Analysis of Management Accounting Systems and Reporting Techniques

VerifiedAdded on 2021/02/21

|19

|5572

|49

Report

AI Summary

This report delves into the realm of management accounting, exploring its core concepts and various systems, including cost accounting, inventory management, job costing, and price optimization. It examines the significance of integrating reporting and systems within organizational processes, using Severn Trent, a UK-based engineering company, as a case study. The report details the benefits of each system and how they apply to real-world scenarios. Furthermore, it evaluates management accounting reporting, covering accounts receivable reports, inventory management reports, performance reports, and budget reports. The analysis extends to how these reports are integrated into organizational processes to enhance efficiency and decision-making. The report highlights the role of management accounting in optimizing costs, managing inventory, and improving overall financial performance within the organization. It also provides a comparison of the benefits and applications of these systems.

Management

Accounting

Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

ACTIVITY 1....................................................................................................................................1

Management Accounting Systems:.............................................................................................1

Management Accounting Reporting:..........................................................................................3

Benefits of management accounting system and their applications:..........................................5

Evaluation of management accounting reporting and system how integrated within

organisational processes:.............................................................................................................5

Preparation of income statements using absorption and marginal techniques:...........................6

Usage of management accounting techniques and preparation of appropriate financial

reporting documents:...................................................................................................................9

Interpretation of Financial Reports:............................................................................................9

ACTIVITY 2....................................................................................................................................9

Planning tools applied for budgetary control:.............................................................................9

Analyse the usage of different planning tools and their application for preparing and

forecasting budgets:..................................................................................................................13

Adoption of management accounting systems to respond financial problems:........................13

Comparison in between organizations in context of use of management accounting's systems

to respond financial issues:.......................................................................................................14

Contribution of management accounting in sustainable success of the organization while

responding financial problems:.................................................................................................15

Application of planning tools to respond financial issue along with attaining sustainable

success:......................................................................................................................................15

CONCLUSION..............................................................................................................................15

INTRODUCTION...........................................................................................................................1

ACTIVITY 1....................................................................................................................................1

Management Accounting Systems:.............................................................................................1

Management Accounting Reporting:..........................................................................................3

Benefits of management accounting system and their applications:..........................................5

Evaluation of management accounting reporting and system how integrated within

organisational processes:.............................................................................................................5

Preparation of income statements using absorption and marginal techniques:...........................6

Usage of management accounting techniques and preparation of appropriate financial

reporting documents:...................................................................................................................9

Interpretation of Financial Reports:............................................................................................9

ACTIVITY 2....................................................................................................................................9

Planning tools applied for budgetary control:.............................................................................9

Analyse the usage of different planning tools and their application for preparing and

forecasting budgets:..................................................................................................................13

Adoption of management accounting systems to respond financial problems:........................13

Comparison in between organizations in context of use of management accounting's systems

to respond financial issues:.......................................................................................................14

Contribution of management accounting in sustainable success of the organization while

responding financial problems:.................................................................................................15

Application of planning tools to respond financial issue along with attaining sustainable

success:......................................................................................................................................15

CONCLUSION..............................................................................................................................15

INTRODUCTION

Management accounting system is primarily regarded as core utility or task of business

entity which circulates and retrieves fiscal information within organisational structure. It

comprises organisation's efficiencies of maintaining liquidity, compliance capacity, company's

economic flexibility and more. Easy accessibility of company's internal information assist

managing personnels in effective and efficient planning and major resources' allocation. On the

ground of such internal information an organisation could choose appropriate alternative and

take decisions with aim of company's future growth (Adegbile, Sarpong and Meissner, 2017).

This study focuses on this management accounting system theory and how much it enables an

organization track financial performance. For this purpose, a reputed engineering company of

UK is taken, named by Severn Trent. It is top regulated water and sewerage company operating

business through headquarter in England. In order to streamline company and to build good

image of company worldwide, Company's line managers adapted different management

accounting's systems for the purpose of spreading and enhancing understanding across various

divisions.

This study is segregated into two major parts. The first part consists of explanation about

management accounting's concept along with various types of management accounting system.

Moreover, it also exhibits significance of integrating reporting and systems within organisational

processes. While second part consists of advantage or features and disadvantage of numerous

planning tools assists in budgetary control's process.

ACTIVITY 1

Management Accounting Systems:

Management accounting is often regarded as managerial and cost accounting which

facilitates a smooth structure of optimising and analysing costs and other trade operations in

order to develop internal fiscal records, schedules and accounts. This term also relates to task of

gathering raw undefined information and converting such information into unique and relevant

information, which finally help in tracking business entity's efficiencies. It usually covers a range

of accounting manifestations such as margins, assessment, capital budgeting and costing of

products. In addition, its primary problem is with the entity's internal variables and the

preparation and presentation of a corporates' financial statement is essential for executives. In

1

Management accounting system is primarily regarded as core utility or task of business

entity which circulates and retrieves fiscal information within organisational structure. It

comprises organisation's efficiencies of maintaining liquidity, compliance capacity, company's

economic flexibility and more. Easy accessibility of company's internal information assist

managing personnels in effective and efficient planning and major resources' allocation. On the

ground of such internal information an organisation could choose appropriate alternative and

take decisions with aim of company's future growth (Adegbile, Sarpong and Meissner, 2017).

This study focuses on this management accounting system theory and how much it enables an

organization track financial performance. For this purpose, a reputed engineering company of

UK is taken, named by Severn Trent. It is top regulated water and sewerage company operating

business through headquarter in England. In order to streamline company and to build good

image of company worldwide, Company's line managers adapted different management

accounting's systems for the purpose of spreading and enhancing understanding across various

divisions.

This study is segregated into two major parts. The first part consists of explanation about

management accounting's concept along with various types of management accounting system.

Moreover, it also exhibits significance of integrating reporting and systems within organisational

processes. While second part consists of advantage or features and disadvantage of numerous

planning tools assists in budgetary control's process.

