Higher National Diploma in Business: Management Accounting Report

VerifiedAdded on 2022/12/26

|18

|3865

|88

Report

AI Summary

This report comprehensively examines management accounting concepts and techniques for decision-making within the context of a small to medium-sized enterprise (SME), Connect Catering Services. It begins by critically evaluating the integration of management accounting systems, such as cost accounting, inventory management, and job costing, with organizational processes. The report then delves into cost analysis, demonstrating the preparation of income statements using both marginal and absorption costing methods, complete with detailed calculations and reconciliations. Furthermore, it explores the application of planning tools, including break-even analysis and variance analysis, to address financial problems and support sustainable success. The report includes financial statements, break-even point analysis and variance analysis to showcase the application of the concepts. Finally, the report provides a conclusion summarizing the key findings and implications of the analysis.

Management

Accounting Concepts

and Techniques for

Decision Makers

Accounting Concepts

and Techniques for

Decision Makers

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1 Critically evaluate how management accounting systems and reporting are integrated

within organisational processes.......................................................................................................3

TASK 2 Calculate cost using appropriate techniques of cost analysis to prepare an Income

Statement using Marginal and Absorption Costs.............................................................................6

TASK 3 Evaluate how planning tools for accounting respond appropriately to solving financial

problems to lead organisations to sustainable success...................................................................11

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................3

TASK 1 Critically evaluate how management accounting systems and reporting are integrated

within organisational processes.......................................................................................................3

TASK 2 Calculate cost using appropriate techniques of cost analysis to prepare an Income

Statement using Marginal and Absorption Costs.............................................................................6

TASK 3 Evaluate how planning tools for accounting respond appropriately to solving financial

problems to lead organisations to sustainable success...................................................................11

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

Management accounting is apart of accounting which helps the management to

understand financial information produced by financial accounting and make managerial

decisions on its basis. Management accounting is basically a procedure of interpreting, analysing

and communicating financial information which helps the management to identify the

shortcomings and achieve objectives and goals of the organisation (Berg and Madsen, 2020).

Connect Catering Services is a SME and a family owned business located at Oxfordshire. The

enterprise provides catering services within the city. Connect Catering feels that the

implementation of the management accounting systems along with financial accounting systems

would enable them to strengthen its decision making which will help the enterprise to survive in

the long run and in this competitive market. In this report various management accounting

system which are essential while making organisational decisions. Various techniques of cost

determination are used and explained.

TASK 1 Critically evaluate how management accounting systems and

reporting are integrated within organisational processes

Management Accounting assists the management in making significant decisions related

to the activities and management of the organisation. These decisions may include; number of

units to be sold in order to earn profit, price determination or how much bonus can the company

is able to give to its members. This further assist the business in working with efficiency and

grabbing every opportunity of growth and expansion.

Here the situation of Connect Catering services will be analysed with the help of

management accounting systems. Connect Caters will be able to obtain organisational reports

with the help of management accounting and with the help of these reports it will be able to

make necessary changes and take required decisions in the organisation itself and the

management.

Management Accounting will provide the organisation with financial information related

to the sale and development of services which will help in preparing financial budgets to

improve efficiency of the management (Căpușneanu and et. Al, 2020).

Majorly used Management Accounting Systems are:

Management accounting is apart of accounting which helps the management to

understand financial information produced by financial accounting and make managerial

decisions on its basis. Management accounting is basically a procedure of interpreting, analysing

and communicating financial information which helps the management to identify the

shortcomings and achieve objectives and goals of the organisation (Berg and Madsen, 2020).

Connect Catering Services is a SME and a family owned business located at Oxfordshire. The

enterprise provides catering services within the city. Connect Catering feels that the

implementation of the management accounting systems along with financial accounting systems

would enable them to strengthen its decision making which will help the enterprise to survive in

the long run and in this competitive market. In this report various management accounting

system which are essential while making organisational decisions. Various techniques of cost

determination are used and explained.

TASK 1 Critically evaluate how management accounting systems and

reporting are integrated within organisational processes

Management Accounting assists the management in making significant decisions related

to the activities and management of the organisation. These decisions may include; number of

units to be sold in order to earn profit, price determination or how much bonus can the company

is able to give to its members. This further assist the business in working with efficiency and

grabbing every opportunity of growth and expansion.

Here the situation of Connect Catering services will be analysed with the help of

management accounting systems. Connect Caters will be able to obtain organisational reports

with the help of management accounting and with the help of these reports it will be able to

make necessary changes and take required decisions in the organisation itself and the

management.

Management Accounting will provide the organisation with financial information related

to the sale and development of services which will help in preparing financial budgets to

improve efficiency of the management (Căpușneanu and et. Al, 2020).

