AAF0436 - Management Accounting and Financial Planning for BETA

VerifiedAdded on 2023/06/18

|12

|3240

|286

Report

AI Summary

This report provides an analysis of management accounting and financial planning concepts, specifically focusing on their application to BETA, an IT company based in Dubai. The report discusses standard costing, including its types (ideal, normal, basic, and currently attainable) and limitations (expense, need for revision, and impact on employee psychology). It then explores target costing, highlighting its advantages and differences from standard costing. The role of the contribution technique in decision-making is examined, along with an example illustrating its application for BETA. Finally, the report analyzes how transfer pricing approaches can improve a firm's profitability. The overall aim is to provide insights into how BETA can leverage these management accounting tools to enhance its financial performance and operational efficiency. Desklib provides access to a wealth of similar solved assignments and study resources for students.

Management Accounting and Financial

Planning AAF0436

1

Planning AAF0436

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Discuss the concept and types of standard costing along with its limitations........................3

Discuss about Target costing and how it differs with Standard costing.................................5

Discuss the role of contribution technique in taking decisions and the way it can help BETA.

Analyse the way transfer pricing approaches helps in improving the profitability of firm.

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

2

MAIN BODY...................................................................................................................................3

Discuss the concept and types of standard costing along with its limitations........................3

Discuss about Target costing and how it differs with Standard costing.................................5

Discuss the role of contribution technique in taking decisions and the way it can help BETA.

Analyse the way transfer pricing approaches helps in improving the profitability of firm.

CONCLUSION................................................................................................................................8

REFERENCES................................................................................................................................9

2

INTRODUCTION

Management accounting is defined as a process associated to preparation of reports about

business operation which helps managers to undertake short term as well as long term decisions.

Management accounting also assist business to fulfil their goals while evaluating measuring in

analysing into protecting and communicating information’s in a systematic manner (Banerjee,

2021). Management accounting play essential role through which business can conduct relevant

cost analysis which helps in determining existing expenses and offer suggestion to conduct

future activities in effective manner. Present report is conducted on better which is operating as

an IT company and conducts Dubai based business while dealing in developing apps, supporting

and maintenance of application, software consultancy, IOT services, etc. In this report discussion

has been conducted on the concept and types of standard costing in addition with its limitation,

along with is target costing. Along with this difference with standard costing is also discussed in

this report. At last role of contribution technique and the manner in which transfer pricing

approach helps in making improvement in profitability of firm is also discussed in present report.

3

Management accounting is defined as a process associated to preparation of reports about

business operation which helps managers to undertake short term as well as long term decisions.

Management accounting also assist business to fulfil their goals while evaluating measuring in

analysing into protecting and communicating information’s in a systematic manner (Banerjee,

2021). Management accounting play essential role through which business can conduct relevant

cost analysis which helps in determining existing expenses and offer suggestion to conduct

future activities in effective manner. Present report is conducted on better which is operating as

an IT company and conducts Dubai based business while dealing in developing apps, supporting

and maintenance of application, software consultancy, IOT services, etc. In this report discussion

has been conducted on the concept and types of standard costing in addition with its limitation,

along with is target costing. Along with this difference with standard costing is also discussed in

this report. At last role of contribution technique and the manner in which transfer pricing

approach helps in making improvement in profitability of firm is also discussed in present report.

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

MAIN BODY

Discuss the concept and types of standard costing along with its limitations.

Standard costing is inclusive of setting of predetermined cost estimates as to provide a

basis for the comparison with actual cost. There are mainly three primary categories of standard

cost which is ideal standard, basic standard cost and currently attainable standard cost. It has

been underlined that it is basically a procedure to eliminate the overall amount of expenses

which can take place during the time of production in the estimated cost which is further

compared with actual research with an aim to determine difference between them (Alves, Lichtig

and Rybkowski, 2017). It helps to collect information along with the reason behind the variation.

Main purpose of this is to have estimated budget in a correct manner and determine the

performance of operations. This will help better to control extra cost that can be an occurred with

the help of his better can conduct prior researches and can determine a base of the standard for

next year.

