Management Accounting: Principles, Techniques, and Budgetary Control

VerifiedAdded on 2020/06/06

|12

|3397

|60

Report

AI Summary

This report explores key aspects of management accounting, starting with an introduction to its principles and importance within an organizational context. It delves into various methods and techniques used for management accounting reporting, including budgetary reports and account receivable reporting. The report then analyzes profit calculation using both absorption and marginal costing techniques, providing detailed calculations. Furthermore, it examines the advantages and disadvantages of different planning tools employed in budgetary control. Finally, the report discusses how organizations can apply management accounting to address financial problems, offering a comprehensive overview of the subject. The report is a valuable resource for students and professionals seeking to understand and apply management accounting principles in real-world scenarios.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Principle of management accounting and importance of management accounting in

organisational context.................................................................................................................1

P2. Different methods and techniques used for management accounting reporting...................2

TASK 2............................................................................................................................................4

P3 Analysation of profit by using absorption and marginal costing technique..........................4

TASK 3............................................................................................................................................5

P4 Advantages and disadvantages of various type of planning tools used in budgetary control5

P5 Ways in which organisations could apply the management accounting to respond financial

problems......................................................................................................................................7

CONCLUSION ...............................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION...........................................................................................................................1

TASK 1............................................................................................................................................1

P1. Principle of management accounting and importance of management accounting in

organisational context.................................................................................................................1

P2. Different methods and techniques used for management accounting reporting...................2

TASK 2............................................................................................................................................4

P3 Analysation of profit by using absorption and marginal costing technique..........................4

TASK 3............................................................................................................................................5

P4 Advantages and disadvantages of various type of planning tools used in budgetary control5

P5 Ways in which organisations could apply the management accounting to respond financial

problems......................................................................................................................................7

CONCLUSION ...............................................................................................................................8

REFERENCES................................................................................................................................9

INTRODUCTION

Management accounting is a concept adopted by the managers and accountants to support

the structure of organisation (Routledge, Tucker and Lowe, 2014). As per chaining business

requirement scope of management accounting has become vast. Objective of this project is to

define the principle of management accounting which is applied on organisations. Importance of

management accounting subject to integrate accounting system within an organisation. Various

types of methods used for management accounting reporting are also defined in this context.

Calculation of profit by using marginal and absorption costing are discussed here as well.

Advantages and disadvantages of planning tools used in budgetary control are also elaborated.

Ways to adapt management accounting system within organisation are also illustrated here.

TASK 1

P1. Principle of management accounting and importance of management accounting in

organisational context

Management accounting

Management accounting system is a tool used in organisation to assist managers and

accountants to deal with day to day business transactions and business problems. Various types

of definitions and descriptions are given in respect of management accounting system and

management accounting principles. Basically, the management accounting principles are formed

to support the structure of business subjected to decision making, strategic planning and internal

business process with utilisation of resources as well as capacity of organisation to improve the

decision support system to accomplish organisational goals.

Features of management accounting

Management accounting remain Helpful in decision making

Provides accurate information and details rather then decisions

It has selective nature

it assist managers and accountants to make effective plans to attain objectives

this accounting system basically remain associated with future events and forecast

