Management Accounting Report: Budgeting and Financial Analysis

VerifiedAdded on 2020/10/22

|19

|4107

|129

Report

AI Summary

This report comprehensively examines management accounting principles and their practical applications, focusing on Jupiter PLC as a case study. It begins by defining management accounting, outlining its essential requirements, and differentiating it from financial accounting. The report delves into various management accounting reports, including cost reports, budgets, and performance reports, evaluating their benefits and applications. It critically assesses the integration of management accounting systems with organizational processes, emphasizing accuracy and efficiency. The report further explores planning tools, such as budgetary control, analyzing their advantages and disadvantages, and demonstrating their application through case studies and financial forecasting. It then compares different organizational approaches to adopting management accounting systems to address financial problems, ultimately evaluating planning tools for solving financial challenges and achieving sustainable success for Jupiter PLC. The report includes detailed analysis of marginal and absorption costing, and various budgets, like operational, cash, and master budgets, to facilitate effective financial planning and decision-making.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Explaining management accounting with its essential requirements and types....................1

1.2 Explaining different methods of management accounting reporting.....................................2

1.3 Evaluating benefits of management accounting system with its application........................2

1.4 Critical evaluation of management accounting system and reporting is integrated with

process of organization................................................................................................................3

TASK 2............................................................................................................................................4

TASK 3............................................................................................................................................5

3.1 Explaining advantages and disadvantages of planning tools with application of Budgetary

control .........................................................................................................................................5

Analysing application of various planning tools for forecasting and preparing budget..............6

TASK 4............................................................................................................................................7

4.1 Comparing organization for purpose of adopting management accounting system to

respond to financial problems......................................................................................................7

4.2 Analysing context of financial problem that management accounting will lead to

sustainable success of organization ............................................................................................9

4.3 Evaluating planning tools of accounting for purpose of solving financial problems to lead

with sustainable success.............................................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

1.1 Explaining management accounting with its essential requirements and types....................1

1.2 Explaining different methods of management accounting reporting.....................................2

1.3 Evaluating benefits of management accounting system with its application........................2

1.4 Critical evaluation of management accounting system and reporting is integrated with

process of organization................................................................................................................3

TASK 2............................................................................................................................................4

TASK 3............................................................................................................................................5

3.1 Explaining advantages and disadvantages of planning tools with application of Budgetary

control .........................................................................................................................................5

Analysing application of various planning tools for forecasting and preparing budget..............6

TASK 4............................................................................................................................................7

4.1 Comparing organization for purpose of adopting management accounting system to

respond to financial problems......................................................................................................7

4.2 Analysing context of financial problem that management accounting will lead to

sustainable success of organization ............................................................................................9

4.3 Evaluating planning tools of accounting for purpose of solving financial problems to lead

with sustainable success.............................................................................................................10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Accounting is replicated as process of identifying, measuring and communicating

economic data for allowing judgements and informed decision through users of data as per

American Accounting Association. The present report will discuss about essential requirements

of management accounting with its types. This report will reflect various types of management

accounting reports with its need as well. It will also show various planning tools with its

advantages and disadvantages and benefit to Jupiter PLC. In the similar aspect, it will articulate

planning tools for responding to solve financial problems to lead organization for attaining

sustainable success.

TASK 1

1.1 Explaining management accounting with its essential requirements and types

Management accounting system is replicated as process of identifying, measuring,

analysing, communicating and interpreting financial information for accomplishing objectives of

organization. It is also known as cost accounting. Financial and management accounting could

be differed by management accounting information with objective of assisting managers for

taking decisions but financial accounting has targeted of offering information to its external

parties. The process of preparing management reports and accounts offers accurate and timely

statistical financial information required through managers for establishing regular and decision

of short term. It consists of numerous reports which are formed for accomplishing management

requirements. There are various types of management accounting system such as job costing,

inventory management and cost accounting system (Nitzl, 2018).

Job costing system: It is referred as system of allocation of cost of manufacturing to

specific individual item or might be product batched. It had engagement of practice of

accumulation of data on cost on basis of production job or particular service of Jupiter

PLC. The information is required for submitting cost data to a customer under contract

where cost id directly refunded. It has requirement of accumulating three types of direct

information about labour, overhead and direct material as well.

Cost accounting system: It is a framework which is applied through Jupiter PLC for

approximate the cost of products for inventory valuation, cost control and profitability

analysis. With context of this system, cost allocation is performed on basis of traditional

or activity based costing system. The cost of actual product is important for effective

1

Accounting is replicated as process of identifying, measuring and communicating

economic data for allowing judgements and informed decision through users of data as per

American Accounting Association. The present report will discuss about essential requirements

of management accounting with its types. This report will reflect various types of management

accounting reports with its need as well. It will also show various planning tools with its

advantages and disadvantages and benefit to Jupiter PLC. In the similar aspect, it will articulate

planning tools for responding to solve financial problems to lead organization for attaining

sustainable success.

TASK 1

1.1 Explaining management accounting with its essential requirements and types

Management accounting system is replicated as process of identifying, measuring,

analysing, communicating and interpreting financial information for accomplishing objectives of

organization. It is also known as cost accounting. Financial and management accounting could

be differed by management accounting information with objective of assisting managers for

taking decisions but financial accounting has targeted of offering information to its external

parties. The process of preparing management reports and accounts offers accurate and timely

statistical financial information required through managers for establishing regular and decision

of short term. It consists of numerous reports which are formed for accomplishing management

requirements. There are various types of management accounting system such as job costing,

inventory management and cost accounting system (Nitzl, 2018).

