Management Accounting Report: NISA Co. Ltd. Case Study Analysis

VerifiedAdded on 2020/01/07

|24

|6846

|313

Report

AI Summary

This report comprehensively examines management accounting principles and their practical application within the context of NISA Co. Ltd., a UK-based retail enterprise. The report begins with an introduction to management accounting, its techniques, and essential requirements, highlighting its role in financial planning and decision-making. It then delves into various management accounting methods, including cost analysis, performance measurement, project decision-making, planning, budgeting, and financial statement analysis. The report further explores different costing methods, contrasting marginal and absorption costing, and analyzes the budgetary control system tailored for NISA Co. Ltd. Additionally, it discusses various management accounting systems aimed at mitigating financial challenges faced by NISA Ltd. The report emphasizes the importance of these tools for effective business operations, forecasting, and strategic decision-making, providing insights into how NISA Co. Ltd. can optimize its financial strategies and enhance its overall performance.

Management

Accounting

1

Accounting

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1) Management accounting and its techniques' essential requirements....................................3

P2) Management accounting methods.........................................................................................5

TASK 2............................................................................................................................................8

P3) Different costing methods and differences between marginal and absorption costing.........8

TASK 3..........................................................................................................................................12

P4) Budgetary Control system for NISA Co. Ltd......................................................................12

P5) Different management accounting systems to reduce financial problem for Nisa Ltd.......17

CONCLUSION..............................................................................................................................19

REFERENCE.................................................................................................................................20

2

INTRODUCTION...........................................................................................................................3

TASK 1............................................................................................................................................3

P1) Management accounting and its techniques' essential requirements....................................3

P2) Management accounting methods.........................................................................................5

TASK 2............................................................................................................................................8

P3) Different costing methods and differences between marginal and absorption costing.........8

TASK 3..........................................................................................................................................12

P4) Budgetary Control system for NISA Co. Ltd......................................................................12

P5) Different management accounting systems to reduce financial problem for Nisa Ltd.......17

CONCLUSION..............................................................................................................................19

REFERENCE.................................................................................................................................20

2

INTRODUCTION

Management accounting is multidisciplinary approach to expand business entity and

managing its overall operations. It is useful approach for forecasting and decision making related

to further business operations. The present report is based on understanding different

management accounting tools and systems of Nisa ltd. It is small scale retail sector enterprise of

UK that provides groceries and food items. Different management accounting tools and methods

can be described to signify its importance. In addition to this, several costing methods to prepare

income statement that present financial position of organization is able to understand through

this assignment. Moreover, positive and negative aspects of budgeting can be expressed which is

considered as key component for preparing strategies and monitoring excess of production.

Along with this, several management accounting systems for reducing economic problems of

entity is to be expressed effectively. Hence, through this study, learners are able to understand

significance of management accounting tools for decision making regarding operating further

business activities.

TASK 1

P1) Management accounting and its techniques' essential requirements

Management Accounting:- Process of preparing management reports and accounts that

provie timely and accurate Financial and statistics information that requires by managers to run

business in day to day and short term decisions (Bellah and et. al., 2013). Unlikely Financial

reports that are published for external share or stake holders in yearly basis by organization

management accounting provide monthly or weakly reports to run business for internal

departments like purchase manager, sales manager or Chief executive officer. These reports

generally shows amount of cash in hand, purchase order, Sales revenue generated, Accounts

payable and receivable, Outstanding debts, raw material, inventory purchase and may also

include trends chart, variance analysis and other statistics

Different Type of Management Accounting: Tools & Technique used in management

accounting.

Financial Planning: The main objective of any business is to achieve objective.

Objective can be of any kind but for NISA Company which is retail sector company 505 -

3

Management accounting is multidisciplinary approach to expand business entity and

managing its overall operations. It is useful approach for forecasting and decision making related

to further business operations. The present report is based on understanding different

management accounting tools and systems of Nisa ltd. It is small scale retail sector enterprise of

UK that provides groceries and food items. Different management accounting tools and methods

can be described to signify its importance. In addition to this, several costing methods to prepare

income statement that present financial position of organization is able to understand through

this assignment. Moreover, positive and negative aspects of budgeting can be expressed which is

considered as key component for preparing strategies and monitoring excess of production.

Along with this, several management accounting systems for reducing economic problems of

entity is to be expressed effectively. Hence, through this study, learners are able to understand

significance of management accounting tools for decision making regarding operating further

business activities.

