Management Accounting Report: Concepts, Methods, and Analysis

VerifiedAdded on 2020/11/23

|13

|3941

|341

Report

AI Summary

This report delves into the realm of management accounting, providing a detailed analysis of its concepts, methods, and practical applications. It begins by exploring the fundamental concepts of management accounting, emphasizing its role in organizational decision-making and performance evaluation. The report then examines various reporting methods, including inventory management reports, debtors aging reports, and budgetary reports, highlighting their significance in financial analysis and control. Furthermore, it presents a comparative analysis of cost accounting techniques, specifically absorption costing and marginal costing, illustrating their impact on income statement preparation and financial reporting. The report also discusses planning tools, such as budgetary control and activity-based costing, assessing their advantages and disadvantages. Finally, it addresses how organizations adapt management accounting systems to address financial problems, offering insights into strategic financial management. The report uses the example of Zylla, a firm, to illustrate these principles and provide practical examples.

MANAGEMENT

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

LO1..................................................................................................................................................1

P1. Management accounting concepts and its needs..............................................................1

P2 Different methods applied for management accounting reporting...................................3

LO2..................................................................................................................................................5

P3 Cost analysis to prepare an income statement using absorption cost and marginal cost.. 5

LO3..................................................................................................................................................7

P4 Define advantages and disadvantages of differed kinds of planning tools which used in

budgetary control and activity based costing.........................................................................7

LO4..................................................................................................................................................8

P5 How Organizations are adapting management accounting systems to respond to financial

problems.................................................................................................................................8

CONCLUSION ...............................................................................................................................9

REFERENCES..............................................................................................................................11

INTRODUCTION...........................................................................................................................1

LO1..................................................................................................................................................1

P1. Management accounting concepts and its needs..............................................................1

P2 Different methods applied for management accounting reporting...................................3

LO2..................................................................................................................................................5

P3 Cost analysis to prepare an income statement using absorption cost and marginal cost.. 5

LO3..................................................................................................................................................7

P4 Define advantages and disadvantages of differed kinds of planning tools which used in

budgetary control and activity based costing.........................................................................7

LO4..................................................................................................................................................8

P5 How Organizations are adapting management accounting systems to respond to financial

problems.................................................................................................................................8

CONCLUSION ...............................................................................................................................9

REFERENCES..............................................................................................................................11

INTRODUCTION

Management Accounting is used by managers for better information of organization and

id is a type of provision made for systematic decision making to assist management and

performance business. Internal activities of firm requires perfection and accuracy in each and

every task.. Zylla also adopts various techniques and methods of management accounting to

reach its financial objectives. It uses these tools to decide costs and resolve financial problems in

smart way. Management accounting is used in devising planning, decision making, and proving

expertise to in various reports. There illustration of risk plan, strategic management and

performance in this report. Its techniques help in operational ability and cost mechanism. Present

report will represent various budgetary techniques, costing system, reporting methods and

techniques of appraisal in internal administration (Kotas, 2014). It emphasizes on tasks,

operations, detailed information and other divisions. It also includes partnering in various

management systems to assist formulation and implementations of strategic techniques. It varies

from financial accounting in various ways. Creditors, shareholders use financial accounting

publicly while management accounting is used within organization itself. It is computed towards

the needs of managers by using management information system. There is variance analysis,

activity based costing, transfer pricing and much more.

LO1

P1. Management accounting concepts and its needs

Management accounting is a needed for evaluation of data for basic needs of

organizational goals. It can be considered as a mathematical tool which fix data in assertive form

of decision that business making and planning for managerial professionals to predict budgets in

different functional departments. These techniques are targeted in a prominent way in an

organization with complete effectiveness to attain managerial objectives. It is a combination of

financial and non-financial statements to provide data so that outstanding decisions are taken in

organization.

Various phases of management are seen techniques of accounting are as follows:

Job Costing: Transaction activity determines costs incurred in each and every activity of

business. Costs are required in every department to demonstrate its requirement (Ceulemans,

1

Management Accounting is used by managers for better information of organization and

id is a type of provision made for systematic decision making to assist management and

performance business. Internal activities of firm requires perfection and accuracy in each and

every task.. Zylla also adopts various techniques and methods of management accounting to

reach its financial objectives. It uses these tools to decide costs and resolve financial problems in

smart way. Management accounting is used in devising planning, decision making, and proving

expertise to in various reports. There illustration of risk plan, strategic management and

performance in this report. Its techniques help in operational ability and cost mechanism. Present

report will represent various budgetary techniques, costing system, reporting methods and

techniques of appraisal in internal administration (Kotas, 2014). It emphasizes on tasks,

operations, detailed information and other divisions. It also includes partnering in various

management systems to assist formulation and implementations of strategic techniques. It varies

from financial accounting in various ways. Creditors, shareholders use financial accounting

publicly while management accounting is used within organization itself. It is computed towards

the needs of managers by using management information system. There is variance analysis,

activity based costing, transfer pricing and much more.

