Management Budget Forecast Assessment: Financial Risk and Ethics

VerifiedAdded on 2020/05/04

|20

|4380

|33

Report

AI Summary

This report presents a comprehensive management budget forecast assessment, encompassing various financial aspects. It begins with a cash budget analysis for Maan Snack Bar, examining cash flow trends and their implications, including potential consequences of persistent deficits and strategies to address them. The report then delves into annual budgeted expenses, sales budgets, and financial statements such as income statements and balance sheets. It also explores financial risk and mitigation strategies, specifically for the BHP Billiton Group, addressing interest rate, environmental compliance, and commodity price risks. Furthermore, the report emphasizes the importance of ethics and codes of practice in budget forecasting, highlighting the benefits of ethical considerations. Key Performing Indicators (KPIs) and forecasting trends, including a graphical representation of a company's net profits, are also discussed. The report concludes by underscoring the significance of feasibility studies to compare projections with market growth and development.

MANAGEMENT BUDGET FORECAST

ASSESSMENTs ACTIVITY 2

ASSESSMENTs ACTIVITY 2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Task 2.1......................................................................................................................................4

Cash Budget...........................................................................................................................4

Analysis of facts derived from Cash Budget..........................................................................5

Action Plan for upcoming year..............................................................................................6

Task 2.2......................................................................................................................................7

Annual Budgeted Expense for the year 2016.........................................................................7

Expenditure milestones..........................................................................................................9

Type of verifiable data and sources that can provide information to prepare budget and

forecast...................................................................................................................................9

Task 2.3......................................................................................................................................9

Sales Budget for August.........................................................................................................9

Assumptions and parameters for accuracy, relevance and compliance...............................10

Task 2.4....................................................................................................................................11

Budgeted Income Statements...............................................................................................11

Bank Account.......................................................................................................................12

Budgeted Balance Sheet.......................................................................................................12

Task 2.5....................................................................................................................................14

Financial risk and its control for BHP Billiton Group........................................................14

Task 2.6....................................................................................................................................14

Ethics and code of practice related to budget forecast.........................................................14

Importance of ethics.............................................................................................................15

Task 2.7....................................................................................................................................16

Forecasting trends- example................................................................................................16

Graphical representation of XYZ Pty Ltd’ Net profits of 4 years........................................17

XYZ Pty Ltd’s Performance................................................................................................18

Task 2.1......................................................................................................................................4

Cash Budget...........................................................................................................................4

Analysis of facts derived from Cash Budget..........................................................................5

Action Plan for upcoming year..............................................................................................6

Task 2.2......................................................................................................................................7

Annual Budgeted Expense for the year 2016.........................................................................7

Expenditure milestones..........................................................................................................9

Type of verifiable data and sources that can provide information to prepare budget and

forecast...................................................................................................................................9

Task 2.3......................................................................................................................................9

Sales Budget for August.........................................................................................................9

Assumptions and parameters for accuracy, relevance and compliance...............................10

Task 2.4....................................................................................................................................11

Budgeted Income Statements...............................................................................................11

Bank Account.......................................................................................................................12

Budgeted Balance Sheet.......................................................................................................12

Task 2.5....................................................................................................................................14

Financial risk and its control for BHP Billiton Group........................................................14

Task 2.6....................................................................................................................................14

Ethics and code of practice related to budget forecast.........................................................14

Importance of ethics.............................................................................................................15

Task 2.7....................................................................................................................................16

Forecasting trends- example................................................................................................16

Graphical representation of XYZ Pty Ltd’ Net profits of 4 years........................................17

XYZ Pty Ltd’s Performance................................................................................................18

Task 2.8....................................................................................................................................18

Key Performing Indicators / Ratios......................................................................................18

Other Key Performing Indicators helpful for forecasting estimates....................................19

Importance of feasibility study to compare projections with market growth and

development.........................................................................................................................21

References................................................................................................................................23

Key Performing Indicators / Ratios......................................................................................18

Other Key Performing Indicators helpful for forecasting estimates....................................19

Importance of feasibility study to compare projections with market growth and

development.........................................................................................................................21

References................................................................................................................................23