Types of standards

There are basically four types of standards

Ideal or Perfect standard-

It is mainly a measure that can be easily obtained in normal form of condition. In this it is

essential for better to implement appropriate and accurate cost for their material and labour in

addition with maximum possible output that better produce with highest efficiency. It has been

identified that these measures are basically very tight and do not offer any space for kind of

spoilage wastage or inefficiency during work.

Normal standards-

Normal standards are basically expected to be fulfilled in future which can be the time

period of one business cycle. The standard has been duly framed by better on the basis of its

average capacity which can assist in regression as well as boom. Furthermore, it has been

underlined that the cost recognise in this method remains same for the whole cycle and does not

get revised.

Basic standards-

Basic standards are basically developed by organisation for a define time period. It has

been identified that these measures basically stay un- altered. However, they kept revised

4

Discuss the concept and types of standard costing along with its limitations.

Standard costing is inclusive of setting of predetermined cost estimates as to provide a

basis for the comparison with actual cost. There are mainly three primary categories of standard

cost which is ideal standard, basic standard cost and currently attainable standard cost. It has

been underlined that it is basically a procedure to eliminate the overall amount of expenses

which can take place during the time of production in the estimated cost which is further

compared with actual research with an aim to determine difference between them (Alves, Lichtig

and Rybkowski, 2017). It helps to collect information along with the reason behind the variation.

Main purpose of this is to have estimated budget in a correct manner and determine the

performance of operations. This will help better to control extra cost that can be an occurred with

the help of his better can conduct prior researches and can determine a base of the standard for

next year.

Types of standards

There are basically four types of standards

Ideal or Perfect standard-

It is mainly a measure that can be easily obtained in normal form of condition. In this it is

essential for better to implement appropriate and accurate cost for their material and labour in

addition with maximum possible output that better produce with highest efficiency. It has been

identified that these measures are basically very tight and do not offer any space for kind of

spoilage wastage or inefficiency during work.

Normal standards-

Normal standards are basically expected to be fulfilled in future which can be the time

period of one business cycle. The standard has been duly framed by better on the basis of its

average capacity which can assist in regression as well as boom. Furthermore, it has been

underlined that the cost recognise in this method remains same for the whole cycle and does not

get revised.

Basic standards-

Basic standards are basically developed by organisation for a define time period. It has

been identified that these measures basically stay un- altered. However, they kept revised

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

sometime as per the fluctuations occur in price (Bielefeld and Schneider, 2017). Basic standard is

being utilised by better for identification of actual results along with expected results in simple

terms the standard are basically act as measure for other grades.

Currently attainable standards-

These are basically form of standard which are achievable by particular level of efforts.

In addition to this it has been identified that it allows for normal waste, spoilage and non-

productive time. Currently attainable standards are basically for short period of time and is

associated to current condition of work. These standards are being duly followed by better with

an aim to bring efficiency in business operations.

Limitations of standard costing

Expensive tool -

This must need knowledge of expert level in order to set a fixed measures and further

make analysis of them on the basis of results. It has been evaluated that learning of expenses tool

is basically acquired by professional in which better is required to invest lot of money n selection

and recruitment process of such individuals.

Demands regular revision-

Because of fluctuations in frequent level in the market inflation and price level it is

essential to BETA make updating of these measures on continuous basis. However, it is low as

well as complicated process in which better is required to spend comparatively more time.

Effects employee Psychology-

Employees play important role for an organisation. The main limitation of standard costing

is that it affects employee psychology in which organisation management must ensure that level

set a required to be attainable that can be easily fulfilled by employees, as high and unattainable

e measures will lead BETA to face decrease in employee motivation and morale which can affect

their performance.

As per the above discussion it has been identified that standard costing offers a base of

expenses to an organisation according to which it is required to perform its task. However, there

are different constraints of this techniques. However due to the significant advantage of this tool

business organisation can analyse performance and can further control various operation cost that

helps in performing business operations in effective manner.

5

being utilised by better for identification of actual results along with expected results in simple

terms the standard are basically act as measure for other grades.

Currently attainable standards-

These are basically form of standard which are achievable by particular level of efforts.