Majorly used Management Accounting Systems are:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Cost Accounting System: It is one of the most significant system of

management accounting system. Accounting techniques in this system helps in

identifying certain costs involved in tasks and projects of the organisation, with

the help of this identification the management will be able to compare their

profits with their costs and take necessary decisions and plan accordingly. In

context to Connect Caters Services, the company uses Cost Accounting System

with which they are able to manage all their relevant cost like that of its

processes, raw materials and of supply and distribution of products manufactured

(Doktoralina and Apollo, 2019).

Inventory Management System: Inventory management system consists of

various techniques which assists the manager to maintain the level of stock in the

organisation. This system involves the process of stocking and restocking the

organisation's inventory so as to increase overall sales as stock will be available

when needed. Connect Caters Services uses this system with its various

techniques to manage inventory. Techniques may include LIFO, FIFO, JIT and

ABC analysis.

Job Costing System: Manufacturers of goods and services both use Job costing

system as it helps the accountant in estimating the cost required to perform every

job. With the help of this system the accountant is able to assess costs of every

department separately (Le and Dang, 2020). Job costing system measure the cost

which is required for executing business activities and completion of jobs. The

information obtained by this analysis is used by the managers to formulate

trading strategies which proves to be very useful for the business.

Management accounting reporting is a system which helps the book keeper to display

management accounting information in an effective form which aids the business to make

significant strategic decisions to make the organisation more efficient. Management accounting

reporting highlights the profitability of the business so that the equity capital holders of the

company can analyse it. This segment has various techniques like budgetary report, account

receivable ageing report, job costs report etc.

Budgetary Reports: Budget reports have proved significant in measuring performance

of any business in financial terms. Budget reports are generally developed for small and

management accounting system. Accounting techniques in this system helps in

identifying certain costs involved in tasks and projects of the organisation, with

the help of this identification the management will be able to compare their

profits with their costs and take necessary decisions and plan accordingly. In

context to Connect Caters Services, the company uses Cost Accounting System

with which they are able to manage all their relevant cost like that of its

processes, raw materials and of supply and distribution of products manufactured

(Doktoralina and Apollo, 2019).

Inventory Management System: Inventory management system consists of

various techniques which assists the manager to maintain the level of stock in the

organisation. This system involves the process of stocking and restocking the

organisation's inventory so as to increase overall sales as stock will be available

when needed. Connect Caters Services uses this system with its various

techniques to manage inventory. Techniques may include LIFO, FIFO, JIT and

ABC analysis.

Job Costing System: Manufacturers of goods and services both use Job costing

system as it helps the accountant in estimating the cost required to perform every

job. With the help of this system the accountant is able to assess costs of every

department separately (Le and Dang, 2020). Job costing system measure the cost

which is required for executing business activities and completion of jobs. The

information obtained by this analysis is used by the managers to formulate

trading strategies which proves to be very useful for the business.

Management accounting reporting is a system which helps the book keeper to display

management accounting information in an effective form which aids the business to make

significant strategic decisions to make the organisation more efficient. Management accounting

reporting highlights the profitability of the business so that the equity capital holders of the

company can analyse it. This segment has various techniques like budgetary report, account

receivable ageing report, job costs report etc.

Budgetary Reports: Budget reports have proved significant in measuring performance

of any business in financial terms. Budget reports are generally developed for small and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

medium scale enterprises but they also are used in large-scale enterprises by considering

various departments. They are made on the basis of past performance of the business and

with this analysis they can predict future unfavourable situations (Mahajan and

Deobagkar, 2020). Budgets are equipped with the information based on the present costs

and expenditure which are compared to expected or future expenditure and costs.

Accounting reports which are obtained from budgets assists the management in forming

strategies to earn more profit, reducing costs and understand the behaviour of suppliers

and stakeholders. It will enable Connect Catering Services to compare present

performance with the predicted performance. With the budget report Connect Caters

estimate the amount of expected profit and filter out activities that can become the cause

of failure in achieving so. It also helps in analysing new opportunities which are there in

the market and also which will arrive in the near future.

Account Receivable Ageing Report: Businesses dependent on non-cash sales maintain

account receivable ageing reports. These are of great significance for the business itself.

With the help of this report the management is able to identify accounts of receivables

who frequently turn into bad debts and the management also is able to find problems in

the collection process of the organisation (NICOLETA, 2019). Comparatively more bad

debt means the company will have to change its credit sales policy in a away that money

can be realised faster and no bad debts occur. Management with the help of these reports

will be able to keep a watch on the credit period of debtors and also the cash flow of the

business. This will aid the management in taking important decisions such as increasing

or decreasing the credit period as per the requirement of the company. With polices

formed by Connect Cater Services, the business will collect money from debtors in an

effective way with minimum bad debts.

