Management Accounting Systems and Decision Making Report

VerifiedAdded on 2020/09/08

|17

|5378

|90

Report

AI Summary

This report delves into the realm of management accounting, focusing on its critical role in organizational decision-making. It explores various management accounting systems, including job costing, target costing, and contract costing, highlighting their benefits and applications within a business context. The report provides a comparative analysis of absorption and marginal costing techniques, illustrating their impact on profit calculations and the reasons for profit discrepancies. Furthermore, it examines planning tools such as budgeting, capital budgeting, and ratio analysis. The report concludes with a discussion on the effectiveness of management accounting in addressing financial challenges faced by Nero Ltd.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

SECTION 1......................................................................................................................................1

1. Importance of management accounting in decision making...................................................1

2. Types of management accounting system used for reporting.................................................2

3. Benefits of management accounting systems and their application in organizational context

.....................................................................................................................................................4

4. (a) Absorption and marginal costing techniques.....................................................................5

4. (b) Supporting calculation regarding difference in the profits from each methods................7

4. (c) Reconciled Profit and Loss statement................................................................................8

SECTION B...................................................................................................................................10

Part A : Planning tools of management accounting..................................................................10

Part B: Management accounting used in dealing with the financial problems ........................11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................1

SECTION 1......................................................................................................................................1

1. Importance of management accounting in decision making...................................................1

2. Types of management accounting system used for reporting.................................................2

3. Benefits of management accounting systems and their application in organizational context

.....................................................................................................................................................4

4. (a) Absorption and marginal costing techniques.....................................................................5

4. (b) Supporting calculation regarding difference in the profits from each methods................7

4. (c) Reconciled Profit and Loss statement................................................................................8

SECTION B...................................................................................................................................10

Part A : Planning tools of management accounting..................................................................10

Part B: Management accounting used in dealing with the financial problems ........................11

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

Index of Tables

Table 1: Statement of Profit and loss using absorption costing in Quarter 1..................................5

Table 2: Statement of Profit and Loss using Marginal Costing Method for Quarter 1...................6

Table 3: Statement of Profit and Loss using Absorption Costing for Quarter 2..............................6

Table 4: Statement of Profit and Loss using Marginal Costing Method for Quarter 2...................7

Table 5: Calculation for under absorption in Quarter 1...................................................................8

Table 6: Calculation for under absorption for Quarter 2.................................................................8

Table 7: Reconciled profit and Loss Statement for Quarter 1.........................................................8

Table 8: Reconciled Profit and Loss statement for Quarter 2..........................................................9

Table 1: Statement of Profit and loss using absorption costing in Quarter 1..................................5

Table 2: Statement of Profit and Loss using Marginal Costing Method for Quarter 1...................6

Table 3: Statement of Profit and Loss using Absorption Costing for Quarter 2..............................6

Table 4: Statement of Profit and Loss using Marginal Costing Method for Quarter 2...................7

Table 5: Calculation for under absorption in Quarter 1...................................................................8

Table 6: Calculation for under absorption for Quarter 2.................................................................8

Table 7: Reconciled profit and Loss Statement for Quarter 1.........................................................8

Table 8: Reconciled Profit and Loss statement for Quarter 2..........................................................9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Management accounting is a practice where financial statements are analysed and

interpreted in order to take better long term and short decision for the company. The report

discusses about the role of management accounting in decision making process of the entity

which further helps in making future forecasts of profits as well. Further, the report focuses on

calculation of profits by using absorption and marginal costing techniques. The reasons for of

difference in the profits from the two methods will also be focussed on. Several types of

management accounting systems will also be discussed in the report. Moreover, three main

planning tools such as budgeting, capital budgeting and ratio analysis are compared and

contrasted based on their benefits. In the end, the report ponders on the effectiveness of

management accounting ion order to deal with the financial problems that arise in Nero Ltd. Will

also be discussed.

SECTION 1

1. Importance of management accounting in decision making

Management accounting is a practice where accounting information is used for better

decision making. It is an important tool to manage the performance of control functions. It is a

process of preparation of management reports which helps in providing financial data to the

managers so that short term and long-term decisions can be taken accurately and within specific

period. It helps in identifying, measuring, analysing, interpreting and communicating information

to the internal and external sources. Analysing and evaluating the reports, managers can make

better quantitative and qualitative decisions for the organization.

There is a vast difference between management accounting and financial accounting. It is

focussed on providing information mostly to the outsiders. However, management accounting

major used for internal decision making (Bodie, 2013).

Major role is played by management accounting for better decision making in the

organization. Some of its roles are discussed below:

Helps in forecasting for future: According to the current and past trends of profits and

sales that has been experienced in the entity, management accounting helps in forecasting

for the upcoming years as well. It evaluates the risk that may come up in the enterprise

and helps in taking corrective action to mitigate the risk beforehand.

1

Management accounting is a practice where financial statements are analysed and

interpreted in order to take better long term and short decision for the company. The report

discusses about the role of management accounting in decision making process of the entity

which further helps in making future forecasts of profits as well. Further, the report focuses on

calculation of profits by using absorption and marginal costing techniques. The reasons for of

difference in the profits from the two methods will also be focussed on. Several types of

management accounting systems will also be discussed in the report. Moreover, three main

planning tools such as budgeting, capital budgeting and ratio analysis are compared and

contrasted based on their benefits. In the end, the report ponders on the effectiveness of

management accounting ion order to deal with the financial problems that arise in Nero Ltd. Will

also be discussed.

SECTION 1

1. Importance of management accounting in decision making

Management accounting is a practice where accounting information is used for better

decision making. It is an important tool to manage the performance of control functions. It is a

process of preparation of management reports which helps in providing financial data to the

managers so that short term and long-term decisions can be taken accurately and within specific

period. It helps in identifying, measuring, analysing, interpreting and communicating information

to the internal and external sources. Analysing and evaluating the reports, managers can make

better quantitative and qualitative decisions for the organization.

There is a vast difference between management accounting and financial accounting. It is

focussed on providing information mostly to the outsiders. However, management accounting

major used for internal decision making (Bodie, 2013).

