Angelo Limited: Managerial Accounting Report on ABC Costing System

VerifiedAdded on 2020/12/10

|17

|5216

|490

Report

AI Summary

This report provides a comprehensive overview of the Activity-Based Costing (ABC) system in managerial accounting. It begins by defining ABC costing and contrasting it with traditional costing methods, highlighting the advantages of ABC in terms of cost accuracy. The report then applies ABC principles to Angelo Limited, a manufacturer of laboratory equipment parts, detailing the calculation of overhead costs and profitability for two product types, Alpha and Beta. The analysis includes the use of cost drivers to allocate overhead expenses and determine per-unit profitability. The report concludes with a discussion of the advantages and disadvantages of ABC, emphasizing its role in improving decision-making and cost management. This report serves as a practical application of ABC principles, providing valuable insights into its implementation and impact on financial performance.

MANAGERIAL

ACCOUNTING

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

EXECUTIVE SUMMARY

This report is sited to define the meaning of ABC costing system. Concept of traditional

approach of costing and ABC costing elaborated subject to organisation. Managers would be

able to understand the use of ABC costing system in order to determine the cost of each activity

form under manufacturing and production process.

This report is sited to define the meaning of ABC costing system. Concept of traditional

approach of costing and ABC costing elaborated subject to organisation. Managers would be

able to understand the use of ABC costing system in order to determine the cost of each activity

form under manufacturing and production process.

Table of Contents

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION ..........................................................................................................................1

MAIN BODY...................................................................................................................................1

Activity based costing ...........................................................................................................1

Traditional based costing........................................................................................................1

Comparison between ABC and traditional approach of costing............................................3

Calculation of overhead costs and profitability according to Activity Based Cost information.4

Conclusion in respect with advantages and disadvantages of ABC for management accounting

................................................................................................................................................8

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

EXECUTIVE SUMMARY.............................................................................................................2

INTRODUCTION ..........................................................................................................................1

MAIN BODY...................................................................................................................................1

Activity based costing ...........................................................................................................1

Traditional based costing........................................................................................................1

Comparison between ABC and traditional approach of costing............................................3

Calculation of overhead costs and profitability according to Activity Based Cost information.4

Conclusion in respect with advantages and disadvantages of ABC for management accounting

................................................................................................................................................8

CONCLUSION..............................................................................................................................12

REFERENCES..............................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Managerial accounting refers to the process that involves making reports, and with the

help of these reports managers take decisions. Activity based costing is a method of calculating

cost of operations by dividing the cost among different activities. This accounting concentrates

on internal performance of an organization which ultimately lead to success and growth (Dale

and Plunkett, 2017). This report is based on Angelo Limited, which manufactures parts of

laboratory equipments. Details of Activity based costing and its comparison with traditional

approach to costing has been given. After that, calculation of profits and comparison of profit

percentage have been done on the basis of information given about two parts. Lastly, advantages

and disadvantages of ABC for management accounting are discussed.

MAIN BODY

Activity based costing

This technique of costing also known as ABC costing, it determines all those activities

which are associated with the production, analyse the cost of those activities and determines the

cost of product. Activity based costing is a system to recognize the relation between costs,

activities and manufactured products and it is also identifies the cost which is assigned to

activities overhead and then it is assigned to those cost of product. This costing is mostly used in

manufacturing industries where they enhance the costing data. This costing system is used in

product, target, for analysing profits, customer profits etc. It is widely popular when an

organizations is developing a better focus on corporate and making cost strategies better. This is

based on the system where the unit of work, events, task with specified goals, setting new

machines for production, designs for new products, providing finished goods etc. It is helpful in

transferring the costing of high volume products to the lover volume products and raising the

unit cost of lower volume of products. This costing is used in accounting methods to

management, salaries to office members (DRURY, 2013).

Traditional based costing

This technique decides the cost of products based on average overhead rate. This method

includes all indirect costs in production and applies these costs equally across the board using a

consistent technique such as machine hour etc.

1

Managerial accounting refers to the process that involves making reports, and with the

help of these reports managers take decisions. Activity based costing is a method of calculating

cost of operations by dividing the cost among different activities. This accounting concentrates

on internal performance of an organization which ultimately lead to success and growth (Dale

and Plunkett, 2017). This report is based on Angelo Limited, which manufactures parts of

laboratory equipments. Details of Activity based costing and its comparison with traditional

approach to costing has been given. After that, calculation of profits and comparison of profit

percentage have been done on the basis of information given about two parts. Lastly, advantages

and disadvantages of ABC for management accounting are discussed.

