Management Accounting: Financial Planning, Cost Analysis, and Problems

VerifiedAdded on 2023/01/13

|19

|3950

|63

Report

AI Summary

This report delves into the core principles of management accounting, emphasizing its practical application within a business context. It examines the use of financial data for informed decision-making, monitoring, and control. The report provides a detailed analysis of income statements derived from both marginal and absorption costing methods, illustrating the treatment of direct and indirect costs. It also addresses various financial challenges such as low credibility, revenue shortfalls, and poor cost estimation. The report highlights the role of management accounting tools and techniques in mitigating these threats and fostering sustainable success, including budget control, cost-volume-profit analysis, and pricing strategies. Through calculations and explanations, the report offers insights into how these tools can be leveraged to overcome financial issues and achieve long-term organizational goals.

B07544

Management

Accounting

Management

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...............................................................................................................1

TASK 2...............................................................................................................................2

L.0.2: Apply a range of management accounting techniques...........................................2

P3 Calculate costs using appropriate techniques of cost analysis to prepare an

income statement using marginal and absorption costs................................................2

M2 Accurately apply a range of management accounting techniques and produce

appropriate financial reporting documents.....................................................................6

L.O.3: Explain the use of planning tools used in management accounting......................7

P4 Explain the Advantages and disadvantages of different types of planning tools

used for budgetary control:............................................................................................7

M3. Analyze the use of different planning tools and their application for forecasting

budgets...........................................................................................................................9

L.O.4: Compare ways in which organizations could use management accounting to

respond to financial problems..........................................................................................10

P5. Compare how organizations are adapting of management accounting systems to

respond to financial problems and sustainable success:............................................10

M4. Analyze how, in responding to financial problems, management accounting can

lead organizations to sustainable success:.................................................................14

CONCLUSION:................................................................................................................15

REFERENCES................................................................................................................16

TASK 2...............................................................................................................................2

L.0.2: Apply a range of management accounting techniques...........................................2

P3 Calculate costs using appropriate techniques of cost analysis to prepare an

income statement using marginal and absorption costs................................................2

M2 Accurately apply a range of management accounting techniques and produce

appropriate financial reporting documents.....................................................................6

L.O.3: Explain the use of planning tools used in management accounting......................7

P4 Explain the Advantages and disadvantages of different types of planning tools

used for budgetary control:............................................................................................7

M3. Analyze the use of different planning tools and their application for forecasting

budgets...........................................................................................................................9

L.O.4: Compare ways in which organizations could use management accounting to

respond to financial problems..........................................................................................10

P5. Compare how organizations are adapting of management accounting systems to

respond to financial problems and sustainable success:............................................10

M4. Analyze how, in responding to financial problems, management accounting can

lead organizations to sustainable success:.................................................................14

CONCLUSION:................................................................................................................15

REFERENCES................................................................................................................16

INTRODUCTION

The objective of this report is introducing the management accounting fundamentals

which can be practice in the wider business environment. This project report will

investigate about uses of management accounting financial data to get planning

decisions and the monitoring and control of finance within organizations.

This project report consists of two types of Income statement; Income statement

through marginal costing and Income statement through absorption costing methods.

How to solve financial problems of the business is discussed in this report. To

understand how marginal and absorption costing methods work, calculations has been

done which shows treatment of direct and indirect costs. There are many financial

problems and issues like low credibility, less revenue, poor cost estimation,

mismatching of data’s in financial statement and high debts taken from the market.

These threats can weak Company’s wealth. To handle such threat there are some tools

and techniques of management accounting systems which help business to overcome

from these financial issues. How these tools solve firms problems are shown in the

project. Additional to solving threats, the concept of sustainable success also discussed

in respect with management accounting systems.

1 | P a g e

The objective of this report is introducing the management accounting fundamentals

which can be practice in the wider business environment. This project report will

investigate about uses of management accounting financial data to get planning

decisions and the monitoring and control of finance within organizations.

This project report consists of two types of Income statement; Income statement

through marginal costing and Income statement through absorption costing methods.

How to solve financial problems of the business is discussed in this report. To

understand how marginal and absorption costing methods work, calculations has been

done which shows treatment of direct and indirect costs. There are many financial

problems and issues like low credibility, less revenue, poor cost estimation,

mismatching of data’s in financial statement and high debts taken from the market.

These threats can weak Company’s wealth. To handle such threat there are some tools

and techniques of management accounting systems which help business to overcome

from these financial issues. How these tools solve firms problems are shown in the

project. Additional to solving threats, the concept of sustainable success also discussed

in respect with management accounting systems.