Job costing system: It is referred as system of allocation of cost of manufacturing to

specific individual item or might be product batched. It had engagement of practice of

accumulation of data on cost on basis of production job or particular service of Jupiter

PLC. The information is required for submitting cost data to a customer under contract

where cost id directly refunded. It has requirement of accumulating three types of direct

information about labour, overhead and direct material as well.

Cost accounting system: It is a framework which is applied through Jupiter PLC for

approximate the cost of products for inventory valuation, cost control and profitability

analysis. With context of this system, cost allocation is performed on basis of traditional

or activity based costing system. The cost of actual product is important for effective

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

roles. Cost accounting is type of accounting system whose objective is to capture Jupiter

PLC's cost of production via weighing its input cost of production.

Inventory management: It is referred as method of overseeing and controlling the

ordering, application and storage of various components where Jupiter PLC's production

of sold goods. The efficient tracking of quantities across location of stock and managers

had gained insight and capability for taking decision about sufficient inventory.

1.2 Explaining different methods of management accounting reporting

Managerial accounting lays special emphasis on internal information gained through

financial accounting. Generally, it is applied for decision making, planning and controlling.

Management accountants has high dependency on various financial statements consist of income

statement, balance sheet and cash flow statement. The types of management account reports are:

Cost reports: The cost has been calculated of manufactured items through management

accounting. It is performed via considering cost, raw product overhead, labour along with

consideration of extra cost. The aggregate is categorised in amount of goods which are

produced as all data is directly summarized in cost report. Generally, this report helps in

permitting managers with capability of reflecting cost value of products vs selling price.

The profit margin has been controlled and planned through managers.

Budget: It is one of key element for preparing budget in management accounting.

Budgets are directly formed with applying budget of previous year and adjusted in

prediction of future. All revenue and expense sources are listed in budget of Jupiter PLC.

It had been attained for attaining its goals and objectives to stay in budgeted amount.

Performance reports: The budgets are applied through management accountants for

comparing expenditures and revenue to budgeted amounts. The computed variations are

evaluated by shaping innovative budgets along with concerned information of amount

listed in this performance report of Jupiter PLC (Hiebl, 2018).

1.3 Evaluating benefits of management accounting system with its application

The benefits of specific management accounting system are evaluated as follows:

Job Costing system: In this system, cost might be directly ascertained at stage of job

completion and it provides scope for purpose of controlling cost. The profit which had

been earned through each individual job is replicated as job costing. Management could

be able for estimating cost of job with context of previous records. However, there is

2

PLC's cost of production via weighing its input cost of production.

Inventory management: It is referred as method of overseeing and controlling the

ordering, application and storage of various components where Jupiter PLC's production

of sold goods. The efficient tracking of quantities across location of stock and managers

had gained insight and capability for taking decision about sufficient inventory.

1.2 Explaining different methods of management accounting reporting

Managerial accounting lays special emphasis on internal information gained through

financial accounting. Generally, it is applied for decision making, planning and controlling.

Management accountants has high dependency on various financial statements consist of income

statement, balance sheet and cash flow statement. The types of management account reports are:

Cost reports: The cost has been calculated of manufactured items through management

accounting. It is performed via considering cost, raw product overhead, labour along with

consideration of extra cost. The aggregate is categorised in amount of goods which are

produced as all data is directly summarized in cost report. Generally, this report helps in

permitting managers with capability of reflecting cost value of products vs selling price.

The profit margin has been controlled and planned through managers.

Budget: It is one of key element for preparing budget in management accounting.

Budgets are directly formed with applying budget of previous year and adjusted in

prediction of future. All revenue and expense sources are listed in budget of Jupiter PLC.

It had been attained for attaining its goals and objectives to stay in budgeted amount.

Performance reports: The budgets are applied through management accountants for

comparing expenditures and revenue to budgeted amounts. The computed variations are

evaluated by shaping innovative budgets along with concerned information of amount

listed in this performance report of Jupiter PLC (Hiebl, 2018).

1.3 Evaluating benefits of management accounting system with its application

The benefits of specific management accounting system are evaluated as follows:

Job Costing system: In this system, cost might be directly ascertained at stage of job

completion and it provides scope for purpose of controlling cost. The profit which had

been earned through each individual job is replicated as job costing. Management could

be able for estimating cost of job with context of previous records. However, there is

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

absence of standardization of job along with requirement of close supervision. It is

expensive and no possibility of cost control as its controlling steps are considered after

incurring expenses in Jupiter PLC.

Cost Accounting system: Cost accounting is directly based on kind, efficiency and

adequacy of installation of this system. It substitutes loss, waste and inefficiency through

fixing standards. It leads to innovative and improved production method which is

followed with this system and helps in cost reduction. However, previous performance is

availability in records of costing but decisions are taken by management for future

perspective of Jupiter PLC. Here the cost of previous year is not similar in succeeding

year as cost data is not useful. It fails for solving problems on basis of work study,

motion and time study along with operation research.

Inventory management system: This system helps Jupiter PLC for lowering cost as if it

has huge amount of inventory then it will not tend for ability for running this organization

in smooth aspect. In the similar aspect, effective inventory systems products helps in

increasing operating performance along with productivity as well. On the contrary, this

system cost very high and price is replicated as an issue for firms like Jupiter PLC

(Lawson and White, 2018).