ACTIVITY 1

Management Accounting Systems:

Management accounting is often regarded as managerial and cost accounting which

facilitates a smooth structure of optimising and analysing costs and other trade operations in

order to develop internal fiscal records, schedules and accounts. This term also relates to task of

gathering raw undefined information and converting such information into unique and relevant

information, which finally help in tracking business entity's efficiencies. It usually covers a range

of accounting manifestations such as margins, assessment, capital budgeting and costing of

products. In addition, its primary problem is with the entity's internal variables and the

preparation and presentation of a corporates' financial statement is essential for executives. In

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

addition, executives of a organization can schedule short-term plans and day-to-day operations

with the support of management accounting (Balaman, 2016). Management Accounting

System can be described as an inner organisational process which defines the information of

economic and fiscal development of the company, the capacity to fulfil obligation, resource

allocation and more. It collects the significant information such as profitability, income,

excellent debts, etc. and report such data for managerial or business decision-making. Severn

Trent has also adopted different systems to handle and manage their different operations with

aim to achieve targets. Following discussed are key systems of managerial accounting as

follows:

Cost Accounting System: It is defined as a procedure of controlling the transformation

into finished goods of raw materials. In addition, it is mainly used by manufacturers to record

manufacturing operations. Cost accounting system pertains to a structure that offers an

anticipated inventory valuation, controlling costs, and beneficial evaluation cost of its items to a

business. The respective scheme evaluates the input expenses of each manufacturing stage for

this phase, as well as for fixed expenses such as depreciation on equipment and machinery

(Chang and et.al, 2014). A standard cost accounting system operates by monitoring raw materials

as they move through phases of manufacturing and in real-time progressively transform in to

finished products. In Severn Trent, it assist management officials in determining costs involved

in purifying and supply of water to different parties and people.

Inventory Management System: It is specified as a management system that keeps

record relevant to inventory like collecting inventory information stored in warehouse, inventory

supply, and much more. Inventory management is quite crucial for an company's supervisor to

be able to identify regularly regarding storage and stock supply. This systems assists in

effectively managing level of wide ranger of items of stock and control expenses originated

through inventory processes. This systems is mostly proffered by manufacturing industry as

business belongs to such industry as these business entities have small, moderate and large sized

stock items and different processed inventories (Turban, Volonino and Wood, 2015). Managing

such wast amount of inventory is difficult but by applying this system stock managers can easily

handle such task. In Severn Trent, managers are adopting it to manage storage of water and other

its inventory or store item. This also enables businesses to keep just-in-time inventory structure

where products should only be ordered as required from providers and supplies. No additional

2

with the support of management accounting (Balaman, 2016). Management Accounting

System can be described as an inner organisational process which defines the information of

economic and fiscal development of the company, the capacity to fulfil obligation, resource

allocation and more. It collects the significant information such as profitability, income,

excellent debts, etc. and report such data for managerial or business decision-making. Severn

Trent has also adopted different systems to handle and manage their different operations with

aim to achieve targets. Following discussed are key systems of managerial accounting as

follows:

Cost Accounting System: It is defined as a procedure of controlling the transformation

into finished goods of raw materials. In addition, it is mainly used by manufacturers to record

manufacturing operations. Cost accounting system pertains to a structure that offers an

anticipated inventory valuation, controlling costs, and beneficial evaluation cost of its items to a

business. The respective scheme evaluates the input expenses of each manufacturing stage for

this phase, as well as for fixed expenses such as depreciation on equipment and machinery

(Chang and et.al, 2014). A standard cost accounting system operates by monitoring raw materials

as they move through phases of manufacturing and in real-time progressively transform in to

finished products. In Severn Trent, it assist management officials in determining costs involved

in purifying and supply of water to different parties and people.

Inventory Management System: It is specified as a management system that keeps

record relevant to inventory like collecting inventory information stored in warehouse, inventory

supply, and much more. Inventory management is quite crucial for an company's supervisor to

be able to identify regularly regarding storage and stock supply. This systems assists in

effectively managing level of wide ranger of items of stock and control expenses originated

through inventory processes. This systems is mostly proffered by manufacturing industry as

business belongs to such industry as these business entities have small, moderate and large sized

stock items and different processed inventories (Turban, Volonino and Wood, 2015). Managing

such wast amount of inventory is difficult but by applying this system stock managers can easily

handle such task. In Severn Trent, managers are adopting it to manage storage of water and other

its inventory or store item. This also enables businesses to keep just-in-time inventory structure

where products should only be ordered as required from providers and supplies. No additional

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

amounts are purchased and stored on subsequent stage for processing. Here are three most used

methods of inventory recording:

LIFO: The last technique in, first out (LIFO) is applied to determine an stock accounting

value. The LIFO technique works on the assumption that first item sold is the last item of

the stock bought.

FIFO: It represents of "first-in, first-out," is indeed a practice related to entering of

inventory in records which presumes that first items held in stock are first items sold.

Therefore, the stock at year end is made up of the latest in inventory products (Lavia

López and Hiebl, 2014).

Average cost method: A weighted average cost of stock is used in this method for

valuing inventories at year end.

Job costing system: Job Costing system relates to an order-specific costing procedure

that is used in circumstances where each manufacturing job is distinct and conducted in

accordance with specific client requirements. It includes maintaining a direct and indirect cost

account of corporation, which is strongly linked to a job requiring heavy labour and material

input. Job costing systems systemically ascertain production expenses by separating them into

overheads, direct materials and labor costs, and forecasting them at their true value (Modell,

2014). Manufacturing companies use work costs to regulate use of raw materials, hours of work

and facilities by individually assigning the price of each consumer order. Severn Trent applying

this system to maintain accountability in its distinct job processes involved in water supply

system.

Price Optimisation System: It is represented as a structure used to sustain rates at the

time of manufacturing. This process helps to control the price of different goods at a point in

time. Through it managers track and analyse the impact on demand as a result of change in price

of company's products. In long-term this process provides competitive benefits by minimising

the prices of different products (Leitner, 2013). In Severn Trent rate of water supply is

determined by business managers by applying results of these system. Price of items fixed under

this system also provides cost effectiveness.