Cost Reports: Purchase of inventory, cost incurred on labours and overheads are the

manufacturing costs for an organisation. Total manufacturing costs and other significant

costs are divided by the number of units produced or the monetary value of the services

produced. Cost reports contain information regarding the cost incurred on producing a

single unit along with its selling price and profit earned (Shariati, Talebnia and Royaee,

2020). This report assist the companies decide profit margins it should keep for their

products. It also helps the management to measure areas of significant expenditure,

various departments. They are made on the basis of past performance of the business and

with this analysis they can predict future unfavourable situations (Mahajan and

Deobagkar, 2020). Budgets are equipped with the information based on the present costs

and expenditure which are compared to expected or future expenditure and costs.

Accounting reports which are obtained from budgets assists the management in forming

strategies to earn more profit, reducing costs and understand the behaviour of suppliers

and stakeholders. It will enable Connect Catering Services to compare present

performance with the predicted performance. With the budget report Connect Caters

estimate the amount of expected profit and filter out activities that can become the cause

of failure in achieving so. It also helps in analysing new opportunities which are there in

the market and also which will arrive in the near future.

Account Receivable Ageing Report: Businesses dependent on non-cash sales maintain

account receivable ageing reports. These are of great significance for the business itself.

With the help of this report the management is able to identify accounts of receivables

who frequently turn into bad debts and the management also is able to find problems in

the collection process of the organisation (NICOLETA, 2019). Comparatively more bad

debt means the company will have to change its credit sales policy in a away that money

can be realised faster and no bad debts occur. Management with the help of these reports

will be able to keep a watch on the credit period of debtors and also the cash flow of the

business. This will aid the management in taking important decisions such as increasing

or decreasing the credit period as per the requirement of the company. With polices

formed by Connect Cater Services, the business will collect money from debtors in an

effective way with minimum bad debts.

Cost Reports: Purchase of inventory, cost incurred on labours and overheads are the

manufacturing costs for an organisation. Total manufacturing costs and other significant

costs are divided by the number of units produced or the monetary value of the services

produced. Cost reports contain information regarding the cost incurred on producing a

single unit along with its selling price and profit earned (Shariati, Talebnia and Royaee,

2020). This report assist the companies decide profit margins it should keep for their

products. It also helps the management to measure areas of significant expenditure,

along with exercising systematic analysis of total costs involved in specific projects.

Department of management of Connect Caters formulates documents to distinguishing

the explanation regarding extravagant cash outflow or costs which are not advantageous

for the company.

Performance Reports: To review the performance of a business at its workplace these

reports are formulated. In large-scale organisations performance reports of departments

are also developed. These reports are made to make decisions for the future of the

company. Exceptional workers who achieve targets on time and even exceed their goals

are appreciated for their performance in the organisation and under performers are given

warning and also motivation to work effectively. Connect Caters form performance

report to identify departments which are not working effectively and efficiently.

