Analysis of Management Accounting Systems & Techniques for Agmet Plc

VerifiedAdded on 2020/10/22

|20

|5703

|222

Report

AI Summary

This report comprehensively analyzes management accounting systems and techniques within the context of Agmet Plc. It begins by defining management accounting and its essential requirements, including cost accounting, inventory management, job costing, and price optimization systems. The report then explores various management accounting reports such as segmental, performance, accounts receivables ageing, and inventory management reports, highlighting their importance to management. It delves into the benefits of these systems, particularly in price optimization, cost control, and job costing. Furthermore, it provides detailed explanations and comparisons of absorption and marginal costing methods, including the preparation of income statements under each method. The report also covers the calculation of breakeven points and margin of safety, along with the application of various management accounting techniques and planning tools for budgetary control. It discusses the merits and demerits of these tools and provides a comparison of adapting management accounting systems to respond to financial problems, concluding with an evaluation of planning tools for achieving sustainable success.

MANAGEMENT

ACCOUNTING SYSTEMS &

TECHNIQUES

ACCOUNTING SYSTEMS &

TECHNIQUES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

A. Management accounting and essential requirement of different types of accounting...........1

B. Explaining management accounting reports and importance of reports to management.......2

C. Benefits of management accounting systems.........................................................................3

Integrated management accounting system................................................................................4

TASK 2............................................................................................................................................5

A.1) Explanation of absorption and marginal costing method...................................................5

A.2) Preparing Income Statement by considering absorption and marginal costing..................5

B. Calculation of breakeven point and Margin of safety............................................................8

Difference between marginal and absorption costing.................................................................8

C. Applying range of management techniques with its significance..........................................9

D. Producing financial reports with appropriate interpretation..................................................9

TASK 3..........................................................................................................................................10

A. Merits and demerits of various types of planning tools for budgetary control....................10

B. Application of planning tools for the purpose for analysing and forecasting budget..........11

C. Providing comparison for adapting management accounting system for responding

financial problems.....................................................................................................................13

D. Analysing management accounting techniques which are used for responding financial

problems....................................................................................................................................14

E. Evaluating planning tools for solving financial problems which leads to sustainable success

...................................................................................................................................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION ..........................................................................................................................1

TASK 1............................................................................................................................................1

A. Management accounting and essential requirement of different types of accounting...........1

B. Explaining management accounting reports and importance of reports to management.......2

C. Benefits of management accounting systems.........................................................................3

Integrated management accounting system................................................................................4

TASK 2............................................................................................................................................5

A.1) Explanation of absorption and marginal costing method...................................................5

A.2) Preparing Income Statement by considering absorption and marginal costing..................5

B. Calculation of breakeven point and Margin of safety............................................................8

Difference between marginal and absorption costing.................................................................8

C. Applying range of management techniques with its significance..........................................9

D. Producing financial reports with appropriate interpretation..................................................9

TASK 3..........................................................................................................................................10

A. Merits and demerits of various types of planning tools for budgetary control....................10

B. Application of planning tools for the purpose for analysing and forecasting budget..........11

C. Providing comparison for adapting management accounting system for responding

financial problems.....................................................................................................................13

D. Analysing management accounting techniques which are used for responding financial

problems....................................................................................................................................14

E. Evaluating planning tools for solving financial problems which leads to sustainable success

...................................................................................................................................................15

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION

Management accounting is referred as presentation of accounting information for

formulating its policies which should be adopted through management. This report will help in

assisting its regular activities. The present report will discuss about various accounting systems

and techniques of Agmet. It would be providing management accounting's essential requirements

and kinds . It will be explaining various management accounting reports with its significance. It

would be reflecting income statement through both absorption and marginal costing methods

with its importance and appropriate interpretation. Further, it will state various planning tools for

purpose of budgetary control with its merits, demerits and application. In the similar aspect, it

would be providing comparison for adapting management accounting system for responding its

financial problems. It will analyse this management accounting techniques and evaluation of

planning tools for solving financial issues which would lead to sustainable success of

organization. The present report has explained management accounting techniques on basis of

Agmet Plc.

TASK 1

A. Management accounting and essential requirement of different types of accounting

Management accounting is one of the vital part of organisation as management is able to

take better decisions with regard to internal operations. In simple words, financial accounting

provides information with context to reports which is imparted to organisation's management for

assessing internal health and event of any deficiencies being observed or any decision-making

done (Laudon and Laudon, 2016). On the other hand, costs can be controlled in a better way by

evaluating managerial reports. The different types of management accounting and requirements

are highlighted below-

1. Cost accounting system-

As the name suggests, cost accounting system is used to control expenditures which may

affect company's operational activities up to a high extent. By controlling expenses, more

production could be performed through Agmet in fewer expenditures. This means that

production process can be increased and in relation to this, expenditures can be controlled by

Agmet's management. Actual costing means that it utilises only actual costs that are incurred in

production. Standard costing implies clearly that budgeted costs are substituted for actual cost.