Management Accounting Reporting:

Management accounting reporting could be defined as a document report that effectively

presents statistics or company outcomes data. In addition, this report is compelled in each quarter

3

methods of inventory recording:

LIFO: The last technique in, first out (LIFO) is applied to determine an stock accounting

value. The LIFO technique works on the assumption that first item sold is the last item of

the stock bought.

FIFO: It represents of "first-in, first-out," is indeed a practice related to entering of

inventory in records which presumes that first items held in stock are first items sold.

Therefore, the stock at year end is made up of the latest in inventory products (Lavia

López and Hiebl, 2014).

Average cost method: A weighted average cost of stock is used in this method for

valuing inventories at year end.

Job costing system: Job Costing system relates to an order-specific costing procedure

that is used in circumstances where each manufacturing job is distinct and conducted in

accordance with specific client requirements. It includes maintaining a direct and indirect cost

account of corporation, which is strongly linked to a job requiring heavy labour and material

input. Job costing systems systemically ascertain production expenses by separating them into

overheads, direct materials and labor costs, and forecasting them at their true value (Modell,

2014). Manufacturing companies use work costs to regulate use of raw materials, hours of work

and facilities by individually assigning the price of each consumer order. Severn Trent applying

this system to maintain accountability in its distinct job processes involved in water supply

system.

Price Optimisation System: It is represented as a structure used to sustain rates at the

time of manufacturing. This process helps to control the price of different goods at a point in

time. Through it managers track and analyse the impact on demand as a result of change in price

of company's products. In long-term this process provides competitive benefits by minimising

the prices of different products (Leitner, 2013). In Severn Trent rate of water supply is

determined by business managers by applying results of these system. Price of items fixed under

this system also provides cost effectiveness.

Management Accounting Reporting:

Management accounting reporting could be defined as a document report that effectively

presents statistics or company outcomes data. In addition, this report is compelled in each quarter

3

presenting financial accessibility in a business entity. Reporting process is generally considered

as a part of managerial structure as it help in efficient circulation of information. Such

information is mainly obtained from different systems as discussed above. Circulation of

relevant information throughout the different levels of management accounting is important as it

provide assistance in taking appropriate decisions and actions (Kaiser, El Arbi and Ahlemann,

2015). In Severn Trent reporting and systems of management accounting runs simultaneously to

increase the operational efficiencies and provide quickness in decision-making structure. All

level of managing officials are involved in managerial reporting focuses on value addition in

information circulated in reporting process. In this context following are the significant reports

prepared by managerial officials, as follows:

Account receivable report: These types of reports are produced by those businesses that

deal with their customers in credit-terms. It enables to evaluate the complete funds owed

that clients need to pay. In Severn Trent, this report is being produced by managerial

personnels to maintain an overall track record of amount outstanding and to be received

from clients. This report contributes towards identification of debtors who may be

bankrupt in near future. It assist in minimising the amount of bad debts over a specific

period. In company any modification in credit policies are done on the basis of outputs of

this report.

Inventory management report: Such sort of report is mainly prepared in manufacturing

companies for keeping systematic record of its inventory's items. In Severn Trent this

report is being prepared by officials who are responsible for maintaining record of

inventory. It holds detailed but vital information and data of stocks which help business

entity in operating business tasks effectively. It is quite useful to managers since it can

assist evaluate inventory situation either in transport or in store (Kalkhouran and et.al,

2015). It is also very essential to produce this sort of report for all businesses like Severn

Trent as it can assist to operate the company properly and effectively. This report

contains all types of stock or inventory-related information.

Performance report: This form of report is used in most businesses to screen the

efficiency of the entire business enterprise and the people working for the entity. In

Severn Trent, the executives draw up such report to assess the attempts taken by the staff

to effectively perform all allocated duties. The managerial people within company also

4

as a part of managerial structure as it help in efficient circulation of information. Such

information is mainly obtained from different systems as discussed above. Circulation of

relevant information throughout the different levels of management accounting is important as it

provide assistance in taking appropriate decisions and actions (Kaiser, El Arbi and Ahlemann,

2015). In Severn Trent reporting and systems of management accounting runs simultaneously to

increase the operational efficiencies and provide quickness in decision-making structure. All

level of managing officials are involved in managerial reporting focuses on value addition in

information circulated in reporting process. In this context following are the significant reports

prepared by managerial officials, as follows:

Account receivable report: These types of reports are produced by those businesses that

deal with their customers in credit-terms. It enables to evaluate the complete funds owed

that clients need to pay. In Severn Trent, this report is being produced by managerial

personnels to maintain an overall track record of amount outstanding and to be received

from clients. This report contributes towards identification of debtors who may be

bankrupt in near future. It assist in minimising the amount of bad debts over a specific

period. In company any modification in credit policies are done on the basis of outputs of

this report.

Inventory management report: Such sort of report is mainly prepared in manufacturing

companies for keeping systematic record of its inventory's items. In Severn Trent this

report is being prepared by officials who are responsible for maintaining record of

inventory. It holds detailed but vital information and data of stocks which help business

entity in operating business tasks effectively. It is quite useful to managers since it can

assist evaluate inventory situation either in transport or in store (Kalkhouran and et.al,

2015). It is also very essential to produce this sort of report for all businesses like Severn

Trent as it can assist to operate the company properly and effectively. This report

contains all types of stock or inventory-related information.

Performance report: This form of report is used in most businesses to screen the

efficiency of the entire business enterprise and the people working for the entity. In

Severn Trent, the executives draw up such report to assess the attempts taken by the staff

to effectively perform all allocated duties. The managerial people within company also

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

uses this report to set and allot amount of bonuses, employment benefits and other

incentives depending on their performance to the employees. The company's market

status and position could also be evaluated using it. It benefits the entity as it can direct

executives to evaluate whether or not their company performs well.

Budget report: The managers produce this report to match the business's budget

predictions and real results. It is an vital internal report that the management primarily

uses to evaluate whether or not company can fulfill its goals. This reports are produced in

Severn Trent by company's managing officials to assure that all organizational and

executive operations or tasks are carried out in the proposed fiscal budget or not. It is

beneficial for the business as it could assist business executives in making adequate

economic decisions to improve and achieve determined growth targets.