In addition to this it has been identified that it allows for normal waste, spoilage and non-

productive time. Currently attainable standards are basically for short period of time and is

associated to current condition of work. These standards are being duly followed by better with

an aim to bring efficiency in business operations.

Limitations of standard costing

Expensive tool -

This must need knowledge of expert level in order to set a fixed measures and further

make analysis of them on the basis of results. It has been evaluated that learning of expenses tool

is basically acquired by professional in which better is required to invest lot of money n selection

and recruitment process of such individuals.

Demands regular revision-

Because of fluctuations in frequent level in the market inflation and price level it is

essential to BETA make updating of these measures on continuous basis. However, it is low as

well as complicated process in which better is required to spend comparatively more time.

Effects employee Psychology-

Employees play important role for an organisation. The main limitation of standard costing

is that it affects employee psychology in which organisation management must ensure that level

set a required to be attainable that can be easily fulfilled by employees, as high and unattainable

e measures will lead BETA to face decrease in employee motivation and morale which can affect

their performance.

As per the above discussion it has been identified that standard costing offers a base of

expenses to an organisation according to which it is required to perform its task. However, there

are different constraints of this techniques. However due to the significant advantage of this tool

business organisation can analyse performance and can further control various operation cost that

helps in performing business operations in effective manner.

5

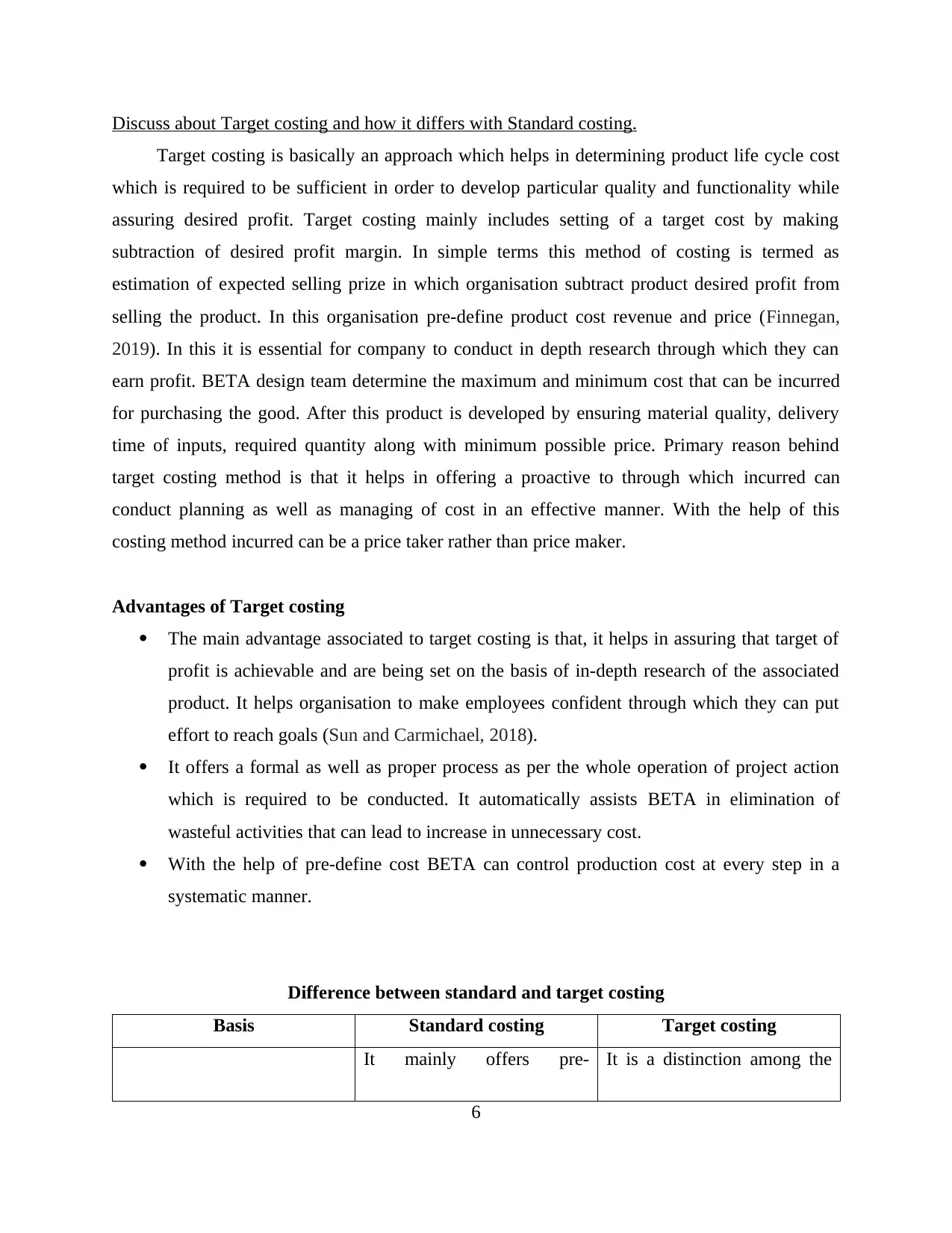

Discuss about Target costing and how it differs with Standard costing.

Target costing is basically an approach which helps in determining product life cycle cost

which is required to be sufficient in order to develop particular quality and functionality while

assuring desired profit. Target costing mainly includes setting of a target cost by making

subtraction of desired profit margin. In simple terms this method of costing is termed as

estimation of expected selling prize in which organisation subtract product desired profit from

selling the product. In this organisation pre-define product cost revenue and price (Finnegan,

2019). In this it is essential for company to conduct in depth research through which they can

earn profit. BETA design team determine the maximum and minimum cost that can be incurred

for purchasing the good. After this product is developed by ensuring material quality, delivery

time of inputs, required quantity along with minimum possible price. Primary reason behind

