Management Ethics and Governance: A Case Study Report

VerifiedAdded on 2023/02/01

|16

|4112

|20

Report

AI Summary

This report delves into the critical role of ethics in corporate governance, emphasizing its value in the workplace. It examines the Aristotelian concept of virtue ethics and the application of utilitarianism in analyzing ethical dilemmas, particularly in the context of financial services. The report uses a case study involving Freedom, its customers, and the implications of their actions. It analyzes issues such as the asymmetry of power and information, conflicts of interest, and the importance of accountability. The discussion covers ethical issues in corporate governance, theoretical considerations, and the practical application of utility theory. The report also assesses the implications of corporate actions, such as the sale of insurance policies and the handling of customer complaints, in the context of ethical standards and legal requirements. The report concludes by highlighting the importance of transparency, ethical behavior, and adherence to regulatory frameworks for maintaining customer trust and ensuring responsible corporate governance.

Running head: MANAGEMENT

Ethics and Governance

Name of the student:

Name of the university:

Author note:

Ethics and Governance

Name of the student:

Name of the university:

Author note:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1

MANAGEMENT

Executive summary

Considering the good of others is the main motto of ethics. This is applicable in all of the

workplace conditions. The cases of arrogance and pride in terms of exertion of power and

authority is prevalent from the ancient times. With the advancement in civilisation and

technologies, there has been simultaneous development in the ideas and values. Aristotelian

concept is the most appropriate in terms of understanding the applicability of the virtue ethics

in the workplace issues. In this, the main focus is on measuring the impact of the decisions on

the clients. Utilitarianism or utility theory is applied for analysing the issues in treating the

customers of Freedom. Consciousness towards indulging in the misdeeds is an attempt

towards restoring loyalty, trust and dependence from clients like Mr Stewart, his son and Mr

Orton.

MANAGEMENT

Executive summary

Considering the good of others is the main motto of ethics. This is applicable in all of the

workplace conditions. The cases of arrogance and pride in terms of exertion of power and

authority is prevalent from the ancient times. With the advancement in civilisation and

technologies, there has been simultaneous development in the ideas and values. Aristotelian

concept is the most appropriate in terms of understanding the applicability of the virtue ethics

in the workplace issues. In this, the main focus is on measuring the impact of the decisions on

the clients. Utilitarianism or utility theory is applied for analysing the issues in treating the

customers of Freedom. Consciousness towards indulging in the misdeeds is an attempt

towards restoring loyalty, trust and dependence from clients like Mr Stewart, his son and Mr

Orton.

2

MANAGEMENT

Table of contents

Introduction................................................................................................................................3

Discussion..................................................................................................................................3

Volume 1................................................................................................................................3

1.1 Four observations.............................................................................................................3

Ethical issues in corporate governance..................................................................................4

Theoretical considerations.....................................................................................................5

Utility theory..........................................................................................................................5

Application of the theory into the case scenario....................................................................5

Conclusion................................................................................................................................11

References................................................................................................................................11

MANAGEMENT

Table of contents

Introduction................................................................................................................................3

Discussion..................................................................................................................................3

Volume 1................................................................................................................................3

1.1 Four observations.............................................................................................................3

Ethical issues in corporate governance..................................................................................4

Theoretical considerations.....................................................................................................5

Utility theory..........................................................................................................................5

Application of the theory into the case scenario....................................................................5

Conclusion................................................................................................................................11

References................................................................................................................................11

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3

MANAGEMENT

Introduction

Ethics is vital, which adds value to the corporate governance in the workplace. Within

this, mention can be made of the Accounting Professional and Ethical Standard Board,

Limited, which standardizes the business operations. Access and permission to use this code

is granted in terms of the transactional services in the parameters of Public Interest Entities,

Partner Rotation, Non-assurance services and Fees among others (Ferrell, Fraedrich and

Ferrell, 2015). All the employees in the workplace ought to comply with the standards and

codes of APES 110 issued by Accounting Professional and Ethical Standard Board. This is

also applicable in case of the personnel hailing from outside Australia and practising in

Australia. Corporation Act (2001) is incorporated in the business operations, which acts

assistance in legalizing the instruments needed for standardizing the audits and reviews

(APESB, 2010). This assignment attempts to shed light on the corporate governance through

the theoretical consideration, that is, utility theories.

Discussion

Volume 1

1.1 Four observations

According to the observation of the Commission’s work, the four observations are

connection between conduct and reward, asymmetry of power and information between

financial services entities and their customers, effects of conflicts between duty and interest

and holding entities to account. Final and the Interim Report are vital doctrines in this case.

