Management Accounting Report: Ovation System Analysis and Techniques

VerifiedAdded on 2020/12/26

|19

|5519

|181

Report

AI Summary

This report on management accounting provides a comprehensive analysis of various techniques and their applications within the context of Ovation System. It begins with an introduction to management accounting, differentiating it from financial accounting and outlining different types of management accounting systems such as cost accounting, job costing, and inventory management. The report then explores different types of management accounting reports, including budget reports, accounts receivable reports, and inventory reports, highlighting their significance to management decision-making. Task 2 delves into specific accounting methods like absorption and marginal costing, including income statement preparation and cost-profit analysis, such as break-even analysis. Furthermore, the report examines planning tools for budgetary control, evaluates the integration of management accounting systems, and assesses their role in responding to financial problems, comparing Ovation System to a competitor. The report concludes by evaluating planning tools for achieving sustainable organizational success.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

A. Explaining types of management accounting with its essential requirements.......................1

B. Explaining different types of management accounting reports with their significance to

management................................................................................................................................3

C. Benefits of management accounting systems and their application.......................................4

D. Critical evaluation of the integration of management accounting systems and reporting ....5

TASK 2............................................................................................................................................5

A. (1) Explaining Absorption and Marginal Costing..................................................................5

A. (2) & C. Preparing income statement using both absorption and marginal costing

techniques with a financial reporting document on it.................................................................6

B. & D. Calculations on Cost Profit Analysis (break-even analysis) with an interpretation of

business activity data..................................................................................................................8

TASK 3..........................................................................................................................................10

A. Explaining demerits and merits of different planning tools for budgetary control..............10

B. Application of planning tools for analysing, preparing and forecasting budget .................11

C. Comparing adapting management accounting systems for responding to financial problems

...................................................................................................................................................12

D. Analysing management accounting techniques that could lead organisation to sustainable

success.......................................................................................................................................14

E. Evaluating planning tools for solving financial problems to attain sustainable success......14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

A. Explaining types of management accounting with its essential requirements.......................1

B. Explaining different types of management accounting reports with their significance to

management................................................................................................................................3

C. Benefits of management accounting systems and their application.......................................4

D. Critical evaluation of the integration of management accounting systems and reporting ....5

TASK 2............................................................................................................................................5

A. (1) Explaining Absorption and Marginal Costing..................................................................5

A. (2) & C. Preparing income statement using both absorption and marginal costing

techniques with a financial reporting document on it.................................................................6

B. & D. Calculations on Cost Profit Analysis (break-even analysis) with an interpretation of

business activity data..................................................................................................................8

TASK 3..........................................................................................................................................10

A. Explaining demerits and merits of different planning tools for budgetary control..............10

B. Application of planning tools for analysing, preparing and forecasting budget .................11

C. Comparing adapting management accounting systems for responding to financial problems

...................................................................................................................................................12

D. Analysing management accounting techniques that could lead organisation to sustainable

success.......................................................................................................................................14

E. Evaluating planning tools for solving financial problems to attain sustainable success......14

CONCLUSION..............................................................................................................................15

REFERENCES..............................................................................................................................16

INTRODUCTION

Management accounting is employed through senior management of organization for

extracting critical data of business on the basis of financial position through which daily

decisions related to operations are made. Present report will discuss all concepts related to

management accounting with reference to Ovation System. There will be appropriate

understanding on management accounting system with its various types. It will be applying

different range of management accounting techniques such as absorption and marginal costing

with its profit and loss statement. It will reflect calculation of break-even point and margin of

safety on its similar context. This report will also represent planning tools which are applicable

in management accounting with their merits and limitations. Further, it will articulate proper

comparison in between Ovation System and Compound Security System (major competitor) with

application of management accounting to respond on its financial problems. In the same series, it

will evaluate planning tools for solving financial problems and lead to attain organizational

success.

TASK 1

A. Explaining types of management accounting with its essential requirements

Accounting is of two types which are management and financial. Management

accounting is referred as the process of preparation of accounts and reports which give

appropriate and timely information related to finance and statistics to its managers for taking

decision from short and long term perspective. There is a huge requirement of managers of

department for forming various reports and to communicate information to team of senior

management. This data is not shared with lenders, other external parties and shareholders.

Financial accounting is replicated as a process of summarising, reporting and recording each

transaction of organization for giving accurate picture of its fiscal performance (Nitzl, 2018).

There are various types of management accounting systems such as:

Cost accounting system: It is a system of accounting which is used through

manufacturers for tracing activities of production with application of perpetual inventory system.

In simple words, accounting system is framed for manufacturers who track inventory flow on

continuous basis at different stages of production. It tracks raw materials on this stage and

converts the same into finished goods. These materials are used in production and on immediate

1

Management accounting is employed through senior management of organization for

extracting critical data of business on the basis of financial position through which daily

decisions related to operations are made. Present report will discuss all concepts related to

management accounting with reference to Ovation System. There will be appropriate

understanding on management accounting system with its various types. It will be applying

different range of management accounting techniques such as absorption and marginal costing

with its profit and loss statement. It will reflect calculation of break-even point and margin of

safety on its similar context. This report will also represent planning tools which are applicable

in management accounting with their merits and limitations. Further, it will articulate proper

comparison in between Ovation System and Compound Security System (major competitor) with

application of management accounting to respond on its financial problems. In the same series, it

will evaluate planning tools for solving financial problems and lead to attain organizational

success.