target costing method is that it helps in offering a proactive to through which incurred can

conduct planning as well as managing of cost in an effective manner. With the help of this

costing method incurred can be a price taker rather than price maker.

Advantages of Target costing

The main advantage associated to target costing is that, it helps in assuring that target of

profit is achievable and are being set on the basis of in-depth research of the associated

product. It helps organisation to make employees confident through which they can put

effort to reach goals (Sun and Carmichael, 2018).

It offers a formal as well as proper process as per the whole operation of project action

which is required to be conducted. It automatically assists BETA in elimination of

wasteful activities that can lead to increase in unnecessary cost.

With the help of pre-define cost BETA can control production cost at every step in a

systematic manner.

Difference between standard and target costing

Basis Standard costing Target costing

It mainly offers pre- It is a distinction among the

6

Target costing is basically an approach which helps in determining product life cycle cost

which is required to be sufficient in order to develop particular quality and functionality while

assuring desired profit. Target costing mainly includes setting of a target cost by making

subtraction of desired profit margin. In simple terms this method of costing is termed as

estimation of expected selling prize in which organisation subtract product desired profit from

selling the product. In this organisation pre-define product cost revenue and price (Finnegan,

2019). In this it is essential for company to conduct in depth research through which they can

earn profit. BETA design team determine the maximum and minimum cost that can be incurred

for purchasing the good. After this product is developed by ensuring material quality, delivery

time of inputs, required quantity along with minimum possible price. Primary reason behind

target costing method is that it helps in offering a proactive to through which incurred can

conduct planning as well as managing of cost in an effective manner. With the help of this

costing method incurred can be a price taker rather than price maker.

Advantages of Target costing

The main advantage associated to target costing is that, it helps in assuring that target of

profit is achievable and are being set on the basis of in-depth research of the associated

product. It helps organisation to make employees confident through which they can put

effort to reach goals (Sun and Carmichael, 2018).

It offers a formal as well as proper process as per the whole operation of project action

which is required to be conducted. It automatically assists BETA in elimination of

wasteful activities that can lead to increase in unnecessary cost.

With the help of pre-define cost BETA can control production cost at every step in a

systematic manner.