TASK 1

P1) Management accounting and its techniques' essential requirements

Management Accounting:- Process of preparing management reports and accounts that

provie timely and accurate Financial and statistics information that requires by managers to run

business in day to day and short term decisions (Bellah and et. al., 2013). Unlikely Financial

reports that are published for external share or stake holders in yearly basis by organization

management accounting provide monthly or weakly reports to run business for internal

departments like purchase manager, sales manager or Chief executive officer. These reports

generally shows amount of cash in hand, purchase order, Sales revenue generated, Accounts

payable and receivable, Outstanding debts, raw material, inventory purchase and may also

include trends chart, variance analysis and other statistics

Different Type of Management Accounting: Tools & Technique used in management

accounting.

Financial Planning: The main objective of any business is to achieve objective.

Objective can be of any kind but for NISA Company which is retail sector company 505 -

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Type of paper : Assignment definitely would be to maximize profit by maximize sales.

So financial planning can help to achieve it (Brigham and Houston, 2011). Financial Statement Analysis: Profit and loss & balance sheet are important report of

company. These report are analyses at different period. These reports help manager to

analyses growth of business concern. These reports are made through various competitive

financial statements, common size statements and ratio analysis. Ratio Analysis: It is used to analyses company profitability, efficiency variability, and

liquidity (Chandra, 2011). They are current ratio, Quick ratio, return on equity ratio,

Equity and Debts ratio, Dividend payout ratio and earning per share ratios. Cost Accounting system: Cost accounting represents cost data in product wise, process

wise, department and branch wise. These cost data are compared with determined one.

This consist of two cost gives management a reason between differences of cost and

optimal best solution is taken to fill the gap. So retail company like NISA can use this

accounting to control cost of production and transportation cost so that goods can be sold

at reasonable rate (Chapman, Hopwood and Shields, 2011). Fund Flow Analysis: This analysis find out the movement of fund from one period to

another. Moreover, this analysis is very useful to know whether the fund is properly used

or not in a year when compared to the previous year. The Working capital changes and

funds from operation are also find out through this analysis. Standard Costing: It is predetermined cost. It provide yardstick for measuring actual

performance. It is used to find reasons in deviation if any in cost accounting (Gesimba,

Alvar and Mante, 2014). Marginal Costing: It is used to fixed the selling price, Selection of best sales mix, best

use of scarce raw material and resources, to take a decision whether to buy or to make a

product. Purchase or reject bulk order. This is based on fixed, variable and contribution in

business (Hult, Craighead and Ketchen Jr, 2010). Budgetary Control: Future financial needs are determined under this tools. It is used to

control financial performance of business. Business operations are directed in desired

direction.

4

So financial planning can help to achieve it (Brigham and Houston, 2011). Financial Statement Analysis: Profit and loss & balance sheet are important report of

company. These report are analyses at different period. These reports help manager to

analyses growth of business concern. These reports are made through various competitive

financial statements, common size statements and ratio analysis. Ratio Analysis: It is used to analyses company profitability, efficiency variability, and

liquidity (Chandra, 2011). They are current ratio, Quick ratio, return on equity ratio,

Equity and Debts ratio, Dividend payout ratio and earning per share ratios. Cost Accounting system: Cost accounting represents cost data in product wise, process

wise, department and branch wise. These cost data are compared with determined one.

This consist of two cost gives management a reason between differences of cost and

optimal best solution is taken to fill the gap. So retail company like NISA can use this

accounting to control cost of production and transportation cost so that goods can be sold

at reasonable rate (Chapman, Hopwood and Shields, 2011). Fund Flow Analysis: This analysis find out the movement of fund from one period to

another. Moreover, this analysis is very useful to know whether the fund is properly used

or not in a year when compared to the previous year. The Working capital changes and

funds from operation are also find out through this analysis. Standard Costing: It is predetermined cost. It provide yardstick for measuring actual

performance. It is used to find reasons in deviation if any in cost accounting (Gesimba,

Alvar and Mante, 2014). Marginal Costing: It is used to fixed the selling price, Selection of best sales mix, best

use of scarce raw material and resources, to take a decision whether to buy or to make a

product. Purchase or reject bulk order. This is based on fixed, variable and contribution in

business (Hult, Craighead and Ketchen Jr, 2010). Budgetary Control: Future financial needs are determined under this tools. It is used to

control financial performance of business. Business operations are directed in desired

direction.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Revaluation Accounting: Fixed assets are revalued as per revaluation accounting so that

capital is fairly represented with assets value. It helps in finding out fair value of capital

employed. Historical Cost Accounting: It means cost are recorded after being incurred it can be

used for predetermined cost to evaluate performance (Łukaszewski and Wilk, 2016).