This is in terms of gaining an insight into the performance of the person towards adhering to

the terms and conditions of the legislations. Monitoring the performance results in awarding

the rewards according to the performance levels. As per the arguments of McAlister and

Ferrell, 2016), misconducts in case of rewards is against the ethics. Yet in cases of incentives,

bonus and commission schemes, the industries use measurement scale for maintaining the

balance between the sales and profit.

MANAGEMENT

Introduction

Ethics is vital, which adds value to the corporate governance in the workplace. Within

this, mention can be made of the Accounting Professional and Ethical Standard Board,

Limited, which standardizes the business operations. Access and permission to use this code

is granted in terms of the transactional services in the parameters of Public Interest Entities,

Partner Rotation, Non-assurance services and Fees among others (Ferrell, Fraedrich and

Ferrell, 2015). All the employees in the workplace ought to comply with the standards and

codes of APES 110 issued by Accounting Professional and Ethical Standard Board. This is

also applicable in case of the personnel hailing from outside Australia and practising in

Australia. Corporation Act (2001) is incorporated in the business operations, which acts

assistance in legalizing the instruments needed for standardizing the audits and reviews

(APESB, 2010). This assignment attempts to shed light on the corporate governance through

the theoretical consideration, that is, utility theories.

Discussion

Volume 1

1.1 Four observations

According to the observation of the Commission’s work, the four observations are

connection between conduct and reward, asymmetry of power and information between

financial services entities and their customers, effects of conflicts between duty and interest

and holding entities to account. Final and the Interim Report are vital doctrines in this case.

This is in terms of gaining an insight into the performance of the person towards adhering to

the terms and conditions of the legislations. Monitoring the performance results in awarding

the rewards according to the performance levels. As per the arguments of McAlister and

Ferrell, 2016), misconducts in case of rewards is against the ethics. Yet in cases of incentives,

bonus and commission schemes, the industries use measurement scale for maintaining the

balance between the sales and profit.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4

MANAGEMENT

In terms of the entities and individuals, capability is the main aspect. Entities are set

in terms of the terms and conditions of the deals, trades and transactions. Detailed knowledge

of the understanding of transactions and consumers is next to impossible in terms of the

power to negotiate the terms. Intermediaries enhance the process of dealing with the financial

services. Here, the expectations relate to catering towards the interest of the clients’ interest.

Dempsey, (2017) opines that financial services, violating the laws are not properly held to

account.

Synthesis of these ideas results in formation of the fact that interest of the client,

intermediary and the provider of the products and services differ and are opposed.

Ethical issues in corporate governance

Ethical problems aggravates the complexities for the managers in terms of mapping

the outcomes in terms of corporate social responsibility. The parameters covered in this

direction are protecting the employees, preserving the ecological biodiversity among others.

In this case, value judgment is used for undertaking relevant decisions (Müller et al., 2016).

Some of the issues, which leads to dilemmas in exercising the corporate governance are as

follows:

Existence of ethical rights and duties between business and society- companies

dealing in the services, which are not socially acceptable, gives rise to ethical

dilemmas. Typical examples in this direction are the companies dealing with the

production of cigarettes, drugs among others.

Moral rights between company and the stakeholders- In order to maintain the stability

in the relationship with the customers, the companies need to avert indulging in

unethical activities like manipulation of the accounts’ book for projecting higher

profits (Nwanji et al., 2019). Along with this, mention can be made of the instances of

reducing the workforce for projecting higher earnings. This can be related with the

MANAGEMENT

In terms of the entities and individuals, capability is the main aspect. Entities are set

in terms of the terms and conditions of the deals, trades and transactions. Detailed knowledge

of the understanding of transactions and consumers is next to impossible in terms of the

power to negotiate the terms. Intermediaries enhance the process of dealing with the financial

services. Here, the expectations relate to catering towards the interest of the clients’ interest.

Dempsey, (2017) opines that financial services, violating the laws are not properly held to

account.

Synthesis of these ideas results in formation of the fact that interest of the client,

intermediary and the provider of the products and services differ and are opposed.

Ethical issues in corporate governance

Ethical problems aggravates the complexities for the managers in terms of mapping

the outcomes in terms of corporate social responsibility. The parameters covered in this

direction are protecting the employees, preserving the ecological biodiversity among others.

In this case, value judgment is used for undertaking relevant decisions (Müller et al., 2016).

