Management and Financial Accounts: Analysis and Differences Report

VerifiedAdded on 2023/01/12

|7

|1285

|33

Report

AI Summary

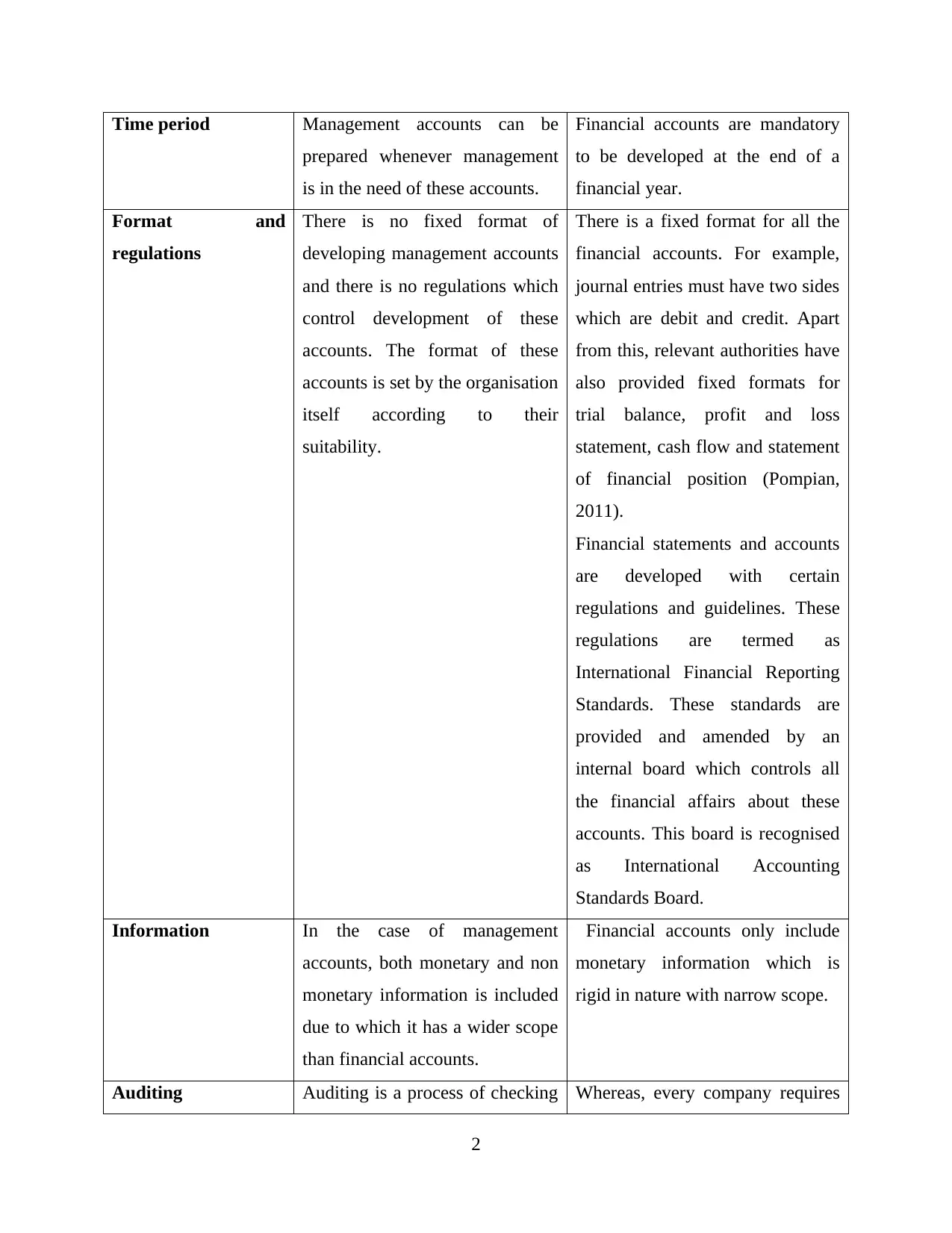

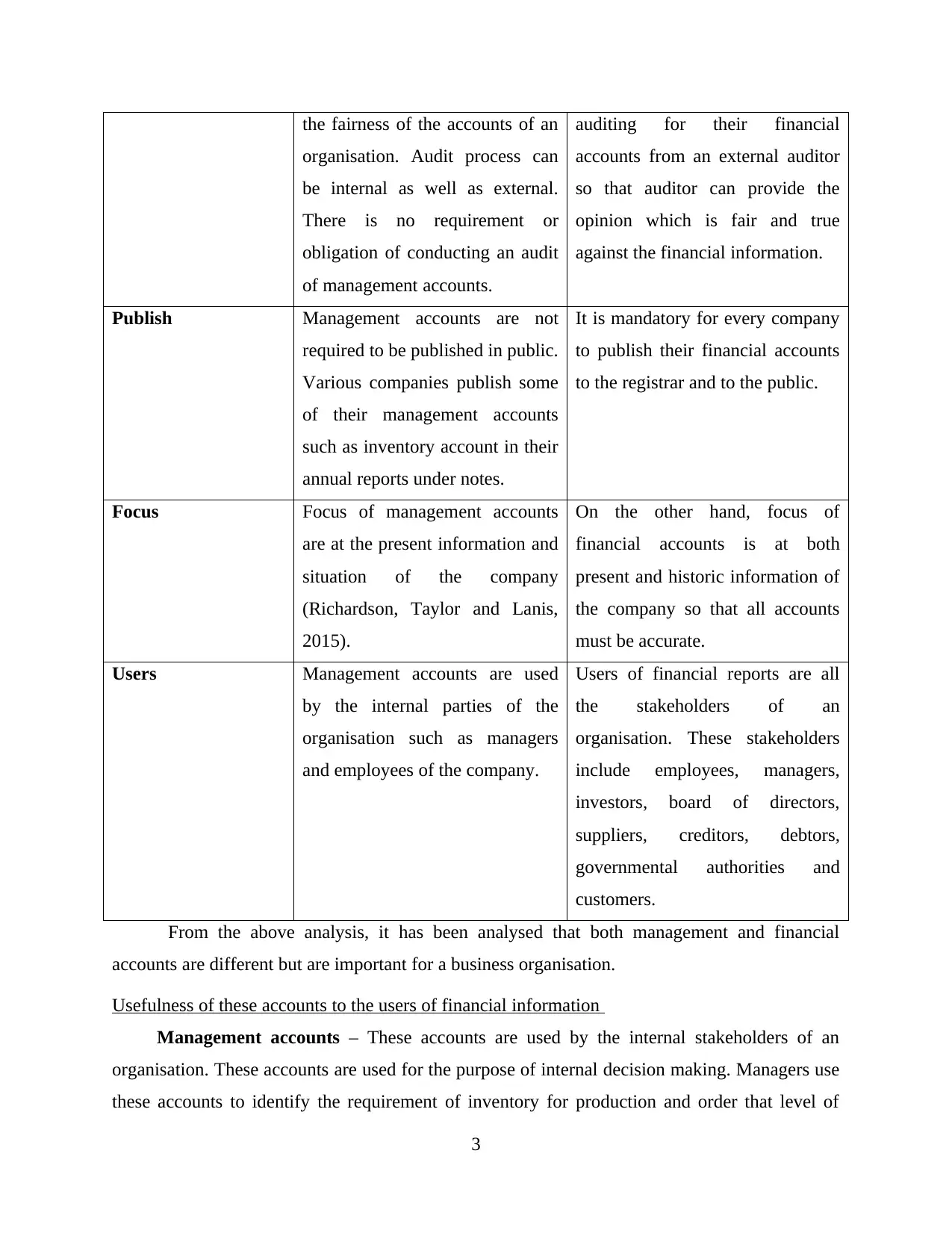

This report provides a comprehensive comparison of management and financial accounts, highlighting their key differences and respective uses. The introduction defines accountancy and its role in business, setting the stage for a detailed analysis of the two types of accounts. The main body differentiates between management accounts, which are internally focused and flexible, and financial accounts, which adhere to strict standards like IFRS and are used for external reporting. It examines differences in objectives, compulsion, time periods, formats, information scope, auditing requirements, publication, and user groups. The report then explores the usefulness of each account type to various stakeholders, including managers, employees, shareholders, creditors, and governmental authorities. It emphasizes how management accounts support internal decision-making, while financial accounts facilitate external reporting and investment analysis. The conclusion summarizes the importance of both account types for effective business control and management.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.