1 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 2

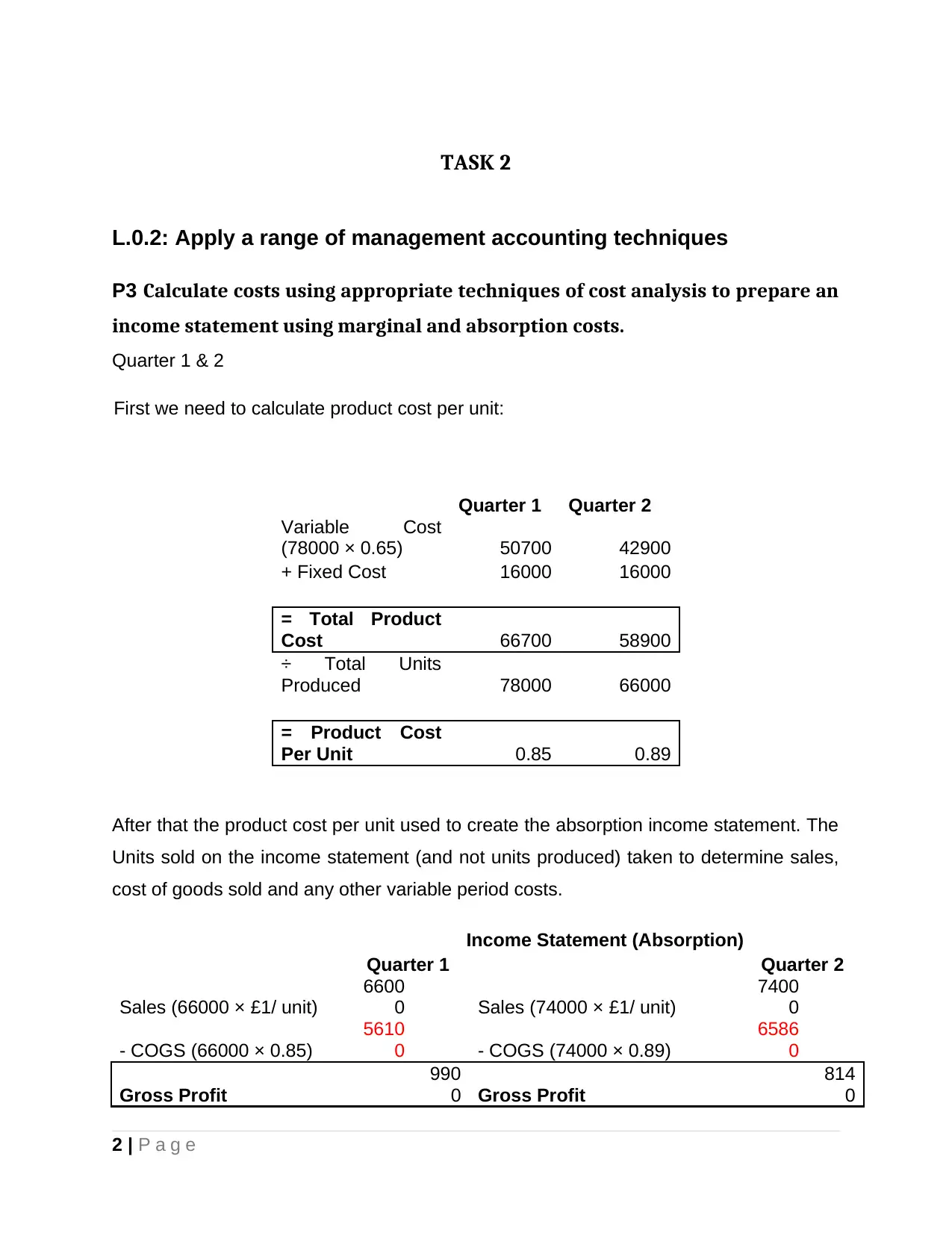

L.0.2: Apply a range of management accounting techniques

P3 Calculate costs using appropriate techniques of cost analysis to prepare an

income statement using marginal and absorption costs.

Quarter 1 & 2

First we need to calculate product cost per unit:

Quarter 1 Quarter 2

Variable Cost

(78000 × 0.65) 50700 42900

+ Fixed Cost 16000 16000

= Total Product

Cost 66700 58900

÷ Total Units

Produced 78000 66000

= Product Cost

Per Unit 0.85 0.89

After that the product cost per unit used to create the absorption income statement. The

Units sold on the income statement (and not units produced) taken to determine sales,

cost of goods sold and any other variable period costs.

Income Statement (Absorption)

Quarter 1 Quarter 2

Sales (66000 × £1/ unit)

6600

0 Sales (74000 × £1/ unit)

7400

0

- COGS (66000 × 0.85)

5610

0 - COGS (74000 × 0.89)

6586

0

Gross Profit

990

0 Gross Profit

814

0

2 | P a g e

L.0.2: Apply a range of management accounting techniques

P3 Calculate costs using appropriate techniques of cost analysis to prepare an

income statement using marginal and absorption costs.

Quarter 1 & 2

First we need to calculate product cost per unit:

Quarter 1 Quarter 2

Variable Cost

(78000 × 0.65) 50700 42900

+ Fixed Cost 16000 16000

= Total Product

Cost 66700 58900

÷ Total Units

Produced 78000 66000

= Product Cost

Per Unit 0.85 0.89

After that the product cost per unit used to create the absorption income statement. The

Units sold on the income statement (and not units produced) taken to determine sales,

cost of goods sold and any other variable period costs.

Income Statement (Absorption)

Quarter 1 Quarter 2

Sales (66000 × £1/ unit)

6600

0 Sales (74000 × £1/ unit)

7400

0

- COGS (66000 × 0.85)

5610

0 - COGS (74000 × 0.89)

