Management Accounting and Control: Tottenham Plc. Analysis

VerifiedAdded on 2020/01/28

|13

|4123

|61

Report

AI Summary

This report provides a comprehensive analysis of management accounting practices, particularly within the context of Tottenham Plc. It explores the importance of management accounting for sustainable organizational development and examines key concepts such as relevant costs, decision-making processes, and responsibility accounting. The report delves into various aspects, including quantitative decision problems, relevant cost identification, opportunity costs, and shutdown decisions. Furthermore, it analyzes outsourcing decisions and the application of standard costing frameworks. The report uses examples to illustrate financial decisions and strategic considerations. The assignment covers topics such as cost analysis, revenue generation, and the implementation of management accounting tools to achieve organizational objectives. The report concludes by emphasizing the role of management accounting in achieving long-term goals and controlling costs.

Management Accounting

& Control

& Control

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

PART.A...........................................................................................................................................3

a)..................................................................................................................................................3

b).................................................................................................................................................6

PART.B............................................................................................................................................8

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION...........................................................................................................................3

PART.A...........................................................................................................................................3

a)..................................................................................................................................................3

b).................................................................................................................................................6

PART.B............................................................................................................................................8

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

INTRODUCTION

Management accounting practices are the key part for developing of organisation in a

sustainable use. Nowadays, every organisation is opting the management accounting practices in

their business(Zimmerman and Yahya-Zadeh, 2011). Management accounting practices are

helpful for the development of the firm as this would lead to gain the better decisions for the firm

so as to get the effective run. There are so many qualified management accountants who look

after all the key related management practices in the firm(Granlund, 2011). Tottenham Plc. Is

required to adopt effective management accounting practices which are used for the fixing the

price for the product which cited company going to produce or going to buy from various sub

contractors. Before going to fix the price of the products, there is need to make the strategy in

order to understand the potential consumers perception about the product.

PART.A

a).

The decisions are taken by the top level authority in Tottenham Plc. After taking extensive

research about the market where the cited company is going to operate. There are so many

components which are going to opt while taking decisions in the firm. Basically a quantitative

decision problems includes six major sections which are mentioned hereunder;

1) A target which could be quantified Sometimes alluded to as 'target work', e.g. expansion of

revenues or minimisation of aggregate cost of the product(Ahmad-Zaluki, Campbell and

Goodacre, 2011).

2) Many decision issues have at least one constraints, e.g. scarce raw materials, limited labour,

and so on. The cited company needs to locate the targets which are going to maximise revenues

subject to characterized limitations.

3) A scope of option game-plans under consideration. For instance, keeping in mind the end goal

to limit expenses of an assembling operation, the accessible decisions might be:

i) to keep producing as at present.

ii) to change the assembling technique

iii) to sub-contract the work to an outsider.

4) Forecasting of the increasing expenses and advantages of every option strategy.

Management accounting practices are the key part for developing of organisation in a

sustainable use. Nowadays, every organisation is opting the management accounting practices in

their business(Zimmerman and Yahya-Zadeh, 2011). Management accounting practices are

helpful for the development of the firm as this would lead to gain the better decisions for the firm

so as to get the effective run. There are so many qualified management accountants who look

after all the key related management practices in the firm(Granlund, 2011). Tottenham Plc. Is

required to adopt effective management accounting practices which are used for the fixing the

price for the product which cited company going to produce or going to buy from various sub

contractors. Before going to fix the price of the products, there is need to make the strategy in

order to understand the potential consumers perception about the product.

PART.A

a).

The decisions are taken by the top level authority in Tottenham Plc. After taking extensive

research about the market where the cited company is going to operate. There are so many

components which are going to opt while taking decisions in the firm. Basically a quantitative

decision problems includes six major sections which are mentioned hereunder;

1) A target which could be quantified Sometimes alluded to as 'target work', e.g. expansion of

revenues or minimisation of aggregate cost of the product(Ahmad-Zaluki, Campbell and

Goodacre, 2011).

2) Many decision issues have at least one constraints, e.g. scarce raw materials, limited labour,

and so on. The cited company needs to locate the targets which are going to maximise revenues

subject to characterized limitations.

3) A scope of option game-plans under consideration. For instance, keeping in mind the end goal

to limit expenses of an assembling operation, the accessible decisions might be:

i) to keep producing as at present.

ii) to change the assembling technique

iii) to sub-contract the work to an outsider.

4) Forecasting of the increasing expenses and advantages of every option strategy.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

5) implementation of the decision criteria or target work, e.g. the estimation of expected benefit

or contribution, and the positioning of decisions.

6) Decision of preferred options(Ahmad-Zaluki, Campbell and Goodacre, 2011.).

Significant expenses for basic leadership

The costs which ought to be utilized for decision making are regularly alluded to as "significant

cost”. Relevant cost is the cost which is suitable to supporting for making on of particular

administrative decisions.

To influence a decision a cost must be:

a) Future: Past expenses are immaterial, as management accountants can't influence them by

current decisions and they are basic to whole alternatives that they may pick.

b) Incremental: Expenditures which are going to be acquired or stayed away for settling on a

decision. Any cost which is going to be occurred regardless of whether the decision is made are

not, are said to be enhancement to the decision.

c) Cash flow: Depreciation is that kind of cost which is not consider in the cash flow. Thus, the

book benefit of existing gear is not relevant , yet, the disposal value is significant.