Some of the issues, which leads to dilemmas in exercising the corporate governance are as

follows:

Existence of ethical rights and duties between business and society- companies

dealing in the services, which are not socially acceptable, gives rise to ethical

dilemmas. Typical examples in this direction are the companies dealing with the

production of cigarettes, drugs among others.

Moral rights between company and the stakeholders- In order to maintain the stability

in the relationship with the customers, the companies need to avert indulging in

unethical activities like manipulation of the accounts’ book for projecting higher

profits (Nwanji et al., 2019). Along with this, mention can be made of the instances of

reducing the workforce for projecting higher earnings. This can be related with the

5

MANAGEMENT

component of Letters Patent, one of the critical element in the Final Report of the

Commission.

Ethical issues relating to the relationship between companies- In this, the cases of

hostile takeover and industry espionage can be related. Typical example of this is the

acquisition. Hostile takeover destroys the stability in the relationship between the

companies. Takeovers resulting in higher profits are beneficial, indicating the

expansion in the scope and arena of the businesses. This can be related with the

element of Public Engagement, which is accounted as an important element of the

Royal Public Commission final Report.

Political contribution- Political assistance in terms of strategic alliances is assistance

in the development of the policies of expansion. According to the arguments of

Davies, (2016), taking financial assistance from the political parties is unethical, as it

generates biasness, contradicting the aspect of public welfare.

Bribery- it is a form of corruption, which affects the efficiency in the business

operations.

Theoretical considerations

Utility theory

Utilitarianism aggravates the complexities towards capitalization, attaching ethical

connotations to the expenses behind the achievement of targets and increasing the profit

margin. According to Du Plessis, Hargovan and Harris, (2018), utilitarianism is a rational

approach towards maintaining the workplace ethics. Most of the industries adopt

utilitarianism in terms of executing the accounting practices. The main factor in this case is

undertaking the decisions after evaluating its benefits on the stakeholders and shareholders.

Application of the theory into the case scenario

Distribution of the life insurance to the consumers over telephone reflects the

conscious approach of Freedom towards their wellbeing. Evidence based practice reflects the

MANAGEMENT

component of Letters Patent, one of the critical element in the Final Report of the

Commission.

Ethical issues relating to the relationship between companies- In this, the cases of

hostile takeover and industry espionage can be related. Typical example of this is the

acquisition. Hostile takeover destroys the stability in the relationship between the

companies. Takeovers resulting in higher profits are beneficial, indicating the

expansion in the scope and arena of the businesses. This can be related with the

element of Public Engagement, which is accounted as an important element of the

Royal Public Commission final Report.

Political contribution- Political assistance in terms of strategic alliances is assistance

in the development of the policies of expansion. According to the arguments of

Davies, (2016), taking financial assistance from the political parties is unethical, as it

generates biasness, contradicting the aspect of public welfare.

Bribery- it is a form of corruption, which affects the efficiency in the business

operations.

Theoretical considerations

Utility theory

Utilitarianism aggravates the complexities towards capitalization, attaching ethical

connotations to the expenses behind the achievement of targets and increasing the profit

margin. According to Du Plessis, Hargovan and Harris, (2018), utilitarianism is a rational

approach towards maintaining the workplace ethics. Most of the industries adopt

utilitarianism in terms of executing the accounting practices. The main factor in this case is

undertaking the decisions after evaluating its benefits on the stakeholders and shareholders.

Application of the theory into the case scenario

Distribution of the life insurance to the consumers over telephone reflects the

conscious approach of Freedom towards their wellbeing. Evidence based practice reflects the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6

MANAGEMENT

transparency in the corporate governance activities. Proper and accurate evidence from Mr

Bruce Stewart legalizes the process of selling the insurance policies. Along with this, Zaharia,

and Zaharia, (2015) states that notification of the substantial changes to the Commission

nullifies the chance of illegal activities and decisions. The written form of notification is

fruitful in terms of aligning the decision-making process with the element of submissions, a

critical component of the Final report of the Commission. The decision to cease selling of the

insurance products except the funeral insurance and loan protection cover through the sales

outbound call was apt and according to the standards and protocols of the legislative

requirements. These aspects relates to the presence of utilitarianism in the business practices

especially in the parameter of accounts.