Statistical Tools: To solve management problems various tools of statistics are used like

method of least square, regression, quality control etc.

P2) Management accounting methods

There are several methods applied for effective management accounting including cost

analysis, budgeting, performance measurement, project decision making and so on. Therefore,

some of the management accounting tools and techniques can be described as below:- Cost analysis:- Management accounting of Nisa Ltd determines costing to prepare

income statement. On the basis of which, financial position of organization is presented

therefore several ideas are created for enhancing its profit earning capacity same as

creating balance between incurred expenses and gained income (Malhotra and Temponi,

2010). In this regard, different costing methods are used such as; marginal, absorption,

demand based, competition basis etc. Therefore, analysis of cost is interrelated with

balance of production and distribution of goods. Moreover, fluctuations in market

demand affects pricing strategies in increasing in demand effects on productivity

positively. On the other hand, decreasing in demand reflects production and supplement

of goods negatively. Thus, cost analysis is effective for fund allocation and creating

balance between expenses and income of the organization. Performance measurement:- As management accounting is multidisciplinary approach

in which employees performance analyzed that creates several ideas for enhancing their

working efficiencies. However, it is useful for improving their skills such as

communication, problem solving, listening and working in group. It influences personal

and professional development of entity. In addition to this, performance of employees

and organization get managed effectively. Hence, performance evaluation is great

technique of management accounting that is interrelated with organization's effectiveness.

5

capital is fairly represented with assets value. It helps in finding out fair value of capital

employed. Historical Cost Accounting: It means cost are recorded after being incurred it can be

used for predetermined cost to evaluate performance (Łukaszewski and Wilk, 2016).

Statistical Tools: To solve management problems various tools of statistics are used like

method of least square, regression, quality control etc.

P2) Management accounting methods

There are several methods applied for effective management accounting including cost

analysis, budgeting, performance measurement, project decision making and so on. Therefore,

some of the management accounting tools and techniques can be described as below:- Cost analysis:- Management accounting of Nisa Ltd determines costing to prepare

income statement. On the basis of which, financial position of organization is presented

therefore several ideas are created for enhancing its profit earning capacity same as

creating balance between incurred expenses and gained income (Malhotra and Temponi,

2010). In this regard, different costing methods are used such as; marginal, absorption,

demand based, competition basis etc. Therefore, analysis of cost is interrelated with

balance of production and distribution of goods. Moreover, fluctuations in market

demand affects pricing strategies in increasing in demand effects on productivity

positively. On the other hand, decreasing in demand reflects production and supplement

of goods negatively. Thus, cost analysis is effective for fund allocation and creating

balance between expenses and income of the organization. Performance measurement:- As management accounting is multidisciplinary approach

in which employees performance analyzed that creates several ideas for enhancing their

working efficiencies. However, it is useful for improving their skills such as

communication, problem solving, listening and working in group. It influences personal

and professional development of entity. In addition to this, performance of employees

and organization get managed effectively. Hence, performance evaluation is great

technique of management accounting that is interrelated with organization's effectiveness.

5

In this process, performance management is obtained through using this tool (Malhotra

and Temponi, 2010). Project decision making:- Under this system, management accountant of Nisa Ltd

accomplishes tasks through decision making for projecting. It includes estimation for cost

incurred and forecasting time to be spend on projection. In accordance to this, decision

making process is implemented for effective project planning and scheduling to reach out

set target. It is useful for best use of resources and fund that impacts on productivity and

profitability of entity (Shelby, 2013). Therefore, projecting relating to effectiveness of

organization and increasing its quality services is possible through using management

accounting tools adequately. In this regard, management accounting is helpful to succeed

any project through effective forecasting and decision making process. It involves entire

elements that project accomplishment such as cost, time and quality used for projecting. Planning and budgeting:- Management accountant of Nisa Ltd analyzes entire business

operations and further prepares strategic plans for effectiveness of organization. In this

regard, according to critical evaluation of overall activities, decisions are made for

enhancing quality services and valuable market position that affects long term

sustainability. However, planning is prepared for short term as well long term periodicity.

Including this, it is considered that several ideas are created for optimum utilization of

resources and fund. It affects productivity and profitability of organization for making

decisions regarding business operations. Therefore, adequate production and distribution

of goods can be gained through budget process system. Along with this, management

accountant of entity recognizes all factors such as finance, production, risk management,

marketing and sales. Thus, attractive organizational structure is created through this tool.