Different terms:

d) Common costs: Costs which will be identical for all options are immaterial, e.g. lease or rates

on a plant would be caused whatever items are created(Hoque, 2011).

e) Sunk costs: This is the past cost which are constantly insignificant. These are like-fixed cost,

improvement costs as of now brought about.

f) Committed costs: A future cash outflow which is going to be incurred be obtain in any case,

whatever the current decision will be? , e.g. contracts which have already made, can't be

modified.

Opportunity cost:

Opportunity cost is the cost which is also known as relevant cost in the business. Opportunity

cost is the advantage forgone by picking one opportunity rather than the following best option.

An opportunity cost is simply defined by way of taking examples:

An organization is thinking about distributing a limited edition book which is bound in an

extraordinary leather. It has in stock the leather was getting a few years back for $2,000. To

purchase a proportionate amount now cited company need to spend cost $4,000. The

or contribution, and the positioning of decisions.

6) Decision of preferred options(Ahmad-Zaluki, Campbell and Goodacre, 2011.).

Significant expenses for basic leadership

The costs which ought to be utilized for decision making are regularly alluded to as "significant

cost”. Relevant cost is the cost which is suitable to supporting for making on of particular

administrative decisions.

To influence a decision a cost must be:

a) Future: Past expenses are immaterial, as management accountants can't influence them by

current decisions and they are basic to whole alternatives that they may pick.

b) Incremental: Expenditures which are going to be acquired or stayed away for settling on a

decision. Any cost which is going to be occurred regardless of whether the decision is made are

not, are said to be enhancement to the decision.

c) Cash flow: Depreciation is that kind of cost which is not consider in the cash flow. Thus, the

book benefit of existing gear is not relevant , yet, the disposal value is significant.

Different terms:

d) Common costs: Costs which will be identical for all options are immaterial, e.g. lease or rates

on a plant would be caused whatever items are created(Hoque, 2011).

e) Sunk costs: This is the past cost which are constantly insignificant. These are like-fixed cost,

improvement costs as of now brought about.

f) Committed costs: A future cash outflow which is going to be incurred be obtain in any case,

whatever the current decision will be? , e.g. contracts which have already made, can't be

modified.

Opportunity cost:

Opportunity cost is the cost which is also known as relevant cost in the business. Opportunity

cost is the advantage forgone by picking one opportunity rather than the following best option.

An opportunity cost is simply defined by way of taking examples:

An organization is thinking about distributing a limited edition book which is bound in an

extraordinary leather. It has in stock the leather was getting a few years back for $2,000. To

purchase a proportionate amount now cited company need to spend cost $4,000. The

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

organization has no arrangements to utilize the leather for different purposes, in spite of the fact

that it could be considered for the potential outcomes(Lambert and Sponem, 2012). like- of

utilizing it to cover desk area decorations, in swap for other material which could cost $1800, the

another use of selling it if a purchaser could be found if the proceeds are exceeds over $1600.

In computing the probable benefit from the proposed book before choosing to proceed

with the venture, the leather is not going to be costed at $2,000. The cost was acquired in the past

for reasons unknown which is not applicable now. The leather exists and this can be utilized over

the book without acquiring a particular cost. In utilizing the leather over the book, then the cited

company lose the opportunities, the organization will lose the chances of either discarding it for

$1600 or of utilizing it to spare an expense of $1800 on desk furniture(Vakalfotis, Ballantine and

Wall, 2013).

The better of these options, from the perspective of profiting from the leather, is the last

mentioned. "Lost opportunity" cost of $1800 will accordingly be incorporated into the cost of the

book for decision making process.

For making the decisions for the firm, relevant cost would be the total of:

avoidable expense costs', i.e. the costs which will be brought about if the book venture is

affirmed, and will be kept away from, if this would not implemented.

Shutdown issues cover the undermentioned decisions in the Tottenham Plc:

a) Whether or not to shut down an industrial facility, office, product line or other action, either in

making loss to the firm or impossible to run due to the over expensiveness.

b) If the decision is to close down, regardless of whether the conclusion ought to be perpetual or

temporary(Frezatti and et. al., 2011). Shutdown decisions frequently include long lasting

considerations, and capital incomes and expenses.

c)Shutdown ought to bring about investment funds in yearly working expenses for various years

in the future years.

d)Closure brings about arrival of some fixed assets available to be purchased. There are few

assets which have less scrap value, on the other hand, few property may have a generous sales

value.

that it could be considered for the potential outcomes(Lambert and Sponem, 2012). like- of

utilizing it to cover desk area decorations, in swap for other material which could cost $1800, the

another use of selling it if a purchaser could be found if the proceeds are exceeds over $1600.

In computing the probable benefit from the proposed book before choosing to proceed

with the venture, the leather is not going to be costed at $2,000. The cost was acquired in the past

for reasons unknown which is not applicable now. The leather exists and this can be utilized over

the book without acquiring a particular cost. In utilizing the leather over the book, then the cited

company lose the opportunities, the organization will lose the chances of either discarding it for

$1600 or of utilizing it to spare an expense of $1800 on desk furniture(Vakalfotis, Ballantine and

Wall, 2013).