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

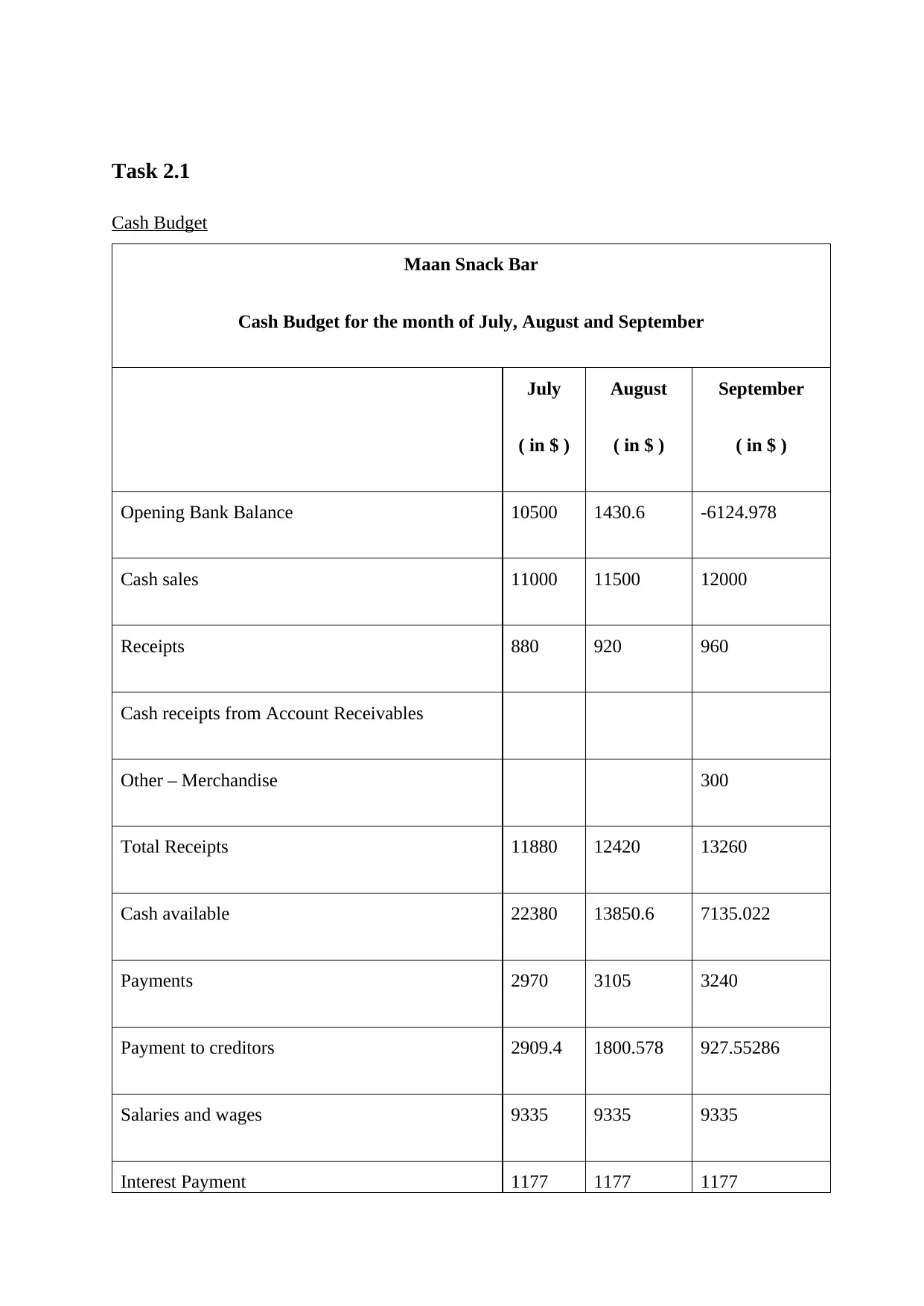

Task 2.1

Cash Budget

Maan Snack Bar

Cash Budget for the month of July, August and September

July

( in $ )

August

( in $ )

September

( in $ )

Opening Bank Balance 10500 1430.6 -6124.978

Cash sales 11000 11500 12000

Receipts 880 920 960

Cash receipts from Account Receivables

Other – Merchandise 300

Total Receipts 11880 12420 13260

Cash available 22380 13850.6 7135.022

Payments 2970 3105 3240

Payment to creditors 2909.4 1800.578 927.55286

Salaries and wages 9335 9335 9335

Interest Payment 1177 1177 1177

Cash Budget

Maan Snack Bar

Cash Budget for the month of July, August and September

July

( in $ )

August

( in $ )

September

( in $ )

