Management Accounting Report: Financial Analysis and Techniques

VerifiedAdded on 2020/06/06

|15

|4498

|87

Report

AI Summary

This report delves into the crucial aspects of management accounting systems, essential for businesses of all sizes. It explores various accounting systems and reporting methods, including performance, accounts receivable, and inventory management reports. The report examines costing methods like cost-volume-profit analysis, flexible budgeting, absorption costing, and marginal costing, analyzing their impact on net profitability. It further discusses the merits and demerits of different budgeting types and the application of the balance scorecard method to address financial issues within Tech Imda Ltd. The report provides a comprehensive analysis of financial transactions, planning, and decision-making processes within an organization, offering valuable insights into effective management accounting practices.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Management accounting and their essential requirement.....................................................1

P2: Different types of reporting method.....................................................................................3

M1: Benefits of accounting system ............................................................................................4

D1: Critical analysis of management accounting reporting method...........................................4

TASK 2............................................................................................................................................4

P3: Methods of costing use in net profitability..........................................................................4

M2: Analysis of management accounting techniques.................................................................7

D2: Apply and analyse data of business activities......................................................................7

TASK 3............................................................................................................................................8

P4: Merits and demerits of various types of budget....................................................................8

M3: Evaluation of planning tools................................................................................................9

D3: Critical analysis to overcome financial issues.....................................................................9

TASK 4............................................................................................................................................9

P5: Balance scorecard method....................................................................................................9

M4: Analysis of financial issues...............................................................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1: Management accounting and their essential requirement.....................................................1

P2: Different types of reporting method.....................................................................................3

M1: Benefits of accounting system ............................................................................................4

D1: Critical analysis of management accounting reporting method...........................................4

TASK 2............................................................................................................................................4

P3: Methods of costing use in net profitability..........................................................................4

M2: Analysis of management accounting techniques.................................................................7

D2: Apply and analyse data of business activities......................................................................7

TASK 3............................................................................................................................................8

P4: Merits and demerits of various types of budget....................................................................8

M3: Evaluation of planning tools................................................................................................9

D3: Critical analysis to overcome financial issues.....................................................................9

TASK 4............................................................................................................................................9

P5: Balance scorecard method....................................................................................................9

M4: Analysis of financial issues...............................................................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

This particular project report is all about explaining crucial aspects related with

management accounting systems. It is an essential part for every business organisation, whether

operating in small or large scale need to use effective system. All financial and non-financial

transaction are recorded into their respective format by using appropriate tools and techniques.

This project report provide vital information about different types of accounting system and

reporting. With the help of various costing methods to analyse net profitability of an organisation

are discuss underneath. Merits and demerits of various budgets those are used in planning

process are explain in this project. Further, this provide valuable information about use of

balance scorecard to overcome all financial problems those are arises in Tech Imda Ltd (Hilton,

and Platt, 2013).

TASK 1

P1: Management accounting and their essential requirement

Nowadays, it has been seen that management is always trying to search for an effective

system which can lead to record all necessary transaction those are incurred during the time. The

primary motive of every department to make use of data in effective manner to increase overall

profitability for Tech Ltd. According to the mentioned case, it has been observed that company

has found that their performance are not going in right direction because of which plenty of

issues are arises in an organisation. To deal with all those, management has decided to appoint a

new trainee management accountant that can help the company face all crucial implications

(Wickramasinghe and Alawattage, 2012). It is an important function which is use to make use of

accounting data for the purpose of making effective planning, organising and evaluating their

overall growth for an organisation. While, accounting is said to be systematic recording of

financial data which summarise in order to make proper transferring information in their

respective made format.

Management accounting is a set format which includes partnering in effective company

decision-making, devising planning and delivery expertise at the time of financial reporting. This

seems to a appropriate system and help managers to take crucial decision in order to attain their

aims and objectives (Management Accounting, 2017). There are various similarities which are

been seen in between management accounting and financial accounting. Both of them are having

1

This particular project report is all about explaining crucial aspects related with

management accounting systems. It is an essential part for every business organisation, whether

operating in small or large scale need to use effective system. All financial and non-financial

transaction are recorded into their respective format by using appropriate tools and techniques.

This project report provide vital information about different types of accounting system and

reporting. With the help of various costing methods to analyse net profitability of an organisation

are discuss underneath. Merits and demerits of various budgets those are used in planning

process are explain in this project. Further, this provide valuable information about use of

balance scorecard to overcome all financial problems those are arises in Tech Imda Ltd (Hilton,

and Platt, 2013).

TASK 1

P1: Management accounting and their essential requirement

Nowadays, it has been seen that management is always trying to search for an effective

system which can lead to record all necessary transaction those are incurred during the time. The

primary motive of every department to make use of data in effective manner to increase overall

profitability for Tech Ltd. According to the mentioned case, it has been observed that company

has found that their performance are not going in right direction because of which plenty of

issues are arises in an organisation. To deal with all those, management has decided to appoint a

new trainee management accountant that can help the company face all crucial implications

(Wickramasinghe and Alawattage, 2012). It is an important function which is use to make use of

accounting data for the purpose of making effective planning, organising and evaluating their

overall growth for an organisation. While, accounting is said to be systematic recording of

financial data which summarise in order to make proper transferring information in their

respective made format.

Management accounting is a set format which includes partnering in effective company

decision-making, devising planning and delivery expertise at the time of financial reporting. This

seems to a appropriate system and help managers to take crucial decision in order to attain their

aims and objectives (Management Accounting, 2017). There are various similarities which are

been seen in between management accounting and financial accounting. Both of them are having

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

their importance that make them difference from one another. This is a appropriate process of

evaluating process of business cost and operations to prepare internal accounting report, record

to take crucial decision in respect to attain overall growth for an organisation.