The better of these options, from the perspective of profiting from the leather, is the last

mentioned. "Lost opportunity" cost of $1800 will accordingly be incorporated into the cost of the

book for decision making process.

For making the decisions for the firm, relevant cost would be the total of:

avoidable expense costs', i.e. the costs which will be brought about if the book venture is

affirmed, and will be kept away from, if this would not implemented.

Shutdown issues cover the undermentioned decisions in the Tottenham Plc:

a) Whether or not to shut down an industrial facility, office, product line or other action, either in

making loss to the firm or impossible to run due to the over expensiveness.

b) If the decision is to close down, regardless of whether the conclusion ought to be perpetual or

temporary(Frezatti and et. al., 2011). Shutdown decisions frequently include long lasting

considerations, and capital incomes and expenses.

c)Shutdown ought to bring about investment funds in yearly working expenses for various years

in the future years.

d)Closure brings about arrival of some fixed assets available to be purchased. There are few

assets which have less scrap value, on the other hand, few property may have a generous sales

value.

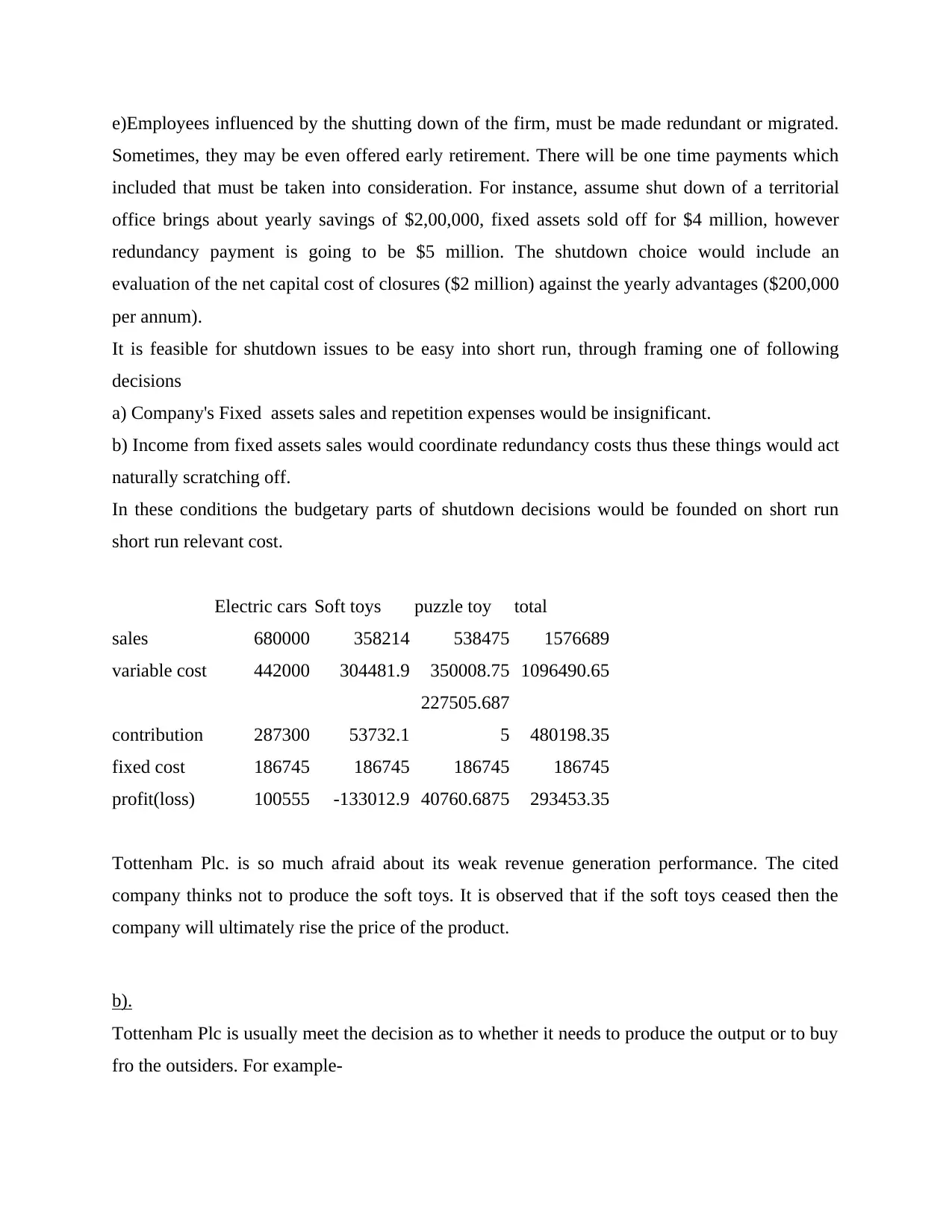

e)Employees influenced by the shutting down of the firm, must be made redundant or migrated.