Opening Bank Balance 10500 1430.6 -6124.978

Cash sales 11000 11500 12000

Receipts 880 920 960

Cash receipts from Account Receivables

Other – Merchandise 300

Total Receipts 11880 12420 13260

Cash available 22380 13850.6 7135.022

Payments 2970 3105 3240

Payment to creditors 2909.4 1800.578 927.55286

Salaries and wages 9335 9335 9335

Interest Payment 1177 1177 1177

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

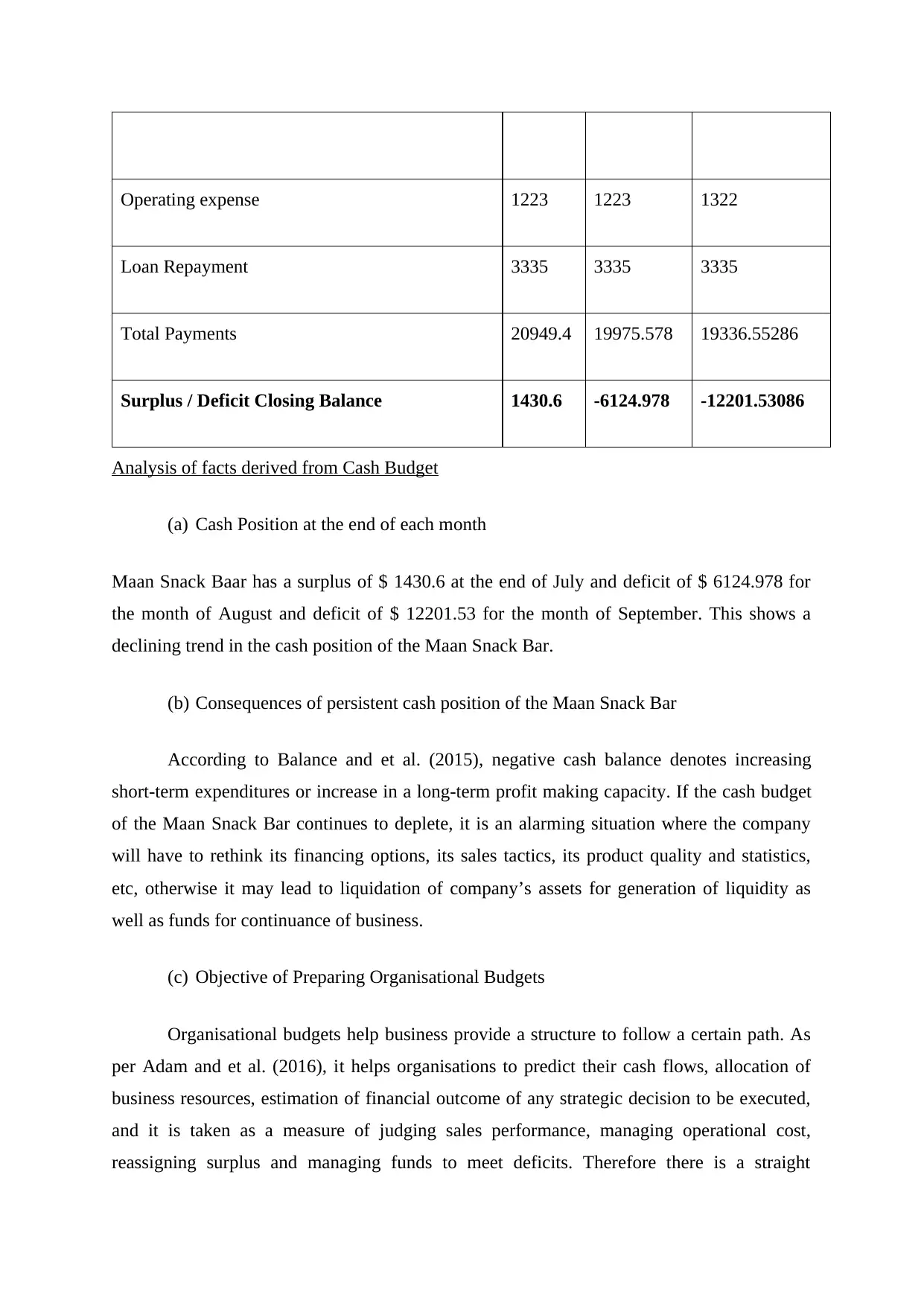

Operating expense 1223 1223 1322

Loan Repayment 3335 3335 3335

Total Payments 20949.4 19975.578 19336.55286

Surplus / Deficit Closing Balance 1430.6 -6124.978 -12201.53086

Analysis of facts derived from Cash Budget

(a) Cash Position at the end of each month

Maan Snack Baar has a surplus of $ 1430.6 at the end of July and deficit of $ 6124.978 for

the month of August and deficit of $ 12201.53 for the month of September. This shows a

declining trend in the cash position of the Maan Snack Bar.

(b) Consequences of persistent cash position of the Maan Snack Bar

According to Balance and et al. (2015), negative cash balance denotes increasing

short-term expenditures or increase in a long-term profit making capacity. If the cash budget

of the Maan Snack Bar continues to deplete, it is an alarming situation where the company

will have to rethink its financing options, its sales tactics, its product quality and statistics,

etc, otherwise it may lead to liquidation of company’s assets for generation of liquidity as

well as funds for continuance of business.

(c) Objective of Preparing Organisational Budgets

Organisational budgets help business provide a structure to follow a certain path. As

per Adam and et al. (2016), it helps organisations to predict their cash flows, allocation of

business resources, estimation of financial outcome of any strategic decision to be executed,

and it is taken as a measure of judging sales performance, managing operational cost,

reassigning surplus and managing funds to meet deficits. Therefore there is a straight

Loan Repayment 3335 3335 3335

Total Payments 20949.4 19975.578 19336.55286

Surplus / Deficit Closing Balance 1430.6 -6124.978 -12201.53086

Analysis of facts derived from Cash Budget

(a) Cash Position at the end of each month

Maan Snack Baar has a surplus of $ 1430.6 at the end of July and deficit of $ 6124.978 for

the month of August and deficit of $ 12201.53 for the month of September. This shows a

declining trend in the cash position of the Maan Snack Bar.

(b) Consequences of persistent cash position of the Maan Snack Bar

According to Balance and et al. (2015), negative cash balance denotes increasing

short-term expenditures or increase in a long-term profit making capacity. If the cash budget

of the Maan Snack Bar continues to deplete, it is an alarming situation where the company

will have to rethink its financing options, its sales tactics, its product quality and statistics,

etc, otherwise it may lead to liquidation of company’s assets for generation of liquidity as

well as funds for continuance of business.

(c) Objective of Preparing Organisational Budgets

Organisational budgets help business provide a structure to follow a certain path. As

per Adam and et al. (2016), it helps organisations to predict their cash flows, allocation of

business resources, estimation of financial outcome of any strategic decision to be executed,

and it is taken as a measure of judging sales performance, managing operational cost,

reassigning surplus and managing funds to meet deficits. Therefore there is a straight

relationship among organizational budgeting and its attainment of objectives. It helps the

business to keep track of its strategic decision and planning so as to enhance its revenues,

improve its profitability, reduce cost and overall performance.