Basis Management accounting Financial accounting

Meaning Accounting to this particular accounting

systems which is used to deliver crucial

data to the managers to prepare effective

plans and policies.

In this accounting, which assist in

targeting over preparation of financial

statements for Tech Imda in order to

deliver crucial interest to the concern

parties.

Necessity There is less essential for an

organisation to make proper recording

of different accounting data.

This would be provide significant

financial statements to make use of

different accounting data.

Aims This will assist management in crucial

planning and make appropriate decision

through providing specific detail

information on various matters.

Under this report, delivery of financial

data is to external parties to control

external impacts.

Format This seems for particular form of an

organisation to make a well systematic

format to record accounting data.

It is important for every company to make

use of valuable financial transaction in

different statements.

Examples Management accounting reports often

consists of details of companies total

cash, recent generation of sales income

and current state of account payables.

There are certain examples such as

balance sheet summarises the value owns

and owes as of a particular date. Financial

accuracy is being govern by both local and

global accounting standards.

Importance of using management accounting system:

It is an important accounting process of preparing management report and account that

would provide accurate and timely information about financial and statistical data to managers to

make short-term and long term obligations. It will guide and advice management at every single

steps to take valuable decision regarding increasing profitability for the company.

Types of accounting system

2

evaluating process of business cost and operations to prepare internal accounting report, record

to take crucial decision in respect to attain overall growth for an organisation.

Basis Management accounting Financial accounting

Meaning Accounting to this particular accounting

systems which is used to deliver crucial

data to the managers to prepare effective

plans and policies.

In this accounting, which assist in

targeting over preparation of financial

statements for Tech Imda in order to

deliver crucial interest to the concern

parties.

Necessity There is less essential for an

organisation to make proper recording

of different accounting data.

This would be provide significant

financial statements to make use of

different accounting data.

Aims This will assist management in crucial

planning and make appropriate decision

through providing specific detail

information on various matters.

Under this report, delivery of financial

data is to external parties to control

external impacts.

Format This seems for particular form of an

organisation to make a well systematic

format to record accounting data.

It is important for every company to make

use of valuable financial transaction in

different statements.

Examples Management accounting reports often

consists of details of companies total

cash, recent generation of sales income

and current state of account payables.

There are certain examples such as

balance sheet summarises the value owns

and owes as of a particular date. Financial

accuracy is being govern by both local and

global accounting standards.

Importance of using management accounting system:

It is an important accounting process of preparing management report and account that

would provide accurate and timely information about financial and statistical data to managers to

make short-term and long term obligations. It will guide and advice management at every single

steps to take valuable decision regarding increasing profitability for the company.