In this process, planning including forecasting and decision making is implemented by

preparing budget (Swayne, Duncan and Ginter, 2012). Financial management analysis:- There are various financial tools such as income

statement, balance sheet, profit and loss account, cash flow and fund flow statement.

Thus, by identifying these sources, several tools and techniques are presented that is

useful for fund allocation as well resource management. Hence, management accounting

as financial statement analysis is one of the great component for economic stability and

6

and Temponi, 2010). Project decision making:- Under this system, management accountant of Nisa Ltd

accomplishes tasks through decision making for projecting. It includes estimation for cost

incurred and forecasting time to be spend on projection. In accordance to this, decision

making process is implemented for effective project planning and scheduling to reach out

set target. It is useful for best use of resources and fund that impacts on productivity and

profitability of entity (Shelby, 2013). Therefore, projecting relating to effectiveness of

organization and increasing its quality services is possible through using management

accounting tools adequately. In this regard, management accounting is helpful to succeed

any project through effective forecasting and decision making process. It involves entire

elements that project accomplishment such as cost, time and quality used for projecting. Planning and budgeting:- Management accountant of Nisa Ltd analyzes entire business

operations and further prepares strategic plans for effectiveness of organization. In this

regard, according to critical evaluation of overall activities, decisions are made for

enhancing quality services and valuable market position that affects long term

sustainability. However, planning is prepared for short term as well long term periodicity.

Including this, it is considered that several ideas are created for optimum utilization of

resources and fund. It affects productivity and profitability of organization for making

decisions regarding business operations. Therefore, adequate production and distribution

of goods can be gained through budget process system. Along with this, management

accountant of entity recognizes all factors such as finance, production, risk management,

marketing and sales. Thus, attractive organizational structure is created through this tool.

In this process, planning including forecasting and decision making is implemented by

preparing budget (Swayne, Duncan and Ginter, 2012). Financial management analysis:- There are various financial tools such as income

statement, balance sheet, profit and loss account, cash flow and fund flow statement.

Thus, by identifying these sources, several tools and techniques are presented that is

useful for fund allocation as well resource management. Hence, management accounting

as financial statement analysis is one of the great component for economic stability and

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

increasing profit earning capacity of organization. It is key element for financial

management and operating further business activities. Including this, it is useful for

economic stability and creating balance between incurred expenses and gained revenue

that affects productivity and profitability of small scale enterprise. In accordance to this,

management accounting is useful to present monetary structure and systematic evaluation

of entity at high level (Talke, Salomo and Rost, 2010). Therefore, various tools and

techniques are obtained for enhancing financial position that is interrelated with other

departments' performance including production of goods, efficient fund and resources for

business operations and so on. However, financial statement analysis is one of the great

tool for enlargement of Nisa Ltd and increasing its quality services for organization's

effectiveness. Statistical techniques:- Management accounting tool as statistical techniques including

mean, mode and median that is valuable to reduce problem occur at workplace. In this

process, actual performance of business organization is obtained that presents

quantitative methods for determining problems and solving out issues. Thus, forecasting

and taking decisions for further business operations. It is useful for effectiveness of small

business unit and enhancing its quality services for long term sustainability in market.

Under this system, different techniques are applied that is affected with production and

supplement of goods. However, statistical techniques are bases for estimation and

forecasting regarding business operations. Including this, mathematics and specific

calculation for further implementation (Angelakis, Theriou and Floropoulos, 2010).

Under this system, linear programming, regression method and data analysis is obtained

for recognizing actual business performance as well making decisions for enlargement of

small business unit. In this process, applying statistical tools and techniques is useful to

allocate resources and fund efficiently. Therefore, mathematical calculation and critical

analysis on organization's structure is created as per which varieties of ideas are

generated regarding market efficiency and increasing in demand for goods. Hence,

management accounting tool as statistical technique is useful to present current business

performance and managing systematic business operations at large scale.

7

management and operating further business activities. Including this, it is useful for

economic stability and creating balance between incurred expenses and gained revenue

that affects productivity and profitability of small scale enterprise. In accordance to this,

management accounting is useful to present monetary structure and systematic evaluation

of entity at high level (Talke, Salomo and Rost, 2010). Therefore, various tools and

techniques are obtained for enhancing financial position that is interrelated with other

departments' performance including production of goods, efficient fund and resources for

business operations and so on. However, financial statement analysis is one of the great

tool for enlargement of Nisa Ltd and increasing its quality services for organization's

effectiveness. Statistical techniques:- Management accounting tool as statistical techniques including

mean, mode and median that is valuable to reduce problem occur at workplace. In this

process, actual performance of business organization is obtained that presents

quantitative methods for determining problems and solving out issues. Thus, forecasting

and taking decisions for further business operations. It is useful for effectiveness of small

business unit and enhancing its quality services for long term sustainability in market.

