Analysis of Strategic Management in Nonprofit Organizations (MGMT)

VerifiedAdded on 2020/04/21

|13

|3208

|141

Report

AI Summary

This report delves into the realm of strategic management within nonprofit organizations, examining critical aspects such as their tax-exempt status, ownership structures, and diverse funding sources. The research investigates the methods employed by these organizations to manage financial records, highlighting key differences from for-profit entities. The report explores the utilization of assets, emphasizing the importance of careful financial handling due to limited resources, and the role of the Balanced Scorecard in performance measurement. Additionally, it covers the administration of budgetary records and the literature review comparing and contrasting nonprofit and for-profit entities. The findings are based on a quantitative research approach, utilizing surveys to gather insights from nonprofit managers, shedding light on the core missions and objectives of nonprofit organizations and their approaches to strategic management.

STRATEGIC MANAGEMENT IN NON-PROFIT ORGANIZATIONS

November 15, 2017

November 15, 2017

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

M A N A G E M E N T I N N O N P R O F I T O R G A N I Z A T I O N S P a g e | 2

Table of Contents

Introduction................................................................................................................................................3

Research Questions................................................................................................................................4

Research Method Used...........................................................................................................................4

Findings.......................................................................................................................................................5

Discussion...............................................................................................................................................6

Utilization of Assets................................................................................................................................7

Administration of Budgetary Records....................................................................................................8

Literature Review........................................................................................................................................9

Conclusion: Final View..........................................................................................................................11

References................................................................................................................................................12

Table of Contents

Introduction................................................................................................................................................3

Research Questions................................................................................................................................4

Research Method Used...........................................................................................................................4

Findings.......................................................................................................................................................5

Discussion...............................................................................................................................................6

Utilization of Assets................................................................................................................................7

Administration of Budgetary Records....................................................................................................8

Literature Review........................................................................................................................................9

Conclusion: Final View..........................................................................................................................11

References................................................................................................................................................12

M A N A G E M E N T I N N O N P R O F I T O R G A N I Z A T I O N S P a g e | 3

Introduction

A nonprofit association is a partnership or an affiliation that does business for the advantage of

the overall population without investors and a benefit thought process. There are monstrous

group benefits as a not-for-profit and acknowledges everybody paying little respect to capacity

to pay. Nonprofit organizations are approved to assess excluded status which causes them to

give services to people in general and are relied upon to be powerful bosses of their finances

and also to be proficient. In doing as such, they can pick up exclusions from the government,

and state wages assessments as well as request deductible charge commitments (Adeolu &

Afolabi, 2010).

According to Ahmed & Mohamed (2017), the subject of responsibility on accounts and

financing as well as performance measurement has turned out to be earnest for nonprofit

organizations as they experience expanding rivalry from a multiplying number of offices, all

contending for the rare benefactor, establishment, and government financing. However, the

general population execution reports and numerous interior execution estimation frameworks

of these organizations concentrate just on money-related measures, for example, gifts,

consumptions, and working cost proportions. Accomplishment for nonprofits ought to be

Nonprofit

organization

Cash flow

management

Cash

Management

Plan

Different

funding

sources

Planning for

new projects

Accomplish

more

projects

Keep

employees and

hire more

Introduction

A nonprofit association is a partnership or an affiliation that does business for the advantage of

the overall population without investors and a benefit thought process. There are monstrous

group benefits as a not-for-profit and acknowledges everybody paying little respect to capacity

to pay. Nonprofit organizations are approved to assess excluded status which causes them to

give services to people in general and are relied upon to be powerful bosses of their finances

and also to be proficient. In doing as such, they can pick up exclusions from the government,

and state wages assessments as well as request deductible charge commitments (Adeolu &

Afolabi, 2010).

According to Ahmed & Mohamed (2017), the subject of responsibility on accounts and

financing as well as performance measurement has turned out to be earnest for nonprofit

organizations as they experience expanding rivalry from a multiplying number of offices, all

contending for the rare benefactor, establishment, and government financing. However, the

general population execution reports and numerous interior execution estimation frameworks

of these organizations concentrate just on money-related measures, for example, gifts,

consumptions, and working cost proportions. Accomplishment for nonprofits ought to be

Nonprofit

organization

Cash flow

management

Cash

Management

Plan

Different

funding

sources

Planning for

new projects

Accomplish

more

projects

Keep

employees and

hire more

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

M A N A G E M E N T I N N O N P R O F I T O R G A N I Z A T I O N S P a g e | 4

measured by how successfully and productively they address the issues of their voting

demographics. Monetary contemplations can play an empowering or obliging part; however,

will once in a while be the essential target. At the smaller scale, automatic level, organizations

may have heap measures to track and control nearby activities. These measures, in any case,

don't identify with general authoritative mission and targets (Alfonso et al., 2010).

Research Questions

1) Are nonprofit organizations tax-exempt?

2) What is the ownership structure of nonprofit organizations?

3) What is the source of funds for nonprofit organizations?

4) How are financial records managed by a nonprofit organization?