it increase the efficiency level of organisation in respect of performance

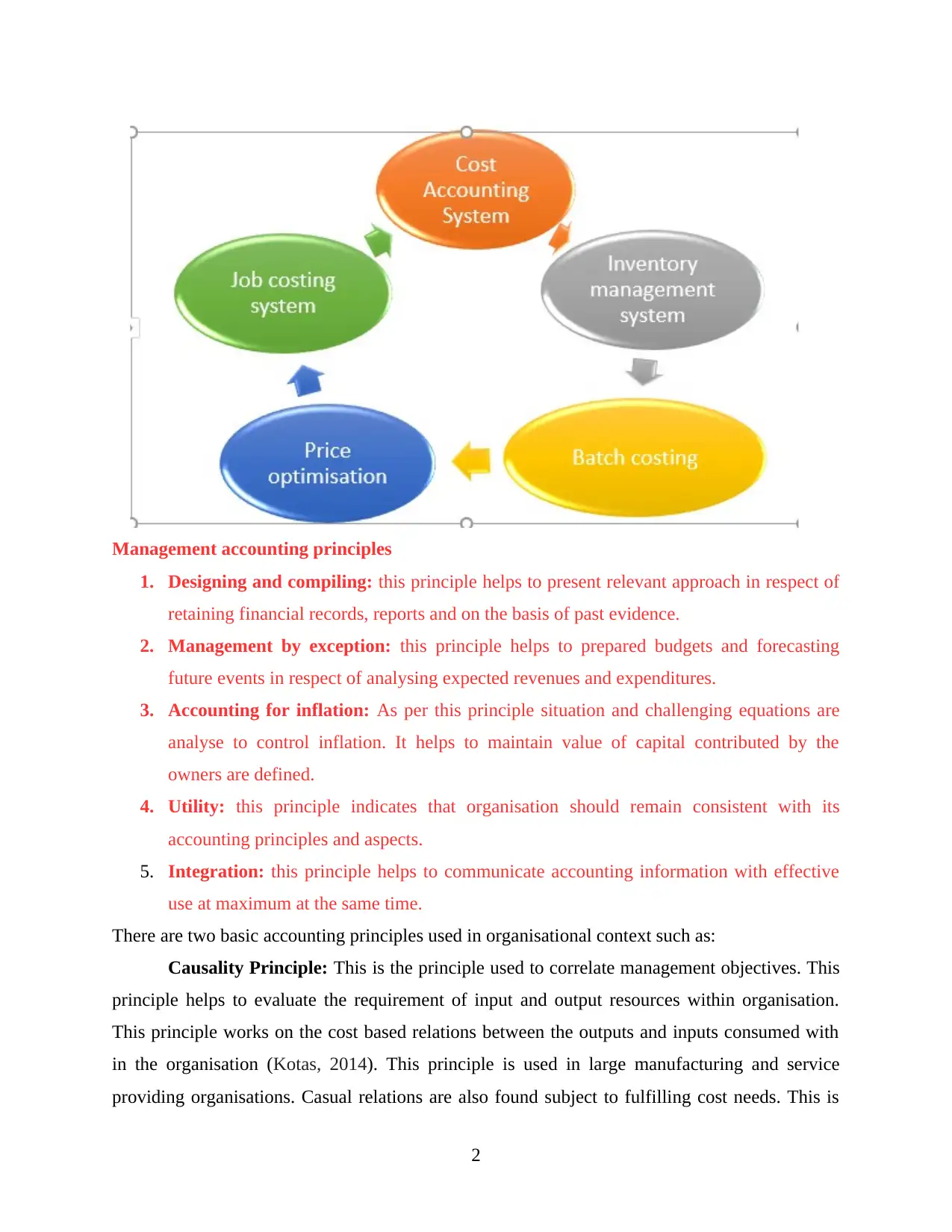

Management accounting system (Chart)

1

Management accounting is a concept adopted by the managers and accountants to support

the structure of organisation (Routledge, Tucker and Lowe, 2014). As per chaining business

requirement scope of management accounting has become vast. Objective of this project is to

define the principle of management accounting which is applied on organisations. Importance of

management accounting subject to integrate accounting system within an organisation. Various

types of methods used for management accounting reporting are also defined in this context.

Calculation of profit by using marginal and absorption costing are discussed here as well.

Advantages and disadvantages of planning tools used in budgetary control are also elaborated.

Ways to adapt management accounting system within organisation are also illustrated here.

TASK 1

P1. Principle of management accounting and importance of management accounting in

organisational context

Management accounting

Management accounting system is a tool used in organisation to assist managers and

accountants to deal with day to day business transactions and business problems. Various types

of definitions and descriptions are given in respect of management accounting system and

management accounting principles. Basically, the management accounting principles are formed

to support the structure of business subjected to decision making, strategic planning and internal

business process with utilisation of resources as well as capacity of organisation to improve the

decision support system to accomplish organisational goals.

Features of management accounting

Management accounting remain Helpful in decision making

Provides accurate information and details rather then decisions

It has selective nature

it assist managers and accountants to make effective plans to attain objectives

this accounting system basically remain associated with future events and forecast

it increase the efficiency level of organisation in respect of performance

Management accounting system (Chart)

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Management accounting principles

1. Designing and compiling: this principle helps to present relevant approach in respect of

retaining financial records, reports and on the basis of past evidence.

2. Management by exception: this principle helps to prepared budgets and forecasting

future events in respect of analysing expected revenues and expenditures.