TASK 1

A. Explaining types of management accounting with its essential requirements

Accounting is of two types which are management and financial. Management

accounting is referred as the process of preparation of accounts and reports which give

appropriate and timely information related to finance and statistics to its managers for taking

decision from short and long term perspective. There is a huge requirement of managers of

department for forming various reports and to communicate information to team of senior

management. This data is not shared with lenders, other external parties and shareholders.

Financial accounting is replicated as a process of summarising, reporting and recording each

transaction of organization for giving accurate picture of its fiscal performance (Nitzl, 2018).

There are various types of management accounting systems such as:

Cost accounting system: It is a system of accounting which is used through

manufacturers for tracing activities of production with application of perpetual inventory system.

In simple words, accounting system is framed for manufacturers who track inventory flow on

continuous basis at different stages of production. It tracks raw materials on this stage and

converts the same into finished goods. These materials are used in production and on immediate

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

aspect, these are recorded and credited through its accounts and debited from goods in process

account. It comprises of actual, normal and standard costing. Actual costing: It uses rate of actual and direct cost with its application for identifying the

cost of specific items. The hours of manufacturing time are analysed by managers along

with requirement of calculating actual cost of producing a particular product. Normal costing: It uses annual overhead rate which is predetermined for allocating

manufacturing overhead to its particular products. In simple form, its rate is directly

based on the expected overhead costs for whole accounting year and its volume of

production. Example could be rent or mortgage and depreciation on machine used for

producing products.

Standard costing: This is estimated and predetermined cost for performing operation to

manufacture any good on the basis of normal condition. It is applicable as the target cost

and developed through analysis of historical data from motion or time study. Its example

could be cost of direct material, labour or manufacturing overhead (Saeidi and Othman,

2017).

Job Costing system: It engages the process of accumulating information related to cost

associated along with proper production or service job. There is a huge requirement of

information for submitting information of reimbursed cost to specific customer. The application

of information is used for identifying the accuracy for estimating system of organization. It has

gained capability for quoting price which allows for obtaining reasonable margin. This particular

information is used for allocating the cost of inventory to its goods which were manufactured. In

this system, it has to accumulate information related to direct material, labour and overhead. For

instance, it is appropriate for determining constructing cost of custom machine, building

construction and to design software program.

Inventory management system: It tracks goods via whole supply chain or business

proportion which is operated in it. This system covers each item of production to warehouse to

shipping, retail and each movement of stock and parts in it. There are various systems of

managing inventory such as periodic inventory, JIT, LIFO and FIFO. Periodic inventory: It is the system which updates on periodic aspect. It does not make

any effort for proper record of either cost of sales or of inventory.

2

account. It comprises of actual, normal and standard costing. Actual costing: It uses rate of actual and direct cost with its application for identifying the

cost of specific items. The hours of manufacturing time are analysed by managers along

with requirement of calculating actual cost of producing a particular product. Normal costing: It uses annual overhead rate which is predetermined for allocating

manufacturing overhead to its particular products. In simple form, its rate is directly

based on the expected overhead costs for whole accounting year and its volume of

production. Example could be rent or mortgage and depreciation on machine used for

producing products.

Standard costing: This is estimated and predetermined cost for performing operation to

manufacture any good on the basis of normal condition. It is applicable as the target cost

and developed through analysis of historical data from motion or time study. Its example

could be cost of direct material, labour or manufacturing overhead (Saeidi and Othman,

2017).

Job Costing system: It engages the process of accumulating information related to cost

associated along with proper production or service job. There is a huge requirement of

information for submitting information of reimbursed cost to specific customer. The application

of information is used for identifying the accuracy for estimating system of organization. It has

gained capability for quoting price which allows for obtaining reasonable margin. This particular

information is used for allocating the cost of inventory to its goods which were manufactured. In

this system, it has to accumulate information related to direct material, labour and overhead. For

instance, it is appropriate for determining constructing cost of custom machine, building

construction and to design software program.

Inventory management system: It tracks goods via whole supply chain or business

proportion which is operated in it. This system covers each item of production to warehouse to

shipping, retail and each movement of stock and parts in it. There are various systems of

managing inventory such as periodic inventory, JIT, LIFO and FIFO. Periodic inventory: It is the system which updates on periodic aspect. It does not make

any effort for proper record of either cost of sales or of inventory.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

JIT (Just in Time): It is a common technique for leaning methodology for designing to

raise efficiency and to cut cost. In the similar series, waste has been decreased through

receiving goods with its requirement.