5) Why do nonprofit organizations exist?

Research Method Used

In this part, the examination system utilized as a bit of the examination is described. The

geological area where the examination was driven, the examination plan and the general

population and test are portrayed. A quantitative approach was taken after. Ansgar & Diana

(2011) portray quantitative research as a formal, objective, strategic to delineate and test

affiliations in addition to exploring conditions and the last-item relationship among factors.

Reviews might be utilized for outlines, valuable and exploratory research. An expressive

examination setup was utilized. Moreover, a survey is utilized to collect exceptional information

for delineating expansive people, particularly making it difficult to watch.

measured by how successfully and productively they address the issues of their voting

demographics. Monetary contemplations can play an empowering or obliging part; however,

will once in a while be the essential target. At the smaller scale, automatic level, organizations

may have heap measures to track and control nearby activities. These measures, in any case,

don't identify with general authoritative mission and targets (Alfonso et al., 2010).

Research Questions

1) Are nonprofit organizations tax-exempt?

2) What is the ownership structure of nonprofit organizations?

3) What is the source of funds for nonprofit organizations?

4) How are financial records managed by a nonprofit organization?

5) Why do nonprofit organizations exist?

Research Method Used

In this part, the examination system utilized as a bit of the examination is described. The

geological area where the examination was driven, the examination plan and the general

population and test are portrayed. A quantitative approach was taken after. Ansgar & Diana

(2011) portray quantitative research as a formal, objective, strategic to delineate and test

affiliations in addition to exploring conditions and the last-item relationship among factors.

Reviews might be utilized for outlines, valuable and exploratory research. An expressive

examination setup was utilized. Moreover, a survey is utilized to collect exceptional information

for delineating expansive people, particularly making it difficult to watch.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

M A N A G E M E N T I N N O N P R O F I T O R G A N I Z A T I O N S P a g e | 5

A framework gets data from a case of individuals by procedures for self-report, that is, the

general public reacts to a development of demand postured by the specialist. In this

examination, the data was gathered through independently directed studies scattered

inevitably to the subjects by the examiner. The review was picked since it gives a right depiction

or record of the qualities, for instance, lead, suppositions, points of confinement, sentiments,

and information of a specific individual, condition or gathering. This chart has met the targets of

the examination, to be specific to pick the learning and perspectives of respondents concerning

the administration.

Findings

Information was acquired from self-controlled reviews or surveys, wrapped up by 32 directors

(n=32), a 43% reaction rate; enduring that single portion of the aggregate masses of 394

supervisors in various organizations may provoke an honest to a good conclusion. The way

additionally upholds this that a little fragment of the pros in this present business has non-

administrative posts, for instance, they might be secured with supervisory.

A total of 22 reviews was gotten, in any case, only 93 surveys were usable for this examination

and met the required joining criteria as talked about in the previous part. This tended to 43% of

A framework gets data from a case of individuals by procedures for self-report, that is, the

general public reacts to a development of demand postured by the specialist. In this

examination, the data was gathered through independently directed studies scattered

inevitably to the subjects by the examiner. The review was picked since it gives a right depiction

or record of the qualities, for instance, lead, suppositions, points of confinement, sentiments,

and information of a specific individual, condition or gathering. This chart has met the targets of

the examination, to be specific to pick the learning and perspectives of respondents concerning

the administration.

Findings

Information was acquired from self-controlled reviews or surveys, wrapped up by 32 directors

(n=32), a 43% reaction rate; enduring that single portion of the aggregate masses of 394

supervisors in various organizations may provoke an honest to a good conclusion. The way

additionally upholds this that a little fragment of the pros in this present business has non-

administrative posts, for instance, they might be secured with supervisory.

A total of 22 reviews was gotten, in any case, only 93 surveys were usable for this examination

and met the required joining criteria as talked about in the previous part. This tended to 43% of