Major role is played by management accounting for better decision making in the

organization. Some of its roles are discussed below:

Helps in forecasting for future: According to the current and past trends of profits and

sales that has been experienced in the entity, management accounting helps in forecasting

for the upcoming years as well. It evaluates the risk that may come up in the enterprise

and helps in taking corrective action to mitigate the risk beforehand.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Identification of key performance metrics: It assesses the potential of each department

based on the contribution made by them to maximize organizational goals. According to

it, estimation for further year is made.

Collecting and comparing available data: It collects and compare present data and take

future decisions for upcoming financial year based on it. Further, the estimated data is

also compared with the actual ones and find the variations in the expected figures. If the

variance is above 10%, manager have to take serious actions so that the variation can be

reduced to zero (Tran-Thanh, Chapman and et. al, 2012).

Assessing the performance: Accounting manager uses various advanced accounting

techniques in order to assess the performance of the organization. The tools include,

balanced scorecard, key performance indicators, scenario planning, Management

Information System (MIS) etc.

Analysing rate of return: Before making any heavy investment in any project or fixed

asset, manager analyse the profits using various methods such as payback period, Net

Present Value (NPV), Expected Rate of Return (EROR). It analyses different aspects in

order to choose most profitable project from all the available choices (Caglio and Ditillo,

2012).

2. Types of management accounting system used for reporting

Management accounting system helps to collect data related to finance from business

operations for instance, data of sales, inventory shift, change in the cost of raw material cost.

Further, it converts the data into reports so that analysis can be made easily. There are various

types of management accounting system that are made

Job costing system:

Job costing system is a system of management costing in which information about the

cost to be incurred on a specific production or service related task is collected. This information

may be collected to submit to a customer related for reimbursement of cost under a particular

contract. The information is also used of quotation of price for a particular job to generate an

adequate profit. This information may also be used to assign inventories for production. The

information is gathered regarding direct material, direct labour, and overheads associated with

the job. Job costing is different form the contract and target costing the aspects that under this

system of management costing firstly the predictions are made about the cost of the job on the

2

based on the contribution made by them to maximize organizational goals. According to

it, estimation for further year is made.

Collecting and comparing available data: It collects and compare present data and take

future decisions for upcoming financial year based on it. Further, the estimated data is

also compared with the actual ones and find the variations in the expected figures. If the

variance is above 10%, manager have to take serious actions so that the variation can be

reduced to zero (Tran-Thanh, Chapman and et. al, 2012).

Assessing the performance: Accounting manager uses various advanced accounting

techniques in order to assess the performance of the organization. The tools include,

balanced scorecard, key performance indicators, scenario planning, Management

Information System (MIS) etc.

Analysing rate of return: Before making any heavy investment in any project or fixed

asset, manager analyse the profits using various methods such as payback period, Net

Present Value (NPV), Expected Rate of Return (EROR). It analyses different aspects in

order to choose most profitable project from all the available choices (Caglio and Ditillo,

2012).

2. Types of management accounting system used for reporting

Management accounting system helps to collect data related to finance from business

operations for instance, data of sales, inventory shift, change in the cost of raw material cost.

Further, it converts the data into reports so that analysis can be made easily. There are various

types of management accounting system that are made

Job costing system:

Job costing system is a system of management costing in which information about the

cost to be incurred on a specific production or service related task is collected. This information

may be collected to submit to a customer related for reimbursement of cost under a particular

contract. The information is also used of quotation of price for a particular job to generate an

adequate profit. This information may also be used to assign inventories for production. The

information is gathered regarding direct material, direct labour, and overheads associated with

the job. Job costing is different form the contract and target costing the aspects that under this

system of management costing firstly the predictions are made about the cost of the job on the

2

basis of direct material, direct labour and overheads to be incurred and quotations are formed

based on that predictions and later reimbursements are made by the customer for the cost

incurred in process of job.

Target costing system:

Target costing system is a costing technique in which the company makes a plan for the

price points, product cost and margins from the sale that it needs to make from the new product.

If the planned level of cost is not achieved by the company then the entire project is cancelled.

Target costing system is the most efficient system of achieving consistent profitability in the

production sector. The management of the company has the power to continuously track the

manufacturing from the design phase to the production's end part. This system takes certain steps

to make the plan for the product, steps include conducting research, calculation of maximum

cost, engineering the product, ongoing activities in the production. The target costing system

differs from contract and job costing systems on the part that under both the other system no plan

is made against the price point, product cost and margin of the product and also no quotations are

filled for the cost cover for the new product under the other two systems (Christ and Burritt,

2013).

Contract costing:

Under Contract costing system cost is tracked which is associated with a particular

contract of a client. These commitments are made between two parties to complete a task within

a specific period. If the two parties agree to provide fees to the company, then this

reimbursement is done on the cost, in parts, incurred by the company in order to complete the

terms within the contract. The process for expenses of cost includes, fixed cost, cost plus, time

and material. The contract costing may also work on considerable amount of overhead allocation

for the task to complete. This system of management costing is different from job and target

costing on the base that this costing system follows the contract basis instead of job or target

setting, under this system reimbursement is done on the basis of cost incurred by the company in

the process of completion of the terms of the contracts. No pre-planning or prediction of the cost

is done under this contract.

3

based on that predictions and later reimbursements are made by the customer for the cost

incurred in process of job.

Target costing system:

Target costing system is a costing technique in which the company makes a plan for the

price points, product cost and margins from the sale that it needs to make from the new product.

If the planned level of cost is not achieved by the company then the entire project is cancelled.

Target costing system is the most efficient system of achieving consistent profitability in the

production sector. The management of the company has the power to continuously track the

manufacturing from the design phase to the production's end part. This system takes certain steps

to make the plan for the product, steps include conducting research, calculation of maximum

cost, engineering the product, ongoing activities in the production. The target costing system

differs from contract and job costing systems on the part that under both the other system no plan

is made against the price point, product cost and margin of the product and also no quotations are

filled for the cost cover for the new product under the other two systems (Christ and Burritt,

2013).