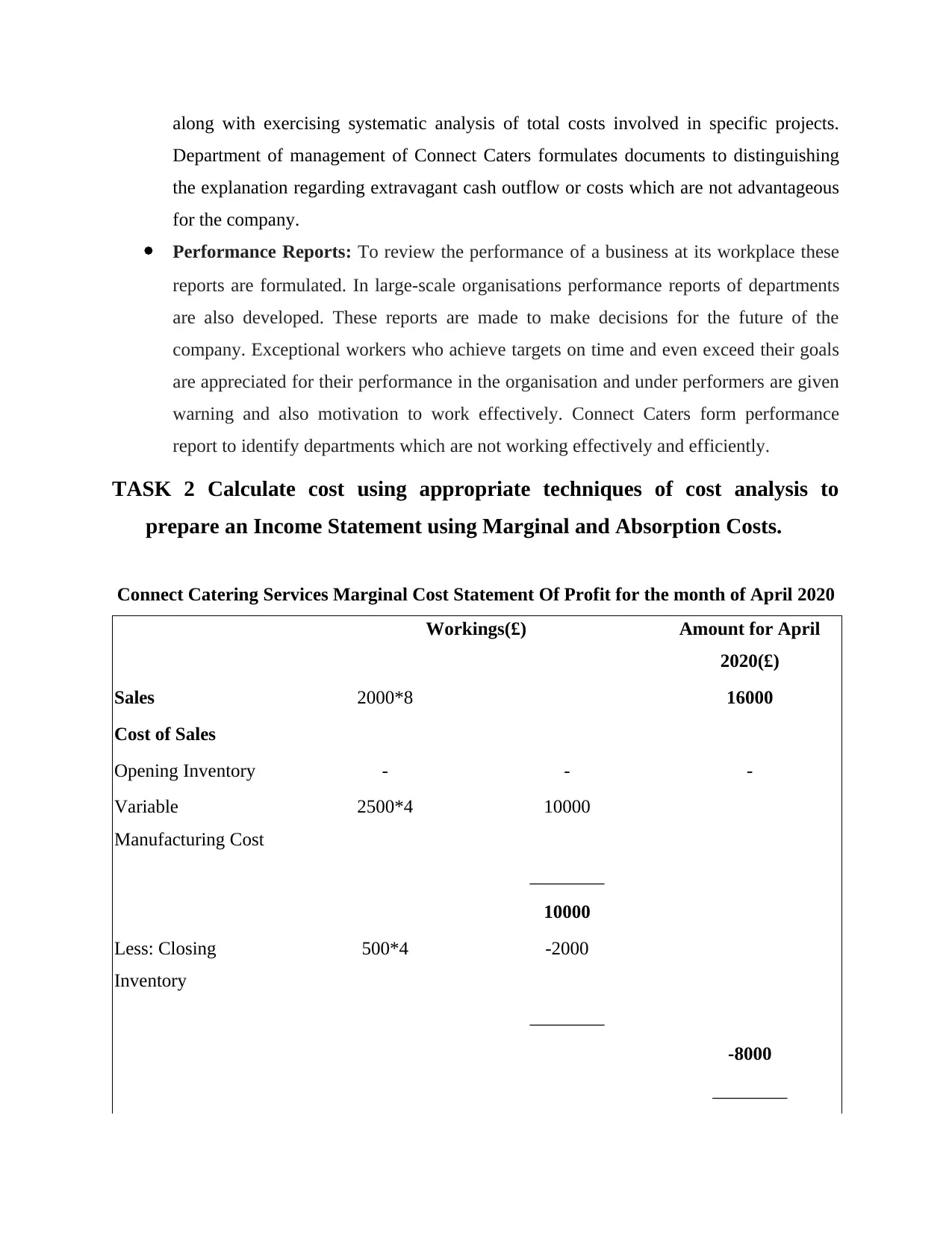

TASK 2 Calculate cost using appropriate techniques of cost analysis to

prepare an Income Statement using Marginal and Absorption Costs.

Connect Catering Services Marginal Cost Statement Of Profit for the month of April 2020

Workings(£) Amount for April

2020(£)

Sales 2000*8 16000

Cost of Sales

Opening Inventory - - -

Variable

Manufacturing Cost

2500*4 10000

________

10000

Less: Closing

Inventory

500*4 -2000

________

-8000

________

Department of management of Connect Caters formulates documents to distinguishing

the explanation regarding extravagant cash outflow or costs which are not advantageous

for the company.

Performance Reports: To review the performance of a business at its workplace these

reports are formulated. In large-scale organisations performance reports of departments

are also developed. These reports are made to make decisions for the future of the

company. Exceptional workers who achieve targets on time and even exceed their goals

are appreciated for their performance in the organisation and under performers are given

warning and also motivation to work effectively. Connect Caters form performance

report to identify departments which are not working effectively and efficiently.

TASK 2 Calculate cost using appropriate techniques of cost analysis to

prepare an Income Statement using Marginal and Absorption Costs.

Connect Catering Services Marginal Cost Statement Of Profit for the month of April 2020

Workings(£) Amount for April

2020(£)