(d) Stakeholders and consulting methods to promote understanding, goodwill and

ongoing cooperation

Business owners, decision makers, suppliers, customers and employees are the

primary stakeholders who shall be consulted for the purpose of augmenting understanding

and cooperation and increasing the goodwill value. There are many consulting methodologies

to promote understanding, goodwill and ongoing cooperation which can be adopted.

According to the words of Pinheiro, (2014), few of such methodologies include focused

workshops, brainstorming sessions and social interaction activities. This brings these

stakeholders together to better understanding and enhanced cooperation between each other,

which eventually helps build goodwill of the business.

Action Plan for upcoming year

Increase in cash sales: As per the words of Cox (2014), cash sales can be

increased by bulk sales customers by selling more quantities even for lesser margins,

also greater promotional activities may lead to broader network of clients, and making

attractive offers to retail clients may lead to generation of higher cash inflows. Higher

cash flows, better credit periods, higher net profits are some evidence that supports

future financial improvements.

Reduction in cash payments: Cash payments can be reduced by giving new

suppliers an opportunity, who can give longer credit periods or discounts on cash

payments, chose last dates for huge payment settlements, reduced overstocking, late

invoices from suppliers, better negotiations, improving tax compliances, etc.

Saving in overall labour cost: Overall labour costs can be saved by cross

training new employees, investing in technology and machinery with higher

production capacity, outsourcing certain activities, best employee retention, regular

reviews, Commission based payroll, reduced perquisites, etc.

Improvement in operating expenditure: Operating expenses can be improved

or reduced through controlling the wastage and providing an order of products by

assessing the sales of the previous year. The same will result into ordering the product

business to keep track of its strategic decision and planning so as to enhance its revenues,

improve its profitability, reduce cost and overall performance.

(d) Stakeholders and consulting methods to promote understanding, goodwill and

ongoing cooperation

Business owners, decision makers, suppliers, customers and employees are the

primary stakeholders who shall be consulted for the purpose of augmenting understanding

and cooperation and increasing the goodwill value. There are many consulting methodologies

to promote understanding, goodwill and ongoing cooperation which can be adopted.

According to the words of Pinheiro, (2014), few of such methodologies include focused

workshops, brainstorming sessions and social interaction activities. This brings these

stakeholders together to better understanding and enhanced cooperation between each other,

which eventually helps build goodwill of the business.

Action Plan for upcoming year

Increase in cash sales: As per the words of Cox (2014), cash sales can be

increased by bulk sales customers by selling more quantities even for lesser margins,

also greater promotional activities may lead to broader network of clients, and making

attractive offers to retail clients may lead to generation of higher cash inflows. Higher

cash flows, better credit periods, higher net profits are some evidence that supports

future financial improvements.

Reduction in cash payments: Cash payments can be reduced by giving new

suppliers an opportunity, who can give longer credit periods or discounts on cash

payments, chose last dates for huge payment settlements, reduced overstocking, late

invoices from suppliers, better negotiations, improving tax compliances, etc.

Saving in overall labour cost: Overall labour costs can be saved by cross

training new employees, investing in technology and machinery with higher

production capacity, outsourcing certain activities, best employee retention, regular

reviews, Commission based payroll, reduced perquisites, etc.

Improvement in operating expenditure: Operating expenses can be improved

or reduced through controlling the wastage and providing an order of products by

assessing the sales of the previous year. The same will result into ordering the product

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

which is in demand and reduce the chances of having dead stock. Further appropriate

budgets such as marketing budget etc. should be prepared so that we know the extent

to which we have to spent on same.

Task 2.2

Annual Budgeted Expense for the year 2016

Maan Snack Bar

Annual Expense Budget for coming the year 2016

Particulars Monthly

( in $ )

Budgeted

Annual

( in $ )

Expected Fee 450000

Marketing Expense

Fixed Advertising 7800

Variable Advertising 18000

Total Marketing Expense 25800

Financial Expense

Fixed Interest paid 2400 28800

Bank charges 300 3600

budgets such as marketing budget etc. should be prepared so that we know the extent

to which we have to spent on same.

Task 2.2

Annual Budgeted Expense for the year 2016

Maan Snack Bar

Annual Expense Budget for coming the year 2016

Particulars Monthly

( in $ )

Budgeted

Annual

( in $ )