M A N A G E M E N T I N N O N P R O F I T O R G A N I Z A T I O N S P a g e | 6

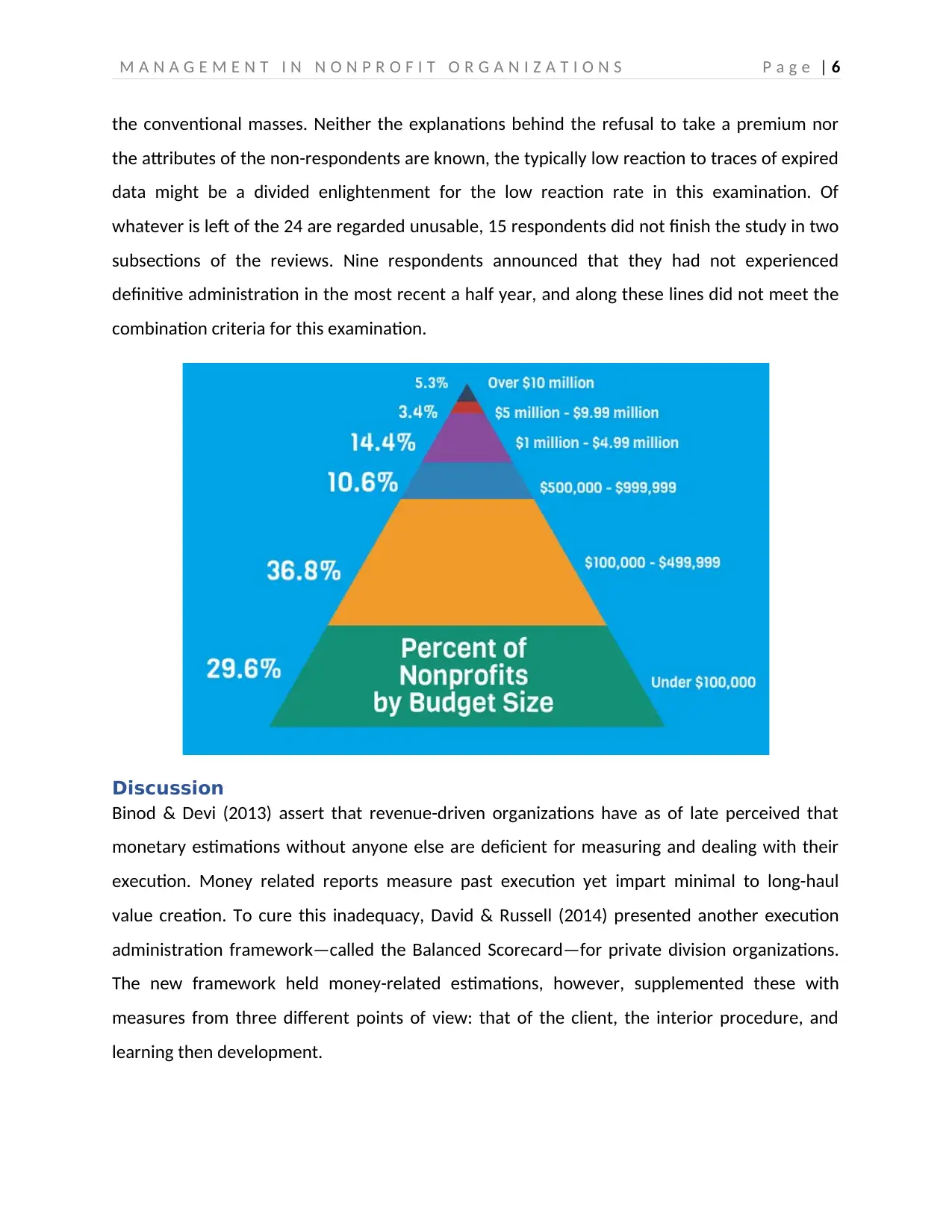

the conventional masses. Neither the explanations behind the refusal to take a premium nor

the attributes of the non-respondents are known, the typically low reaction to traces of expired

data might be a divided enlightenment for the low reaction rate in this examination. Of

whatever is left of the 24 are regarded unusable, 15 respondents did not finish the study in two

subsections of the reviews. Nine respondents announced that they had not experienced

definitive administration in the most recent a half year, and along these lines did not meet the

combination criteria for this examination.