Sales 2000*8 16000

Cost of Sales

Opening Inventory - - -

Variable

Manufacturing Cost

2500*4 10000

________

10000

Less: Closing

Inventory

500*4 -2000

________

-8000

________

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

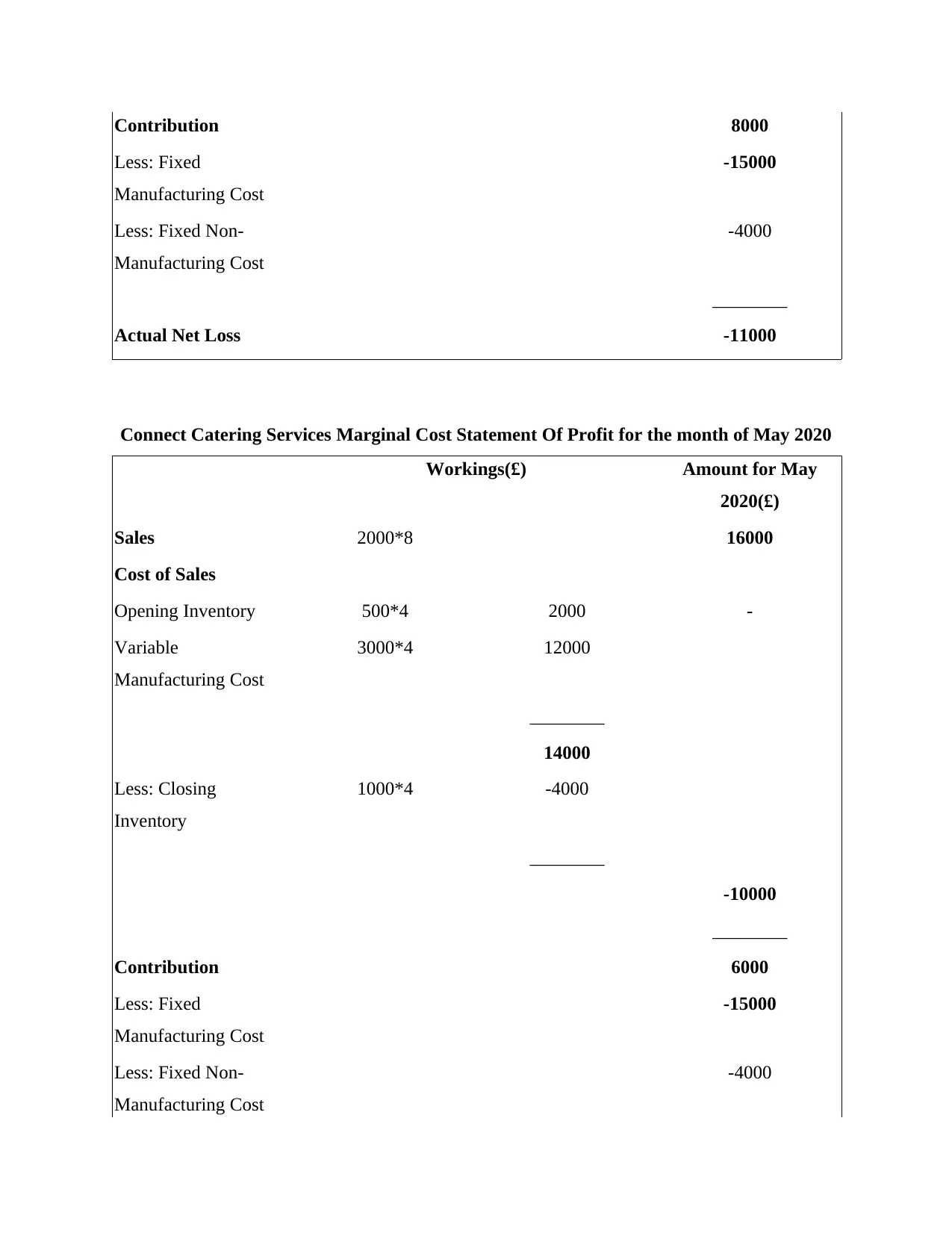

Contribution 8000

Less: Fixed

Manufacturing Cost

-15000

Less: Fixed Non-

Manufacturing Cost

-4000

________

Actual Net Loss -11000

Connect Catering Services Marginal Cost Statement Of Profit for the month of May 2020

Workings(£) Amount for May

2020(£)

Sales 2000*8 16000

Cost of Sales

Opening Inventory 500*4 2000 -

Variable

Manufacturing Cost

3000*4 12000

________

14000

Less: Closing

Inventory

1000*4 -4000

________

-10000

________

Contribution 6000

Less: Fixed

Manufacturing Cost

-15000

Less: Fixed Non-

Manufacturing Cost

-4000

Less: Fixed

Manufacturing Cost

-15000

Less: Fixed Non-

Manufacturing Cost

-4000

________

Actual Net Loss -11000

Connect Catering Services Marginal Cost Statement Of Profit for the month of May 2020

Workings(£) Amount for May

2020(£)

Sales 2000*8 16000

Cost of Sales

Opening Inventory 500*4 2000 -

Variable

Manufacturing Cost

3000*4 12000

________

14000

Less: Closing

Inventory

1000*4 -4000

________

-10000

________

Contribution 6000

Less: Fixed

Manufacturing Cost

-15000

Less: Fixed Non-

Manufacturing Cost

-4000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

________

Actual Net Loss -13000

Actual Net Loss -13000

Connect Catering Services Absorption Cost Statement of Profit for the month of April

2020

Workings(£) Amount for April

2020(£)

Sales 2000*8 16000

Cost of Sales

Opening Inventory - - -

Finished Goods 2500*10 25000

Less: Closing

Inventory

500*10 -5000

________

-20000

________

Actual Gross Loss -4000

Less: Fixed Non-

Manufacturing Cost

-4000

________

Actual Net Loss -8000

Connect Catering Services Absorption Cost Statement of Profit for the month of May 2020

Workings(£) Amount for May

2020(£)