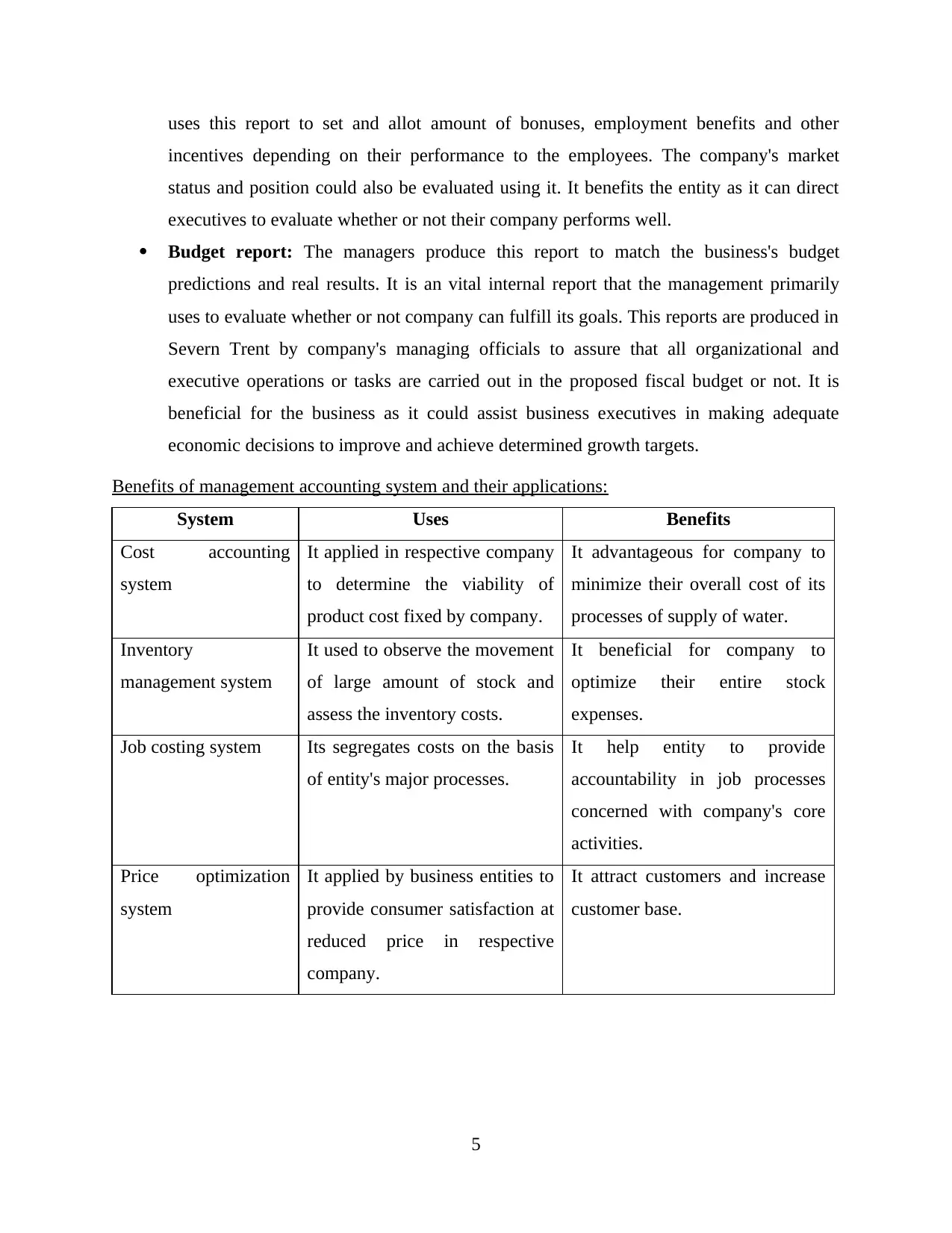

Benefits of management accounting system and their applications:

System Uses Benefits

Cost accounting

system

It applied in respective company

to determine the viability of

product cost fixed by company.

It advantageous for company to

minimize their overall cost of its

processes of supply of water.

Inventory

management system

It used to observe the movement

of large amount of stock and

assess the inventory costs.

It beneficial for company to

optimize their entire stock

expenses.

Job costing system Its segregates costs on the basis

of entity's major processes.

It help entity to provide

accountability in job processes

concerned with company's core

activities.

Price optimization

system

It applied by business entities to

provide consumer satisfaction at

reduced price in respective

company.

It attract customers and increase

customer base.

5

incentives depending on their performance to the employees. The company's market

status and position could also be evaluated using it. It benefits the entity as it can direct

executives to evaluate whether or not their company performs well.

Budget report: The managers produce this report to match the business's budget

predictions and real results. It is an vital internal report that the management primarily

uses to evaluate whether or not company can fulfill its goals. This reports are produced in

Severn Trent by company's managing officials to assure that all organizational and

executive operations or tasks are carried out in the proposed fiscal budget or not. It is

beneficial for the business as it could assist business executives in making adequate

economic decisions to improve and achieve determined growth targets.

Benefits of management accounting system and their applications:

System Uses Benefits

Cost accounting

system

It applied in respective company

to determine the viability of

product cost fixed by company.

It advantageous for company to

minimize their overall cost of its

processes of supply of water.

Inventory

management system

It used to observe the movement

of large amount of stock and

assess the inventory costs.

It beneficial for company to

optimize their entire stock

expenses.

Job costing system Its segregates costs on the basis

of entity's major processes.

It help entity to provide

accountability in job processes

concerned with company's core

activities.

Price optimization

system

It applied by business entities to

provide consumer satisfaction at

reduced price in respective

company.

It attract customers and increase

customer base.

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Evaluation of management accounting reporting and system how integrated within organisational

processes:

Managerial personnels tries to interlink business processes with management accounting

aspects like its systems and reporting. Main motive behind it is to smooth-en the overall business

performance. In entity like Severn Trent, managing officials established a structure to closely

link all business functions with system and reporting of management accounting. As in entity

finance and accounting processes are dedicated to provide information for reporting under MA

and its systems. Company emphasizes on such integration as it ensures improvement in

company's internal and external performance.