1

Management accounting is referred as presentation of accounting information for

formulating its policies which should be adopted through management. This report will help in

assisting its regular activities. The present report will discuss about various accounting systems

and techniques of Agmet. It would be providing management accounting's essential requirements

and kinds . It will be explaining various management accounting reports with its significance. It

would be reflecting income statement through both absorption and marginal costing methods

with its importance and appropriate interpretation. Further, it will state various planning tools for

purpose of budgetary control with its merits, demerits and application. In the similar aspect, it

would be providing comparison for adapting management accounting system for responding its

financial problems. It will analyse this management accounting techniques and evaluation of

planning tools for solving financial issues which would lead to sustainable success of

organization. The present report has explained management accounting techniques on basis of

Agmet Plc.

TASK 1

A. Management accounting and essential requirement of different types of accounting

Management accounting is one of the vital part of organisation as management is able to

take better decisions with regard to internal operations. In simple words, financial accounting

provides information with context to reports which is imparted to organisation's management for

assessing internal health and event of any deficiencies being observed or any decision-making

done (Laudon and Laudon, 2016). On the other hand, costs can be controlled in a better way by

evaluating managerial reports. The different types of management accounting and requirements

are highlighted below-

1. Cost accounting system-

As the name suggests, cost accounting system is used to control expenditures which may

affect company's operational activities up to a high extent. By controlling expenses, more

production could be performed through Agmet in fewer expenditures. This means that

production process can be increased and in relation to this, expenditures can be controlled by

Agmet's management. Actual costing means that it utilises only actual costs that are incurred in

production. Standard costing implies clearly that budgeted costs are substituted for actual cost.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

On the other hand, normal costing suggests that actual labour, materials and overheads costs are

included. Thus, cost accounting system is quite beneficial for company.

2. Inventory management system-

It is used by management so that only desired stock is optimised through Agmet and no

extra inventory handling costs are incurred. In relation to this, if excess inventory is ordered, it

leads to maximisation of expenditures and wastage of scarce resources. Thus, JIT (Just-In-Time)

approach is used for maintaining adequate level of inventory and attain maximum production in

the best possible manner.

3. Job costing system-

There are various jobs which are done by overheads and job costing helps to assess on

which maximum costs are made in order to have efficient production (Senftlechner and Hiebl,

2015). Costs of materials, labour and overheads are accomplished and accordingly, expenses are

made. Agmet is benefited as it is mainly engaged in production of chemicals and as a result,

various expenditures are made. It helps organisation to effectively ascertain costs of jobs.

4. Price optimisation system-

It is another management accounting system which helps to quote prices of products in a

better way. Mathematical model is implemented for price determination and is used to assess

whether demand of products varies in relation to its price quoted by company. This means that

Agmet is able to analyse the view whether customers would be willing to pay for price or it has

to lower the same for attaining customers' satisfaction (Ax and Greve, 2017).

B. Explaining management accounting reports and importance of reports to management

1. Segmental report-

The segmental report provides an overview of entire company's divisions performance

for particular period in effective manner. Management of Agmet seeks units' execution over

tasks and whether they are adequately performing or not. Users of accounting information are

benefited with such reports and are able to take decisions. Moreover, it is prepared and used by

public organisations and private firms are out of the purview. Hence, company is able to make

proper decisions as entire performance of divisions are assessed with ease.

2

included. Thus, cost accounting system is quite beneficial for company.

2. Inventory management system-

It is used by management so that only desired stock is optimised through Agmet and no

extra inventory handling costs are incurred. In relation to this, if excess inventory is ordered, it

leads to maximisation of expenditures and wastage of scarce resources. Thus, JIT (Just-In-Time)

approach is used for maintaining adequate level of inventory and attain maximum production in

the best possible manner.

3. Job costing system-

There are various jobs which are done by overheads and job costing helps to assess on

which maximum costs are made in order to have efficient production (Senftlechner and Hiebl,

2015). Costs of materials, labour and overheads are accomplished and accordingly, expenses are

made. Agmet is benefited as it is mainly engaged in production of chemicals and as a result,

various expenditures are made. It helps organisation to effectively ascertain costs of jobs.

4. Price optimisation system-

It is another management accounting system which helps to quote prices of products in a

better way. Mathematical model is implemented for price determination and is used to assess

whether demand of products varies in relation to its price quoted by company. This means that

Agmet is able to analyse the view whether customers would be willing to pay for price or it has

to lower the same for attaining customers' satisfaction (Ax and Greve, 2017).

B. Explaining management accounting reports and importance of reports to management

1. Segmental report-

The segmental report provides an overview of entire company's divisions performance

for particular period in effective manner. Management of Agmet seeks units' execution over

tasks and whether they are adequately performing or not. Users of accounting information are

benefited with such reports and are able to take decisions. Moreover, it is prepared and used by

public organisations and private firms are out of the purview. Hence, company is able to make

proper decisions as entire performance of divisions are assessed with ease.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2. Performance report-

It is another useful managerial report which helps Agmet to effectively ascertain

individual performances of employees. This is essentially required so that company may be able

to carry out deficiencies in every divisions and improvement may be initiated. It helps

employee's to effectively perform in accordance to allocated tasks and with such analysis,

performances can be improved leading to increase in efficiency and thus, maximum output can

be obtained. Hence, Agmet is able to maximise output with performance reports (Bui and De

Villiers, 2017).

3. Accounts receivables ageing report-

Customers are provided with goods on credit basis by Agmet. It is required that timely

payment should be made by them to company so that operational activities may not be

hampered. In addition to this, accounts receivables ageing report is prepared and given to

management so that it may assess money outstanding from debtors. Thus, company collects

money from them and if credit remains due for long, then strict credit policies may be

implemented.