MAIN BODY

Activity based costing

This technique of costing also known as ABC costing, it determines all those activities

which are associated with the production, analyse the cost of those activities and determines the

cost of product. Activity based costing is a system to recognize the relation between costs,

activities and manufactured products and it is also identifies the cost which is assigned to

activities overhead and then it is assigned to those cost of product. This costing is mostly used in

manufacturing industries where they enhance the costing data. This costing system is used in

product, target, for analysing profits, customer profits etc. It is widely popular when an

organizations is developing a better focus on corporate and making cost strategies better. This is

based on the system where the unit of work, events, task with specified goals, setting new

machines for production, designs for new products, providing finished goods etc. It is helpful in

transferring the costing of high volume products to the lover volume products and raising the

unit cost of lower volume of products. This costing is used in accounting methods to

management, salaries to office members (DRURY, 2013).

Traditional based costing

This technique decides the cost of products based on average overhead rate. This method

includes all indirect costs in production and applies these costs equally across the board using a

consistent technique such as machine hour etc.

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Traditional costing is based on the volume of production resources in which it is

consumed from overhead to products. In this method the overhead costs is usually amounted on

either a direct labour or on machine hours used. In this costing the trouble made when the

overhead is higher than the allocation, but when there is a massive change in overhead applied

that makes a small change in the volume of resources consumed. It firstly assigned the indirect

costs either traced and allocated, but depends on the specific cost item which directly traced to

service departments which provide services to other departments. This costing system is used on

the basis of allocation overhead , direct labour hours. This system basic difficulty that is doesn't

gave the exact information of cost price of product and services to decision makers.

Importance of traditional based approach of costing:-

Activity based costing method is rather a broader concept than traditional costing

methods. Traditional costing method are less complex or simple in nature, involves low cost and

also less time consuming than other method. This method have its origin from longer time which

makes it easy to understand as it does not require so much expertise and knowledge. According

to this method of costing, overhead costs are allocated on the basis of volume of consumption of

resources. As coming to results, choice of method for every organization depends upon various

circumstances and situations (Christopher, 2016). For instance, in a smaller organisation where

departments are not there and in a larger organization where various departments are there, so

larger organisation will be more complex in nature and they mostly prefer to use ABC. But

smaller organisation may use traditional approach to costing.

Importance of Activity Based Costing:-

They are using different variation in activity based costing method. Each one has the

unique characteristics but they follow the same principles in costing method.

ABC method has nine basic steps that define the scope, identifying the activities,

collected data, build the model, lay out process, identify which type of ABC to use and

take action.

ABC method is used for the cost assessment of scientific pricing the main principle. In

this the cost which assess priced scientifically.

Homberg in 2002 did a study in depth about the use of activity based costing and founded

most effective ways to cut the overhead costs. As per perspective of Hoberg other ways

to use that costing in efficient manner and for reducing overhead.

2

consumed from overhead to products. In this method the overhead costs is usually amounted on

either a direct labour or on machine hours used. In this costing the trouble made when the

overhead is higher than the allocation, but when there is a massive change in overhead applied

that makes a small change in the volume of resources consumed. It firstly assigned the indirect

costs either traced and allocated, but depends on the specific cost item which directly traced to

service departments which provide services to other departments. This costing system is used on

the basis of allocation overhead , direct labour hours. This system basic difficulty that is doesn't

gave the exact information of cost price of product and services to decision makers.

Importance of traditional based approach of costing:-

Activity based costing method is rather a broader concept than traditional costing

methods. Traditional costing method are less complex or simple in nature, involves low cost and

also less time consuming than other method. This method have its origin from longer time which

makes it easy to understand as it does not require so much expertise and knowledge. According

to this method of costing, overhead costs are allocated on the basis of volume of consumption of

resources. As coming to results, choice of method for every organization depends upon various

circumstances and situations (Christopher, 2016). For instance, in a smaller organisation where

departments are not there and in a larger organization where various departments are there, so

larger organisation will be more complex in nature and they mostly prefer to use ABC. But

smaller organisation may use traditional approach to costing.

Importance of Activity Based Costing:-

They are using different variation in activity based costing method. Each one has the

unique characteristics but they follow the same principles in costing method.

ABC method has nine basic steps that define the scope, identifying the activities,

collected data, build the model, lay out process, identify which type of ABC to use and

take action.

ABC method is used for the cost assessment of scientific pricing the main principle. In

this the cost which assess priced scientifically.