Under this system, different techniques are applied that is affected with production and

supplement of goods. However, statistical techniques are bases for estimation and

forecasting regarding business operations. Including this, mathematics and specific

calculation for further implementation (Angelakis, Theriou and Floropoulos, 2010).

Under this system, linear programming, regression method and data analysis is obtained

for recognizing actual business performance as well making decisions for enlargement of

small business unit. In this process, applying statistical tools and techniques is useful to

allocate resources and fund efficiently. Therefore, mathematical calculation and critical

analysis on organization's structure is created as per which varieties of ideas are

generated regarding market efficiency and increasing in demand for goods. Hence,

management accounting tool as statistical technique is useful to present current business

performance and managing systematic business operations at large scale.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Management reporting:- Accounting and management reports are prepared to present

actual business performance and further making decisions on the basis of recognition of

recorded data. In this process, different reports are recorded including financial

statements such as balance sheet, income statement, profit and loss account and so on.

Therefore, management reporting is element to determine actual organization

performance and enhancing quality services for effectiveness of firm. However,

accounting reports including purchase and sales account as well income expenditure

statement that affects market position of entity. In this regard, reporting for accounting in

the form of finance, production and distribution of goods are obtained (Bowen, Call and

Rajgopal, 2010). It is interrelated with expansion of entity and increasing its efficiencies

at high level. Auditing of financial statements affects financial performance and

production system of firm. Thus, management reporting is useful to keeping records of

business operations as well creating innovations for their enhancement. It is interrelated

with developing interest of customers towards goods and services of small business

entity.

Hence, above mentioned management accounting methods are interlinked with

management of overall business operations. Including this, expansion of Nisa Ltd and its quality

services can be enhanced at high level for making place to sustain company's good reputation for

long term period. It is related to forecasting and decision making for further business operations.

For example; production and distribution of groceries and performance of entity including

planning to operate business activities is created by which several tools are used for decision-

making and enhancing quality services of entity. Therefore, management accounting components

are related to enlargement of small business enterprise and increasing its profit earning to

carrying out business entity efficiently. In this process, entire activities of business organization

get managed for utilizing raw material used in production system same as enhancing its

efficiency for long term sustainability (Cadez and Guilding, 2012).

TASK 2

P3) Different costing methods and differences between marginal and absorption costing

Costing also terms as pricing is considered as key tool for determining cost of goods and

services to be produced. Further, by analyzing price of product, income statement is prepared

8

actual business performance and further making decisions on the basis of recognition of

recorded data. In this process, different reports are recorded including financial

statements such as balance sheet, income statement, profit and loss account and so on.

Therefore, management reporting is element to determine actual organization

performance and enhancing quality services for effectiveness of firm. However,

accounting reports including purchase and sales account as well income expenditure

statement that affects market position of entity. In this regard, reporting for accounting in

the form of finance, production and distribution of goods are obtained (Bowen, Call and

Rajgopal, 2010). It is interrelated with expansion of entity and increasing its efficiencies

at high level. Auditing of financial statements affects financial performance and

production system of firm. Thus, management reporting is useful to keeping records of

business operations as well creating innovations for their enhancement. It is interrelated

with developing interest of customers towards goods and services of small business

entity.

Hence, above mentioned management accounting methods are interlinked with

management of overall business operations. Including this, expansion of Nisa Ltd and its quality

services can be enhanced at high level for making place to sustain company's good reputation for

long term period. It is related to forecasting and decision making for further business operations.

For example; production and distribution of groceries and performance of entity including

planning to operate business activities is created by which several tools are used for decision-

making and enhancing quality services of entity. Therefore, management accounting components

are related to enlargement of small business enterprise and increasing its profit earning to

carrying out business entity efficiently. In this process, entire activities of business organization

get managed for utilizing raw material used in production system same as enhancing its

efficiency for long term sustainability (Cadez and Guilding, 2012).