Difference between standard and target costing

Basis Standard costing Target costing

It mainly offers pre- It is a distinction among the

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Meaning determined cost based on

assessments and old

encounters.

objective cost and wanted

benefit.

Longevity

The actions can be set for

short just as long time-frame.

They are consistently for

quite a while length,

ordinarily for full life pattern

of item.

Purpose

It targets decreasing the

expense of item in future.

Its will likely contend in

advertise and support itself in

since a long time ago run.

Revision of standards

In this, guidelines are re-

examined yearly or after a

specific time-frame.

It is a persistent interaction

and is performed alongside

the day-by-day tasks.

Grounds of estimation

Evaluations are made by the

authentic data accessible to

them.

Value of cost as well as profit

depends on the exploration

directed by planning group.

However, the previously mentioned two strategies are not quite the same as one another,

yet the two of them centres around same things which are - diminishing the expense of tasks, to

decrease the cost of item, increment their productivity and get proficiency BETA.

Discuss the role of contribution technique in taking decisions and the way it can help BETA.

This is basically a tool to understand the impact of direct and variable cost upon the net

profit that has been earned by company. It further assists in determining the value every product

and expenses upon business (Hansen, Mowen and Heitger, 2021). This evaluates the overhead

associated to different projects and determine their performance by making comparison of the

changes within marginal cost of product. This basically works on a basic formula which is.

Contribution = Revenue - Variable and direct cost

It is an effective system which assist in determining the strength as well as weakness of

cost structured by making differentiation of the expenses into fixed and variable.

Role of contribution analysis

7

assessments and old

encounters.

objective cost and wanted

benefit.

Longevity

The actions can be set for

short just as long time-frame.

They are consistently for

quite a while length,

ordinarily for full life pattern

of item.

Purpose

It targets decreasing the

expense of item in future.

Its will likely contend in

advertise and support itself in

since a long time ago run.

Revision of standards

In this, guidelines are re-

examined yearly or after a

specific time-frame.

It is a persistent interaction

and is performed alongside

the day-by-day tasks.

Grounds of estimation

Evaluations are made by the

authentic data accessible to

them.

Value of cost as well as profit

depends on the exploration

directed by planning group.

However, the previously mentioned two strategies are not quite the same as one another,

yet the two of them centres around same things which are - diminishing the expense of tasks, to

decrease the cost of item, increment their productivity and get proficiency BETA.

Discuss the role of contribution technique in taking decisions and the way it can help BETA.

This is basically a tool to understand the impact of direct and variable cost upon the net

profit that has been earned by company. It further assists in determining the value every product

and expenses upon business (Hansen, Mowen and Heitger, 2021). This evaluates the overhead

associated to different projects and determine their performance by making comparison of the

changes within marginal cost of product. This basically works on a basic formula which is.

Contribution = Revenue - Variable and direct cost

It is an effective system which assist in determining the strength as well as weakness of

cost structured by making differentiation of the expenses into fixed and variable.

Role of contribution analysis

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Ascertaining minimum sale price-

This form of analysis assists in generation of knowledge associated to the lowest charge

at which a product can be duly sold. It has been evaluated that there are different cases in which

consumers ask for discounts and sometime company have largest stock hold by themselves and

wants to clear that even at a lesser price value. In this situation this tool suggests the least price

for this purpose and aid company to not reduced amount below the maximum price. As in this

case organisation fails to recover even its variable expense that can further affect their

profitability.

Clear analysis of profit-

It is a tool which develops a link between profit and volume of sales with the assistance

of graphical representation. With the help of this managers can effectively interpret income that

has been duly earn by company by selling particular units.

Calculates breakeven point-

It is essential for every new organisation to decide its break even before leading towards

generation of profitability (Sellitto and de Almeida, 2019). With the help of contribution analysis

organisation can a certain this point and can have information associated to the lowest number of

units which is required to sell for the purpose to recover all expenses in effective manner.

Decides the margin of safety-

Contribution technique assist in evaluating margin of safety. It has been evaluated that it

offers organisation information associated to the goods quantity which is required to be sold to

start earning profit. For example, if breakeven point is 10000 units than margin of safety would

be unit number 10001.