B. Explaining different types of management accounting reports with their significance to

management

Managerial accounting reports gives information for trimming cost and rewarding

employees on the basis of high performance . It signifies the best financial outcomes of business

which are undertaken and time sensitivity of information related to finance. There are various

types of management accounting reports which are used by Ovation System such as:

Budget report: It is an internal report which is applicable through management for

comparing the budgeted projections which are estimated along with obtained number of actual

performance in specific duration. These are inaccurate and differ in huge aspect from

organization's actual performance. Ovation System could prepare this report on quarterly,

monthly and annual basis. It will give detailed overview about performance from its previous

years and fluctuations on this aspect. These are invaluable method for Ovation System for

monitoring business's financial health. It helps in making or buying decisions and with providing

a better understanding on performance variances (Budget Report, 2018.).

Accounts Receivable report: It is a critical tool for proper management of cash flow

with extension of credit to its customers. The problems related to collection process of Ovation

System could be extracted by its managers. If these accounts receivable reports are analysed on

periodic aspect then it would keep collection department from overviewing old debts (Bui and

De Villiers, 2017).

Inventory reports: This report gives information for helping the business to improve

decision making skills. Information related to current inventory and owners of direct businesses

on the basis of sensible purchase are outlined. It consists of items such as hourly labour costs,

inventory waste and cost of per unit overhead. The different assembly lines are compared within

business for highlighting improvement areas for giving bonus to departments that are performing

well. In nutshell, it optimises the level of inventory and ensures about appropriate tracking.

There are different methods for extracting inventory control report in Ovation System (Reports

of Inventory Management, 2018).

3

raise efficiency and to cut cost. In the similar series, waste has been decreased through

receiving goods with its requirement.

B. Explaining different types of management accounting reports with their significance to

management

Managerial accounting reports gives information for trimming cost and rewarding

employees on the basis of high performance . It signifies the best financial outcomes of business

which are undertaken and time sensitivity of information related to finance. There are various

types of management accounting reports which are used by Ovation System such as:

Budget report: It is an internal report which is applicable through management for

comparing the budgeted projections which are estimated along with obtained number of actual

performance in specific duration. These are inaccurate and differ in huge aspect from

organization's actual performance. Ovation System could prepare this report on quarterly,

monthly and annual basis. It will give detailed overview about performance from its previous

years and fluctuations on this aspect. These are invaluable method for Ovation System for

monitoring business's financial health. It helps in making or buying decisions and with providing

a better understanding on performance variances (Budget Report, 2018.).

Accounts Receivable report: It is a critical tool for proper management of cash flow

with extension of credit to its customers. The problems related to collection process of Ovation

System could be extracted by its managers. If these accounts receivable reports are analysed on

periodic aspect then it would keep collection department from overviewing old debts (Bui and

De Villiers, 2017).

Inventory reports: This report gives information for helping the business to improve

decision making skills. Information related to current inventory and owners of direct businesses

on the basis of sensible purchase are outlined. It consists of items such as hourly labour costs,

inventory waste and cost of per unit overhead. The different assembly lines are compared within

business for highlighting improvement areas for giving bonus to departments that are performing

well. In nutshell, it optimises the level of inventory and ensures about appropriate tracking.

There are different methods for extracting inventory control report in Ovation System (Reports

of Inventory Management, 2018).

3

C. Benefits of management accounting systems and their application

Cost accounting system: This system helps in clustering expenses and revenues through

cost object by distribution channel, product line and product for identifying profitable or need of

support. It extracts exact cause of issue and suggests appropriate solution to management. In the

similar aspect, it examines cost structure of possible acquisition with its appropriate justification.

The occurrence of actual cost could be compared with standard or budgeted cost for observing

business contribution to spend as compared to expected. The capability of business for

supporting increased level of sales by exploring amount which is exceeding capacity. It also

includes charges of direct labour to inventory along with allocation of factory overhead to stock.

It gives help for process of decision making and accuracy of financial accounts had been checked

in Ovation System.

Job costing system: The cost might be ascertained with completion of job at any stage

which provides scope for controlling costs by performing appropriate steps in Ovation System.

Each job helps in earning profit and individually it is known as Job costing. The management

could properly estimate each cost of job by considering previous records in it. Its actual cost of

present job could be compared with previous job execution. It might predetermine overhead

recovery rate on basis of budget. There is absence of under and over recovery of its overheads. It

helps in implementing budgetary control system with appropriate estimation with context of job

costing. The suitability of job costing is along with cost and contracts and it facilitates pricing of

each particular job (Hope, Thomas and Vyas, 2017).

Inventory management system: This system helps in achieving productivity and

efficiency in operations. With this context, adequate supply of specific product to accomplish its

demand which is very important to increase sales and customer services. If inventory

management system is computerized or manual then it would determine trend and to prepared for

requirements of customer. It streamlines operations as in facilities of manufacturing must

maintain appropriate inventory of supply which is mandatory for manufacturing products of

Ovation System. It is major advantage of an effective system of inventory management. It helps

for identifying adjustments of lead time and ensures about stock belongs to sale. In the similar

aspect, it decreases liabilities and loss created through overstock. It keeps proper track on supply

and demand and decline in sales to determine one time occurrence for preventing over orders of

particular products.