3. Accounting for inflation: As per this principle situation and challenging equations are

analyse to control inflation. It helps to maintain value of capital contributed by the

owners are defined.

4. Utility: this principle indicates that organisation should remain consistent with its

accounting principles and aspects.

5. Integration: this principle helps to communicate accounting information with effective

use at maximum at the same time.

There are two basic accounting principles used in organisational context such as:

Causality Principle: This is the principle used to correlate management objectives. This

principle helps to evaluate the requirement of input and output resources within organisation.

This principle works on the cost based relations between the outputs and inputs consumed with

in the organisation (Kotas, 2014). This principle is used in large manufacturing and service

providing organisations. Casual relations are also found subject to fulfilling cost needs. This is

2

1. Designing and compiling: this principle helps to present relevant approach in respect of

retaining financial records, reports and on the basis of past evidence.

2. Management by exception: this principle helps to prepared budgets and forecasting

future events in respect of analysing expected revenues and expenditures.

3. Accounting for inflation: As per this principle situation and challenging equations are

analyse to control inflation. It helps to maintain value of capital contributed by the

owners are defined.

4. Utility: this principle indicates that organisation should remain consistent with its

accounting principles and aspects.

5. Integration: this principle helps to communicate accounting information with effective

use at maximum at the same time.

There are two basic accounting principles used in organisational context such as:

Causality Principle: This is the principle used to correlate management objectives. This

principle helps to evaluate the requirement of input and output resources within organisation.

This principle works on the cost based relations between the outputs and inputs consumed with

in the organisation (Kotas, 2014). This principle is used in large manufacturing and service

providing organisations. Casual relations are also found subject to fulfilling cost needs. This is

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

often straight forward to deal with strong relations in between inputs and outputs of products and

services.

Analogy principle: This principle is used by the organisations to communicate past and

future outcomes. This principle is governed by the main user of management accounting system.

This helps the managers to find out difference between past and future outcomes and assist

managers to make future plans and strategic planning (Granlund, 2011).

Concept of management accounting

There are some concepts used in applicability to causality and modelling principles such

as attributable, capacity, cost, homogeneity, managerial objective, integrated data

orientation, resources, responsiveness, traceability and work.

Analogy principle contains the concept of avoid ability, interdependence and

interchangeability.

Essential requirement of management accounting

To sort accounting equations and making growth and development plans.

Making strategies and plans for better forecast and estimation

Management decisions and plans depends upon information which are provided by

various type of management accoutring system.

Making financial statements and reports for analyse financial performance of

organisation

To assist managers and accountants in taking decisions for better growth and

development.

Importance of Management accounting subject to integrate management accounting

system within an organisation:

Management accounting system is helpful to resolve the complex and critical problems,

issues and conflicts of an organisation (Benson and et. al., 2015). This system supports the

internal divisions and departments of the organisation to control and evaluate the business

strategies and plans. It assists the senior management level for making and preparing competitive

decision making process and company’s strategy. Management accounting system provides a

path to management accountants subjected to business problems and issues. This provides an

overall overview and analysis to managers subject to financial accountants, tax accountants and

internal auditors.

3

services.

Analogy principle: This principle is used by the organisations to communicate past and

future outcomes. This principle is governed by the main user of management accounting system.

This helps the managers to find out difference between past and future outcomes and assist

managers to make future plans and strategic planning (Granlund, 2011).

Concept of management accounting

There are some concepts used in applicability to causality and modelling principles such

as attributable, capacity, cost, homogeneity, managerial objective, integrated data

orientation, resources, responsiveness, traceability and work.

Analogy principle contains the concept of avoid ability, interdependence and

interchangeability.

Essential requirement of management accounting

To sort accounting equations and making growth and development plans.

Making strategies and plans for better forecast and estimation

Management decisions and plans depends upon information which are provided by

various type of management accoutring system.

Making financial statements and reports for analyse financial performance of

organisation

To assist managers and accountants in taking decisions for better growth and

development.

Importance of Management accounting subject to integrate management accounting

system within an organisation:

Management accounting system is helpful to resolve the complex and critical problems,

issues and conflicts of an organisation (Benson and et. al., 2015). This system supports the

internal divisions and departments of the organisation to control and evaluate the business

strategies and plans. It assists the senior management level for making and preparing competitive

decision making process and company’s strategy. Management accounting system provides a

path to management accountants subjected to business problems and issues. This provides an

overall overview and analysis to managers subject to financial accountants, tax accountants and

internal auditors.