This procedure is exceptionally helpful to BETA organization as it gives data about

various things to it. This can be seen in example:

For example, A software has been manufactured by BETA for which sale price has been

decided as $100 per unit. Following are the costs incurred on its production.

Fixed cost = $1000

Variable cost = $3000

Revenue on sale of 100 units = 100*100 = $10000

The total expense incurred in production is 3000 + 1000 = $4000.

8

This form of analysis assists in generation of knowledge associated to the lowest charge

at which a product can be duly sold. It has been evaluated that there are different cases in which

consumers ask for discounts and sometime company have largest stock hold by themselves and

wants to clear that even at a lesser price value. In this situation this tool suggests the least price

for this purpose and aid company to not reduced amount below the maximum price. As in this

case organisation fails to recover even its variable expense that can further affect their

profitability.

Clear analysis of profit-

It is a tool which develops a link between profit and volume of sales with the assistance

of graphical representation. With the help of this managers can effectively interpret income that

has been duly earn by company by selling particular units.

Calculates breakeven point-

It is essential for every new organisation to decide its break even before leading towards

generation of profitability (Sellitto and de Almeida, 2019). With the help of contribution analysis

organisation can a certain this point and can have information associated to the lowest number of

units which is required to sell for the purpose to recover all expenses in effective manner.

Decides the margin of safety-

Contribution technique assist in evaluating margin of safety. It has been evaluated that it

offers organisation information associated to the goods quantity which is required to be sold to

start earning profit. For example, if breakeven point is 10000 units than margin of safety would

be unit number 10001.

This procedure is exceptionally helpful to BETA organization as it gives data about

various things to it. This can be seen in example:

For example, A software has been manufactured by BETA for which sale price has been

decided as $100 per unit. Following are the costs incurred on its production.

Fixed cost = $1000

Variable cost = $3000

Revenue on sale of 100 units = 100*100 = $10000

The total expense incurred in production is 3000 + 1000 = $4000.

8

On selling 30 units the firm will acquire revenue of $3000. Subsequent to selling 40

units, its pay would raise to $ 4000. On 41st unit the sum produced would be $4100 and now the

benefit procured by business is 41000-4000 = $100.

As per the above example, one might say that BETA must sell no less than 30

programming, just to recuperate its variable expense. Selling even one unit less would mean a

phase of conclusion, as this is a phase of misfortune at which organizations will in general close

their organizations down. 40 unit is their breakeven point. At this level, they are not procuring

any point, however can recover the entire sum which have been contributed by them for the

creation of programming.

Starting here, even an offer of single item will begin producing benefits to BETA. Its 41st

unit is its Margin of security. After this the entire sum produced by firm is its benefit.

Along these lines, contribution analysis tool is exceptionally helpful for the business for

choosing the base number of units it is needed to sell for recuperating its variable expenses,

generally use and for procuring benefits.

Analyse the way transfer pricing approaches helps in improving the profitability of firm.

It is mainly defined as a price at which one unit of organisation is being duly transferred to

other division either within the form or in other branch of same business. This is basically

depended upon the organisation that whether an organisation move its goods at cost price or after

adding some profit. Primary motive behind this is to charge profit in order to take advantage of

tax deduction.

There are four approaches of transfer pricing which helps in leveraging the income of firm.

Comparable uncontrolled price method-

Comparable uncontrol price method helps in creating relation among uncontrol as well as

control transaction among two unrelated parties with making comparison in their circumstances

as well as price (Kristensen, 2021). With the help of this BETA can determine the price that can

charge for its product which led cause to remain acceptable for the buyers and business through

which additional profit can be earned. It offers strategic price that helps organisation to enhance

price profitability.

Cost Plus method-

9

units, its pay would raise to $ 4000. On 41st unit the sum produced would be $4100 and now the

benefit procured by business is 41000-4000 = $100.

As per the above example, one might say that BETA must sell no less than 30

programming, just to recuperate its variable expense. Selling even one unit less would mean a

phase of conclusion, as this is a phase of misfortune at which organizations will in general close

their organizations down. 40 unit is their breakeven point. At this level, they are not procuring

any point, however can recover the entire sum which have been contributed by them for the

creation of programming.