LO1

P1. Management accounting concepts and its needs

Management accounting is a needed for evaluation of data for basic needs of

organizational goals. It can be considered as a mathematical tool which fix data in assertive form

of decision that business making and planning for managerial professionals to predict budgets in

different functional departments. These techniques are targeted in a prominent way in an

organization with complete effectiveness to attain managerial objectives. It is a combination of

financial and non-financial statements to provide data so that outstanding decisions are taken in

organization.

Various phases of management are seen techniques of accounting are as follows:

Job Costing: Transaction activity determines costs incurred in each and every activity of

business. Costs are required in every department to demonstrate its requirement (Ceulemans,

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Molderez and Van Liedekerke, 2015). Thus, all mandatory records are made in accounting

systems like direct labor, direct material and other related costs.

Inventory management: It helps in maintenance of export-import of business. It depends on

managing the steadiness of inventories. It should be kept in mind by the production department

that business profitability and consumer demand are major goals of any firm and so organization

should be cautious for it.

Price optimization: Firm earns profit by putting the best and profitable price. Various prices are

fixed up on products and services by rising profit in business. Thus, depending on each and every

product such type of variations are made at various locations. Zylla earns profit if such

techniques are operated carefully.

Cost Accounting: Cost incurred at part of business is illustrated by Zylla. Therefore, for the

production of goods and services huge amount of fund is required (Collier, 2015). So there is

balancing of fund required and investment of fund in production costing technique so that fruitful

results are availed. This technique is mainly useful to know actual cost incurred on every product

to bring results. Like, this perfect management of firm can be confirmed and its practices are

optimized that are based on cost efficiency and capability. Zylla uses this technique in a very

deliberate and technical way.

Auditing: Preparation of audits helps in upbringing of work culture of organization in all possible

ways. All managerial professionals are bound so that meaningful decisions are taken internal

information are known by the accountants relevant to operating expenditures, profit, costs and

other information. Zylla has perfect functional and operational steadiness which has been made

by regular improvements in internal practices of administration. Assets, liabilities and profits are

major accounting parts of accounting systems. Auditing aids in determining these parts in a

suitable time period. It can be considered as the best form of examining and providing surety of

compliance to requirements of firm. There is main use of internal audit. It is done by first party

of organisation which doesn't possess any absolute interest in its outcomes. Compliance,

performance, corrective actions and risks are major tasks of audits. Mainly four phases of audit

exist i.e audit preparation, performance, reporting, follow up and reporting. Auditor, clients and

various other paties perform the first phase (Dekker, 2016.). Second phase is known for

fieldwork which is performed for gathering of information and that includes practices like on-site

audit, meeting with auditee, understanding the whole process and finally controlling the entire

2

systems like direct labor, direct material and other related costs.

Inventory management: It helps in maintenance of export-import of business. It depends on

managing the steadiness of inventories. It should be kept in mind by the production department

that business profitability and consumer demand are major goals of any firm and so organization

should be cautious for it.

Price optimization: Firm earns profit by putting the best and profitable price. Various prices are

fixed up on products and services by rising profit in business. Thus, depending on each and every

product such type of variations are made at various locations. Zylla earns profit if such

techniques are operated carefully.

Cost Accounting: Cost incurred at part of business is illustrated by Zylla. Therefore, for the

production of goods and services huge amount of fund is required (Collier, 2015). So there is

balancing of fund required and investment of fund in production costing technique so that fruitful

results are availed. This technique is mainly useful to know actual cost incurred on every product

to bring results. Like, this perfect management of firm can be confirmed and its practices are

optimized that are based on cost efficiency and capability. Zylla uses this technique in a very

deliberate and technical way.

Auditing: Preparation of audits helps in upbringing of work culture of organization in all possible

ways. All managerial professionals are bound so that meaningful decisions are taken internal

information are known by the accountants relevant to operating expenditures, profit, costs and

other information. Zylla has perfect functional and operational steadiness which has been made

by regular improvements in internal practices of administration. Assets, liabilities and profits are

major accounting parts of accounting systems. Auditing aids in determining these parts in a

suitable time period. It can be considered as the best form of examining and providing surety of

compliance to requirements of firm. There is main use of internal audit. It is done by first party

of organisation which doesn't possess any absolute interest in its outcomes. Compliance,

performance, corrective actions and risks are major tasks of audits. Mainly four phases of audit

exist i.e audit preparation, performance, reporting, follow up and reporting. Auditor, clients and

various other paties perform the first phase (Dekker, 2016.). Second phase is known for

fieldwork which is performed for gathering of information and that includes practices like on-site

audit, meeting with auditee, understanding the whole process and finally controlling the entire

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

system. Then, third phase involves communication of results that are investigated. Report

prepared should be clear and transparent.