3

This not only improves the capability and strengths to think properly and effectively but

also supports professional and marketing managers to deal with uncertain market situations. In

multinational and global organisations, managerial accounting system is found in an integrated

form. Organisational divisions and departments remain bifurcated as per the nature and type but

remain integrated as per management’s point of view. Management accounting system is an

essential requirement to an organisation to build ethical managerial relations within departments

and divisions of an organisation.

P2. Different methods and techniques used for management accounting reporting

Management accounting reporting is one of the managerial works which is done by the

cost accountants and departmental managers (Sargent, Borthick and Lederberg, 2011.).

Accountants and managers prepare the accounting reports and submit these to the senior level

management. Senior managers are the experts and specialists who analyse and evaluate the

reports as well as make strategies and plans. Management accounting reports are used in decision

making process and in making competitive strategies as well. Below are some methods and

techniques are defined helps in decision making process:

Budgetary reports: This is one of the common techniques which is used by the

organisation to analyse and evaluate future opportunities. Budgets present the future planning

and strategic management subjected to organisational goals and objectives. Budgetary reports

contain the information related to projected income and expenditure subjected to management

and operations. Budgets provide the prior information to managers and accountants about future

events and projects.

Account receivable reporting: This reporting method helps to trace the records of

debtors and collection receivables from buyers and customers. Account receivable reports assist

the managers and accountants to decide the payback period of debtors (Parker, 2012). These

reports are prepared with the help of cash flow statements, sales records, debtor’s information

and records. With help of account receivable reports, managers become eligible to decide the pay

back policy to debtor. Basically, the payback policies are used by the organisation such as 30, 60

and 90 days policy. This reporting technique helps to sort out the issues that occur in collection

process.

Job cost report methods: These reports are produced by the production and

manufacturing departments of an organisation. This is the technique used to sort out the plans

4

also supports professional and marketing managers to deal with uncertain market situations. In

multinational and global organisations, managerial accounting system is found in an integrated

form. Organisational divisions and departments remain bifurcated as per the nature and type but

remain integrated as per management’s point of view. Management accounting system is an

essential requirement to an organisation to build ethical managerial relations within departments

and divisions of an organisation.

P2. Different methods and techniques used for management accounting reporting

Management accounting reporting is one of the managerial works which is done by the

cost accountants and departmental managers (Sargent, Borthick and Lederberg, 2011.).

Accountants and managers prepare the accounting reports and submit these to the senior level

management. Senior managers are the experts and specialists who analyse and evaluate the

reports as well as make strategies and plans. Management accounting reports are used in decision

making process and in making competitive strategies as well. Below are some methods and

techniques are defined helps in decision making process:

Budgetary reports: This is one of the common techniques which is used by the

organisation to analyse and evaluate future opportunities. Budgets present the future planning

and strategic management subjected to organisational goals and objectives. Budgetary reports

contain the information related to projected income and expenditure subjected to management

and operations. Budgets provide the prior information to managers and accountants about future

events and projects.

Account receivable reporting: This reporting method helps to trace the records of

debtors and collection receivables from buyers and customers. Account receivable reports assist

the managers and accountants to decide the payback period of debtors (Parker, 2012). These

reports are prepared with the help of cash flow statements, sales records, debtor’s information

and records. With help of account receivable reports, managers become eligible to decide the pay

back policy to debtor. Basically, the payback policies are used by the organisation such as 30, 60

and 90 days policy. This reporting technique helps to sort out the issues that occur in collection

process.

Job cost report methods: These reports are produced by the production and

manufacturing departments of an organisation. This is the technique used to sort out the plans

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

and strategies subjected to specific tasks and projects. There are various types of cost analysis

done in this technique. Job cost report provides the information and data related to cost incurred

on particular job centre and project.

Manufacturing and inventories reporting: These accounting information are useful to

those organisations which operated large inventory and stock stores. With this accounting report,

managers would be able to estimate the required amount of input to produce desired amount of

output. These reports help to communicate the information between production department and

inventory department of an organisation. This report gives the information related to inventories

in stocks and production process.