Sales 2000*8 16000

Cost of Sales

Opening Inventory 500*9 4500 -

Finished Goods 3000*9 27000

2020

Workings(£) Amount for April

2020(£)

Sales 2000*8 16000

Cost of Sales

Opening Inventory - - -

Finished Goods 2500*10 25000

Less: Closing

Inventory

500*10 -5000

________

-20000

________

Actual Gross Loss -4000

Less: Fixed Non-

Manufacturing Cost

-4000

________

Actual Net Loss -8000

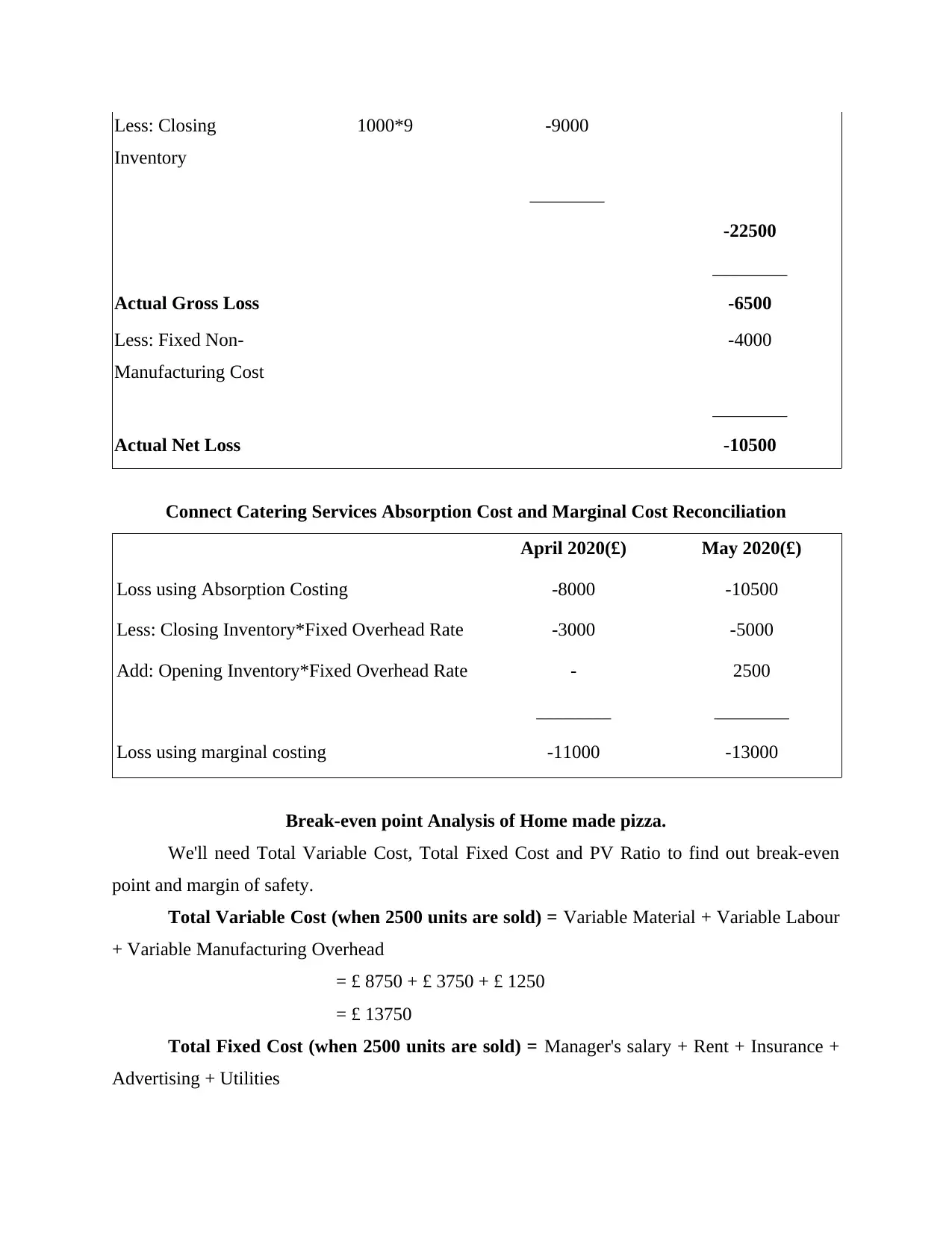

Connect Catering Services Absorption Cost Statement of Profit for the month of May 2020

Workings(£) Amount for May

2020(£)

Sales 2000*8 16000

Cost of Sales

Opening Inventory 500*9 4500 -

Finished Goods 3000*9 27000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Less: Closing

Inventory

1000*9 -9000

________

-22500

________

Actual Gross Loss -6500

Less: Fixed Non-

Manufacturing Cost

-4000

________

Actual Net Loss -10500

Connect Catering Services Absorption Cost and Marginal Cost Reconciliation

April 2020(£) May 2020(£)