P2 Different methods applied for management accounting reporting

A report consists of detailed information as per date and time. It includes information

regarding cash inflows that comes from different organizational practices and costs incurred in

various activities of firms. Zylla prepares report in same manner. These records help in effective

decision making and determination of profitability by managerial professional which in turn

reduces costs. Different reporting techniques of Zylla are:

Inventory management report : Inventory management is a report which needs quantity, quality

and cost of products which are initially manufactured and then delivery is done in competitive

and tough market. Fine analysis can be made only from information that aids in evaluation of

demands of products as well as capability of reordering the goods. It is an imperative method as

it bridges the efficiency and development of the firm (Ceulemans, Molderez and Van

Liedekerke, 2015). Usually, organizations compete to make inventories at best level. To fulfill

the demands and avoid hike in prices of goods an issue of having satisfactory products is always

there so that there is no overstocking problems in department. Usually small scale companies

face these types of problems with sophisticated tools at their disposal. Inventory reports are

accessed at accurate time and are moved to stock movement. It is then started with activities like

creating custom reports, underselling, avoiding overselling and cost of goods involved. Various

features are involved in inventory management report that includes inventory stock on hand

report, customizing report with proper attributes, detailed report of inventory, inventory location

report, stock recorder report, incoming of stock report and lastly historic inventory report. First

step goes with simple identification of goods and services. Then a detailed overview of inventory

is reported which involves a list of variants and products. After this, listed amount of stock and

bound up sales is on hand. Then proper comparison is done at different locations. Finally,

management of report and reorder report are done for filtration of purchase. Finally, average cost

is determined for every variant and then desired stock is exported.

Debtors aging report: It is a mandatory report which have controls over extensions on credits of a

firm. It is helpful in preparation of account receivable report (Arkorful and Abaidoo, 2015.).

Therefore, powerful ideas are made for the completion of company's procedure. Records of

debtors who are liable to make payments of goods and services are involved in the record. On the

3

prepared should be clear and transparent.

P2 Different methods applied for management accounting reporting

A report consists of detailed information as per date and time. It includes information

regarding cash inflows that comes from different organizational practices and costs incurred in

various activities of firms. Zylla prepares report in same manner. These records help in effective

decision making and determination of profitability by managerial professional which in turn

reduces costs. Different reporting techniques of Zylla are:

Inventory management report : Inventory management is a report which needs quantity, quality

and cost of products which are initially manufactured and then delivery is done in competitive

and tough market. Fine analysis can be made only from information that aids in evaluation of

demands of products as well as capability of reordering the goods. It is an imperative method as

it bridges the efficiency and development of the firm (Ceulemans, Molderez and Van

Liedekerke, 2015). Usually, organizations compete to make inventories at best level. To fulfill

the demands and avoid hike in prices of goods an issue of having satisfactory products is always

there so that there is no overstocking problems in department. Usually small scale companies

face these types of problems with sophisticated tools at their disposal. Inventory reports are

accessed at accurate time and are moved to stock movement. It is then started with activities like

creating custom reports, underselling, avoiding overselling and cost of goods involved. Various

features are involved in inventory management report that includes inventory stock on hand

report, customizing report with proper attributes, detailed report of inventory, inventory location

report, stock recorder report, incoming of stock report and lastly historic inventory report. First

step goes with simple identification of goods and services. Then a detailed overview of inventory

is reported which involves a list of variants and products. After this, listed amount of stock and

bound up sales is on hand. Then proper comparison is done at different locations. Finally,

management of report and reorder report are done for filtration of purchase. Finally, average cost

is determined for every variant and then desired stock is exported.

Debtors aging report: It is a mandatory report which have controls over extensions on credits of a

firm. It is helpful in preparation of account receivable report (Arkorful and Abaidoo, 2015.).

Therefore, powerful ideas are made for the completion of company's procedure. Records of

debtors who are liable to make payments of goods and services are involved in the record. On the

3

contrary, bad and doubtful debts are also included in it. Invoices that are more in length and are

due are under receivables and useful. An estimation is made out of accumulation of products

from uncollected receivables that comes under doubtful accounts. It is mainly useful if any

company faces problem in collecting information or mere customers grow up their business

through cash only basis.

Budgetary Reports: New and innovative ideas are generated through. Thus, prediction of

required costs of each department is each done in order to control expenses. It is meaningful in

allocation of resources. Zylla use this technique to make use of budgetary report so that more

profit can be achieved and accurate business can be done. Management system becomes more

attainable and systematic. Actual performance is compared with budgeted projections in fixed

period. It actually shows the closeness of actual budget with budgeted performance (Collier,

2015). For example, financial managers can correct difficulties in reports by making

performance more inline. Then their accuracy and realistic articulation is measured in real form.

There is possibility of adjustments if assumptions are closer during period.

Cost accounting Reports: It computes with manufacturing costs and delivery costs of goods.