Sometimes, they may be even offered early retirement. There will be one time payments which

included that must be taken into consideration. For instance, assume shut down of a territorial

office brings about yearly savings of $2,00,000, fixed assets sold off for $4 million, however

redundancy payment is going to be $5 million. The shutdown choice would include an

evaluation of the net capital cost of closures ($2 million) against the yearly advantages ($200,000

per annum).

It is feasible for shutdown issues to be easy into short run, through framing one of following

decisions

a) Company's Fixed assets sales and repetition expenses would be insignificant.

b) Income from fixed assets sales would coordinate redundancy costs thus these things would act

naturally scratching off.

In these conditions the budgetary parts of shutdown decisions would be founded on short run

short run relevant cost.

Electric cars Soft toys puzzle toy total

sales 680000 358214 538475 1576689

variable cost 442000 304481.9 350008.75 1096490.65

contribution 287300 53732.1

227505.687

5 480198.35

fixed cost 186745 186745 186745 186745

profit(loss) 100555 -133012.9 40760.6875 293453.35

Tottenham Plc. is so much afraid about its weak revenue generation performance. The cited

company thinks not to produce the soft toys. It is observed that if the soft toys ceased then the

company will ultimately rise the price of the product.

b).

Tottenham Plc is usually meet the decision as to whether it needs to produce the output or to buy

fro the outsiders. For example-

Sometimes, they may be even offered early retirement. There will be one time payments which

included that must be taken into consideration. For instance, assume shut down of a territorial

office brings about yearly savings of $2,00,000, fixed assets sold off for $4 million, however

redundancy payment is going to be $5 million. The shutdown choice would include an

evaluation of the net capital cost of closures ($2 million) against the yearly advantages ($200,000

per annum).

It is feasible for shutdown issues to be easy into short run, through framing one of following

decisions

a) Company's Fixed assets sales and repetition expenses would be insignificant.

b) Income from fixed assets sales would coordinate redundancy costs thus these things would act

naturally scratching off.

In these conditions the budgetary parts of shutdown decisions would be founded on short run

short run relevant cost.

Electric cars Soft toys puzzle toy total

sales 680000 358214 538475 1576689

variable cost 442000 304481.9 350008.75 1096490.65

contribution 287300 53732.1

227505.687

5 480198.35

fixed cost 186745 186745 186745 186745

profit(loss) 100555 -133012.9 40760.6875 293453.35

Tottenham Plc. is so much afraid about its weak revenue generation performance. The cited

company thinks not to produce the soft toys. It is observed that if the soft toys ceased then the

company will ultimately rise the price of the product.

b).

Tottenham Plc is usually meet the decision as to whether it needs to produce the output or to buy