Homberg in 2002 did a study in depth about the use of activity based costing and founded

most effective ways to cut the overhead costs. As per perspective of Hoberg other ways

to use that costing in efficient manner and for reducing overhead.

2

Comparison between ABC and traditional approach of costing

Activity Based Costing Traditional Costing

Activity based costing is more accurate than

traditional because it uses important factors

before assigning the cost of the product.

Traditional costing is won't always be accurate

because it doesn't use factor in non

manufacturing expenses or which it determines

overhead costs which affects specific products.

This costing is used when there is a crucial

accuracy,it is most precise & costly to

implement. But most of them preferred this

costing.

This costing is used when the accuracy won't be

affected by the production activity or when it is

considered that the time is limited.

Activity based costing is on internal use

because by this they can see all relevant

spending and can prepare on the basis of

relevant documents.

Traditional costing is on external use because it

is easy to determine the value of products for

outsiders.

Overhead cost remains high at that time the

small changes occurred in the cost of product

makes large differences in overall.

In Traditional costing when the cost of

overhead is lower as compared with the direct

costs, because it is done when it is most

accurate.

It determines all production relating activities,

assigning cost and to determine the cost of that

product.

In this, the cost of product is assigned by

averaging the overhead rates. This is used to

make out the indirect cost is in production and

applied those costs on equally bases on cost

driver ( machine hours).

Activity based costing should be used when

the priority is accuracy as ABC costing

ensures accuracy, because in case of high

overhead the small changes in the product

leads to large differences and by using this

method it becomes easy to analyse and

Traditional costing technique is beneficial when

all the priority is about the time and accuracy

becomes not so important in production

activities because in case when overhead is low

in comparison of direct costs, it will be more

accurate in this situation. It works good when

3

Activity Based Costing Traditional Costing

Activity based costing is more accurate than

traditional because it uses important factors

before assigning the cost of the product.

Traditional costing is won't always be accurate

because it doesn't use factor in non

manufacturing expenses or which it determines

overhead costs which affects specific products.

This costing is used when there is a crucial

accuracy,it is most precise & costly to

implement. But most of them preferred this

costing.

This costing is used when the accuracy won't be

affected by the production activity or when it is

considered that the time is limited.

Activity based costing is on internal use

because by this they can see all relevant

spending and can prepare on the basis of

relevant documents.

Traditional costing is on external use because it

is easy to determine the value of products for

outsiders.

Overhead cost remains high at that time the

small changes occurred in the cost of product

makes large differences in overall.

In Traditional costing when the cost of

overhead is lower as compared with the direct

costs, because it is done when it is most

accurate.

It determines all production relating activities,

assigning cost and to determine the cost of that

product.

In this, the cost of product is assigned by

averaging the overhead rates. This is used to

make out the indirect cost is in production and

applied those costs on equally bases on cost

driver ( machine hours).

Activity based costing should be used when

the priority is accuracy as ABC costing

ensures accuracy, because in case of high

overhead the small changes in the product

leads to large differences and by using this

method it becomes easy to analyse and

Traditional costing technique is beneficial when

all the priority is about the time and accuracy

becomes not so important in production

activities because in case when overhead is low

in comparison of direct costs, it will be more

accurate in this situation. It works good when

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

understand all the indirect cost and activities.

From the view of internal use the decision

maker will be able to easily analyse the

spending and indirect cost accurately. This

technique ensures the effective and efficient

utilisation of funds because by this method it is

easy to find out the areas of wasteful

spendings.

the production is of single line or similar goods

are produced. Moreover, in this situation it

becomes easier for external use to identify and

evaluate the value of products.