Zylla uses this technique to make reports of all type of cost incurred in different activities of its

business and therefore outstanding controlling is done on the costs of products. It assures costs of

production, labor costs, overheads which are covered under inventory. Thus, managers create

new views and plan alternative ideas for further use. These proposed ideas consequently reduce

manufacturing costs. Revenues and expenses information is provided which are based on credits

and debits of cost centers. It also helps in knowing current cost of business. Cost accounting

includes important element known as overheads that includes administration overhead, factory

staff, sales staff, cost of money, distribution overhead, repair and maintenance, supplies etc. are

categorised into indirect and direct costs. These are controllable and uncontrollable costs.

Uncontrollable costs are not affected by action of management while opposite happens in

controllable costs.

Performance Reports: These reports are handled by managerial heads and professionals of the

business so that entity and workforce performance can be properly assessed properly. It is

fruitful in creating appropriate profits from the market and knowledge (Colmenar-Santos, et.al.,

2016 ). Therefore, operational practices have good effect and these reports fuel up managers for

effective analysis and helps in decision making process to bring work culture in action. Zylla use

4

due are under receivables and useful. An estimation is made out of accumulation of products

from uncollected receivables that comes under doubtful accounts. It is mainly useful if any

company faces problem in collecting information or mere customers grow up their business

through cash only basis.

Budgetary Reports: New and innovative ideas are generated through. Thus, prediction of

required costs of each department is each done in order to control expenses. It is meaningful in

allocation of resources. Zylla use this technique to make use of budgetary report so that more

profit can be achieved and accurate business can be done. Management system becomes more

attainable and systematic. Actual performance is compared with budgeted projections in fixed

period. It actually shows the closeness of actual budget with budgeted performance (Collier,

2015). For example, financial managers can correct difficulties in reports by making

performance more inline. Then their accuracy and realistic articulation is measured in real form.

There is possibility of adjustments if assumptions are closer during period.

Cost accounting Reports: It computes with manufacturing costs and delivery costs of goods.

Zylla uses this technique to make reports of all type of cost incurred in different activities of its

business and therefore outstanding controlling is done on the costs of products. It assures costs of

production, labor costs, overheads which are covered under inventory. Thus, managers create

new views and plan alternative ideas for further use. These proposed ideas consequently reduce

manufacturing costs. Revenues and expenses information is provided which are based on credits

and debits of cost centers. It also helps in knowing current cost of business. Cost accounting

includes important element known as overheads that includes administration overhead, factory

staff, sales staff, cost of money, distribution overhead, repair and maintenance, supplies etc. are

categorised into indirect and direct costs. These are controllable and uncontrollable costs.

Uncontrollable costs are not affected by action of management while opposite happens in

controllable costs.

Performance Reports: These reports are handled by managerial heads and professionals of the

business so that entity and workforce performance can be properly assessed properly. It is

fruitful in creating appropriate profits from the market and knowledge (Colmenar-Santos, et.al.,

2016 ). Therefore, operational practices have good effect and these reports fuel up managers for

effective analysis and helps in decision making process to bring work culture in action. Zylla use

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

this report very properly and encourage employee's work with rewards, bonuses and various

other benefits.