Types of accounting system

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

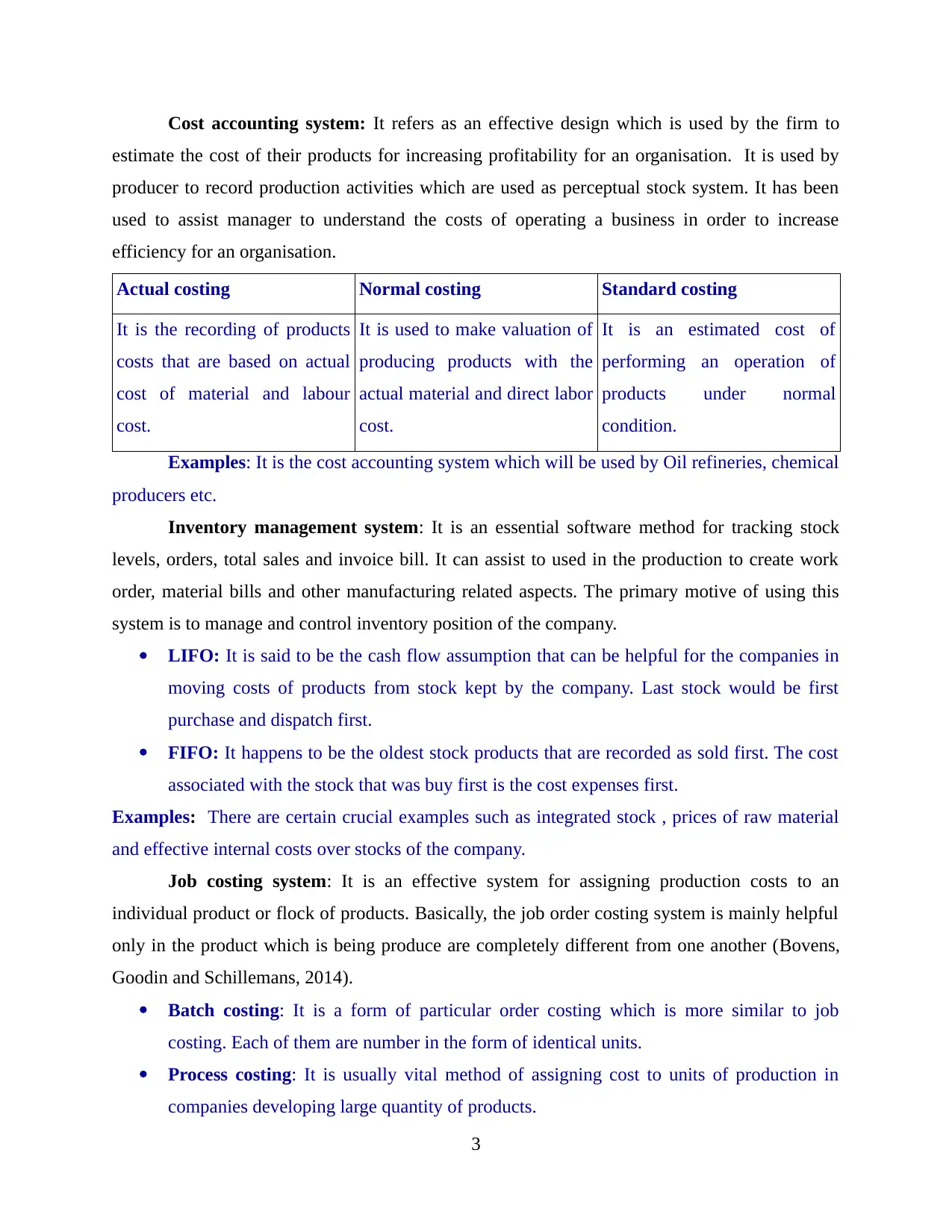

Cost accounting system: It refers as an effective design which is used by the firm to

estimate the cost of their products for increasing profitability for an organisation. It is used by

producer to record production activities which are used as perceptual stock system. It has been

used to assist manager to understand the costs of operating a business in order to increase

efficiency for an organisation.

Actual costing Normal costing Standard costing

It is the recording of products

costs that are based on actual

cost of material and labour

cost.

It is used to make valuation of

producing products with the

actual material and direct labor

cost.

It is an estimated cost of

performing an operation of

products under normal

condition.

Examples: It is the cost accounting system which will be used by Oil refineries, chemical

producers etc.

Inventory management system: It is an essential software method for tracking stock

levels, orders, total sales and invoice bill. It can assist to used in the production to create work

order, material bills and other manufacturing related aspects. The primary motive of using this

system is to manage and control inventory position of the company.

LIFO: It is said to be the cash flow assumption that can be helpful for the companies in

moving costs of products from stock kept by the company. Last stock would be first

purchase and dispatch first.

FIFO: It happens to be the oldest stock products that are recorded as sold first. The cost

associated with the stock that was buy first is the cost expenses first.

Examples: There are certain crucial examples such as integrated stock , prices of raw material

and effective internal costs over stocks of the company.

Job costing system: It is an effective system for assigning production costs to an

individual product or flock of products. Basically, the job order costing system is mainly helpful

only in the product which is being produce are completely different from one another (Bovens,

Goodin and Schillemans, 2014).

Batch costing: It is a form of particular order costing which is more similar to job

costing. Each of them are number in the form of identical units.

Process costing: It is usually vital method of assigning cost to units of production in

companies developing large quantity of products.

3

estimate the cost of their products for increasing profitability for an organisation. It is used by

producer to record production activities which are used as perceptual stock system. It has been

used to assist manager to understand the costs of operating a business in order to increase

efficiency for an organisation.

Actual costing Normal costing Standard costing

It is the recording of products

costs that are based on actual

cost of material and labour

cost.

It is used to make valuation of

producing products with the

actual material and direct labor

cost.

It is an estimated cost of

performing an operation of

products under normal

condition.

Examples: It is the cost accounting system which will be used by Oil refineries, chemical

producers etc.

Inventory management system: It is an essential software method for tracking stock

levels, orders, total sales and invoice bill. It can assist to used in the production to create work

order, material bills and other manufacturing related aspects. The primary motive of using this

system is to manage and control inventory position of the company.

LIFO: It is said to be the cash flow assumption that can be helpful for the companies in

moving costs of products from stock kept by the company. Last stock would be first

purchase and dispatch first.

FIFO: It happens to be the oldest stock products that are recorded as sold first. The cost

associated with the stock that was buy first is the cost expenses first.

Examples: There are certain crucial examples such as integrated stock , prices of raw material

and effective internal costs over stocks of the company.

Job costing system: It is an effective system for assigning production costs to an

individual product or flock of products. Basically, the job order costing system is mainly helpful

only in the product which is being produce are completely different from one another (Bovens,

Goodin and Schillemans, 2014).

Batch costing: It is a form of particular order costing which is more similar to job

costing. Each of them are number in the form of identical units.

Process costing: It is usually vital method of assigning cost to units of production in

companies developing large quantity of products.

3

Examples: It is used as building construction industry hence each building must be unique.

P2: Different types of reporting method

In accordance with increasing more effective outcome for Tech UK by using valuable

methods of reporting. The main aim of managers is to make sure that every data those are being

taken from every financial department must be analyse in their respective statements. It has been

seen that these reports are more crucial for an organisation because on that basis most of the

investors and stakeholder would be able to make their future capital investment decisions. The

financial position of the company would be analyse in an effective manner in order to maintain

the position during the last couple of year. On the basis of that there are various important

aspects those are essential for increasing overall profitability for an organisation. There are

various types of accounting reporting system use by the company. Some of them are discussed

underneath:

Performance report: It is one of the important report which is used to make proper

comparison of the actual performance with the previous one. They need to reach to a valuable

solution to incur more effective ways to increase overall productivity of an organisation. For this

purpose, management can uses various key performance indicators and other effective tools and

techniques for the company (Christ, 2014).

Account receivable report: This report will provide important data regarding total lists

of unpaid customers invoices and credit memos. Through this, company would be able to make

easily valuation of total time of recovery regarding overdue payment can examine in more

effectively.