4

Cost accounting system: This system helps in clustering expenses and revenues through

cost object by distribution channel, product line and product for identifying profitable or need of

support. It extracts exact cause of issue and suggests appropriate solution to management. In the

similar aspect, it examines cost structure of possible acquisition with its appropriate justification.

The occurrence of actual cost could be compared with standard or budgeted cost for observing

business contribution to spend as compared to expected. The capability of business for

supporting increased level of sales by exploring amount which is exceeding capacity. It also

includes charges of direct labour to inventory along with allocation of factory overhead to stock.

It gives help for process of decision making and accuracy of financial accounts had been checked

in Ovation System.

Job costing system: The cost might be ascertained with completion of job at any stage

which provides scope for controlling costs by performing appropriate steps in Ovation System.

Each job helps in earning profit and individually it is known as Job costing. The management

could properly estimate each cost of job by considering previous records in it. Its actual cost of

present job could be compared with previous job execution. It might predetermine overhead

recovery rate on basis of budget. There is absence of under and over recovery of its overheads. It

helps in implementing budgetary control system with appropriate estimation with context of job

costing. The suitability of job costing is along with cost and contracts and it facilitates pricing of

each particular job (Hope, Thomas and Vyas, 2017).

Inventory management system: This system helps in achieving productivity and

efficiency in operations. With this context, adequate supply of specific product to accomplish its

demand which is very important to increase sales and customer services. If inventory

management system is computerized or manual then it would determine trend and to prepared for

requirements of customer. It streamlines operations as in facilities of manufacturing must

maintain appropriate inventory of supply which is mandatory for manufacturing products of

Ovation System. It is major advantage of an effective system of inventory management. It helps

for identifying adjustments of lead time and ensures about stock belongs to sale. In the similar

aspect, it decreases liabilities and loss created through overstock. It keeps proper track on supply

and demand and decline in sales to determine one time occurrence for preventing over orders of

particular products.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

D. Critical evaluation of the integration of management accounting systems and reporting

It is a system of software application which helps in standardizing procedures for tracing

each transaction and appropriate dissemination of information related to its financials. The

reporting activities are interlinked to various functional areas of business like point of sales, back

office, stores and front office. The whole information is streamlined with its output and input of

functions of financial reporting and management accounting. However, integration management

accounting system is adopted then it would directly enhances financial system along with

accuracy, speed, efficiency through proper process of financial information. It helps in enabling

and relay on real time information with context of business transactions.

Integrated management accounting serves as shop of one stop on basis of its information

which consists of managerial, cash flow and financial accounting. It has huge requirement of

maintaining separate procedure of accounting for preparing reports of financial, cash flow and

management. It has been critiqued that, data which is processed on automated aspect and

bookkeeping and accounts are simplified with application of this system. It substitutes

complicated and tedious activities of reconciliation and performs with non-integrated

management accounting system. This adaption is mandatory not a choice due to increment in

complexities of world of modern business with application of efficient system to maximise its

performance. However, Ovation System must ensure to choose affordable, user friendly and to

update flexible system to ignore complications in this implementation (Diouf and Boiral, 2017).

TASK 2

A. (1) Explaining Absorption and Marginal Costing

Absorption costing:

It is managerial costing method of allocating cost by including both fixed cost and

variable expenses in production of inventory. In absorption costing method all the expenses

incurred that is material cost, and indirect cost like overhead cost are considered while evaluating

the final price of a product (Noreen, Brewer and Garrison, 2014). It helps to recover all expenses

of production from the selling cost of that product. It is widely used technique of ascertaining

cost of a product. Absorption method of costing is also referred as full costing as it present more

comprehensive and accurate expenses incurred on the production of inventory.

Marginal Costing:

5

It is a system of software application which helps in standardizing procedures for tracing

each transaction and appropriate dissemination of information related to its financials. The

reporting activities are interlinked to various functional areas of business like point of sales, back

office, stores and front office. The whole information is streamlined with its output and input of

functions of financial reporting and management accounting. However, integration management

accounting system is adopted then it would directly enhances financial system along with

accuracy, speed, efficiency through proper process of financial information. It helps in enabling

and relay on real time information with context of business transactions.

Integrated management accounting serves as shop of one stop on basis of its information

which consists of managerial, cash flow and financial accounting. It has huge requirement of

maintaining separate procedure of accounting for preparing reports of financial, cash flow and

management. It has been critiqued that, data which is processed on automated aspect and

bookkeeping and accounts are simplified with application of this system. It substitutes

complicated and tedious activities of reconciliation and performs with non-integrated

management accounting system. This adaption is mandatory not a choice due to increment in

complexities of world of modern business with application of efficient system to maximise its

performance. However, Ovation System must ensure to choose affordable, user friendly and to

update flexible system to ignore complications in this implementation (Diouf and Boiral, 2017).