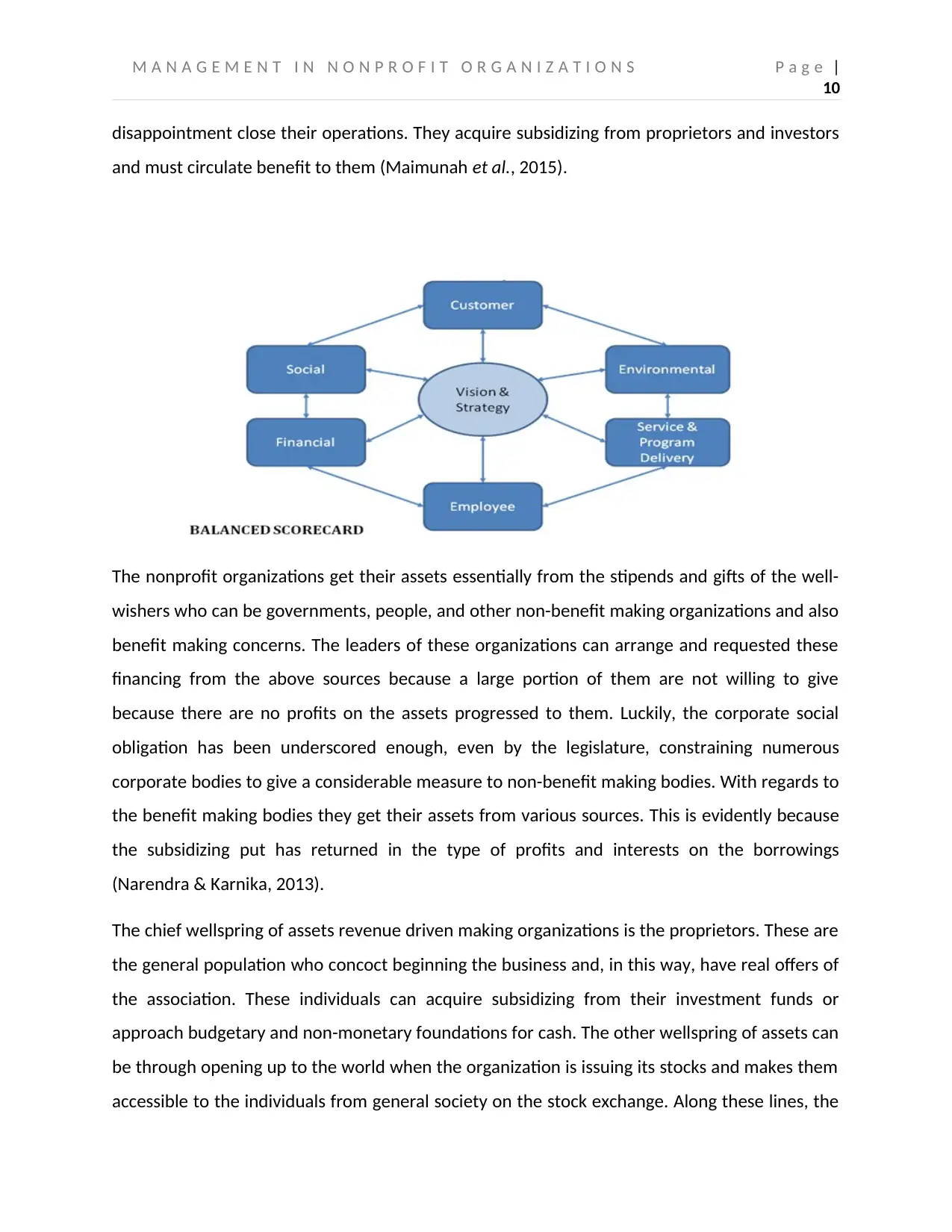

Discussion

Binod & Devi (2013) assert that revenue-driven organizations have as of late perceived that

monetary estimations without anyone else are deficient for measuring and dealing with their

execution. Money related reports measure past execution yet impart minimal to long-haul

value creation. To cure this inadequacy, David & Russell (2014) presented another execution

administration framework—called the Balanced Scorecard—for private division organizations.

The new framework held money-related estimations, however, supplemented these with

measures from three different points of view: that of the client, the interior procedure, and

learning then development.

the conventional masses. Neither the explanations behind the refusal to take a premium nor

the attributes of the non-respondents are known, the typically low reaction to traces of expired

data might be a divided enlightenment for the low reaction rate in this examination. Of

whatever is left of the 24 are regarded unusable, 15 respondents did not finish the study in two

subsections of the reviews. Nine respondents announced that they had not experienced

definitive administration in the most recent a half year, and along these lines did not meet the

combination criteria for this examination.

Discussion

Binod & Devi (2013) assert that revenue-driven organizations have as of late perceived that

monetary estimations without anyone else are deficient for measuring and dealing with their

execution. Money related reports measure past execution yet impart minimal to long-haul

value creation. To cure this inadequacy, David & Russell (2014) presented another execution

administration framework—called the Balanced Scorecard—for private division organizations.

The new framework held money-related estimations, however, supplemented these with

measures from three different points of view: that of the client, the interior procedure, and

learning then development.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

M A N A G E M E N T I N N O N P R O F I T O R G A N I Z A T I O N S P a g e | 7

The underlying concentration and utilization of the Balanced Scorecard were in the revenue

driven private sector. In any case, the open door for the scorecard to enhance the

administration of nonprofits ought to be significantly more prominent. Revenue driven looking

for partnerships, the money related point of view gives a reasonable long-run objective, yet it

gives a requirement instead of a goal for nonprofits. Despite the fact that these organizations

should unquestionably monitor what they are going through and follow budgetary spending

plans, their prosperity cannot be measured by how intently they continue spending to planned

sums. Regardless of the possibility that they control spending with the goal that real costs are

kept well beneath planned sums (Elaine & Dawn, 2011).

Utilization of Assets

This is another vital zone of distinction amongst benefit and nonprofit organizations. Rather

than benefit making organizations, they utilize their cash, most importantly, to compensate

their staff group to persuade them. They likewise utilize their assets to grow their operations by

opening new product offerings through securing of new hardware and gear; to open new

branches and operations in different regions and districts. Non-benefit influencing

organizations to utilize their assets for the most part by giving fundamental products and

enterprises to the general population, and the exercises that they were set up to embrace.

These organizations are extremely cautious in the way they handle their finances since they

The underlying concentration and utilization of the Balanced Scorecard were in the revenue

driven private sector. In any case, the open door for the scorecard to enhance the

administration of nonprofits ought to be significantly more prominent. Revenue driven looking

for partnerships, the money related point of view gives a reasonable long-run objective, yet it

gives a requirement instead of a goal for nonprofits. Despite the fact that these organizations

should unquestionably monitor what they are going through and follow budgetary spending

plans, their prosperity cannot be measured by how intently they continue spending to planned

sums. Regardless of the possibility that they control spending with the goal that real costs are

kept well beneath planned sums (Elaine & Dawn, 2011).