Contract costing:

Under Contract costing system cost is tracked which is associated with a particular

contract of a client. These commitments are made between two parties to complete a task within

a specific period. If the two parties agree to provide fees to the company, then this

reimbursement is done on the cost, in parts, incurred by the company in order to complete the

terms within the contract. The process for expenses of cost includes, fixed cost, cost plus, time

and material. The contract costing may also work on considerable amount of overhead allocation

for the task to complete. This system of management costing is different from job and target

costing on the base that this costing system follows the contract basis instead of job or target

setting, under this system reimbursement is done on the basis of cost incurred by the company in

the process of completion of the terms of the contracts. No pre-planning or prediction of the cost

is done under this contract.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3. Benefits of management accounting systems and their application in organizational context

The main management accounting system that have been discussed are, Job costing,

target costing and contract costing.

Job Costing: The major advantage of job costing is that the managers are able to calculate

profits that have been incurred from each job. It further helps in ascertaining the desired results

that is expected out of the job in near future. It is the best activity that can be adopted by a

manufacturing concern. Also, companies providing customized thing can also find out the cost

involved in it by using this method. It is the best suited technique for those who have continuous

manufacturing setting such as factories, manufacturing concern and utilities companies (Figge

and Hahn, 2013).

Job costing is an effective method that helps in assessing the performance of individuals

and well as the team in terms of cost control, efficiency of the team members and productivity as

well. It is an adequate method to determine the average cost of each unit that has been produced.

The cost can be assessed at every stage of completion of the job which helps in controlling the

cost at every step of manufacturing. Moreover, corrective actions can be taken by the entity in

order to control the cost and maximize profits.

Target Costing: The focus of this type of costing is to identify the cost of the product so that it

can generate desired profit margin. It helps in reducing the cost of production so that the set

target of profits can be achieved. Further, it plays a key role in acquiring the products which are

best suited do that cost can be reduced to the minimum. It creates a financial flexibility in the

organization. Moreover, reduced cost attracts the maximum number of customers towards the

organization. It elevates the customer base of the enterprise. It is a formal and systematic way to

focus on optimization of cost. Since, formal set up of cost optimization is more appropriate for

small organizations. It is medium sized organization and targeting costing method is the best

approach to achieve organizational goals.

Another emphases of target costing is on reducing the time involved in product cycle. It

means that unnecessary steps from manufacturing cycle have been eliminated which ultimately

saves the time involved in production as well. It adds value to the end consumer as they get the

products offered by the entity at reduced prices than before. A shorter time cycle helps the

manufacturer to be a first mover in the market and maximize profits. It also helps in attracting

maximum customers in the first go before any other competitors come to the market.

4

The main management accounting system that have been discussed are, Job costing,

target costing and contract costing.

Job Costing: The major advantage of job costing is that the managers are able to calculate

profits that have been incurred from each job. It further helps in ascertaining the desired results

that is expected out of the job in near future. It is the best activity that can be adopted by a

manufacturing concern. Also, companies providing customized thing can also find out the cost

involved in it by using this method. It is the best suited technique for those who have continuous

manufacturing setting such as factories, manufacturing concern and utilities companies (Figge

and Hahn, 2013).

Job costing is an effective method that helps in assessing the performance of individuals

and well as the team in terms of cost control, efficiency of the team members and productivity as

well. It is an adequate method to determine the average cost of each unit that has been produced.

The cost can be assessed at every stage of completion of the job which helps in controlling the

cost at every step of manufacturing. Moreover, corrective actions can be taken by the entity in

order to control the cost and maximize profits.

Target Costing: The focus of this type of costing is to identify the cost of the product so that it

can generate desired profit margin. It helps in reducing the cost of production so that the set

target of profits can be achieved. Further, it plays a key role in acquiring the products which are

best suited do that cost can be reduced to the minimum. It creates a financial flexibility in the

organization. Moreover, reduced cost attracts the maximum number of customers towards the

organization. It elevates the customer base of the enterprise. It is a formal and systematic way to

focus on optimization of cost. Since, formal set up of cost optimization is more appropriate for

small organizations. It is medium sized organization and targeting costing method is the best

approach to achieve organizational goals.

Another emphases of target costing is on reducing the time involved in product cycle. It

means that unnecessary steps from manufacturing cycle have been eliminated which ultimately

saves the time involved in production as well. It adds value to the end consumer as they get the

products offered by the entity at reduced prices than before. A shorter time cycle helps the

manufacturer to be a first mover in the market and maximize profits. It also helps in attracting

maximum customers in the first go before any other competitors come to the market.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contracting costing: It is mostly conducted by builders, civil contractors, ship builders and

mechanical engineer firms. The manufacturing is basically conducted based on the demands of

the customers and can be customized according to their taste and preferences. It helps in

ascertaining the cost that have been incurred of each contract separately. It helps in analysing the

profits that have been generated from each contract and assess the cost incurred in it. The larger

jobs continues for more than a year. Contracting cost make it easy to analyse the cost year by

year. Since, each contract is different and unique, one can be distinguished with the other with

the help of it based on the cost incurred and profits generated (Hall and West, 2013).

The contractor can assess the cost incurred upto a particular period and can make

estimated about the profits as well. It can further distribute the expenses so that optimum

utilization of the available resources is made. It can analyse the profits it generated from different

contract and estimate the prices of further contracts based on it.