LO2

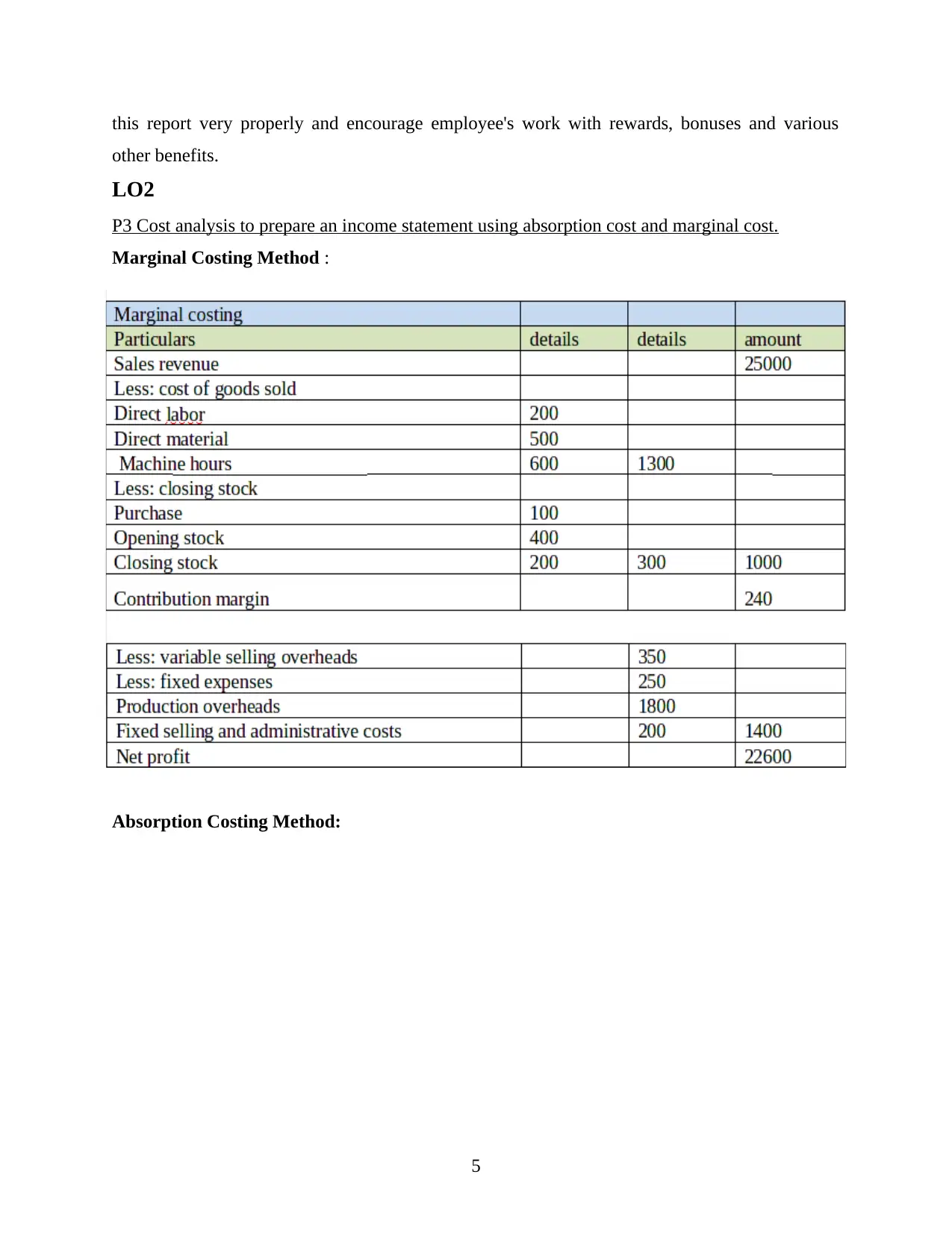

P3 Cost analysis to prepare an income statement using absorption cost and marginal cost.

Marginal Costing Method :