1.4 Critical evaluation of management accounting system and reporting is integrated with

process of organization

Integration of management accounting is known as software application which directly

standardises procedure of tracing numerous transaction and to disseminate the financial

information. In the similar aspect, it interlinks the activities of reporting of various functional

areas of Jupiter PLC like point of sales, front and back office along with stores. Simultaneously,

it streamlines output and input information of functions of financial reporting and management

accounting. The integrated financial system will be adopted and it would enhance accuracy,

efficiency and speed for processing financial information. It simplifies accounting process of

Jupiter PLC and decreases duplicate work (Ax and Greve, 2017). It substitutes reconcile among

different margin reflected by accounting methods.

Similarly, it is non integral system where financial accounting records are appropriately

maintained at strict accuracy level for acquiring needs of outsiders. It provides great accuracy but

on the contrary, it is combination of whole data as it runs risk by giving huge information on

3

expensive and no possibility of cost control as its controlling steps are considered after

incurring expenses in Jupiter PLC.

Cost Accounting system: Cost accounting is directly based on kind, efficiency and

adequacy of installation of this system. It substitutes loss, waste and inefficiency through

fixing standards. It leads to innovative and improved production method which is

followed with this system and helps in cost reduction. However, previous performance is

availability in records of costing but decisions are taken by management for future

perspective of Jupiter PLC. Here the cost of previous year is not similar in succeeding

year as cost data is not useful. It fails for solving problems on basis of work study,

motion and time study along with operation research.

Inventory management system: This system helps Jupiter PLC for lowering cost as if it

has huge amount of inventory then it will not tend for ability for running this organization

in smooth aspect. In the similar aspect, effective inventory systems products helps in

increasing operating performance along with productivity as well. On the contrary, this

system cost very high and price is replicated as an issue for firms like Jupiter PLC

(Lawson and White, 2018).

1.4 Critical evaluation of management accounting system and reporting is integrated with

process of organization

Integration of management accounting is known as software application which directly

standardises procedure of tracing numerous transaction and to disseminate the financial

information. In the similar aspect, it interlinks the activities of reporting of various functional

areas of Jupiter PLC like point of sales, front and back office along with stores. Simultaneously,

it streamlines output and input information of functions of financial reporting and management

accounting. The integrated financial system will be adopted and it would enhance accuracy,

efficiency and speed for processing financial information. It simplifies accounting process of

Jupiter PLC and decreases duplicate work (Ax and Greve, 2017). It substitutes reconcile among

different margin reflected by accounting methods.

Similarly, it is non integral system where financial accounting records are appropriately

maintained at strict accuracy level for acquiring needs of outsiders. It provides great accuracy but

on the contrary, it is combination of whole data as it runs risk by giving huge information on

3

financial aspect. The financial reports are designed on frequent aspect as operation of Jupiter Plc

are understood through readers. It substitutes identical entries and adds additional level of

complexity for entering data which is undertaken in business's accounting side. Further integral

accounting has need of financial accounting team which is responsible for quarterly reports of

production and work on daily report cycle for accomplishing requirements of Jupiter's managers

with its operation.

TASK 2

Marginal costing: It is a costing technique where marginal cost such as variable cost is

directly charged to units of cost but fixed cost for specific duration is fully written off against the

contribution.

Absorption costing: It is a management accounting method where all expenses and

associated cost related to manufacturing of single product is required for external reporting of

GAAP. In simple words, cost of finished unit in inventory consist of direct labor, material and

both overhead of fixed and variable manufacturing (Granlund and Lukka, 2017).