Expected Fee 450000

Marketing Expense

Fixed Advertising 7800

Variable Advertising 18000

Total Marketing Expense 25800

Financial Expense

Fixed Interest paid 2400 28800

Bank charges 300 3600

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

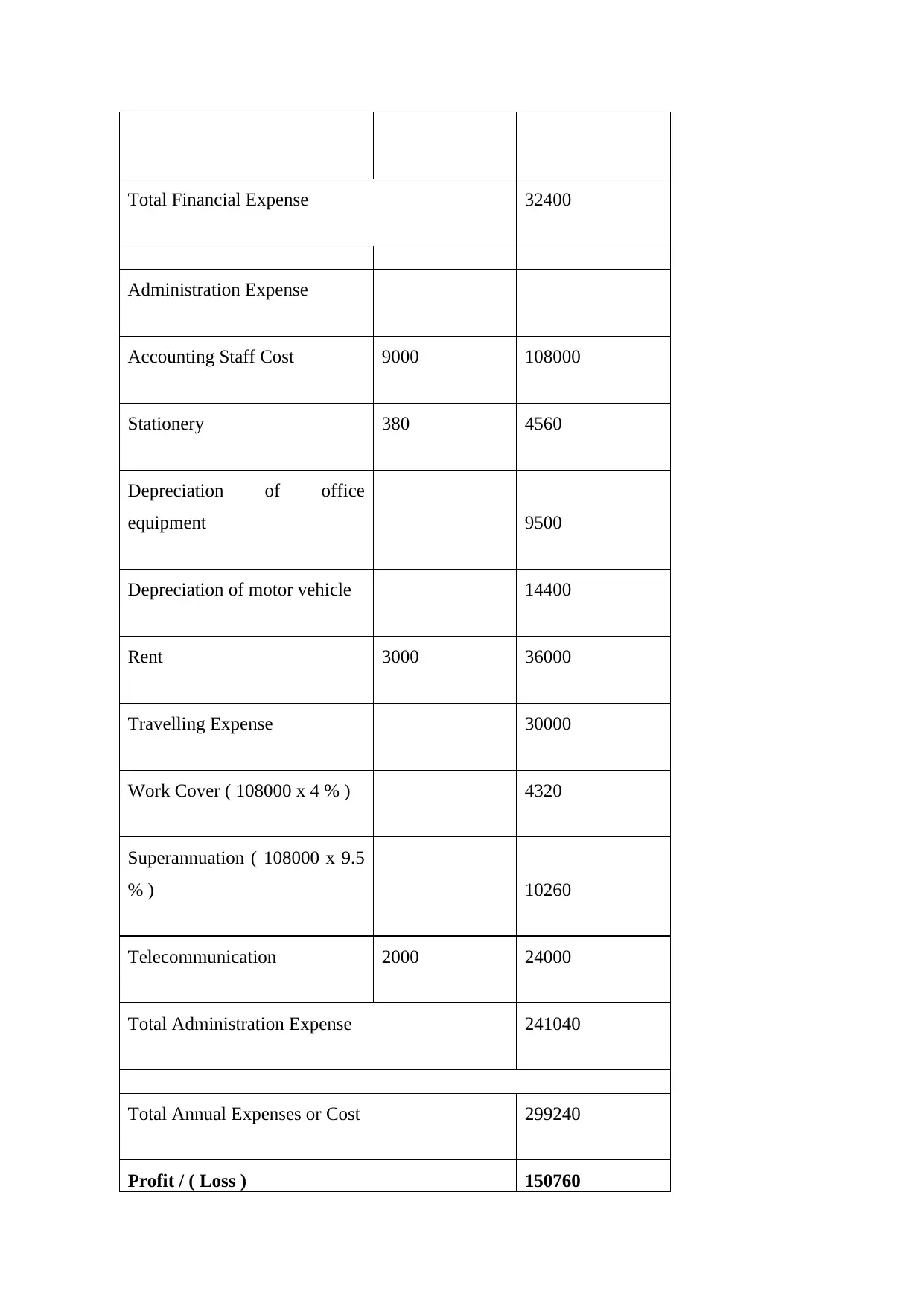

Total Financial Expense 32400

Administration Expense

Accounting Staff Cost 9000 108000

Stationery 380 4560

Depreciation of office

equipment 9500

Depreciation of motor vehicle 14400

Rent 3000 36000

Travelling Expense 30000

Work Cover ( 108000 x 4 % ) 4320

Superannuation ( 108000 x 9.5

% ) 10260

Telecommunication 2000 24000

Total Administration Expense 241040

Total Annual Expenses or Cost 299240

Profit / ( Loss ) 150760

Administration Expense

Accounting Staff Cost 9000 108000

Stationery 380 4560

Depreciation of office

equipment 9500

Depreciation of motor vehicle 14400

Rent 3000 36000

Travelling Expense 30000

Work Cover ( 108000 x 4 % ) 4320

Superannuation ( 108000 x 9.5

% ) 10260

Telecommunication 2000 24000

Total Administration Expense 241040

Total Annual Expenses or Cost 299240

Profit / ( Loss ) 150760

Expenditure milestones

In the current situation expenditure milestones are expected to be set up based on

certain characteristics like specific - in terms of figures so as to measure at the year-end, there

should be deadlines so as to mark it timeliness, progressive nature and doable and

significance which does not portray a bigger picture and encourage procrastination.

According to the views of Klychova and et al., (2014), generally, expenditure milestones are

set up based on past experiences, practices, industry standards and adopted practices in past.

Therefore it is assumed that the assumptions and practices remain constant without any

change in the coming year 2016.

Type of verifiable data and sources that can provide information to prepare budget and

forecast

Type of verifiable data and sources for budget preparation and forecast are statements

of financial institutions, vouchers, receipts and invoices, documents of purchase orders and

from suppliers, statutory returns and taxation returns. As per the views of Brigham and et al.,

(2013), other sources like industry norms and standards, competitor’s statistics, market

scenario and economic trends also help budget and forecast.