Utilization of Assets

This is another vital zone of distinction amongst benefit and nonprofit organizations. Rather

than benefit making organizations, they utilize their cash, most importantly, to compensate

their staff group to persuade them. They likewise utilize their assets to grow their operations by

opening new product offerings through securing of new hardware and gear; to open new

branches and operations in different regions and districts. Non-benefit influencing

organizations to utilize their assets for the most part by giving fundamental products and

enterprises to the general population, and the exercises that they were set up to embrace.

These organizations are extremely cautious in the way they handle their finances since they

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

M A N A G E M E N T I N N O N P R O F I T O R G A N I Z A T I O N S P a g e | 8

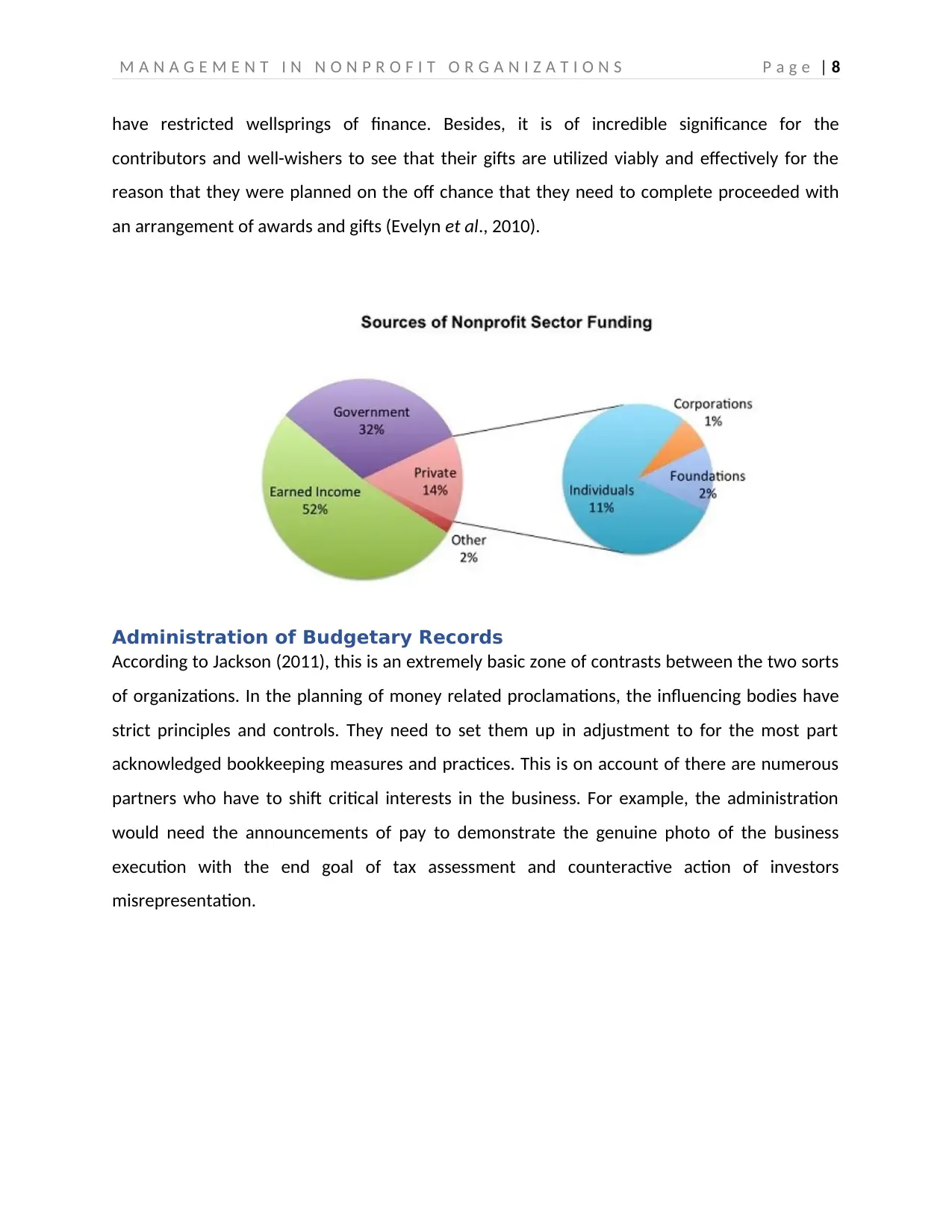

have restricted wellsprings of finance. Besides, it is of incredible significance for the

contributors and well-wishers to see that their gifts are utilized viably and effectively for the

reason that they were planned on the off chance that they need to complete proceeded with

an arrangement of awards and gifts (Evelyn et al., 2010).