6586

0

Gross Profit

990

0 Gross Profit

814

0

2 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

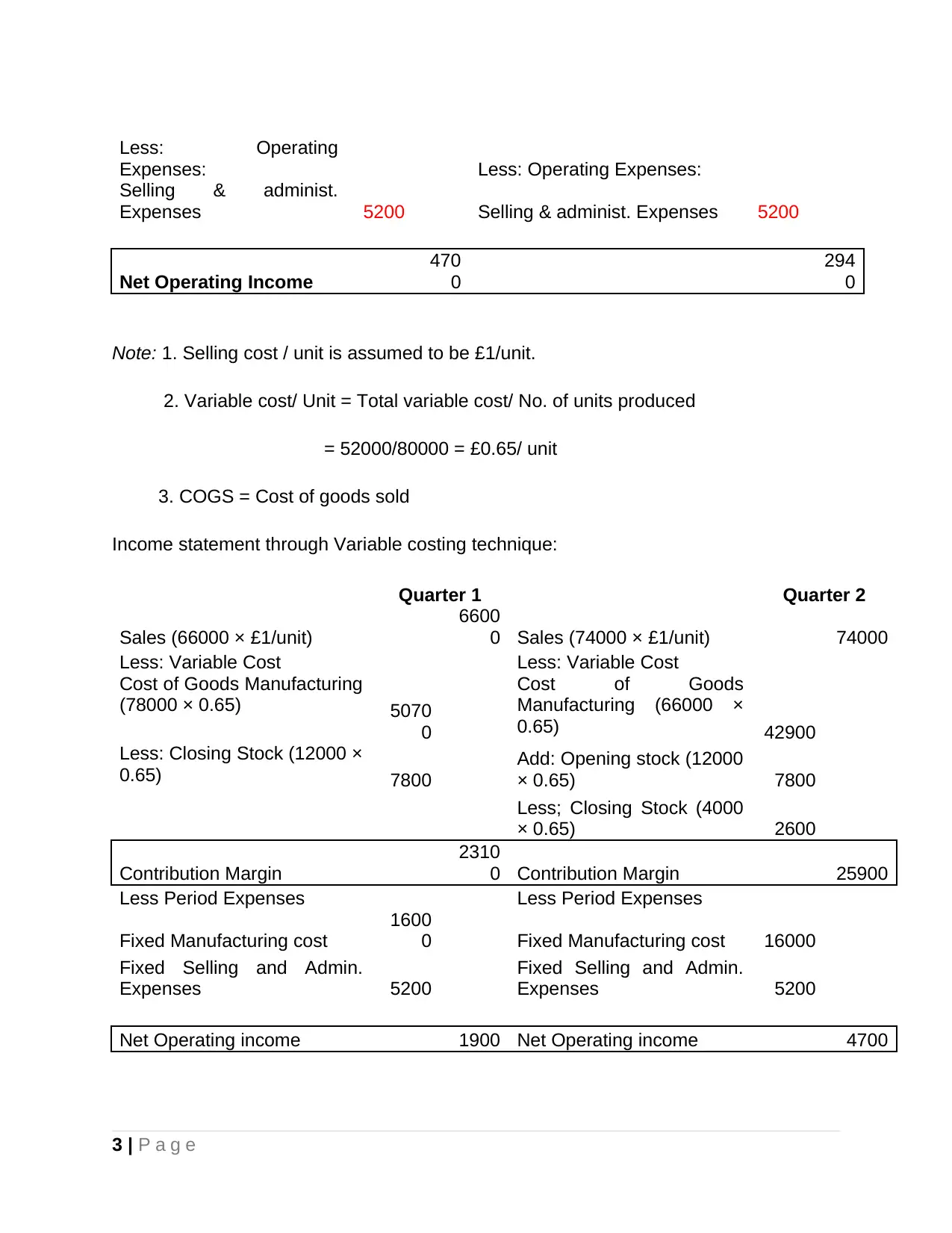

Less: Operating

Expenses: Less: Operating Expenses:

Selling & administ.

Expenses 5200 Selling & administ. Expenses 5200

Net Operating Income

470

0

294

0

Note: 1. Selling cost / unit is assumed to be £1/unit.

2. Variable cost/ Unit = Total variable cost/ No. of units produced

= 52000/80000 = £0.65/ unit

3. COGS = Cost of goods sold

Income statement through Variable costing technique:

Quarter 1 Quarter 2

Sales (66000 × £1/unit)

6600

0 Sales (74000 × £1/unit) 74000

Less: Variable Cost Less: Variable Cost

Cost of Goods Manufacturing

(78000 × 0.65) 5070

0

Cost of Goods

Manufacturing (66000 ×

0.65) 42900

Less: Closing Stock (12000 ×

0.65) 7800

Add: Opening stock (12000

× 0.65) 7800

Less; Closing Stock (4000

× 0.65) 2600

Contribution Margin

2310

0 Contribution Margin 25900

Less Period Expenses Less Period Expenses

Fixed Manufacturing cost

1600

0 Fixed Manufacturing cost 16000

Fixed Selling and Admin.

Expenses 5200

Fixed Selling and Admin.

Expenses 5200

Net Operating income 1900 Net Operating income 4700

3 | P a g e

Expenses: Less: Operating Expenses:

Selling & administ.

Expenses 5200 Selling & administ. Expenses 5200

Net Operating Income

470

0

294

0

Note: 1. Selling cost / unit is assumed to be £1/unit.

2. Variable cost/ Unit = Total variable cost/ No. of units produced

= 52000/80000 = £0.65/ unit

3. COGS = Cost of goods sold

Income statement through Variable costing technique:

Quarter 1 Quarter 2

Sales (66000 × £1/unit)

6600

0 Sales (74000 × £1/unit) 74000

Less: Variable Cost Less: Variable Cost

Cost of Goods Manufacturing

(78000 × 0.65) 5070

0

Cost of Goods

Manufacturing (66000 ×

0.65) 42900

Less: Closing Stock (12000 ×

0.65) 7800

Add: Opening stock (12000

× 0.65) 7800

Less; Closing Stock (4000

× 0.65) 2600

Contribution Margin

2310

0 Contribution Margin 25900

Less Period Expenses Less Period Expenses

Fixed Manufacturing cost

1600

0 Fixed Manufacturing cost 16000

Fixed Selling and Admin.

Expenses 5200

Fixed Selling and Admin.