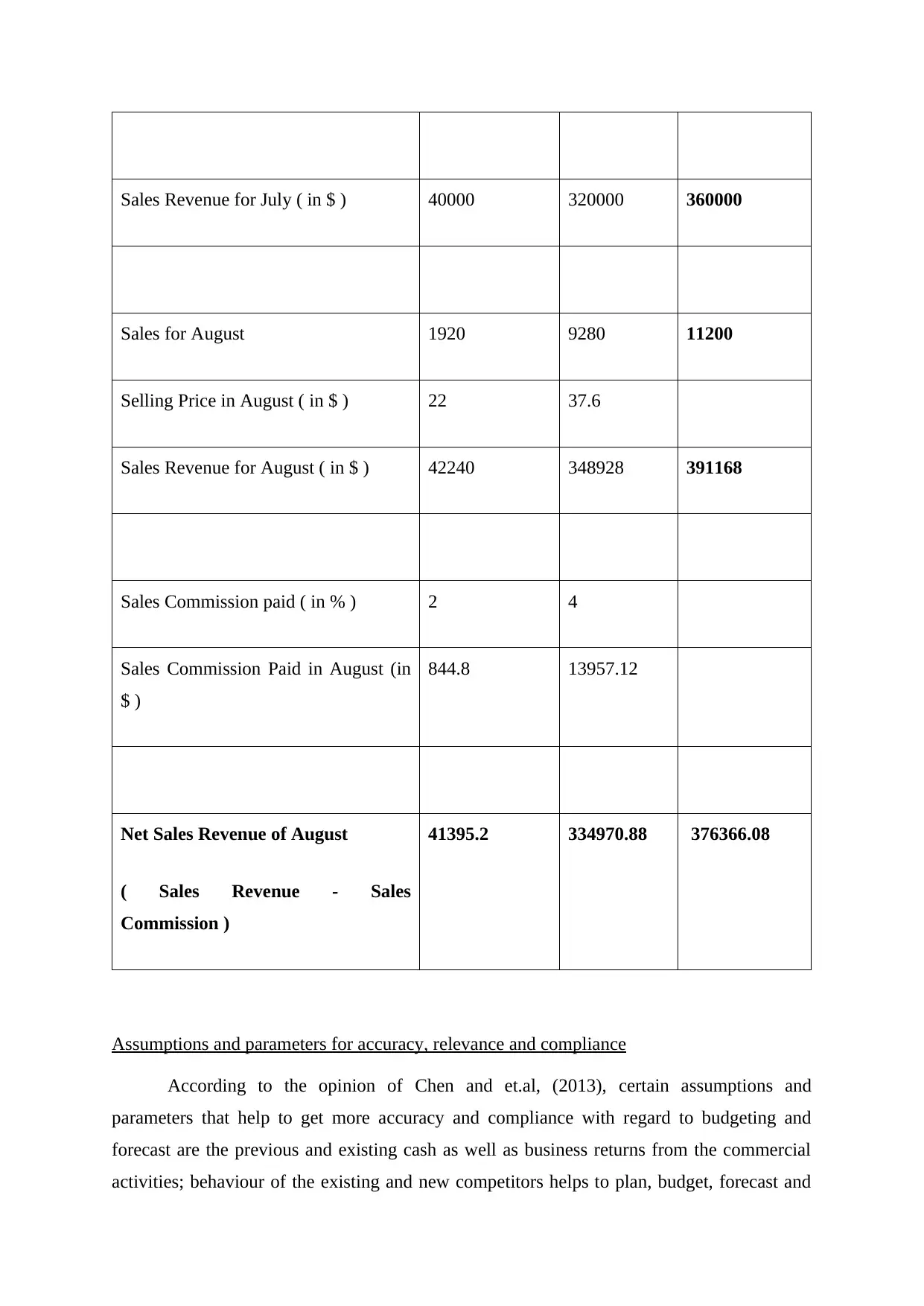

Task 2.3

Sales Budget for August

Sales Budget of Streama of August

Particulars Apple Orange Total

Sales for July 2000 8000 10000

Selling Price in July ( in $ ) 20 40

In the current situation expenditure milestones are expected to be set up based on

certain characteristics like specific - in terms of figures so as to measure at the year-end, there

should be deadlines so as to mark it timeliness, progressive nature and doable and

significance which does not portray a bigger picture and encourage procrastination.

According to the views of Klychova and et al., (2014), generally, expenditure milestones are

set up based on past experiences, practices, industry standards and adopted practices in past.

Therefore it is assumed that the assumptions and practices remain constant without any

change in the coming year 2016.

Type of verifiable data and sources that can provide information to prepare budget and

forecast

Type of verifiable data and sources for budget preparation and forecast are statements

of financial institutions, vouchers, receipts and invoices, documents of purchase orders and

from suppliers, statutory returns and taxation returns. As per the views of Brigham and et al.,

(2013), other sources like industry norms and standards, competitor’s statistics, market

scenario and economic trends also help budget and forecast.

Task 2.3

Sales Budget for August

Sales Budget of Streama of August

Particulars Apple Orange Total

Sales for July 2000 8000 10000

Selling Price in July ( in $ ) 20 40

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Sales Revenue for July ( in $ ) 40000 320000 360000

Sales for August 1920 9280 11200

Selling Price in August ( in $ ) 22 37.6

Sales Revenue for August ( in $ ) 42240 348928 391168

Sales Commission paid ( in % ) 2 4

Sales Commission Paid in August (in

$ )

844.8 13957.12

Net Sales Revenue of August

( Sales Revenue - Sales

Commission )

41395.2 334970.88 376366.08

Assumptions and parameters for accuracy, relevance and compliance

According to the opinion of Chen and et.al, (2013), certain assumptions and

parameters that help to get more accuracy and compliance with regard to budgeting and

forecast are the previous and existing cash as well as business returns from the commercial

activities; behaviour of the existing and new competitors helps to plan, budget, forecast and