Inventory management report: Such kind of accounting report is more helpful for an

operational stage of department as they are working totally on overall capacity of total inventory

position. On the basis of total position of stock which they can delivery in accordance to increase

desire output. There are various tools and techniques available in order to manage their total

inventory position. Such as stock turnover ratio, ABC costing and other important method.

Job cost report: This particular report is useful for the production management in order

to determine total cost a company is going to incur on the production of an individual and group

of products. It happens to be an important aspect for the department to make use of financial

transactions in an effective manner.

4

P2: Different types of reporting method

In accordance with increasing more effective outcome for Tech UK by using valuable

methods of reporting. The main aim of managers is to make sure that every data those are being

taken from every financial department must be analyse in their respective statements. It has been

seen that these reports are more crucial for an organisation because on that basis most of the

investors and stakeholder would be able to make their future capital investment decisions. The

financial position of the company would be analyse in an effective manner in order to maintain

the position during the last couple of year. On the basis of that there are various important

aspects those are essential for increasing overall profitability for an organisation. There are

various types of accounting reporting system use by the company. Some of them are discussed

underneath:

Performance report: It is one of the important report which is used to make proper

comparison of the actual performance with the previous one. They need to reach to a valuable

solution to incur more effective ways to increase overall productivity of an organisation. For this

purpose, management can uses various key performance indicators and other effective tools and

techniques for the company (Christ, 2014).

Account receivable report: This report will provide important data regarding total lists

of unpaid customers invoices and credit memos. Through this, company would be able to make

easily valuation of total time of recovery regarding overdue payment can examine in more

effectively.

Inventory management report: Such kind of accounting report is more helpful for an

operational stage of department as they are working totally on overall capacity of total inventory

position. On the basis of total position of stock which they can delivery in accordance to increase

desire output. There are various tools and techniques available in order to manage their total

inventory position. Such as stock turnover ratio, ABC costing and other important method.

Job cost report: This particular report is useful for the production management in order

to determine total cost a company is going to incur on the production of an individual and group

of products. It happens to be an important aspect for the department to make use of financial

transactions in an effective manner.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

M1: Benefits of accounting system

Every organisation is using appropriate accounting systems in order to record their

crucial financial transaction in more effective and safe manner. All the above discuss accounting

system are having their own importance which will make them different from one another. Such

as cost accounting would be liable to analyse total cost and expenditure Tech Imda is use during

the production process. While some other like inventory management and job cost are having

major influence to the department.

D1: Critical analysis of management accounting reporting method

It has been determine that every data collected by the manager for the purpose of

preparing reports analyse in an effective manner. All important report which are discuss in the

above report are providing valuable information to the company. This will assist investors to

make crucial decision regarding their capital investments in various projects of the company.

Performance report are needed to be analyse in regular basis.

TASK 2

P3: Methods of costing use in net profitability

Cost is an essential aspect for an organisation which is related with production of

products and services. It is directly related with the company. This seems to make use of

microeconomic aspects in their business operations to get more valuable results during the period

of time (Zang, 2011). In context to this, there are various cost related aspects are needed to taken

into consideration. Some of them are discuss underneath:

Cost volume profit(CVP): It is an essential tools which is help for measuring different

alternation in costs and total volume which would affect operating incomes of an organisation.

Flexible budgeting: This seems to be related with adjusted or flexes aspects that changes

in more effective manner as compare to static budget.

Absorption costing: This particular costing method is applicable over the production of

product and service by considering all factors. It will consists of both variable and fixed cost.

Marginal costing: According to this particular costing techniques which is use by

manager during the time of producing an additional product. As this costs is mainly related with

variable cost and fixed costs are apportioned (Chen and et. al., 2011).

Income statement on the basis of Marginal costing method:

5

Every organisation is using appropriate accounting systems in order to record their

crucial financial transaction in more effective and safe manner. All the above discuss accounting

system are having their own importance which will make them different from one another. Such

as cost accounting would be liable to analyse total cost and expenditure Tech Imda is use during

the production process. While some other like inventory management and job cost are having

major influence to the department.

D1: Critical analysis of management accounting reporting method

It has been determine that every data collected by the manager for the purpose of

preparing reports analyse in an effective manner. All important report which are discuss in the

above report are providing valuable information to the company. This will assist investors to

make crucial decision regarding their capital investments in various projects of the company.

Performance report are needed to be analyse in regular basis.

TASK 2

P3: Methods of costing use in net profitability

Cost is an essential aspect for an organisation which is related with production of

products and services. It is directly related with the company. This seems to make use of

microeconomic aspects in their business operations to get more valuable results during the period

of time (Zang, 2011). In context to this, there are various cost related aspects are needed to taken

into consideration. Some of them are discuss underneath:

Cost volume profit(CVP): It is an essential tools which is help for measuring different

alternation in costs and total volume which would affect operating incomes of an organisation.

Flexible budgeting: This seems to be related with adjusted or flexes aspects that changes

in more effective manner as compare to static budget.

Absorption costing: This particular costing method is applicable over the production of

product and service by considering all factors. It will consists of both variable and fixed cost.

Marginal costing: According to this particular costing techniques which is use by

manager during the time of producing an additional product. As this costs is mainly related with

variable cost and fixed costs are apportioned (Chen and et. al., 2011).