TASK 2

A. (1) Explaining Absorption and Marginal Costing

Absorption costing:

It is managerial costing method of allocating cost by including both fixed cost and

variable expenses in production of inventory. In absorption costing method all the expenses

incurred that is material cost, and indirect cost like overhead cost are considered while evaluating

the final price of a product (Noreen, Brewer and Garrison, 2014). It helps to recover all expenses

of production from the selling cost of that product. It is widely used technique of ascertaining

cost of a product. Absorption method of costing is also referred as full costing as it present more

comprehensive and accurate expenses incurred on the production of inventory.

Marginal Costing:

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It is the method of costing technique where the variable expense is considered to

determine the price of the inventory and fixed cost will consider as completely written off

against profit in that period (Quinn, Elafi and Mulgrew, 2017). Only variable cost are charged to

operations processes. It is not considered as a system of costing but taken as a technique which

concerned as change in the cost and profit from production with the change in variable expenses

in production of that product. It is not considered as a suitable technique to ascertain cost of

inventory as it does not determine the fixed cost in production whether it increases with

production or not.

A. (2) & C. Preparing income statement using both absorption and marginal costing techniques

with a financial reporting document on it

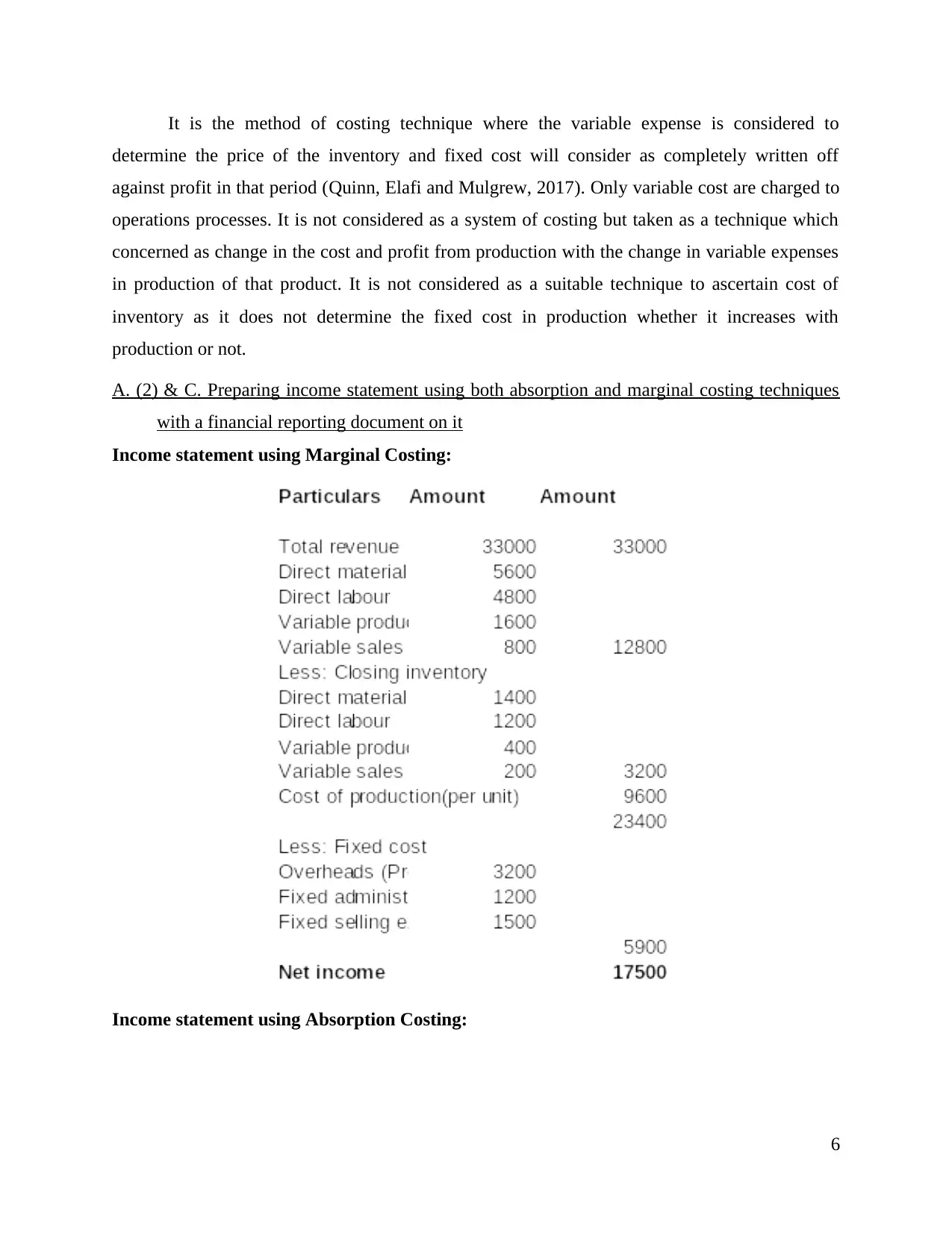

Income statement using Marginal Costing:

Income statement using Absorption Costing:

6

determine the price of the inventory and fixed cost will consider as completely written off

against profit in that period (Quinn, Elafi and Mulgrew, 2017). Only variable cost are charged to

operations processes. It is not considered as a system of costing but taken as a technique which

concerned as change in the cost and profit from production with the change in variable expenses

in production of that product. It is not considered as a suitable technique to ascertain cost of

inventory as it does not determine the fixed cost in production whether it increases with

production or not.