4. Inventory management report-

Inventory report is provided to management in order to asses’ demand of production

department so that adequate manufacturing can be done with ease. This means that desired

quantities which are needed for meeting production is stipulated in inventory management report

which is then ordered by management. Thus, excess quantity is not ordered and no handling

costs are incurred for keeping stock in warehouse (Management accounting reports, 2017).

C. Benefits of management accounting systems

Price optimisation-

It is quite beneficial for Agmet as it helps to quote prices of products in relation to

demand and preferences of customers up to a high extent. Firm is able to take advantage of such

technique because if higher prices are set, then customer's will get attracted to rivals

(Honggowati and et.al, 2017).

3

It is another useful managerial report which helps Agmet to effectively ascertain

individual performances of employees. This is essentially required so that company may be able

to carry out deficiencies in every divisions and improvement may be initiated. It helps

employee's to effectively perform in accordance to allocated tasks and with such analysis,

performances can be improved leading to increase in efficiency and thus, maximum output can

be obtained. Hence, Agmet is able to maximise output with performance reports (Bui and De

Villiers, 2017).

3. Accounts receivables ageing report-

Customers are provided with goods on credit basis by Agmet. It is required that timely

payment should be made by them to company so that operational activities may not be

hampered. In addition to this, accounts receivables ageing report is prepared and given to

management so that it may assess money outstanding from debtors. Thus, company collects

money from them and if credit remains due for long, then strict credit policies may be

implemented.

4. Inventory management report-

Inventory report is provided to management in order to asses’ demand of production

department so that adequate manufacturing can be done with ease. This means that desired

quantities which are needed for meeting production is stipulated in inventory management report

which is then ordered by management. Thus, excess quantity is not ordered and no handling

costs are incurred for keeping stock in warehouse (Management accounting reports, 2017).

C. Benefits of management accounting systems

Price optimisation-

It is quite beneficial for Agmet as it helps to quote prices of products in relation to

demand and preferences of customers up to a high extent. Firm is able to take advantage of such

technique because if higher prices are set, then customer's will get attracted to rivals

(Honggowati and et.al, 2017).

3

Cost accounting-

Various costs are analysed by management and unnecessary expenditures are clarified by

cost accounting system. It is useful for company in order to attain efficiency with regard to

company's operational activities which requires incurring different costs for attaining

manufacturing. Cost accounting system is beneficial as costs that do not form part of current

project are assessed and then eradicated for enhancing desired production.

Job costing system-

Job costing is helpful as there are various costs incurred on overheads, materials and

labour which are needed in order to attain manufacturing in the best possible manner. Costs are

analysed for different jobs and steps are taken to eradicate those costs which are not efficiently

generating output. Hence, this system is quite effective for Agmet to make proper analysis of

production costs.

Inventory system-

Stock is an integral part of company in order to attain production in a better way.

Inventory needs to be ordered in desired quantity so that Agmet may effectively produce items

and no wastage may occur (Leotta, Rizza and Ruggeri, 2017). In relation to this, if stock is not

being ordered in adequate manner, then it leads to loss of scarce resources. Hence, organisation

can attain benefits out of inventory system of management accounting in order to accomplish

desired production and that too without wastage of the same.

D. Integrated management accounting system

Integrated management accounting system helps in standardizing procedures for tracing

transactions and disseminates information related to finance. It helps in interconnecting its

reporting activities of various functional areas of business. It helps in enabling real time

information with context of business transactions. In the similar aspect, it serves as stop for

whole accounting information which consist of financial, managerial and cash flow accounting

(Integrated management accounting system, 2018).

4

Various costs are analysed by management and unnecessary expenditures are clarified by

cost accounting system. It is useful for company in order to attain efficiency with regard to

company's operational activities which requires incurring different costs for attaining

manufacturing. Cost accounting system is beneficial as costs that do not form part of current

project are assessed and then eradicated for enhancing desired production.

Job costing system-

Job costing is helpful as there are various costs incurred on overheads, materials and

labour which are needed in order to attain manufacturing in the best possible manner. Costs are

analysed for different jobs and steps are taken to eradicate those costs which are not efficiently

generating output. Hence, this system is quite effective for Agmet to make proper analysis of

production costs.

Inventory system-

Stock is an integral part of company in order to attain production in a better way.

Inventory needs to be ordered in desired quantity so that Agmet may effectively produce items

and no wastage may occur (Leotta, Rizza and Ruggeri, 2017). In relation to this, if stock is not

being ordered in adequate manner, then it leads to loss of scarce resources. Hence, organisation

can attain benefits out of inventory system of management accounting in order to accomplish

desired production and that too without wastage of the same.

D. Integrated management accounting system

Integrated management accounting system helps in standardizing procedures for tracing

transactions and disseminates information related to finance. It helps in interconnecting its

reporting activities of various functional areas of business. It helps in enabling real time

information with context of business transactions. In the similar aspect, it serves as stop for

whole accounting information which consist of financial, managerial and cash flow accounting

(Integrated management accounting system, 2018).