Expenses 5200

Net Operating income 1900 Net Operating income 4700

3 | P a g e

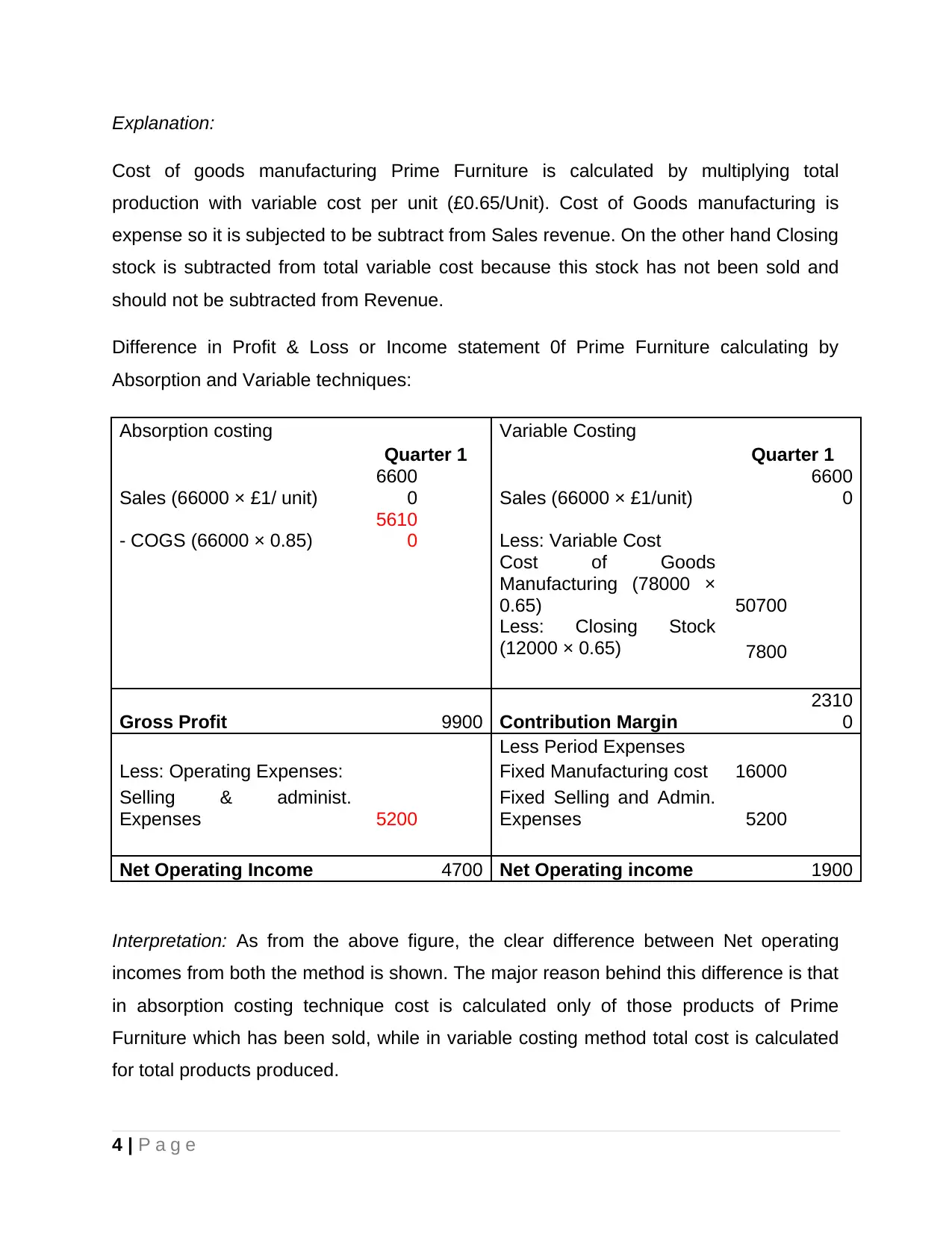

Explanation:

Cost of goods manufacturing Prime Furniture is calculated by multiplying total

production with variable cost per unit (£0.65/Unit). Cost of Goods manufacturing is

expense so it is subjected to be subtract from Sales revenue. On the other hand Closing

stock is subtracted from total variable cost because this stock has not been sold and

should not be subtracted from Revenue.

Difference in Profit & Loss or Income statement 0f Prime Furniture calculating by

Absorption and Variable techniques:

Absorption costing Variable Costing

Quarter 1 Quarter 1

Sales (66000 × £1/ unit)

6600

0 Sales (66000 × £1/unit)

6600

0

- COGS (66000 × 0.85)

5610

0 Less: Variable Cost

Cost of Goods

Manufacturing (78000 ×

0.65) 50700

Less: Closing Stock

(12000 × 0.65) 7800

Gross Profit 9900 Contribution Margin

2310

0

Less Period Expenses

Less: Operating Expenses: Fixed Manufacturing cost 16000

Selling & administ.

Expenses 5200

Fixed Selling and Admin.

Expenses 5200

Net Operating Income 4700 Net Operating income 1900

Interpretation: As from the above figure, the clear difference between Net operating

incomes from both the method is shown. The major reason behind this difference is that

in absorption costing technique cost is calculated only of those products of Prime

Furniture which has been sold, while in variable costing method total cost is calculated

for total products produced.

4 | P a g e

Cost of goods manufacturing Prime Furniture is calculated by multiplying total

production with variable cost per unit (£0.65/Unit). Cost of Goods manufacturing is

expense so it is subjected to be subtract from Sales revenue. On the other hand Closing

stock is subtracted from total variable cost because this stock has not been sold and

should not be subtracted from Revenue.

Difference in Profit & Loss or Income statement 0f Prime Furniture calculating by

Absorption and Variable techniques:

Absorption costing Variable Costing

Quarter 1 Quarter 1

Sales (66000 × £1/ unit)

6600

0 Sales (66000 × £1/unit)

6600

0

- COGS (66000 × 0.85)

5610

0 Less: Variable Cost

Cost of Goods

Manufacturing (78000 ×

0.65) 50700

Less: Closing Stock

(12000 × 0.65) 7800

Gross Profit 9900 Contribution Margin

2310

0

Less Period Expenses

Less: Operating Expenses: Fixed Manufacturing cost 16000

Selling & administ.