Sales for August 1920 9280 11200

Selling Price in August ( in $ ) 22 37.6

Sales Revenue for August ( in $ ) 42240 348928 391168

Sales Commission paid ( in % ) 2 4

Sales Commission Paid in August (in

$ )

844.8 13957.12

Net Sales Revenue of August

( Sales Revenue - Sales

Commission )

41395.2 334970.88 376366.08

Assumptions and parameters for accuracy, relevance and compliance

According to the opinion of Chen and et.al, (2013), certain assumptions and

parameters that help to get more accuracy and compliance with regard to budgeting and

forecast are the previous and existing cash as well as business returns from the commercial

activities; behaviour of the existing and new competitors helps to plan, budget, forecast and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

execute strategic decisions; the expenditure limits marked by the business helps keep track of

cash flows due any changes; statistics of market growth and market share helps decide best

options; levels of productivity of business outputs and the regulatory as well as governmental

stability.

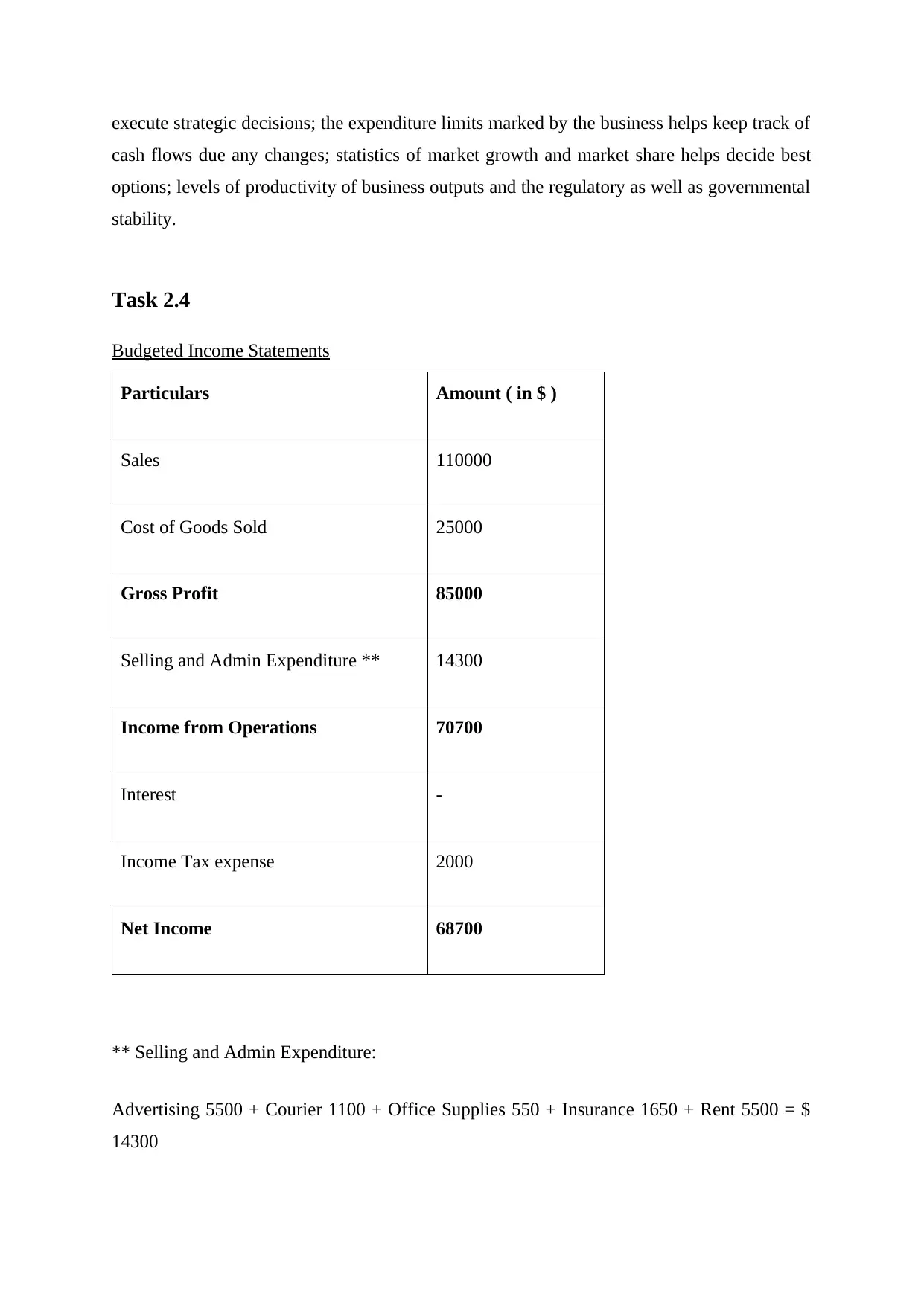

Task 2.4

Budgeted Income Statements

Particulars Amount ( in $ )

Sales 110000

Cost of Goods Sold 25000

Gross Profit 85000

Selling and Admin Expenditure ** 14300

Income from Operations 70700

Interest -

Income Tax expense 2000

Net Income 68700

** Selling and Admin Expenditure:

Advertising 5500 + Courier 1100 + Office Supplies 550 + Insurance 1650 + Rent 5500 = $

14300

cash flows due any changes; statistics of market growth and market share helps decide best

options; levels of productivity of business outputs and the regulatory as well as governmental

stability.