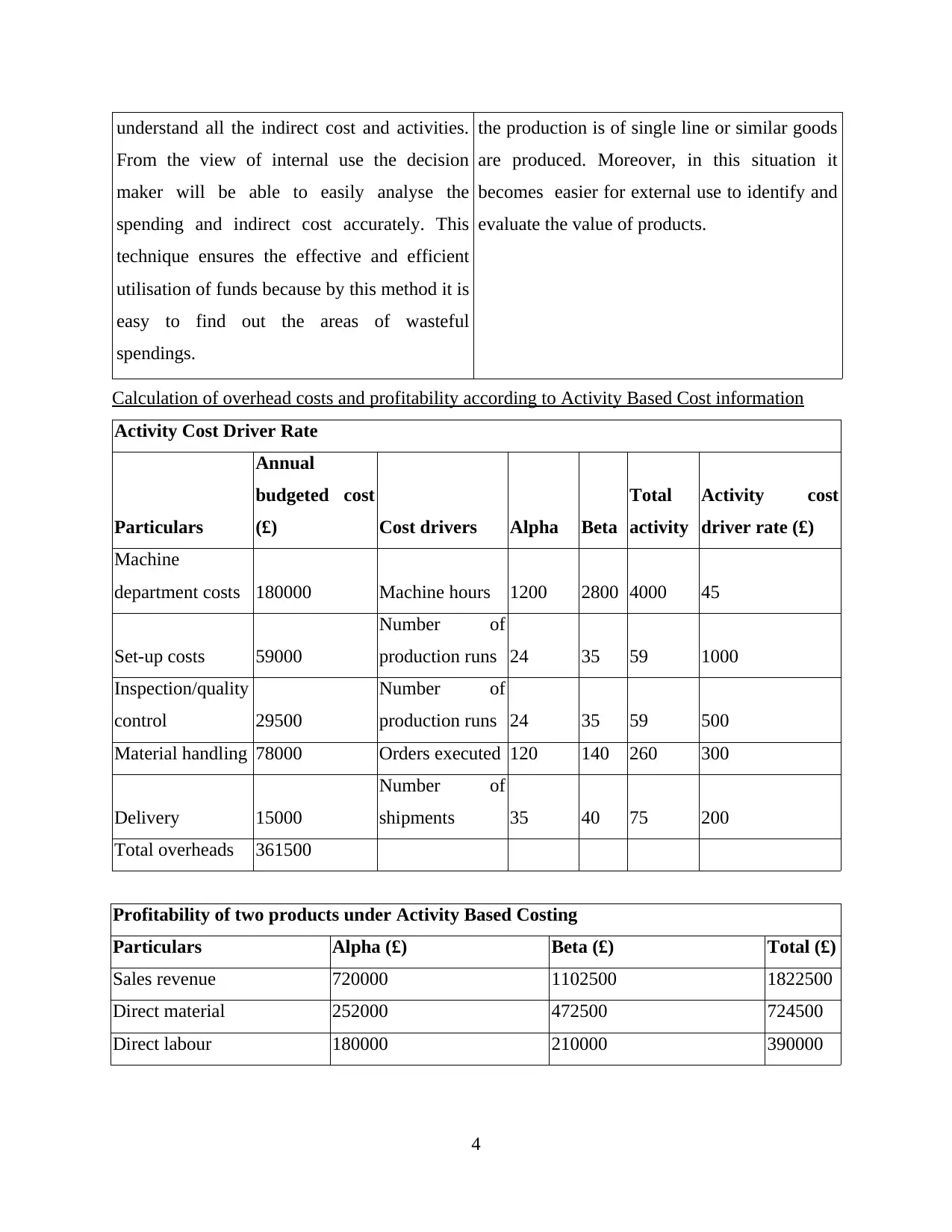

Calculation of overhead costs and profitability according to Activity Based Cost information

Activity Cost Driver Rate

Particulars

Annual

budgeted cost

(£) Cost drivers Alpha Beta

Total

activity

Activity cost

driver rate (£)

Machine

department costs 180000 Machine hours 1200 2800 4000 45

Set-up costs 59000

Number of

production runs 24 35 59 1000

Inspection/quality

control 29500

Number of

production runs 24 35 59 500

Material handling 78000 Orders executed 120 140 260 300

Delivery 15000

Number of

shipments 35 40 75 200

Total overheads 361500

Profitability of two products under Activity Based Costing

Particulars Alpha (£) Beta (£) Total (£)

Sales revenue 720000 1102500 1822500

Direct material 252000 472500 724500

Direct labour 180000 210000 390000

4

From the view of internal use the decision

maker will be able to easily analyse the

spending and indirect cost accurately. This

technique ensures the effective and efficient

utilisation of funds because by this method it is

easy to find out the areas of wasteful

spendings.

the production is of single line or similar goods

are produced. Moreover, in this situation it

becomes easier for external use to identify and

evaluate the value of products.