Income statement on the basis of Marginal costing method:

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

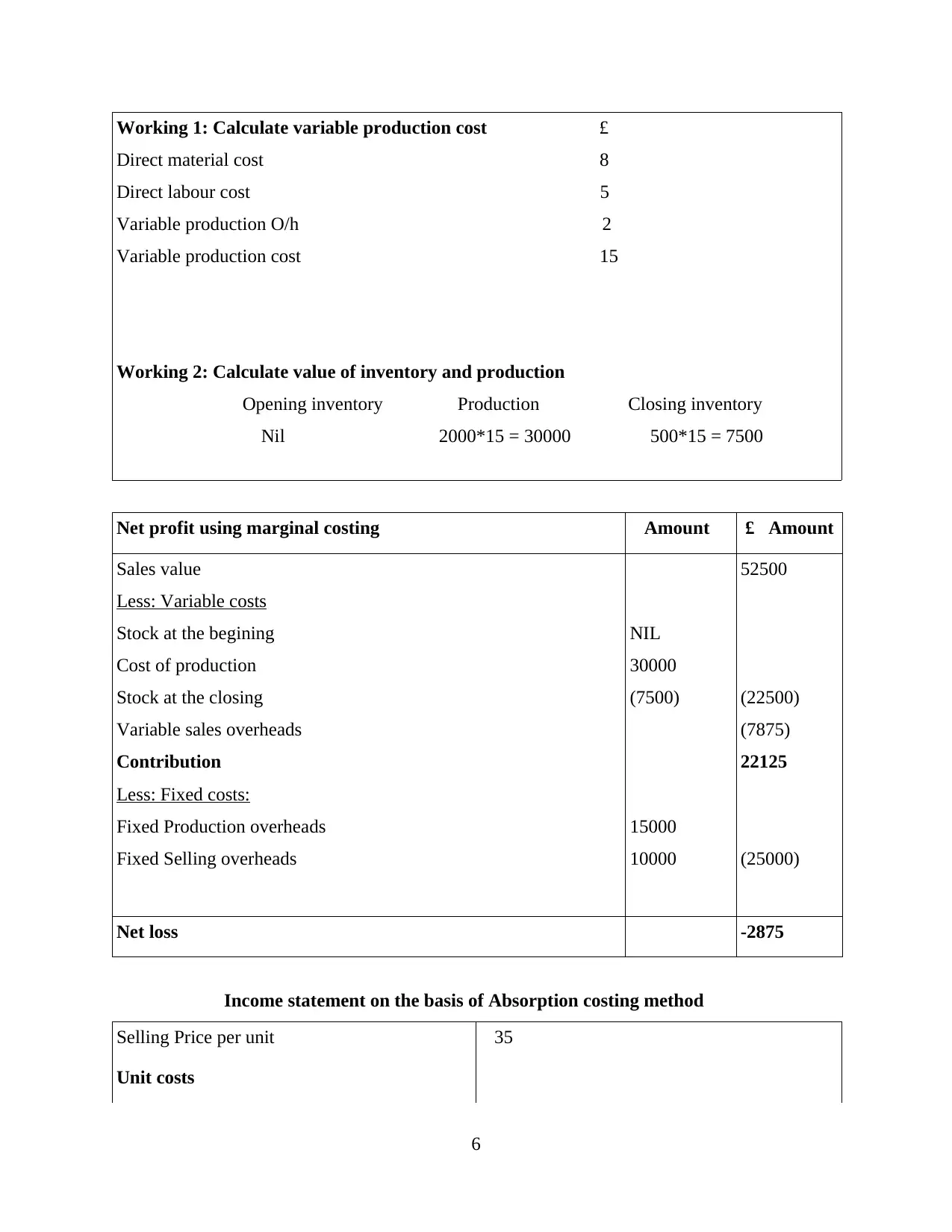

Working 1: Calculate variable production cost £

Direct material cost 8

Direct labour cost 5

Variable production O/h 2

Variable production cost 15

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

Nil 2000*15 = 30000 500*15 = 7500

Net profit using marginal costing £Amount £ Amount

Sales value

Less: Variable costs

Stock at the begining

Cost of production

Stock at the closing

Variable sales overheads

Contribution

Less: Fixed costs:

Fixed Production overheads

Fixed Selling overheads

NIL

30000

(7500)

15000

10000

52500

(22500)

(7875)

22125

(25000)

Net loss -2875

Income statement on the basis of Absorption costing method

Selling Price per unit £35

Unit costs

6

Direct material cost 8

Direct labour cost 5

Variable production O/h 2

Variable production cost 15

Working 2: Calculate value of inventory and production

Opening inventory Production Closing inventory

Nil 2000*15 = 30000 500*15 = 7500

Net profit using marginal costing £Amount £ Amount

Sales value

Less: Variable costs

Stock at the begining

Cost of production

Stock at the closing

Variable sales overheads

Contribution

Less: Fixed costs:

Fixed Production overheads

Fixed Selling overheads

NIL

30000

(7500)

15000

10000

52500

(22500)

(7875)

22125

(25000)