TASK 2

P3) Different costing methods and differences between marginal and absorption costing

Costing also terms as pricing is considered as key tool for determining cost of goods and

services to be produced. Further, by analyzing price of product, income statement is prepared

8

that presents financial performance of Nisa Ltd. In this regard, various methods are used for

price determination and also to increase economic profile of entity. It is obtained as base for fund

allocation and manner for financial management of small business enterprise. In this regard,

several tools and techniques are applied for costing methods and making decisions for short term

as well long time periodicity. In addition to this, applying costing methods are benefited for

setting price of products according to cost incurred manufacturing and production of goods

including advertising for grocery items (Englund and Gerdin, 2011). However, costing is a

technique for preparing income statements that generates ideas related to creating balance

between expenditure and revenue. Thus, through costing method, market position, earning

capacity and estimations are obtained for making decisions regarding financial position and other

sectors' performance. Therefore, costing methods as marginal and absorption can be expressed as

follows that affects production and return on this process. However, management accountant of

Nisa Ltd analyses marginal and absorption as following to prepare income statement for

presenting entity's actual business performance such as:-

Marginal costing:- Under this costing method, decisions take on the basis of cost of

goods. In this process, different techniques are used for determining price and income statement

preparation. However, profit earning tools are presented for decision making regarding further

business operations. Including this, it is determined that if sales price is greater than marginal

cost then process system is profitable. While, on the other hand, if sales price is lower than

marginal cost then it will not be in favor of organization's effectiveness. Marginal cost is

evaluated through following formula as;-

Marginal Cost (MC) = change is cost (C)\change is quantity (Q)

In this process, cost incurred in production process is divided by changes in quantity

used therefore cost per unit is determined. It creates several ideas for further production and

distribution of goods and services. However, decisions are made on the basis of marginal costing

for investment related to business operations. In this process, fixed expenses are not added to

variable for deducting with gross profit. In accordance to this, cost incurred in production system

including purchasing raw material and prices incurred in production of goods are analyzed. On

9

price determination and also to increase economic profile of entity. It is obtained as base for fund

allocation and manner for financial management of small business enterprise. In this regard,

several tools and techniques are applied for costing methods and making decisions for short term

as well long time periodicity. In addition to this, applying costing methods are benefited for

setting price of products according to cost incurred manufacturing and production of goods

including advertising for grocery items (Englund and Gerdin, 2011). However, costing is a

technique for preparing income statements that generates ideas related to creating balance

between expenditure and revenue. Thus, through costing method, market position, earning

capacity and estimations are obtained for making decisions regarding financial position and other

sectors' performance. Therefore, costing methods as marginal and absorption can be expressed as

follows that affects production and return on this process. However, management accountant of

Nisa Ltd analyses marginal and absorption as following to prepare income statement for

presenting entity's actual business performance such as:-

Marginal costing:- Under this costing method, decisions take on the basis of cost of

goods. In this process, different techniques are used for determining price and income statement

preparation. However, profit earning tools are presented for decision making regarding further

business operations. Including this, it is determined that if sales price is greater than marginal

cost then process system is profitable. While, on the other hand, if sales price is lower than

marginal cost then it will not be in favor of organization's effectiveness. Marginal cost is

evaluated through following formula as;-

Marginal Cost (MC) = change is cost (C)\change is quantity (Q)

In this process, cost incurred in production process is divided by changes in quantity

used therefore cost per unit is determined. It creates several ideas for further production and

distribution of goods and services. However, decisions are made on the basis of marginal costing

for investment related to business operations. In this process, fixed expenses are not added to

variable for deducting with gross profit. In accordance to this, cost incurred in production system

including purchasing raw material and prices incurred in production of goods are analyzed. On