Calculation of overhead costs and profitability according to Activity Based Cost information

Activity Cost Driver Rate

Particulars

Annual

budgeted cost

(£) Cost drivers Alpha Beta

Total

activity

Activity cost

driver rate (£)

Machine

department costs 180000 Machine hours 1200 2800 4000 45

Set-up costs 59000

Number of

production runs 24 35 59 1000

Inspection/quality

control 29500

Number of

production runs 24 35 59 500

Material handling 78000 Orders executed 120 140 260 300

Delivery 15000

Number of

shipments 35 40 75 200

Total overheads 361500

Profitability of two products under Activity Based Costing

Particulars Alpha (£) Beta (£) Total (£)

Sales revenue 720000 1102500 1822500

Direct material 252000 472500 724500

Direct labour 180000 210000 390000

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Total manufacturing

overheads 432000 682500 1114500

Manufacturing overheads:

Machine department costs

(45*1200;45*2800) 54000 126000 180000

Set-up costs

(1000*24;1000*35) 24000 35000 59000

Inspection/quality control

costs (500*24;500*35) 12000 17500 29500

Material handling

(300*120;300*140) 36000 42000 78000

Delivery (200*35;200*40) 7000 8000 15000

Total overheads 133000 228500 361500

Profit 155000 191500 346500

Per unit profit 6.53 3.24

% overheads 36.79% 63.21% 100.00%

overhead cost per unit 20.83 21.76

Interpretation:

From the above calculations, profitability has been evaluated on the basis of Activity

based costing. Using cost drivers, activity based cost driver rate is calculated. There are two parts

of product manufactured by Angelo limited namely alpha and beta. According to problem,

various manufacturing costs are mentioned such as direct labour and direct material along with

this selling prices per unit are also given. Total output in units of alpha are 7200 units and of beta

are 10500 units. Later, various heads under overhead costs have been mentioned such as machine

department costs, set-up costs, inspection/quality control costs, material handling costs and

delivery costs. For purpose of breaking down them according to profitability, cost drivers like

machine hours, number of production runs, orders executed and number of shipments have been

used. Firstly, activity based cost driver rate is calculated by annual budgeted costs of overheads

and cost drivers. After that profitability is ascertained for two given parts that are alpha and beta.

Profitability is calculated by deducting all the costs from total sales revenue. Here all the costs

5

overheads 432000 682500 1114500

Manufacturing overheads:

Machine department costs

(45*1200;45*2800) 54000 126000 180000

Set-up costs

(1000*24;1000*35) 24000 35000 59000

Inspection/quality control

costs (500*24;500*35) 12000 17500 29500

Material handling

(300*120;300*140) 36000 42000 78000

Delivery (200*35;200*40) 7000 8000 15000

Total overheads 133000 228500 361500

Profit 155000 191500 346500

Per unit profit 6.53 3.24

% overheads 36.79% 63.21% 100.00%

overhead cost per unit 20.83 21.76

Interpretation:

From the above calculations, profitability has been evaluated on the basis of Activity

based costing. Using cost drivers, activity based cost driver rate is calculated. There are two parts

of product manufactured by Angelo limited namely alpha and beta. According to problem,

various manufacturing costs are mentioned such as direct labour and direct material along with

this selling prices per unit are also given. Total output in units of alpha are 7200 units and of beta

are 10500 units. Later, various heads under overhead costs have been mentioned such as machine

department costs, set-up costs, inspection/quality control costs, material handling costs and

delivery costs. For purpose of breaking down them according to profitability, cost drivers like

machine hours, number of production runs, orders executed and number of shipments have been

used. Firstly, activity based cost driver rate is calculated by annual budgeted costs of overheads

and cost drivers. After that profitability is ascertained for two given parts that are alpha and beta.

Profitability is calculated by deducting all the costs from total sales revenue. Here all the costs

5

refers to direct labour, direct material which are knowns as manufacturing overheads if

combined. Also total overhead costs are deducted from sales revenue for deriving profit. Profit

per unit, percentage of overheads to total overheads and overhead cost per unit are presented

(Govindan, Khodaverdi and Jafarian, 2013).

Thus if one is concerned on comparison, then overhead cost per unit of Alpha is 20.83

and of Beta it is 21.76 which is greater than former part. Overhead costs refers to costs which are

not directly associated with specific product units. Ultimately, these overhead expenses impacts

on profit and loss statements. As and when these costs increases, profits of income statement

decreases. Balanced proportion of overhead costs can give competitive advantage to Angelo

limited. Most of organizations on monthly basis ascertain overhead costs. Calculation of

overhead costs is involves step by step process. This process starts with making list of all

business expenses, then categorization of each individual expense is done on the basis of direct

and indirect association with production, after that all overhead costs are accumulated and

compared to sales as well as to labour cost.

Profits per unit of alpha and beta are 6.53 and 3.24 respectively. As one can see that

profit per unit of alpha is more than from beta. Thus it implies that alpha part of product is more

beneficial to Angelo limited in terms of profitability. Profit is essential for an organization to

grow and expand. Expansion can be in form of diverse operations or in establishing new office.

