BBAC501 Management Accounting Assignment: Profitability Analysis

VerifiedAdded on 2022/12/12

|10

|1937

|264

Homework Assignment

AI Summary

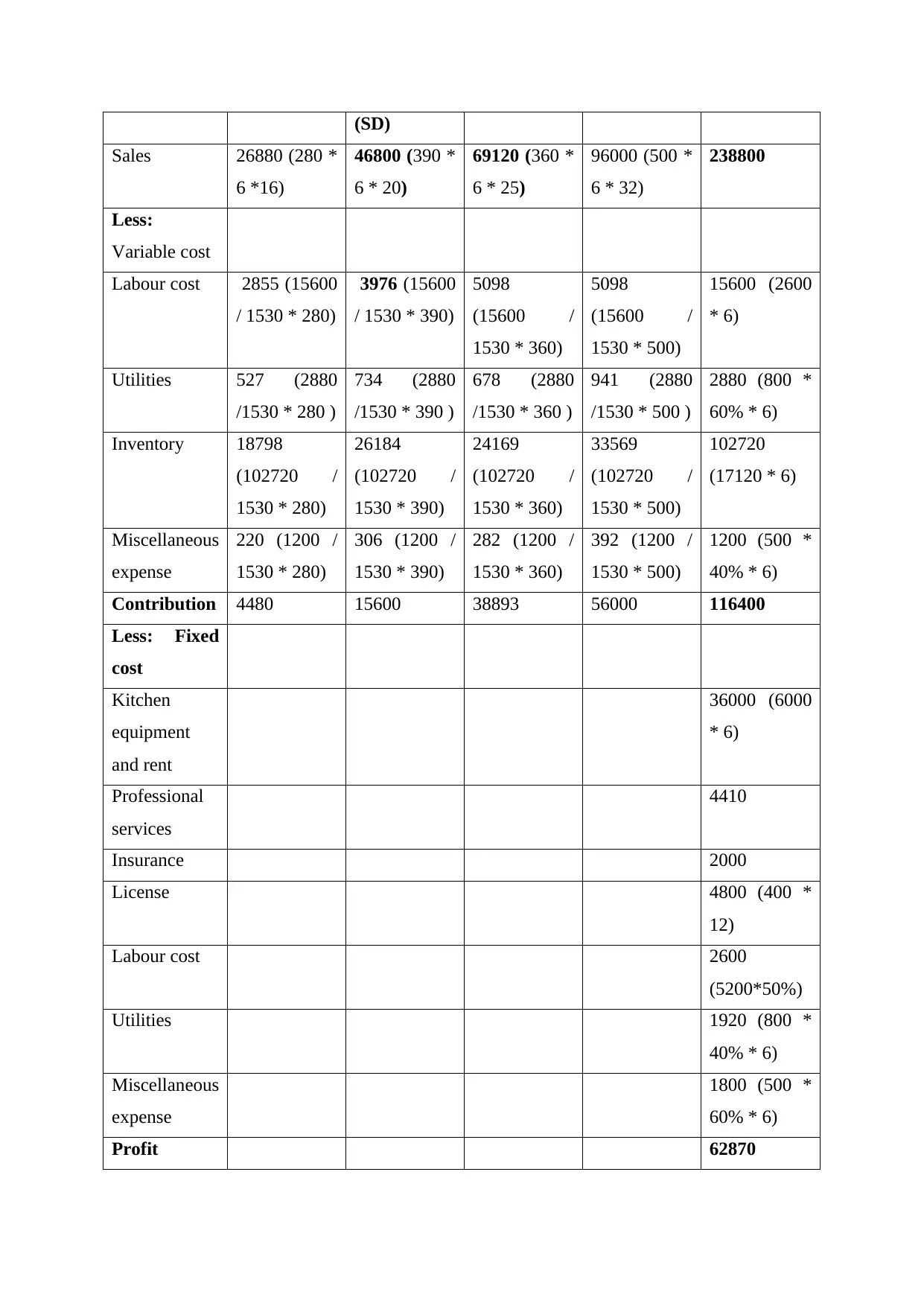

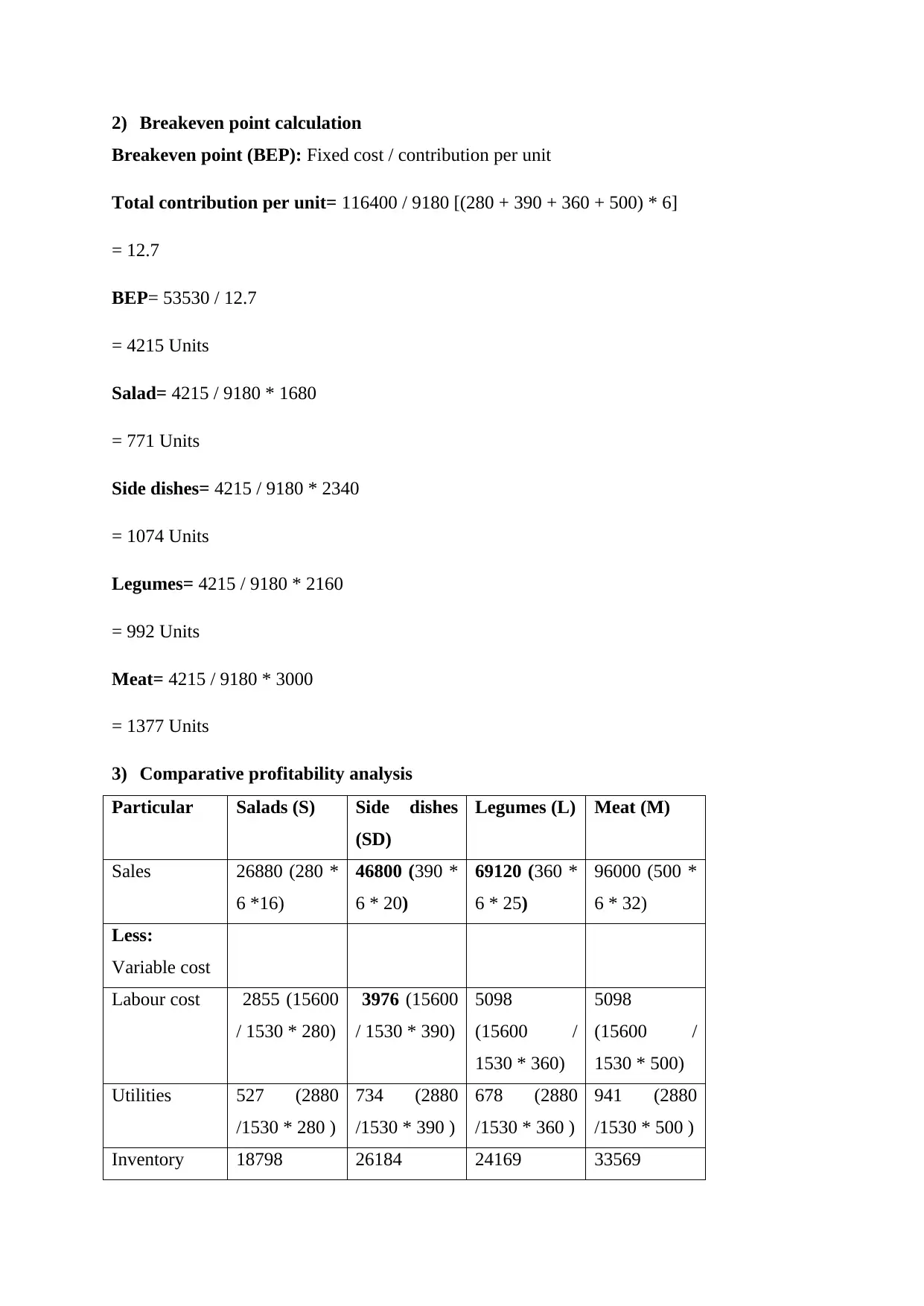

This assignment, a solution to a Management Accounting assignment, is divided into two parts, addressing key concepts in financial analysis. Part A includes an itemized income statement, breakeven point calculation, and a comparative profitability analysis across different menu items (Salads, Side dishes, Legumes, and Meat), concluding with an interpretation of the results, including margin of safety. Part B focuses on the expected profitability of financial statements and offers recommendations for improvement. The analysis involves detailed calculations of sales, variable costs (labor, utilities, inventory), and fixed costs (kitchen equipment, professional services, insurance, licenses, labor, utilities, and miscellaneous expenses) to determine profit or loss for each menu item. The assignment utilizes the provided data to calculate the breakeven point, recompute the margin of safety, and assess the impact of changes in sales volume on profitability. The final part offers recommendations for cost reduction and promotion strategies to improve the business's financial performance. Overall, the document provides a comprehensive overview of financial statement analysis and profitability assessment in the context of a business.

1 out of 10

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.