Absence of documents regarding recording of the decision aggravates the

complexities in producing the claims and the verdict. Here, in comparison to disbelief,

documentation by a public company gets more highlighted. According to the public

availability of the documents, Commission undertook the evidence after direct suspension of

the sales of life insurance through outbound sales calls. Aligning with the arguments of

Schaltegger and Burritt, (2018), reference can be cited of the period of 2016, when Insurance

Policy was sold to Mr Stewart’s son. This was an additional assistance for him as his only

source of income was the Disability Support Pension. This approach aligns with the codes

and conventions of workplace ethics in case of the employees suffering from disabilities. In

this case, the element of Witnesses, mentioned in the Final Report of the Commission, is vital

in terms of measuring the reliability and validity of the clauses and conditions brought in by

the victim.

Mr Stewart learnt that his son had taken out insurance after the son received a letter

from the company. The Protection Plan involved coverage for accident, injury and funeral.

Disseminating the information related to the duration of the premiums is an attempt towards

MANAGEMENT

transparency in the corporate governance activities. Proper and accurate evidence from Mr

Bruce Stewart legalizes the process of selling the insurance policies. Along with this, Zaharia,

and Zaharia, (2015) states that notification of the substantial changes to the Commission

nullifies the chance of illegal activities and decisions. The written form of notification is

fruitful in terms of aligning the decision-making process with the element of submissions, a

critical component of the Final report of the Commission. The decision to cease selling of the

insurance products except the funeral insurance and loan protection cover through the sales

outbound call was apt and according to the standards and protocols of the legislative

requirements. These aspects relates to the presence of utilitarianism in the business practices

especially in the parameter of accounts.

Absence of documents regarding recording of the decision aggravates the

complexities in producing the claims and the verdict. Here, in comparison to disbelief,

documentation by a public company gets more highlighted. According to the public

availability of the documents, Commission undertook the evidence after direct suspension of

the sales of life insurance through outbound sales calls. Aligning with the arguments of

Schaltegger and Burritt, (2018), reference can be cited of the period of 2016, when Insurance

Policy was sold to Mr Stewart’s son. This was an additional assistance for him as his only

source of income was the Disability Support Pension. This approach aligns with the codes

and conventions of workplace ethics in case of the employees suffering from disabilities. In

this case, the element of Witnesses, mentioned in the Final Report of the Commission, is vital

in terms of measuring the reliability and validity of the clauses and conditions brought in by

the victim.

Mr Stewart learnt that his son had taken out insurance after the son received a letter

from the company. The Protection Plan involved coverage for accident, injury and funeral.

Disseminating the information related to the duration of the premiums is an attempt towards

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7

MANAGEMENT

ensuring the wellbeing of the stakeholders. In one of the instances, Mr Steward telephoned

Freedom for cancelling the policy on his son’s behalf. One of the representatives assured Mr

Stewart that recording of the call would be listened to. As per the assumptions of Tricker,

(2015), these calling options reflects the attempts towards averting the information gaps,

which can lead to negative results. Typical evidence of this lies in reverting back to Stewart

by the Company, indicating a conscious approach towards the needs and interest of Stewart

and his son. However, clarity regarding the disability in case of the son is a striking aspect in

case of Stewart. According to the revelations of the Final Report published by the

Commission, the Commission team members collaborate for submitting the prepared

research report to the Board panel.

Adherence to the Corporations Act (2001) is necessary for Freedom in terms of

ensuring that the financial services are effectively licensed. In this, the personnel ensure that

the personnel comply with the standards and codes of the financial laws. Insufficiency in the

quality assurance coverage reflects the unethical approach of the Insurance representatives in

terms of collecting the customer responses. In the breach report, the ASIC provided the link

to the remuneration structures with negative connotations to the vulnerable consumers.

Between 2013 and 2015, Freedom incorporated the volume based commission structure. In

the revelations of Rodriguez-Fernandez, (2016), incorporation of the variants in the models

can be related with the approach towards affecting the interest and decisions of the clients

like Mr Stewart and his son.

As a matter of specification, ethical issues arise when there is a problem to be solved

for achieving clear outcomes. In case of the non-availability of the outcomes, there is a

dilemmatic situation. These conditions result in the win-win, win-lose or lose-lose situation.

On the other hand, if the problem has win-win possibility, it is not accounted under ethical

issue of ethical dilemma. In such a situation, the decision matters in terms of the mutual

MANAGEMENT

ensuring the wellbeing of the stakeholders. In one of the instances, Mr Steward telephoned

Freedom for cancelling the policy on his son’s behalf. One of the representatives assured Mr

Stewart that recording of the call would be listened to. As per the assumptions of Tricker,

(2015), these calling options reflects the attempts towards averting the information gaps,

which can lead to negative results. Typical evidence of this lies in reverting back to Stewart

by the Company, indicating a conscious approach towards the needs and interest of Stewart

and his son. However, clarity regarding the disability in case of the son is a striking aspect in

case of Stewart. According to the revelations of the Final Report published by the

Commission, the Commission team members collaborate for submitting the prepared

research report to the Board panel.

