Management Accounting: Special Order Analysis and Decision Making

VerifiedAdded on 2020/02/19

|4

|599

|43

Homework Assignment

AI Summary

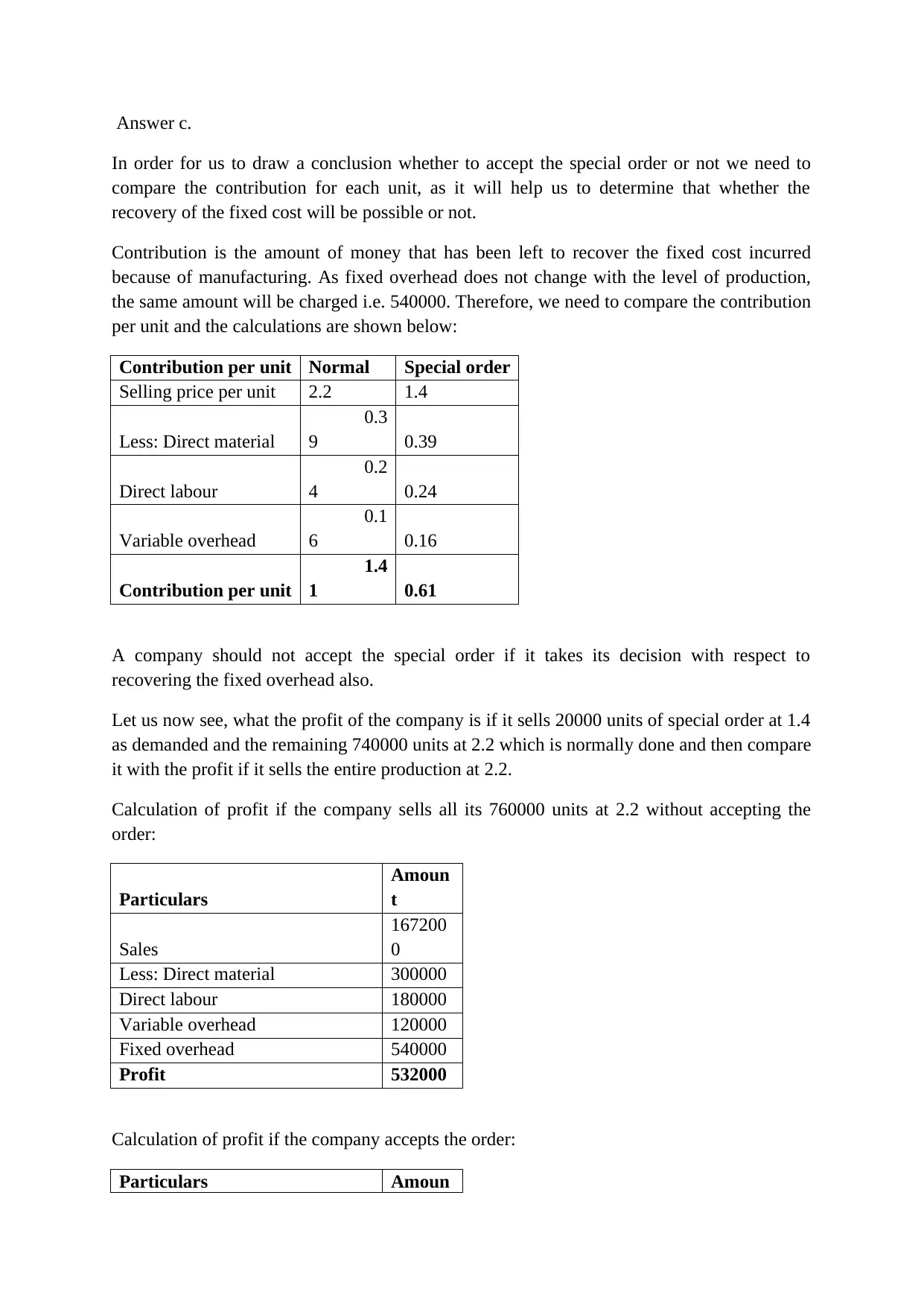

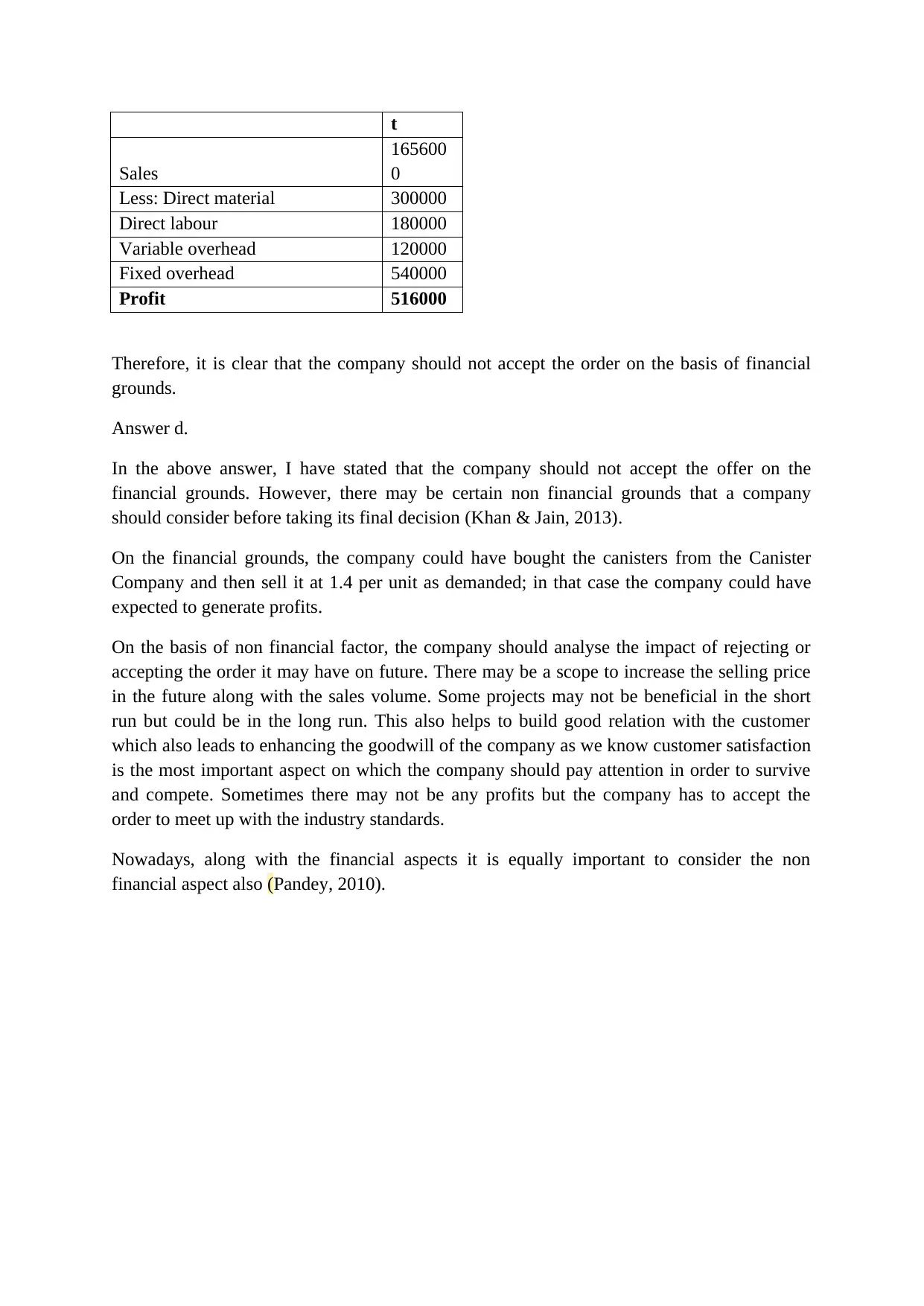

This assignment solution delves into a management accounting problem concerning a special order decision. The analysis begins by calculating the contribution per unit for both normal and special orders, comparing the profitability of each option. The solution then evaluates whether accepting the special order is financially beneficial by comparing the profit generated from selling at normal prices versus accepting the special order. The financial analysis concludes that the company should not accept the special order based on the financial grounds. Furthermore, the solution considers non-financial factors, such as building customer relationships, and long-term implications. The assignment includes references to support the analysis and conclusions, providing a comprehensive understanding of the decision-making process in management accounting.

1 out of 4

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.