc is also effective or favourable

performance indicator. It reflects that customers are satisfied and they want to take

frequent repeat purchase decision (Hult, Craighead and Ketchen Jr,2010). On the

contrary, lower satisfaction level of buyers reflects that organization must take initiative

to improve product or service quality.

Cost reduction-Significant reduction in cost of products and services is also favourable

aspect which depicts that organization can easily operate its business at global level. This

tends to enhance profitability (Kaplan and Atkinson, 2015).

2.3 Suggesting improvements to reduce cost, enhance value and quality

There are several measures can be taken by organization to reduce cost and enhance

value as well as quality of products and services. These improvements are listed as follows- Cost reduction-The most effective method for reduction in reducing cost through

restructuring production process (Malhotra and Temponi, 2010). Under this organization

can review overall process of production which in turn company can easily reduce cost of

production. Effective management-For reducing cost, effective management can be ensued in term of

material, workforce and other related factors (Swayne, Duncan and Ginter, 2012). Here,

Next plc can provide training for its workforce so as enhance their skills and knowledge

so as to support production activities. Similarly, material should be managed in such a

manner that it saves storage cost and maintain consistent flow of production.

Value enhancement and Improvement in service quality

For value enhancement of business competent workforce must be there in organization

which tends to improve service quality (Talke, Salomo and Rost, 2010). However, management

must communicate regarding requirement of consumers so they can effectively increase

satisfaction level of the same. Furthermore, research and development activities should be

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

focused by corporation thereby customers expectations will be met by implementing appropriate

marketing strategies. Similarly, total quality management can be applied in business which leads

to maintain good quality of products and services.

TASK 3

3.1 Purpose and nature of budgeting process

Budget refers to the process of forecasting future cash and expenses incurred in business.

It aids to given certainty for business thereby management can effectively formulate strategies to

enhance overall rate of return. Furthermore, budget makes it possible for company to allocate

financial resources in an effectual manner. This tends to control expenses incurred on production

process with the implementation of right kind of strategy. Similarly, budgeting process is helpful

in implementing policy decisions. Therefore, the budget serves as important managerial tools

which proves to be effective in implementing important strategies such expansion.

The process of budget begins with setting goals such as profit maximization, high

customer base and reduction in cost of production. After setting objectives necessary information

is gathered from internal and external environment of business. This facilitates to forecast future

need of business in an effectual manner. Accordingly budget is prepared for future time span of

Antonio Ltd and after completing overall process the phase of budgeting implementation begins.

Apart from this, after implementation of budget the same will be controlled with active efforts of

management of Antonio Ltd. The last process is of evaluation of business performance against

set objectives.

3.2 Selecting appropriate budgeting methods for organization and its needs

There are several budget methods like sales, cash and operating as well as production

budget. The selected budget methods are zero base budgeting and cash budget. It facilitates

corporation in allocating financial resources in most effective project generating higher rate of

return. Here, cash budget is very important for organization as it depicts cash position of firm in

particular financial year. This is segregated into two parts such as income and expenses related to

future business activities. This derives cash balance at the end of each year so that accordingly

corporation can reduce uncertainties (Choosing a Budget Method, 2016).

On the other hand zero based budgeting is another methods wherein management just

prepare budget by taking into account current profit and loss. At the same time, corporation will

11

marketing strategies. Similarly, total quality management can be applied in business which leads

to maintain good quality of products and services.

TASK 3

3.1 Purpose and nature of budgeting process

Budget refers to the process of forecasting future cash and expenses incurred in business.

It aids to given certainty for business thereby management can effectively formulate strategies to

enhance overall rate of return. Furthermore, budget makes it possible for company to allocate

financial resources in an effectual manner. This tends to control expenses incurred on production

process with the implementation of right kind of strategy. Similarly, budgeting process is helpful

in implementing policy decisions. Therefore, the budget serves as important managerial tools

which proves to be effective in implementing important strategies such expansion.