Loss using Absorption Costing -8000 -10500

Less: Closing Inventory*Fixed Overhead Rate -3000 -5000

Add: Opening Inventory*Fixed Overhead Rate - 2500

________ ________

Loss using marginal costing -11000 -13000

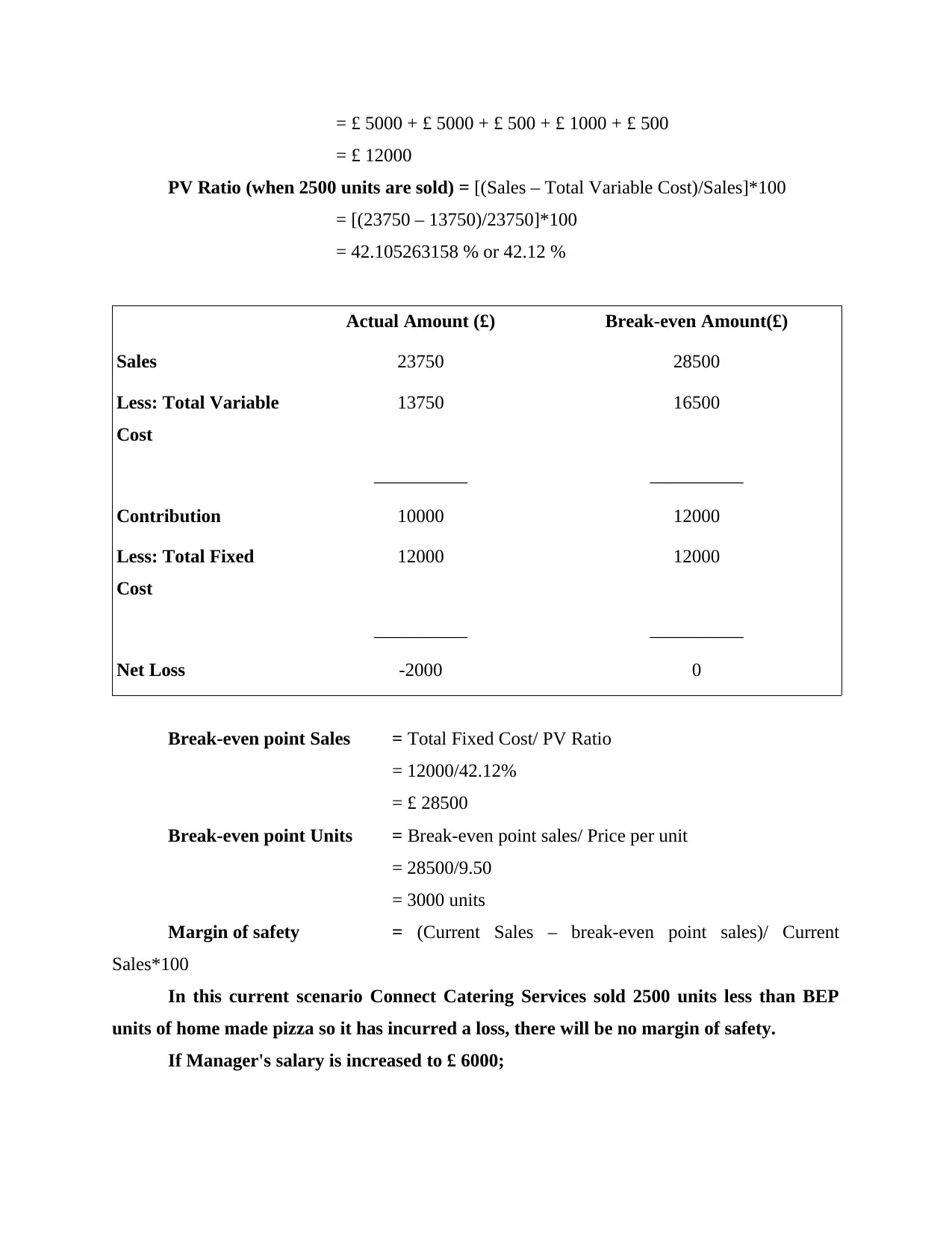

Break-even point Analysis of Home made pizza.

We'll need Total Variable Cost, Total Fixed Cost and PV Ratio to find out break-even

point and margin of safety.