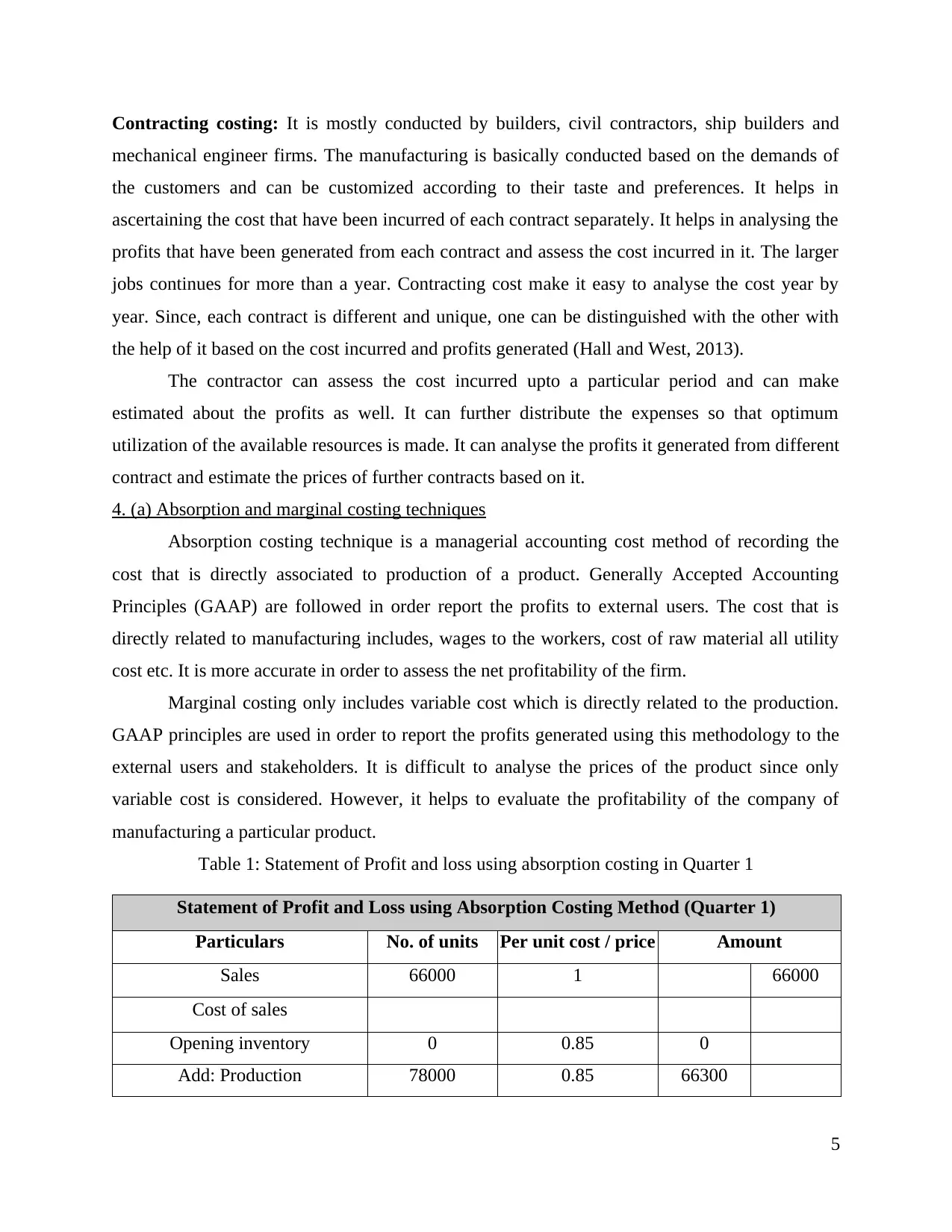

4. (a) Absorption and marginal costing techniques

Absorption costing technique is a managerial accounting cost method of recording the

cost that is directly associated to production of a product. Generally Accepted Accounting

Principles (GAAP) are followed in order report the profits to external users. The cost that is

directly related to manufacturing includes, wages to the workers, cost of raw material all utility

cost etc. It is more accurate in order to assess the net profitability of the firm.

Marginal costing only includes variable cost which is directly related to the production.

GAAP principles are used in order to report the profits generated using this methodology to the

external users and stakeholders. It is difficult to analyse the prices of the product since only

variable cost is considered. However, it helps to evaluate the profitability of the company of

manufacturing a particular product.