TASK 2

P3 Analysation of profit by using absorption and marginal costing technique

Marginal costing: this is one of the costing technique used by the production and

manufacturing organisations. Marginal costing techniques is commonly used by the organisation

to analyse the cost of the product by considering all the variable aspects and cost. This cost

techniques consider all the variable expenses such as direct labour, material and wages and

overheads while calculating the cost of per unit (Islam and Hu, 2012). Fixed expenses, cost and

overhears are not considered in marginal cotinga technique. This costing method is beneficial for

those organisations and industries which deals in variable products and services.

Absorption costing: this is also one of the cost evaluating technique which helps the

managers and accountants to calculate the cost of per unit and product. This cost techniques also

considered as overall cost evaluating technique. This technique helps to ascertain the cost of per

unit by including both variable and fixed costs. Organisations are adopting this technique with in

their operation and management. This not only helps the organisations to calculate the cost of

product but also helps to set the profit margin to earn optimum return on product and services.

Calculation of profit by using absorption costing technique

Particulars Calculation Amount

Sales 52500

Less: cost of goods sold (W/N 1)

Cost of opening inventory

Direct labour -7500

5

done in this technique. Job cost report provides the information and data related to cost incurred

on particular job centre and project.

Manufacturing and inventories reporting: These accounting information are useful to

those organisations which operated large inventory and stock stores. With this accounting report,

managers would be able to estimate the required amount of input to produce desired amount of

output. These reports help to communicate the information between production department and

inventory department of an organisation. This report gives the information related to inventories

in stocks and production process.

TASK 2

P3 Analysation of profit by using absorption and marginal costing technique

Marginal costing: this is one of the costing technique used by the production and

manufacturing organisations. Marginal costing techniques is commonly used by the organisation

to analyse the cost of the product by considering all the variable aspects and cost. This cost

techniques consider all the variable expenses such as direct labour, material and wages and

overheads while calculating the cost of per unit (Islam and Hu, 2012). Fixed expenses, cost and

overhears are not considered in marginal cotinga technique. This costing method is beneficial for

those organisations and industries which deals in variable products and services.

Absorption costing: this is also one of the cost evaluating technique which helps the

managers and accountants to calculate the cost of per unit and product. This cost techniques also

considered as overall cost evaluating technique. This technique helps to ascertain the cost of per

unit by including both variable and fixed costs. Organisations are adopting this technique with in

their operation and management. This not only helps the organisations to calculate the cost of

product but also helps to set the profit margin to earn optimum return on product and services.

Calculation of profit by using absorption costing technique

Particulars Calculation Amount

Sales 52500

Less: cost of goods sold (W/N 1)

Cost of opening inventory

Direct labour -7500

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Direct material -12000

Variable production overheads -3000

Fixed overheads -7500

Less: cost of closing inventory -10000 -40000

Profit before deduction fixed

overheads and selling and

distribution expenses 12500

Less: Fixed production overheads -15000

-2500

Less: selling and distribution

expense

fixed overheads -10000

variable overheads -7875

Net profit or loss -20375

Calculation of profit by using marginal costing technique

Particulars Amount

Sales 52500

Less: cost of goods sold

Cost of opening inventory

Direct labour -7500

Direct material -12000

Variable production overheads -3000

Less: cost of closing inventory -7500 -30000

Profit before selling and distribution expenses 22500

Less: selling and distribution expense

variable overheads -7875

Net profit or loss 14625

Working Notes:

1. Calculation of cost of goods sold under absorbtion costing technique

Particulars Details Amount

6

Variable production overheads -3000

Fixed overheads -7500

Less: cost of closing inventory -10000 -40000

Profit before deduction fixed

overheads and selling and

distribution expenses 12500

Less: Fixed production overheads -15000

-2500

Less: selling and distribution

expense

fixed overheads -10000

variable overheads -7875

Net profit or loss -20375

Calculation of profit by using marginal costing technique

Particulars Amount

Sales 52500

Less: cost of goods sold

Cost of opening inventory

Direct labour -7500

Direct material -12000

Variable production overheads -3000

Less: cost of closing inventory -7500 -30000

Profit before selling and distribution expenses 22500

Less: selling and distribution expense

variable overheads -7875

Net profit or loss 14625

Working Notes:

1. Calculation of cost of goods sold under absorbtion costing technique

Particulars Details Amount

6

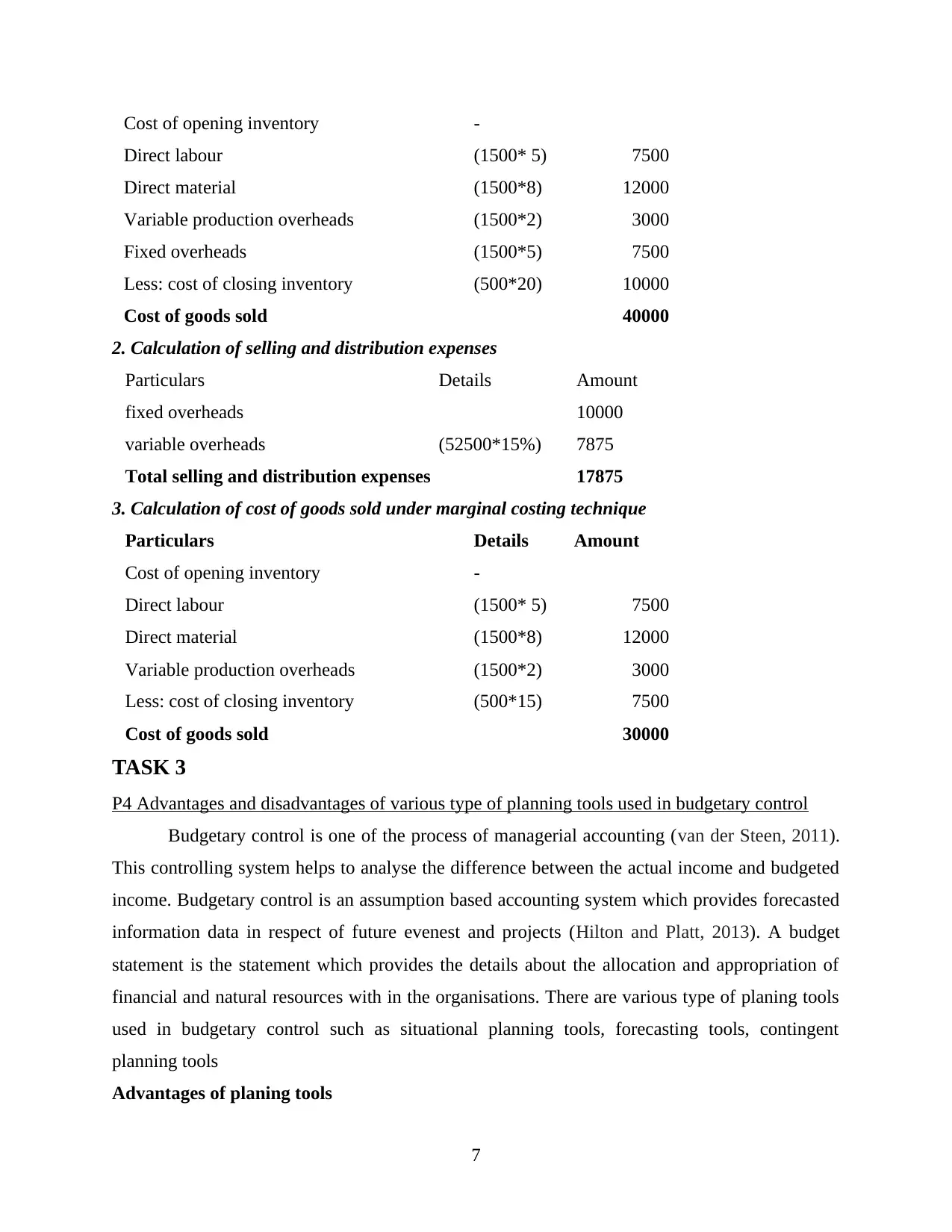

Cost of opening inventory -

Direct labour (1500* 5) 7500

Direct material (1500*8) 12000

Variable production overheads (1500*2) 3000

Fixed overheads (1500*5) 7500

Less: cost of closing inventory (500*20) 10000

Cost of goods sold 40000

2. Calculation of selling and distribution expenses

Particulars Details Amount

fixed overheads 10000

variable overheads (52500*15%) 7875

Total selling and distribution expenses 17875

3. Calculation of cost of goods sold under marginal costing technique

Particulars Details Amount

Cost of opening inventory -

Direct labour (1500* 5) 7500

Direct material (1500*8) 12000

Variable production overheads (1500*2) 3000

Less: cost of closing inventory (500*15) 7500

Cost of goods sold 30000

TASK 3

P4 Advantages and disadvantages of various type of planning tools used in budgetary control

Budgetary control is one of the process of managerial accounting (van der Steen, 2011).