Net loss -2875

Income statement on the basis of Absorption costing method

Selling Price per unit £35

Unit costs

6

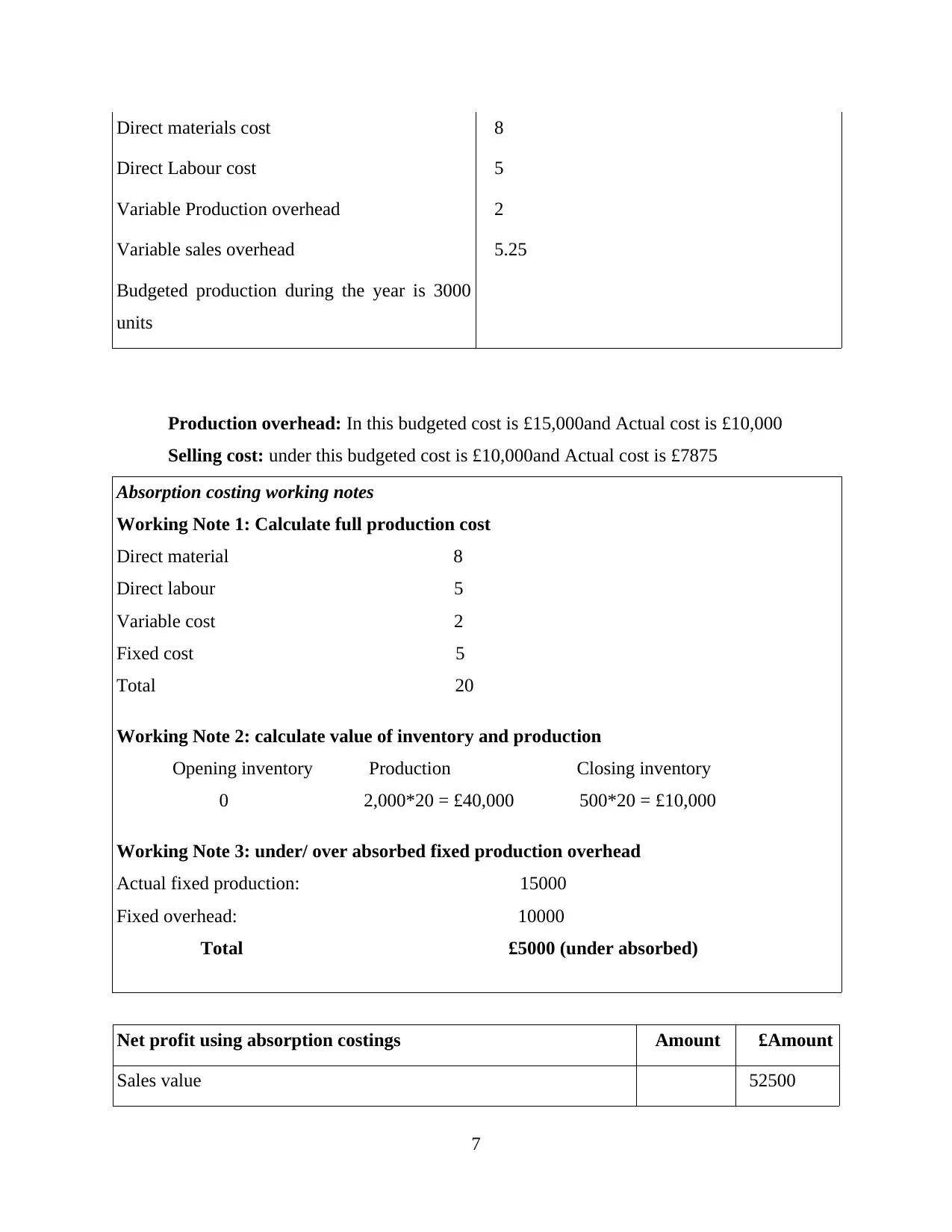

Direct materials cost £8

Direct Labour cost £5

Variable Production overhead £2

Variable sales overhead £5.25

Budgeted production during the year is 3000

units

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Selling cost: under this budgeted cost is £10,000and Actual cost is £7875

Absorption costing working notes

Working Note 1: Calculate full production cost

Direct material £8

Direct labour £5

Variable cost £2

Fixed cost £5

Total £20

Working Note 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40,000 500*20 = £10,000

Working Note 3: under/ over absorbed fixed production overhead

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000 (under absorbed)

Net profit using absorption costings £Amount £Amount

Sales value 52500

7

Direct Labour cost £5

Variable Production overhead £2

Variable sales overhead £5.25

Budgeted production during the year is 3000

units

Production overhead: In this budgeted cost is £15,000and Actual cost is £10,000

Selling cost: under this budgeted cost is £10,000and Actual cost is £7875

Absorption costing working notes

Working Note 1: Calculate full production cost

Direct material £8

Direct labour £5

Variable cost £2

Fixed cost £5

Total £20

Working Note 2: calculate value of inventory and production

Opening inventory Production Closing inventory

0 2,000*20 = £40,000 500*20 = £10,000

Working Note 3: under/ over absorbed fixed production overhead

Actual fixed production: £15000

Fixed overhead: £10000

Total £5000 (under absorbed)