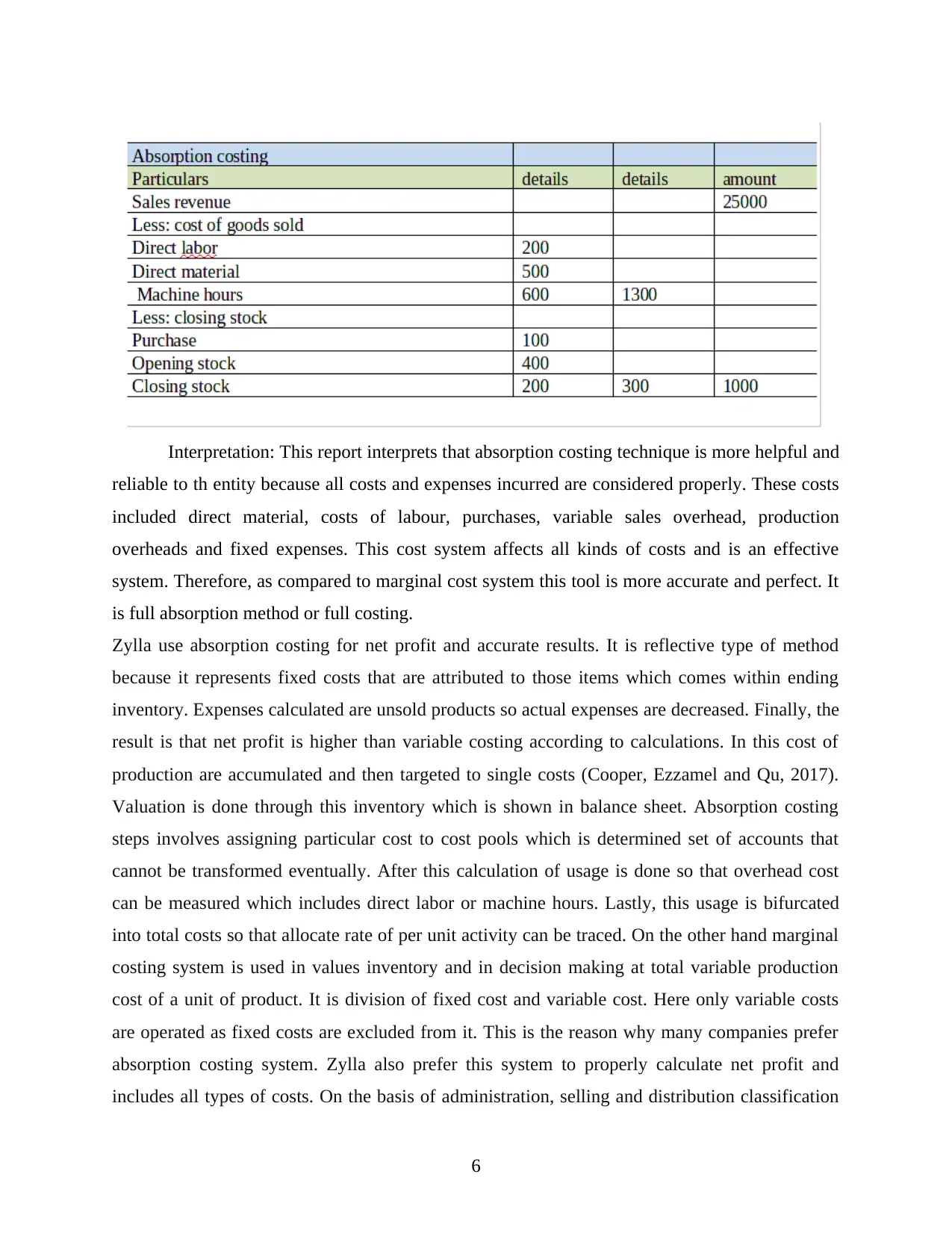

Absorption Costing Method:

5

other benefits.

LO2

P3 Cost analysis to prepare an income statement using absorption cost and marginal cost.

Marginal Costing Method :

Absorption Costing Method:

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Interpretation: This report interprets that absorption costing technique is more helpful and

reliable to th entity because all costs and expenses incurred are considered properly. These costs

included direct material, costs of labour, purchases, variable sales overhead, production

overheads and fixed expenses. This cost system affects all kinds of costs and is an effective

system. Therefore, as compared to marginal cost system this tool is more accurate and perfect. It

is full absorption method or full costing.

Zylla use absorption costing for net profit and accurate results. It is reflective type of method

because it represents fixed costs that are attributed to those items which comes within ending

inventory. Expenses calculated are unsold products so actual expenses are decreased. Finally, the

result is that net profit is higher than variable costing according to calculations. In this cost of

production are accumulated and then targeted to single costs (Cooper, Ezzamel and Qu, 2017).

Valuation is done through this inventory which is shown in balance sheet. Absorption costing

steps involves assigning particular cost to cost pools which is determined set of accounts that

cannot be transformed eventually. After this calculation of usage is done so that overhead cost

can be measured which includes direct labor or machine hours. Lastly, this usage is bifurcated

into total costs so that allocate rate of per unit activity can be traced. On the other hand marginal

costing system is used in values inventory and in decision making at total variable production

cost of a unit of product. It is division of fixed cost and variable cost. Here only variable costs

are operated as fixed costs are excluded from it. This is the reason why many companies prefer

absorption costing system. Zylla also prefer this system to properly calculate net profit and

includes all types of costs. On the basis of administration, selling and distribution classification

6

reliable to th entity because all costs and expenses incurred are considered properly. These costs

included direct material, costs of labour, purchases, variable sales overhead, production

overheads and fixed expenses. This cost system affects all kinds of costs and is an effective

system. Therefore, as compared to marginal cost system this tool is more accurate and perfect. It

is full absorption method or full costing.

Zylla use absorption costing for net profit and accurate results. It is reflective type of method

because it represents fixed costs that are attributed to those items which comes within ending

inventory. Expenses calculated are unsold products so actual expenses are decreased. Finally, the

result is that net profit is higher than variable costing according to calculations. In this cost of

production are accumulated and then targeted to single costs (Cooper, Ezzamel and Qu, 2017).

Valuation is done through this inventory which is shown in balance sheet. Absorption costing

steps involves assigning particular cost to cost pools which is determined set of accounts that

cannot be transformed eventually. After this calculation of usage is done so that overhead cost

can be measured which includes direct labor or machine hours. Lastly, this usage is bifurcated

into total costs so that allocate rate of per unit activity can be traced. On the other hand marginal

costing system is used in values inventory and in decision making at total variable production

cost of a unit of product. It is division of fixed cost and variable cost. Here only variable costs

are operated as fixed costs are excluded from it. This is the reason why many companies prefer

absorption costing system. Zylla also prefer this system to properly calculate net profit and

includes all types of costs. On the basis of administration, selling and distribution classification

6

of overheads are done. Engagement of fixed costs directly affects profitability of the firm. While

profit volume ratio determines marginal cost profitability (Lew, Pacana and Kulpa, 2017). Net

profit is attained per unit through cost per unit. While absorption costing system is different

method. In this, report data is shown in quite different and conventional way. That's why this

method is adopted by Zylla company. It is satisfied from this method. No further issues

regarding costs are created through this report. But in marginal costing method cost data outlines

entire contribution of each and every production of department. Here variances in opening and

closing stock affect cost per unit in report.