Task 2.4

Budgeted Income Statements

Particulars Amount ( in $ )

Sales 110000

Cost of Goods Sold 25000

Gross Profit 85000

Selling and Admin Expenditure ** 14300

Income from Operations 70700

Interest -

Income Tax expense 2000

Net Income 68700

** Selling and Admin Expenditure:

Advertising 5500 + Courier 1100 + Office Supplies 550 + Insurance 1650 + Rent 5500 = $

14300

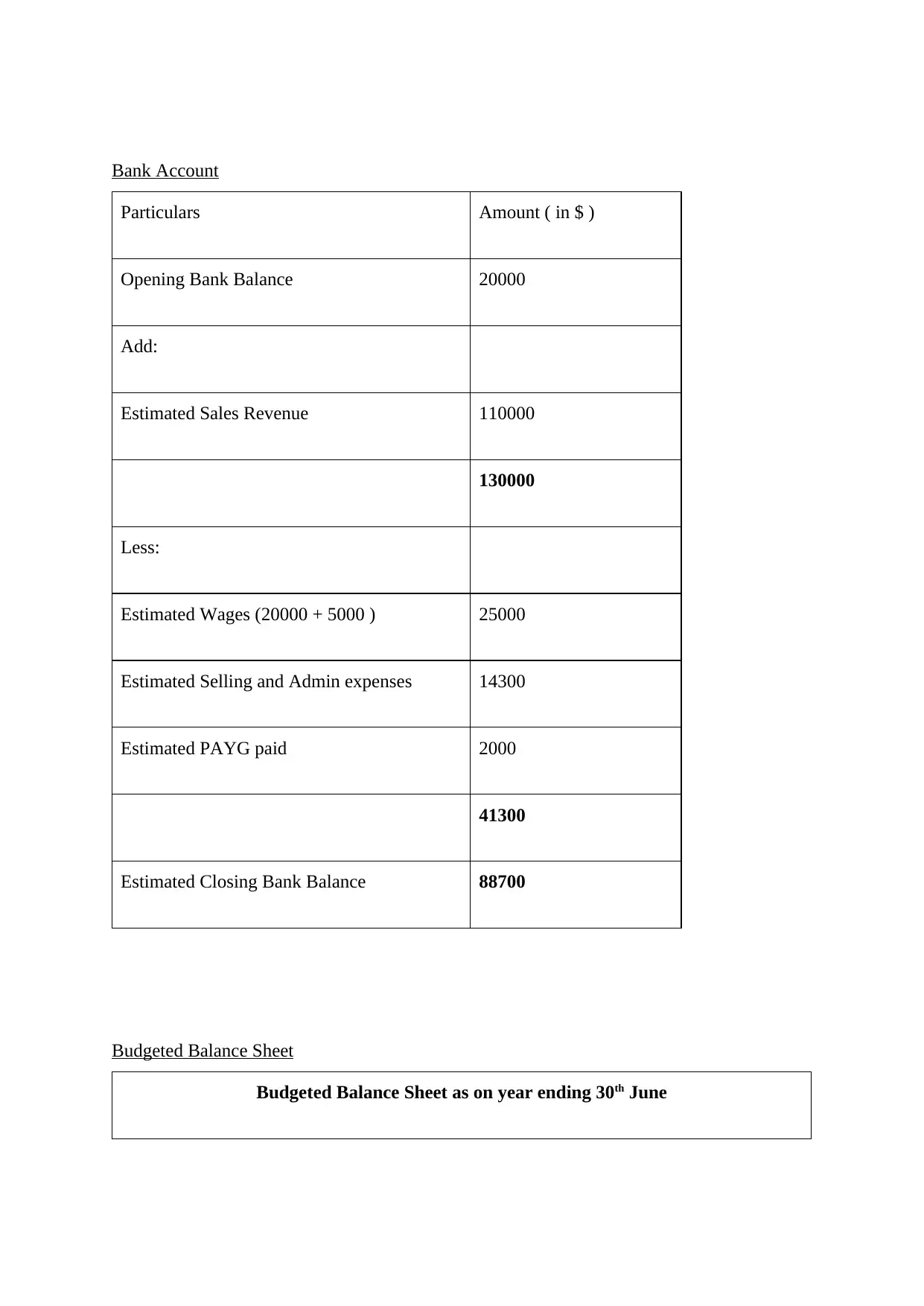

Bank Account

Particulars Amount ( in $ )

Opening Bank Balance 20000

Add:

Estimated Sales Revenue 110000

130000

Less:

Estimated Wages (20000 + 5000 ) 25000

Estimated Selling and Admin expenses 14300

Estimated PAYG paid 2000

41300

Estimated Closing Bank Balance 88700

Budgeted Balance Sheet

Budgeted Balance Sheet as on year ending 30th June

Particulars Amount ( in $ )

Opening Bank Balance 20000

Add:

Estimated Sales Revenue 110000

130000

Less:

Estimated Wages (20000 + 5000 ) 25000

Estimated Selling and Admin expenses 14300

Estimated PAYG paid 2000

41300

Estimated Closing Bank Balance 88700

Budgeted Balance Sheet

Budgeted Balance Sheet as on year ending 30th June

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.