This controlling system helps to analyse the difference between the actual income and budgeted

income. Budgetary control is an assumption based accounting system which provides forecasted

information data in respect of future evenest and projects (Hilton and Platt, 2013). A budget

statement is the statement which provides the details about the allocation and appropriation of

financial and natural resources with in the organisations. There are various type of planing tools

used in budgetary control such as situational planning tools, forecasting tools, contingent

planning tools

Advantages of planing tools

7

Direct labour (1500* 5) 7500

Direct material (1500*8) 12000

Variable production overheads (1500*2) 3000

Fixed overheads (1500*5) 7500

Less: cost of closing inventory (500*20) 10000

Cost of goods sold 40000

2. Calculation of selling and distribution expenses

Particulars Details Amount

fixed overheads 10000

variable overheads (52500*15%) 7875

Total selling and distribution expenses 17875

3. Calculation of cost of goods sold under marginal costing technique

Particulars Details Amount

Cost of opening inventory -

Direct labour (1500* 5) 7500

Direct material (1500*8) 12000

Variable production overheads (1500*2) 3000

Less: cost of closing inventory (500*15) 7500

Cost of goods sold 30000

TASK 3

P4 Advantages and disadvantages of various type of planning tools used in budgetary control

Budgetary control is one of the process of managerial accounting (van der Steen, 2011).

This controlling system helps to analyse the difference between the actual income and budgeted

income. Budgetary control is an assumption based accounting system which provides forecasted

information data in respect of future evenest and projects (Hilton and Platt, 2013). A budget

statement is the statement which provides the details about the allocation and appropriation of

financial and natural resources with in the organisations. There are various type of planing tools

used in budgetary control such as situational planning tools, forecasting tools, contingent

planning tools

Advantages of planing tools

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Planning tools helps the managers and accountants to make a flexible budget. This contains the

detailed analysis and critical evaluation process subject to budgets.

Planning tools clear the vision and mission of framing the budgets and forecasting the

plan in respect of future plans and projects (Parker, 2012). Planning tools provides a path

to estimate the future outcomes and results by framing strategies and plans.

Planning tools lead the organisational departments towards faster achievements and more

effective manner to accomplish the goals and objectives on an organisation.

There is a team of experts and specialist remain centralised towards analysing the plans

and evaluate the informations in effective manner. Planning tools motivates the managers

and accountants subject to making the plans and strategies according to future

uncertainties.

Planning tools remain focused around organisational objectives and aims subject to future

sustainability and growth of entity. This also support the managers in decision making

process.

Disadvantages of planning tools

Planning tools are not the surety of sustainable success of organisation. Budgets do not

provide the clear information about the future uncertainty and plans.

It become difficult for small and medium size enterprises to adopt the planning tools for

budget and forecasting the plans (Qian, Burritt and Monroe, 2011). It contain the

complex business issues and conflicts which become the barrier subject to sustainable

growth.

Organisations have to pay high implementing and installation cost reading planning tools

for budgetary control.

There is a lake of accuracy and uncertainty found in implementing planing tools for

budgetary control. It reduce the credibility subject to forecasting and planning for future

task and projects.

It takes too much time to frame the process of planing and forecasting. Accurate

information data and resources are essential requirement to make effective planning and

forecasting budget and statements.

8

detailed analysis and critical evaluation process subject to budgets.

Planning tools clear the vision and mission of framing the budgets and forecasting the

plan in respect of future plans and projects (Parker, 2012). Planning tools provides a path

to estimate the future outcomes and results by framing strategies and plans.

Planning tools lead the organisational departments towards faster achievements and more

effective manner to accomplish the goals and objectives on an organisation.

There is a team of experts and specialist remain centralised towards analysing the plans

and evaluate the informations in effective manner. Planning tools motivates the managers

and accountants subject to making the plans and strategies according to future

uncertainties.

Planning tools remain focused around organisational objectives and aims subject to future

sustainability and growth of entity. This also support the managers in decision making

process.

