Comparison of Management and Financial Accounting for Business

VerifiedAdded on 2023/01/11

|6

|1090

|45

Report

AI Summary

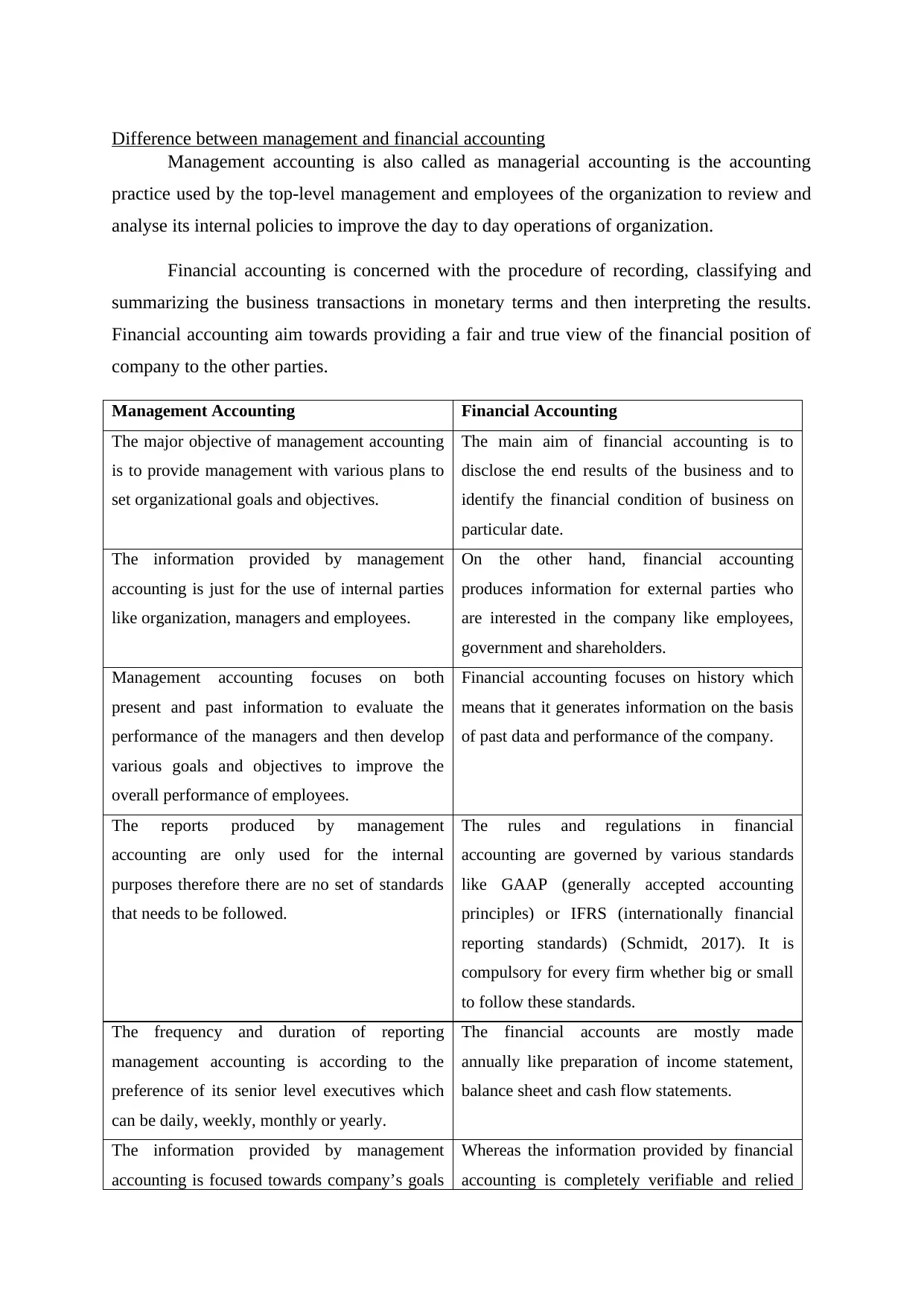

This report provides a comparative analysis of management and financial accounting, elucidating their distinct objectives, target users, and reporting methodologies. Management accounting, also known as managerial accounting, is designed for internal use, assisting in operational improvements and strategic planning. Conversely, financial accounting focuses on providing a comprehensive overview of a company's financial position to external stakeholders such as investors, creditors, and the government. The report details the key differences in their approaches, including the application of standards like GAAP and IFRS in financial accounting. Furthermore, it emphasizes the importance of financial information to various users, outlining how financial statements like balance sheets, income statements, and cash flow analyses are crucial for informed decision-making by owners, creditors, employees, investors, government bodies, shareholders, and suppliers. The report underscores the significance of financial data in assessing a company's performance and making strategic financial decisions.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.