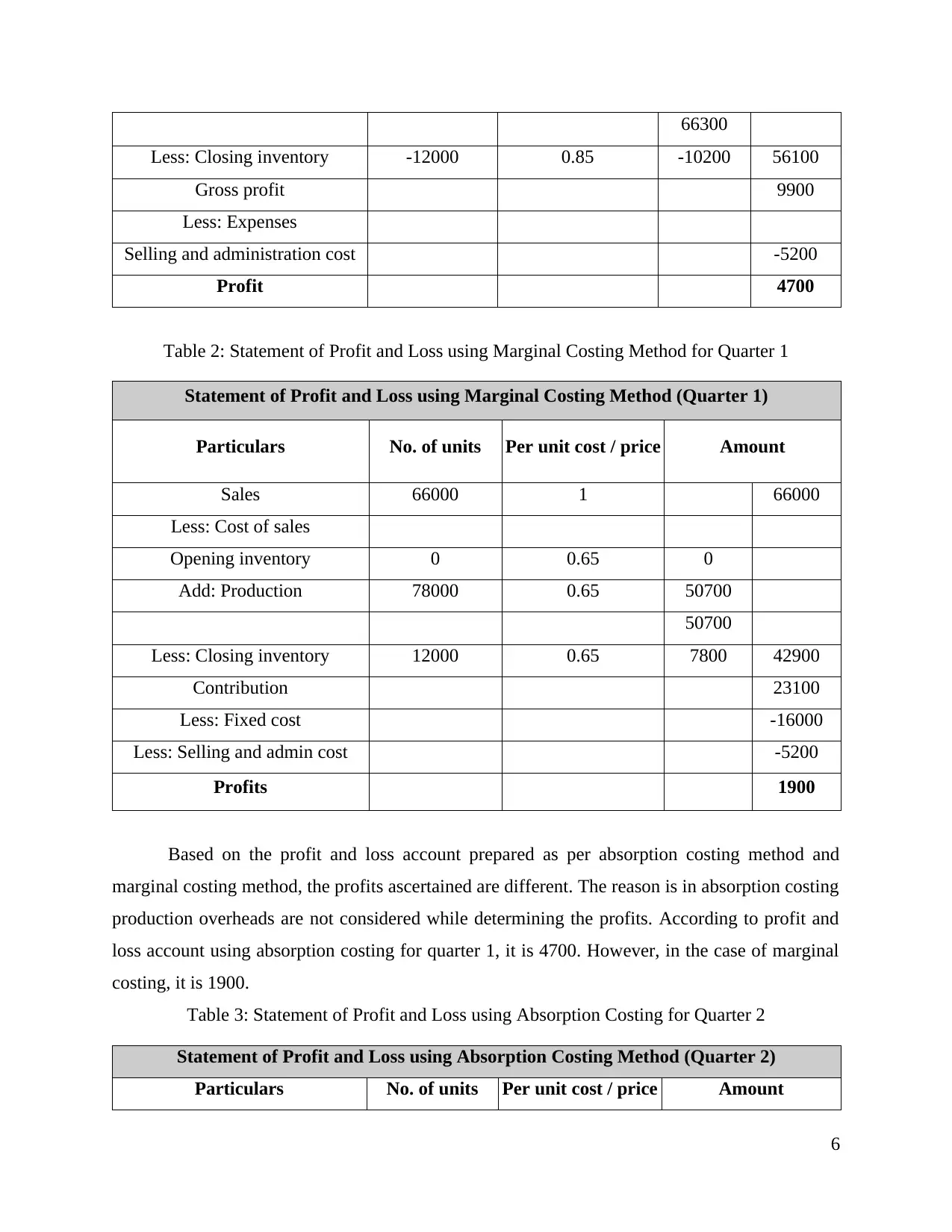

Table 1: Statement of Profit and loss using absorption costing in Quarter 1

Statement of Profit and Loss using Absorption Costing Method (Quarter 1)

Particulars No. of units Per unit cost / price Amount

Sales 66000 1 66000

Cost of sales

Opening inventory 0 0.85 0

Add: Production 78000 0.85 66300

5

mechanical engineer firms. The manufacturing is basically conducted based on the demands of

the customers and can be customized according to their taste and preferences. It helps in

ascertaining the cost that have been incurred of each contract separately. It helps in analysing the

profits that have been generated from each contract and assess the cost incurred in it. The larger

jobs continues for more than a year. Contracting cost make it easy to analyse the cost year by

year. Since, each contract is different and unique, one can be distinguished with the other with

the help of it based on the cost incurred and profits generated (Hall and West, 2013).

The contractor can assess the cost incurred upto a particular period and can make

estimated about the profits as well. It can further distribute the expenses so that optimum

utilization of the available resources is made. It can analyse the profits it generated from different

contract and estimate the prices of further contracts based on it.

4. (a) Absorption and marginal costing techniques

Absorption costing technique is a managerial accounting cost method of recording the

cost that is directly associated to production of a product. Generally Accepted Accounting

Principles (GAAP) are followed in order report the profits to external users. The cost that is

directly related to manufacturing includes, wages to the workers, cost of raw material all utility

cost etc. It is more accurate in order to assess the net profitability of the firm.

Marginal costing only includes variable cost which is directly related to the production.

GAAP principles are used in order to report the profits generated using this methodology to the

external users and stakeholders. It is difficult to analyse the prices of the product since only

variable cost is considered. However, it helps to evaluate the profitability of the company of

manufacturing a particular product.

Table 1: Statement of Profit and loss using absorption costing in Quarter 1

Statement of Profit and Loss using Absorption Costing Method (Quarter 1)

Particulars No. of units Per unit cost / price Amount

Sales 66000 1 66000

Cost of sales

Opening inventory 0 0.85 0

Add: Production 78000 0.85 66300

5

66300

Less: Closing inventory -12000 0.85 -10200 56100

Gross profit 9900

Less: Expenses

Selling and administration cost -5200

Profit 4700

Table 2: Statement of Profit and Loss using Marginal Costing Method for Quarter 1

Statement of Profit and Loss using Marginal Costing Method (Quarter 1)

Particulars No. of units Per unit cost / price Amount

Sales 66000 1 66000

Less: Cost of sales

Opening inventory 0 0.65 0

Add: Production 78000 0.65 50700

50700

Less: Closing inventory 12000 0.65 7800 42900

Contribution 23100

Less: Fixed cost -16000

Less: Selling and admin cost -5200

Profits 1900

Based on the profit and loss account prepared as per absorption costing method and

marginal costing method, the profits ascertained are different. The reason is in absorption costing

production overheads are not considered while determining the profits. According to profit and

loss account using absorption costing for quarter 1, it is 4700. However, in the case of marginal

costing, it is 1900.

Table 3: Statement of Profit and Loss using Absorption Costing for Quarter 2

Statement of Profit and Loss using Absorption Costing Method (Quarter 2)

Particulars No. of units Per unit cost / price Amount

6

Less: Closing inventory -12000 0.85 -10200 56100

Gross profit 9900

Less: Expenses

Selling and administration cost -5200

Profit 4700

Table 2: Statement of Profit and Loss using Marginal Costing Method for Quarter 1

Statement of Profit and Loss using Marginal Costing Method (Quarter 1)

Particulars No. of units Per unit cost / price Amount

Sales 66000 1 66000

Less: Cost of sales

Opening inventory 0 0.65 0

Add: Production 78000 0.65 50700

50700

Less: Closing inventory 12000 0.65 7800 42900

Contribution 23100

Less: Fixed cost -16000

Less: Selling and admin cost -5200

Profits 1900

Based on the profit and loss account prepared as per absorption costing method and

marginal costing method, the profits ascertained are different. The reason is in absorption costing

production overheads are not considered while determining the profits. According to profit and

loss account using absorption costing for quarter 1, it is 4700. However, in the case of marginal

costing, it is 1900.