A. (2) & C. Preparing income statement using both absorption and marginal costing techniques

with a financial reporting document on it

Income statement using Marginal Costing:

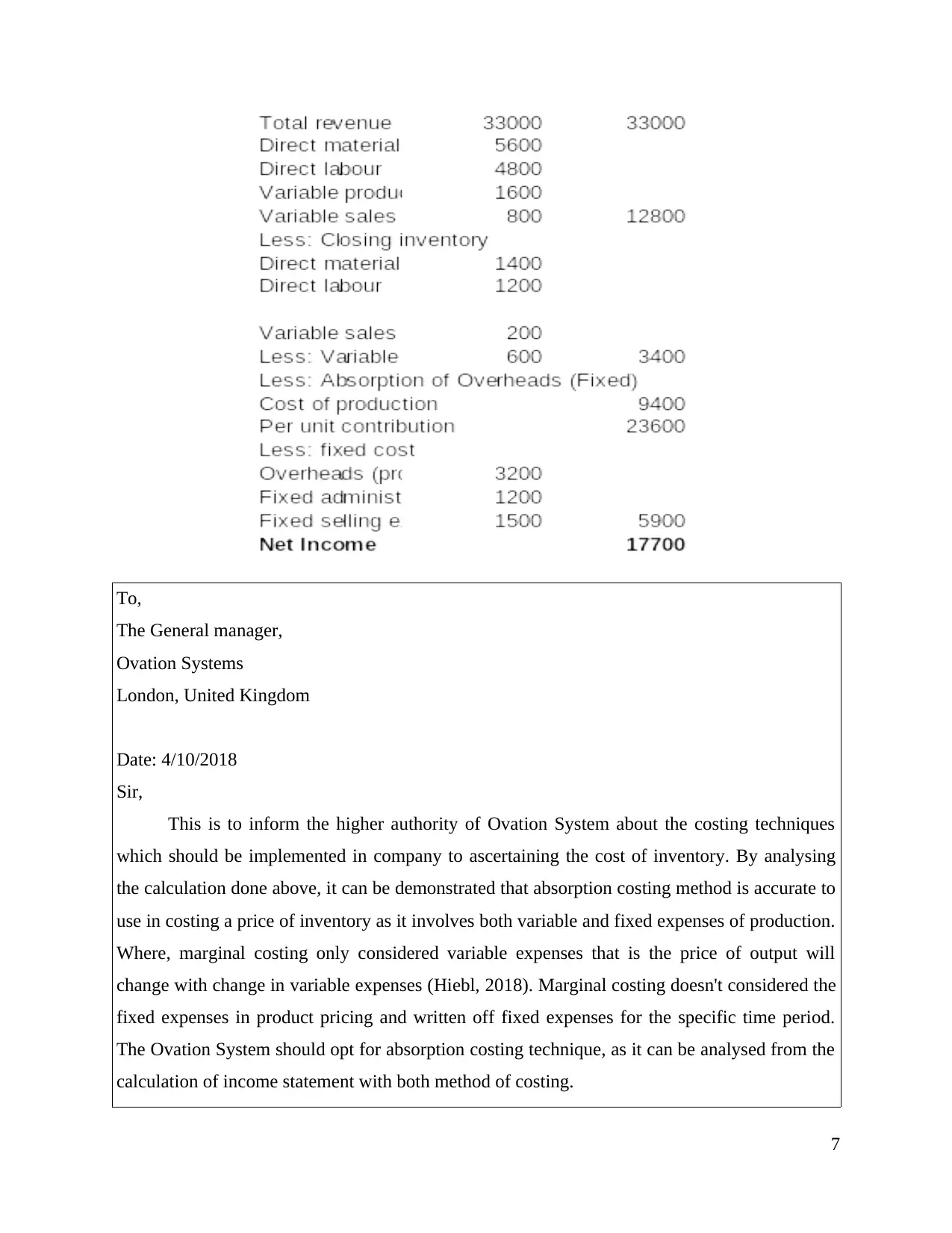

Income statement using Absorption Costing:

6

To,

The General manager,

Ovation Systems

London, United Kingdom

Date: 4/10/2018

Sir,

This is to inform the higher authority of Ovation System about the costing techniques

which should be implemented in company to ascertaining the cost of inventory. By analysing

the calculation done above, it can be demonstrated that absorption costing method is accurate to

use in costing a price of inventory as it involves both variable and fixed expenses of production.

Where, marginal costing only considered variable expenses that is the price of output will

change with change in variable expenses (Hiebl, 2018). Marginal costing doesn't considered the

fixed expenses in product pricing and written off fixed expenses for the specific time period.

The Ovation System should opt for absorption costing technique, as it can be analysed from the

calculation of income statement with both method of costing.