Expenses 5200

Fixed Selling and Admin.

Expenses 5200

Net Operating Income 4700 Net Operating income 1900

Interpretation: As from the above figure, the clear difference between Net operating

incomes from both the method is shown. The major reason behind this difference is that

in absorption costing technique cost is calculated only of those products of Prime

Furniture which has been sold, while in variable costing method total cost is calculated

for total products produced.

4 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

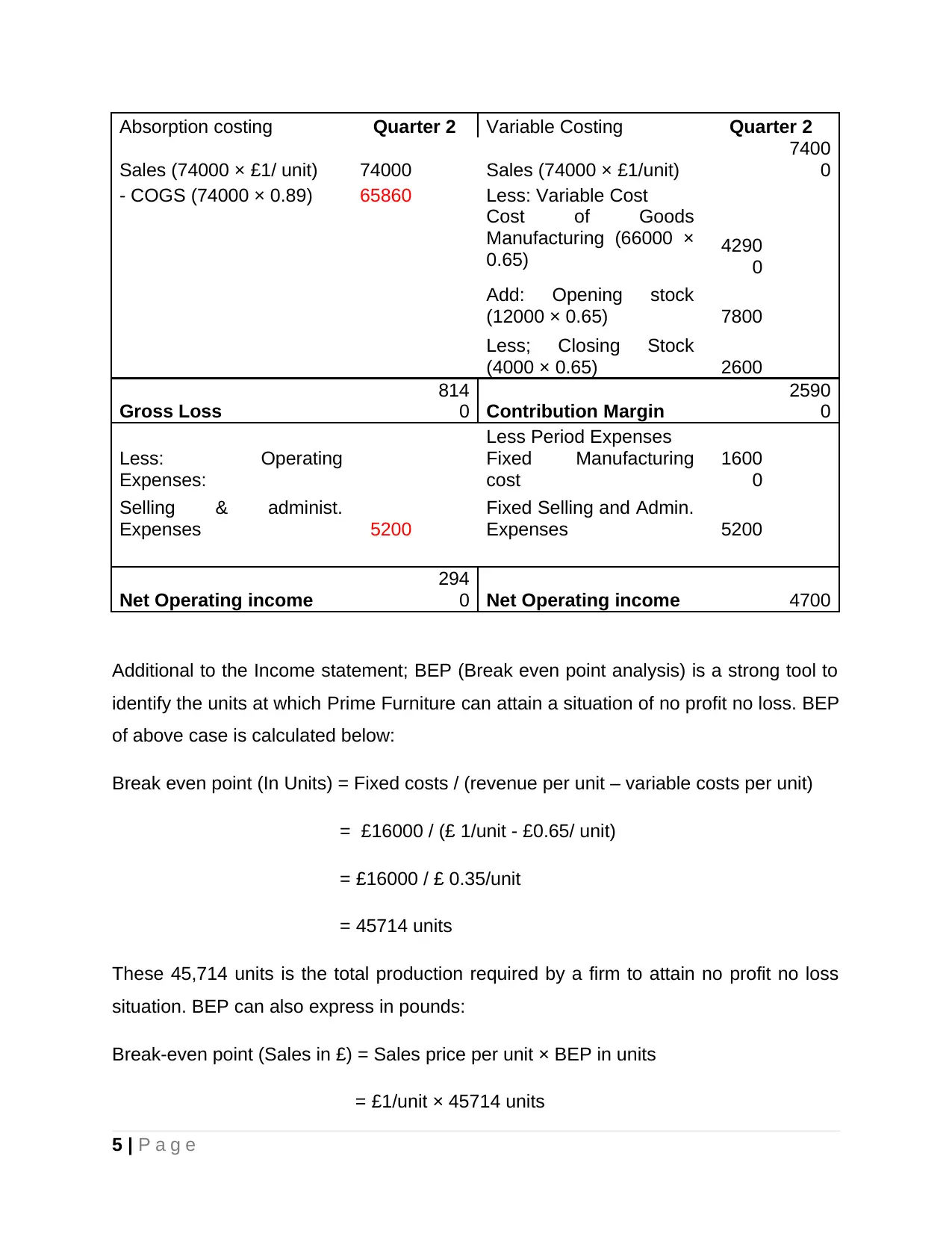

Absorption costing Quarter 2 Variable Costing Quarter 2

Sales (74000 × £1/ unit) 74000 Sales (74000 × £1/unit)

7400

0

- COGS (74000 × 0.89) 65860 Less: Variable Cost

Cost of Goods

Manufacturing (66000 ×

0.65) 4290

0

Add: Opening stock

(12000 × 0.65) 7800

Less; Closing Stock

(4000 × 0.65) 2600

Gross Loss

814

0 Contribution Margin

2590

0

Less Period Expenses

Less: Operating

Expenses:

Fixed Manufacturing

cost

1600

0

Selling & administ.

Expenses 5200

Fixed Selling and Admin.

Expenses 5200

Net Operating income

294

0 Net Operating income 4700

Additional to the Income statement; BEP (Break even point analysis) is a strong tool to

identify the units at which Prime Furniture can attain a situation of no profit no loss. BEP

of above case is calculated below:

Break even point (In Units) = Fixed costs / (revenue per unit – variable costs per unit)

= £16000 / (£ 1/unit - £0.65/ unit)

= £16000 / £ 0.35/unit

= 45714 units

These 45,714 units is the total production required by a firm to attain no profit no loss

situation. BEP can also express in pounds:

Break-even point (Sales in £) = Sales price per unit × BEP in units

= £1/unit × 45714 units

5 | P a g e

Sales (74000 × £1/ unit) 74000 Sales (74000 × £1/unit)

7400

0

- COGS (74000 × 0.89) 65860 Less: Variable Cost

Cost of Goods

Manufacturing (66000 ×

0.65) 4290

0

Add: Opening stock

(12000 × 0.65) 7800

Less; Closing Stock

(4000 × 0.65) 2600

Gross Loss

814

0 Contribution Margin

2590

0

Less Period Expenses

Less: Operating

Expenses:

Fixed Manufacturing

cost

1600

0

Selling & administ.