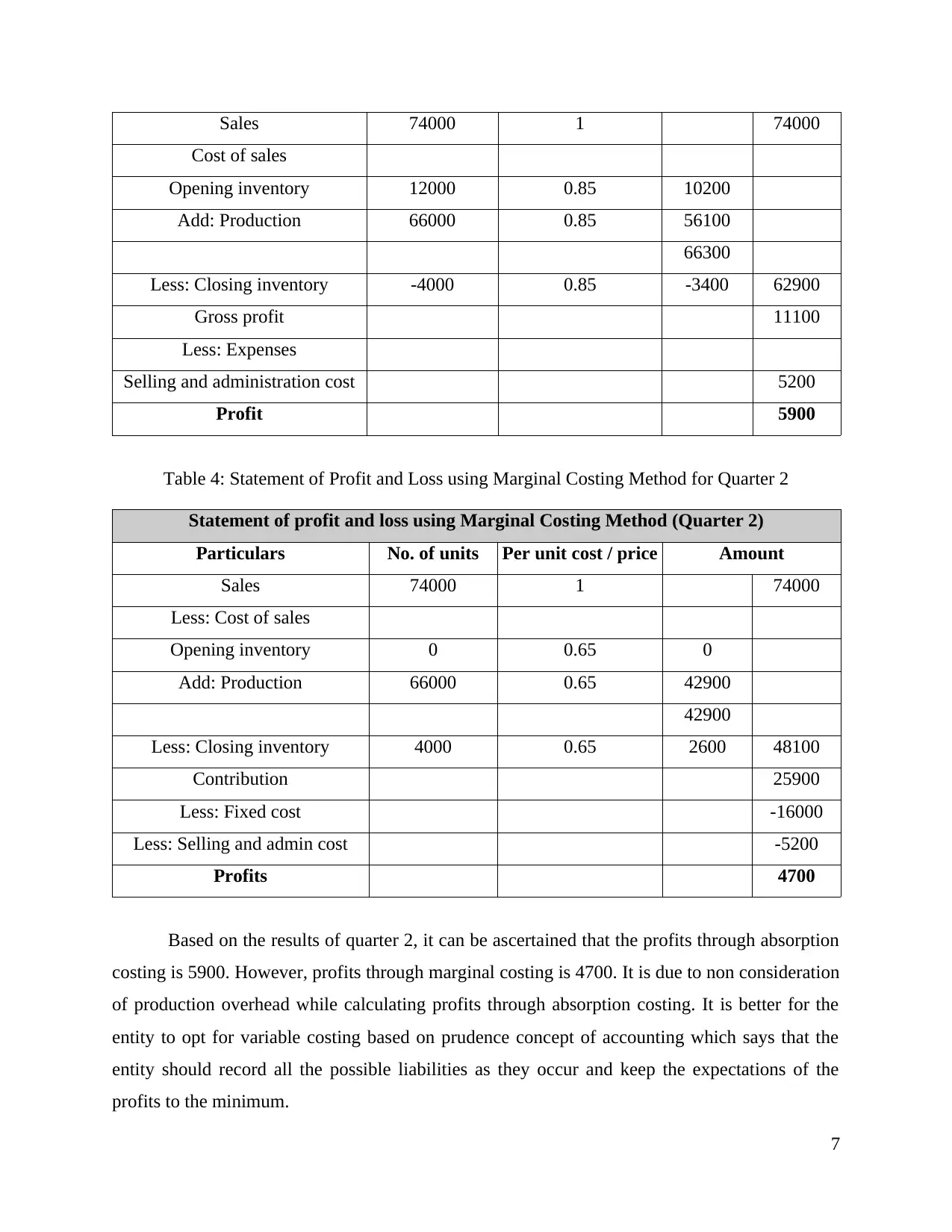

Table 3: Statement of Profit and Loss using Absorption Costing for Quarter 2

Statement of Profit and Loss using Absorption Costing Method (Quarter 2)

Particulars No. of units Per unit cost / price Amount

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Sales 74000 1 74000

Cost of sales

Opening inventory 12000 0.85 10200

Add: Production 66000 0.85 56100

66300

Less: Closing inventory -4000 0.85 -3400 62900

Gross profit 11100

Less: Expenses

Selling and administration cost 5200

Profit 5900

Table 4: Statement of Profit and Loss using Marginal Costing Method for Quarter 2

Statement of profit and loss using Marginal Costing Method (Quarter 2)

Particulars No. of units Per unit cost / price Amount

Sales 74000 1 74000

Less: Cost of sales

Opening inventory 0 0.65 0

Add: Production 66000 0.65 42900

42900

Less: Closing inventory 4000 0.65 2600 48100

Contribution 25900

Less: Fixed cost -16000

Less: Selling and admin cost -5200

Profits 4700

Based on the results of quarter 2, it can be ascertained that the profits through absorption

costing is 5900. However, profits through marginal costing is 4700. It is due to non consideration

of production overhead while calculating profits through absorption costing. It is better for the

entity to opt for variable costing based on prudence concept of accounting which says that the

entity should record all the possible liabilities as they occur and keep the expectations of the

profits to the minimum.

7

Cost of sales

Opening inventory 12000 0.85 10200

Add: Production 66000 0.85 56100

66300

Less: Closing inventory -4000 0.85 -3400 62900

Gross profit 11100

Less: Expenses

Selling and administration cost 5200

Profit 5900

Table 4: Statement of Profit and Loss using Marginal Costing Method for Quarter 2

Statement of profit and loss using Marginal Costing Method (Quarter 2)