Disadvantages of planning tools

Planning tools are not the surety of sustainable success of organisation. Budgets do not

provide the clear information about the future uncertainty and plans.

It become difficult for small and medium size enterprises to adopt the planning tools for

budget and forecasting the plans (Qian, Burritt and Monroe, 2011). It contain the

complex business issues and conflicts which become the barrier subject to sustainable

growth.

Organisations have to pay high implementing and installation cost reading planning tools

for budgetary control.

There is a lake of accuracy and uncertainty found in implementing planing tools for

budgetary control. It reduce the credibility subject to forecasting and planning for future

task and projects.

It takes too much time to frame the process of planing and forecasting. Accurate

information data and resources are essential requirement to make effective planning and

forecasting budget and statements.

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

P5 Ways in which organisations could apply the management accounting to respond financial

problems

Management accounting is becoming the essential and prior requirement of business and

organisations. This one of the management accounting system which helps the managers and

accountants to operate the functions and operations of business in effective manner

(Implementation of management accounting tool in organisation, 2017.). Now a days

management accounting system is playing a vital role in responding financial problems of an

organisation. Business and entities are adapting planning tools to control the financial risks and

analysing the risk factors associated with management and planning process. There are various

type of financial challenges are occurs with in the organisation. Arrangement of financial

resources and application them as per the financial needs are the main financial problems which

occurs in front of managers.

Organisations are adapting the management accounting system to achieve core

competence and attain competitive advantages. Management information system, cost

accounting system and financial risk analysis systems are the main management accounting

systems used subject to financial problems. Management accounting plays vital role in

responding the financial problems in effective manner. There are various type of financial

accounting tools and system used by the managers. This helps to make the financial statements

such as cash flow statements, income and expenditure statements and financial position

statement of the company. Managers and accountants become eligible to find out the conflicts

and issues which occurs while making finical plans and procedures subject to generate financial

resources. Management accounting aspects clear the conflicts and issues and provide clear

information to managers about best financial options.

CONCLUSION

Management accounting is one of the managerial tool which helps the managers and

accountants to make strategies and plans. This reports is prepared to define the management

accounting principle and its important to integrate management accounting system with in the

organisation. Various type of cost accounting techniques used in management accounting

reporting elaborate in this context. Profit calculation techniques in cost accounting system also

defined with practical scenario. Marginal and abortion costing techniques defined in this report

with practical scenario. Advantages and disadvantages of different type of planning tools used in

9

problems

Management accounting is becoming the essential and prior requirement of business and

organisations. This one of the management accounting system which helps the managers and

accountants to operate the functions and operations of business in effective manner

(Implementation of management accounting tool in organisation, 2017.). Now a days

management accounting system is playing a vital role in responding financial problems of an

organisation. Business and entities are adapting planning tools to control the financial risks and

analysing the risk factors associated with management and planning process. There are various

type of financial challenges are occurs with in the organisation. Arrangement of financial

resources and application them as per the financial needs are the main financial problems which

occurs in front of managers.

Organisations are adapting the management accounting system to achieve core

competence and attain competitive advantages. Management information system, cost

accounting system and financial risk analysis systems are the main management accounting

systems used subject to financial problems. Management accounting plays vital role in

responding the financial problems in effective manner. There are various type of financial

accounting tools and system used by the managers. This helps to make the financial statements

such as cash flow statements, income and expenditure statements and financial position

statement of the company. Managers and accountants become eligible to find out the conflicts

and issues which occurs while making finical plans and procedures subject to generate financial

resources. Management accounting aspects clear the conflicts and issues and provide clear

information to managers about best financial options.

CONCLUSION

Management accounting is one of the managerial tool which helps the managers and

accountants to make strategies and plans. This reports is prepared to define the management

accounting principle and its important to integrate management accounting system with in the

organisation. Various type of cost accounting techniques used in management accounting

reporting elaborate in this context. Profit calculation techniques in cost accounting system also

defined with practical scenario. Marginal and abortion costing techniques defined in this report

with practical scenario. Advantages and disadvantages of different type of planning tools used in

9

budgetary control also illustrated in this report. Ways are compared that how management

accounting systems are helping subject to respond financial problems with in the organisation.

10

accounting systems are helping subject to respond financial problems with in the organisation.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.