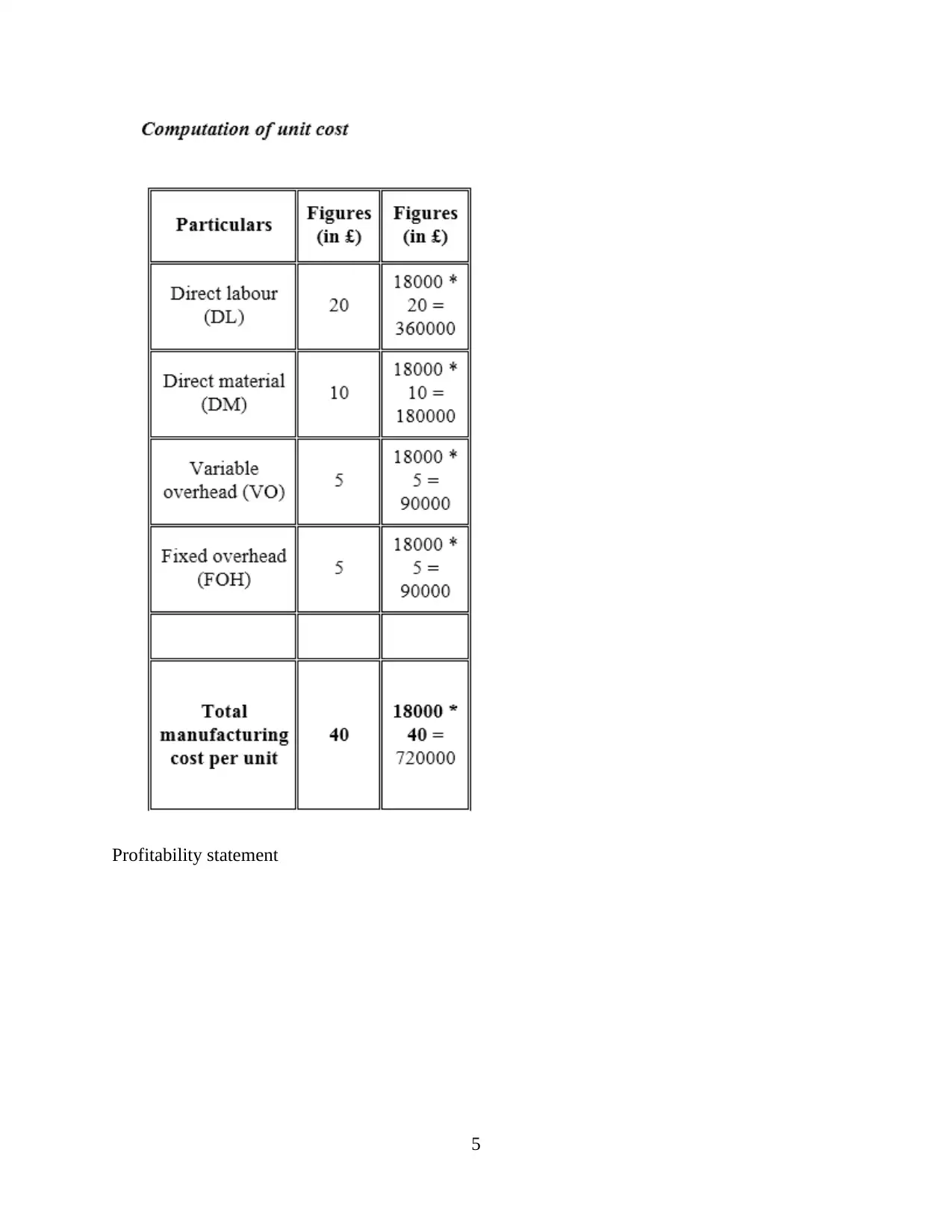

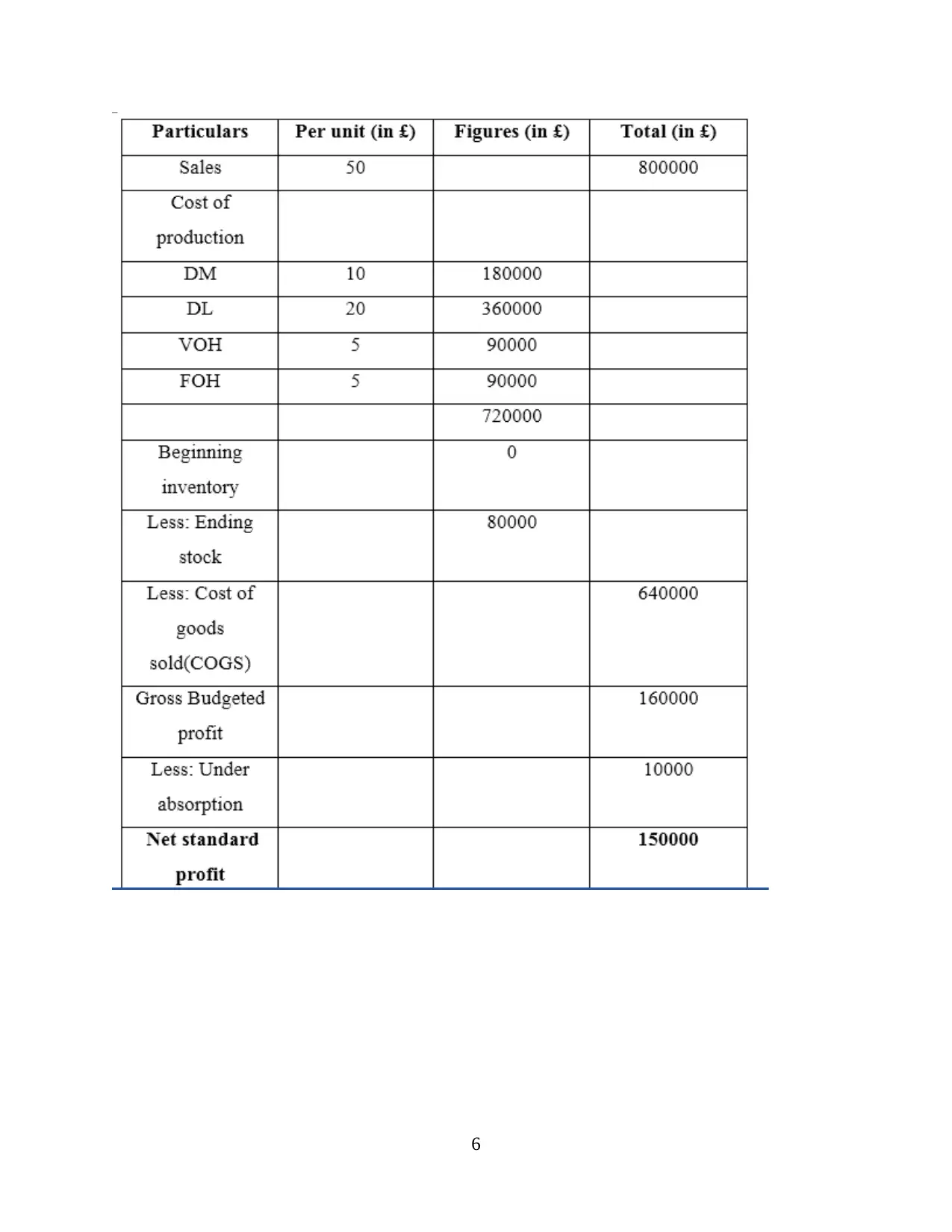

Absorption costing

4

are understood through readers. It substitutes identical entries and adds additional level of

complexity for entering data which is undertaken in business's accounting side. Further integral

accounting has need of financial accounting team which is responsible for quarterly reports of

production and work on daily report cycle for accomplishing requirements of Jupiter's managers

with its operation.