Along with this, profit increases ability of an organisation to borrow money from financial

institutions and banks. As profitability of Angelo limited is disclosed for communication to

external users in financial statements. So this information of profit assists in attracting investors.

Also an enterprise can hire more personnels because of increment in affordability.

Now coming to next part that is percentage of overhead costs which is 36.79 of alpha and

63.21 of beta to overall overhead costs. One can see that percentage of overhead costs of beta is

more as compared with alpha which denotes that there is less profit in beta than alpha. Overall

profit of alpha is 155000 and of beta is 191500. So profit of former is less than latter but profit

per unit of former is more than latter.

Total overhead costs of alpha is 133000 and of beta is 228500. expenses that comprises

total manufacturing overheads are machine department costs, set-up costs, inspection/quality

control costs, material handling costs, and delivery costs which are divided according to cost

drivers of activity based costing.

6

combined. Also total overhead costs are deducted from sales revenue for deriving profit. Profit

per unit, percentage of overheads to total overheads and overhead cost per unit are presented

(Govindan, Khodaverdi and Jafarian, 2013).

Thus if one is concerned on comparison, then overhead cost per unit of Alpha is 20.83

and of Beta it is 21.76 which is greater than former part. Overhead costs refers to costs which are

not directly associated with specific product units. Ultimately, these overhead expenses impacts

on profit and loss statements. As and when these costs increases, profits of income statement

decreases. Balanced proportion of overhead costs can give competitive advantage to Angelo

limited. Most of organizations on monthly basis ascertain overhead costs. Calculation of

overhead costs is involves step by step process. This process starts with making list of all

business expenses, then categorization of each individual expense is done on the basis of direct

and indirect association with production, after that all overhead costs are accumulated and

compared to sales as well as to labour cost.

Profits per unit of alpha and beta are 6.53 and 3.24 respectively. As one can see that

profit per unit of alpha is more than from beta. Thus it implies that alpha part of product is more

beneficial to Angelo limited in terms of profitability. Profit is essential for an organization to

grow and expand. Expansion can be in form of diverse operations or in establishing new office.

Along with this, profit increases ability of an organisation to borrow money from financial

institutions and banks. As profitability of Angelo limited is disclosed for communication to

external users in financial statements. So this information of profit assists in attracting investors.

Also an enterprise can hire more personnels because of increment in affordability.

Now coming to next part that is percentage of overhead costs which is 36.79 of alpha and

63.21 of beta to overall overhead costs. One can see that percentage of overhead costs of beta is

more as compared with alpha which denotes that there is less profit in beta than alpha. Overall

profit of alpha is 155000 and of beta is 191500. So profit of former is less than latter but profit

per unit of former is more than latter.

Total overhead costs of alpha is 133000 and of beta is 228500. expenses that comprises

total manufacturing overheads are machine department costs, set-up costs, inspection/quality

control costs, material handling costs, and delivery costs which are divided according to cost

drivers of activity based costing.

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Types of Overhead

Administrative overhead:- In this overhead it includes the items such as utilities,

supporting functions, planning etc. These costs are overheads, are not directly related to any

particular function nor its results generating profits. These costs has the role of supporting

business other functions (Schaltegger and Burritt, 2017). Administrative overhead rates are

regularly charged by the universities on research. In accounting terms millions were wasted in

every year on overheads by universities administrators.

Example:-

Employee salary: In this it is considered that overheads as cost must paid

regardless of sales and profits of company. Salary differs from wage as salary but it is not

affected by working hours and time that's why it remain constant.

Office Equipment and supplies: In this it includes equipments like printer,

computers, refrigerator, fax machine etc. they are not directly result in sales and profit, they are

also in use for supporting functions and can provide business operations.

Manufacturing Overhead:- In this all costs are endured by a business that is in the

platform by which product and service is created (Cheung, 2016). It refers to those overheads

which is categorised with in a factory or office. In this there are cases in which the usage of

overheads that separates them.

Example:

Property taxes on production facilities:- Every property unless government owned is

subject to form of property tax. Taxes on production factories are categorised by manufacturing

overheads which may not be avoided.

Applications of business overheads:-Business overheads are calculated by accountant

for budgeting purpose, so the business has an idea how much they charge from consumers in

order to make profits.

Cost Classification:

Cost classification refers to the separation of expenses in different categories, in

economic terms it involves in fixed cost, variable cost, opportunity cost, production cost and

sunk costs. As per this, accounting costs are classified as either directly or indirectly for a

business. It define as the cost separates in expenses in various forms. Classification system uses

management attention in certain costs, that considered more crucial (Pentland and et. al., 2012).