7

The General manager,

Ovation Systems

London, United Kingdom

Date: 4/10/2018

Sir,

This is to inform the higher authority of Ovation System about the costing techniques

which should be implemented in company to ascertaining the cost of inventory. By analysing

the calculation done above, it can be demonstrated that absorption costing method is accurate to

use in costing a price of inventory as it involves both variable and fixed expenses of production.

Where, marginal costing only considered variable expenses that is the price of output will

change with change in variable expenses (Hiebl, 2018). Marginal costing doesn't considered the

fixed expenses in product pricing and written off fixed expenses for the specific time period.

The Ovation System should opt for absorption costing technique, as it can be analysed from the

calculation of income statement with both method of costing.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Implementing absorption costing will give higher net income that is 17700 pounds,

where marginal costing will give only 17500 pounds of net profit. Hence, using absorption

costing techniques will help the company to show accurate profit calculation to set final cost of

goods and services. This method is very important as it includes fixed manufacturing cost which

is also important in manufacturing process which required to be recovered from selling price of

products. Adopting absorption costing will provide complete picture of cost per unit of a

product line that will be helpful for a company management in evaluating profitability by

determining prices for the product and services offered by the company.

Thanks & Regards,

Management Accounting Officer

B. & D. Calculations on Cost Profit Analysis (break-even analysis) with an interpretation of

business activity data

Calculation on Break-Even analysis:

8

where marginal costing will give only 17500 pounds of net profit. Hence, using absorption

costing techniques will help the company to show accurate profit calculation to set final cost of

goods and services. This method is very important as it includes fixed manufacturing cost which

is also important in manufacturing process which required to be recovered from selling price of

products. Adopting absorption costing will provide complete picture of cost per unit of a

product line that will be helpful for a company management in evaluating profitability by

determining prices for the product and services offered by the company.

Thanks & Regards,

Management Accounting Officer

B. & D. Calculations on Cost Profit Analysis (break-even analysis) with an interpretation of

business activity data

Calculation on Break-Even analysis:

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

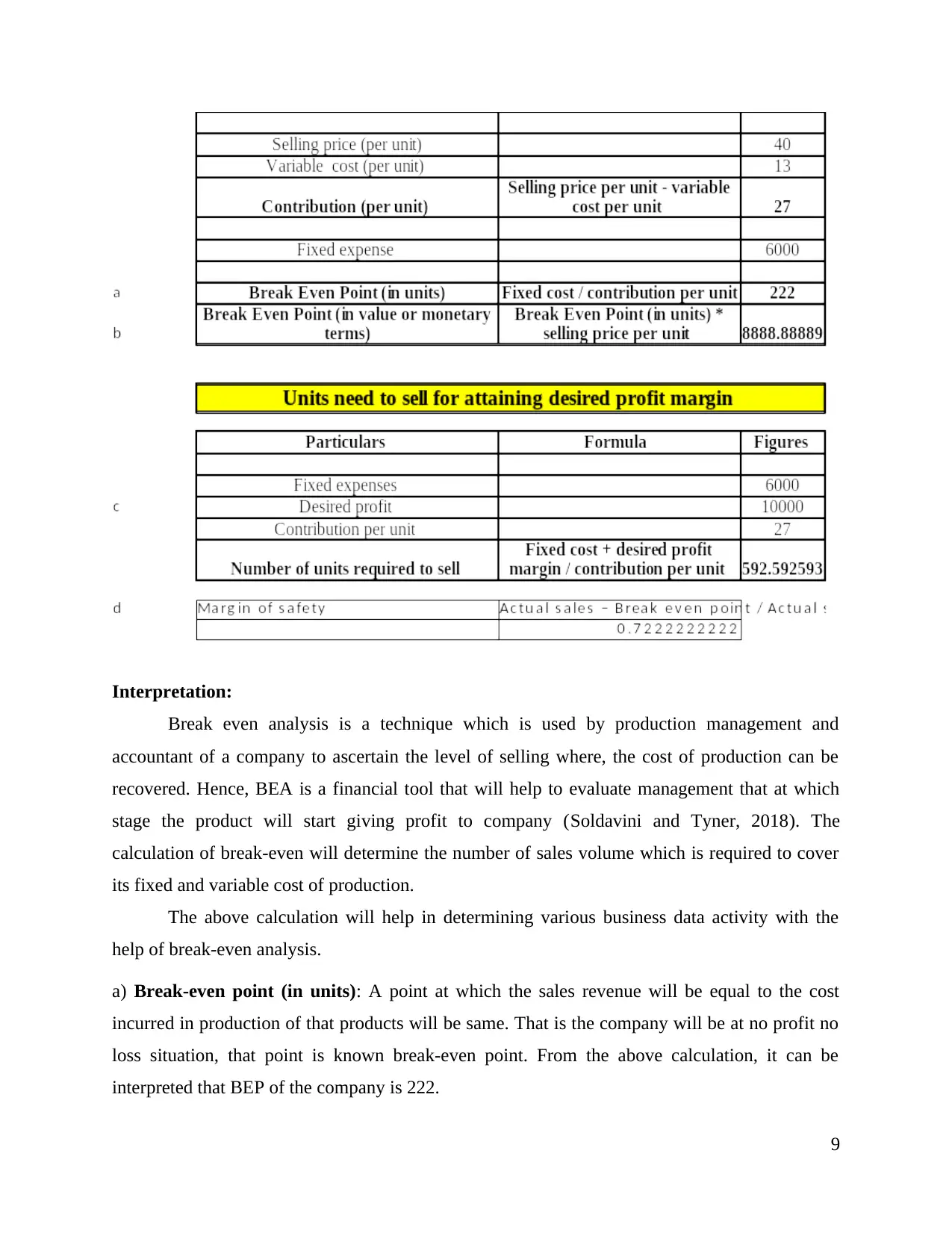

Interpretation:

Break even analysis is a technique which is used by production management and

accountant of a company to ascertain the level of selling where, the cost of production can be

recovered. Hence, BEA is a financial tool that will help to evaluate management that at which

stage the product will start giving profit to company (Soldavini and Tyner, 2018). The

calculation of break-even will determine the number of sales volume which is required to cover

its fixed and variable cost of production.

The above calculation will help in determining various business data activity with the

help of break-even analysis.

a) Break-even point (in units): A point at which the sales revenue will be equal to the cost

incurred in production of that products will be same. That is the company will be at no profit no

loss situation, that point is known break-even point. From the above calculation, it can be

interpreted that BEP of the company is 222.

9

Break even analysis is a technique which is used by production management and

accountant of a company to ascertain the level of selling where, the cost of production can be

recovered. Hence, BEA is a financial tool that will help to evaluate management that at which

stage the product will start giving profit to company (Soldavini and Tyner, 2018). The

calculation of break-even will determine the number of sales volume which is required to cover

its fixed and variable cost of production.

The above calculation will help in determining various business data activity with the

help of break-even analysis.

a) Break-even point (in units): A point at which the sales revenue will be equal to the cost

incurred in production of that products will be same. That is the company will be at no profit no

loss situation, that point is known break-even point. From the above calculation, it can be

interpreted that BEP of the company is 222.

9

b) Break-even point (in monetary term): The BEP value of company where the cost of

production is equal to the sales revenue is pound 8888.889.

c) Desired profit: The number of product that is required to sell in order to earn the desired

profit of pound 10,000 is 592.59259 units of product.

d) Margin of safety: The safety margin required if 800 products are sold is 722.

TASK 3

A. Explaining demerits and merits of different planning tools for budgetary control

According to CIMA, Budgeting is referred as formal quantitative expression of plan of

management. As it is quantified in monetary aspect which is prepared and approved prior at

given duration reflecting planned income which is generated and capital attained for specifying

objective.

Cash Budget: It refers to appropriate estimation of inflow and outflow of cash for

particular business at specific duration of time. Generally, it is used for assessing whether

liquidity for operation is sufficient or not. Its main objective is to give current status of

organization about its position of cash at single point of time. This tool helps in prioritizing the

period of payment related to budget (Ax and Greve, 2017).

Advantages

It helps management for concentrating on its attention on important concerns which are

not proceeding as per plan.

The communication is improved and gives appropriate understanding along with

consonant relationship within its employees.

Coordination is improved in context of each activity within all departments of Ovation

System.

It helps in reducing cost and to maximise profit in efficient aspect.

It improves thinking of management and devise efficient as well as effective method of

handling its resources.

Disadvantages

It is fully built on the basis of subjective estimate.

The cooperation and operation of staff is associated with success.

It takes huge time for accomplishing its objective.

10

production is equal to the sales revenue is pound 8888.889.

c) Desired profit: The number of product that is required to sell in order to earn the desired

profit of pound 10,000 is 592.59259 units of product.

d) Margin of safety: The safety margin required if 800 products are sold is 722.

TASK 3

A. Explaining demerits and merits of different planning tools for budgetary control

According to CIMA, Budgeting is referred as formal quantitative expression of plan of

management. As it is quantified in monetary aspect which is prepared and approved prior at

given duration reflecting planned income which is generated and capital attained for specifying

objective.

Cash Budget: It refers to appropriate estimation of inflow and outflow of cash for

particular business at specific duration of time. Generally, it is used for assessing whether

liquidity for operation is sufficient or not. Its main objective is to give current status of

organization about its position of cash at single point of time. This tool helps in prioritizing the

period of payment related to budget (Ax and Greve, 2017).

Advantages

It helps management for concentrating on its attention on important concerns which are

not proceeding as per plan.

The communication is improved and gives appropriate understanding along with

consonant relationship within its employees.

Coordination is improved in context of each activity within all departments of Ovation

System.

It helps in reducing cost and to maximise profit in efficient aspect.

It improves thinking of management and devise efficient as well as effective method of

handling its resources.

Disadvantages

It is fully built on the basis of subjective estimate.

The cooperation and operation of staff is associated with success.

It takes huge time for accomplishing its objective.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.