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

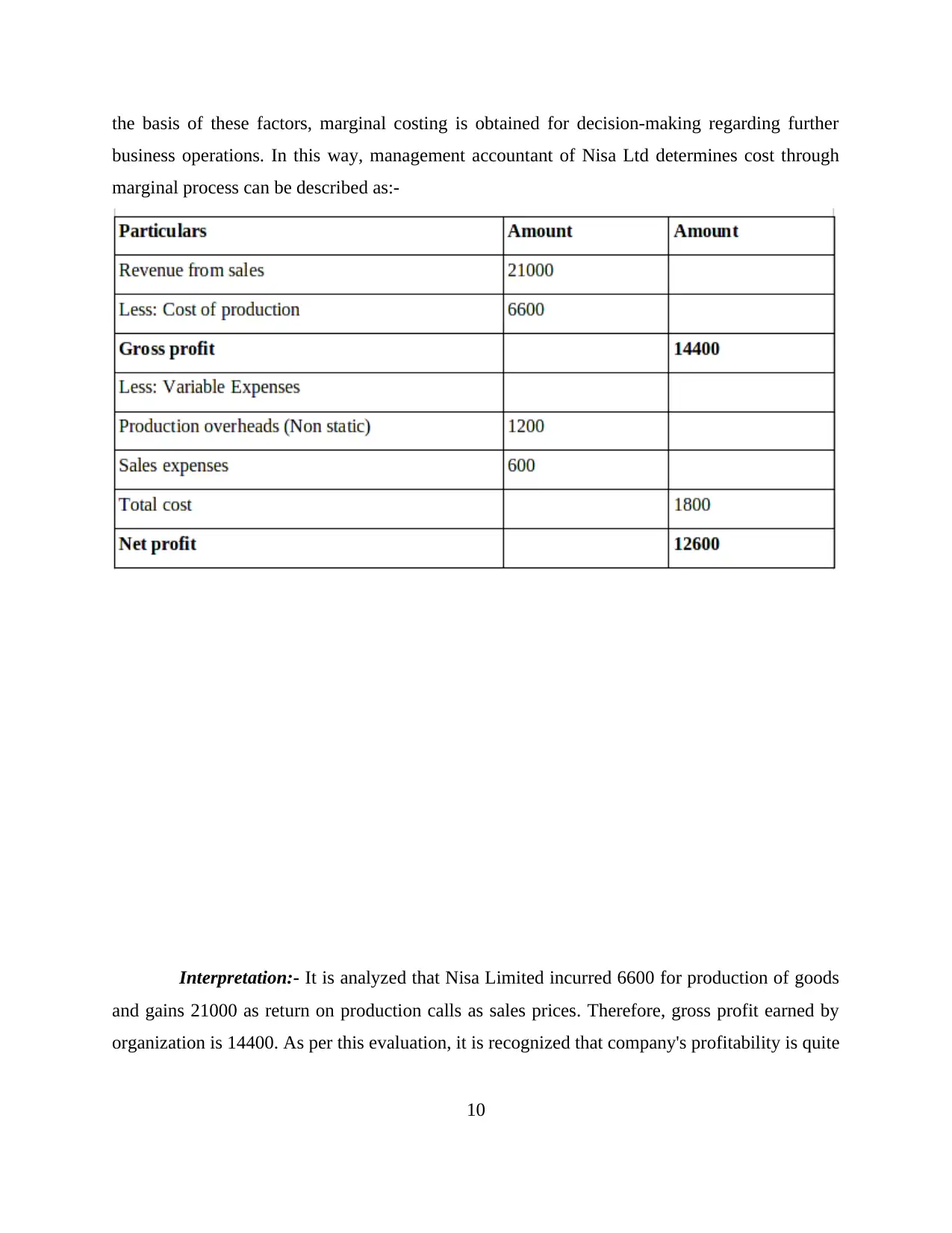

the basis of these factors, marginal costing is obtained for decision-making regarding further

business operations. In this way, management accountant of Nisa Ltd determines cost through

marginal process can be described as:-

Interpretation:- It is analyzed that Nisa Limited incurred 6600 for production of goods

and gains 21000 as return on production calls as sales prices. Therefore, gross profit earned by

organization is 14400. As per this evaluation, it is recognized that company's profitability is quite

10

business operations. In this way, management accountant of Nisa Ltd determines cost through

marginal process can be described as:-

Interpretation:- It is analyzed that Nisa Limited incurred 6600 for production of goods

and gains 21000 as return on production calls as sales prices. Therefore, gross profit earned by

organization is 14400. As per this evaluation, it is recognized that company's profitability is quite

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

well and in future time, it can be enhanced at high level. However, for measuring net profit gross

profit is deducted with cost incurred in spending for production of goods. In this process, total

cost expenses is obtained as 1800. Thus, net profit incurred by company is 12600. According to

this profitability, it can be foretasted that in further years, Nisa Ltd can invent fund at high level

for adequate production and distribution of groceries. However, profit earning capacity of

organization can be enhanced that impacts on productivity and profitability of firm.

Absorption costing:- Through this costing method, decisions are made for further investment on

business operations. In this process, this tool is valuable for long term planning strategies.

However, under this system, costing for further implementation regarding long term periodicity

is obtained for enhancing its profitability at high level. In addition to this, for absorption costing,

direct and indirect expenditures. It is valuable for long term decision making that is helpful for

long term sustainability of organization effectively (Cadez and Guilding, 2012). In this regard,g

into account indirect expenses (overheads) as well as direct costs. management accountant of

Nisa Ltd evaluates following data interpretation regarding decision making for further business

operations as:-

11

profit is deducted with cost incurred in spending for production of goods. In this process, total

cost expenses is obtained as 1800. Thus, net profit incurred by company is 12600. According to

this profitability, it can be foretasted that in further years, Nisa Ltd can invent fund at high level

for adequate production and distribution of groceries. However, profit earning capacity of

organization can be enhanced that impacts on productivity and profitability of firm.

