Managerial Accounting Assignment: Costing and Pricing Strategies

VerifiedAdded on 2021/04/17

|6

|1057

|43

Homework Assignment

AI Summary

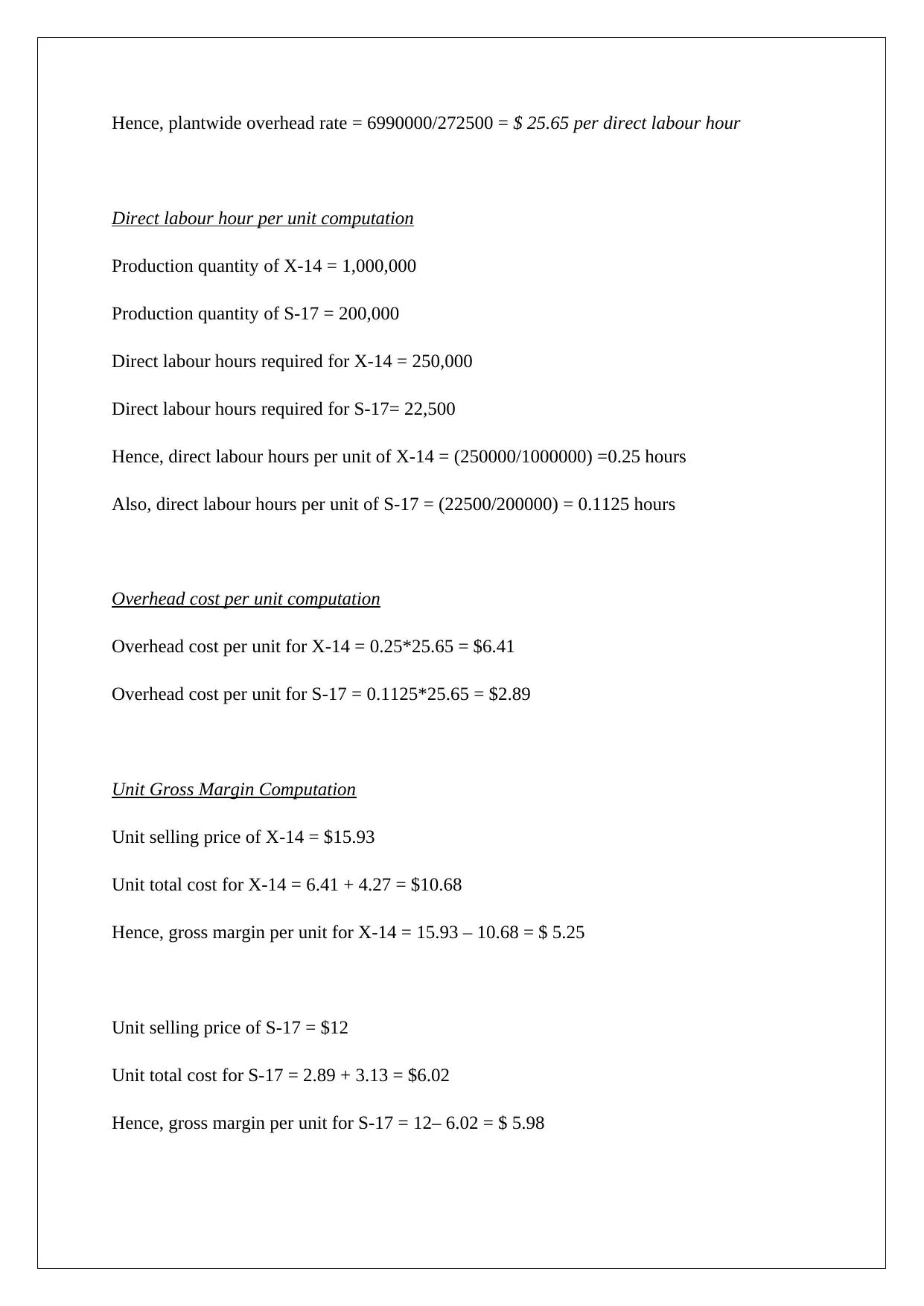

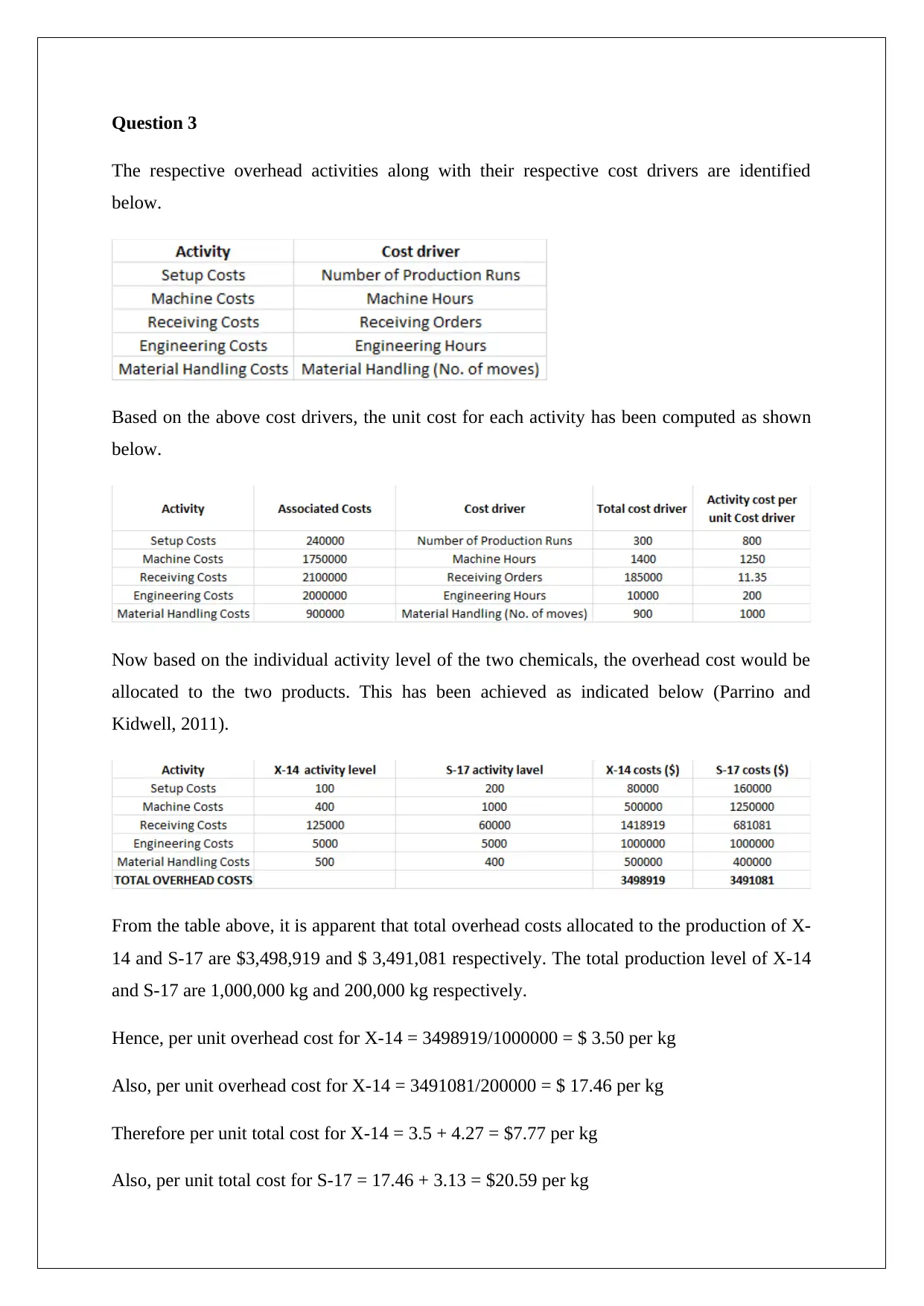

This assignment solution addresses a managerial accounting problem involving two chemicals, X-14 and S-17, produced by South Pacific Chemicals. The core of the assignment involves comparing the traditional costing method with Activity-Based Costing (ABC) to accurately allocate overhead costs. The student computes plantwide overhead rates, direct labor hours per unit, and overhead costs per unit under both methods. The analysis reveals that the traditional costing system over-allocates overhead costs to X-14 and under-allocates them to S-17. The solution then uses ABC to re-evaluate costs, calculate gross margins, and recommend pricing strategies. Based on the ABC system, the assignment suggests that the company reduce the price of X-14 and increase the price of S-17 to improve its competitive position and profitability. The solution also includes relevant references supporting the concepts discussed.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.