7

Administrative overhead:- In this overhead it includes the items such as utilities,

supporting functions, planning etc. These costs are overheads, are not directly related to any

particular function nor its results generating profits. These costs has the role of supporting

business other functions (Schaltegger and Burritt, 2017). Administrative overhead rates are

regularly charged by the universities on research. In accounting terms millions were wasted in

every year on overheads by universities administrators.

Example:-

Employee salary: In this it is considered that overheads as cost must paid

regardless of sales and profits of company. Salary differs from wage as salary but it is not

affected by working hours and time that's why it remain constant.

Office Equipment and supplies: In this it includes equipments like printer,

computers, refrigerator, fax machine etc. they are not directly result in sales and profit, they are

also in use for supporting functions and can provide business operations.

Manufacturing Overhead:- In this all costs are endured by a business that is in the

platform by which product and service is created (Cheung, 2016). It refers to those overheads

which is categorised with in a factory or office. In this there are cases in which the usage of

overheads that separates them.

Example:

Property taxes on production facilities:- Every property unless government owned is

subject to form of property tax. Taxes on production factories are categorised by manufacturing

overheads which may not be avoided.

Applications of business overheads:-Business overheads are calculated by accountant

for budgeting purpose, so the business has an idea how much they charge from consumers in

order to make profits.

Cost Classification:

Cost classification refers to the separation of expenses in different categories, in

economic terms it involves in fixed cost, variable cost, opportunity cost, production cost and

sunk costs. As per this, accounting costs are classified as either directly or indirectly for a

business. It define as the cost separates in expenses in various forms. Classification system uses

management attention in certain costs, that considered more crucial (Pentland and et. al., 2012).

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Significance

On the basis of production and process: A factory may bear various types of costs in

production process. They are sub divided in direct and in direct expenditure. Direct

expenditure are those which is easily identified wholly with a unit cost. It includes

material, labour and direct expenses. Indirect expenses are those incurred advantage of

cost centre and not easily identified.

On the basis of element or nature: In this cost is divided into material, labour and

expenses. It includes materials which are produces or provide services, labour which is

needed to convert raw material into finished goods and other expenses which are needed

in course of production and distribution (Chen and et. al., 2012).

On the basis of function: in this the cost is classified in production, administration,

selling and distribution, research and development cost. In production it includes direct

material, labour, manufacturing activity. In administrative cost it incurred cost by policy

formulation and implementation, which is related to research, development.

Conclusion in respect with advantages and disadvantages of ABC for management accounting

Angelo Ltd manufacturers wants to install a plant to manufacture the laboratory

equipments. This plant will emphasise the production units and boost the efficiency. Managers

wants to calculate the cost of each and every activity. For this purpose users managers have

decided to install ABC costing system. This system will initiate following changes

characteristics within organisation.

Advantages of ABC:

As in Activity Based Costing, products are categorized in different categories, so it helps

in realizing actual costs of manufacturing process of that specific categories.

Better decision making: It improves the decision of any organisation manager's as they

may use the certain data of product cost. It also useful to fix the selling price as more

accurate product cost data is available.

Tracing of overheads costs: It is used to trace the costs in field of managerial obligation,

departments, procedure, customers besides the product costs.

Accurate Product Cost: In AB costing it is focusing on the causes and effects related in

cost incur which brings accuracy and reliability. Angelo Ltd. Manufactures recognises

the consuming activities by a product, activities which causes cost. It support functions in

8

On the basis of production and process: A factory may bear various types of costs in

production process. They are sub divided in direct and in direct expenditure. Direct

expenditure are those which is easily identified wholly with a unit cost. It includes

material, labour and direct expenses. Indirect expenses are those incurred advantage of

cost centre and not easily identified.

On the basis of element or nature: In this cost is divided into material, labour and

expenses. It includes materials which are produces or provide services, labour which is

needed to convert raw material into finished goods and other expenses which are needed

in course of production and distribution (Chen and et. al., 2012).

On the basis of function: in this the cost is classified in production, administration,

selling and distribution, research and development cost. In production it includes direct

material, labour, manufacturing activity. In administrative cost it incurred cost by policy

formulation and implementation, which is related to research, development.