TASK 2

Marginal costing: It is a costing technique where marginal cost such as variable cost is

directly charged to units of cost but fixed cost for specific duration is fully written off against the

contribution.

Absorption costing: It is a management accounting method where all expenses and

associated cost related to manufacturing of single product is required for external reporting of

GAAP. In simple words, cost of finished unit in inventory consist of direct labor, material and

both overhead of fixed and variable manufacturing (Granlund and Lukka, 2017).

Absorption costing

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Profitability statement

5

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

6

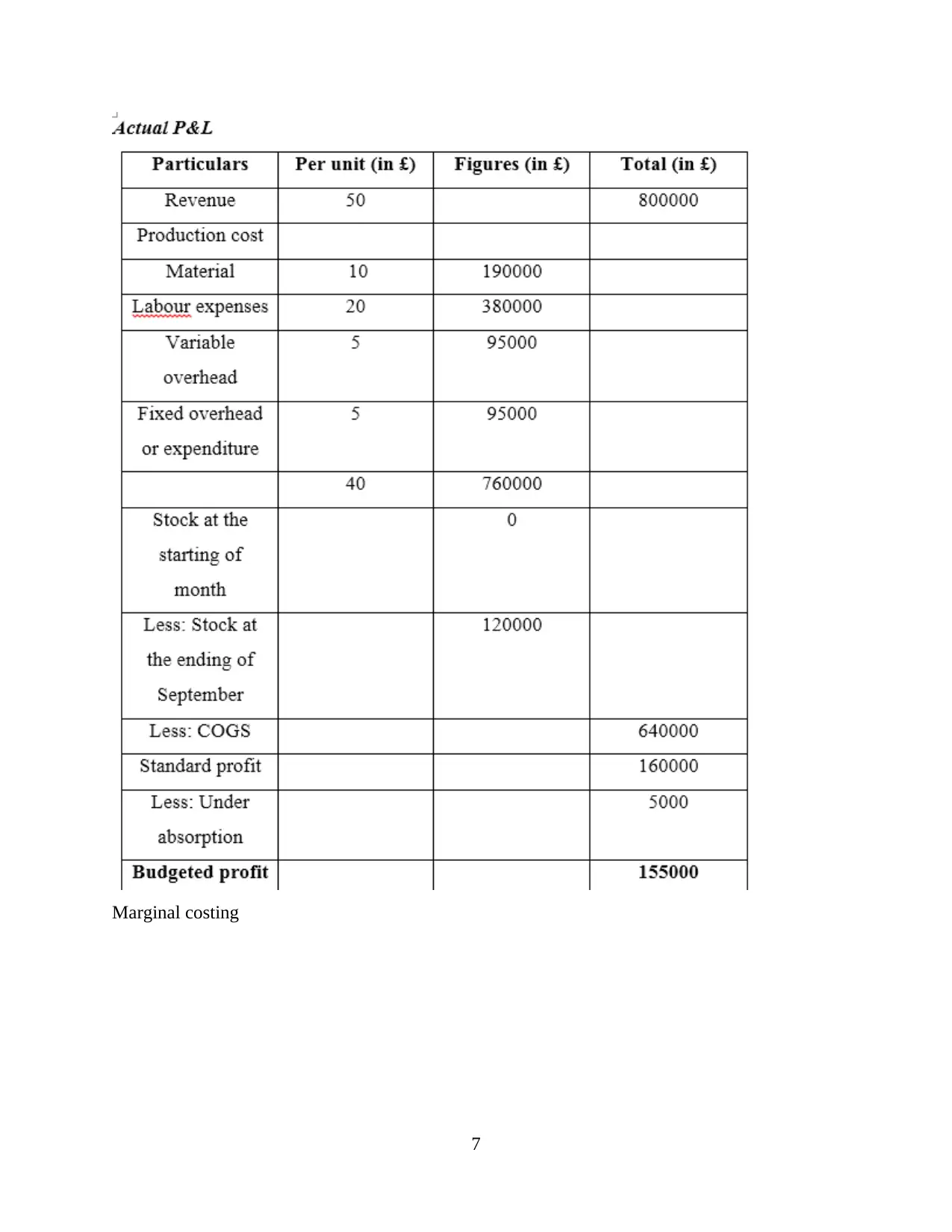

Marginal costing

7

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

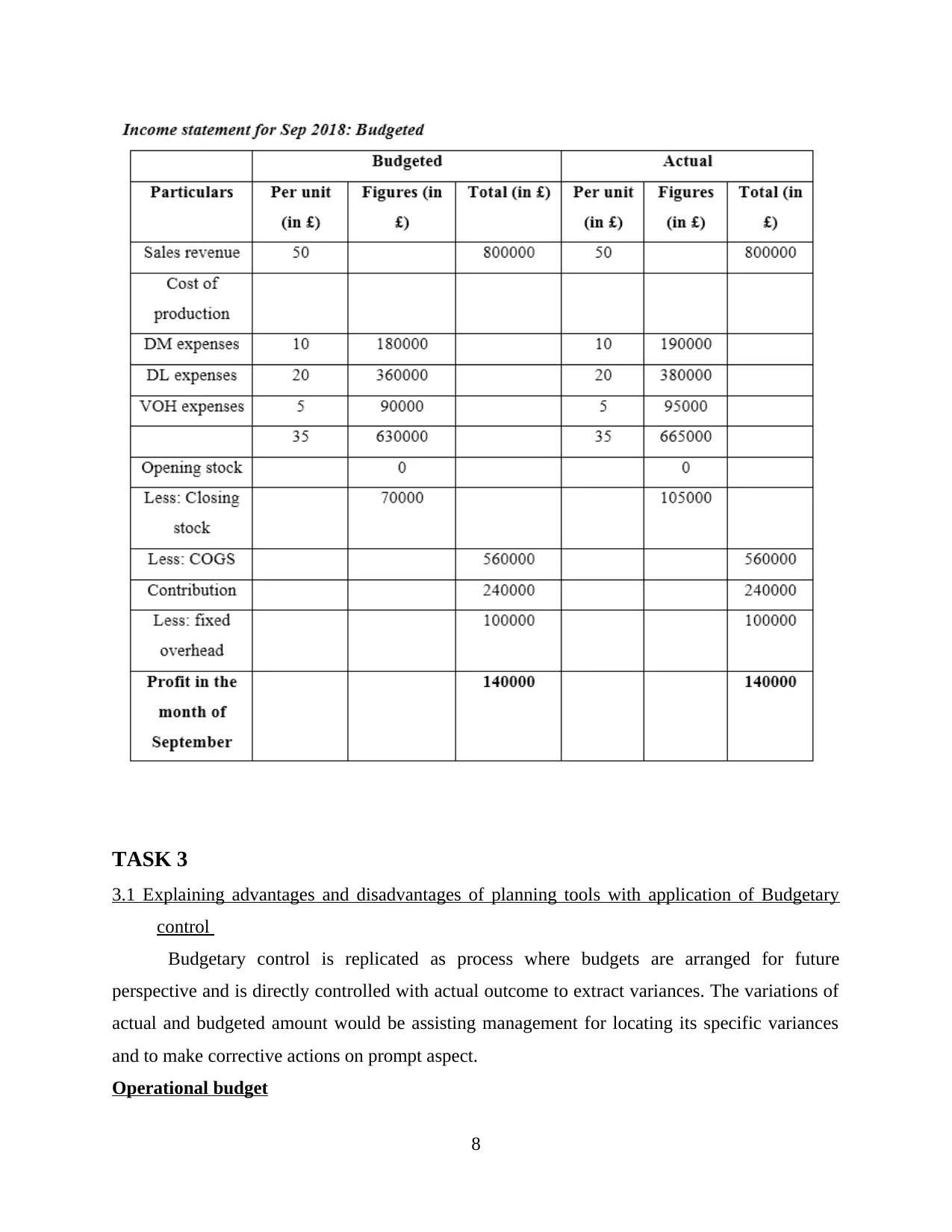

TASK 3

3.1 Explaining advantages and disadvantages of planning tools with application of Budgetary

control

Budgetary control is replicated as process where budgets are arranged for future

perspective and is directly controlled with actual outcome to extract variances. The variations of

actual and budgeted amount would be assisting management for locating its specific variances

and to make corrective actions on prompt aspect.

Operational budget

8

3.1 Explaining advantages and disadvantages of planning tools with application of Budgetary

control

Budgetary control is replicated as process where budgets are arranged for future

perspective and is directly controlled with actual outcome to extract variances. The variations of

actual and budgeted amount would be assisting management for locating its specific variances

and to make corrective actions on prompt aspect.