The process of budget begins with setting goals such as profit maximization, high

customer base and reduction in cost of production. After setting objectives necessary information

is gathered from internal and external environment of business. This facilitates to forecast future

need of business in an effectual manner. Accordingly budget is prepared for future time span of

Antonio Ltd and after completing overall process the phase of budgeting implementation begins.

Apart from this, after implementation of budget the same will be controlled with active efforts of

management of Antonio Ltd. The last process is of evaluation of business performance against

set objectives.

3.2 Selecting appropriate budgeting methods for organization and its needs

There are several budget methods like sales, cash and operating as well as production

budget. The selected budget methods are zero base budgeting and cash budget. It facilitates

corporation in allocating financial resources in most effective project generating higher rate of

return. Here, cash budget is very important for organization as it depicts cash position of firm in

particular financial year. This is segregated into two parts such as income and expenses related to

future business activities. This derives cash balance at the end of each year so that accordingly

corporation can reduce uncertainties (Choosing a Budget Method, 2016).

On the other hand zero based budgeting is another methods wherein management just

prepare budget by taking into account current profit and loss. At the same time, corporation will

11

not assistance from previous budget. For the purpose of making cash budget all expanses are

calculated in accordance with production flow so that management can provide justification to

their higher authority (Different Budget Methods, 2016). Use of zero base budget proves to be

effective in efficient allocation of resources. It can be critically evaluated that zero base

budgeting require relatively extensive time and manpower. In addition to this, sales and

production budget are also important through which management of Antonio Ltd come to know

about expenses to be made in coming financial year. It will be helpful for corporation to enhance

sales turnover and reduce overall cost of production which leads to increase overall rate of

return. At the same time, Antonio Ltd should use production budget and sales budget for meeting

its objectives related to monetary aspect.