fro the outsiders. For example-

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

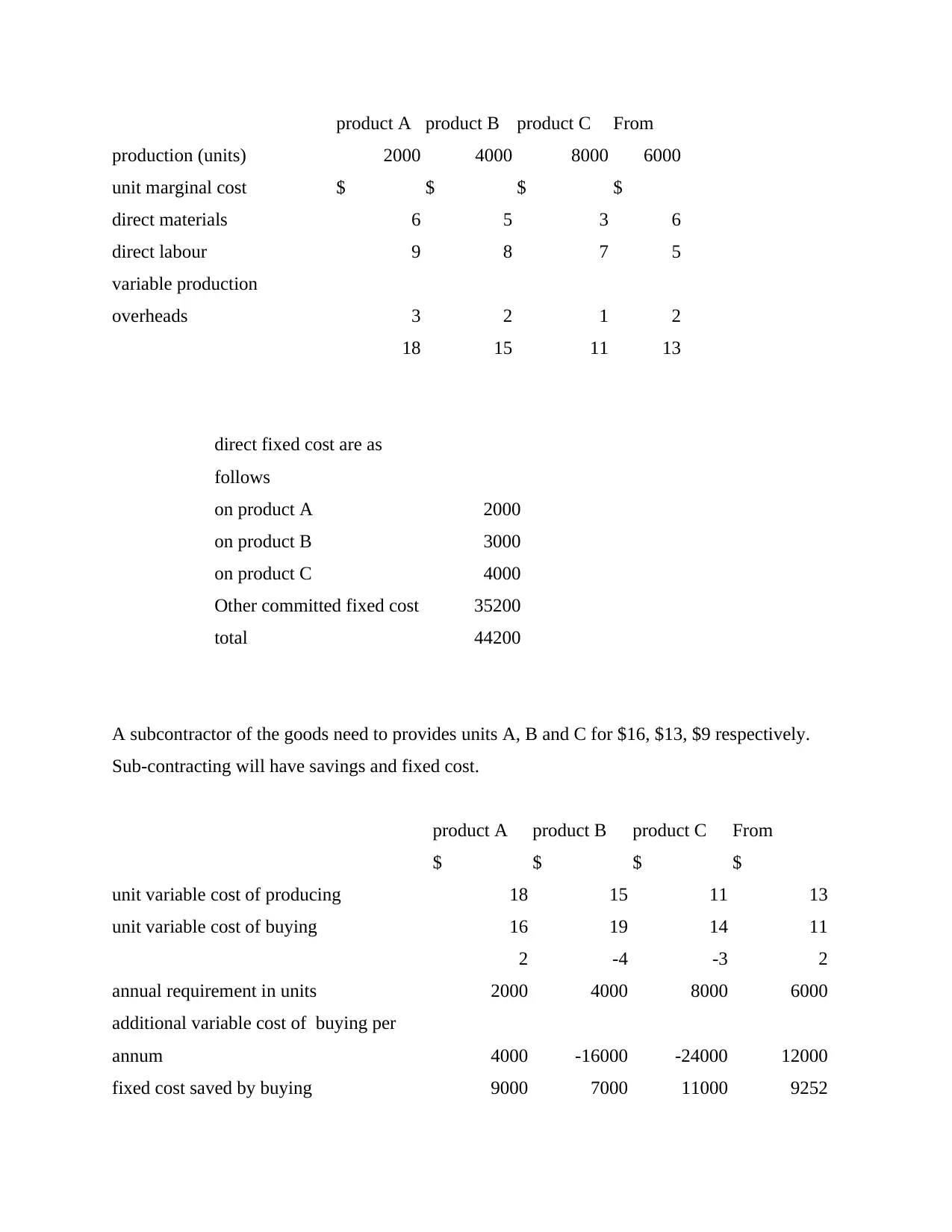

product A product B product C From

production (units) 2000 4000 8000 6000

unit marginal cost $ $ $ $

direct materials 6 5 3 6

direct labour 9 8 7 5

variable production

overheads 3 2 1 2

18 15 11 13

direct fixed cost are as

follows

on product A 2000

on product B 3000

on product C 4000

Other committed fixed cost 35200

total 44200

A subcontractor of the goods need to provides units A, B and C for $16, $13, $9 respectively.

Sub-contracting will have savings and fixed cost.

product A product B product C From

$ $ $ $

unit variable cost of producing 18 15 11 13

unit variable cost of buying 16 19 14 11

2 -4 -3 2

annual requirement in units 2000 4000 8000 6000

additional variable cost of buying per

annum 4000 -16000 -24000 12000

fixed cost saved by buying 9000 7000 11000 9252

production (units) 2000 4000 8000 6000

unit marginal cost $ $ $ $

direct materials 6 5 3 6

direct labour 9 8 7 5

variable production

overheads 3 2 1 2

18 15 11 13

direct fixed cost are as

follows

on product A 2000

on product B 3000

on product C 4000

Other committed fixed cost 35200

total 44200

A subcontractor of the goods need to provides units A, B and C for $16, $13, $9 respectively.

Sub-contracting will have savings and fixed cost.

product A product B product C From

$ $ $ $

unit variable cost of producing 18 15 11 13

unit variable cost of buying 16 19 14 11

2 -4 -3 2

annual requirement in units 2000 4000 8000 6000

additional variable cost of buying per

annum 4000 -16000 -24000 12000

fixed cost saved by buying 9000 7000 11000 9252

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

extra total cost of buying -5000 9000 13000 2748

The cited company would save the $5000 by sub- contracting Product A.

Under this example, relevant cost are the variable costs of in-house manufacture, the variable

cost of buying components, and finally the savings in fixed cost.

Other critical considerations are as per the following:

i) If the cited organisation will buy the product A, then the organization will have save limit. By

what method, the cited organisation ought to that extra limit be productively utilized?

ii) Would the sub-contractor worker be solid with conveyance times, and handle great control

and quality through producing internally(Caglio and Ditillo, 2012).

iii) Does the cited organization wish to be adaptable and keep up better control over

operations by framing everything itself?

PART.B

One of the primary targets of Tottenham Plc. is to limit the cost of production and to limit

the cost as these are the scarce resources under the cited company. Management accounting

helps to give a various devices keeping in mind the end goal to accomplish the firm's long term

objectives. In this specific circumstance, the framework for gathering and detailing income and

cost data by territories of obligation is called duty accounting. It depends on the presumption that

directors ought to be considered responsible of their execution. Responsibility accounting

framework coordinates obligation centre inside the association. Although, responsibility centres

ate the places where through which cost and income can be controlled. There are diverse sorts of

responsibility centres, like- revenue centre, investment centre, income centre and cost

centre(Østergren and Stensaker, 2011).

Under standard costing framework, pre- determined forecasting of items and services will

be built up and after that compared with the real cost as they are incurred. Forecasting cost are

standard costs, which ought to be brought about under proficient operations. Variance is the

outcome which have been comparing the actual results with the anticipated results. There is also

required to highlight that standard cost is different to the budgeted cost. The foremost contrasts

between them come under the scope(Qian, Burritt and Monroe, 2011). Both are worried with

setting down cost limits for controlling. However, planned expenses force reduce to aggregate

The cited company would save the $5000 by sub- contracting Product A.

Under this example, relevant cost are the variable costs of in-house manufacture, the variable

cost of buying components, and finally the savings in fixed cost.

Other critical considerations are as per the following:

i) If the cited organisation will buy the product A, then the organization will have save limit. By

what method, the cited organisation ought to that extra limit be productively utilized?

ii) Would the sub-contractor worker be solid with conveyance times, and handle great control

and quality through producing internally(Caglio and Ditillo, 2012).

iii) Does the cited organization wish to be adaptable and keep up better control over

operations by framing everything itself?