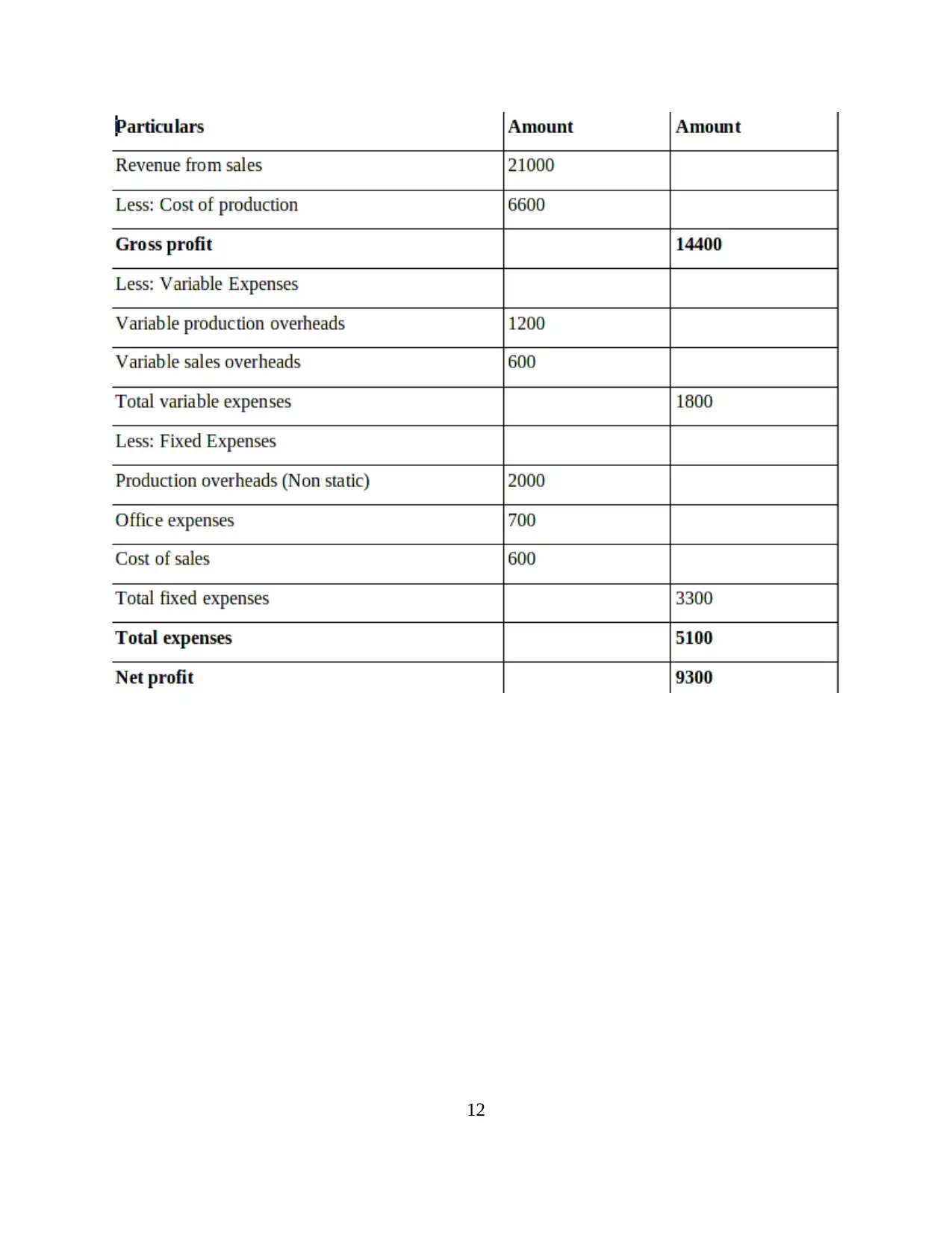

Absorption costing:- Through this costing method, decisions are made for further investment on

business operations. In this process, this tool is valuable for long term planning strategies.

However, under this system, costing for further implementation regarding long term periodicity

is obtained for enhancing its profitability at high level. In addition to this, for absorption costing,

direct and indirect expenditures. It is valuable for long term decision making that is helpful for

long term sustainability of organization effectively (Cadez and Guilding, 2012). In this regard,g

into account indirect expenses (overheads) as well as direct costs. management accountant of

Nisa Ltd evaluates following data interpretation regarding decision making for further business

operations as:-

11

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 24

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.