Expenses 5200

Fixed Selling and Admin.

Expenses 5200

Net Operating income

294

0 Net Operating income 4700

Additional to the Income statement; BEP (Break even point analysis) is a strong tool to

identify the units at which Prime Furniture can attain a situation of no profit no loss. BEP

of above case is calculated below:

Break even point (In Units) = Fixed costs / (revenue per unit – variable costs per unit)

= £16000 / (£ 1/unit - £0.65/ unit)

= £16000 / £ 0.35/unit

= 45714 units

These 45,714 units is the total production required by a firm to attain no profit no loss

situation. BEP can also express in pounds:

Break-even point (Sales in £) = Sales price per unit × BEP in units

= £1/unit × 45714 units

5 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

= £45714

Interpretation: Prime Furniture should generate 45714 pound sales revenue to attain no

profit no loss situation.

6 | P a g e

Interpretation: Prime Furniture should generate 45714 pound sales revenue to attain no

profit no loss situation.

6 | P a g e

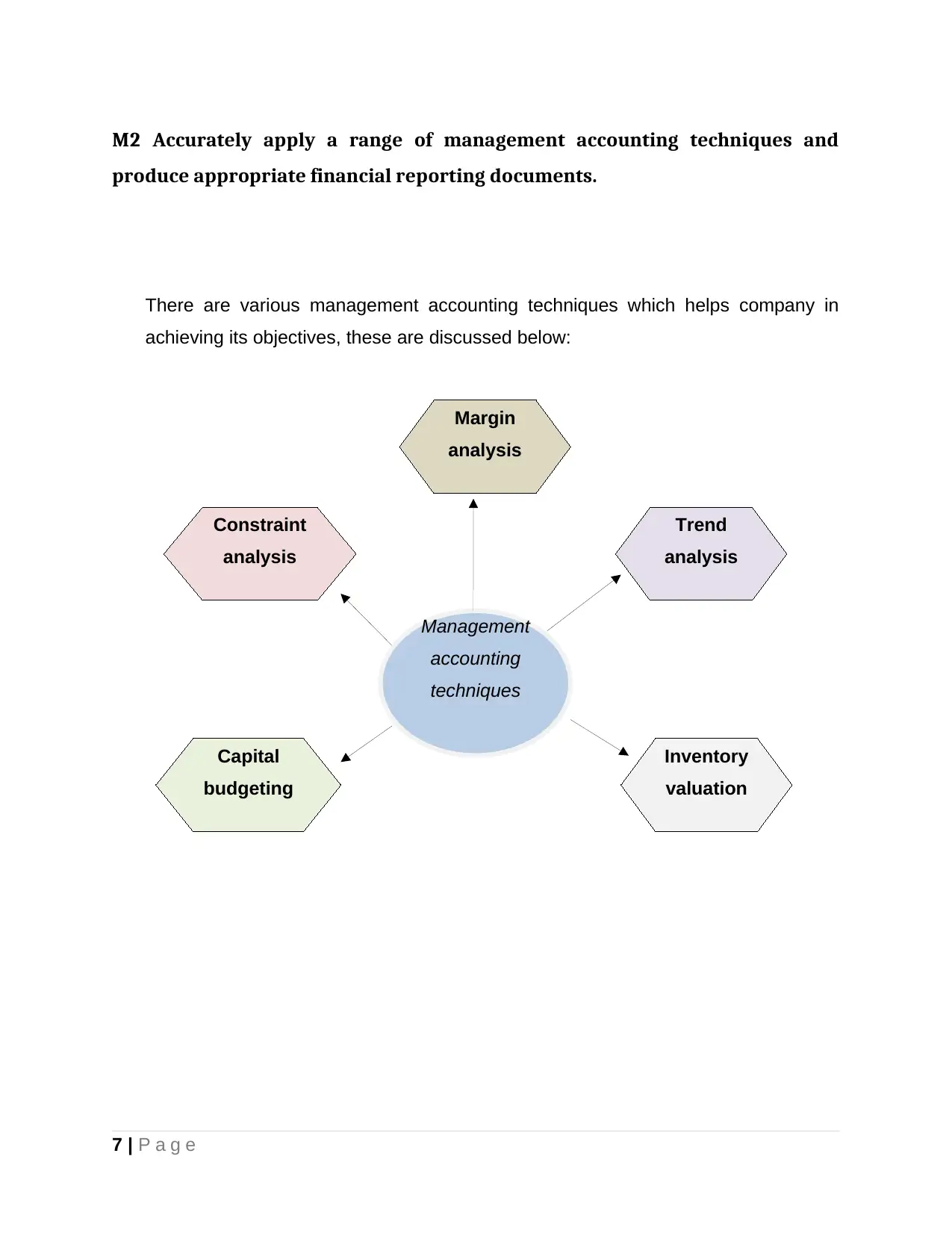

M2 Accurately apply a range of management accounting techniques and

produce appropriate financial reporting documents.

There are various management accounting techniques which helps company in

achieving its objectives, these are discussed below:

7 | P a g e

Management

accounting

techniques

Constraint

analysis

Trend

analysis

Capital

budgeting

Inventory

valuation

Margin

analysis

produce appropriate financial reporting documents.