Operational budget

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

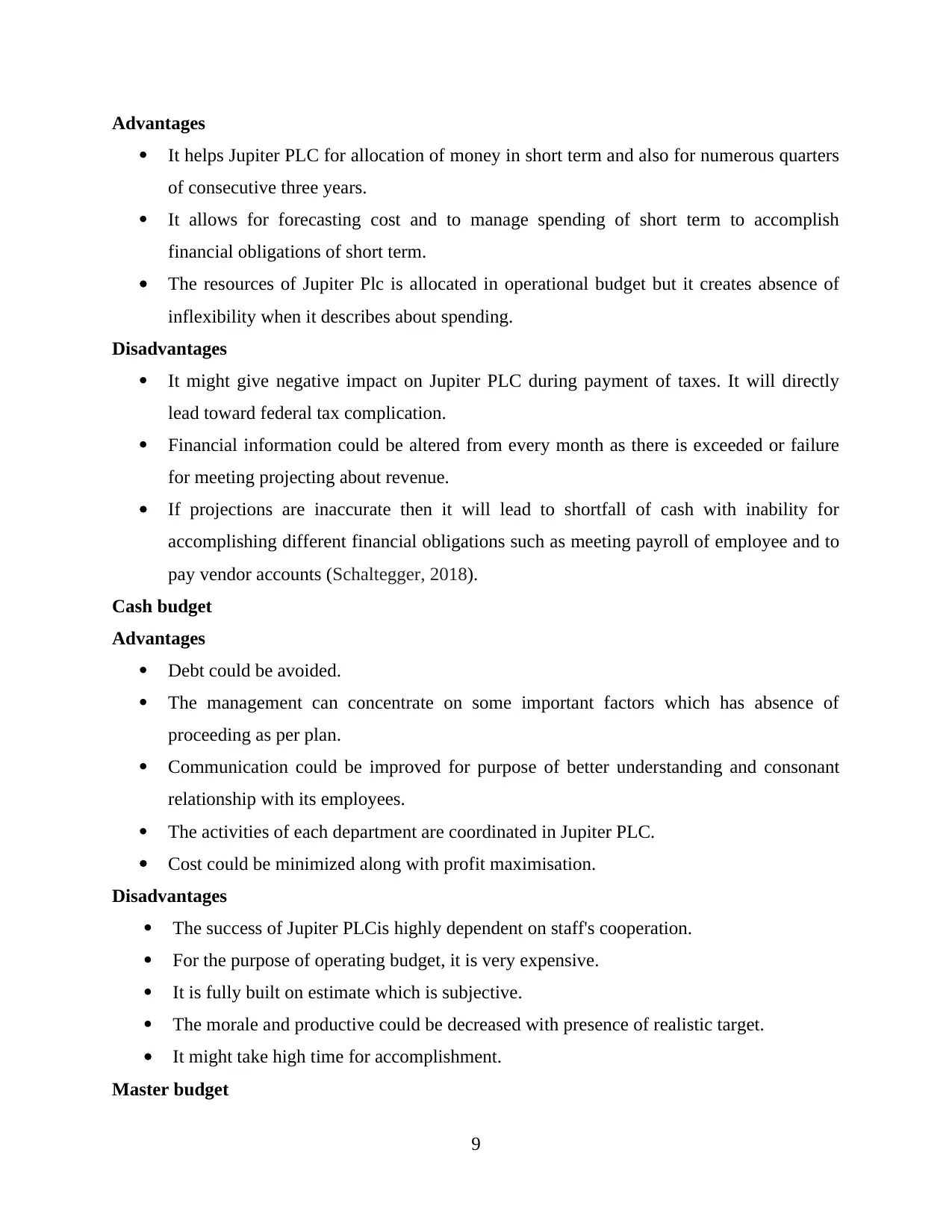

Advantages

It helps Jupiter PLC for allocation of money in short term and also for numerous quarters

of consecutive three years.

It allows for forecasting cost and to manage spending of short term to accomplish

financial obligations of short term.

The resources of Jupiter Plc is allocated in operational budget but it creates absence of

inflexibility when it describes about spending.

Disadvantages

It might give negative impact on Jupiter PLC during payment of taxes. It will directly

lead toward federal tax complication.

Financial information could be altered from every month as there is exceeded or failure

for meeting projecting about revenue.

If projections are inaccurate then it will lead to shortfall of cash with inability for

accomplishing different financial obligations such as meeting payroll of employee and to

pay vendor accounts (Schaltegger, 2018).

Cash budget

Advantages

Debt could be avoided.

The management can concentrate on some important factors which has absence of

proceeding as per plan.

Communication could be improved for purpose of better understanding and consonant

relationship with its employees.

The activities of each department are coordinated in Jupiter PLC.

Cost could be minimized along with profit maximisation.

Disadvantages

The success of Jupiter PLCis highly dependent on staff's cooperation.

For the purpose of operating budget, it is very expensive.

It is fully built on estimate which is subjective.

The morale and productive could be decreased with presence of realistic target.

It might take high time for accomplishment.

Master budget

9

It helps Jupiter PLC for allocation of money in short term and also for numerous quarters

of consecutive three years.

It allows for forecasting cost and to manage spending of short term to accomplish

financial obligations of short term.

The resources of Jupiter Plc is allocated in operational budget but it creates absence of

inflexibility when it describes about spending.

Disadvantages

It might give negative impact on Jupiter PLC during payment of taxes. It will directly

lead toward federal tax complication.

Financial information could be altered from every month as there is exceeded or failure

for meeting projecting about revenue.

If projections are inaccurate then it will lead to shortfall of cash with inability for

accomplishing different financial obligations such as meeting payroll of employee and to

pay vendor accounts (Schaltegger, 2018).

Cash budget

Advantages

Debt could be avoided.

The management can concentrate on some important factors which has absence of

proceeding as per plan.

Communication could be improved for purpose of better understanding and consonant

relationship with its employees.

The activities of each department are coordinated in Jupiter PLC.

Cost could be minimized along with profit maximisation.

Disadvantages

The success of Jupiter PLCis highly dependent on staff's cooperation.

For the purpose of operating budget, it is very expensive.

It is fully built on estimate which is subjective.

The morale and productive could be decreased with presence of realistic target.

It might take high time for accomplishment.