PART.B

One of the primary targets of Tottenham Plc. is to limit the cost of production and to limit

the cost as these are the scarce resources under the cited company. Management accounting

helps to give a various devices keeping in mind the end goal to accomplish the firm's long term

objectives. In this specific circumstance, the framework for gathering and detailing income and

cost data by territories of obligation is called duty accounting. It depends on the presumption that

directors ought to be considered responsible of their execution. Responsibility accounting

framework coordinates obligation centre inside the association. Although, responsibility centres

ate the places where through which cost and income can be controlled. There are diverse sorts of

responsibility centres, like- revenue centre, investment centre, income centre and cost

centre(Østergren and Stensaker, 2011).

Under standard costing framework, pre- determined forecasting of items and services will

be built up and after that compared with the real cost as they are incurred. Forecasting cost are

standard costs, which ought to be brought about under proficient operations. Variance is the

outcome which have been comparing the actual results with the anticipated results. There is also

required to highlight that standard cost is different to the budgeted cost. The foremost contrasts

between them come under the scope(Qian, Burritt and Monroe, 2011). Both are worried with

setting down cost limits for controlling. However, planned expenses force reduce to aggregate

cost for an association and standard cost are joined to items and to individual assembling

operations.

Standard costing frameworks are connected in cost centre where the product could be

calculated and the information required to deliver every unit of product could be determined.

Subsequently, standard costing is most suited to associations which produce the similar

products on a repetitive basis(Cadez and Guilding, 2012). However, standard costing framework

is specially used in the production of output. But, these can apply additionally to administration

enterprises, like-transport and to parts of general society area. Furthermore, associations that

create an extensive variety of items could utilize a standard costing framework in their

operations. Hereunder, the standard cost is going to established for the repetitive basis.

Unit standard cost are determined by joining the standard cost from the operations which

are essential to make their product. It also need to point out that under standard costing, there is

not only compare the actual cost to the budgeted cost, but also, report the actual cost to the cost

centre. Standard costing is the framework which does not easily use for the non repetitive

product manufacturing firms(Grabner and Moers, 2013). If the company use the effective cost

control then there is need to fix the standard cost after having careful analysis. Cost standards

must be set up for all classes of costs and for all cost centre. Standard cost can be set up taking

after two methodologies. Firstly, verifiable records can be utilized as a part of request to

estimate work and material utilization. Besides, designing learns about every operation, which

depend on cautious determinations of material, labour and equipments, can be utilized to set up

the standard cost. Because, as a result of their wide learning of engineers are frequently required

in setting these standard cost. It must be specified that utilizing historical records may

incorporate past wasteful aspects(Strumickas and Valanciene, 2015). Standard costing

frameworks is contrasted with designing reviews less time and cost consuming and broadly

utilized as a part of practice.

Keeping in mind the end goal to set up standard cost for material three things must be

understand about the material sources of info: what sorts of information sources are utilized.

Generally determinations for materials, covering quality and amount, are entered on a bill of

materials(Arjaliès and Mundy, 2013). This bill states the correct amount of materials for every

operation finishing an output . Furthermore, managers and the top level authority ought to take

advice form the cost accountants, material specialists or providers in fixing on quality choices.

operations.

Standard costing frameworks are connected in cost centre where the product could be

calculated and the information required to deliver every unit of product could be determined.

Subsequently, standard costing is most suited to associations which produce the similar

products on a repetitive basis(Cadez and Guilding, 2012). However, standard costing framework

is specially used in the production of output. But, these can apply additionally to administration

enterprises, like-transport and to parts of general society area. Furthermore, associations that

create an extensive variety of items could utilize a standard costing framework in their

operations. Hereunder, the standard cost is going to established for the repetitive basis.

Unit standard cost are determined by joining the standard cost from the operations which

are essential to make their product. It also need to point out that under standard costing, there is

not only compare the actual cost to the budgeted cost, but also, report the actual cost to the cost

centre. Standard costing is the framework which does not easily use for the non repetitive

product manufacturing firms(Grabner and Moers, 2013). If the company use the effective cost

control then there is need to fix the standard cost after having careful analysis. Cost standards

must be set up for all classes of costs and for all cost centre. Standard cost can be set up taking

after two methodologies. Firstly, verifiable records can be utilized as a part of request to

estimate work and material utilization. Besides, designing learns about every operation, which

depend on cautious determinations of material, labour and equipments, can be utilized to set up

the standard cost. Because, as a result of their wide learning of engineers are frequently required

in setting these standard cost. It must be specified that utilizing historical records may

incorporate past wasteful aspects(Strumickas and Valanciene, 2015). Standard costing

frameworks is contrasted with designing reviews less time and cost consuming and broadly

utilized as a part of practice.

Keeping in mind the end goal to set up standard cost for material three things must be

understand about the material sources of info: what sorts of information sources are utilized.