Starting here, even an offer of single item will begin producing benefits to BETA. Its 41st

unit is its Margin of security. After this the entire sum produced by firm is its benefit.

Along these lines, contribution analysis tool is exceptionally helpful for the business for

choosing the base number of units it is needed to sell for recuperating its variable expenses,

generally use and for procuring benefits.

Analyse the way transfer pricing approaches helps in improving the profitability of firm.

It is mainly defined as a price at which one unit of organisation is being duly transferred to

other division either within the form or in other branch of same business. This is basically

depended upon the organisation that whether an organisation move its goods at cost price or after

adding some profit. Primary motive behind this is to charge profit in order to take advantage of

tax deduction.

There are four approaches of transfer pricing which helps in leveraging the income of firm.

Comparable uncontrolled price method-

Comparable uncontrol price method helps in creating relation among uncontrol as well as

control transaction among two unrelated parties with making comparison in their circumstances

as well as price (Kristensen, 2021). With the help of this BETA can determine the price that can

charge for its product which led cause to remain acceptable for the buyers and business through

which additional profit can be earned. It offers strategic price that helps organisation to enhance

price profitability.

Cost Plus method-

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This form of method is being basically used by parties which deals in semi furnished

goods. In this seller of product charges, a market price along with cost of goods sold from the

purchase. Main aim behind this is to earn enough amount which is direct as well as direct

expenses recovered out of it. With the help of this BETA can estimate the value that can be

charged by them while transferring goods which helps in maximizing.

Transactional net margin method-

Transactional net margin method helps in a certain in the profit via the net profit of

control transaction. This value is further being utilised for making comparison with control

affairs. With the help of this BETA can recognise profit which can be generated from sales

manufacturing and distribution activities. It automatically helps in enhancing overall level of

profitability by significantly making improvement in cost maintenance techniques.

Profit split method-

It is one of the five transfer pricing methods that an organisation can utilise to ensure that

transaction among related company is being carried out at a fair market price. Furthermore, it has

been underlined that it is an effective method that helps in evaluating the manner in which third

party divide profit associated with similar form of transaction (Luca, 2018). Profit split method is

basically applied in intangible assets which is basically difficult to get a path. With the help of

this BETA can understand prices in a more effective manner. It also helps in determining

accurate value of asset. Profit split method will help company to decide the part of tax which is

required to pay associated to particular transaction which automatically helps organisation to

restrict themselves for paying extra taxes. This help organisation to make improvement in its

profitability in effective manner.

CONCLUSION

According to the above-mentioned report it has been concluded that there are different forms

of management accounting techniques which will significantly help organisation to control costs

as well as revenue of organisation. It offers standards and a base which helps in determining

different variations between a budget value and actual results. This will help organisation to

undertake accurate decisions or conduct business operations in effective manner. This report

states that contribution analysis assists in evaluating the extent at which product can cover its

fixed cost and variable and the point that will help organisation to measure profitability. With the

10

goods. In this seller of product charges, a market price along with cost of goods sold from the

purchase. Main aim behind this is to earn enough amount which is direct as well as direct

expenses recovered out of it. With the help of this BETA can estimate the value that can be

charged by them while transferring goods which helps in maximizing.

Transactional net margin method-

Transactional net margin method helps in a certain in the profit via the net profit of

control transaction. This value is further being utilised for making comparison with control

affairs. With the help of this BETA can recognise profit which can be generated from sales

manufacturing and distribution activities. It automatically helps in enhancing overall level of

profitability by significantly making improvement in cost maintenance techniques.

Profit split method-

It is one of the five transfer pricing methods that an organisation can utilise to ensure that

transaction among related company is being carried out at a fair market price. Furthermore, it has

been underlined that it is an effective method that helps in evaluating the manner in which third

party divide profit associated with similar form of transaction (Luca, 2018). Profit split method is

basically applied in intangible assets which is basically difficult to get a path. With the help of

this BETA can understand prices in a more effective manner. It also helps in determining

accurate value of asset. Profit split method will help company to decide the part of tax which is

required to pay associated to particular transaction which automatically helps organisation to

restrict themselves for paying extra taxes. This help organisation to make improvement in its

profitability in effective manner.