Adherence to the Corporations Act (2001) is necessary for Freedom in terms of

ensuring that the financial services are effectively licensed. In this, the personnel ensure that

the personnel comply with the standards and codes of the financial laws. Insufficiency in the

quality assurance coverage reflects the unethical approach of the Insurance representatives in

terms of collecting the customer responses. In the breach report, the ASIC provided the link

to the remuneration structures with negative connotations to the vulnerable consumers.

Between 2013 and 2015, Freedom incorporated the volume based commission structure. In

the revelations of Rodriguez-Fernandez, (2016), incorporation of the variants in the models

can be related with the approach towards affecting the interest and decisions of the clients

like Mr Stewart and his son.

As a matter of specification, ethical issues arise when there is a problem to be solved

for achieving clear outcomes. In case of the non-availability of the outcomes, there is a

dilemmatic situation. These conditions result in the win-win, win-lose or lose-lose situation.

On the other hand, if the problem has win-win possibility, it is not accounted under ethical

issue of ethical dilemma. In such a situation, the decision matters in terms of the mutual

8

MANAGEMENT

interest of the parties involved. In the case scenario, the possible outcomes is problematic to

achieve, as Mr Stewart was unaware of his son’s disability. However, Rasche, Morsing and

Moon, (2017), this adds hypothetical parameter to the outcomes. The presence of alternatives

relates to the ethical approach in terms of respecting the mutual interest of the clients and the

customers. If Freedom had revalued the assets, it would have allowed the company to align

the standards of the operations with the accounting standards.