Particulars No. of units Per unit cost / price Amount

Sales 74000 1 74000

Less: Cost of sales

Opening inventory 0 0.65 0

Add: Production 66000 0.65 42900

42900

Less: Closing inventory 4000 0.65 2600 48100

Contribution 25900

Less: Fixed cost -16000

Less: Selling and admin cost -5200

Profits 4700

Based on the results of quarter 2, it can be ascertained that the profits through absorption

costing is 5900. However, profits through marginal costing is 4700. It is due to non consideration

of production overhead while calculating profits through absorption costing. It is better for the

entity to opt for variable costing based on prudence concept of accounting which says that the

entity should record all the possible liabilities as they occur and keep the expectations of the

profits to the minimum.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

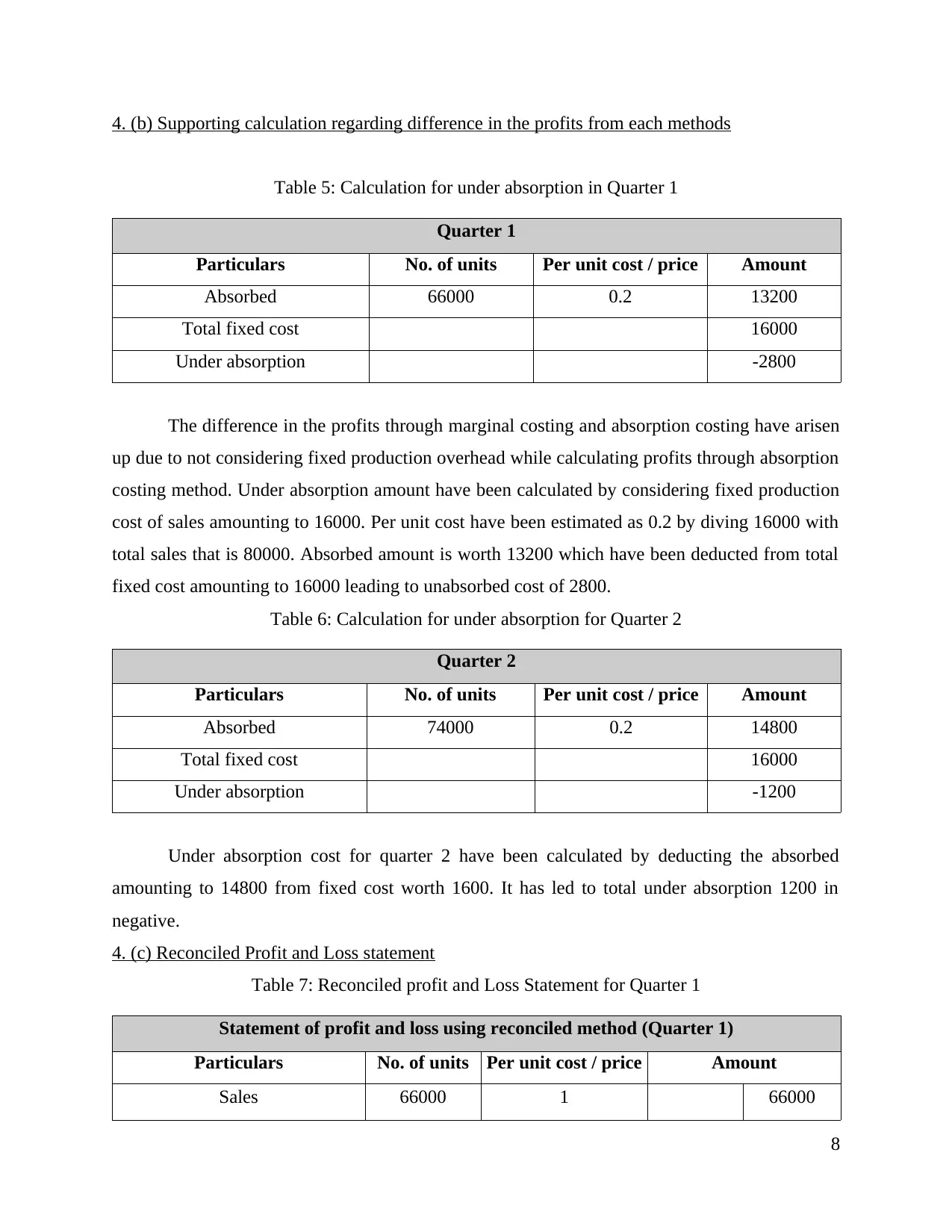

4. (b) Supporting calculation regarding difference in the profits from each methods

Table 5: Calculation for under absorption in Quarter 1

Quarter 1

Particulars No. of units Per unit cost / price Amount

Absorbed 66000 0.2 13200

Total fixed cost 16000

Under absorption -2800

The difference in the profits through marginal costing and absorption costing have arisen

up due to not considering fixed production overhead while calculating profits through absorption

costing method. Under absorption amount have been calculated by considering fixed production

cost of sales amounting to 16000. Per unit cost have been estimated as 0.2 by diving 16000 with

total sales that is 80000. Absorbed amount is worth 13200 which have been deducted from total

fixed cost amounting to 16000 leading to unabsorbed cost of 2800.

Table 6: Calculation for under absorption for Quarter 2

Quarter 2

Particulars No. of units Per unit cost / price Amount

Absorbed 74000 0.2 14800

Total fixed cost 16000

Under absorption -1200

Under absorption cost for quarter 2 have been calculated by deducting the absorbed

amounting to 14800 from fixed cost worth 1600. It has led to total under absorption 1200 in

negative.

4. (c) Reconciled Profit and Loss statement

Table 7: Reconciled profit and Loss Statement for Quarter 1

Statement of profit and loss using reconciled method (Quarter 1)

Particulars No. of units Per unit cost / price Amount

Sales 66000 1 66000

8

Table 5: Calculation for under absorption in Quarter 1

Quarter 1

Particulars No. of units Per unit cost / price Amount

Absorbed 66000 0.2 13200

Total fixed cost 16000

Under absorption -2800

The difference in the profits through marginal costing and absorption costing have arisen

up due to not considering fixed production overhead while calculating profits through absorption

costing method. Under absorption amount have been calculated by considering fixed production

cost of sales amounting to 16000. Per unit cost have been estimated as 0.2 by diving 16000 with

total sales that is 80000. Absorbed amount is worth 13200 which have been deducted from total

fixed cost amounting to 16000 leading to unabsorbed cost of 2800.

Table 6: Calculation for under absorption for Quarter 2

Quarter 2

Particulars No. of units Per unit cost / price Amount

Absorbed 74000 0.2 14800

Total fixed cost 16000

Under absorption -1200

Under absorption cost for quarter 2 have been calculated by deducting the absorbed

amounting to 14800 from fixed cost worth 1600. It has led to total under absorption 1200 in

negative.