There are various management accounting techniques which helps company in

achieving its objectives, these are discussed below:

7 | P a g e

Management

accounting

techniques

Constraint

analysis

Trend

analysis

Capital

budgeting

Inventory

valuation

Margin

analysis

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1. Margin Analysis: This technique helps company in avoiding overproduction

situations. It helps company in knowing the unit to be produced to attain no

profit no loss situation through breakeven point analysis.

2. Constraint analysis: This technique helps company in evaluating the hurdles

which stops company in achieving optimum production and increased

revenue. It also states the reason behind this hurdle and provides suitable

solution.

3. Capital budgeting: This is very helpful tool or techniques which helps

company in taking strategic decisions related to capital expenditures. In this

method NPV (net present value) of all investments is calculated to know

which expenditure can give more returns.

4. Inventory valuation: This technique helps operation managers to know what

the actual cost is related with inventory. In this method direct and indirect

cost of production is separated to get the amount which directly impact

inventory production.

5. Trend Analysis: In this technique future estimation about revenue and

expenses is done to know how much fund is required to achieve desired

sales.

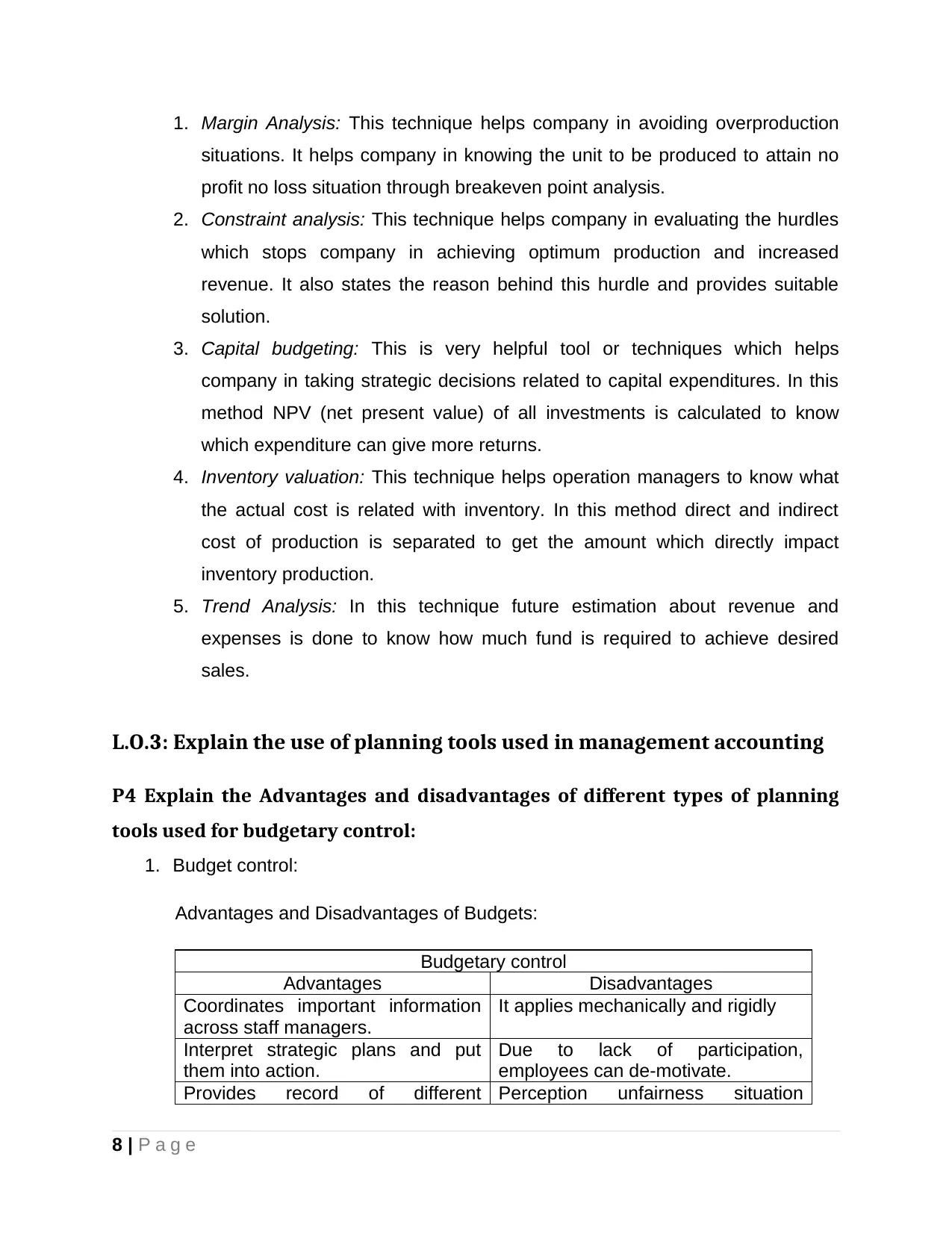

L.O.3: Explain the use of planning tools used in management accounting

P4 Explain the Advantages and disadvantages of different types of planning

tools used for budgetary control:

1. Budget control:

Advantages and Disadvantages of Budgets:

Budgetary control

Advantages Disadvantages

Coordinates important information

across staff managers.

It applies mechanically and rigidly

Interpret strategic plans and put

them into action.

Due to lack of participation,

employees can de-motivate.

Provides record of different Perception unfairness situation

8 | P a g e

situations. It helps company in knowing the unit to be produced to attain no

profit no loss situation through breakeven point analysis.

2. Constraint analysis: This technique helps company in evaluating the hurdles

which stops company in achieving optimum production and increased

revenue. It also states the reason behind this hurdle and provides suitable

solution.

3. Capital budgeting: This is very helpful tool or techniques which helps

company in taking strategic decisions related to capital expenditures. In this

method NPV (net present value) of all investments is calculated to know

which expenditure can give more returns.