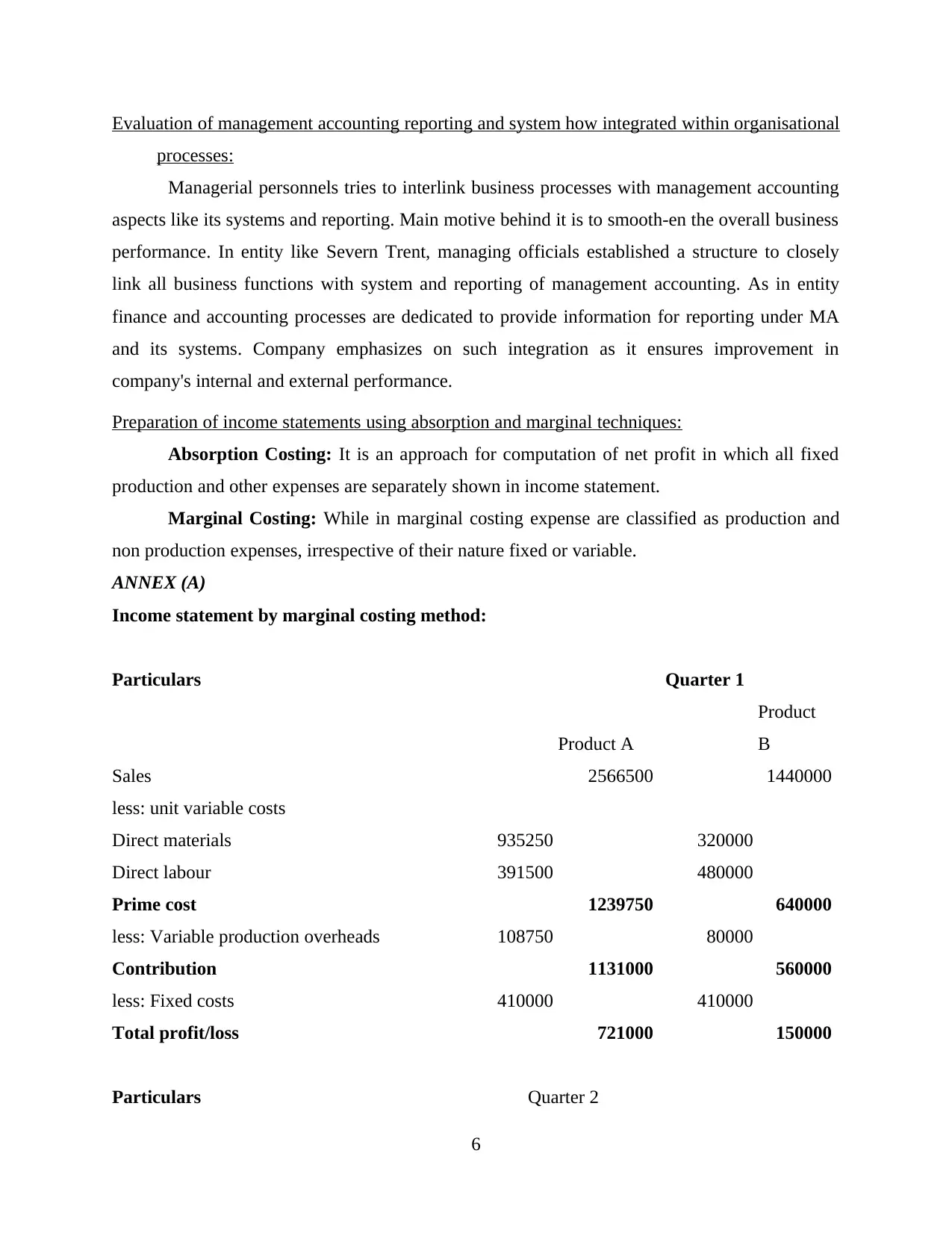

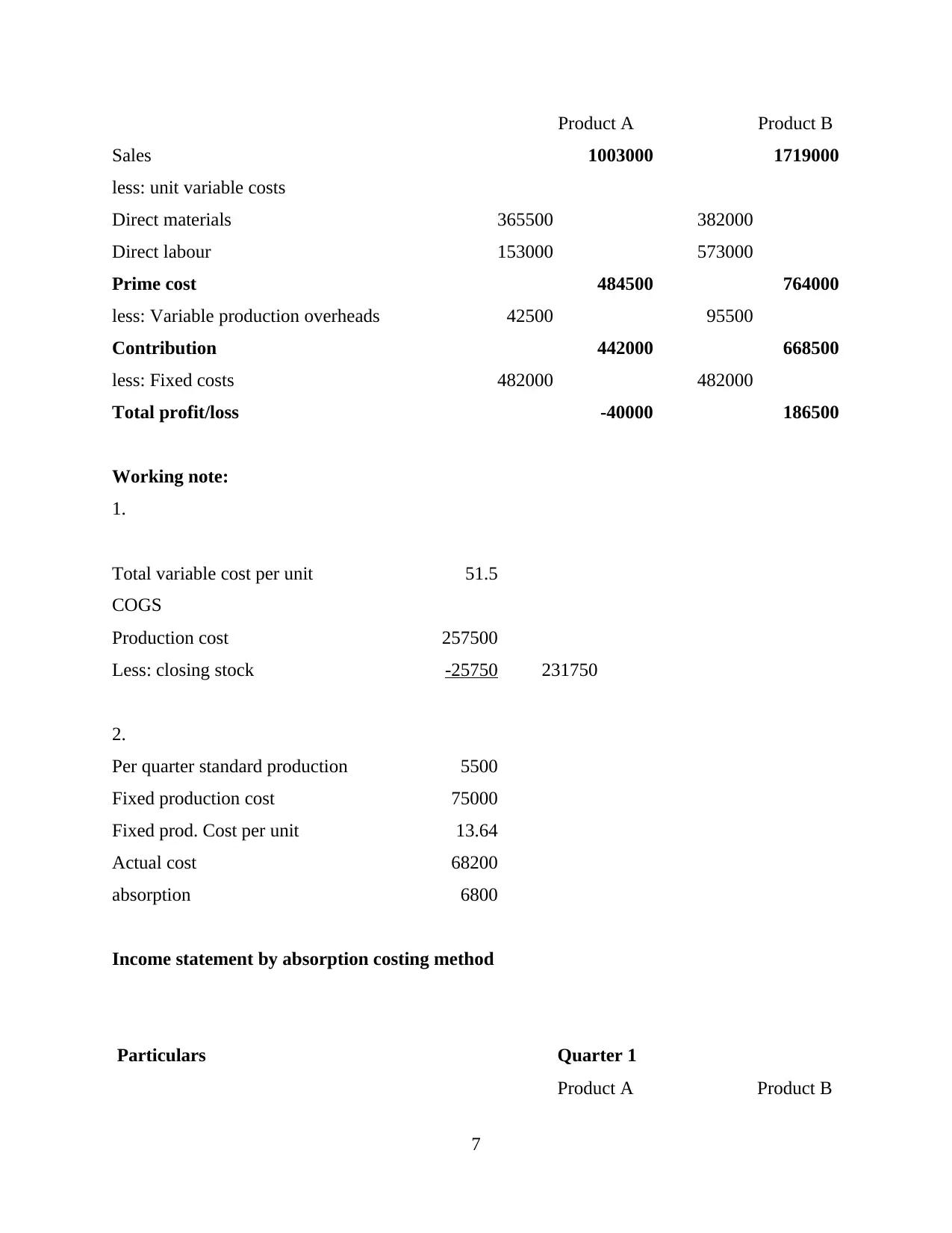

Preparation of income statements using absorption and marginal techniques:

Absorption Costing: It is an approach for computation of net profit in which all fixed

production and other expenses are separately shown in income statement.

Marginal Costing: While in marginal costing expense are classified as production and

non production expenses, irrespective of their nature fixed or variable.

ANNEX (A)

Income statement by marginal costing method:

Particulars Quarter 1

Product A

Product

B

Sales 2566500 1440000

less: unit variable costs

Direct materials 935250 320000

Direct labour 391500 480000

Prime cost 1239750 640000

less: Variable production overheads 108750 80000

Contribution 1131000 560000

less: Fixed costs 410000 410000

Total profit/loss 721000 150000

Particulars Quarter 2

6

processes:

Managerial personnels tries to interlink business processes with management accounting

aspects like its systems and reporting. Main motive behind it is to smooth-en the overall business

performance. In entity like Severn Trent, managing officials established a structure to closely

link all business functions with system and reporting of management accounting. As in entity

finance and accounting processes are dedicated to provide information for reporting under MA

and its systems. Company emphasizes on such integration as it ensures improvement in

company's internal and external performance.

Preparation of income statements using absorption and marginal techniques:

Absorption Costing: It is an approach for computation of net profit in which all fixed

production and other expenses are separately shown in income statement.

Marginal Costing: While in marginal costing expense are classified as production and

non production expenses, irrespective of their nature fixed or variable.

ANNEX (A)

Income statement by marginal costing method:

Particulars Quarter 1

Product A

Product

B

Sales 2566500 1440000

less: unit variable costs

Direct materials 935250 320000

Direct labour 391500 480000

Prime cost 1239750 640000

less: Variable production overheads 108750 80000

Contribution 1131000 560000

less: Fixed costs 410000 410000

Total profit/loss 721000 150000

Particulars Quarter 2

6

Product A Product B

Sales 1003000 1719000

less: unit variable costs

Direct materials 365500 382000

Direct labour 153000 573000

Prime cost 484500 764000

less: Variable production overheads 42500 95500

Contribution 442000 668500

less: Fixed costs 482000 482000

Total profit/loss -40000 186500

Working note:

1.

Total variable cost per unit 51.5

COGS

Production cost 257500

Less: closing stock -25750 231750

2.