LO3

P4 advantages and disadvantages of differed kinds of planning tools

Activity Based Costing

This is a very meaningful essay technique with the help of that process of forecasting of

budget is needed to be taken. In addition to this, there are differed kinds of needs which directly

affects terms as are planning, distributing, marketing, production etc. In this term, there are

number of advantages and disadvantages of budgetary will be discussed as follows:

Advantages

It is one of the appropriate and accurate techniques of costing, with help of this there can be

accurate calculation and understanding of budget. Total cost is not considered for examination of

all cost incurred in the operational activities of firm (Lichfield, Kettle and Whitbread, 2016). In

this, only unit cost is needed to add in terms to calculation.

Disadvantages

Under this, there is a need of high sustainable resources and higher attention as it is helpful in

focusing over gathered information which is on high cost. In this term, present method of costing

focuses over profit margin and traditional concept of costing put consideration over efficiencies

of business.

Zero Based Costing

In this, it can be said that it is not inclusive of any kind of past data and performance of

enterprise so it can be dynamic and flexible. Under this, it can be said that budget-developing

plan has to put consideration over current as well as future needs.

Advantages

7

profit volume ratio determines marginal cost profitability (Lew, Pacana and Kulpa, 2017). Net

profit is attained per unit through cost per unit. While absorption costing system is different

method. In this, report data is shown in quite different and conventional way. That's why this

method is adopted by Zylla company. It is satisfied from this method. No further issues

regarding costs are created through this report. But in marginal costing method cost data outlines

entire contribution of each and every production of department. Here variances in opening and

closing stock affect cost per unit in report.

LO3

P4 advantages and disadvantages of differed kinds of planning tools

Activity Based Costing

This is a very meaningful essay technique with the help of that process of forecasting of

budget is needed to be taken. In addition to this, there are differed kinds of needs which directly

affects terms as are planning, distributing, marketing, production etc. In this term, there are

number of advantages and disadvantages of budgetary will be discussed as follows:

Advantages

It is one of the appropriate and accurate techniques of costing, with help of this there can be

accurate calculation and understanding of budget. Total cost is not considered for examination of

all cost incurred in the operational activities of firm (Lichfield, Kettle and Whitbread, 2016). In

this, only unit cost is needed to add in terms to calculation.

Disadvantages

Under this, there is a need of high sustainable resources and higher attention as it is helpful in

focusing over gathered information which is on high cost. In this term, present method of costing

focuses over profit margin and traditional concept of costing put consideration over efficiencies

of business.

Zero Based Costing

In this, it can be said that it is not inclusive of any kind of past data and performance of

enterprise so it can be dynamic and flexible. Under this, it can be said that budget-developing

plan has to put consideration over current as well as future needs.

Advantages

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Under this, there is a need to make changes as per requirements of firm and is helpful in order to

satisfy numbers of technique (Libby, 2017). In addition to this, all budget need to get start from

Zero balance and it will be inclusive of lower cost. It focuses over flexible budgets, focused

operations, lower cost, and disciplined execution. It is highly used for non-profit enterprises.

Disadvantages

one of the major shortcomings about this is that it is a time consuming process, the high paper

work is need to include at time of preparation of Zero based budgeting. The manager can work as

to develop fear and oppose new ideas at the time of changes taken place.

Incremental Budgeting

This term is based on assumption with some changes in the process of budgeting. It is prepared

with the use of previous period budget amounts and is added for a new period of budget. In this

term, it can be said that allocation of resources are totally based upon the allocation of above

period.

Advantages

The one of primary advantage is that it is based on recent financial results.

In this effect of changes can be seen easily.

It is suitable for firm where requirement of funding are fixed and within the deviation.

Disadvantages

This kind of approach will work as to makes manager spends more and budget can be

easily available and it may lead to irrelevant spending of funds which is not to be

warranted.

It encourages higher budgeting. It may lead to reduction in cost and no incentives for

managers.

LO 4

P5 How Organizations are adapting management accounting systems to respond to financial

problems.

Management accounting is the overall process to manage the proper implementation

process and market oriented deals and effective management task oriented process in order to

make the most prominent and effective marketing tools and techniques. Overall, it brings new

method of performance and task oriented process. Besides, besides, it also helps to take over the

functioning level of task oriented process (Chiwamit, Modell and Scapens, 2017). Management

8

satisfy numbers of technique (Libby, 2017). In addition to this, all budget need to get start from

Zero balance and it will be inclusive of lower cost. It focuses over flexible budgets, focused

operations, lower cost, and disciplined execution. It is highly used for non-profit enterprises.

Disadvantages

one of the major shortcomings about this is that it is a time consuming process, the high paper

work is need to include at time of preparation of Zero based budgeting. The manager can work as

to develop fear and oppose new ideas at the time of changes taken place.

Incremental Budgeting

This term is based on assumption with some changes in the process of budgeting. It is prepared

with the use of previous period budget amounts and is added for a new period of budget. In this

term, it can be said that allocation of resources are totally based upon the allocation of above

period.

Advantages

The one of primary advantage is that it is based on recent financial results.

In this effect of changes can be seen easily.

It is suitable for firm where requirement of funding are fixed and within the deviation.