4. (c) Reconciled Profit and Loss statement

Table 7: Reconciled profit and Loss Statement for Quarter 1

Statement of profit and loss using reconciled method (Quarter 1)

Particulars No. of units Per unit cost / price Amount

Sales 66000 1 66000

8

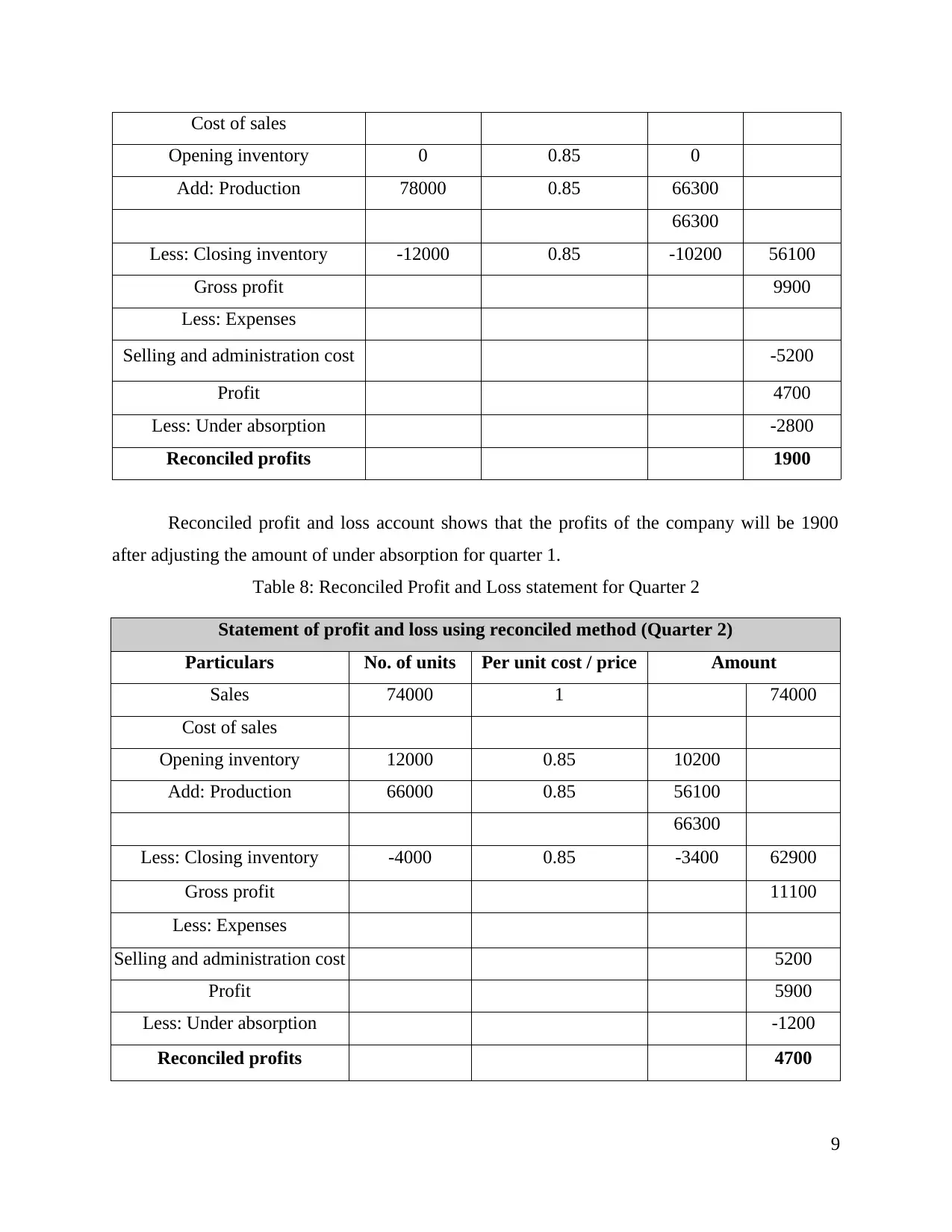

Cost of sales

Opening inventory 0 0.85 0

Add: Production 78000 0.85 66300

66300

Less: Closing inventory -12000 0.85 -10200 56100

Gross profit 9900

Less: Expenses

Selling and administration cost -5200

Profit 4700

Less: Under absorption -2800

Reconciled profits 1900

Reconciled profit and loss account shows that the profits of the company will be 1900

after adjusting the amount of under absorption for quarter 1.

Table 8: Reconciled Profit and Loss statement for Quarter 2

Statement of profit and loss using reconciled method (Quarter 2)

Particulars No. of units Per unit cost / price Amount

Sales 74000 1 74000

Cost of sales

Opening inventory 12000 0.85 10200

Add: Production 66000 0.85 56100

66300

Less: Closing inventory -4000 0.85 -3400 62900

Gross profit 11100

Less: Expenses

Selling and administration cost 5200

Profit 5900

Less: Under absorption -1200

Reconciled profits 4700

9

Opening inventory 0 0.85 0

Add: Production 78000 0.85 66300

66300

Less: Closing inventory -12000 0.85 -10200 56100

Gross profit 9900

Less: Expenses

Selling and administration cost -5200

Profit 4700

Less: Under absorption -2800

Reconciled profits 1900

Reconciled profit and loss account shows that the profits of the company will be 1900

after adjusting the amount of under absorption for quarter 1.

Table 8: Reconciled Profit and Loss statement for Quarter 2

Statement of profit and loss using reconciled method (Quarter 2)

Particulars No. of units Per unit cost / price Amount

Sales 74000 1 74000

Cost of sales

Opening inventory 12000 0.85 10200

Add: Production 66000 0.85 56100

66300

Less: Closing inventory -4000 0.85 -3400 62900

Gross profit 11100

Less: Expenses

Selling and administration cost 5200

Profit 5900

Less: Under absorption -1200

Reconciled profits 4700

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.