Administration of Budgetary Records

According to Jackson (2011), this is an extremely basic zone of contrasts between the two sorts

of organizations. In the planning of money related proclamations, the influencing bodies have

strict principles and controls. They need to set them up in adjustment to for the most part

acknowledged bookkeeping measures and practices. This is on account of there are numerous

partners who have to shift critical interests in the business. For example, the administration

would need the announcements of pay to demonstrate the genuine photo of the business

execution with the end goal of tax assessment and counteractive action of investors

misrepresentation.

have restricted wellsprings of finance. Besides, it is of incredible significance for the

contributors and well-wishers to see that their gifts are utilized viably and effectively for the

reason that they were planned on the off chance that they need to complete proceeded with

an arrangement of awards and gifts (Evelyn et al., 2010).

Administration of Budgetary Records

According to Jackson (2011), this is an extremely basic zone of contrasts between the two sorts

of organizations. In the planning of money related proclamations, the influencing bodies have

strict principles and controls. They need to set them up in adjustment to for the most part

acknowledged bookkeeping measures and practices. This is on account of there are numerous

partners who have to shift critical interests in the business. For example, the administration

would need the announcements of pay to demonstrate the genuine photo of the business

execution with the end goal of tax assessment and counteractive action of investors

misrepresentation.

M A N A G E M E N T I N N O N P R O F I T O R G A N I Z A T I O N S P a g e | 9

The investors have premiums in the business detailing that the business can pay them the

arrival on their put subsidizes as reasonable profits on their shareholdings. Their budgetary

proclamations must be reviewed completely by government examiners to guarantee

straightforwardness and responsibility. With regards to nonprofit organizations, their budgetary

reports are likewise examined yet they have less weight and desire since are for the most part

to fulfill the contributors and well-wishers that their assets are appropriately misused by the

association. It ought to be noticed that, there are set up bookkeeping and announcing

guidelines for the non-benefit organizations to guarantee consistency in the way budgetary

reports are readied (Madia, 2011).

Literature Review

The main purpose of thought is surely the reason behind which every association flourishes.

The nonprofit organizations, as expressed above, regularly get their assets from the gifts,

keeping in mind the end goal to do their services that are instrumental to the general public.

For example, giving alleviation, sustenance, protect, safeguard, ecological preservation and

arrangement of restorative help to the casualties of different normal and man impacted

calamities. Benefit making organizations are framed to deliver and offer merchandise and

enterprises with the sole point of making benefits as well as excess. It ought to be noticed that

benefit influencing worries to connect with themselves in the creation of merchandise and

ventures that have a popularity by purchasers, and which if there should be an occurrence of

The investors have premiums in the business detailing that the business can pay them the

arrival on their put subsidizes as reasonable profits on their shareholdings. Their budgetary

proclamations must be reviewed completely by government examiners to guarantee

straightforwardness and responsibility. With regards to nonprofit organizations, their budgetary

reports are likewise examined yet they have less weight and desire since are for the most part

to fulfill the contributors and well-wishers that their assets are appropriately misused by the

association. It ought to be noticed that, there are set up bookkeeping and announcing

guidelines for the non-benefit organizations to guarantee consistency in the way budgetary

reports are readied (Madia, 2011).

Literature Review

The main purpose of thought is surely the reason behind which every association flourishes.

The nonprofit organizations, as expressed above, regularly get their assets from the gifts,

keeping in mind the end goal to do their services that are instrumental to the general public.

For example, giving alleviation, sustenance, protect, safeguard, ecological preservation and

arrangement of restorative help to the casualties of different normal and man impacted

calamities. Benefit making organizations are framed to deliver and offer merchandise and

enterprises with the sole point of making benefits as well as excess. It ought to be noticed that

benefit influencing worries to connect with themselves in the creation of merchandise and

ventures that have a popularity by purchasers, and which if there should be an occurrence of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

M A N A G E M E N T I N N O N P R O F I T O R G A N I Z A T I O N S P a g e |

10

disappointment close their operations. They acquire subsidizing from proprietors and investors

and must circulate benefit to them (Maimunah et al., 2015).

The nonprofit organizations get their assets essentially from the stipends and gifts of the well-

wishers who can be governments, people, and other non-benefit making organizations and also

benefit making concerns. The leaders of these organizations can arrange and requested these

financing from the above sources because a large portion of them are not willing to give

because there are no profits on the assets progressed to them. Luckily, the corporate social

obligation has been underscored enough, even by the legislature, constraining numerous

corporate bodies to give a considerable measure to non-benefit making bodies. With regards to

the benefit making bodies they get their assets from various sources. This is evidently because

the subsidizing put has returned in the type of profits and interests on the borrowings

(Narendra & Karnika, 2013).

The chief wellspring of assets revenue driven making organizations is the proprietors. These are

the general population who concoct beginning the business and, in this way, have real offers of

the association. These individuals can acquire subsidizing from their investment funds or

approach budgetary and non-monetary foundations for cash. The other wellspring of assets can

be through opening up to the world when the organization is issuing its stocks and makes them

accessible to the individuals from general society on the stock exchange. Along these lines, the

10

disappointment close their operations. They acquire subsidizing from proprietors and investors

and must circulate benefit to them (Maimunah et al., 2015).

