Case Study: Analyzing Make or Buy Decisions in Management Accounting

VerifiedAdded on 2023/05/28

|6

|1141

|105

Case Study

AI Summary

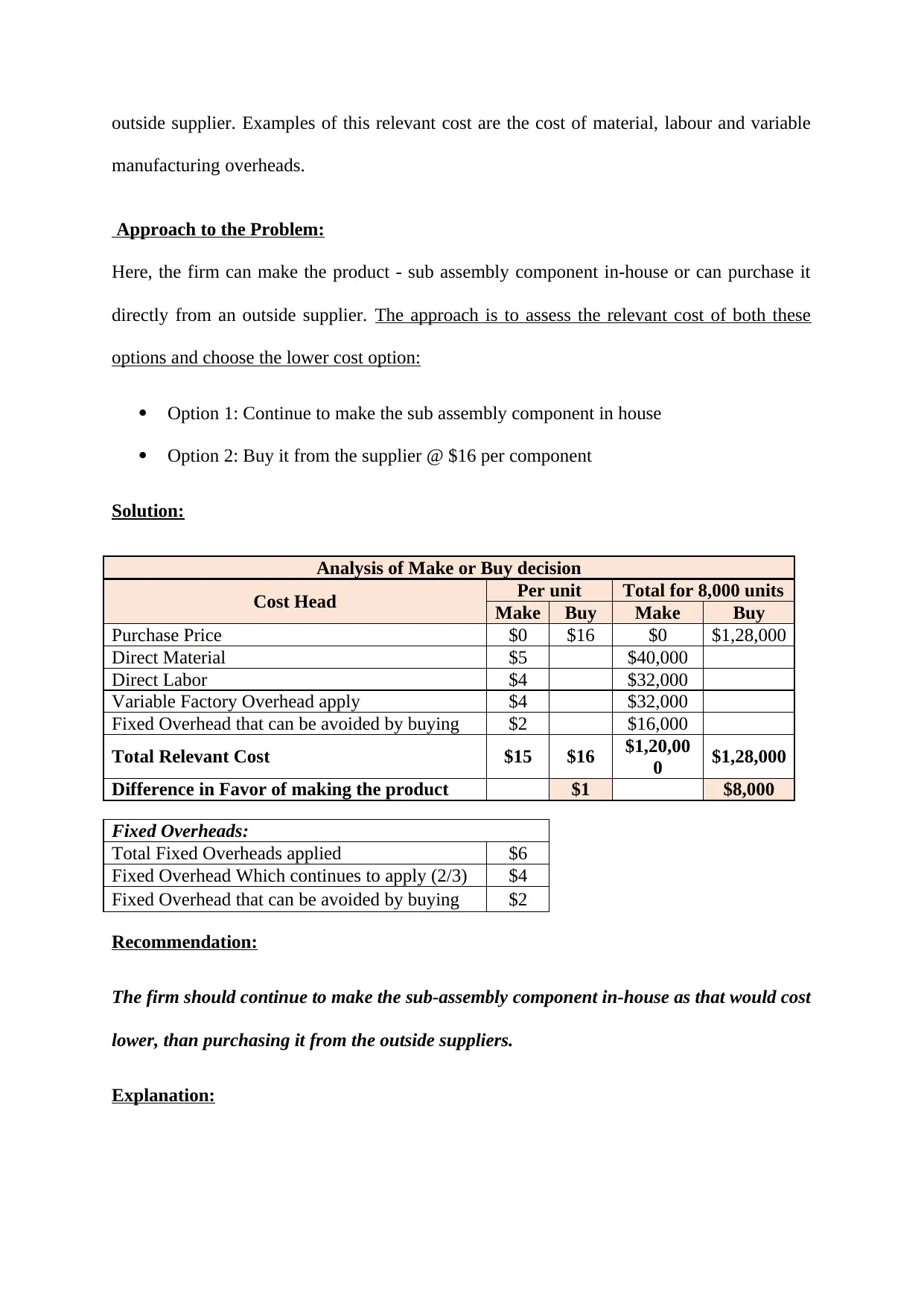

This case study analyzes a make or buy decision faced by a firm considering whether to manufacture a sub-assembly component in-house or purchase it from an external supplier. The assignment presents cost estimates for in-house production, including direct materials, direct labor, variable factory overhead, and fixed factory overhead. The supplier offers to provide the sub-assembly at a set price. The analysis involves calculating the relevant costs, considering which fixed overhead costs are avoidable if the component is purchased externally. The solution determines the per-unit cost for both options, considering the relevant costs, and recommends whether the firm should continue to make the component or buy it, ultimately concluding that the firm should continue making the sub-assembly component in-house due to cost savings. The case study emphasizes the importance of understanding relevant costs in making strategic decisions and provides a detailed breakdown of the cost analysis, including references to support the approach.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.