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TASK 2

A.1) Explanation of absorption and marginal costing method

Absorption costing: It is also referred as full costing as conventional technique for

pertaining cost. It is considered as practice for charging overall costs with both fixed and variable

to products, operations and processes. This technique is oldest and widely used for ascertaining

cost. In this method, cost is formed through direct and overhead cost which is absorbed on

appropriate basis. In simple words, cost of finished unit with context of inventory comprises

direct labour and material along with variable and fixed manufacturing overhead. It is directly

contrasted with direct or variable costing. In this technique, fixed manufacturing overhead cost is

not assigned or allocated to manufactured products. Variable costing is applicable for process of

decision making in management. There is a huge requirement of absorption costing for income

tax and financial reporting. Hence, it is defined as a way for accumulating cost linked with

process of production and apportioned in separate products (Absorption costing, 2018).

Generally, it is mandatory for accounting standards for creating inventory valuation which is

mentioned in balance sheet of organization.

Marginal costing: It is referred as principle where variable cost is directly charged to its

cost units and fixed is instantly attributed to relevant period which is written off in whole aspect.

It is ascertained to marginal technique and provides impact on change in volume or kind of result

for creating difference among variable and fixed cost. This concept is based on cost's behaviour

which varies from its volume of result. It is also known as variable costing where all variable

expenses are accumulated and cost per unit is pertained. In this approach, it is not possible for

determining amount of net per profit per product but contribution per product could be identified

towards profits and fixed overheads. Generally, this term implies involvement of additional cost

for generating an extra unit of result (Hiebl, 2018).

A.2) Preparing Income Statement by considering absorption and marginal costing

Income statement on basis of Marginal costing

Particulars Figures Figures

Sales 33000 33000

5

A.1) Explanation of absorption and marginal costing method

Absorption costing: It is also referred as full costing as conventional technique for

pertaining cost. It is considered as practice for charging overall costs with both fixed and variable

to products, operations and processes. This technique is oldest and widely used for ascertaining

cost. In this method, cost is formed through direct and overhead cost which is absorbed on

appropriate basis. In simple words, cost of finished unit with context of inventory comprises

direct labour and material along with variable and fixed manufacturing overhead. It is directly

contrasted with direct or variable costing. In this technique, fixed manufacturing overhead cost is

not assigned or allocated to manufactured products. Variable costing is applicable for process of

decision making in management. There is a huge requirement of absorption costing for income

tax and financial reporting. Hence, it is defined as a way for accumulating cost linked with

process of production and apportioned in separate products (Absorption costing, 2018).

Generally, it is mandatory for accounting standards for creating inventory valuation which is

mentioned in balance sheet of organization.

Marginal costing: It is referred as principle where variable cost is directly charged to its

cost units and fixed is instantly attributed to relevant period which is written off in whole aspect.

It is ascertained to marginal technique and provides impact on change in volume or kind of result

for creating difference among variable and fixed cost. This concept is based on cost's behaviour

which varies from its volume of result. It is also known as variable costing where all variable

expenses are accumulated and cost per unit is pertained. In this approach, it is not possible for

determining amount of net per profit per product but contribution per product could be identified

towards profits and fixed overheads. Generally, this term implies involvement of additional cost

for generating an extra unit of result (Hiebl, 2018).