The nonprofit organizations get their assets essentially from the stipends and gifts of the well-

wishers who can be governments, people, and other non-benefit making organizations and also

benefit making concerns. The leaders of these organizations can arrange and requested these

financing from the above sources because a large portion of them are not willing to give

because there are no profits on the assets progressed to them. Luckily, the corporate social

obligation has been underscored enough, even by the legislature, constraining numerous

corporate bodies to give a considerable measure to non-benefit making bodies. With regards to

the benefit making bodies they get their assets from various sources. This is evidently because

the subsidizing put has returned in the type of profits and interests on the borrowings

(Narendra & Karnika, 2013).

The chief wellspring of assets revenue driven making organizations is the proprietors. These are

the general population who concoct beginning the business and, in this way, have real offers of

the association. These individuals can acquire subsidizing from their investment funds or

approach budgetary and non-monetary foundations for cash. The other wellspring of assets can

be through opening up to the world when the organization is issuing its stocks and makes them

accessible to the individuals from general society on the stock exchange. Along these lines, the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

M A N A G E M E N T I N N O N P R O F I T O R G A N I Z A T I O N S P a g e |

11

organization can fund-raise for its exercises, for example, the development of its operations

(Patricia et al., 2012).

Additionally, an organization can take a credit which is completed in two routes, to start with,

like cold hard cash from the money related or non-budgetary foundation, whereby it is required

to pay the obligation on the advance the premium. The other path is to advise on issuing

corporate securities whereby the organization commits to pay the bondholders their main sum

after the lapse of securities in addition to general intrigue installments. The other way can be

the wander financing. This is the point at which the investment stores benefit assets to

organizations with gigantic potential for development and gainfulness, and they finance it up to

80% and take up shares in it which they may pitch to proprietors when the organization

balances out (Pederzini, 2016). The investment finances ordinarily favor organizations that are

mechanically arranged.

Mergers and acquisitions are strategies of awesome significance for any business beginning

which can't contend adequately with different contenders. A merger is a point at which the two

organizations of equivalent monetary may partner to frame a major venture and advantage

from the economies of scale and synergistic impacts. This is typically by picking up a

noteworthy piece of the overall industry and a high cost of its stocks in money markets. The

securing is the point at which a substantial firm assumes control over the operations of a little

firm in a similar industry (Rothaermel, 2013).

Conclusion: Final View

Amid the previous years, nonprofit organizations have received and adjusted the private

segment Balanced Scorecard to their circumstances. A few have hoisted the part of mission and

client to the highest point of the pecking order of viewpoints, perceiving that nonprofits ought

to be responsible for how well they address an issue in the public eye instead of how well they

raise finances or control costs. Additionally, as the people or gatherings that give money related

help to nonprofits are normally unique about the individuals who are the immediate recipients

of the services given, numerous nonprofits perceive contributors or funders, and also

beneficiaries, as their clients.

11

organization can fund-raise for its exercises, for example, the development of its operations

(Patricia et al., 2012).

Additionally, an organization can take a credit which is completed in two routes, to start with,

like cold hard cash from the money related or non-budgetary foundation, whereby it is required

to pay the obligation on the advance the premium. The other path is to advise on issuing

corporate securities whereby the organization commits to pay the bondholders their main sum

after the lapse of securities in addition to general intrigue installments. The other way can be

the wander financing. This is the point at which the investment stores benefit assets to

organizations with gigantic potential for development and gainfulness, and they finance it up to

80% and take up shares in it which they may pitch to proprietors when the organization

balances out (Pederzini, 2016). The investment finances ordinarily favor organizations that are

mechanically arranged.

Mergers and acquisitions are strategies of awesome significance for any business beginning

which can't contend adequately with different contenders. A merger is a point at which the two

organizations of equivalent monetary may partner to frame a major venture and advantage

from the economies of scale and synergistic impacts. This is typically by picking up a

noteworthy piece of the overall industry and a high cost of its stocks in money markets. The

securing is the point at which a substantial firm assumes control over the operations of a little

firm in a similar industry (Rothaermel, 2013).

Conclusion: Final View

Amid the previous years, nonprofit organizations have received and adjusted the private

segment Balanced Scorecard to their circumstances. A few have hoisted the part of mission and

client to the highest point of the pecking order of viewpoints, perceiving that nonprofits ought

to be responsible for how well they address an issue in the public eye instead of how well they

raise finances or control costs. Additionally, as the people or gatherings that give money related

help to nonprofits are normally unique about the individuals who are the immediate recipients

of the services given, numerous nonprofits perceive contributors or funders, and also

beneficiaries, as their clients.

M A N A G E M E N T I N N O N P R O F I T O R G A N I Z A T I O N S P a g e |

12

References

Adeolu O. Adewuyi, Afolabi E. Olowookere. (2010). CSR and sustainable community development in

Nigeria: WAPCO, a case from the cement industry. Social Responsibility Journal, 6(4).