Generally determinations for materials, covering quality and amount, are entered on a bill of

materials(Arjaliès and Mundy, 2013). This bill states the correct amount of materials for every

operation finishing an output . Furthermore, managers and the top level authority ought to take

advice form the cost accountants, material specialists or providers in fixing on quality choices.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

After the standard amounts are set up costs for every material part should be set up. The standard

costs are acquired from the buying division that knows best what suppliers gives the most proper

material in the most sensible time period and at the no more sensible cost(Davies and Crawford,

2011). The standard expenses for material are then ascertained by duplicating the amount

standard that ought to be utilized per unit by the standard cost paid for every unit.

The way toward setting up direct labour models is like material. Every manufacturing

process performed by labours which will be investigated with a specific end goal to decide the

quantity of standard hours required by a normal workers to finish the job. Exercises like- clean-

up, setup, and routine upkeep are incorporated into the standard time(Parker, 2012). Although,

every single unnecessary movement by specialists ought to be slighted on the grounds that as

appeared in the realistic a day is not spent in totally gainful work.

The cost accountants in the cited company will multiply the standard labour cost to the standard

hours. Besides, an overhead standard rate is the foreordained overhead rate, which is a budgeted

and consistent charge per unit of movement that is utilized to relegate overhead to the period's

generation.

This rate speaks to a normal cost for every unit of activity(Hiebl and M.R, 2014). To compute

forecasted overhead rate, the association separates budgeted future general expenses at a

particular level by that movement level. The standard overhead rate is typically in light of a rate

for each direct labour. separate rate for fixed and variable overheads are imperative for planning

and control. Although, Variable overhead costs fluctuate straightforwardly with the output and

these are connected to genuine profits as per the predetermined rate. Conversely, fixed expenses

don't change with change with the output(Otley and Emmanuel, 2013). because of this, a

standard output must be planned keeping in mind the end goal to compute fixed overhead rate.

After the measures for direct material, direct labour, overhead has been fixed a standard cost card

as appeared underneath is framed.

The guidelines inside a card should constantly be audited keeping in mind the end goal to

guarantee that the standards displays current targets. Besides, the guidelines give now the

premise to a point by point difference examination(Fullerton, Kennedy and Widener, S.K.,

2013).

costs are acquired from the buying division that knows best what suppliers gives the most proper

material in the most sensible time period and at the no more sensible cost(Davies and Crawford,

2011). The standard expenses for material are then ascertained by duplicating the amount

standard that ought to be utilized per unit by the standard cost paid for every unit.

The way toward setting up direct labour models is like material. Every manufacturing

process performed by labours which will be investigated with a specific end goal to decide the

quantity of standard hours required by a normal workers to finish the job. Exercises like- clean-

up, setup, and routine upkeep are incorporated into the standard time(Parker, 2012). Although,

every single unnecessary movement by specialists ought to be slighted on the grounds that as

appeared in the realistic a day is not spent in totally gainful work.

The cost accountants in the cited company will multiply the standard labour cost to the standard

hours. Besides, an overhead standard rate is the foreordained overhead rate, which is a budgeted

and consistent charge per unit of movement that is utilized to relegate overhead to the period's

generation.

This rate speaks to a normal cost for every unit of activity(Hiebl and M.R, 2014). To compute

forecasted overhead rate, the association separates budgeted future general expenses at a

particular level by that movement level. The standard overhead rate is typically in light of a rate

for each direct labour. separate rate for fixed and variable overheads are imperative for planning

and control. Although, Variable overhead costs fluctuate straightforwardly with the output and

these are connected to genuine profits as per the predetermined rate. Conversely, fixed expenses

don't change with change with the output(Otley and Emmanuel, 2013). because of this, a

standard output must be planned keeping in mind the end goal to compute fixed overhead rate.

After the measures for direct material, direct labour, overhead has been fixed a standard cost card

as appeared underneath is framed.

The guidelines inside a card should constantly be audited keeping in mind the end goal to

guarantee that the standards displays current targets. Besides, the guidelines give now the

premise to a point by point difference examination(Fullerton, Kennedy and Widener, S.K.,

2013).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The standard expenses said give a premise against which genuine cost can be measured and

deviations computed. Deviations assessment is the way toward sorting the nature of the contrasts

between genuine expenses and standard expenses and looking for clarifications for those

distinctions. Unfavourable deviations emerge when the real consumption surpasses the standard

stipend(Granlund, 2011). While on the other hand, positive deviations emerge when the real use

is not as much as the standard remittance. Deviation analysis ought to help top level executives

to figure out who or what is in charge of every deviation. Besides, it is imperative for the top

level executives to know when to act and when it is a bit much. Because of this, administrators

build up upper and lower cutoff points of adequate deviations from standard as show in the

realistic. In the event that deviations are inside the satisfactory range, top level executives must

not take activities. In any case, if the actual expenses are altogether unique then the top level

executives need to discover the cause(Zimmerman and Yahya-Zadeh, 2011).