Net profit using absorption costings £Amount £Amount

Sales value 52500

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

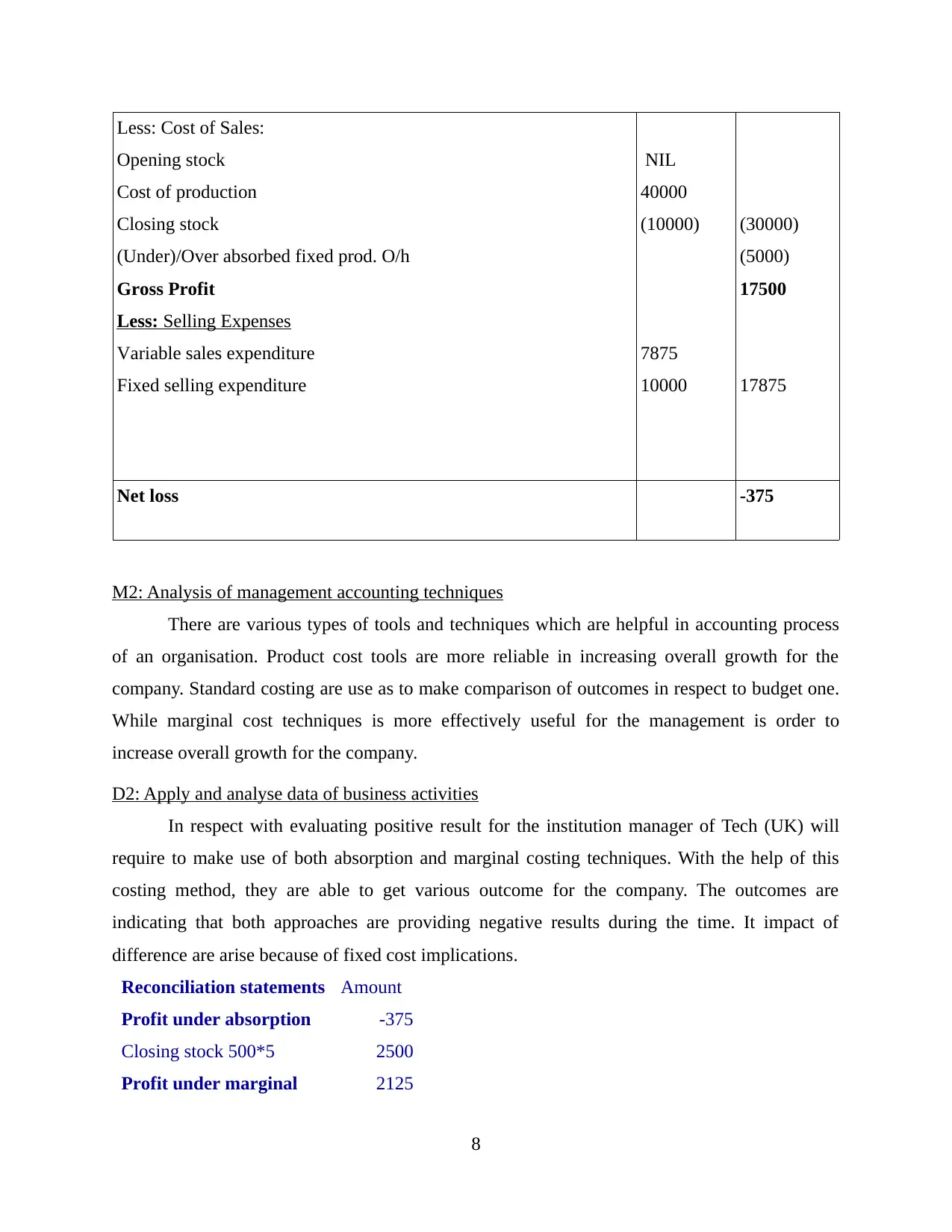

Less: Cost of Sales:

Opening stock

Cost of production

Closing stock

(Under)/Over absorbed fixed prod. O/h

Gross Profit

Less: Selling Expenses

Variable sales expenditure

Fixed selling expenditure

NIL

40000

(10000)

7875

10000

(30000)

(5000)

17500

17875

Net loss -375

M2: Analysis of management accounting techniques

There are various types of tools and techniques which are helpful in accounting process

of an organisation. Product cost tools are more reliable in increasing overall growth for the

company. Standard costing are use as to make comparison of outcomes in respect to budget one.

While marginal cost techniques is more effectively useful for the management is order to

increase overall growth for the company.

D2: Apply and analyse data of business activities

In respect with evaluating positive result for the institution manager of Tech (UK) will

require to make use of both absorption and marginal costing techniques. With the help of this

costing method, they are able to get various outcome for the company. The outcomes are

indicating that both approaches are providing negative results during the time. It impact of

difference are arise because of fixed cost implications.

Reconciliation statements Amount

Profit under absorption -375

Closing stock 500*5 2500

Profit under marginal 2125

8

Opening stock

Cost of production

Closing stock

(Under)/Over absorbed fixed prod. O/h

Gross Profit

Less: Selling Expenses

Variable sales expenditure

Fixed selling expenditure

NIL

40000

(10000)

7875

10000

(30000)

(5000)

17500

17875

Net loss -375

M2: Analysis of management accounting techniques

There are various types of tools and techniques which are helpful in accounting process

of an organisation. Product cost tools are more reliable in increasing overall growth for the

company. Standard costing are use as to make comparison of outcomes in respect to budget one.

While marginal cost techniques is more effectively useful for the management is order to

increase overall growth for the company.

D2: Apply and analyse data of business activities

In respect with evaluating positive result for the institution manager of Tech (UK) will

require to make use of both absorption and marginal costing techniques. With the help of this

costing method, they are able to get various outcome for the company. The outcomes are

indicating that both approaches are providing negative results during the time. It impact of

difference are arise because of fixed cost implications.

Reconciliation statements Amount

Profit under absorption -375

Closing stock 500*5 2500

Profit under marginal 2125

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

From the above analysis, it has been seen that the net profit getting from marginal costs is

about 2125. The differences is arises because of fixed treatments.

TASK 3

P4: Merits and demerits of various types of budget

Planning is an important part for every business concern in order to analyse their budgets

in more effective manner. It will be formulate by using information about total sales and revenue

generated by the company during the time. Some budget are:

Operation budget: An operational budget is said to be proper estimation and evaluation

of projected income and expenses over the period of time. This will create accurate image for

calculating total sales, production and labour cost or management expenses.