A.2) Preparing Income Statement by considering absorption and marginal costing

Income statement on basis of Marginal costing

Particulars Figures Figures

Sales 33000 33000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

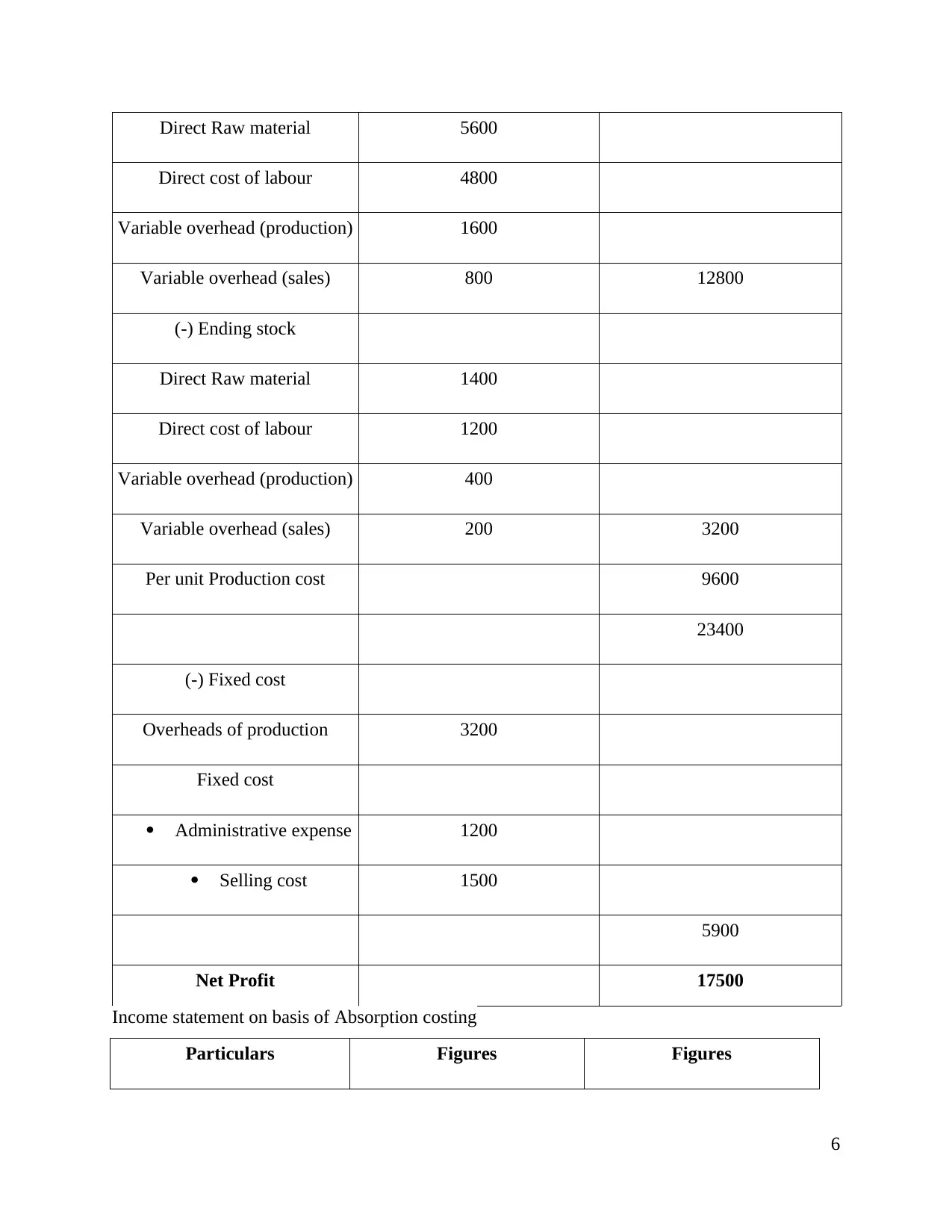

Direct Raw material 5600

Direct cost of labour 4800

Variable overhead (production) 1600

Variable overhead (sales) 800 12800

(-) Ending stock

Direct Raw material 1400

Direct cost of labour 1200

Variable overhead (production) 400

Variable overhead (sales) 200 3200

Per unit Production cost 9600

23400

(-) Fixed cost

Overheads of production 3200

Fixed cost

Administrative expense 1200

Selling cost 1500

5900

Net Profit 17500

Income statement on basis of Absorption costing

Particulars Figures Figures

6

Direct cost of labour 4800

Variable overhead (production) 1600

Variable overhead (sales) 800 12800

(-) Ending stock

Direct Raw material 1400

Direct cost of labour 1200

Variable overhead (production) 400

Variable overhead (sales) 200 3200

Per unit Production cost 9600

23400

(-) Fixed cost

Overheads of production 3200

Fixed cost

Administrative expense 1200

Selling cost 1500

5900

Net Profit 17500

Income statement on basis of Absorption costing

Particulars Figures Figures

6

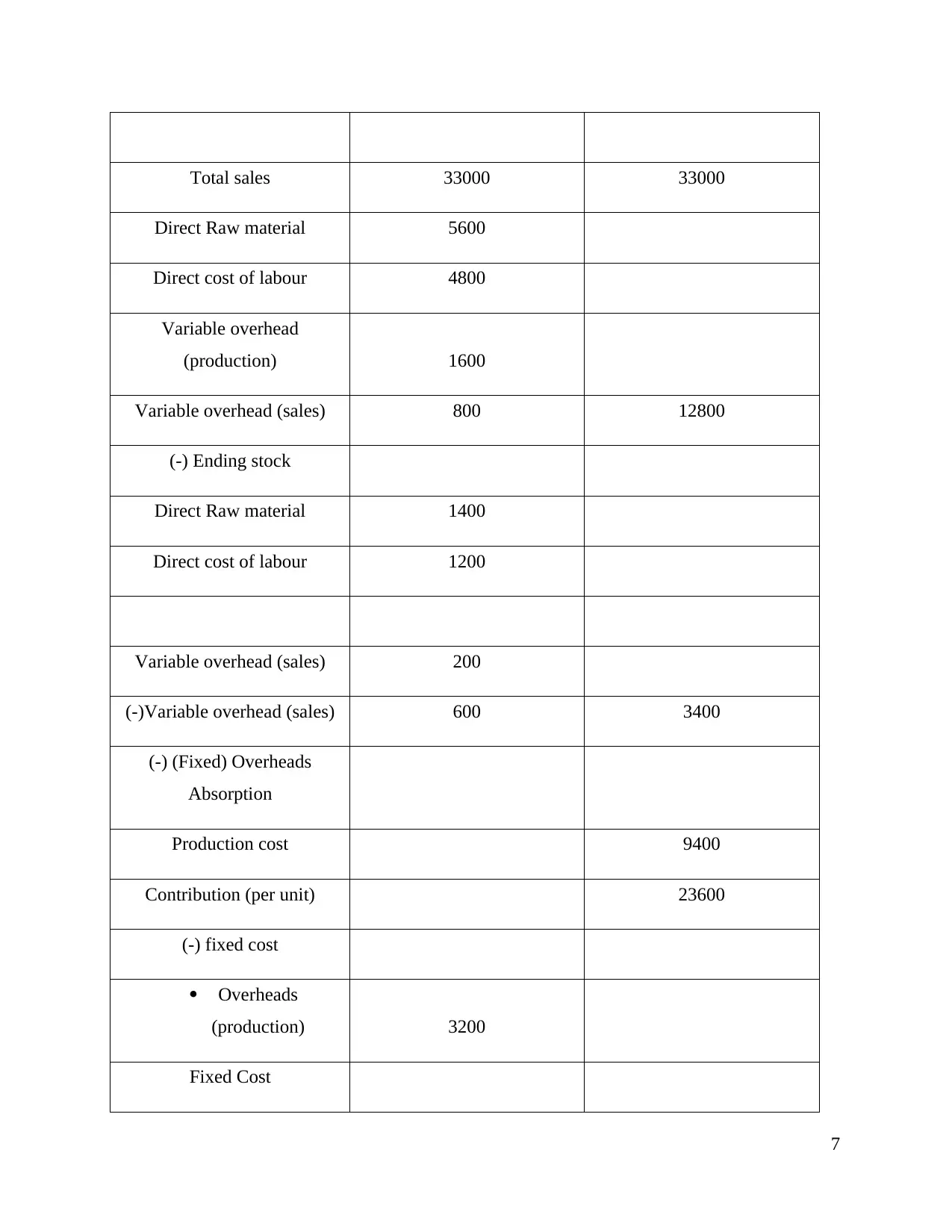

Total sales 33000 33000

Direct Raw material 5600