Per quarter standard production 5500

Fixed production cost 75000

Fixed prod. Cost per unit 13.64

Actual cost 68200

absorption 6800

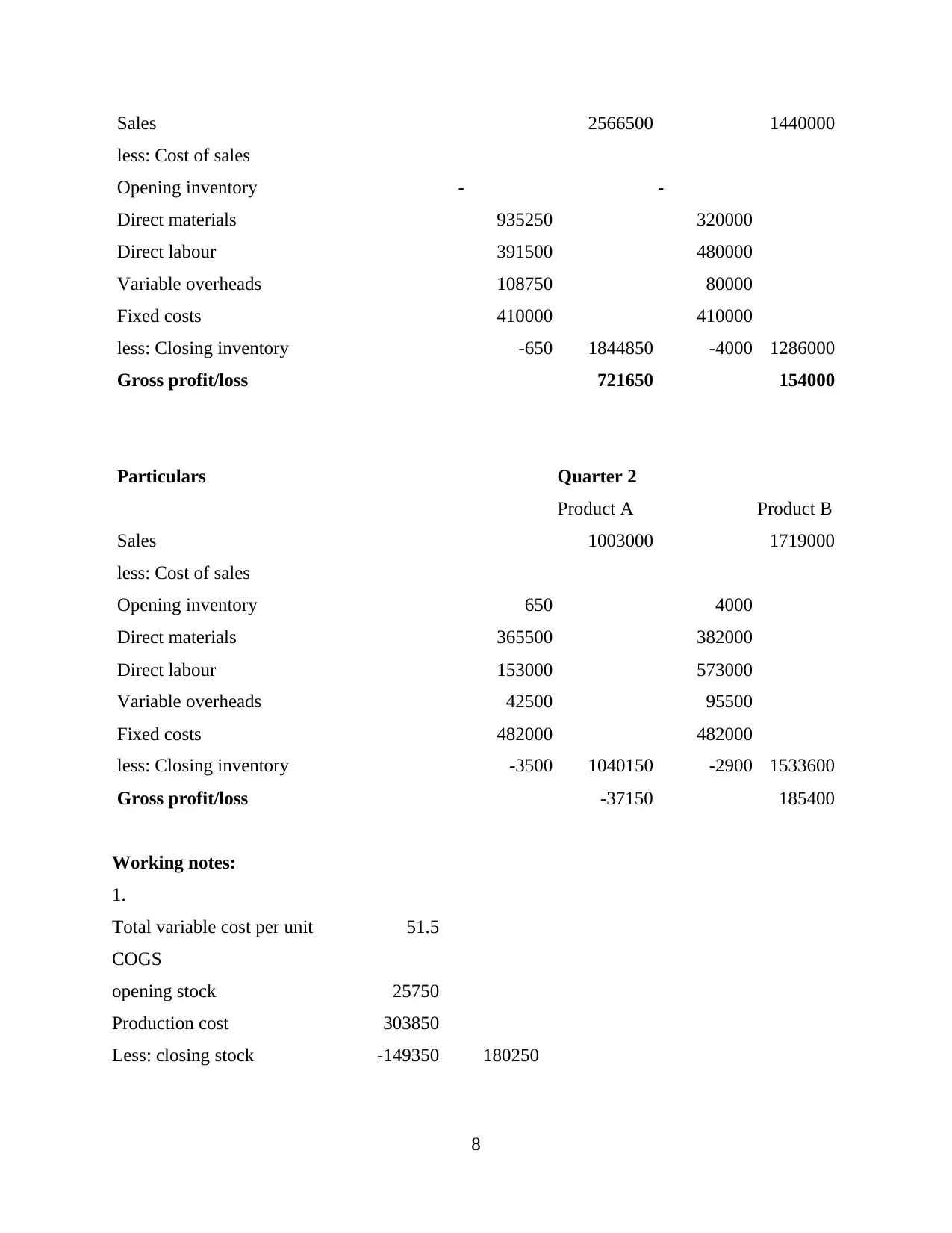

Income statement by absorption costing method

Particulars Quarter 1

Product A Product B

7

Sales 1003000 1719000

less: unit variable costs

Direct materials 365500 382000

Direct labour 153000 573000

Prime cost 484500 764000

less: Variable production overheads 42500 95500

Contribution 442000 668500

less: Fixed costs 482000 482000

Total profit/loss -40000 186500

Working note:

1.

Total variable cost per unit 51.5

COGS

Production cost 257500

Less: closing stock -25750 231750

2.

Per quarter standard production 5500

Fixed production cost 75000

Fixed prod. Cost per unit 13.64

Actual cost 68200

absorption 6800

Income statement by absorption costing method

Particulars Quarter 1

Product A Product B

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Sales 2566500 1440000

less: Cost of sales

Opening inventory - -

Direct materials 935250 320000

Direct labour 391500 480000

Variable overheads 108750 80000

Fixed costs 410000 410000

less: Closing inventory -650 1844850 -4000 1286000

Gross profit/loss 721650 154000

Particulars Quarter 2

Product A Product B

Sales 1003000 1719000

less: Cost of sales

Opening inventory 650 4000

Direct materials 365500 382000

Direct labour 153000 573000

Variable overheads 42500 95500

Fixed costs 482000 482000

less: Closing inventory -3500 1040150 -2900 1533600

Gross profit/loss -37150 185400

Working notes:

1.

Total variable cost per unit 51.5

COGS

opening stock 25750

Production cost 303850

Less: closing stock -149350 180250

8

less: Cost of sales

Opening inventory - -

Direct materials 935250 320000

Direct labour 391500 480000

Variable overheads 108750 80000

Fixed costs 410000 410000

less: Closing inventory -650 1844850 -4000 1286000

Gross profit/loss 721650 154000

Particulars Quarter 2

Product A Product B

Sales 1003000 1719000

less: Cost of sales

Opening inventory 650 4000

Direct materials 365500 382000

Direct labour 153000 573000

Variable overheads 42500 95500

Fixed costs 482000 482000

less: Closing inventory -3500 1040150 -2900 1533600

Gross profit/loss -37150 185400

Working notes:

1.

Total variable cost per unit 51.5

COGS

opening stock 25750

Production cost 303850

Less: closing stock -149350 180250

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2.