Total Variable Cost (when 2500 units are sold) = Variable Material + Variable Labour

+ Variable Manufacturing Overhead

= £ 8750 + £ 3750 + £ 1250

= £ 13750

Total Fixed Cost (when 2500 units are sold) = Manager's salary + Rent + Insurance +

Advertising + Utilities

Inventory

1000*9 -9000

________

-22500

________

Actual Gross Loss -6500

Less: Fixed Non-

Manufacturing Cost

-4000

________

Actual Net Loss -10500

Connect Catering Services Absorption Cost and Marginal Cost Reconciliation

April 2020(£) May 2020(£)

Loss using Absorption Costing -8000 -10500

Less: Closing Inventory*Fixed Overhead Rate -3000 -5000

Add: Opening Inventory*Fixed Overhead Rate - 2500

________ ________

Loss using marginal costing -11000 -13000

Break-even point Analysis of Home made pizza.

We'll need Total Variable Cost, Total Fixed Cost and PV Ratio to find out break-even

point and margin of safety.

Total Variable Cost (when 2500 units are sold) = Variable Material + Variable Labour

+ Variable Manufacturing Overhead

= £ 8750 + £ 3750 + £ 1250

= £ 13750

Total Fixed Cost (when 2500 units are sold) = Manager's salary + Rent + Insurance +

Advertising + Utilities

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

= £ 5000 + £ 5000 + £ 500 + £ 1000 + £ 500

= £ 12000

PV Ratio (when 2500 units are sold) = [(Sales – Total Variable Cost)/Sales]*100

= [(23750 – 13750)/23750]*100

= 42.105263158 % or 42.12 %

Actual Amount (£) Break-even Amount(£)

Sales 23750 28500

Less: Total Variable

Cost

13750 16500

__________ __________

Contribution 10000 12000

Less: Total Fixed

Cost

12000 12000

__________ __________

Net Loss -2000 0

Break-even point Sales = Total Fixed Cost/ PV Ratio

= 12000/42.12%

= £ 28500

Break-even point Units = Break-even point sales/ Price per unit

= 28500/9.50

= 3000 units

Margin of safety = (Current Sales – break-even point sales)/ Current

Sales*100

In this current scenario Connect Catering Services sold 2500 units less than BEP

units of home made pizza so it has incurred a loss, there will be no margin of safety.

If Manager's salary is increased to £ 6000;

= £ 12000

PV Ratio (when 2500 units are sold) = [(Sales – Total Variable Cost)/Sales]*100

= [(23750 – 13750)/23750]*100

= 42.105263158 % or 42.12 %

Actual Amount (£) Break-even Amount(£)

Sales 23750 28500

Less: Total Variable

Cost

13750 16500

__________ __________

Contribution 10000 12000

Less: Total Fixed

Cost

12000 12000

__________ __________

Net Loss -2000 0

Break-even point Sales = Total Fixed Cost/ PV Ratio

= 12000/42.12%

= £ 28500

Break-even point Units = Break-even point sales/ Price per unit

= 28500/9.50

= 3000 units

Margin of safety = (Current Sales – break-even point sales)/ Current

Sales*100

In this current scenario Connect Catering Services sold 2500 units less than BEP

units of home made pizza so it has incurred a loss, there will be no margin of safety.

If Manager's salary is increased to £ 6000;

Total Fixed Cost will also increase to £ 13000, this change will affect the BEP in

following way:

Break-even point Sales = Total Fixed Cost/ PV Ratio

= 13000/42.12%

= £ 30875

Break-even point Units = Break-even point sales/ Price per unit

= 30875/9.50

= 3250 units

Variance Analysis Report

Actual Units Sold = 12000

Budgeted Units Sold = 10000

Budgeted price per unit = 9.50

Sales volume variance = (Actual units sold - Budgeted units sold) * Budgeted

price per unit

= (12000-10000) *9.50

= 2000*9.50

= 19000 Favourable

Flexible budget

Items Actual Budgeted Variance

Sales price 10 9.50 .50 Favourable

Sales units 12000 10000 2000 Favourable

Revenues 120000 95000 25000 Favourable

Fixed cost 15000 12000 3000 Adverse

Variable cost 5 5.50 .50 Favourable

following way:

Break-even point Sales = Total Fixed Cost/ PV Ratio

= 13000/42.12%

= £ 30875

Break-even point Units = Break-even point sales/ Price per unit

= 30875/9.50

= 3250 units

Variance Analysis Report

Actual Units Sold = 12000

Budgeted Units Sold = 10000

Budgeted price per unit = 9.50

Sales volume variance = (Actual units sold - Budgeted units sold) * Budgeted

price per unit

= (12000-10000) *9.50

= 2000*9.50

= 19000 Favourable

Flexible budget

Items Actual Budgeted Variance

Sales price 10 9.50 .50 Favourable

Sales units 12000 10000 2000 Favourable

Revenues 120000 95000 25000 Favourable

Fixed cost 15000 12000 3000 Adverse

Variable cost 5 5.50 .50 Favourable

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.