Direct cost of labour 4800

Variable overhead

(production) 1600

Variable overhead (sales) 800 12800

(-) Ending stock

Direct Raw material 1400

Direct cost of labour 1200

Variable overhead (sales) 200

(-)Variable overhead (sales) 600 3400

(-) (Fixed) Overheads

Absorption

Production cost 9400

Contribution (per unit) 23600

(-) fixed cost

Overheads

(production) 3200

Fixed Cost

7

Direct Raw material 5600

Direct cost of labour 4800

Variable overhead

(production) 1600

Variable overhead (sales) 800 12800

(-) Ending stock

Direct Raw material 1400

Direct cost of labour 1200

Variable overhead (sales) 200

(-)Variable overhead (sales) 600 3400

(-) (Fixed) Overheads

Absorption

Production cost 9400

Contribution (per unit) 23600

(-) fixed cost

Overheads

(production) 3200

Fixed Cost

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Administrative

expense 1200

Selling cost 1500 5900

Net Profit 17700

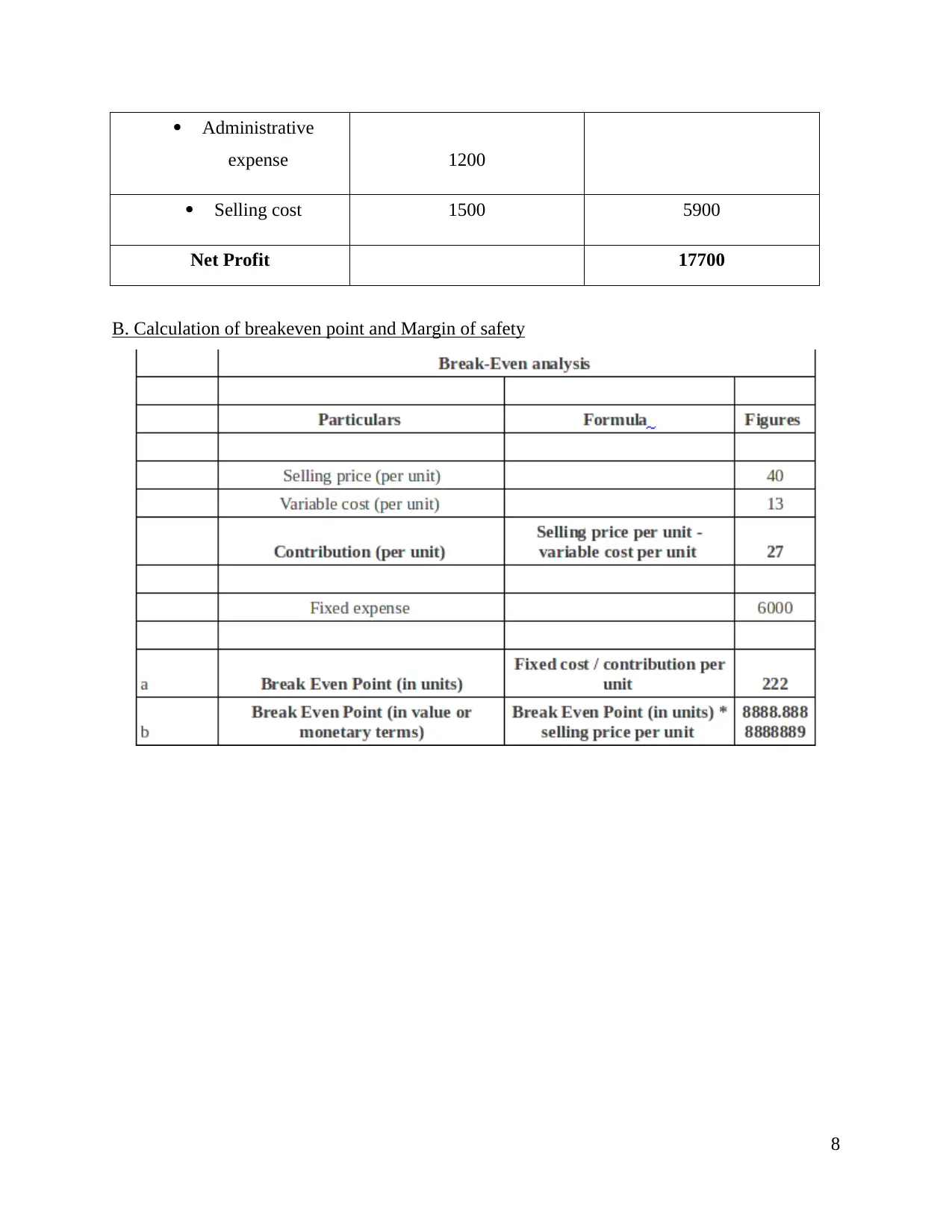

B. Calculation of breakeven point and Margin of safety

8

expense 1200

Selling cost 1500 5900

Net Profit 17700

B. Calculation of breakeven point and Margin of safety

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Difference between marginal and absorption costing

Absorption costing is applied to each cost of production for every produced unit whereas

marginal costing is applied to only inventory cost which had been incurred when individual unit