4. Inventory valuation: This technique helps operation managers to know what

the actual cost is related with inventory. In this method direct and indirect

cost of production is separated to get the amount which directly impact

inventory production.

5. Trend Analysis: In this technique future estimation about revenue and

expenses is done to know how much fund is required to achieve desired

sales.

L.O.3: Explain the use of planning tools used in management accounting

P4 Explain the Advantages and disadvantages of different types of planning

tools used for budgetary control:

1. Budget control:

Advantages and Disadvantages of Budgets:

Budgetary control

Advantages Disadvantages

Coordinates important information

across staff managers.

It applies mechanically and rigidly

Interpret strategic plans and put

them into action.

Due to lack of participation,

employees can de-motivate.

Provides record of different Perception unfairness situation

8 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

organizational activities. arises.

Improves relations with employees

through sound communications.

Politics and resources competition

arises.

Improves resource reallocations of

Prime Furniture

A rigid structure decreases initiative

and advancement at lower levels,

making it impossible to get cash for

another new project for Prime

Furniture.

Provides corrective action tools.

2. Cost volume profit analysis:

Cost volume profit analysis

Advantages Disadvantages

Simplicity of figuring, utilizes a lot of

standard recipes, numbers can be

changed rapidly to decide changes in

factors.

Accuracy: it accept all expense are

fixed, anyway there are blended cost

that changes with creation.

Planning: the breakeven point assists

supervisors with assessing future

spending and entire creation influence

the targets of the business.

Accept deals stays steady yet interest

for an item can change after some

time.

3. Pricing strategy:

Pricing Strategy

Advantages Disadvantages

Client base valuing takes a look at the

objective whether client is happy to pay

for the item to decide the perfect cost,

this outcomes sets the price to be

charged from customer.

The executives valuing, the item is

estimated at what the organization

perceive not what actually customer

can pay. This creates a gap between

actual price and what price should be.

Cost based pricing accepts and deals

stays steady yet interest for an item

can change after some time by Prime

Furniture.

Cost base pricing confuses Prime

Furniture managers and they fixed the

price more than competitors.

9 | P a g e

Improves relations with employees

through sound communications.

Politics and resources competition

arises.

Improves resource reallocations of

Prime Furniture

A rigid structure decreases initiative

and advancement at lower levels,

making it impossible to get cash for

another new project for Prime

Furniture.

Provides corrective action tools.

2. Cost volume profit analysis:

Cost volume profit analysis

Advantages Disadvantages

Simplicity of figuring, utilizes a lot of

standard recipes, numbers can be

changed rapidly to decide changes in

factors.

Accuracy: it accept all expense are

fixed, anyway there are blended cost

that changes with creation.

Planning: the breakeven point assists

supervisors with assessing future

spending and entire creation influence

the targets of the business.

Accept deals stays steady yet interest

for an item can change after some

time.

3. Pricing strategy:

Pricing Strategy

Advantages Disadvantages

Client base valuing takes a look at the

objective whether client is happy to pay

for the item to decide the perfect cost,

this outcomes sets the price to be

charged from customer.

The executives valuing, the item is

estimated at what the organization

perceive not what actually customer

can pay. This creates a gap between

actual price and what price should be.

Cost based pricing accepts and deals

stays steady yet interest for an item

can change after some time by Prime

Furniture.

Cost base pricing confuses Prime

Furniture managers and they fixed the

price more than competitors.

9 | P a g e

M3. Analyze the use of different planning tools and their application for

forecasting budgets

There are various planning tools used by company:

1) Budget control: The budget is a quantitative as well as fiscal articulation

of approach for a characterized future period.

Application: It applied to forecast arranged incomes and costs for request

to accomplish the organization's objectives. In this manner, it is related to

the administrative and bookkeeping capacity of the business.

2) Cost volume profit analysis: Cost volume benefit examination is utilized

by the executives as arranging instrument to assess income from deals,

cost and benefits, this is finished by utilizing a scientific assessment that

ascertains whole changes to deals volume and cost influence benefit in a

future period.

Application: Cost volume benefit investigation is applied by the executives

to forecast the equal initial investment purpose of an item this is the point

that benefits from pay rises to the expense to deliver an item along these

lines there is no misfortune no benefit now.

3) Pricing strategy: Deciding standard price is difficult task for every

business, because company requires experts who have perfect knowledge

of customer demands, latest trends of the market and can do cost analysis

at different level of operations. The basic steps involved in deciding price

is searching price charged by competitors for similar product.

Application: It is applied to forecast how firm can minimize its cost to meet

competitive price and finally implement this strategy under experts’

supervision. Then the goal is decided, management pick an approach

10 | P a g e

forecasting budgets

There are various planning tools used by company:

1) Budget control: The budget is a quantitative as well as fiscal articulation

of approach for a characterized future period.

Application: It applied to forecast arranged incomes and costs for request

to accomplish the organization's objectives. In this manner, it is related to

the administrative and bookkeeping capacity of the business.

2) Cost volume profit analysis: Cost volume benefit examination is utilized

by the executives as arranging instrument to assess income from deals,

cost and benefits, this is finished by utilizing a scientific assessment that

ascertains whole changes to deals volume and cost influence benefit in a

future period.

Application: Cost volume benefit investigation is applied by the executives

to forecast the equal initial investment purpose of an item this is the point

that benefits from pay rises to the expense to deliver an item along these

lines there is no misfortune no benefit now.

3) Pricing strategy: Deciding standard price is difficult task for every

business, because company requires experts who have perfect knowledge

of customer demands, latest trends of the market and can do cost analysis

at different level of operations. The basic steps involved in deciding price

is searching price charged by competitors for similar product.

Application: It is applied to forecast how firm can minimize its cost to meet

competitive price and finally implement this strategy under experts’

supervision. Then the goal is decided, management pick an approach

10 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.