Advantage: These are mainly create on weekly, monthly or annual basis. This will use to

make comparison to data in more effective manner (Otley and Emmanuel, 2013).

Disadvantage: This type of budget consist of various aspects such as experiences

manager that may attempt to implement budgeted slack.

Cash flow statement: It is an effective means of projecting about total inflows and

outflow comes into the business within a definite period of time. It would be helpful to a

company to determine whether sufficient amount of cash is available with Tech UK to operate

their daily operations.

Advantage: This type of cash is responsible for evaluation, whether cash balance would

remain sufficient to fulfil continuous obligations for the company.

Disadvantage: It would cause distortions. This seems to be not equate to profit for the

company. It relies on estimation of data (Lukka and Vinnari, 2014).

Rolling budget: It is known as one of the effective update which consists of a new

budget as recent budget period get completed. It involves additive extension of existent budget

model.

Advantage: It is used to reduce primary elements of uncertainty in budgeting because

they are having detail information of planning and controlling on coming future period of time.

Disadvantage: It used to consider more time, effort and money while preparation of

budget for the company (Akbar, 2010).

9

about 2125. The differences is arises because of fixed treatments.

TASK 3

P4: Merits and demerits of various types of budget

Planning is an important part for every business concern in order to analyse their budgets

in more effective manner. It will be formulate by using information about total sales and revenue

generated by the company during the time. Some budget are:

Operation budget: An operational budget is said to be proper estimation and evaluation

of projected income and expenses over the period of time. This will create accurate image for

calculating total sales, production and labour cost or management expenses.

Advantage: These are mainly create on weekly, monthly or annual basis. This will use to

make comparison to data in more effective manner (Otley and Emmanuel, 2013).

Disadvantage: This type of budget consist of various aspects such as experiences

manager that may attempt to implement budgeted slack.

Cash flow statement: It is an effective means of projecting about total inflows and

outflow comes into the business within a definite period of time. It would be helpful to a

company to determine whether sufficient amount of cash is available with Tech UK to operate

their daily operations.

Advantage: This type of cash is responsible for evaluation, whether cash balance would

remain sufficient to fulfil continuous obligations for the company.

Disadvantage: It would cause distortions. This seems to be not equate to profit for the

company. It relies on estimation of data (Lukka and Vinnari, 2014).

Rolling budget: It is known as one of the effective update which consists of a new

budget as recent budget period get completed. It involves additive extension of existent budget

model.

Advantage: It is used to reduce primary elements of uncertainty in budgeting because

they are having detail information of planning and controlling on coming future period of time.

Disadvantage: It used to consider more time, effort and money while preparation of

budget for the company (Akbar, 2010).

9

Fixed budget: It happens to be utmost important budget that cannot be changes during

sales or other activities which is being increasing at the same period of time.

Advantages: This is used to measure success of small business transactions that are done

during an accounting period of time.

Disadvantage: It has been found that it does not continuous or work of unpredictable

activities.

Process of budget:

In the initial process, proper prediction of budget need can be examine.

On the basis of companies total estimation all income and expenditure collected from

various department are send to the upper level.

After taking prior permission from upper authority, process of budget development get

started to implement.

Completion of budget, it has been again set to top management for the further approval.

At the end, certain reviews would be collected out of budget from various employees and

staffs.

Pricing system:

There are various types of pricing methods which are discuss underneath:

Price skimming: It is an essential pricing method that assist in enhancing total sales

generated from products and services. In initial stage, prices are more high.

Economic pricing: It is an effective techniques for an organisation which is used to set

effective price as low for their different products in order to attract most of the people

(Bodie, 2013).

M3: Evaluation of planning tools

It is necessary to determine necessary aspect for every business enterprises. By this,

future estimation can be examine through attaining by taking simple steps in more effective

manner. There are certain effective ways through which budgets can be managed. Such as

forecasting tools which is helpful to identify total estimation of cost and expenses. Contingency

tools are use to analyse overall risk of the company.

D3: Critical analysis to overcome financial issues

In respect to increase profitability for Tech UK, it is crucial to make evaluation of their

financial problem those are going to affect their business operations. In order to deal with every

10

sales or other activities which is being increasing at the same period of time.

Advantages: This is used to measure success of small business transactions that are done

during an accounting period of time.

Disadvantage: It has been found that it does not continuous or work of unpredictable

activities.

Process of budget:

In the initial process, proper prediction of budget need can be examine.

On the basis of companies total estimation all income and expenditure collected from

various department are send to the upper level.

After taking prior permission from upper authority, process of budget development get

started to implement.

Completion of budget, it has been again set to top management for the further approval.

At the end, certain reviews would be collected out of budget from various employees and

staffs.

Pricing system:

There are various types of pricing methods which are discuss underneath:

Price skimming: It is an essential pricing method that assist in enhancing total sales

generated from products and services. In initial stage, prices are more high.

Economic pricing: It is an effective techniques for an organisation which is used to set

effective price as low for their different products in order to attract most of the people

(Bodie, 2013).

M3: Evaluation of planning tools

It is necessary to determine necessary aspect for every business enterprises. By this,

future estimation can be examine through attaining by taking simple steps in more effective

manner. There are certain effective ways through which budgets can be managed. Such as

forecasting tools which is helpful to identify total estimation of cost and expenses. Contingency

tools are use to analyse overall risk of the company.

D3: Critical analysis to overcome financial issues

In respect to increase profitability for Tech UK, it is crucial to make evaluation of their

financial problem those are going to affect their business operations. In order to deal with every

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.