Ahmed A. Oussii & Mohamed F. Klibi. (2017). Accounting students’ perceptions of important business

communication skills for career success: An exploratory study in the Tunisian context. Journal of

Financial Reporting and Accounting, 15(2), 208-225.

Alfonso Siano, Philip J. Kitchen, Maria G. Confetto. (2010). Financial resources and corporate reputation:

Toward common management principles for managing corporate reputation. Corporate

Communications: An International Journal, 15(1), 68-82.

Amazon.com Announces First Quarter Sales up 15% to $22.72 Billion. (2015). Retrieved from

amazon.com: http://phx.corporate-ir.net/phoenix.zhtml?c=97664&p=irol-

newsArticle&ID=2039598

Ansgar J. Thiessen & Diana J. Ingenhoff. (2011). Safeguarding reputation through strategic, integrated

and situational crisis communication management: Development of the integrative model of

crisis communication. Corporate Communications: An International Journal, 16(1), 8-26.

Binod K. Shrestha and Devi R. Gnyawali. (2013). Insights on strategic management practices in Nepal.

South Asian Journal of Global Business Research, 2(2), 191-210.

David Giles & Russell Yates. (2014). Enabling educational leaders: qualitatively surveying an

organization's culture. International Journal of Organizational Analysis, 94-106.

Elaine E. & Dawn C. (2011). Evidence of improvement in accounting students' communication skills.

International Journal of Educational Management, 25(4), 311-327.

Evelyn L., Don R. & Aimie C. (2010). Successfully managing change during uncertain times. Strategic HR

Review, 12-18.

Eyun Jung Ki, Linda C. Hon. (2012). Causal linkages among relationship quality perception, attitude, and‐

behavior intention in a membership organization. Corporate Communications: An International

Journal, 17(2).

Jackson, C. (2011). Communication skills and accounting: do perceptions match reality? Strategic

Direction, 27(2).

Jim A. & Annelie A. (2014). Deconstructing resistance to organizational change: a social representation

theory approach. International Journal of Organizational Analysis, 342-355.

Kim MacKenzie, Sherrena Buckby, Helen Irvine. (2013). Business research in virtual worlds: possibilities

and practicalities. Accounting, Auditing & Accountability Journal, 352-373.

Liwen Tan, Jingkun Ding. (2015). The frontier and evolution of the strategic management theory: A

scientometric analysis of Strategic Management Journal, 2001-2012. Nankai Business Review

International, 6(1), 20-41.

12

References

Adeolu O. Adewuyi, Afolabi E. Olowookere. (2010). CSR and sustainable community development in

Nigeria: WAPCO, a case from the cement industry. Social Responsibility Journal, 6(4).

Ahmed A. Oussii & Mohamed F. Klibi. (2017). Accounting students’ perceptions of important business

communication skills for career success: An exploratory study in the Tunisian context. Journal of

Financial Reporting and Accounting, 15(2), 208-225.

Alfonso Siano, Philip J. Kitchen, Maria G. Confetto. (2010). Financial resources and corporate reputation:

Toward common management principles for managing corporate reputation. Corporate

Communications: An International Journal, 15(1), 68-82.

Amazon.com Announces First Quarter Sales up 15% to $22.72 Billion. (2015). Retrieved from

amazon.com: http://phx.corporate-ir.net/phoenix.zhtml?c=97664&p=irol-

newsArticle&ID=2039598

Ansgar J. Thiessen & Diana J. Ingenhoff. (2011). Safeguarding reputation through strategic, integrated

and situational crisis communication management: Development of the integrative model of

crisis communication. Corporate Communications: An International Journal, 16(1), 8-26.

Binod K. Shrestha and Devi R. Gnyawali. (2013). Insights on strategic management practices in Nepal.

South Asian Journal of Global Business Research, 2(2), 191-210.

David Giles & Russell Yates. (2014). Enabling educational leaders: qualitatively surveying an

organization's culture. International Journal of Organizational Analysis, 94-106.

Elaine E. & Dawn C. (2011). Evidence of improvement in accounting students' communication skills.

International Journal of Educational Management, 25(4), 311-327.

Evelyn L., Don R. & Aimie C. (2010). Successfully managing change during uncertain times. Strategic HR

Review, 12-18.

Eyun Jung Ki, Linda C. Hon. (2012). Causal linkages among relationship quality perception, attitude, and‐

behavior intention in a membership organization. Corporate Communications: An International

Journal, 17(2).

Jackson, C. (2011). Communication skills and accounting: do perceptions match reality? Strategic

Direction, 27(2).

Jim A. & Annelie A. (2014). Deconstructing resistance to organizational change: a social representation

theory approach. International Journal of Organizational Analysis, 342-355.

Kim MacKenzie, Sherrena Buckby, Helen Irvine. (2013). Business research in virtual worlds: possibilities

and practicalities. Accounting, Auditing & Accountability Journal, 352-373.

Liwen Tan, Jingkun Ding. (2015). The frontier and evolution of the strategic management theory: A

scientometric analysis of Strategic Management Journal, 2001-2012. Nankai Business Review

International, 6(1), 20-41.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.