was generated. With context of marginal costing, overhead costs are charged to expenses where

these are applied to products in absorption costing.

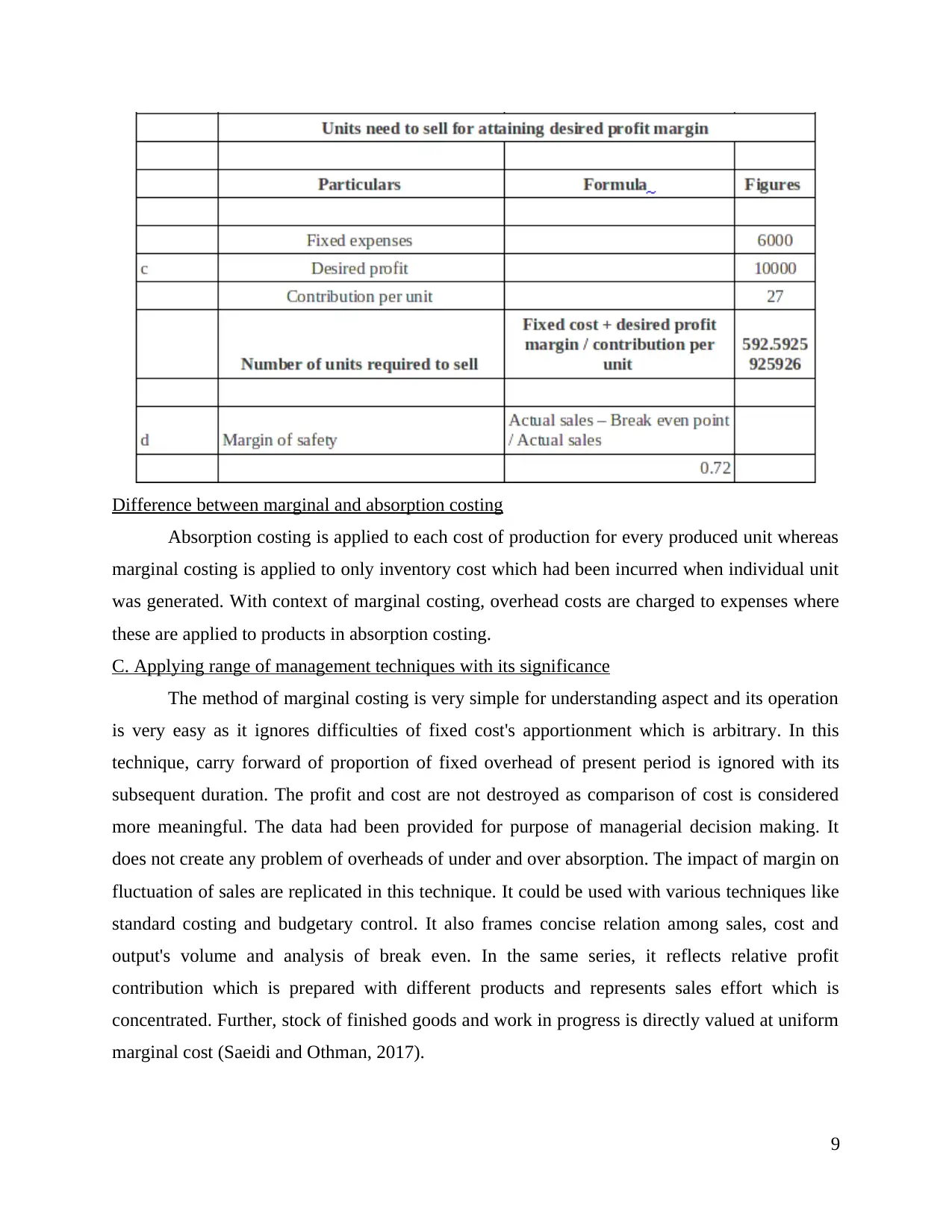

C. Applying range of management techniques with its significance

The method of marginal costing is very simple for understanding aspect and its operation

is very easy as it ignores difficulties of fixed cost's apportionment which is arbitrary. In this

technique, carry forward of proportion of fixed overhead of present period is ignored with its

subsequent duration. The profit and cost are not destroyed as comparison of cost is considered

more meaningful. The data had been provided for purpose of managerial decision making. It

does not create any problem of overheads of under and over absorption. The impact of margin on

fluctuation of sales are replicated in this technique. It could be used with various techniques like

standard costing and budgetary control. It also frames concise relation among sales, cost and

output's volume and analysis of break even. In the same series, it reflects relative profit

contribution which is prepared with different products and represents sales effort which is

concentrated. Further, stock of finished goods and work in progress is directly valued at uniform

marginal cost (Saeidi and Othman, 2017).