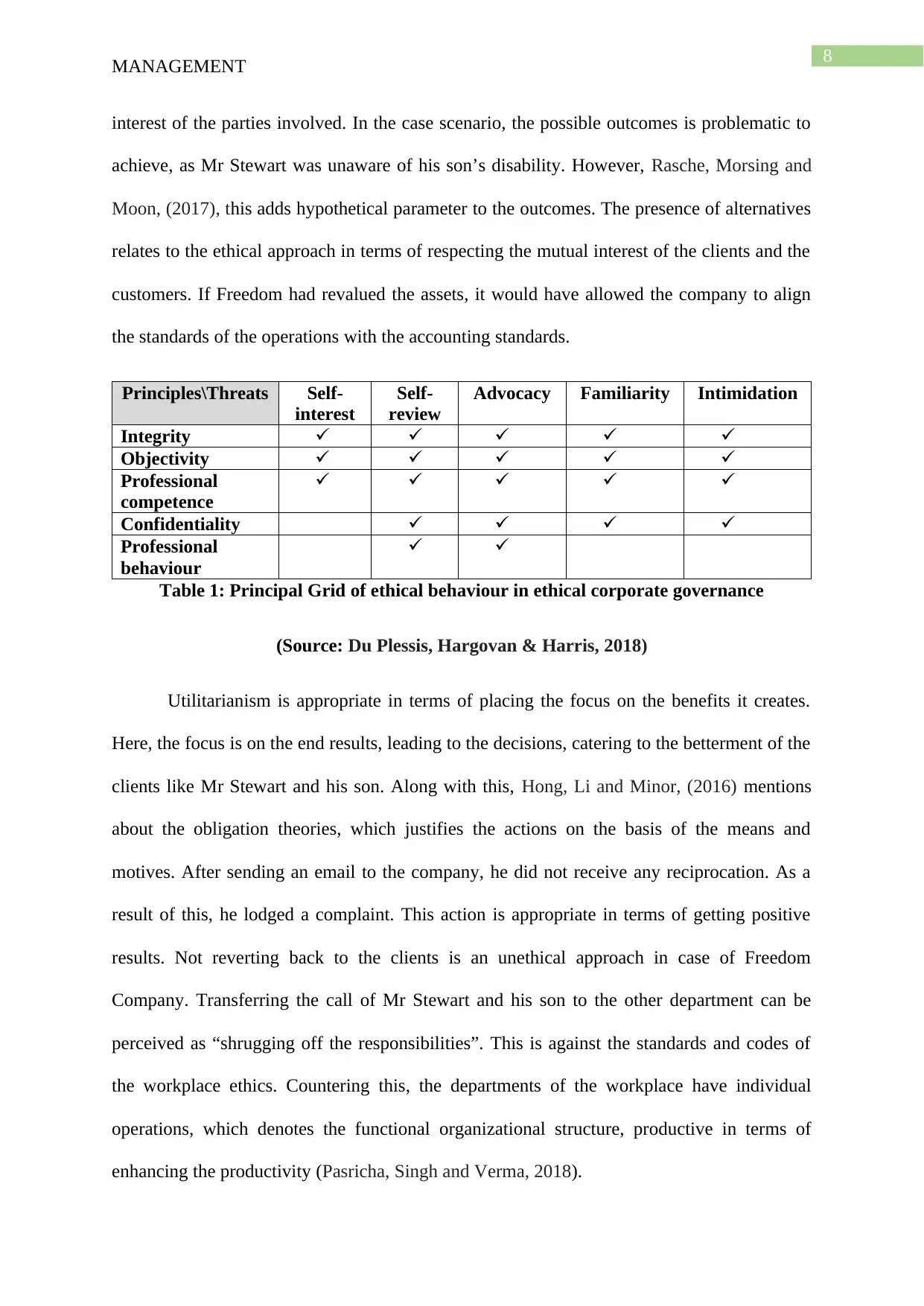

Principles\Threats Self-

interest

Self-

review

Advocacy Familiarity Intimidation

Integrity

Objectivity

Professional

competence

Confidentiality

Professional

behaviour

Table 1: Principal Grid of ethical behaviour in ethical corporate governance

(Source: Du Plessis, Hargovan & Harris, 2018)

Utilitarianism is appropriate in terms of placing the focus on the benefits it creates.

Here, the focus is on the end results, leading to the decisions, catering to the betterment of the

clients like Mr Stewart and his son. Along with this, Hong, Li and Minor, (2016) mentions

about the obligation theories, which justifies the actions on the basis of the means and

motives. After sending an email to the company, he did not receive any reciprocation. As a

result of this, he lodged a complaint. This action is appropriate in terms of getting positive

results. Not reverting back to the clients is an unethical approach in case of Freedom

Company. Transferring the call of Mr Stewart and his son to the other department can be

perceived as “shrugging off the responsibilities”. This is against the standards and codes of

the workplace ethics. Countering this, the departments of the workplace have individual

operations, which denotes the functional organizational structure, productive in terms of

enhancing the productivity (Pasricha, Singh and Verma, 2018).

MANAGEMENT

interest of the parties involved. In the case scenario, the possible outcomes is problematic to

achieve, as Mr Stewart was unaware of his son’s disability. However, Rasche, Morsing and

Moon, (2017), this adds hypothetical parameter to the outcomes. The presence of alternatives

relates to the ethical approach in terms of respecting the mutual interest of the clients and the

customers. If Freedom had revalued the assets, it would have allowed the company to align

the standards of the operations with the accounting standards.

Principles\Threats Self-

interest

Self-

review

Advocacy Familiarity Intimidation

Integrity

Objectivity

Professional

competence

Confidentiality

Professional

behaviour

Table 1: Principal Grid of ethical behaviour in ethical corporate governance

(Source: Du Plessis, Hargovan & Harris, 2018)

Utilitarianism is appropriate in terms of placing the focus on the benefits it creates.

Here, the focus is on the end results, leading to the decisions, catering to the betterment of the

clients like Mr Stewart and his son. Along with this, Hong, Li and Minor, (2016) mentions

about the obligation theories, which justifies the actions on the basis of the means and

motives. After sending an email to the company, he did not receive any reciprocation. As a

result of this, he lodged a complaint. This action is appropriate in terms of getting positive

results. Not reverting back to the clients is an unethical approach in case of Freedom

Company. Transferring the call of Mr Stewart and his son to the other department can be

perceived as “shrugging off the responsibilities”. This is against the standards and codes of

the workplace ethics. Countering this, the departments of the workplace have individual

operations, which denotes the functional organizational structure, productive in terms of

enhancing the productivity (Pasricha, Singh and Verma, 2018).

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9

MANAGEMENT

Clarification regarding the information and its justification safeguards the retention

agent in terms of complying with the ethical standards. Countering this, making disparaging

comments in messenger is unacceptable and against the ethical standards of corporate

governance. Mr Orton accepted the offer, which was inappropriate in terms of the legal

standards of the ethics, which needs to be followed in the workplace. During the call for

cancelling the policy, Mr Stewart asked the company to produce the copies of the sales call

recordings with his son. When the Commission intervened to investigate the matter, it was

found that Mr Stewart did not receive the copies until August 2018. This issue is problematic

in terms of possessing the relevant documents for legalizing the accounting business

operations (Dion et al., 2016).