Per quarter standard

production 5500

Fixed production cost 75000

Fixed prod. Cost per unit 13.64

Actual cost 80476

absorption -5476

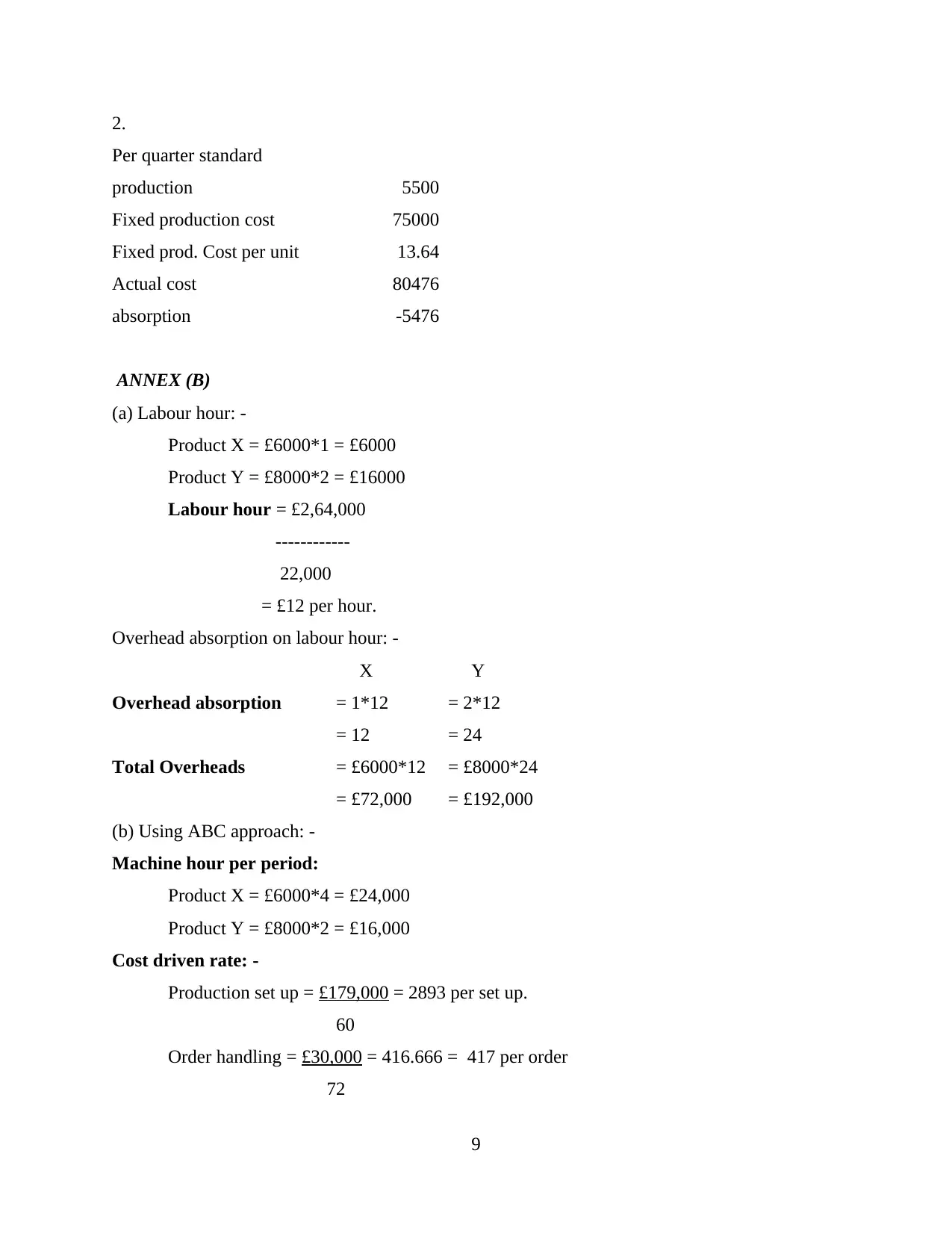

ANNEX (B)

(a) Labour hour: -

Product X = £6000*1 = £6000

Product Y = £8000*2 = £16000

Labour hour = £2,64,000

------------

22,000

= £12 per hour.

Overhead absorption on labour hour: -

X Y

Overhead absorption = 1*12 = 2*12

= 12 = 24

Total Overheads = £6000*12 = £8000*24

= £72,000 = £192,000

(b) Using ABC approach: -

Machine hour per period:

Product X = £6000*4 = £24,000

Product Y = £8000*2 = £16,000

Cost driven rate: -

Production set up = £179,000 = 2893 per set up.

60

Order handling = £30,000 = 416.666 = 417 per order

72

9

Per quarter standard

production 5500

Fixed production cost 75000

Fixed prod. Cost per unit 13.64

Actual cost 80476

absorption -5476

ANNEX (B)

(a) Labour hour: -

Product X = £6000*1 = £6000

Product Y = £8000*2 = £16000

Labour hour = £2,64,000

------------

22,000

= £12 per hour.

Overhead absorption on labour hour: -

X Y

Overhead absorption = 1*12 = 2*12

= 12 = 24

Total Overheads = £6000*12 = £8000*24

= £72,000 = £192,000

(b) Using ABC approach: -

Machine hour per period:

Product X = £6000*4 = £24,000

Product Y = £8000*2 = £16,000

Cost driven rate: -

Production set up = £179,000 = 2893 per set up.

60

Order handling = £30,000 = 416.666 = 417 per order

72

9

Machine cost = £55,000 = 1.375 per order

40,000

Overhead using ABC approach: -

X

Set up = 15*2983 = 44,745

Order = 12*417 = 5004

Machine cost = 24000*1.375 = 33,000

Total 82749

Y

Set up = 45*2983 = 134,235

Order = 60*417 = 25,020

Machine cost = 16000*1.375 = 22,000

Total 181,255

Usage of management accounting techniques and preparation of appropriate financial reporting

documents:

For analysing performance of company form different point of view several techniques

are used by accounting and management personnels. Use of techniques like absorption and

marginal costing provide effectiveness in company's operations. Complete and detailed aspects

of company's performance can be evaluated by applying two or more techniques simultaneously.

An organisation like Severn Trent prepares fiscal reports and statements applying such

techniques for assessing the true position and performance of entity.

Interpretation of Financial Reports:

According to revenue statements produced on the premise of absorption and marginal

costing, the distinction in outcomes from both techniques is analysed owing to distinct

approaches used in both techniques for fixed costs. The figures of net income in respect of Q1 is

Pound 721000 and Pound 150000 respectively for item A and item B, and on other side in

respect of Q2 these are -40000 and 186500 respectively for item A and item B. While through

absorption costing figures of net income in respect of Q1 is 721650 and 154000 for item A and B

10

40,000

Overhead using ABC approach: -

X

Set up = 15*2983 = 44,745

Order = 12*417 = 5004

Machine cost = 24000*1.375 = 33,000

Total 82749

Y

Set up = 45*2983 = 134,235

Order = 60*417 = 25,020

Machine cost = 16000*1.375 = 22,000

Total 181,255

Usage of management accounting techniques and preparation of appropriate financial reporting

documents:

For analysing performance of company form different point of view several techniques

are used by accounting and management personnels. Use of techniques like absorption and

marginal costing provide effectiveness in company's operations. Complete and detailed aspects

of company's performance can be evaluated by applying two or more techniques simultaneously.

An organisation like Severn Trent prepares fiscal reports and statements applying such

techniques for assessing the true position and performance of entity.

Interpretation of Financial Reports:

According to revenue statements produced on the premise of absorption and marginal

costing, the distinction in outcomes from both techniques is analysed owing to distinct

approaches used in both techniques for fixed costs. The figures of net income in respect of Q1 is

Pound 721000 and Pound 150000 respectively for item A and item B, and on other side in

respect of Q2 these are -40000 and 186500 respectively for item A and item B. While through

absorption costing figures of net income in respect of Q1 is 721650 and 154000 for item A and B

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.