Master budget

9

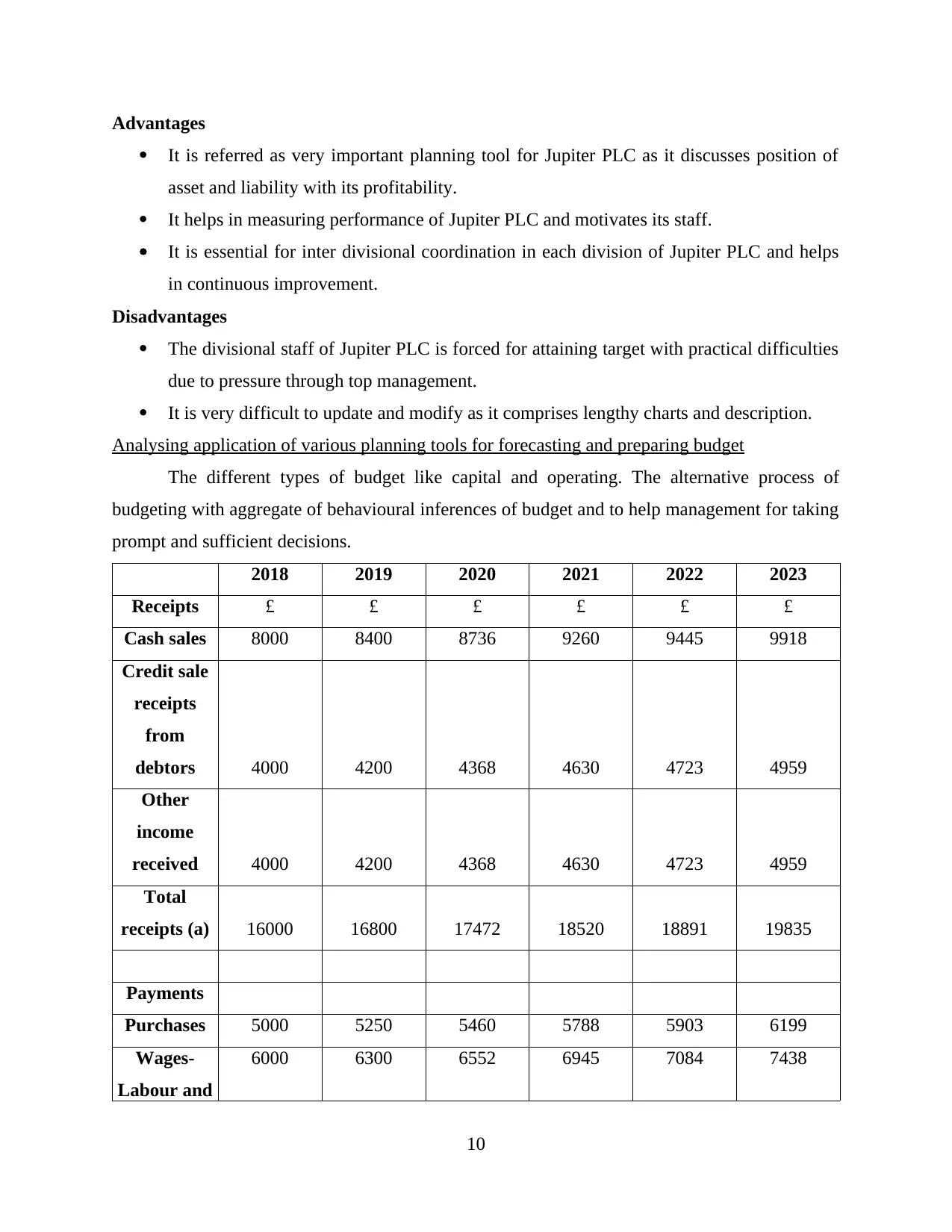

Advantages

It is referred as very important planning tool for Jupiter PLC as it discusses position of

asset and liability with its profitability.

It helps in measuring performance of Jupiter PLC and motivates its staff.

It is essential for inter divisional coordination in each division of Jupiter PLC and helps

in continuous improvement.

Disadvantages

The divisional staff of Jupiter PLC is forced for attaining target with practical difficulties

due to pressure through top management.

It is very difficult to update and modify as it comprises lengthy charts and description.

Analysing application of various planning tools for forecasting and preparing budget

The different types of budget like capital and operating. The alternative process of

budgeting with aggregate of behavioural inferences of budget and to help management for taking

prompt and sufficient decisions.

2018 2019 2020 2021 2022 2023

Receipts £ £ £ £ £ £

Cash sales 8000 8400 8736 9260 9445 9918

Credit sale

receipts

from

debtors 4000 4200 4368 4630 4723 4959

Other

income

received 4000 4200 4368 4630 4723 4959

Total

receipts (a) 16000 16800 17472 18520 18891 19835

Payments

Purchases 5000 5250 5460 5788 5903 6199

Wages-

Labour and

6000 6300 6552 6945 7084 7438

10

It is referred as very important planning tool for Jupiter PLC as it discusses position of

asset and liability with its profitability.

It helps in measuring performance of Jupiter PLC and motivates its staff.

It is essential for inter divisional coordination in each division of Jupiter PLC and helps

in continuous improvement.

Disadvantages

The divisional staff of Jupiter PLC is forced for attaining target with practical difficulties

due to pressure through top management.

It is very difficult to update and modify as it comprises lengthy charts and description.

Analysing application of various planning tools for forecasting and preparing budget

The different types of budget like capital and operating. The alternative process of

budgeting with aggregate of behavioural inferences of budget and to help management for taking

prompt and sufficient decisions.

2018 2019 2020 2021 2022 2023

Receipts £ £ £ £ £ £

Cash sales 8000 8400 8736 9260 9445 9918

Credit sale

receipts

from

debtors 4000 4200 4368 4630 4723 4959

Other

income

received 4000 4200 4368 4630 4723 4959

Total

receipts (a) 16000 16800 17472 18520 18891 19835

Payments

Purchases 5000 5250 5460 5788 5903 6199

Wages-

Labour and

6000 6300 6552 6945 7084 7438

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.