CONCLUSION

From the above report, facts and figure, it has been observed that the Tottenham Plc. Need to

have the proper analysis on management accountants part, so that they could able to find out the

product of the company which are essentials to buy from the sub-contractors or to produce

within the organisation. And also find out the savings which come out from the deviations

between certain producing units and the buying units. As these are the tools and techniques

which are specifically used for making decisions that could assist the cited company to have

sustainable development.

deviations computed. Deviations assessment is the way toward sorting the nature of the contrasts

between genuine expenses and standard expenses and looking for clarifications for those

distinctions. Unfavourable deviations emerge when the real consumption surpasses the standard

stipend(Granlund, 2011). While on the other hand, positive deviations emerge when the real use

is not as much as the standard remittance. Deviation analysis ought to help top level executives

to figure out who or what is in charge of every deviation. Besides, it is imperative for the top

level executives to know when to act and when it is a bit much. Because of this, administrators

build up upper and lower cutoff points of adequate deviations from standard as show in the

realistic. In the event that deviations are inside the satisfactory range, top level executives must

not take activities. In any case, if the actual expenses are altogether unique then the top level

executives need to discover the cause(Zimmerman and Yahya-Zadeh, 2011).

CONCLUSION

From the above report, facts and figure, it has been observed that the Tottenham Plc. Need to

have the proper analysis on management accountants part, so that they could able to find out the

product of the company which are essentials to buy from the sub-contractors or to produce

within the organisation. And also find out the savings which come out from the deviations

between certain producing units and the buying units. As these are the tools and techniques

which are specifically used for making decisions that could assist the cited company to have

sustainable development.

REFERENCES

Books and journals:

Zimmerman, J.L. and Yahya-Zadeh, M., 2011. Accounting for decision making and control.

Issues in Accounting Education. 26(1). pp.258-259.

Granlund, M., 2011. Extending AIS research to management accounting and control issues: A

research note. International Journal of Accounting Information Systems. 12(1). pp.3-19.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2013. Management accounting and control

practices in a lean manufacturing environment. Accounting, Organizations and Society.

38(1). pp.50-71.

Otley, D. and Emmanuel, K.M.C., 2013. Readings in accounting for management control.

Springer.

Hiebl, M.R., 2014. Upper echelons theory in management accounting and control research.

Journal of Management Control. 24(3). pp.223-240.

Parker, L.D., 2012. Qualitative management accounting research: Assessing deliverables and

relevance. Critical perspectives on accounting. 23(1). pp.54-70.

Davies, T. and Crawford, I., 2011. Business accounting and finance. Pearson.

Arjaliès, D.L. and Mundy, J., 2013. The use of management control systems to manage CSR

strategy: A levers of control perspective. Management Accounting Research. 24(4).

pp.284-300.

Strumickas, M. and Valanciene, L., 2015. Research of management accounting changes in

Lithuanian business organizations. Engineering Economics. 63(4).

Grabner, I. and Moers, F., 2013. Management control as a system or a package? Conceptual and

empirical issues. Accounting, Organizations and Society. 38(6). pp.407-419.

Cadez, S. and Guilding, C., 2012. Strategy, strategic management accounting and performance:

a configurational analysis. Industrial Management & Data Systems. 112(3). pp.484-501.

Qian, W., Burritt, R. and Monroe, G., 2011. Environmental management accounting in local

government: A case of waste management. Accounting, Auditing & Accountability

Journal. 24(1). pp.93-128.

Østergren, K. and Stensaker, I., 2011. Management control without budgets: a field study of

‘beyond budgeting’in practice. European Accounting Review. 20(1). pp.149-181.

Books and journals:

Zimmerman, J.L. and Yahya-Zadeh, M., 2011. Accounting for decision making and control.

Issues in Accounting Education. 26(1). pp.258-259.

Granlund, M., 2011. Extending AIS research to management accounting and control issues: A

research note. International Journal of Accounting Information Systems. 12(1). pp.3-19.

Fullerton, R.R., Kennedy, F.A. and Widener, S.K., 2013. Management accounting and control

practices in a lean manufacturing environment. Accounting, Organizations and Society.

38(1). pp.50-71.

Otley, D. and Emmanuel, K.M.C., 2013. Readings in accounting for management control.

Springer.

Hiebl, M.R., 2014. Upper echelons theory in management accounting and control research.

Journal of Management Control. 24(3). pp.223-240.

Parker, L.D., 2012. Qualitative management accounting research: Assessing deliverables and

relevance. Critical perspectives on accounting. 23(1). pp.54-70.

Davies, T. and Crawford, I., 2011. Business accounting and finance. Pearson.

Arjaliès, D.L. and Mundy, J., 2013. The use of management control systems to manage CSR

strategy: A levers of control perspective. Management Accounting Research. 24(4).

pp.284-300.

Strumickas, M. and Valanciene, L., 2015. Research of management accounting changes in

Lithuanian business organizations. Engineering Economics. 63(4).

Grabner, I. and Moers, F., 2013. Management control as a system or a package? Conceptual and

empirical issues. Accounting, Organizations and Society. 38(6). pp.407-419.

Cadez, S. and Guilding, C., 2012. Strategy, strategic management accounting and performance:

a configurational analysis. Industrial Management & Data Systems. 112(3). pp.484-501.

Qian, W., Burritt, R. and Monroe, G., 2011. Environmental management accounting in local

government: A case of waste management. Accounting, Auditing & Accountability

Journal. 24(1). pp.93-128.

Østergren, K. and Stensaker, I., 2011. Management control without budgets: a field study of

‘beyond budgeting’in practice. European Accounting Review. 20(1). pp.149-181.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.