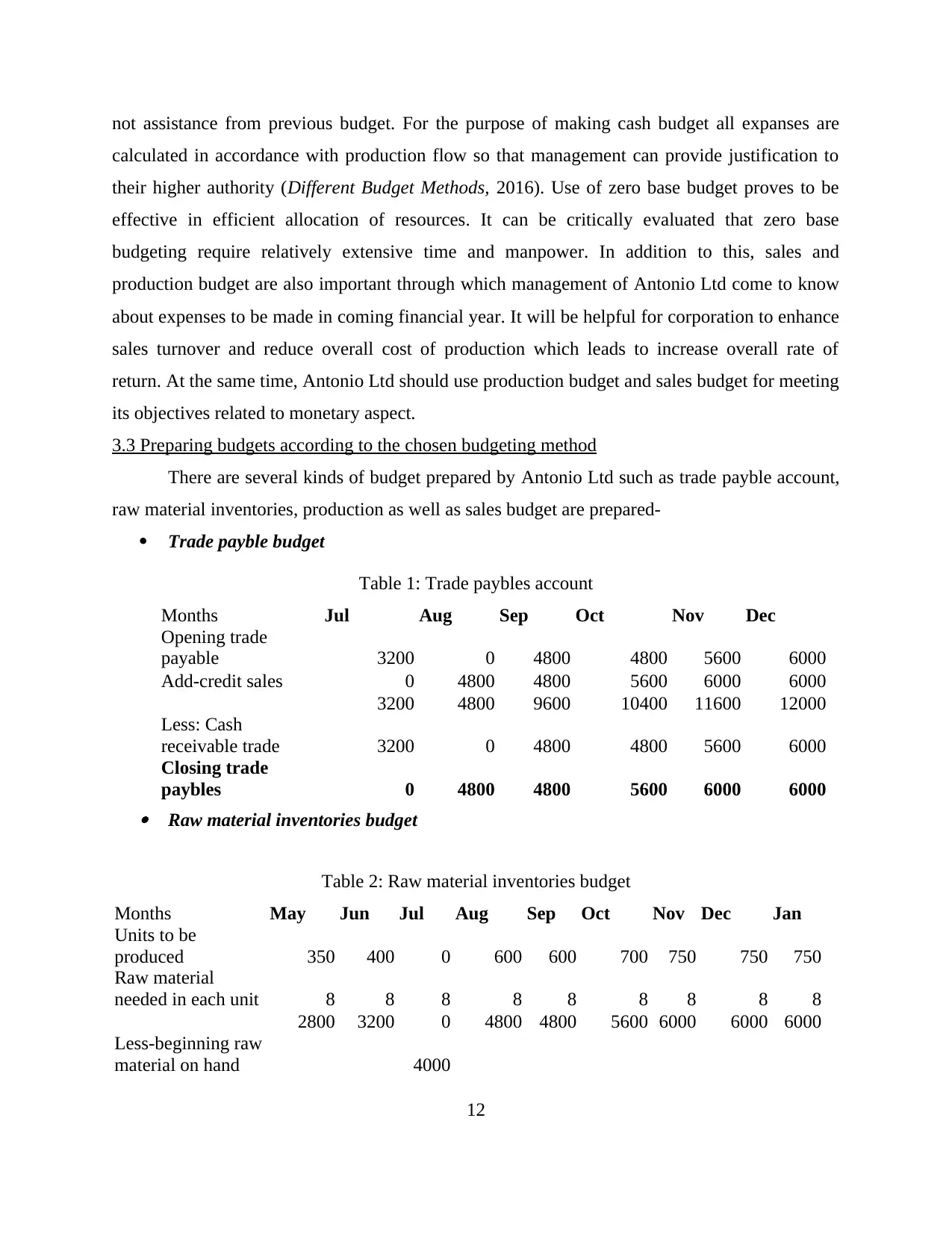

3.3 Preparing budgets according to the chosen budgeting method

There are several kinds of budget prepared by Antonio Ltd such as trade payble account,

raw material inventories, production as well as sales budget are prepared-

Trade payble budget

Table 1: Trade paybles account

Months Jul Aug Sep Oct Nov Dec

Opening trade

payable 3200 0 4800 4800 5600 6000

Add-credit sales 0 4800 4800 5600 6000 6000

3200 4800 9600 10400 11600 12000

Less: Cash

receivable trade 3200 0 4800 4800 5600 6000

Closing trade

paybles 0 4800 4800 5600 6000 6000 Raw material inventories budget

Table 2: Raw material inventories budget

Months May Jun Jul Aug Sep Oct Nov Dec Jan

Units to be

produced 350 400 0 600 600 700 750 750 750

Raw material

needed in each unit 8 8 8 8 8 8 8 8 8

2800 3200 0 4800 4800 5600 6000 6000 6000

Less-beginning raw

material on hand 4000

12

calculated in accordance with production flow so that management can provide justification to

their higher authority (Different Budget Methods, 2016). Use of zero base budget proves to be

effective in efficient allocation of resources. It can be critically evaluated that zero base

budgeting require relatively extensive time and manpower. In addition to this, sales and

production budget are also important through which management of Antonio Ltd come to know

about expenses to be made in coming financial year. It will be helpful for corporation to enhance

sales turnover and reduce overall cost of production which leads to increase overall rate of

return. At the same time, Antonio Ltd should use production budget and sales budget for meeting

its objectives related to monetary aspect.

3.3 Preparing budgets according to the chosen budgeting method

There are several kinds of budget prepared by Antonio Ltd such as trade payble account,

raw material inventories, production as well as sales budget are prepared-

Trade payble budget

Table 1: Trade paybles account

Months Jul Aug Sep Oct Nov Dec

Opening trade

payable 3200 0 4800 4800 5600 6000

Add-credit sales 0 4800 4800 5600 6000 6000

3200 4800 9600 10400 11600 12000

Less: Cash

receivable trade 3200 0 4800 4800 5600 6000

Closing trade

paybles 0 4800 4800 5600 6000 6000 Raw material inventories budget

Table 2: Raw material inventories budget

Months May Jun Jul Aug Sep Oct Nov Dec Jan

Units to be

produced 350 400 0 600 600 700 750 750 750

Raw material

needed in each unit 8 8 8 8 8 8 8 8 8

2800 3200 0 4800 4800 5600 6000 6000 6000

Less-beginning raw

material on hand 4000

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.