CONCLUSION

According to the above-mentioned report it has been concluded that there are different forms

of management accounting techniques which will significantly help organisation to control costs

as well as revenue of organisation. It offers standards and a base which helps in determining

different variations between a budget value and actual results. This will help organisation to

undertake accurate decisions or conduct business operations in effective manner. This report

states that contribution analysis assists in evaluating the extent at which product can cover its

fixed cost and variable and the point that will help organisation to measure profitability. With the

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

help of transfer pricing methods business organisation can improve profitability as well as

performance on simultaneous basis.

REFERENCES

Books and Journals

Alves, T.D.C., Lichtig, W. and Rybkowski, Z.K., 2017. Implementing target value design: Tools

and techniques to manage the process. HERD: Health Environments Research &

Design Journal. 10(3). pp.18-29.

Banerjee, B., 2021. Cost accounting: Theory and practice. PHI Learning Pvt. Ltd..

Bielefeld, B. and Schneider, R., 2017. Costing methods. In Basics Budgeting (pp. 31-50).

Birkhäuser.

Finnegan, M., 2019. Understanding Transfer Pricing and its role in Multinational Corporation

subsidiary revenue and tax reporting: the changing behaviour of MNCs around tax

planning (Doctoral dissertation, Griffith College).

Hansen, D.R., Mowen, M.M. and Heitger, D.L., 2021. Cost management. Cengage Learning.

Kristensen, T.B., 2021. Enabling use of standard variable costing in lean production. Production

Planning & Control. 32(3). pp.169-184.

11

performance on simultaneous basis.

REFERENCES

Books and Journals

Alves, T.D.C., Lichtig, W. and Rybkowski, Z.K., 2017. Implementing target value design: Tools

and techniques to manage the process. HERD: Health Environments Research &

Design Journal. 10(3). pp.18-29.

Banerjee, B., 2021. Cost accounting: Theory and practice. PHI Learning Pvt. Ltd..

Bielefeld, B. and Schneider, R., 2017. Costing methods. In Basics Budgeting (pp. 31-50).

Birkhäuser.

Finnegan, M., 2019. Understanding Transfer Pricing and its role in Multinational Corporation

subsidiary revenue and tax reporting: the changing behaviour of MNCs around tax

planning (Doctoral dissertation, Griffith College).

Hansen, D.R., Mowen, M.M. and Heitger, D.L., 2021. Cost management. Cengage Learning.

Kristensen, T.B., 2021. Enabling use of standard variable costing in lean production. Production

Planning & Control. 32(3). pp.169-184.

11

Luca, O., 2018. Theoretical and Practical Problems of the Transfer Pricing. Cluj Tax FJ, p.61.

Nuhu, N.A., Baird, K. and Appuhamilage, A.B., 2017. The adoption and success of

contemporary management accounting practices in the public sector. Asian Review of

Accounting.

Sellitto, M.A. and de Almeida, F.A., 2019. Analysis of the contribution of waste sorting plants to

the reverse processes of supply chains. Waste Management & Research. 37(2). pp.127-

134.

Sun, Y. and Carmichael, D.G., 2018. Uncertainties related to financial variables within

infrastructure life cycle costing: a literature review. Structure and Infrastructure

Engineering. 14(9). pp.1233-1243.

12

Nuhu, N.A., Baird, K. and Appuhamilage, A.B., 2017. The adoption and success of

contemporary management accounting practices in the public sector. Asian Review of

Accounting.

Sellitto, M.A. and de Almeida, F.A., 2019. Analysis of the contribution of waste sorting plants to

the reverse processes of supply chains. Waste Management & Research. 37(2). pp.127-

134.

Sun, Y. and Carmichael, D.G., 2018. Uncertainties related to financial variables within

infrastructure life cycle costing: a literature review. Structure and Infrastructure

Engineering. 14(9). pp.1233-1243.

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.