Disadvantages

This kind of approach will work as to makes manager spends more and budget can be

easily available and it may lead to irrelevant spending of funds which is not to be

warranted.

It encourages higher budgeting. It may lead to reduction in cost and no incentives for

managers.

LO 4

P5 How Organizations are adapting management accounting systems to respond to financial

problems.

Management accounting is the overall process to manage the proper implementation

process and market oriented deals and effective management task oriented process in order to

make the most prominent and effective marketing tools and techniques. Overall, it brings new

method of performance and task oriented process. Besides, besides, it also helps to take over the

functioning level of task oriented process (Chiwamit, Modell and Scapens, 2017). Management

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

accounting or managerial function are deployed to provide information that management can use

to make good decisions. This management accounting will help to use the system to help in

costing and managing the manufacturing process. This also helps to make the process

implementing and task oriented managing the manufacturing process. There are given some

accounting system that helps to respond to financial problems.

Balanced Score Card (BSC)- It is the strong balanced scorecard is a strategy

performance management tool. It also helps to convey the best performance level. That helps to

bring new opportunity and growth. It is the tool that helps company to get overcome from the

challenges. It is the strategy that helps to control the things that helps to take the powerful nature

of growth.

Generally is refers to a performance management team that has been used by company. It

also helps to take the best approachable process that helps to make the process clear and

advancing. Through company can easily overcome its challenges.

KPI (Key Performance Indicator)- Key Performance indicators is the measurable

values that helps to make the most compatible and growth oriented strategies that should be

adopted by the company while performing the work accordingly. Besides, it also helps to get

over from the challenges (Christ, and Burritt, 2017). This helps to identify the new ways through

company will achieve business objectives and take corrective action plan.

Benchmarking: Benchmarking is comparing ones business processes and performance

metrics to industry bests and best practices. This process or strategy is also beneficial for

selection, planning and delivery of products. Measuring dimensions are quality, time, and cost.

That will helps to promote best targeting goals.

Financial governance: It is the another, this tool is measurable by audits, to process

workflows, to financial controls, data tracking and security. This will help to make the essential

tools and techniques. It is the overall, financial governance will make the proper effectiveness

that helps to measure the lacking point of the business.

CONCLUSION

From the basis of above section it can be concluded that, management accounting is the

most essential and goal oriented process for the organization. Management accounting is the

most essential and goal oriented process through company can easily get the most effective

process that, helps to make the most essential target plan. Overall, it also helps to bring new

9

to make good decisions. This management accounting will help to use the system to help in

costing and managing the manufacturing process. This also helps to make the process

implementing and task oriented managing the manufacturing process. There are given some

accounting system that helps to respond to financial problems.

Balanced Score Card (BSC)- It is the strong balanced scorecard is a strategy

performance management tool. It also helps to convey the best performance level. That helps to

bring new opportunity and growth. It is the tool that helps company to get overcome from the

challenges. It is the strategy that helps to control the things that helps to take the powerful nature

of growth.

Generally is refers to a performance management team that has been used by company. It

also helps to take the best approachable process that helps to make the process clear and

advancing. Through company can easily overcome its challenges.

KPI (Key Performance Indicator)- Key Performance indicators is the measurable

values that helps to make the most compatible and growth oriented strategies that should be

adopted by the company while performing the work accordingly. Besides, it also helps to get

over from the challenges (Christ, and Burritt, 2017). This helps to identify the new ways through

company will achieve business objectives and take corrective action plan.

Benchmarking: Benchmarking is comparing ones business processes and performance

metrics to industry bests and best practices. This process or strategy is also beneficial for

selection, planning and delivery of products. Measuring dimensions are quality, time, and cost.

That will helps to promote best targeting goals.

Financial governance: It is the another, this tool is measurable by audits, to process

workflows, to financial controls, data tracking and security. This will help to make the essential

tools and techniques. It is the overall, financial governance will make the proper effectiveness

that helps to measure the lacking point of the business.

CONCLUSION

From the basis of above section it can be concluded that, management accounting is the

most essential and goal oriented process for the organization. Management accounting is the

most essential and goal oriented process through company can easily get the most effective

process that, helps to make the most essential target plan. Overall, it also helps to bring new

9

target goal that helps to take the most essential. Present study has been based on management

accounting functions that helps Zylla Company for a number of years. Study has summarized the

essential requirement of different types of management accounting. This method has been used

for different marketing tools that provides the best effective goal making charge. Overall, this

brings new better opportunity and growth. In order to take the best approachable task oriented

process. It also explained the advantages and disadvantages of different types of planning tools

used in budgetary control.

10

accounting functions that helps Zylla Company for a number of years. Study has summarized the

essential requirement of different types of management accounting. This method has been used

for different marketing tools that provides the best effective goal making charge. Overall, this

brings new better opportunity and growth. In order to take the best approachable task oriented

process. It also explained the advantages and disadvantages of different types of planning tools

used in budgetary control.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.