9

Absorption costing is applied to each cost of production for every produced unit whereas

marginal costing is applied to only inventory cost which had been incurred when individual unit

was generated. With context of marginal costing, overhead costs are charged to expenses where

these are applied to products in absorption costing.

C. Applying range of management techniques with its significance

The method of marginal costing is very simple for understanding aspect and its operation

is very easy as it ignores difficulties of fixed cost's apportionment which is arbitrary. In this

technique, carry forward of proportion of fixed overhead of present period is ignored with its

subsequent duration. The profit and cost are not destroyed as comparison of cost is considered

more meaningful. The data had been provided for purpose of managerial decision making. It

does not create any problem of overheads of under and over absorption. The impact of margin on

fluctuation of sales are replicated in this technique. It could be used with various techniques like

standard costing and budgetary control. It also frames concise relation among sales, cost and

output's volume and analysis of break even. In the same series, it reflects relative profit

contribution which is prepared with different products and represents sales effort which is

concentrated. Further, stock of finished goods and work in progress is directly valued at uniform

marginal cost (Saeidi and Othman, 2017).

9

Absorption costing technique has major role for preparation of its financial report. It

recognises significance of comprising fixed production cost for its determination and appropriate

pricing policy. The prices on basis of absorption costing ensures about each covered cost. In the

same aspect, it conforms with matching and accrual concept as it has need of similar costs with

revenue for specific accounting period. It has directly recognised for objective of forming

external report and valuation of inventory. Generally, it ignores separation of cost in variable and

fixed elements which are performed in accurate or easy aspect. The over and under absorption of

factory overheads is presented in this technique as it discloses efficient and inefficient

optimisation of resources of production which is impossible for variable costing. It has presence

of fewer fluctuations in profit during constant production but with fluctuation in sales (Jermias,

2017).

D. Producing financial reports with appropriate interpretation

There is appropriate presentation of statement of profit loss by considering both marginal

and absorption costing. According to marginal method, its net income is extracted as 17500 as it

has total sales 33000. In this context, it had generated its direct expense as 12800 which

comprises direct raw material and labour, variable sales and production overhead. Further it had

excluded the ending inventory of 3200 which had calculated cost of production at per unit. In the

similar aspect, all fixed expenses are adjusted which had given net profit.

It had shown income statement on basis of absorption costing with similar revenue of

33000. There is a major difference in absorption and marginal costing for attaining net income

which is adjustment of variable of sales overhead. In the present scenario, every organization is

more focused on profit. The organization generates more net income through absorption costing

as compared to marginal technique. Hence, absorption costing technique is more preferable in

context of profit.

Further, it had performed break even analysis with margin of safety as its contribution per

unit is 27 along with fixed expense of 6000. The business entity had specified its break even as

222 units with monetary value of 8888.88. It had extracted units required to sell for

accomplishing desired profit margin as 25926. It margins of safety is 0.72 when 800 products are

sold.

10

recognises significance of comprising fixed production cost for its determination and appropriate

pricing policy. The prices on basis of absorption costing ensures about each covered cost. In the

same aspect, it conforms with matching and accrual concept as it has need of similar costs with

revenue for specific accounting period. It has directly recognised for objective of forming

external report and valuation of inventory. Generally, it ignores separation of cost in variable and

fixed elements which are performed in accurate or easy aspect. The over and under absorption of

factory overheads is presented in this technique as it discloses efficient and inefficient

optimisation of resources of production which is impossible for variable costing. It has presence

of fewer fluctuations in profit during constant production but with fluctuation in sales (Jermias,

2017).

D. Producing financial reports with appropriate interpretation

There is appropriate presentation of statement of profit loss by considering both marginal

and absorption costing. According to marginal method, its net income is extracted as 17500 as it

has total sales 33000. In this context, it had generated its direct expense as 12800 which

comprises direct raw material and labour, variable sales and production overhead. Further it had

excluded the ending inventory of 3200 which had calculated cost of production at per unit. In the

similar aspect, all fixed expenses are adjusted which had given net profit.

It had shown income statement on basis of absorption costing with similar revenue of

33000. There is a major difference in absorption and marginal costing for attaining net income

which is adjustment of variable of sales overhead. In the present scenario, every organization is

more focused on profit. The organization generates more net income through absorption costing

as compared to marginal technique. Hence, absorption costing technique is more preferable in

context of profit.

Further, it had performed break even analysis with margin of safety as its contribution per

unit is 27 along with fixed expense of 6000. The business entity had specified its break even as

222 units with monetary value of 8888.88. It had extracted units required to sell for

accomplishing desired profit margin as 25926. It margins of safety is 0.72 when 800 products are

sold.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.