One of the striking and unethical aspects is the discontinuation of the call upon

finding that Mrs Stewart is not at home. However, this approach aligns with the accounting

standards, as in absence of the claimant, the policy can be sold to the nominees. This is with

due consideration to the fact that consent is taken from the nominees and they are duly

registered in the company’s records. According to the claims of Mr Stewart, his approach to

the Commission reflects his lack of understanding regarding his son’s actions.

As per the arguments of Lopez and Medina, (2015), confession regarding the

engagement in misdeeds and the impact of the vulnerable customers reflects an attempt to

restore the stability in the relationship with the customers. This approach relates to the ethical

principles and the accounting standards. According to the intensity, the misconduct fell below

the standards and expectations. However, introduction of the Vulnerable Customers Training

in February 2017 can be considered as a compensation for the misdeed. However, Salvioni

and Gennari, (2016), issues of complaints add interrogative parameter to the planning

towards customer relationship management.

MANAGEMENT

Clarification regarding the information and its justification safeguards the retention

agent in terms of complying with the ethical standards. Countering this, making disparaging

comments in messenger is unacceptable and against the ethical standards of corporate

governance. Mr Orton accepted the offer, which was inappropriate in terms of the legal

standards of the ethics, which needs to be followed in the workplace. During the call for

cancelling the policy, Mr Stewart asked the company to produce the copies of the sales call

recordings with his son. When the Commission intervened to investigate the matter, it was

found that Mr Stewart did not receive the copies until August 2018. This issue is problematic

in terms of possessing the relevant documents for legalizing the accounting business

operations (Dion et al., 2016).

One of the striking and unethical aspects is the discontinuation of the call upon

finding that Mrs Stewart is not at home. However, this approach aligns with the accounting

standards, as in absence of the claimant, the policy can be sold to the nominees. This is with

due consideration to the fact that consent is taken from the nominees and they are duly

registered in the company’s records. According to the claims of Mr Stewart, his approach to

the Commission reflects his lack of understanding regarding his son’s actions.

As per the arguments of Lopez and Medina, (2015), confession regarding the

engagement in misdeeds and the impact of the vulnerable customers reflects an attempt to

restore the stability in the relationship with the customers. This approach relates to the ethical

principles and the accounting standards. According to the intensity, the misconduct fell below

the standards and expectations. However, introduction of the Vulnerable Customers Training

in February 2017 can be considered as a compensation for the misdeed. However, Salvioni

and Gennari, (2016), issues of complaints add interrogative parameter to the planning

towards customer relationship management.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10

MANAGEMENT

Informing the Commission regarding ceasing the outbound sales of the products is

ethical. Upon requests of the customers, consistency was maintained in terms of outbound

sales of the products in the website. This was in terms of the evidence produced by Mr Orton.

Producing written statement to the Commission regarding the contents of the outbound sales

is accounted within the ethical rules and regulations. However, he clarified that the coverage

points of the policies were not the substitute to the life cover insurance. As per the

assumptions of Birindelli et al., (2015), combination of the accidental death cover policies

with accidental injury rider is cost effective alternative. Disseminating the information about

the alternatives is an attempt towards diversifying the thought processes and judgmental

capabilities.

In terms of the quality assurance and disciplinary processes, the Commission heard

about the ineffective disciplinary practices adopted by Freedom. The actions accompanied the

sales policy sold to Mr Stewart’s son. Sending initial warning is accounted within the ethical

principles, legitimizing the corporate governance. Mention can be made of the retention

strategies, where Freedom acknowledged 26 instances related to the retention processes.

Most of these instances consisted of the complaints received in the early 2018. Along with

this, Jones et al., (2016), reference can be cited of the information related to the retention

marketing campaigns organized by the company.

Reviewing the instances by ASIC reflects proper handling of the unethical issues in

case of Freedom. This investigation proves apt in terms of producing final verdict for

respecting the individual sentiments and mutual interests of the clients like Mr Stewart, his

son and Mr Orton among others. Not addressing all of the issues in reporting to the

Commission is a major issue for generating evidence based practices in the accounts

(Salvioni and Gennari, 2016). Typical evidence of this lies in the non-inclusion of the case of

treatment towards the vulnerable customers in the Breach statement produced to ASIC.

MANAGEMENT

Informing the Commission regarding ceasing the outbound sales of the products is

ethical. Upon requests of the customers, consistency was maintained in terms of outbound

sales of the products in the website. This was in terms of the evidence produced by Mr Orton.