Conclusion in respect with advantages and disadvantages of ABC for management accounting

Angelo Ltd manufacturers wants to install a plant to manufacture the laboratory

equipments. This plant will emphasise the production units and boost the efficiency. Managers

wants to calculate the cost of each and every activity. For this purpose users managers have

decided to install ABC costing system. This system will initiate following changes

characteristics within organisation.

Advantages of ABC:

As in Activity Based Costing, products are categorized in different categories, so it helps

in realizing actual costs of manufacturing process of that specific categories.

Better decision making: It improves the decision of any organisation manager's as they

may use the certain data of product cost. It also useful to fix the selling price as more

accurate product cost data is available.

Tracing of overheads costs: It is used to trace the costs in field of managerial obligation,

departments, procedure, customers besides the product costs.

Accurate Product Cost: In AB costing it is focusing on the causes and effects related in

cost incur which brings accuracy and reliability. Angelo Ltd. Manufactures recognises

the consuming activities by a product, activities which causes cost. It support functions in

8

advanced manufacturing technology and environment with overhead constitute on large

share of total costs, this costing provides reliable, accurate or correct cost of product and

more realistic cost of products in this manufactured products such as high volume and

low volume products. Angelo Ltd. Manufactures uses both type of product for

manufacturing either lower volume or high volume in case of greater diversity takes

place in the manufactured products (Advantages and disadvantages of ABC costing,

2018). They uses activity based costing and found it reliable and accurate measure of cost

of product. This manufactures company has found less errors and approximation in cost

determination of product. So the company is focusing on the causes and effect relation

(Rezaei, Nispeling, Sarkis and Tavasszy, 2016). Using advanced technology and

environment in support with the functions where overhead constituting on large amount

of total cost. It defines the real nature to control the fixed overhead cost and by which

activities become more visible and clear. The company controls many of the fixed

overhead costs by exercising control over the activities. By focusing on the relation of

cause and effects in cost incurring, ABC produce more accurate and reliable results

while determining the product cost.

Better control of High-Priority Inventory: In activity based costing inventory plays high

priority for better control. It places the tighter and frequent control. It uses class A

inventory where customers requests are m,ore often in use. This class A inventory is used

by Angelo Ltd. Manufactures because it is directly linked with the success of company

and it is helpful for monitoring the demand and ensure the stock level matches that

demand of customers. For analysing AB costing the company Angelo Ltd. Manufactures

uses resources and controlling priority from high priority inventory over that inventory

which has a lower impact in bottom line (Martin and Nakayama, 2013). Company uses

the high priority in inventory for allocating there resources more effectively and

efficiently. Company uses high priority which helps to save time, labour and more

frequent controls the inventory. In this inventory include most of the items in producing

goods and monitoring the demand for it which ensure the stock level which matches the

demand. The company often suggest class A for better control which is used for the

success of the company (Harrison and Lock, 2017).

9

share of total costs, this costing provides reliable, accurate or correct cost of product and

more realistic cost of products in this manufactured products such as high volume and

low volume products. Angelo Ltd. Manufactures uses both type of product for

manufacturing either lower volume or high volume in case of greater diversity takes

place in the manufactured products (Advantages and disadvantages of ABC costing,

2018). They uses activity based costing and found it reliable and accurate measure of cost

of product. This manufactures company has found less errors and approximation in cost

determination of product. So the company is focusing on the causes and effect relation

(Rezaei, Nispeling, Sarkis and Tavasszy, 2016). Using advanced technology and

environment in support with the functions where overhead constituting on large amount

of total cost. It defines the real nature to control the fixed overhead cost and by which

activities become more visible and clear. The company controls many of the fixed

overhead costs by exercising control over the activities. By focusing on the relation of

cause and effects in cost incurring, ABC produce more accurate and reliable results

while determining the product cost.

Better control of High-Priority Inventory: In activity based costing inventory plays high

priority for better control. It places the tighter and frequent control. It uses class A

inventory where customers requests are m,ore often in use. This class A inventory is used

by Angelo Ltd. Manufactures because it is directly linked with the success of company

and it is helpful for monitoring the demand and ensure the stock level matches that

demand of customers. For analysing AB costing the company Angelo Ltd. Manufactures

uses resources and controlling priority from high priority inventory over that inventory

which has a lower impact in bottom line (Martin and Nakayama, 2013). Company uses

the high priority in inventory for allocating there resources more effectively and

efficiently. Company uses high priority which helps to save time, labour and more

frequent controls the inventory. In this inventory include most of the items in producing

goods and monitoring the demand for it which ensure the stock level which matches the

demand. The company often suggest class A for better control which is used for the

success of the company (Harrison and Lock, 2017).

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.