Producing written statement to the Commission regarding the contents of the outbound sales

is accounted within the ethical rules and regulations. However, he clarified that the coverage

points of the policies were not the substitute to the life cover insurance. As per the

assumptions of Birindelli et al., (2015), combination of the accidental death cover policies

with accidental injury rider is cost effective alternative. Disseminating the information about

the alternatives is an attempt towards diversifying the thought processes and judgmental

capabilities.

In terms of the quality assurance and disciplinary processes, the Commission heard

about the ineffective disciplinary practices adopted by Freedom. The actions accompanied the

sales policy sold to Mr Stewart’s son. Sending initial warning is accounted within the ethical

principles, legitimizing the corporate governance. Mention can be made of the retention

strategies, where Freedom acknowledged 26 instances related to the retention processes.

Most of these instances consisted of the complaints received in the early 2018. Along with

this, Jones et al., (2016), reference can be cited of the information related to the retention

marketing campaigns organized by the company.

Reviewing the instances by ASIC reflects proper handling of the unethical issues in

case of Freedom. This investigation proves apt in terms of producing final verdict for

respecting the individual sentiments and mutual interests of the clients like Mr Stewart, his

son and Mr Orton among others. Not addressing all of the issues in reporting to the

Commission is a major issue for generating evidence based practices in the accounts

(Salvioni and Gennari, 2016). Typical evidence of this lies in the non-inclusion of the case of

treatment towards the vulnerable customers in the Breach statement produced to ASIC.

11

MANAGEMENT

Acceptance of Mr Orton regarding governance practices and remuneration is a

deviant behaviour in terms of the workplace culture. This is highly aggressive, adding

to the inappropriateness of the sales practices. Typical evidence of this lies in the

incorporation of ineffective and insufficient quality assurance methods. Failure to provide

training to the staffs aggravate the complexities in fulfilling the needs, demands and

requirements of the customers.

If Freedom had conducted cost benefit analysis, they would have been able to map the

impact on the clients and the customers. In this, Dion, Weisstub and Richet, (2016) refers that

consideration of the behaviours based on the principles of ethical corporate governance is

crucial. Rationality and consciousness in this direction would have been helpful for

measuring the utility value of the principles. Balance in the accounting operations and

standards is missing, which adds a hypothetical approach towards the claims produced in the

final report. In this, mention can be made of the virtue ethics of fairness, which would have

projected equal treatment for the clients and the customers (Hong, Li & Minor, 2016).

Conclusion

Reliance on the routine decisions is beneficial for companies like Freedom in terms of

getting the support of the policies. This type of decisions are productive for the managers, as

they get good guidance. On the other hand, non-routine decisions require high levels of

professional judgement and ethical awareness, which is not always possible in terms of

inadequate supportive materials. Proper consideration of the alternatives is needed for

generating fairness in the accounting operations. Within this, infusing ethical values in the

operations is beneficial for achieving trust, loyalty and dependence from the clients and the

customers. Communication channels need to be proper in terms of maximizing the profit

margin.

MANAGEMENT

Acceptance of Mr Orton regarding governance practices and remuneration is a

deviant behaviour in terms of the workplace culture. This is highly aggressive, adding

to the inappropriateness of the sales practices. Typical evidence of this lies in the

incorporation of ineffective and insufficient quality assurance methods. Failure to provide

training to the staffs aggravate the complexities in fulfilling the needs, demands and

requirements of the customers.

If Freedom had conducted cost benefit analysis, they would have been able to map the

impact on the clients and the customers. In this, Dion, Weisstub and Richet, (2016) refers that

consideration of the behaviours based on the principles of ethical corporate governance is

crucial. Rationality and consciousness in this direction would have been helpful for

measuring the utility value of the principles. Balance in the accounting operations and

standards is missing, which adds a hypothetical approach towards the claims produced in the

final report. In this, mention can be made of the virtue ethics of fairness, which would have

projected equal treatment for the clients and the customers (Hong, Li & Minor, 2016).

Conclusion

Reliance on the routine decisions is beneficial for companies like Freedom in terms of

getting the support of the policies. This type of decisions are productive for the managers, as

they get good guidance. On the other hand, non-routine decisions require high levels of

professional judgement and ethical awareness, which is not always possible in terms of

inadequate supportive materials. Proper consideration of the alternatives is needed for

generating fairness in the accounting operations. Within this, infusing ethical values in the

operations is beneficial for achieving trust, loyalty and dependence from the clients and the

customers. Communication channels need to be proper in terms of maximizing the profit

margin.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.